Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

| Market Size (2025) | USD 5.78 Billion |

| Market Size (2030) | USD 7.62 Billion |

| Growth Rate (2025 - 2030) | 5.68% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Middle-East And Africa Fruits And Vegetable Juice Market Analysis by Mordor Intelligence

The Middle East and Africa fruit and vegetable juice market size stood at USD 5.78 billion in 2025 and is forecast to reach USD 7.62 billion by 2030, reflecting a 5.68% CAGR during 2025-2030. Urbanization, a shift towards health-focused consumption, and supportive nutrition policies drive demand in rapidly expanding modern retail channels across metropolitan areas. Climate-driven hydration needs, government initiatives promoting 100% juice, and advancements in cold-chain technologies collectively support volume growth. The increasing pace of urbanization has fueled demand for convenient, ready-to-drink beverages, making fruit and vegetable juices a preferred option for on-the-go consumers. Consumers are increasingly opting for juices free from added sugars, preservatives, and artificial colors, reinforcing the clean-label trend in retail. Manufacturers are focusing on flavor innovations, clean-label production, and halal certifications to secure premium shelf space and maintain brand equity. While competition remains moderate, regional players leverage local taste preferences and vertically integrated sourcing to counter the scale advantages of multinational companies. Growth opportunities are concentrated in functional blends, organic variants, and digital direct-to-consumer models, driven by the rising adoption of smartphones.

Key Report Takeaways

- By category, fruit juice led with 75.34% revenue share in 2024; vegetable juice is advancing at a 5.91% CAGR through 2030.

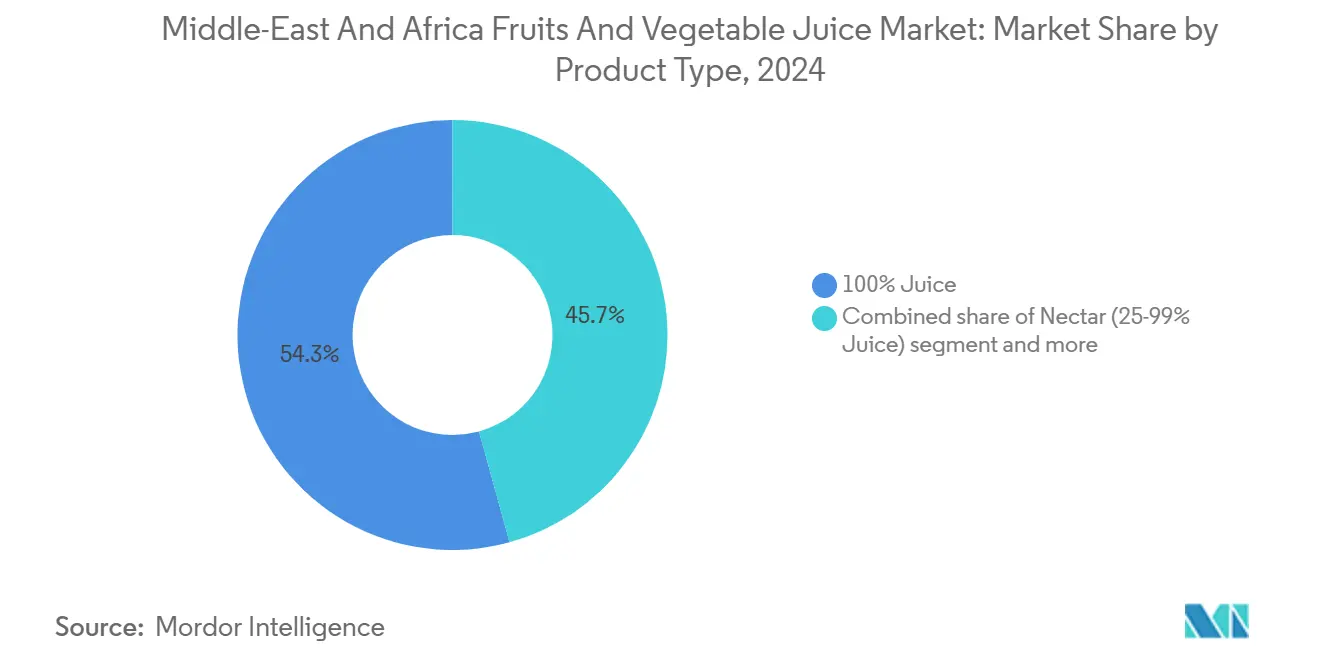

- By product type, 100% juice held 54.28% of the Middle East and Africa fruits and vegetable juice market share in 2024, while it is also projected to expand at a 6.15% CAGR to 2030.

- By nature, conventional variants accounted for 84.92% of the Middle East and Africa fruits and vegetable juice market size in 2024; organic products record the fastest growth at 7.22% CAGR over the same horizon.

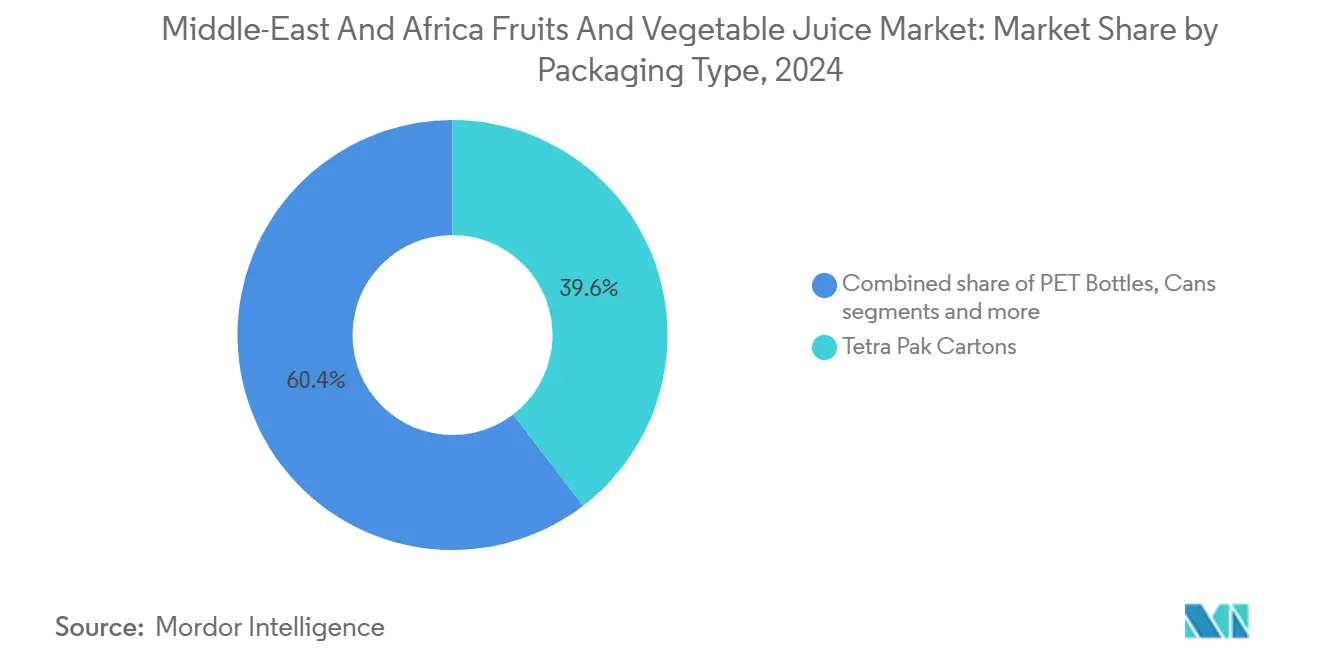

- By packaging, Tetra Pak cartons captured 39.60% share in 2024; PET bottles post the highest forecast CAGR at 6.27% through 2030.

- By distribution channel, supermarkets and hypermarkets represented 44.58% revenue share in 2024, whereas online retail stores are expanding at a 7.12% CAGR to 2030.

- By geography, Saudi Arabia commanded 24.82% revenue contribution in 2024; Nigeria delivers the region’s quickest expansion at 6.38% CAGR to 2030.

Middle-East And Africa Fruits And Vegetable Juice Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health-centric shift from carbonated sodas to 100 % juices | +1.2% | Global, strongest in UAE, Saudi Arabia | Medium term (2-4 years) |

| High climate-driven demand | +0.8% | Middle East and North Africa, extending to Sub-Saharan Africa | Long term (≥ 4 years) |

| Preference for natural and no-additive products | +0.9% | Global, premium segments in GCC states | Medium term (2-4 years) |

| Growing popularity of functional juices | +0.7% | Urban centers across Middle East and Africa, led by UAE, Saudi Arabia | Short term (≤ 2 years) |

| Product innovation and new flavor launches | +0.5% | Regional, with spillover effects across Middle East and Africa | Short term (≤ 2 years) |

| Halal certification as a critical purchase factor | +0.6% | Middle East and Africa-wide, strongest impact in Muslim-majority markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Health-centric shift from carbonated sodas to 100 % juices

With growing awareness of the risks associated with high sugar and artificial ingredients in sodas, consumers are increasingly opting for 100% juices as a natural source of hydration and nutrients. Rich in vitamins, minerals, and antioxidants, juices align with the region's shift toward health-conscious lifestyles. In the Middle East and Africa (MEA), intensified health awareness campaigns are driving a significant transition from carbonated beverages to pure fruit juices. According to the Saudi Food and Drug Authority, Saudi Arabia's government initiatives targeting 85% localization in food production by 2030[1]Source: Saudi Food and Drug Authority, "Public health", www.sfda.gov.sa emphasize nutritional quality standards, favoring 100% juice products over artificially sweetened alternatives. This shift is particularly prominent among urban millennials and Generation Z, who are willing to pay a premium for perceived health benefits. Globally, consumers perceive 100% juice as healthy, natural, and flavorful. This behavioral shift is sustaining demand for fruit-based alternatives while traditional cola consumption declines. Workplace wellness programs and educational institutions further support this trend by promoting healthier beverage options in corporate and academic environments.

High climate-driven demand

Extreme temperatures and water scarcity in the MENA region are significantly influencing beverage consumption patterns. Juice products, valued for their hydration and nutritional properties, are gaining prominence during extended periods of heat. In 2023, the Federal Competitiveness and Statistics Centre recorded an average maximum temperature of 34.4 degrees Celsius in the United Arab Emirates[2]Source: Federal Competitiveness and Statistics Centre, "Climate Statistics 2023", www.uaestat.fcsc.gov.ae. To address climate-induced nutritional gaps, consumers are increasingly opting for functional juice formulations fortified with electrolytes and vitamins. Manufacturers are leveraging the predictable seasonal demand surges for juices, driven by rising temperatures, to optimize capacity planning and inventory management. In nations such as Saudi Arabia, the UAE, and Egypt, juices have become a staple in both traditional diets and modern lifestyles, meeting thermal comfort and nutritional preferences. Juice producers in the MEA region are focusing on developing and marketing flavors suited for hot weather, including citrus, pomegranate, and watermelon blends, which are widely regarded as refreshing. To maintain sustainable raw material supply chains, agricultural strategies are shifting towards cultivating heat-resistant citrus varieties.

Preference for natural and no-additive products

Clean-label positioning is becoming a significant competitive advantage as consumers pay closer attention to ingredient lists and avoid products with artificial preservatives, colors, and flavoring agents. The global trend toward transparency is particularly impactful in markets where traditional fruit consumption emphasizes freshness and purity. High Pressure Processing (HPP) and Pulsed Electric Field (PEF) technologies allow manufacturers to extend shelf life without using chemical additives, meeting consumer demands while addressing distribution challenges in remote areas. In urban markets, especially among affluent consumers in the UAE and Saudi Arabia, "all natural" claims can achieve price premiums of 15-25%. Regulatory frameworks are increasingly supporting natural positioning by introducing standardized definitions and certification requirements to prevent misleading claims. Additionally, encapsulation techniques for bioactive compounds enable manufacturers to fortify juices with vitamins and minerals while maintaining clean-label standards.

Growing popularity of functional juices

Traditional juice categories are being transformed into functional wellness platforms through fortification with vitamins, minerals, probiotics, and botanical extracts to address specific health concerns. Formulations aimed at mental wellness and stress relief are gaining popularity as urban professionals face increasing work-life balance challenges. Immune support formulations, emphasizing vitamin C, zinc, and vitamin D, are strongly resonating with consumers following heightened health awareness from recent global challenges. Consumers focused on digestive wellness are gravitating toward gut health formulations that incorporate probiotic strains and prebiotic fibers in convenient beverage formats. Energy blends that combine traditional fruit bases with adaptogens and natural caffeine are effectively capturing market share from synthetic energy drinks. The functional segment not only meets evolving wellness priorities across age demographics but also benefits from premium pricing structures, boosting manufacturer margins. To meet the growing demand for functional juices, companies are introducing new products. For instance, in December 2024, iPRO, a leader in healthy hydration, launched its New Healthy Juice Drink at Spinneys in the UAE. Staying committed to offering natural beverages, iPRO introduced three refreshing flavors – Orange and Mango Twist, Berry Mix, and Tropical Burst – designed to revitalize households across the UAE.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening sugar-content regulations and sin-tax expansion | -0.9% | GCC states, expanding to North Africa | Medium term (2-4 years) |

| Seasonal raw-material volatility and import-dependence for concentrates | -1.1% | Global, acute in import-dependent markets | Short term (≤ 2 years) |

| Supply chain and distribution challenges in remote areas | -0.6% | Sub-Saharan Africa, rural Middle East and Afrocaregions | Long term (≥ 4 years) |

| Perishability and shelf-life constraints | -0.4% | Hot climate regions, limited cold chain areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tightening sugar-content regulations and sin-tax expansion

Excise tax implementations across Gulf states, including a 50% levy on sweetened beverages in the UAE and Saudi Arabia, are transforming cost structures and shaping consumer purchasing decisions for sugar-containing juice products. The GSO FDS 1820:2023 General Standard for Fruit Juices, Nectars, and Drinks establishes unified specifications across GCC markets, leading to compliance costs and reformulation demands for manufacturers. Reformulating to produce lower-sugar variants requires substantial investment in research and development, as well as consumer acceptance testing, which could disrupt existing product lines and brand positioning. The regulatory framework provides a competitive edge to 100% juice products that naturally contain fruit sugars, while nectar and juice drink categories with added sweeteners face disadvantages. Additionally, compliance monitoring and documentation requirements add to the operational complexities for manufacturers operating across multiple regulatory jurisdictions in the region.

Supply chain and distribution challenges in remote areas

Cold chain infrastructure limitations across Sub-Saharan Africa and remote regions of the Middle East and Africa (MEA) hinder market penetration and inflate distribution costs for perishable juice products. Bottlenecks arise from limited refrigerated storage, unreliable power supplies, and inadequate transportation networks, stalling efficient product flow to underserved markets with notable growth potential. In regions reliant on diesel generators, high energy costs for refrigeration not only escalate operational expenses but also squeeze profitability for distributors catering to remote locales. While IoT monitoring systems and renewable energy solutions present promising avenues to bridge these infrastructure gaps, their successful implementation hinges on synchronized investments from various supply chain stakeholders. Despite a clear demand for nutritious beverages, consumers in remote areas often grapple with limited disposable income, making premium-priced juice products a stretch. This purchasing power limitation intensifies distribution hurdles. To navigate these challenges, last-mile delivery solutions are turning to innovative strategies, such as mobile retail units and collaborations with local distributors who possess a keen understanding of regional market dynamics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Category: Fruit Juice Dominance Drives Market Foundation

Fruit juice holds a dominant 75.34% market share in 2024, highlighting consumers' strong preference for traditional citrus, tropical, and stone fruit varieties influenced by diverse cultural contexts. The region's high fruit production further supports this market. For example, Africa's fruit production reached 137.15 million metric tons in 2023, according to the Food and Agriculture Organization[3]Source: Food and Agriculture Organization, "Crops and livestock products", www.fao.org . On the other hand, the vegetable juice segment, though smaller, is experiencing rapid growth with a 5.91% CAGR through 2030. This growth is primarily driven by health-conscious consumers seeking beverages with functional nutrition and lower sugar content. Urban markets, influenced by wellness trends, place a premium on certain vegetable juices. Varieties such as carrot, beetroot, and green vegetable blends command significant price premiums. Tetra Pak's Juice Index research identifies vegetable nutrition as a key growth trend, with companies like Kagome leading innovations in vegetable juice using advanced aseptic packaging solutions.

Hybrid formulations that combine fruit and vegetable ingredients are emerging as a strategic option. They offer familiar taste profiles while incorporating functional benefits, appealing to health-conscious consumers. This segmentation reflects a broader dietary shift in the region. As awareness of chronic disease prevention increases, traditional fruit-based diets are gradually incorporating vegetable-based nutrition. Additionally, the seasonal availability of both fruit and vegetable juices creates complementary demand cycles. This enables manufacturers to optimize production capacities and streamline raw material procurement, effectively managing diverse agricultural supply chains.

By Product Types: Pure Juice Premiumization Accelerates Growth

In 2024, 100% juice products account for a leading 54.28% market share and demonstrate the highest growth with a 6.15% CAGR (2025-2030). This reflects a strong consumer inclination toward premium, undiluted juices over nectar and juice drink alternatives. This leadership position highlights the effectiveness of premiumization strategies that position pure juice as a healthier alternative to artificially enhanced beverages. Nectar products, with 25-99% juice content, attract price-conscious consumers by providing fruit nutrition at lower price points. Conversely, juice drinks containing less than 25% juice face obstacles due to sugar taxation policies and growing health awareness. Regulatory developments increasingly favor 100% juice products, as excise taxes on sweetened beverages create cost disadvantages for diluted drinks with added sugars.

In Gulf states and urban African markets, growing disposable incomes are encouraging consumers to pay a premium for 100% juice, facilitating a shift away from lower-juice-content options. Manufacturing advancements, including modern processing technologies that preserve nutritional value and extend shelf life without additives, are driving margin growth in the pure juice category. Private label opportunities in the 100% juice segment remain underutilized compared to other beverage categories, presenting retail chains with an opportunity to differentiate themselves and achieve higher margins through exclusive formulations and innovative packaging.

By Nature: Organic Segment Captures Premium Growth Momentum

Conventional juice products hold a dominant 84.92% market share in 2024. Long-standing consumer habits and strong familiarity with conventional juice brands have built significant trust and loyalty. Many consumers continue to choose conventional juices due to their consistent taste, quality, and brand recognition. On the other hand, organic alternatives are experiencing notable growth, with a 7.22% CAGR (2025-2030), reflecting a shift in consumer preferences toward sustainable agriculture and chemical-free production. The organic premium presents lucrative margin opportunities for manufacturers with certified supply chains and processing facilities. Halal organic certification has emerged as a compelling combination, addressing both religious compliance and health-conscious needs among Muslim consumers in the region. However, regulatory frameworks for organic certification vary widely across MEA markets, posing challenges for manufacturers aiming for regional distribution while offering competitive advantages to those adept at managing diverse certification requirements.

Building a supply chain for organic fruit sourcing requires establishing long-term partnerships with certified growers and investing in traceability systems to ensure transparency from farm to finished product. Retailers leverage the appeal of organic positioning by offering premium placements and marketing support for organic products, using them to differentiate their beverage offerings and attract affluent customer segments. Climate change impacts organic agriculture by disrupting traditional growing patterns, but it also raises consumer awareness of sustainability, often favoring organic production methods.

By Packaging Type: Sustainable Innovation Reshapes Format Preferences

Tetra Pak cartons hold a 39.60% market share in 2024, capitalizing on their sustainability focus and extended shelf-life features to perform well in challenging climates. PET bottles, driven by consumer convenience and enhanced urban recycling infrastructure, exhibit the fastest growth with a 6.27% CAGR (2025-2030). Glass bottles cater to premium markets but face logistical challenges such as weight and breakage, particularly in remote areas. Aluminum cans are gaining popularity for single-serving and on-the-go consumption, while pouches and other formats address specific needs like food services and institutional sales.

Tetra Pak's introduction of the Tetra Prisma Aseptic 300 Edge format, which reduces the carbon footprint by up to 76% and includes tethered closures to decrease litter, highlights the industry's focus on eco-friendly innovations that also meet consumer convenience demands. Advances in paper-based barriers, increasing paperboard content from 70% to 80% and achieving 90% renewable content with plant-based polymers, represent significant progress in sustainable packaging technology. The packaging sector increasingly aligns with circular economy principles, with manufacturers investing in recycling infrastructure and consumer education to enhance material recovery and reprocessing at the end of life.

By Distribution Channel: Digital Transformation Accelerates Retail Evolution

Supermarkets and hypermarkets hold a 44.58% share of the juice distribution market in 2024, leveraging their scale advantages and advanced cold chain infrastructure. This establishes them as the primary distribution hubs for juice products in urban and suburban areas. Online retail stores are experiencing the fastest growth, with a 7.12% CAGR (2025-2030), driven by rapid digital adoption and a rising preference for convenience, trends that gained traction during recent global disruptions. Convenience and grocery stores play a critical role by providing last-mile access in densely populated urban regions and catering to impulse purchases. Additionally, other channels, such as food services and institutional sales, focus on specific market segments with customized product formats and pricing.

The digital transformation in juice retail is creating opportunities for direct consumer engagement, subscription services, and personalized product recommendations based on purchase history and dietary preferences. However, cold chain logistics for online juice sales require specialized infrastructure and efficient delivery systems, favoring established e-commerce platforms with refrigerated fulfillment networks. Mobile commerce and social media marketing are particularly effective in reaching younger demographics, who are more inclined to purchase premium juice products through digital channels. While traditional retail partnerships remain essential for market penetration, manufacturers are increasingly investing in omnichannel strategies that integrate online and offline touchpoints for comprehensive market coverage.

Geography Analysis

Saudi Arabia holds a leading 24.82% share of the regional market in 2024, driven by government efforts to enhance food security and boost local production. These initiatives align with the Vision 2030 goals aimed at economic diversification. Additionally, excise tax policies on sweetened beverages create a favorable environment for 100% juice products while contributing to government revenues for infrastructure development. The Saudi Food and Drug Authority has also implemented stricter import controls and mandatory registration processes, ensuring product quality and protecting domestic manufacturers from inferior competition.

Nigeria is the fastest-growing market in the region, with a projected 6.38% CAGR through 2030. This growth is supported by rapid urbanization, a growing middle class, and increased health awareness among younger consumers. The country's large population and improving retail infrastructure offer significant long-term growth opportunities. However, international manufacturers face challenges such as distribution issues in remote areas and currency fluctuations. Despite climate-related agricultural challenges, Egypt is strengthening its position as a regional production hub through expansions in citrus processing capacity.

The United Arab Emirates leverages its strategic role as a trade and logistics hub for the broader MEA markets while advancing domestic food production through initiatives like Food Tech Valley. This initiative has attracted major investments and partnerships with global companies, including PepsiCo and the World Food Programme. Morocco, Turkey, and South Africa contribute notable market shares due to their established agricultural sectors and processing capabilities. However, each faces specific challenges, such as water scarcity, political instability, and economic volatility, which influence their long-term growth prospects. The "Rest of Middle East and Africa" segment includes a variety of markets at different stages of development, with distinct regulatory environments and consumer preferences. This diversity necessitates localized strategies to achieve successful market entry and sustainable growth.

Competitive Landscape

The Middle East and Africa juice market exhibits moderate concentration with established multinational players leveraging vertical integration strategies alongside regional champions that capitalize on local market knowledge and halal certification advantages. Advanced technology adoption has become a key differentiator in this market, with companies increasingly forming strategic digital partnerships to modernize their operations. For instance, in March 2025, Tetra Pak signed a 3-year agreement with Al Rabie to upgrade production facilities in Saudi Arabia. This partnership highlights the industry's emphasis on processing innovations to enhance operational efficiency and product quality.

Growth opportunities are emerging in areas such as functional juice formulations, organic product positioning, and sustainable packaging solutions. These trends align with evolving consumer preferences and allow companies to achieve premium pricing. Additionally, disruptors like Milaf Cola, backed by Saudi Arabia's Public Investment Fund, are gaining momentum. By leveraging nationalist sentiments and incorporating indigenous ingredients, these brands are competing with international players in specific market segments. Regulatory compliance frameworks, particularly those related to halal certification and GSO standardization, act as protective barriers for established players. These frameworks not only reinforce their competitive positioning but also create significant entry barriers for new players lacking the required certifications and local market expertise.

Key players in the market include Almarai Company, Al Rabie Saudi Foods Co., The Coca-Cola Company, Del Monte Foods, Inc., and PepsiCo Inc. These companies are capturing a significant share of the market by launching innovative products that focus on nutritional benefits, such as high fiber content and 100% pure fruit and vegetable concentrates. They are actively responding to changing consumer preferences by consistently introducing new products, ensuring they remain competitive and relevant in the dynamic market environment.

Middle-East And Africa Fruits And Vegetable Juice Industry Leaders

-

Del Monte Foods, Inc

-

Almarai Company

-

Al Rabie Saudi Foods Co. Ltd.

-

The Coca-Cola Company

-

PepsiCo Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Rubicon Arabia has introduced a new line of 100% natural juices for kids in the UAE. Known as the "Rubicon Kids" range, these juices feature clean-label, nutrient-rich blends designed to appeal to children’s tastes while ensuring parents’ confidence.

- February 2025: Almarai Co Ltd has introduced a premium organic fruit juice line made with locally sourced dates and pomegranates, aligning with Vision 2030's environmental goals. Additionally, the company has invested USD 50 million in sustainable packaging technology, reducing plastic usage by 60%.

- January 2025: Sahara for Fruit Processing has launched a new facility in Egypt, boasting an annual capacity of 150,000 tonnes. The facility aims to produce citrus juice concentrates, catering to both domestic markets and exports to North Africa and the Middle East.

- December 2024: iPRO, a leader in healthy hydration, launched its New Healthy Juice Drink at Spinneys in the UAE. Staying committed to offering natural beverages, iPRO introduced three refreshing flavors – Orange and Mango Twist, Berry Mix, and Tropical Burst – designed to revitalize households across the UAE.

Middle-East And Africa Fruits And Vegetable Juice Market Report Scope

This market covers all still juices obtained from fruits and/or vegetables by mechanical processes, reconstituted, often including pulp or vegetable/fruit puree.

The Middle-East and Africa fruits and vegetable juice market is segmented by category, type, distribution channel, and geography. By category, the market is segmented into fruit juices and vegetable juices. By type, the market is segmented into nectar, still juice drinks, and 100% juice. By distribution channel, the market is segmented into supermarkets/hypermarkets, specialty stores, convenience stores, online retail stores, and other distribution channels. The market is studied for different countries across the region to provide a broader perspective, such as Saudi Arabia, South Africa, the Rest of the Middle-East and Africa. The report contains top-line revenues and market share analysis of the key players, highlighting the most adopted strategy of companies in the market. The report offers market size and forecasts in value (USD million) for the above-mentioned segments.

By Category

| Fruit Juice |

| Vegetable juice |

By Product Types

| 100% Juice |

| Nectar (25-99% Juice) |

| Juice Drinks ( Below 25% Juice) |

By Nature

| Conventional |

| Organic |

By Packaging Type

| Tetra Pak Cartons |

| PET Bottles |

| Glass Bottles |

| Cans |

| Pouches and Others |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience/Grocery Stores |

| Online Retail Stores |

| Other Distribution Channel |

By Geography

| United Arab Emirates |

| South Africa |

| Saudi Arabia |

| Nigeria |

| Egypt |

| Morocco |

| Turkey |

| Rest of Middle East and Africa |

| By Category | Fruit Juice |

| Vegetable juice | |

| By Product Types | 100% Juice |

| Nectar (25-99% Juice) | |

| Juice Drinks ( Below 25% Juice) | |

| By Nature | Conventional |

| Organic | |

| By Packaging Type | Tetra Pak Cartons |

| PET Bottles | |

| Glass Bottles | |

| Cans | |

| Pouches and Others | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Online Retail Stores | |

| Other Distribution Channel | |

| By Geography | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

Key Questions Answered in the Report

Which product type is growing fastest?

100% juice leads with a 6.15% CAGR through 2030, fueled by clean-label demand and supportive sugar-tax policies.

What is the main distribution channel?

Supermarkets and hypermarkets hold the largest share at 44.58%, yet online retail records the highest growth at 7.12% CAGR.

Which country offers the quickest growth?

Nigeria advances at a 6.38% CAGR because of urbanization and an expanding middle class.

How do sugar taxes influence category dynamics?

GCC excise levies elevate nectar prices, accelerating consumer migration to naturally sugar-containing 100% juice.

Page last updated on: