Middle East And Africa Commercial HVAC Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

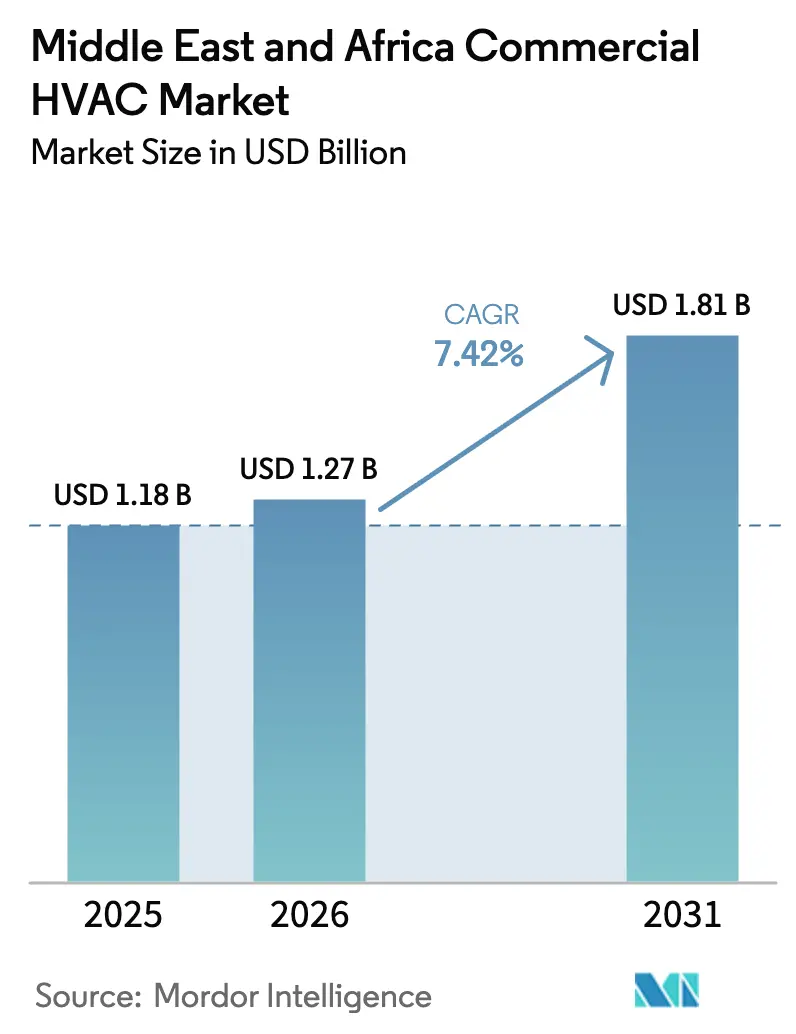

| Base Year Market Size (2025) | USD 1.18 Billion |

| Market Size (2026) | USD 1.27 Billion |

| Market Size (2031) | USD 1.81 Billion |

| Growth Rate (2026 - 2031) | 7.42% CAGR |

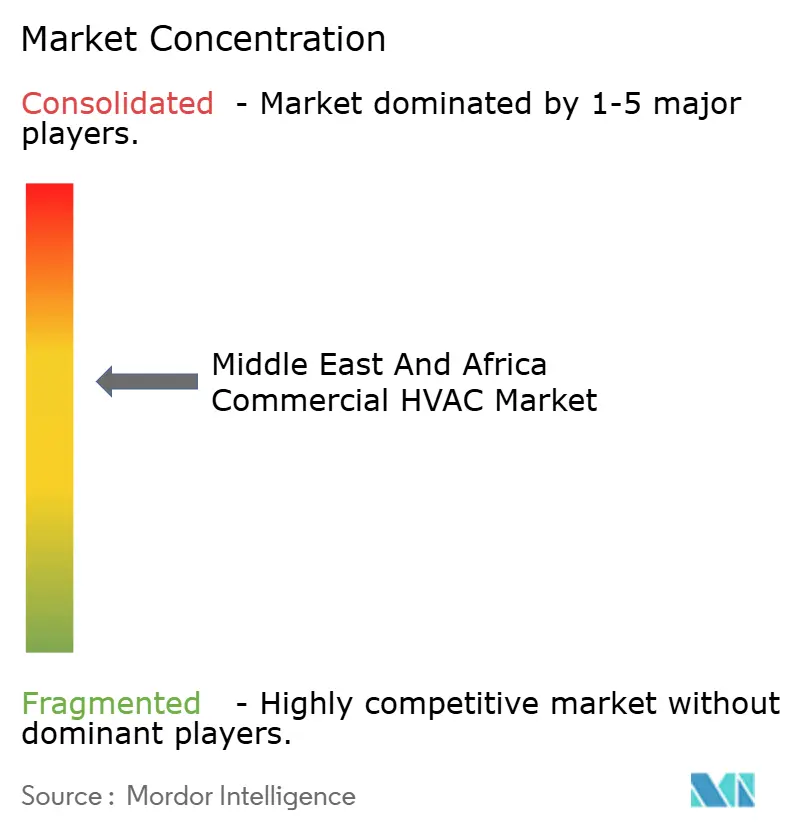

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Commercial HVAC Market Analysis by Mordor Intelligence

The Middle East and Africa commercial HVAC market size was valued at USD 1.18 billion in 2025 and estimated to grow from USD 1.27 billion in 2026 to reach USD 1.81 billion by 2031, at a CAGR of 7.42% during the forecast period (2026-2031). Robust capital spending on transport hubs, data centers and mixed-use “giga projects” is propelling demand even as governments tighten building-energy codes. Variable Refrigerant Flow (VRF) systems continue to displace packaged and rooftop units because they cut electricity use by 48–52% in hot-dry conditions. Retrofit activity outpaces new-build installations as owners replace R-22 equipment to satisfy SASO 2663:2021, UAE ESMA and South Africa SANS 10400-XA mandates. At the same time, precision cooling for hyperscale and edge data centers is generating premium margins, while district-cooling networks in Dubai, Riyadh and Doha are accelerating centralized plant retrofits. Competitive intensity remains moderate: no supplier controls more than 15% revenue, leaving room for regional specialists to scale alongside global incumbents.

Key Report Takeaways

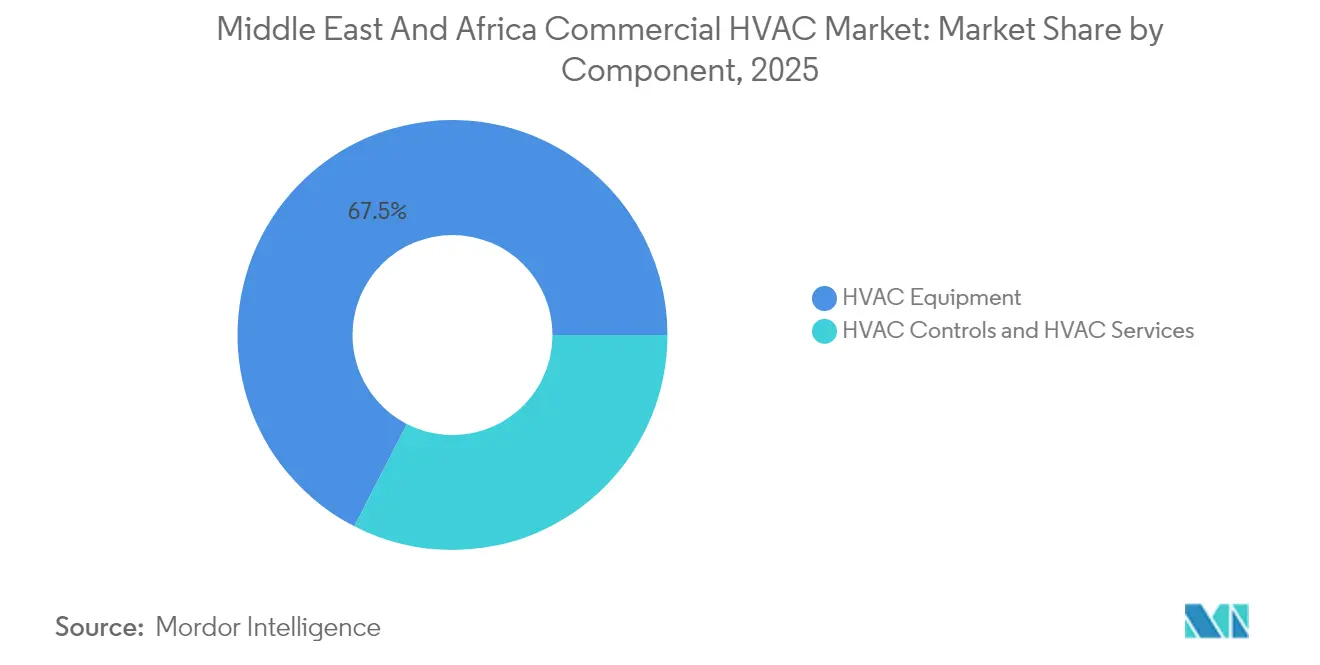

- By component, HVAC equipment captured 67.45% revenue share in 2025; controls posted the fastest expansion at 8.74% CAGR to 2031.

- By system type, VRF commanded 34.30% of the Middle East and Africa commercial HVAC market share in 2025, while the same technology is forecast to grow at 8.21% CAGR through 2031.

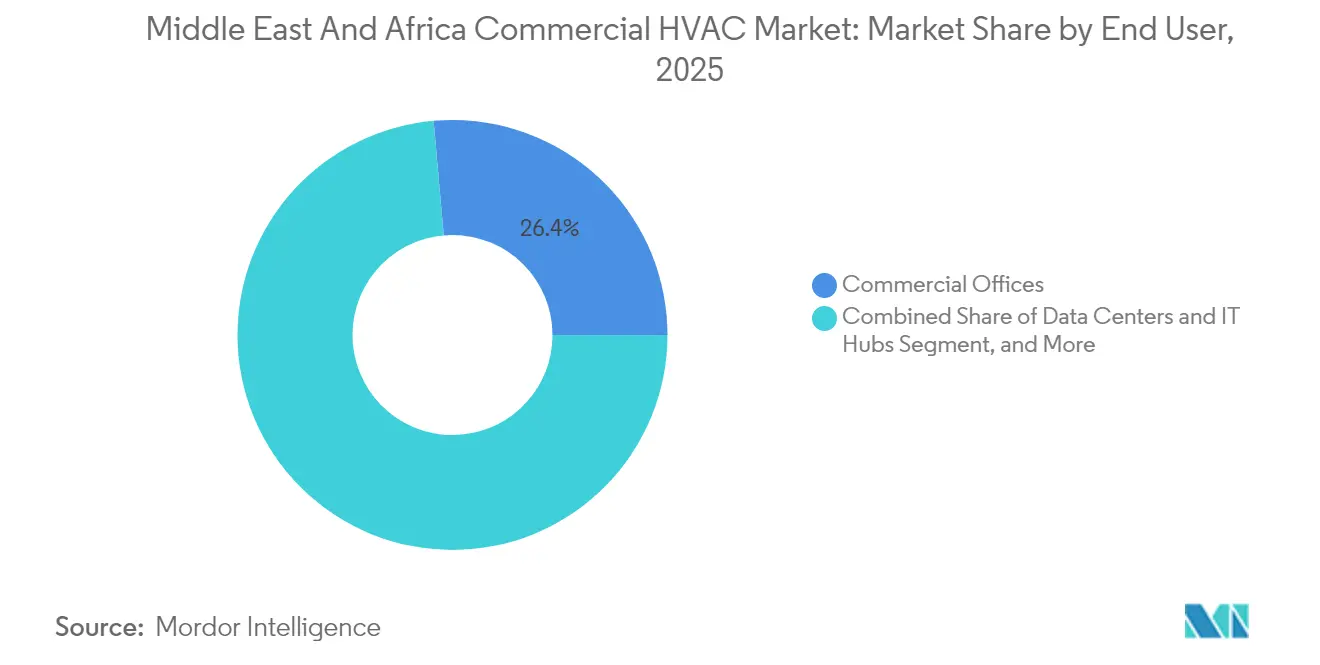

- By end user, commercial offices led with 26.40% revenue in 2025; data centers and IT hubs record the highest projected 7.96% CAGR to 2031.

- By building lifecycle, retrofit projects accounted for 57.10% of the Middle East and Africa commercial HVAC market size in 2025 and advance at an 8.52% CAGR to 2031.

- By country, Saudi Arabia held 27.60% revenue share in 2025 and remains the fastest-growing geography at 8.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global valuation is built by aggregating outputs from multiple regions, with Middle east and africa forming one of the important contributors. Mordor Intelligence's global commercial hvac market size report represents that cumulative total.

Middle East And Africa Commercial HVAC Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in commercial megaproject construction (GCC "giga projects") | +2.1% | GCC countries, with spillover to Egypt | Long term (≥ 4 years) |

| Mandatory energy-efficiency regulations (SASO, UAE ESMA, South Africa SANS 10400-XA) | +1.8% | Global, with early gains in Saudi Arabia, UAE, South Africa | Medium term (2-4 years) |

| Data-center boom driving precision cooling demand | +1.5% | GCC core, spill-over to MEA | Short term (≤ 2 years) |

| District-cooling integration accelerating centralized retrofit HVAC | +1.2% | UAE, Saudi Arabia, Qatar | Medium term (2-4 years) |

| Green-hydrogen industrial clusters requiring specialized HVAC systems | +0.9% | Saudi Arabia, UAE, with potential expansion to Oman | Long term (≥ 4 years) |

| Tourism mega-events (Expo 2030 Riyadh, Egypt Vision 2030) fueling hospitality upgrades | +0.7% | Saudi Arabia, Egypt, with regional tourism spillover | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Commercial Megaproject Construction (GCC “Giga Projects”)

A signficiant hospitality and mixed-use pipeline anchored by Saudi Arabia’s Vision 2030 and the NEOM green hydrogen industrial cluster is reshaping specification requirements. Cooling systems must manage wide indoor-outdoor thermal gradients, stringent humidity targets and 24/7 operation.[1]NEOM Green Hydrogen Company, “NEOM Green Hydrogen Company completes financial close,” neom.com Project developers are favoring modular, factory-assembled chillers and VRF networks that shorten installation schedules and ease phased occupancy. Each flagship site drives follow-on demand for logistics parks, worker camps, and visitor facilities, multiplying the Middle East and Africa commercial HVAC market opportunity. Long-dated service contracts embedded in Public-Private-Partnership frameworks further improve revenue visibility for OEMs and facility managers.

Mandatory Energy-Efficiency Regulations (SASO, UAE ESMA, South Africa SANS 10400-XA)

Minimum Seasonal Energy Efficiency Ratio (SEER) thresholds, refrigerant phase-down schedules and building energy-labeling schemes are accelerating the migration from R-22 and R-410A equipment to high-SEER VRF, inverter split and magnetic-bearing chiller platforms. Saudi Arabia’s SASO 2663:2021 already excludes low-efficiency imports from customs clearance, while ESMA’s 2.78 EER floor in the UAE raises retrofit urgency in Dubai’s pre-2010 office stock.[2]Emirates Authority for Standardization & Metrology, “SASO 2663:2021 Overview,” esma.gov.ae South Africa’s SANS 10400-XA revision extends compliance to commercial properties above 500 m². OEMs able to harmonize product catalogs across this patchwork capture price premiums as building owners avoid future non-compliance penalties.

Data-Center Boom Driving Precision Cooling Demand

Hyperscale and colocation operators are adding more than 300 MW of IT load across the GCC by 2026, with density increments from 6 kW to 12 kW per rack. Precision CRAC-CRAH units, rear-door heat exchangers and liquid-cooling modules dominate bid specifications because servers consume 10-50 times more energy per square meter than conventional commercial space. Governments are tightening water-withdrawal quotas, prompting closed-loop adiabatic systems and treated sewage effluent reuse pilots to offset projected 426 billion-liter annual draw by 2030. Data-center orders therefore command higher margins and remain insulated from macro-cyclical swings because cloud services sustain digital-economy targets.

District-Cooling Integration Accelerating Retrofit HVAC

The GCC accounts for 40% of global district-cooling capacity. Dubai’s Empower alone operates 241,272 refrigeration tons and plans to lift penetration to 40% of the city’s floor space by 2030. Connecting legacy towers to central plants avoids full-scale internal system replacement, cutting electricity consumption by up to 50% and extending asset life to 25 years. The regulatory treatment of district cooling as a utility with cost-pass-through tariffs underpins stable long-term returns, driving public-private investment in chilled-water networks that further expand retrofit demand across the Middle East and Africa commercial HVAC market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex of advanced high-SEER equipment | -1.4% | Global, with acute impact in price-sensitive African markets | Short term (≤ 2 years) |

| Downward price pressure from Chinese and local OEMs | -1.1% | MEA region-wide, particularly intense in Egypt, Nigeria, Kenya | Medium term (2-4 years) |

| Scarcity of skilled technicians for smart-control commissioning | -0.8% | MEA region-wide, particularly acute in sub-Saharan Africa | Long term (≥ 4 years) |

| Water-scarcity limits on cooling-tower deployment | -0.6% | GCC countries, North Africa arid regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capex of Advanced High-SEER Equipment

VRF, magnetic-bearing chillers and inverter splits require 23% more up-front investment than conventional DX packages even though they reduce life-cycle energy cost by 27%. Financing barriers remain pronounced in sub-Saharan Africa where 35% of units sold still use R-22 refrigerant.[3]International Institute of Refrigeration, “Inefficient R22 Air Conditioners Dumped in Africa,” iifiir.org Commercial lenders seldom credit life-cycle savings when underwriting, so pay-back horizons above three years deter smaller property owners. Specialized systems for data centers can triple the bill of materials compared with standard office builds, restricting adoption to well-capitalized developers until equipment prices fall or green-finance mechanisms broaden.

Scarcity of Skilled Technicians for Smart-Control Commissioning

Digitally native HVAC platforms integrate IoT sensors, BACnet/IP gateways, and machine-learning algorithms that require electricians and mechanics with software proficiency. The region faces an estimated 70,000-person shortfall in commissioning and service technicians. Carrier’s TechVantage program aims to train 100,000 globally by 2030, according to Carrier. Daikin is replicating this effort with academies in Côte d’Ivoire and Morocco. Until talent pipelines mature, project schedules continue to elongate, and facility operators outsource analytics functions to OEMs, constraining near-term smart-HVAC penetration in the Middle East and Africa commercial HVAC market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Equipment Dominance Drives Service Expansion

The equipment category represented 67.45% of the Middle East and Africa commercial HVAC market in 2025. Continued skyscraper and airport construction sustains demand for large-tonnage chillers, rooftop units and VRF condensers. Controls, although only 12.5% of spending, log the fastest 8.74% CAGR because building-code updates mandate automation. Predictive analytics services are carving out recurring revenue as owners seek to cut unplanned downtime by 15–20%.

HVAC services lag at present yet gain momentum from OEM contracts that bundle spare-parts availability and remote diagnostics. Johnson Controls’ EasyIO acquisition expanded its Niagara-based Building Management System stack, letting facility managers overlay proprietary optimization apps. As sensor density rises, data-driven performance contracts become standard, reinforcing aftermarket pull-through for spare parts and software subscriptions.

By System Type: VRF Technology Leads Efficiency Revolution

VRF secured 34.30% Middle East and Africa commercial HVAC market share in 2025, rising at 8.21% CAGR. Energy-use intensity and flexible piping layouts give the technology an edge in refurbishing multi-tenant offices. Rooftop units retain traction in cost-sensitive African retail, whereas centrifugal and magnetic-bearing chillers dominate district-cooling plants. Split and ducted split units prevail in low-rise residential and small commercial retrofits where shaft space is limited.

Global VRF shipments advance as manufacturers localize production of R-32 indoor units to meet Kigali Amendment refrigerant targets. Fifteen-year life-cycle cost assessments in Qatar confirm VRF offers 7-15% lower net present cost than constant-volume chilled water in 24-hour facilities. Modular indoor units also allow phased capex aligned with tenant fit-out, improving developer cash flow in volatile commodity-price cycles.

By End User: Data Centers Accelerate Commercial Office Transformation

Commercial offices remained the largest consumer at 26.40% of 2025 revenue, but the data-center and IT-hub segment is projected to book an 7.96% CAGR through 2031. AI training clusters double rack densities, moving operators toward rear-door liquid cooling. Hospitality applications benefit from Saudi Arabia’s accelerated hotel pipeline inside the Red Sea and Diriyah Gate projects, all requiring high-SEER VRF to satisfy luxury comfort metrics.

Institutional demand stays resilient: Saudi Arabia’s Prophet’s Mosque runs the world’s largest chiller system-over 20,000 TR of capacity across six plants-to maintain 23 °C indoors during peak pilgrimage. Retail complexes meanwhile retrofit ducted splits with smart thermostats to remain within ESMA efficiency thresholds and qualify for lower utility tariffs.

By Building Lifecycle: Retrofit Market Drives Innovation

Retrofit and replacement activities accounted for 57.10% of 2025 spending and will outgrow new-build at 8.52% CAGR. Dubai’s Energy Strategy 2050 requires existing assets to cut electricity use 40%, prompting owners to replace constant-volume air handling units with digital VAV boxes connected to cloud-based analytics.

District-cooling connectivity reduces mechanical-room footprints and frees up leasable space, an attractive incentive as yields compress in prime CBD towers. Smart retrofits employ ASHRAE Level II energy audits to scope variable-speed drives, demand-response functionality and solar thermal integration that improve Net Present Value without major structural interventions. As efficiency labels become part of valuation metrics, retrofit spending is expected to remain the backbone of the Middle East and Africa commercial HVAC market.

Geography Analysis

Saudi Arabia generated 27.60% of total spending in 2025 and is forecast to grow 8.12% CAGR to 2031, led by Vision 2030 megaprojects and enforcement of SASO energy criteria. The UAE follows as district-cooling capacity expands; Empower’s record plant underpins ambitions to reach 40% penetration by 2030. Qatar, Kuwait and Bahrain maintain steady demand through airport and rail programs tied to diversification agendas.

Across North Africa, Egypt’s building-energy certificate scheme brings transparency, attracting foreign direct investment into hospitality and light-industrial estates. South Africa leads sub-Saharan uptake thanks to load-shedding mitigation via high-SEER chillers and rooftop solar hybridization. Nigeria, Kenya and Morocco emerge as mid-tier opportunities as urbanization drives office and mall construction, though purchase decisions remain price-sensitive.

Water scarcity overlays the geography mosaic. Gulf data centers are piloting treated sewage effluent for evaporative towers, cutting freshwater draw by 27% without efficiency loss. OEMs that bundle low-water chiller packages and adaptive controls therefore gain a competitive edge in the Middle East and Africa commercial HVAC market.

Coverage of the commercial hvac market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for Europe, North America, and Asia, alongside detailed country-level intelligence for Italy, France, Japan, China, South Korea, and Germany, each shaped by local operating conditions.

Competitive Landscape

The market remains moderately fragmented; the top five manufacturers hold roughly 45% combined share, translating into a market concentration score of 6. Johnson Controls, Daikin and Carrier leverage vertically integrated portfolios and multidecade service footprints. Bosch’s USD 8.1 billion purchase of Johnson Controls’ residential and light commercial business marks a strategic tilt toward premium commercial systems in high-growth regions.

Regional champions such as Zamil Air Conditioners and Al Salem Johnson Controls optimize equipment for sand-dust ingress and 55 °C ambient ratings, protecting share in Gulf governmental tenders. Technology differentiation is converging on digitally enabled, low-GWP products; Trane’s R-290 heat-pump launch adds propane units with zero ODP and ≤3 GWP to the portfolio.

Strategic partnerships diversify channel access: Daikin’s tie-up with Softlogic strengthens commercial distribution in the UAE, while LG’s OSO water-heater acquisition rounds out integrated domestic hot-water/heat-pump offerings. OEMs increasingly bundle financing, energy-performance guarantees and operator training to lock in multi-year service contracts across the Middle East and Africa commercial HVAC market.

Middle East And Africa Commercial HVAC Industry Leaders

Daikin Industries, Ltd.

Lennox International Inc.

Robert Bosch GmbH

Johnson Controls International plc

Carrier Global Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Bosch completed its USD 8.1 billion acquisition of Johnson Controls’ residential and light commercial HVAC businesses, doubling annual HVAC revenue and boosting exposure to commercial growth corridors.

- July 2025: Trane Technologies posted EMEA bookings of USD 704.7 million, up 5%, and raised 2025 revenue guidance to 9% on strong sustainable-HVAC demand.

- July 2025: LG Electronics acquired Norwegian water-heater specialist OSO to integrate stainless-steel hot-water tanks with heat-pump systems globally.

- April 2025: Trane booked USD 720.7 million in EMEA orders, securing a 130% book-to-bill ratio that underscores resilient commercial demand.

Middle East And Africa Commercial HVAC Market Report Scope

The report tracks the revenue accrued through the sale of commercial HVAC equipment and services by various players in the Middle East and Africa market. The report also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates between 2024 and 2029. The report’s scope encompasses market sizing and forecasts for the various market segments.

The Middle East and Africa Commercial HVAC market is segmented by type of component (HVAC equipment [heating equipment and air conditioning/ventilation equipment] and HVAC services), end user (hospitality, commercial buildings, public building, and others), and country (United Arab Emirates, Saudi Arabia, and South Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| HVAC Equipment |

| HVAC Controls |

| HVAC Services |

| Variable Refrigerant Flow (VRF) Systems |

| Packaged and Rooftop Units |

| Chillers and AHU/FCU |

| Split and Ducted Split Systems |

| Hospitality and Leisure |

| Commercial Offices |

| Healthcare and Life-Science Facilities |

| Data Centers and IT Hubs |

| Retail and Shopping Malls |

| Public and Institutional Buildings |

| Other End Users |

| New-Build Installations |

| Retrofit and Replacement |

| United Arab Emirates |

| Saudi Arabia |

| Qatar |

| Kuwait |

| Oman |

| Bahrain |

| South Africa |

| Egypt |

| Other Countries |

| By Component (Value) | HVAC Equipment |

| HVAC Controls | |

| HVAC Services | |

| By System Type | Variable Refrigerant Flow (VRF) Systems |

| Packaged and Rooftop Units | |

| Chillers and AHU/FCU | |

| Split and Ducted Split Systems | |

| By End User | Hospitality and Leisure |

| Commercial Offices | |

| Healthcare and Life-Science Facilities | |

| Data Centers and IT Hubs | |

| Retail and Shopping Malls | |

| Public and Institutional Buildings | |

| Other End Users | |

| By Building Lifecycle | New-Build Installations |

| Retrofit and Replacement | |

| By Country | United Arab Emirates |

| Saudi Arabia | |

| Qatar | |

| Kuwait | |

| Oman | |

| Bahrain | |

| South Africa | |

| Egypt | |

| Other Countries |

Key Questions Answered in the Report

What is the current value of the Middle East and Africa commercial HVAC market?

The market stands at USD 1.27 billion in 2026 and is projected to reach USD 1.81 billion by 2031.

Which country leads regional demand?

Saudi Arabia accounts for 27.60% of 2025 spending and is forecast to record the fastest 8.12% CAGR through 2031.

Why are VRF systems growing rapidly?

VRF cuts electricity consumption by up to 52% in hot-dry climates and therefore secures the highest 8.21% CAGR among system types.

What drives retrofit dominance?

Mandatory SEER and refrigerant regulations plus district-cooling connectivity make retrofit work 57.10% of 2025 revenue, rising at 8.52% CAGR.

How does district cooling affect HVAC demand?

Central plants lower building-level energy use by up to 50% and extend equipment life, propelling smart-control and chiller upgrades across connected towers.

Page last updated on: