Meat Speciation Testing Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

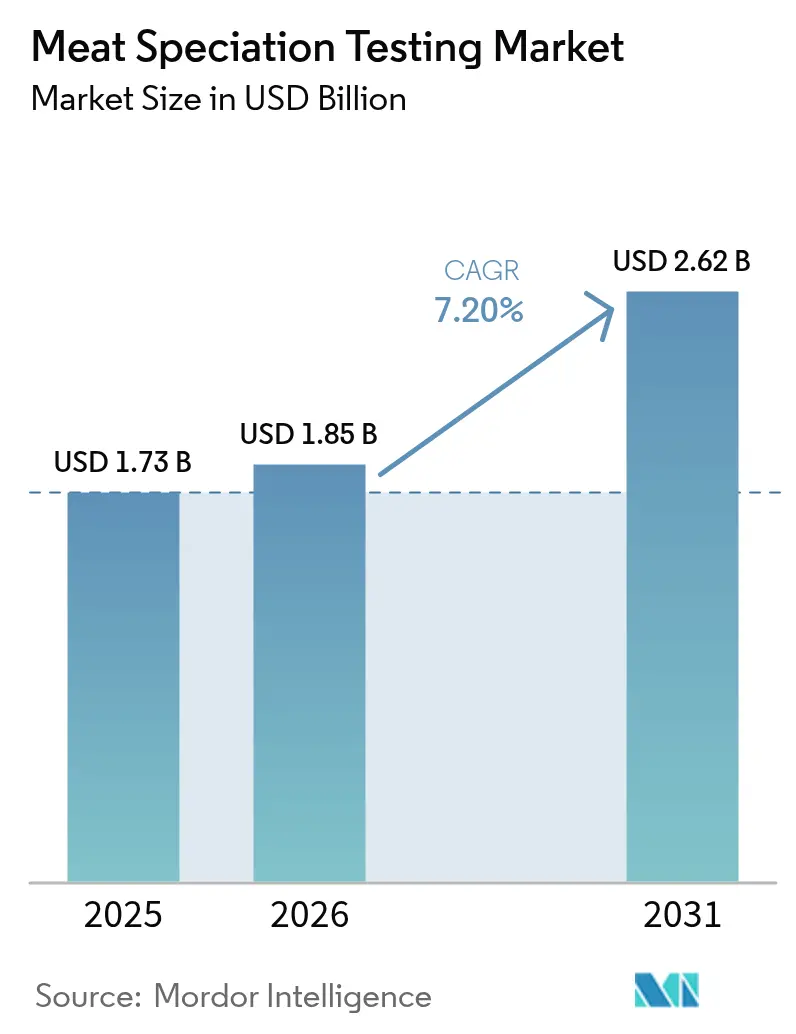

| Market Size (2026) | USD 1.85 Billion |

| Market Size (2031) | USD 2.62 Billion |

| Growth Rate (2026 - 2031) | 7.20% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Meat Speciation Testing Market Analysis by Mordor Intelligence

The global meat species identification testing market size is expected to grow from USD 1.73 billion in 2025 to USD 1.85 billion in 2026 and is forecast to reach USD 2.62 billion by 2031 at 7.20% CAGR over 2026-2031. The market expansion aligns with stricter regulatory measures against meat mislabeling, as evidenced by the U.S. Food Safety and Inspection Service setting January 1, 2028, as the compliance deadline for new meat and poultry product labeling regulations. The increasing focus on food safety, rising consumer awareness about food authenticity, and growing incidents of meat adulteration worldwide are driving the demand for reliable testing methods. Additionally, technological advancements in DNA-based testing techniques and the implementation of stringent food safety standards across regions contribute to market growth. The rise in international meat trade and the need for transparency in the food supply chain further accelerate the adoption of meat species identification testing solutions. [1]U.S. Department of Agriculture, “FSIS Establishes Uniform Compliance Date for Meat and Poultry Labeling,” usda.gov.

Key Report Takeaways

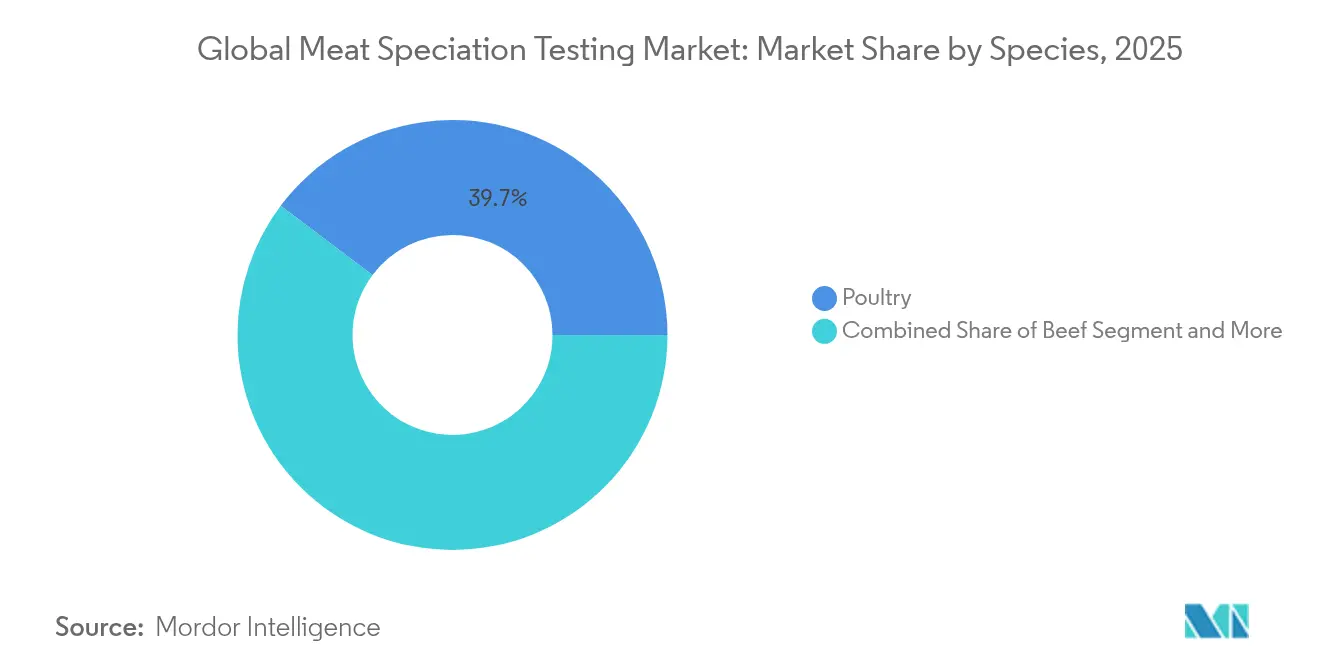

- By species, poultry led with 39.74% of the 2025 meat species identification testing market share and horse meat testing is set to post an 8.02% CAGR from 2026-2031.

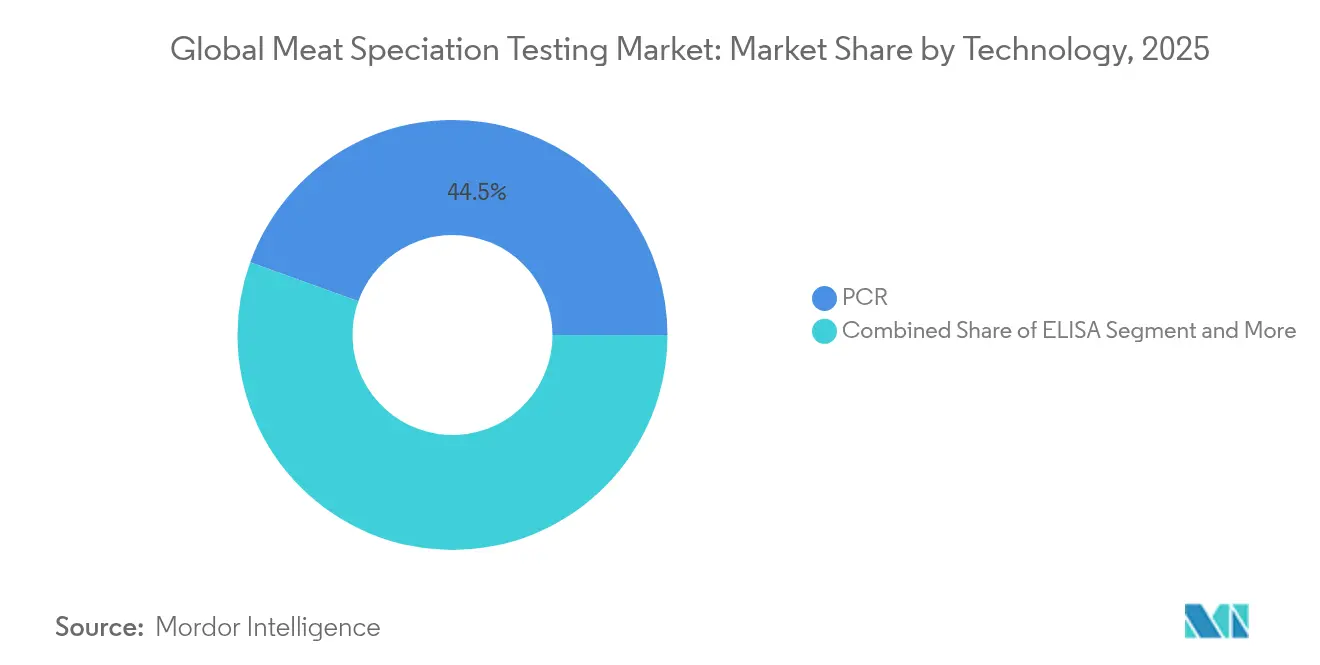

- By technology, polymerase chain reaction (PCR) retained 44.51% revenue share in 2025 while LAMP is forecast to advance at an 8.3% CAGR through 2031.

- By sample type, processed and minced meat captured 37.46% of the meat species identification testing market size in 2025; gelatine and collagen assays will expand at 7.62% CAGR to 2031.

- By testing mode, laboratory services dominated with an 87.55% share in 2025, whereas portable testing kits are projected to rise at an 8.31% CAGR through 2031.

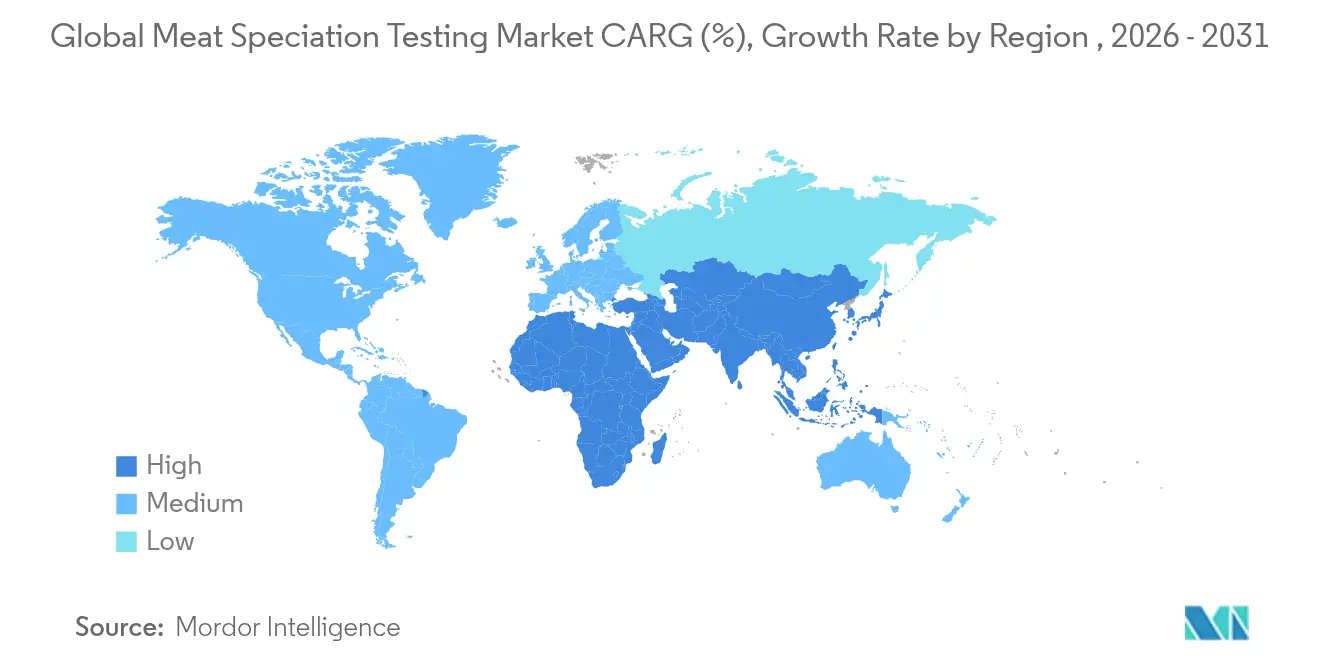

- By geography, Europe accounted for 34.12% of 2025 revenue; Asia-Pacific is projected to grow at a CAGR of 7.53% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Meat Speciation Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened regulatory crackdowns on meat mis-labeling | +1.8% | Global, with early gains in North America, Europe | Medium term (2-4 years) |

| Surge in global halal & kosher certification audits | +1.5% | Global, concentrated in APAC, Middle East | Long term (≥ 4 years) |

| Rising incidents of meat adulteration and food fraud | +2.1% | Global | Short term (≤ 2 years) |

| Consumer awareness of food authenticity and transparency | +1.2% | North America & EU, spill-over to APAC | Medium term (2-4 years) |

| Technological advancements in DNA and PCR testing | +1.4% | Global, with concentration in developed markets | Medium term (2-4 years) |

| Stringent food labeling regulations | +1.6% | Global, with early implementation in EU, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Heightened Regulatory Crackdowns on Meat Mis-labeling

Government agencies are implementing stricter documentation and laboratory verification requirements for animal-raising and origin claims. The USDA has revised its "Product of USA" labeling criteria to specifically require that animals must be born, raised, slaughtered, and processed within the United States. This change aims to enhance transparency in the meat supply chain and protect domestic producers. The European Union has enhanced its African swine fever regulations in 2024, requiring member states to implement more rigorous pathogen detection protocols for pork products. These protocols include mandatory testing at border control points, enhanced surveillance systems, and standardized reporting mechanisms across the EU member states to prevent disease spread and ensure food safety compliance. [2]Publications Office of the European Union, “African Swine Fever Control Measures,” publications.europa.eu.

Surge in Global Halal & Kosher Certification Audits

Indonesia's Halal Product Guarantee Agency has implemented comprehensive testing protocols under updated accreditation regulations. The United States halal certification framework requires traceability plans and testing procedures for high-risk facilities, including protein absence validation and contamination testing, with results maintained for multiple years. DNA extraction and PCR amplification methods have become essential for halal authentication in meat supply chains. CTAB-based methods and commercial kits such as NucleoSpin™ Food demonstrate high extraction efficiency for processed animal by-products.

Rising Incidents of Meat Adulteration and Food Fraud

Food fraud incidents increased significantly, as shown in the 2024 Global Food Fraud Report. The report identified botanical and animal origin fraud as the most frequently reported types, with meat and poultry products among the most affected commodities. These fraudulent activities include species substitution, mislabeling of origin, and adulteration of products. The rise in food fraud has prompted increased scrutiny from regulatory bodies and heightened demand for authentication technologies across the global food supply chain. Food manufacturers and retailers are implementing stricter quality control measures and traceability systems to combat this growing challenge. [3]Food Authenticity, "Global Food Fraud Report," documents.foodauthenticity.global

Consumer Awareness of Food Authenticity and Transparency

The increasing consumer demand for food authenticity has driven advancements in traceability technologies. Merck Animal Health's DNA TraceBack® system uses DNA technology to track products from farm to table, ensuring complete supply chain visibility and product integrity. The system enables real-time monitoring of meat products throughout the distribution process, helping manufacturers maintain quality standards and build consumer trust. The FDA's June 2025 draft guidance for plant-based alternatives to animal-derived foods requires accurate labeling, enabling consumers to make informed decisions and supporting accurate meat species identification. This guidance also establishes standardized labeling requirements that help prevent misrepresentation of food products and strengthen food safety protocols across the industry[4]U.S. Food and Drug Administration, "Labeling of Plant-Based Alternatives to Animal-Derived Foods" fda.gov.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced testing technologies | -1.4% | Global, with acute impact in developing economies | Medium term (2-4 years) |

| Lack of standardized testing protocols across regions | -0.9% | Global, particularly affecting cross-border trade | Long term (≥ 4 years) |

| Shortage of skilled technicians and forensic analysts | -1.1% | Global, concentrated in developing markets | Long term (≥ 4 years) |

| Limited testing infrastructure in developing economies | -1.3% | APAC, Africa, Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Testing Technologies

Triple-quadrupole GC/MS systems and advanced mass spectrometers provide high sensitivity but require substantial capital investment that many small laboratories cannot afford. The instruments' high purchase costs, combined with ongoing maintenance requirements, create significant financial barriers for smaller facilities. The cost of consumables and extraction kits increases operational expenses, with regular calibration and quality control measures adding to the financial burden. While portable LAMP devices and smartphone spectrometers offer potential alternatives, particularly for resource-limited settings, they require broader regulatory approval before they can replace traditional analytical platforms. These emerging technologies show promise in reducing both initial investment and operational costs, but their current limitations in analytical precision and regulatory compliance prevent widespread adoption in laboratory settings.

Lack of Standardized Testing Protocols Across Regions

The harmonization of testing standards has not kept pace with technological advancements. The Asia Pacific Food Law Guide highlights differences in species-testing regulations across multiple jurisdictions, preventing exporters from implementing standardized testing protocols. The European Union's evolving regulations for African swine fever demonstrate how regional health crises create specific requirements that testing laboratories must interpret and implement. This regulatory variation increases testing times and makes laboratory accreditation more complex. The lack of unified standards across regions creates additional challenges for international trade, as laboratories must maintain multiple testing protocols to meet various regulatory requirements. This fragmentation also impacts the efficiency of food safety monitoring systems and increases operational costs for testing facilities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Species: Poultry Dominance Amid Emerging Horse Testing Demand

In 2025, poultry accounted for 39.74% of market revenue, highlighting the meat species identification testing market's concentration in high-volume protein testing. The frequent occurrence of cross-contamination in processed poultry products has increased the adoption of routine PCR monitoring by processors. While horse meat testing represents a smaller segment, it is projected to grow at the highest CAGR of 8.02%, driven by European retailers' efforts to maintain consumer confidence following previous adulteration incidents.

Testing requirements vary across protein categories. Beef testing remains stable due to its high retail prices, which increase the risk of fraudulent substitution. Pork testing focuses on verifying the absence of cross-species contamination to comply with halal and kosher requirements. The demand for mutton and lamb testing is increasing in Middle Eastern markets with strict authenticity regulations. Testing for specialty meats, including venison and ostrich, represents a small but high-margin segment, driven by premium restaurants requiring verified authenticity.

By Sample Type: Processed Meat Complexity Drives Gelatine Growth

Processed and minced meat products accounted for 37.46% of the testing volume in 2025, as species identification becomes more challenging when muscle fibers are processed beyond recognition. The market has adapted by developing multiplex PCR panels that can simultaneously screen multiple ingredients in a single test.

The gelatine and collagen testing segment is projected to grow at a 7.62% CAGR through 2031, driven by increased halal and kosher certification requirements in confectionery and nutraceutical industries. The development of hydrogel-molecular-imprinting sensors, capable of detecting prohibited additives at parts-per-billion levels, has expanded testing applications beyond food to include cosmetic products.

By Technology: PCR Leadership Challenged by LAMP Innovation

PCR accounted for 44.51% of 2025 turnover, driven by its regulatory acceptance and multiplex kits that can detect up to 12 species in one run. The technology's widespread adoption stems from its proven reliability, standardized protocols, and extensive validation across global laboratories. The meat species identification testing market for LAMP systems is projected to grow at 8.3% CAGR, as isothermal amplification eliminates the need for thermal cyclers. LAMP's increasing popularity is attributed to its rapid results, simplified workflow, and reduced equipment requirements.

Sequencing platforms support high-throughput laboratories in validating entire supply chains, offering detailed genetic analysis and species authentication capabilities. Mass spectrometry, specifically LC-MS/MS, enables protein fingerprint methods that detect mechanically separated meat at trace levels, providing crucial insights for food fraud prevention and quality control. CRISPR-Cas biosensors, currently in pilot phase, offer potential single-cell detection capabilities, with ongoing research focusing on improving sensitivity, specificity, and commercial viability for routine testing applications.

By Testing Mode: Laboratory Dominance Faces Portable Kit Disruption

Laboratory testing holds 87.55% market share in 2025, driven by regulatory requirements for accredited testing protocols and complex species identification processes that require sophisticated analytical capabilities in controlled laboratory environments. The dominance of laboratory testing is further reinforced by its ability to handle high-volume sample processing, maintain strict quality control measures, and provide comprehensive analytical reports that meet international standards. Testing kits emerge as the fastest-growing segment with an 8.31% CAGR through 2031, due to advancements in portable diagnostics and point-of-care testing solutions that enable rapid on-site species verification. The increasing demand for quick results, reduced operational costs, and improved accessibility in remote locations contributes to this growth trajectory.

The testing kit segment growth is supported by innovations such as the Dragonfly platform, a portable molecular diagnostic system that combines power-free nucleic acid extraction with lyophilized colorimetric LAMP technology. This system delivers high sensitivity and specificity while eliminating cold-chain storage requirements. The platform's versatility allows for applications across various testing scenarios, from food safety inspections to environmental monitoring, making it particularly valuable for field operations and resource-limited settings. Additionally, the system's user-friendly interface and minimal training requirements enhance its adoption potential across different industry segments.

Geography Analysis

Europe accounted for 34.12% of global revenue in 2025, supported by comprehensive regulatory frameworks and increased consumer awareness following food safety incidents. The region's dominant position stems from its stringent food safety protocols and continuous monitoring systems. Sweden's implementation of new origin labeling requirements for restaurant meals strengthened this position, demonstrating the region's commitment to transparency in food supply chains.

Regional laboratories have enhanced their testing capabilities to meet African swine fever surveillance requirements, which necessitate additional species-specific testing at borders and farms. These enhanced protocols have led to significant investments in testing infrastructure and personnel training across European testing facilities. The systematic approach to disease surveillance has established new benchmarks for food safety testing across the continent.

The Asia-Pacific region is projected to grow at a CAGR of 7.53%, driven by stricter regulations and changing dietary preferences among the expanding middle class. China's introduction of fifty new National Food Safety Standards, requiring enhanced meat authenticity testing methods, has increased demand for automated extraction systems and high-throughput PCR equipment. This technological advancement has catalyzed the modernization of testing facilities across the region.

Regulatory Landscape

Regulatory oversight for meat speciation testing continues to tighten around claim substantiation, official controls, and import certification, which increases routine demand for validated molecular methods. In the United States, USDA-FSIS strengthened label-claim verification through Directive 7000.5 (effective July 2024), enabling sampling for consumer-ready products and potential rescission of label approvals when establishments cannot substantiate claims. FSIS also clarifies field practice through Directive 7000.1, moving away from Species Identification Field Test (SIFT) kits in favor of official laboratory procedures. FSIS program activity reinforces this direction, with the FY2025 Annual Sampling Plan explicitly using PCR for speciation testing in raw and ready-to-eat products.

In Europe, official controls and entry requirements are being reinforced through updated animal-origin certification rules under EU Regulation 2022/2292 (as amended by Delegated Regulation (EU) 2025/637), raising documentation and verification needs for exporters of meat, meat products, and animal-derived additives. For in-market standardization and enforcement, new poultrymeat marketing standards introduced via Commission Delegated Regulation (EU) 2026/343 and Implementing Regulation (EU) 2026/344 (February 2026) incorporate risk-based batch testing requirements, supporting greater uptake of accredited, high-throughput speciation and authenticity workflows. Parallel standard-setting activity, such as NP EN 17882:2024 for DNA barcoding (cytochrome b and COI targets) for mammals and birds, supports method harmonization and laboratory validation across jurisdictions.

Competitive Landscape

The meat species identification testing market shows moderate concentration, with Eurofins Scientific, SGS, and Bureau Veritas maintaining dominant positions through their global laboratory networks. These companies have established comprehensive testing infrastructures that span multiple regions and serve diverse industry needs. Eurofins Scientific operates more than 950 facilities, performs over 450 million analyses annually, and offers more than 200,000 validated testing methods, securing consistent business from multinational food processors. SGS strengthens its market position by combining inspection and authenticity services through its farm-to-fork auditing program, providing integrated solutions for retailers.

Companies establish competitive advantages through technological differentiation, investing in proprietary testing methods and digital solutions to improve service delivery and operational efficiency. The continuous advancement in testing methodologies has enabled faster, more accurate, and cost-effective species identification processes. Eurofins Scientific has developed the patented TAG™ technology, which uses genetic fingerprints for individual animal identification, and multiplex Real-time PCR tests that can detect up to 12 animal species in meat and animal feed.

The partnership between SafetyChain and Eurofins Scientific exemplifies market evolution, offering remote audit certification for food manufacturers and demonstrating the integration of technology platforms with testing services. These collaborations enable companies to expand their service offerings, reach new customer segments, and provide comprehensive solutions that address multiple aspects of food safety and authenticity testing. The integration of digital platforms with traditional testing services has created new opportunities for market growth and service innovation.

Meat Speciation Testing Industry Leaders

-

Eurofins Scientific SE

-

ALS Limited

-

Neogen Corporation

-

SGS SA

-

Bureau Veritas SA

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities are expanding where stricter claim verification intersects with the need to test more frequently across complex product formats, including processed and minced meat, multi-ingredient foods, and gelatine and collagen. Enforcement programs and official control frameworks are embedding routine sampling and laboratory confirmation, illustrated by USDA-FSIS label-claim verification directives and the continued use of PCR speciation testing in the agency's FY2025 sampling plan. In parallel, the EU's updated import certification requirements under Regulation 2022/2292 (amended by 2025/637) increase authentication needs for cross-border trade in meat and animal-derived ingredients.

A second opportunity area is method standardization and workflow modernization aimed at reducing turnaround time and expanding surveillance coverage. Widely referenced technical standards for speciation, including ISO real-time PCR and sequencing-related standards and DNA barcoding standards such as EN 17882, support validation pathways for multiplex panels and multi-species claims. National guidance such as the UK Food Standards Agency's 1% threshold for DNA from unintended species also reinforces sensitivity requirements for routine monitoring. This creates room for providers that combine accredited lab services with field-deployable sample-to-result workflows (automation, multiplexing, and simplified extraction), and for instrument and kit suppliers aligning platforms to standardized acceptance criteria across regulators, certification bodies involved in halal and kosher audits, and multinational food operators.

Recent Industry Developments

- July 2026: USDA-FSIS announced that beginning July 20, 2026, it will extend metals analysis under the National Residue Program to include multi-ingredient processed products containing meat or poultry. The expanded surveillance increases the compliance burden for processors with complex formulations and supports broader adoption of accredited, multi-analyte testing workflows alongside authenticity programs.

- April 2025: Spore.Bio raised USD 23 million in a Series A round led by Singular, bringing total funding to USD 31.3 million to advance its AI-driven microbiology testing platform. While centered on microbiology, the investment highlights continued capital flow into faster, more automated food testing workflows that can be integrated into authenticity and verification programs.

- October 2024: SGS announced the implementation of next-generation sequencing (NGS) for meat and fish speciation testing in the United Kingdom, offering species identification for raw and processed samples using a database covering more than 12,000 species. The move broadens the addressable scope beyond targeted PCR panels and strengthens competitive differentiation for laboratories serving complex authenticity investigations.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of services and kits used to identify animal species in meat and meat based products, so buyers can verify labeling, prevent substitution, and meet food safety and trade requirements.

Scope exclusions: It does not include routine microbiology, chemical contaminant testing, or general quality checks that do not determine species identity.

Segmentation Overview

-

By Species

- Beef

- Pork

- Poultry

- Mutton/Lamb

- Horse

- Others

-

By Technology

- PCR

- ELISA

- DNA Sequencing (NGS)

- Mass-Spectrometry (MALDI-TOF/LC-MS)

- Loop-Mediated Isothermal Amplification (LAMP)

-

By Sample Type

- Raw Muscle Meat

- Processed/Minced Meat

- Ready-to-Eat and Cooked Products

- Gelatine and Collagen

-

By Testing Mode

- Lab Testing

- Testing Kits

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the factual base for the model, especially on meat production and trade flows, inspection intensity, and food fraud enforcement patterns by geography. We reviewed public sources such as USDA and FDA materials, EFSA publications, FAO production statistics, UN Comtrade trade tables, and ISO method references that reflect commonly accepted testing practices.

To convert these external signals into a usable sizing structure, we also screened company filings, investor presentations, laboratory accreditation listings, association websites, and credible press for service offerings and pricing logic. Where needed, a paid subscription covering company financials and a patent database were used to cross-check activity levels and technology direction. The desk sources listed above are illustrative, and many other references were used to collect data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary work focused on laboratories, kit suppliers, food processors, importers, and regulatory facing stakeholders so we could confirm what gets tested, how often it gets tested, and what drives method choice across regions. We used interviews and surveys to tighten assumptions on species mix in testing demand, the split between lab testing and kits, and price ranges by sample type (raw muscle meat versus processed and cooked products), which were then used to sanity-check the model outputs.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 17% | APAC: 43% |

| Mid tier: 52% | Functional/Unit leaders: 27% | EMEA: 35% |

| Smaller Players: 21% | Managers: 56% | Americas: 22% |

Market-Sizing & Forecasting

Sizing was built using a top-down and bottom-up flow, where country level meat processing and trade exposure were used to reconstruct the addressable testing pool, and then filtered by the share of samples that typically require species verification under labeling, export, and fraud risk triggers. Once that demand pool was formed, pricing was applied based on testing mode and sample type, and totals were summed to the regional and global level.

To keep the model tied to reality, we corroborated results with selective bottom-up approximations, such as rolling up a sample of laboratory revenues where disclosure is available, and then checking implied test volumes using typical price per test ranges. Key inputs used in the model include processed meat output as a proxy for complex matrices, import and export volumes for high scrutiny corridors, frequency of compliance testing in regulated categories, the mix of PCR versus ELISA versus sequencing in routine workflows, and the share of cases handled through kits versus lab services. When bottom-up signals were incomplete for smaller labs, gaps were handled using conservative productivity and utilization assumptions that were stress tested in interviews.

Forecasting relied on scenario analysis supported by expert views on enforcement intensity, cross-border trade growth, and the shift toward faster DNA based methods. Growth rates were then applied by region and testing mode, and finally rebalanced so the overall path remains consistent with the validated demand indicators.

Data Validation & Update Cycle

Validation was done through multiple steps, starting with internal checks on math consistency, unit logic, and year-on-year movement by region and testing mode. Outputs were then compared with independent signals, such as changes in meat trade volumes, new labeling or inspection actions, and shifts in method adoption reported by labs and standards bodies.

When a segment showed unusual jumps, assumptions were revisited, and respondents were re-contacted to confirm whether the change came from pricing, volume, or mix. Before sign-off, a second analyst review is completed to challenge key inputs and confirm that the story matches the numbers. Reports are refreshed annually, and interim updates are made when material events affect demand, pricing, or regulations, followed by a final pre-delivery pass so clients receive the latest view.

Mordor Intelligence's Meat Speciation Testing Market Size Compared Against Other Published Estimates

Published market sizes for meat speciation testing can vary a lot because sources do not always count the same revenue streams, and they often use different base years, currencies, and growth assumptions. Differences also show up when one model leans heavily on broad food testing totals, while another builds up from meat specific demand signals.

Testing kits sold for general food authenticity screening are treated differently across studies, and in Mordor Intelligence's view, they sit outside the meat speciation testing scope unless the kit use case is explicitly tied to meat species identification in the defined sample set. Some estimates also blend wider fraud analytics, broader laboratory services, or adjacent authenticity categories, which can inflate the total. On the forecasting side, aggressive assumptions on enforcement ramp-ups and price escalation can raise the final number if they are not cross-checked against actual method mix and sample volumes.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.85 B (2026) | |

| Global Consultancy A | USD 2.50 B (2024) | Uses an earlier base year and appears to include broader food authenticity spend and form factors that are not always tied to meat species verification, which can lift the total when summed across end uses. |

| Regional Consultancy B | USD 2.30 B (2024) | Likely applies higher average price per test assumptions and a wider inclusion of services delivered within general lab testing menus, which can overstate value if test frequency is not anchored to meat specific sampling drivers. |

Overall, the spread mainly comes from scope and pricing logic, followed by base-year timing. By keeping the demand pool anchored to meat related sample volumes and validated method mixes, the estimate stays traceable to clear inputs that can be rechecked and updated as market conditions change.

Key Questions Answered in the Report

What is the current value of the meat species identification testing market?

The market generated USD 1.85 billion in 2026 and is projected to reach USD 2.62 billion by 2031.

Which species category leads revenue?

Poultry commands the largest 2025 share at 39.74% owing to high consumption volumes and cross-contamination risk.

Why is LAMP technology gaining ground?

LAMP offers constant-temperature amplification, portable hardware, and lower per-test costs, driving an 8.3% CAGR through 2031.

Which region is growing fastest?

Asia-Pacific shows the highest forecast growth at 7.53% CAGR, spurred by China’s new food safety standards and wider halal demand.

What restrains wider testing adoption in developing nations?

High capital costs for advanced instruments and lack of harmonized protocols slow uptake despite rising fraud incidents.

Page last updated on: