Pneumatic Conveying Systems Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

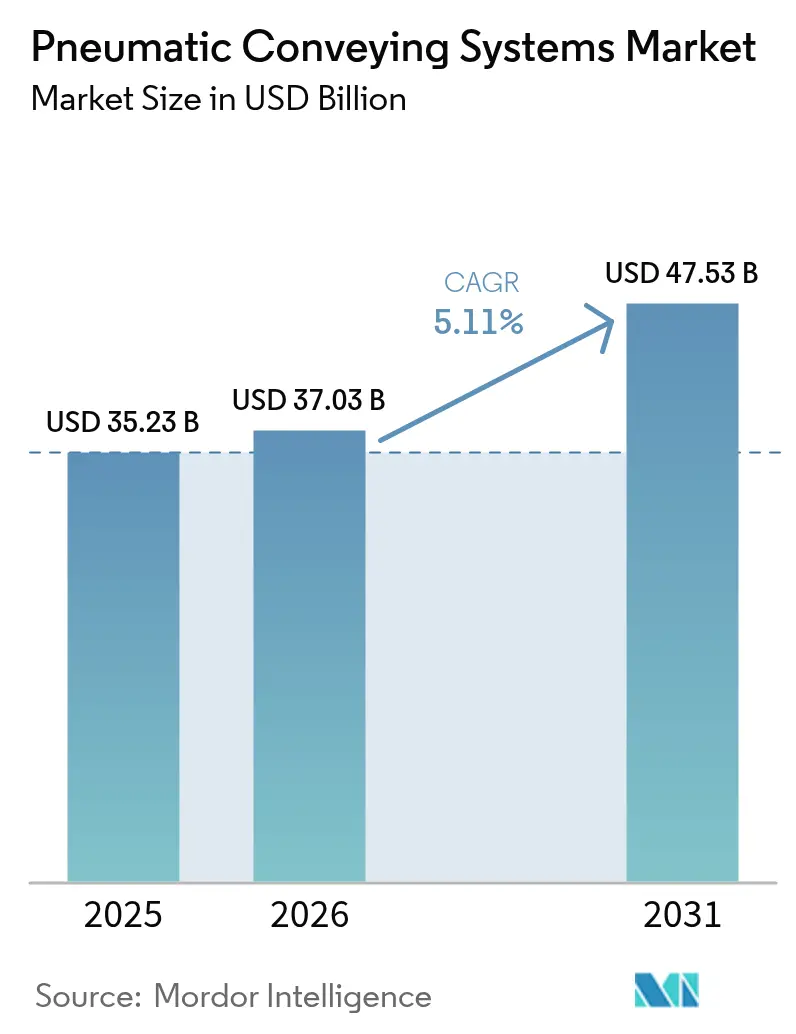

| Market Size (2026) | USD 37.03 Billion |

| Market Size (2031) | USD 47.53 Billion |

| Growth Rate (2026 - 2031) | 5.11% CAGR |

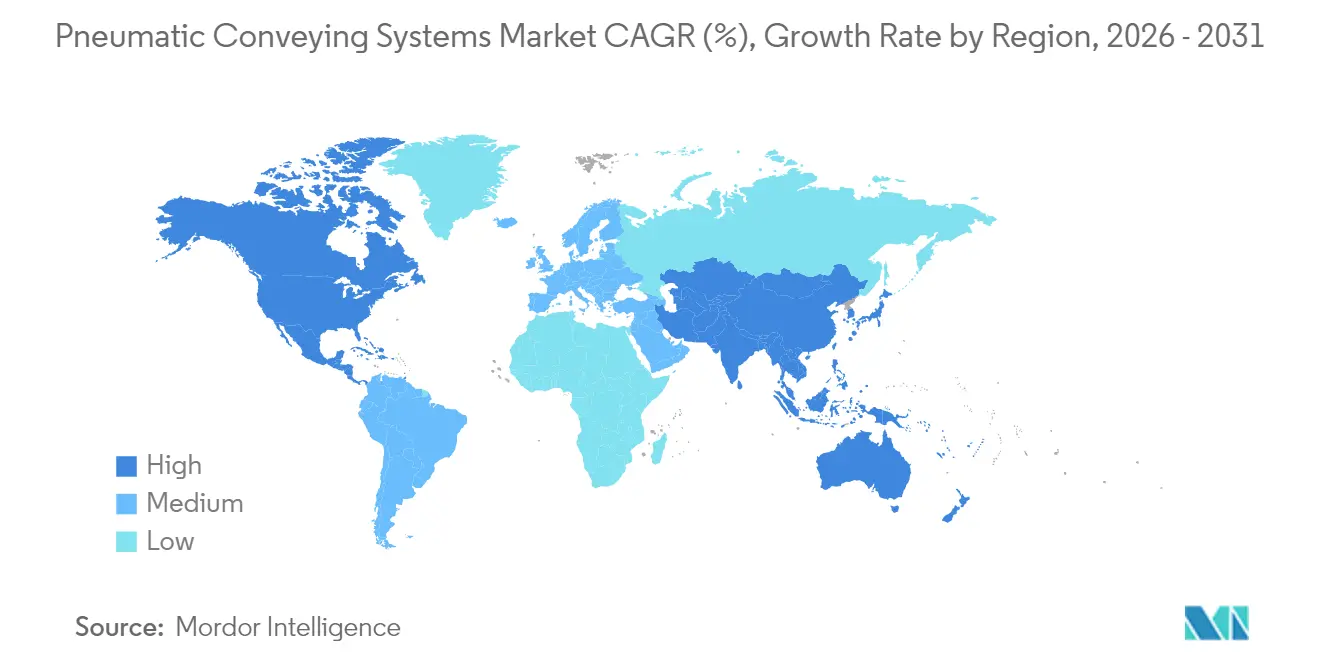

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pneumatic Conveying Systems Market Analysis by Mordor Intelligence

The Pneumatic Conveying Systems market size is expected to grow from USD 35.23 billion in 2025 to USD 37.03 billion in 2026 and is forecast to reach USD 47.53 billion by 2031 at 5.11% CAGR over 2026-2031.

Rising investments in industrial automation, growing emphasis on contamination-free bulk handling, and steady retrofits in mature manufacturing plants sustain near-term demand. Rapid battery gigafactory construction, particularly in the Asia-Pacific region, introduces a new high-growth application stream. Adoption is further reinforced by artificial-intelligence-driven airflow optimisation that cuts operating costs, helping users offset rising electricity prices. Meanwhile, competition intensifies as leading vendors accelerate acquisitions to expand their regional reach and broaden their technology offerings.

Key Report Takeaways

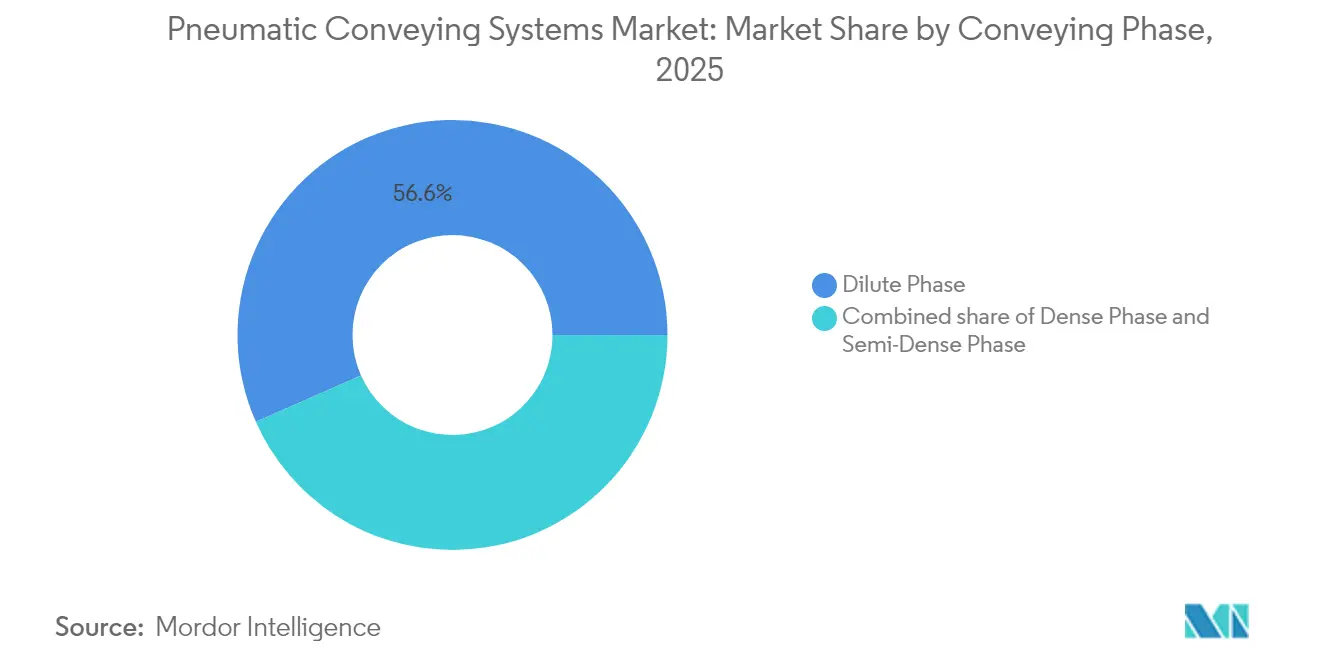

- By conveying phase, dilute phase systems held 56.62% of the pneumatic conveying systems market share in 2025, while dense phase is projected to expand at a 6.74% CAGR through 2031.

- By operating principle, positive-pressure systems commanded a 62.88% share of the pneumatic conveying systems market size in 2025, whereas vacuum conveying systems recorded the fastest growth at a 7.01% CAGR from 2026 to 2031.

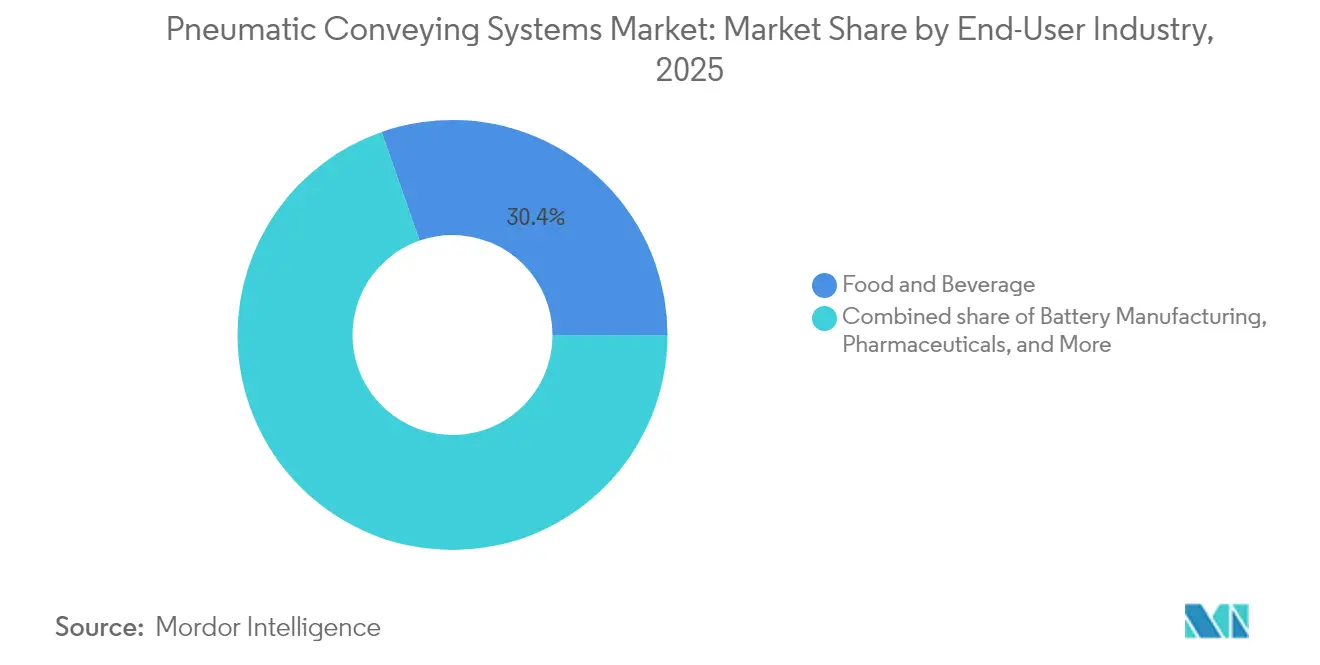

- By end-user industry, the food and beverage sector led with a 30.35% revenue share in 2025; battery manufacturing is forecast to grow at a 8.85% CAGR through 2031.

- By geography, North America accounted for 33.08% of the pneumatic conveying systems market share in 2025, while Asia-Pacific is advancing at a 7.46% CAGR to 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pneumatic Conveying Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | |

|---|---|---|---|

| Rising demand for energy-efficient bulk-handling automation | +0.8% | North America, Europe | Medium term (2-4 years) |

| Stringent food & pharma hygiene regulations favouring closed conveying | +1.2% | North America, EU | Long term (≥ 4 years) |

| Rapid capacity build-out of battery-materials gigafactories | +0.9% | Asia-Pacific, spill-over to North America & Europe | Short term (≤ 2 years) |

| AI-enabled airflow optimisation software cuts OPEX | +0.6% | North America, Europe, emerging Asia-Pacific | Medium term (2-4 years) |

| Growth of bio-based plastics requiring gentle transport | +0.4% | Europe, North America, emerging Asia-Pacific | Long term (≥ 4 years) |

| Increasing retrofits to comply with dust-explosion ATEX codes | +0.7% | Europe, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Energy-Efficient Bulk-Handling Automation

Compressed air systems account for nearly 10% of total industrial electricity use in developed economies, prompting manufacturers to scrutinise energy performance. Dense phase technology operates at lower velocities and uses less air, resulting in up to 50% energy savings compared to dilute phase conveying. Variable-frequency drives, smart sensors, and energy audit programs further optimize consumption, delivering typical payback periods of 18-24 months. Across 206 audited plants, analysts identified potential annual savings of USD 228 million from compressed-air optimisation. These benefits drive sustained upgrades and position dense-phase systems as a strategic lever for achieving decarbonization targets.

Stringent Food & Pharma Hygiene Regulations Favouring Closed Conveying

FDA 21 CFR 110.40 and USDA 7 CFR 58.228 require corrosion-resistant, sanitary transport surfaces, making enclosed pneumatic conveying essential for contamination-free movement of powders and tablets. Vacuum configurations provide negative pressure, preventing product escape and airborne dust, which supports cGMP documentation and HACCP compliance. ISO 8573 oil-free compressed-air standards and air-quality monitoring provisions further cement demand for sealed systems with easy-clean designs. The regulatory compliance imperative secures long-term adoption across food and pharmaceutical facilities.

Rapid Capacity Build-Out of Battery-Materials Gigafactories

Lithium-ion cell production requires gentle, contamination-free handling of cathode and anode powders. Pneumatic conveying accommodates inert-gas purging to manage moisture-sensitive materials, as demonstrated at the ENTEK lithium separator plant in Indiana, where systems span extrusion, coating, and drying lines.(1)U.S. Department of Energy, “Environmental Assessment ENTEK Lithium Separator Manufacturing Facility,” energy.gov Gigafactory roll-outs demand modular conveying designs that scale from pilot to multi-ton flows, presenting sizeable opportunities for specialised vendors. With electric vehicle penetration accelerating, battery plants remain a clear growth catalyst over the next decade.

AI-Enabled Airflow Optimization Software Cuts OPEX

SmartFLX controls, introduced by Conair, apply machine-learning algorithms to adjust vacuum levels, receiver distance, and bulk-density parameters in real-time, trimming energy use by up to 15%. IoT sensors generate granular data that feeds predictive-maintenance models, mitigating downtime and extending component life. Busch Vacuum Solutions’ O11O digital services suite demonstrates retrofit potential by linking multiple generators to a cloud-based dashboard accessible on mobile devices, providing operators with continuous system visibility. These digital innovations strengthen the business case for modernising existing lines and reinforce the transition toward self-optimising networks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High up-front CAPEX versus mechanical conveyors | -1.1% | Global, particularly price-sensitive emerging markets | Short term (≤ 2 years) |

| Component erosion & pipeline wear raise maintenance cost | -0.8% | Global, especially high-throughput applications | Medium term (2-4 years) |

| Carbon-pricing on compressed-air electricity use | -0.5% | Europe & North America leading carbon pricing schemes | Long term (≥ 4 years) |

| Scarcity of dense-phase design & tuning expertise | -0.3% | Global, with acute shortages in emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Up-Front CAPEX Versus Mechanical Conveyors

Pneumatic solutions often cost 40-60% more than belt or drag conveyors because they require compressors, filtration units, and pressure vessels. Added engineering expertise raises design fees, making justification difficult for small manufacturers that prioritise immediate cost reduction. Capital intensity slows adoption in price-sensitive regions, even when lifecycle savings in labour and hygiene compliance favour pneumatic choices.

Component Erosion & Pipeline Wear Raise Maintenance Cost

High-velocity flows of abrasive powders accelerate wear on elbows and pipelines, especially at directional changes. Specialty induction-hardened, or ceramic-lined elbows, extend service life but command premium prices and complex replacement procedures. Centrifugal fan studies indicate that wear increases quadratically with speed, forcing operators to balance throughput against maintenance downtime. Frequent part replacement increases total ownership costs and tempers investment enthusiasm for extremely abrasive duty cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Conveying Phase: Dense Phase Gains Momentum

In 2025, the dilute phase accounted for 56.62% of the pneumatic conveying systems market, but the dense phase is projected to post the highest CAGR of 6.74% from 2026 to 2031. Dense phase operations occur at lower air velocities, reducing energy use by 30-50% while preserving fragile particles, which appeals to pharmaceutical and specialty chemical processors. Semi-dense phase serves intermediate needs and remains a niche option for moderate distances.

Growing regulatory pressure for energy efficiency and reduced dust emissions is accelerating the adoption of dense phase. Vendors enhance their offerings with advanced pressure-control valves and wear-resistant pipeline materials. As manufacturers pursue sustainability certifications, dense-phase solutions are increasingly replacing legacy dilute lines, supporting the trajectory of the pneumatic conveying systems market.

By Operating Principle: Vacuum Systems Accelerate

Positive-pressure technology dominated the pneumatic conveying systems market in 2025 due to proven long-distance capability and lower capital outlay. Nevertheless, vacuum conveying is set to expand at a 7.01% CAGR because its negative-pressure design prevents product escape and protects operators, aligning with stricter hygiene rules. Combination systems that toggle between modes appeal to multi-material plants but represent a smaller share of revenue.

Pharmaceutical buyers increasingly specify vacuum lines for API transfer, while food processors choose them for allergen segregation. Atlas Copco’s oil-free compressors bolster USP-grade air quality, further boosting uptake. Investments in sensor-rich control panels enable automatic leak detection and flow optimisation, enhancing vacuum system reliability and expanding addressable applications.

By End-User Industry: Battery Manufacturing Surges

Food and beverage applications contributed 30.35% of 2025 revenue thanks to pervasive ingredient-handling needs and entrenched sanitary codes. Battery manufacturing, although smaller today, is forecast to log the fastest 8.85% CAGR to 2031, as electric-vehicle demand triggers exponential growth in cathode and separator output.

Chemicals and petrochemicals continue to utilize pneumatic systems for the safe transfer of corrosive powders, while pharmaceuticals show steady gains from the adoption of continuous manufacturing. Plastics processors benefit from pellet and regrind handling flexibility, and mineral processors use pneumatic lines for niche fine-powder tasks despite erosion risks. The breadth of end-use diversity underpins stable baseline demand for the pneumatic conveying systems market.

Geography Analysis

North America led with a 33.08% share in 2025, supported by mature food processing, expansive pharmaceutical capacity, and early uptake of AI-enabled upgrades. Stringent FDA and USDA standards create recurring retrofit cycles, while infrastructure investment incentives encourage energy-efficient revamps. United States installations dominate, followed by Canadian grain and Mexican automotive suppliers that favour sealed systems for paint and resin powders.

The Asia-Pacific is the fastest-growing region, with a 7.46% CAGR from 2026 to 2031, owing to India’s National Manufacturing Policy and China’s acceleration of Industry 4.0. New lithium-ion plants, plastics complexes, and packaged-food facilities specify enclosed conveying from inception, leapfrogging older open-belt alternatives. Local players, such as Tianjin FeiYun, now under the Piab Group, extend the reach of vacuum technology and shorten delivery cycles.

Europe maintains a steady uptake, anchored in ATEX explosion-protection directives and carbon-reduction targets that favour dense-phase solutions. Germany’s chemicals corridor, France’s food sector, and the United Kingdom’s pharmaceutical industry spearhead investments, while Eastern Europe rises due to regulatory synchronisation with EU norms. Nordic manufacturers prioritise ultra-low energy consumption and source advanced, dense-phase packages to meet sustainability charters.

Competitive Landscape

Market concentration remains moderate as global leaders continue to pursue acquisitions to expand their technology portfolios and regional footprints. Atlas Copco strengthened its North American presence by purchasing Air Way in November 2024, adding application engineering capacity in high-margin industries. Coperion finalised the integration of Schenck Process FPM in 2024, consolidating 140 years of engineering expertise under a unified brand and broadening dense phase offerings. Piab’s SEK 250 million acquisition of Tianjin FeiYun has enhanced its China-based vacuum conveying capabilities, catering to clients in additive manufacturing and the battery sector.

Technology differentiation now hinges on AI-driven control software, predictive maintenance analytics, and oil-free compression. Conair’s SmartFLX platform and Busch’s O11O digital services demonstrate how data integration enables 24/7 performance optimization and energy savings. Vendors also develop application-specific wear-resistant elbows to cut lifecycle costs in abrasive duties, addressing a key user pain point. While price competition persists in commodity dilute phase systems, premium dense phase and digitally packaged products command attractive margins, encouraging sustained innovation.

Emerging challengers target cost-sensitive Asian markets with simplified modular skids, but incumbents leverage global service networks and deep process knowledge to defend share. Overall, the pneumatic conveying systems market rewards suppliers that pair mechanical know-how with software intelligence and region-specific support.

Pneumatic Conveying Systems Industry Leaders

Atlas Copco AB

Coperion GmbH

Schenck Process Holding GmbH

Flexicon Corporation

Piab AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: AERZEN partnered with TÜV Rheinland to advance the safety standards for oil-free pneumatic conveying.

- February 2025: Daifuku identified the rising demand for pneumatic conveying integration with AS/RS in India.

- January 2025: Busch Vacuum Solutions rolled out O11O Digital Services, enabling IoT monitoring of multiple vacuum generators.

- November 2024: VAC-U-MAX released updated design guidelines for vacuum conveying automation.

- September 2024: The U.S. Department of Energy completed the environmental assessment for the ENTEK lithium separator plant in Indiana, featuring extensive pneumatic conveying systems.

Global Pneumatic Conveying Systems Market Report Scope

The pneumatic conveying systems market report includes:

| Dilute Phase |

| Semi-Dense Phase |

| Dense Phase |

| Positive-Pressure Conveying |

| Vacuum Conveying |

| Combination (Vacuum + Pressure) |

| Food and Beverage |

| Chemicals and Petrochemicals |

| Pharmaceuticals |

| Plastics and Rubber |

| Minerals and Metals |

| Battery Manufacturing |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Conveying Phase | Dilute Phase | |

| Semi-Dense Phase | ||

| Dense Phase | ||

| By Operating Principle | Positive-Pressure Conveying | |

| Vacuum Conveying | ||

| Combination (Vacuum + Pressure) | ||

| By End-User Industry | Food and Beverage | |

| Chemicals and Petrochemicals | ||

| Pharmaceuticals | ||

| Plastics and Rubber | ||

| Minerals and Metals | ||

| Battery Manufacturing | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the pneumatic conveying systems market by 2031?

The market is forecast to reach USD 47.53 billion by 2031, growing at a 5.11% CAGR over 2026-2031.

Which conveying phase is expanding the fastest?

Dense phase technology is set to grow at a 6.74% CAGR through 2031 due to its energy efficiency and gentle material handling benefits.

Why are vacuum systems gaining traction despite lower market share today?

Vacuum conveying offers superior containment and hygiene, aligning with stringent food and pharmaceutical regulations and posting a 7.01% CAGR forecast.

Which end-user industry shows the highest growth potential?

Battery manufacturing leads with a 8.85% CAGR as gigafactory investments scale global lithium-ion output.

What digital technologies are influencing future system upgrades?

AI-driven airflow optimisation, IoT-enabled predictive maintenance dashboards and cloud analytics are lowering operating costs and improving system reliability.

Page last updated on: