Chemicals & Materials

7th MayStrategic Expansion of Floor Coatings in the MEIA Region

4 Min Read

The Micronized PTFE Report is Segmented by Application (Inks and Coatings, Thermoplastics, Lubricants and Grease, and More), End-User Industry (Automotive and Transportation, Electrical and Electronics, Industrial Processing, Medical and Pharmaceutical, and Packaging), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

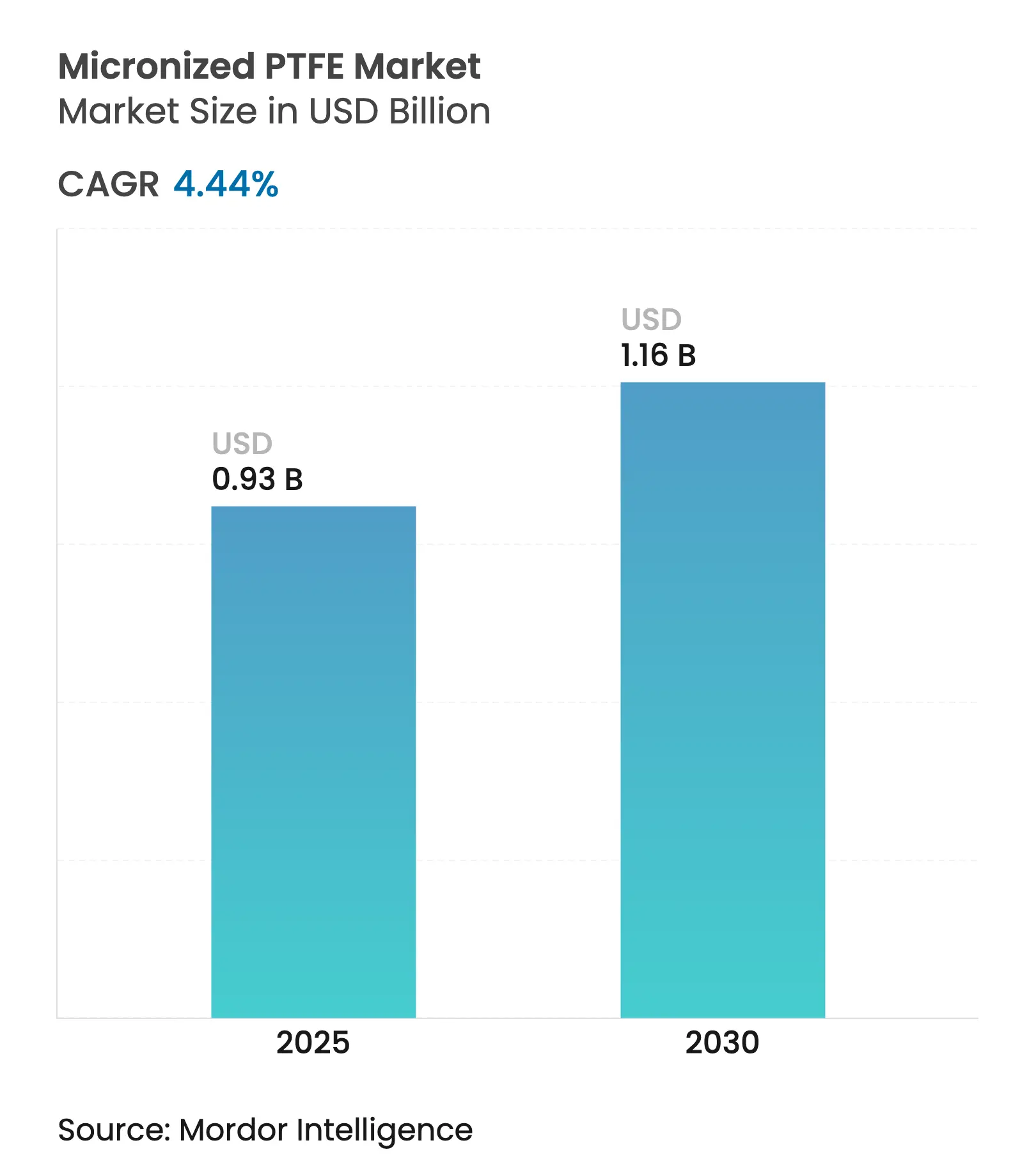

| Market Size (2025) | USD 0.93 Billion |

| Market Size (2030) | USD 1.16 Billion |

| Growth Rate (2025 - 2030) | 4.44 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The Micronized PTFE Market size is estimated at USD 0.93 billion in 2025, and is expected to reach USD 1.16 billion by 2030, at a CAGR of 4.44% during the forecast period (2025-2030). Market growth is underpinned by irreplaceable tribological and chemical-resistance properties that sustain demand in high-performance automotive, electronics, and semiconductor applications despite intensifying PFAS restrictions. Asia-Pacific’s production cost advantages, deep electronics supply chains, and accelerating electric-vehicle build-out keep the region at the forefront of global volume expansion. Meanwhile, rapid uptake of premium coatings, drivetrain lubricants, and additive-manufacturing modifiers underscores a shift away from commodity volumes toward value-added niches. Manufacturers that maintain end-to-end process control and invest in best-in-class emission-capture systems are best placed to navigate tightening compliance regimes while protecting margins.

Key Report Takeaways

Driver Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Surging demand for low-friction thermoplastics in

automotive and electronics

Surging demand for low-friction thermoplastics in

automotive and electronics

| +1.8% | Global (APAC and North America) | Medium term (2–4 years) |

(~) % Impact on CAGR Forecast

:

+1.8%

|

Geographic Relevance

:

Global (APAC and North America)

|

Impact Timeline

:

Medium term (2–4 years)

|

Rapid expansion of inks and industrial/packaging coatings

Rapid expansion of inks and industrial/packaging coatings

| +1.2% | APAC manufacturing hubs | Short term (≤ 2 years) | |||

Growing use in EV drivetrain lubricants and industrial

greases

Growing use in EV drivetrain lubricants and industrial

greases

| +0.8% | North America and EU, APAC scale-up | Long term (≥ 4 years) | |||

Rising adoption in elastomer seals and gaskets

Rising adoption in elastomer seals and gaskets

| +0.6% | Global industrial bases | Medium term (2–4 years) | |||

Increasing usage as additive-manufacturing rheology

modifier

Increasing usage as additive-manufacturing rheology

modifier

| +0.4% | North America and EU | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Surging Demand for Low-Friction Thermoplastics in Automotive and Electronics

Thermoplastic compounders are increasingly adding micronized PTFE to achieve ultra-low coefficients of friction, which help extend the range of electric vehicles and support the demands for semiconductor miniaturization. Automotive power-electronics housings now incorporate PTFE-modified PEEK or PPS blends that maintain dimensional stability at continuous service temperatures of up to 170 °C, thereby safeguarding inverter reliability. Precision electronic gears and slide mechanisms in lithography equipment use the same approach to mitigate particle generation in cleanrooms[1]Cleanroom Technology, “Air Filtration: Advantages of PTFE Materials,” cleanroomtechnology.com.

Rapid Expansion of Inks and Industrial/Packaging Coatings

Digital presses running at more than 300 m min⁻¹ require wax additives that minimise print-head drag; micronized PTFE fulfils this role by lowering surface energy without clouding transparency. Industrial floorings and metal packaging lines use PTFE-fortified coatings that cut maintenance intervals by up to 40%, aligning with lean manufacturing targets. Reformulated grades meet low-PFOA benchmarks, signalling industry willingness to invest in compliance over wholesale substitution.

Growing Use in EV Drivetrain Lubricants and Industrial Greases

PTFE-enhanced oils slash friction by 47% and extend component life by 62.7% in high-speed e-motors, according to laboratory tribometry data. The United States alone consumes 2.4 billion gallons of vehicle lubricants annually, offering a large conversion base toward PTFE-based formulations. Automation developers deploy similar greases in harmonic drives and ball screws to maintain accuracy under 24/7 duty cycles[2]MDPI Lubricants, “Forever Chemicals in Lubrication,” mdpi.com .

Rising Adoption in Elastomer Seals and Gaskets

Aggressive fluids and rising process temperatures force OEMs to shift from nitrile rubbers to PTFE-filled fluoro-elastomers. For example, Parker has validated PTFE micro-powders that double chemical resistance while retaining 300% elongation at break. Aerospace engine builders rely on these seals to suppress leakage at 500 °F service, avoiding costly in-flight maintenance.

Restraint Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Intensifying PFAS regulatory scrutiny and potential bans

Intensifying PFAS regulatory scrutiny and potential bans

| −0.9% | EU and North America leadership | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:

−0.9%

|

Geographic Relevance

:

EU and North America leadership

|

Impact Timeline

:

Short term (≤ 2 years)

|

Volatile TFE-monomer/fluorspar raw-material prices

Volatile TFE-monomer/fluorspar raw-material prices

| −0.5% | Global | Medium term (2–4 years) | |||

Substitution threat from bio-based/silicone micro-powders

Substitution threat from bio-based/silicone micro-powders

| −0.3% | EU leading adoption | Medium term (2–4 years) | |||

| Source: Mordor Intelligence | ||||||

Intensifying PFAS Regulatory Scrutiny and Potential Bans

The European Chemicals Agency’s proposal to restrict 10,000 PFAS chemistries would encapsulate most PTFE fine powders by 2026, allowing only “essential-use” derogations for aerospace, medical, and similar critical fields. Parallel United States rules designate PFOA/PFOS as CERCLA hazardous substances, exposing producers to remediation liabilities. Daikin has earmarked USD 300 million to raise wastewater capture efficiency to 99.9% and retain access to Western markets. Insurers such as Lloyd’s now embed PFAS exclusions in general liability policies, likening the risk profile to historical asbestos claims.

Volatile TFE-monomer/Fluorspar Raw-Material Prices

Geopolitical tensions and supply chain disruptions lead to fluctuations in the costs of tetrafluoroethylene monomer and fluorspar feedstock, putting pressure on margins. China's leading role in fluorspar production heightens supply risks. Additionally, the manufacturing of TFE is constrained to specialized facilities, which are limited in number worldwide. Such price volatility complicates long-term contract negotiations, pushing manufacturers to adopt dynamic pricing strategies. While these strategies can help navigate the market, they might also limit penetration in applications sensitive to price changes. Furthermore, the concentrated supply of these raw materials poses strategic challenges for Western manufacturers, who are increasingly prioritizing supply chain resilience and adherence to regulatory standards.

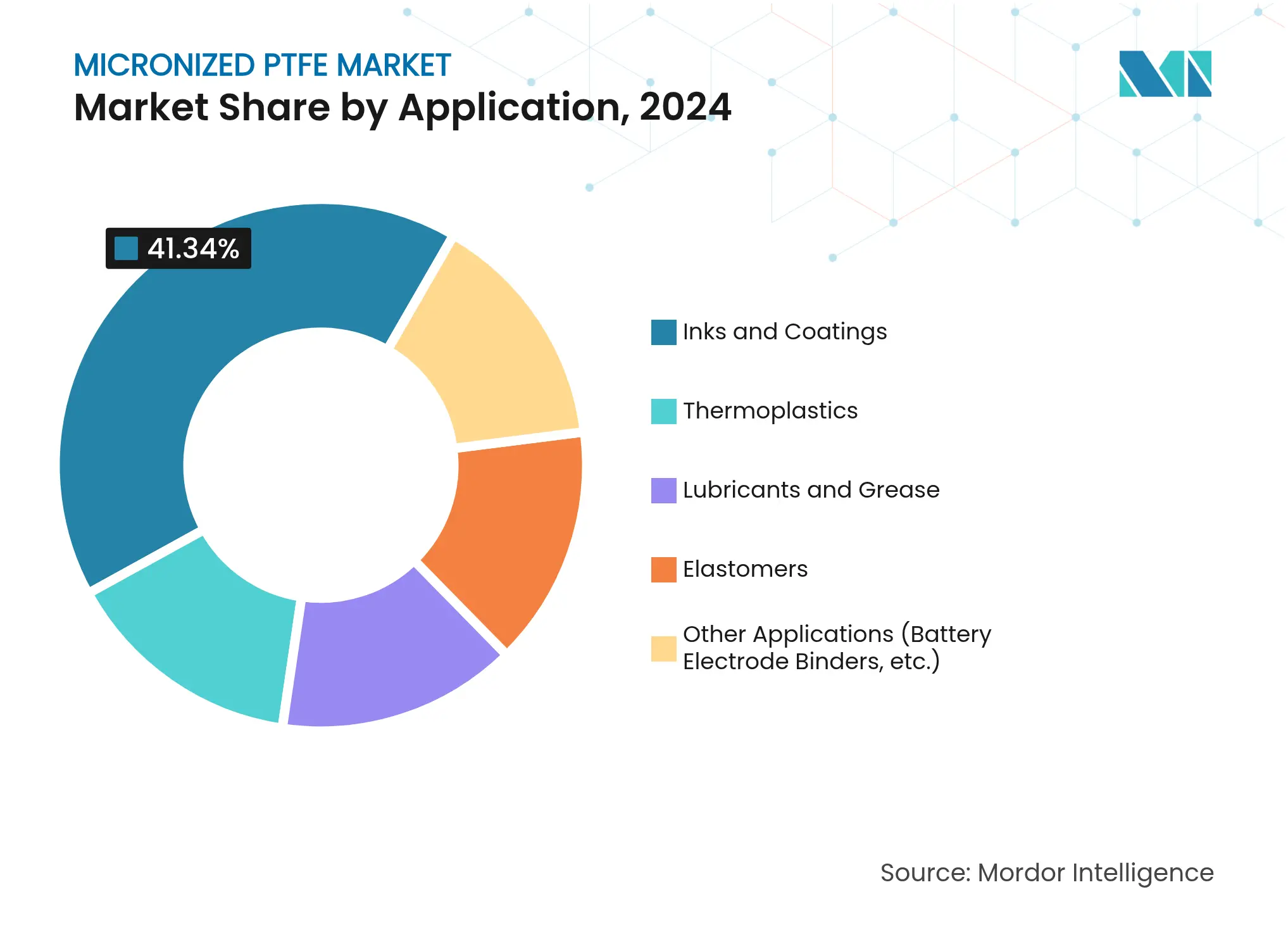

By Application: Inks and Coatings Lead Performance-Critical Segments

Inks and coatings held the largest 41.34% share of the micronized PTFE market in 2024. Lubricants and grease, although smaller at 21.27% of 2024 volume, capture the fastest 5.45% CAGR through 2030 as EV scale-up demands superior thermal and dielectric lubricant traits.

Thermoplastics represent a solid mid-tier, with polypropylene, PEEK, and PPS suppliers blending less than or equal to 5 wt% PTFE to achieve friction coefficients of less than 0.15 μ. The micronized PTFE market share for thermoplastics remains stable around underpinned by steady electronics demand. Elastomers rise as oil and gas upgrade exploration equipment to withstand sour-gas corrosion.

Note: Segment shares of all individual segments available upon report purchase

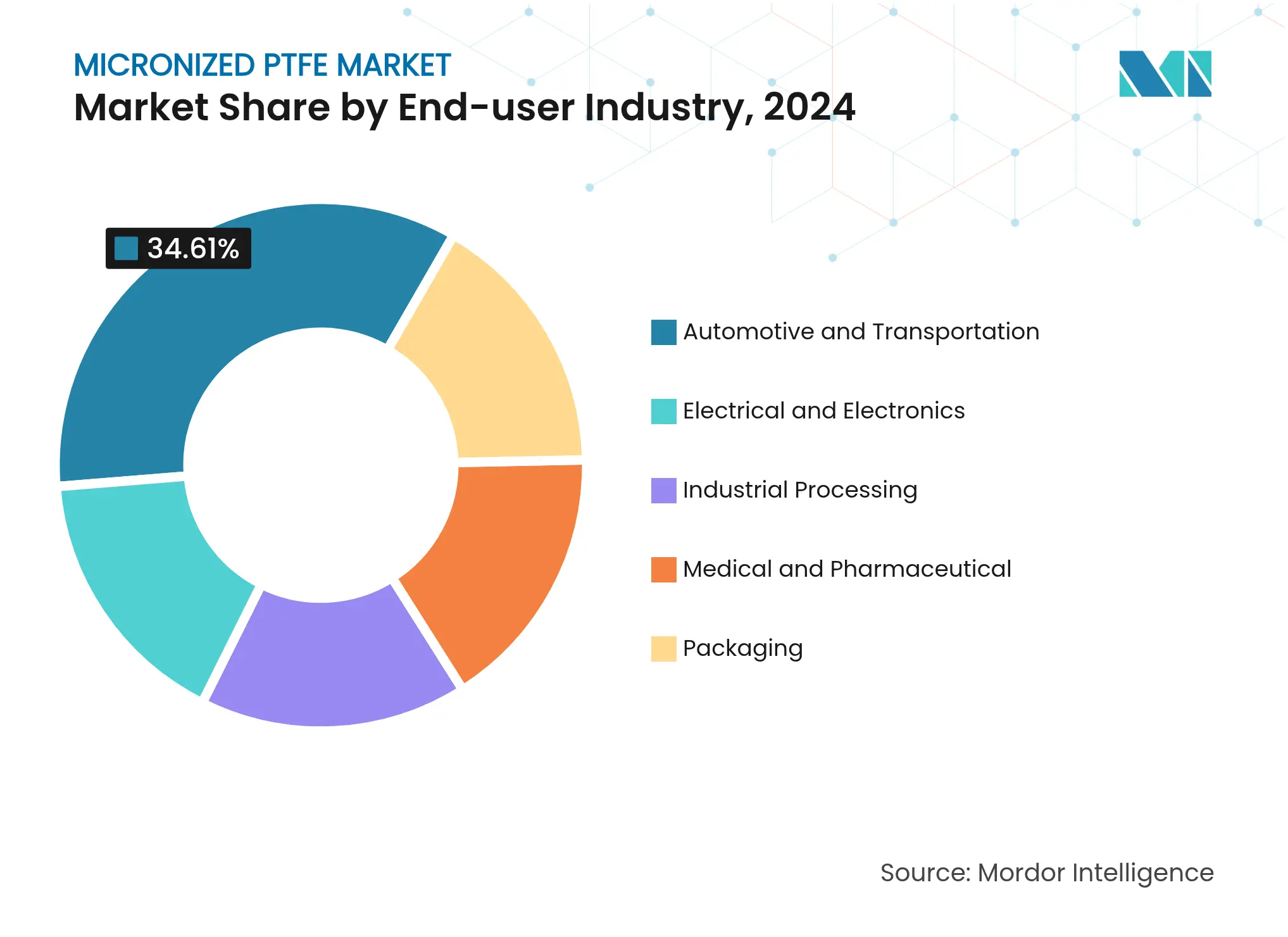

By End-user Industry: Automotive Drives Both Scale and Innovation

The automotive and transportation sector consumed 34.61% of the global volume in 2024. The segment’s 5.86% CAGR outpaces every other end-user group, lifting the micronized PTFE market size for automotive to USD 0.44 billion by 2030. EV makers specify PTFE-filled thermoplastics for battery pack thermal barriers and copper-foil spacers, while tier-one lubricant formulators lead the switch to fluorinated greases.

The electrical and electronics sector is buoyed by semiconductor fab expansions in Taiwan, South Korea, and the United States' CHIPS-Act corridor. Industrial processing leverages PTFE’s non-stick and chemical inertness in filtration plates and diaphragm pumps. Medical and pharmaceutical uses grow steadily on transplantable device coatings and drug-delivery matrices validated for biocompatibility. Packaging lags due to retailer pressure to move toward PFAS-free barriers, opening an avenue for bio-wax competitors.

Note: Segment shares of all individual segments available upon report purchase

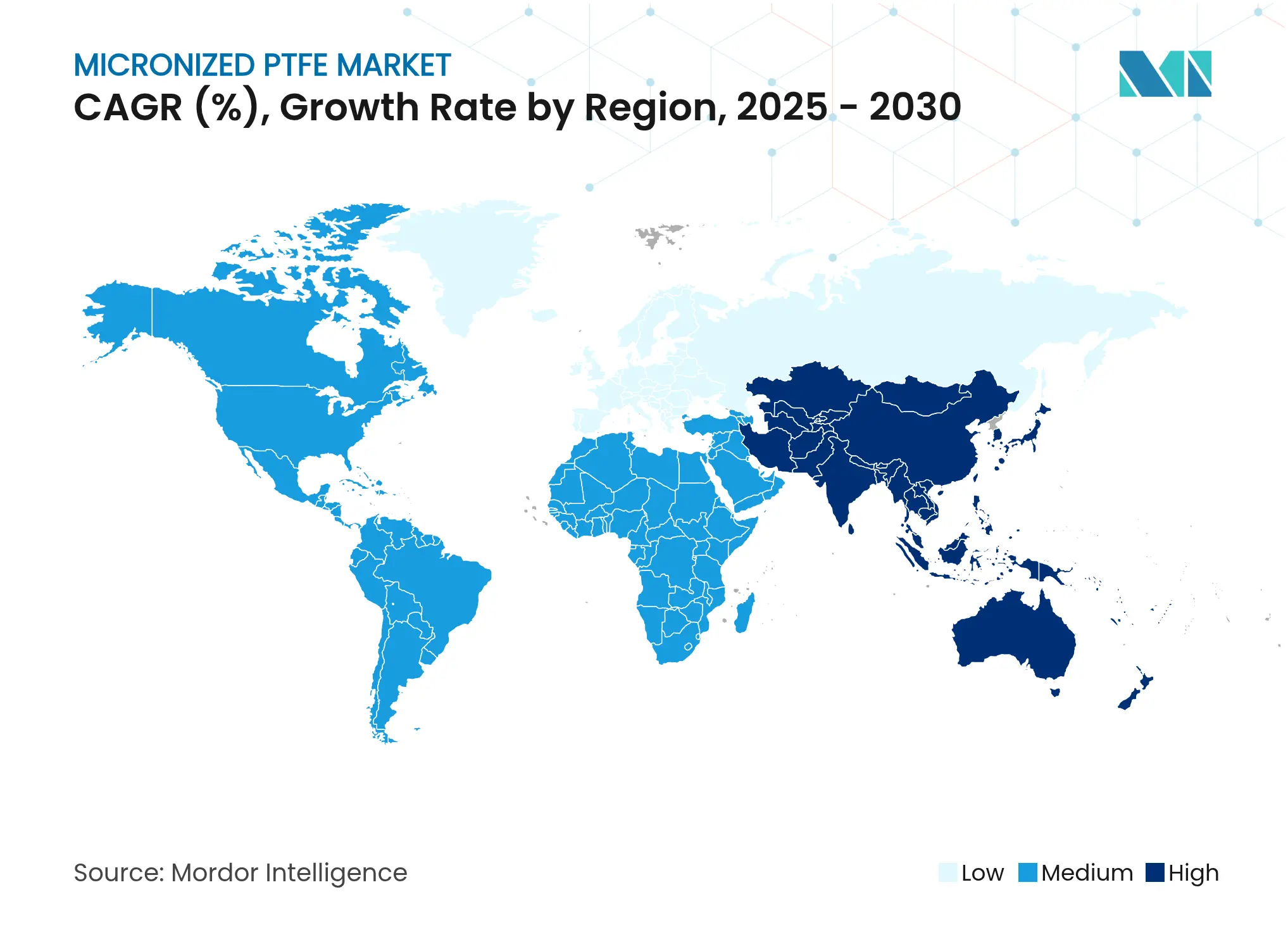

In 2024, the Asia-Pacific region accounted for 46.55% of the micronized PTFE market, with China, Japan, and South Korea collectively controlling 78% of the regional production capacity. The area posts a leading 5.61% CAGR. Government incentives for battery and semiconductor supply chains accelerate local consumption, while exporters benefit from relative cost advantages even after incorporating incremental PFAS-capture investments.

North America’s OEMs benefit from proximity and robust research and development ecosystems, which sustain price premiums. Europe follows but faces the steepest regulatory headwinds. Essential-use exemptions will likely shelter aerospace and medical demand, yet commodity coatings may migrate offshore. South America, the Middle East, and Africa are driven by demand centered on mining, energy, and infrastructure projects that favor durable, low-maintenance materials.

Market Concentration

The market is highly consolidated in nature. Daikin’s integrated fluorspar mining, TFE monomer production, and polymerization assets maintain resilient cost positions. Its USD 300 million wastewater abatement project underscores a strategy to stay ahead of compliance curves. Technologies differentiate themselves through proprietary micronization, which achieves a D50 of 4 μm, enabling optical-grade clarity in clear-coat lacquers. Market realignment is visible: Micro Powders will exit PTFE by the end of 2025, citing an inability to justify retrofitting legacy plants, which opens the market share for incumbents ready to supply compliant grades.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size and Growth Forecasts (Value)

6. Competitive Landscape

7. Market Opportunities and Future Outlook

The Micronized PTFE Market report includes:

Strategic Expansion of Floor Coatings in the MEIA Region

4 Min Read

Unlocking Supplier Partnerships in the Africa Lubricants Market

5 Min Read

Unlocking Saudi Arabia’s Regional Tourism Growth Potential

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.