Chemicals & Materials

7th MayStrategic Expansion of Floor Coatings in the MEIA Region

4 Min Read

The PTFE Fabric Market Report is Segmented by Type (PTFE-Coated Fabric, Non-Woven PTFE Fabric, PTFE Fiber-Made Fabric, and EPTFE Laminates), Application (Filtration, Heat-Sealing, Conveyor Belts, and Other Applications (Architectural Membranes, Etc. )) and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

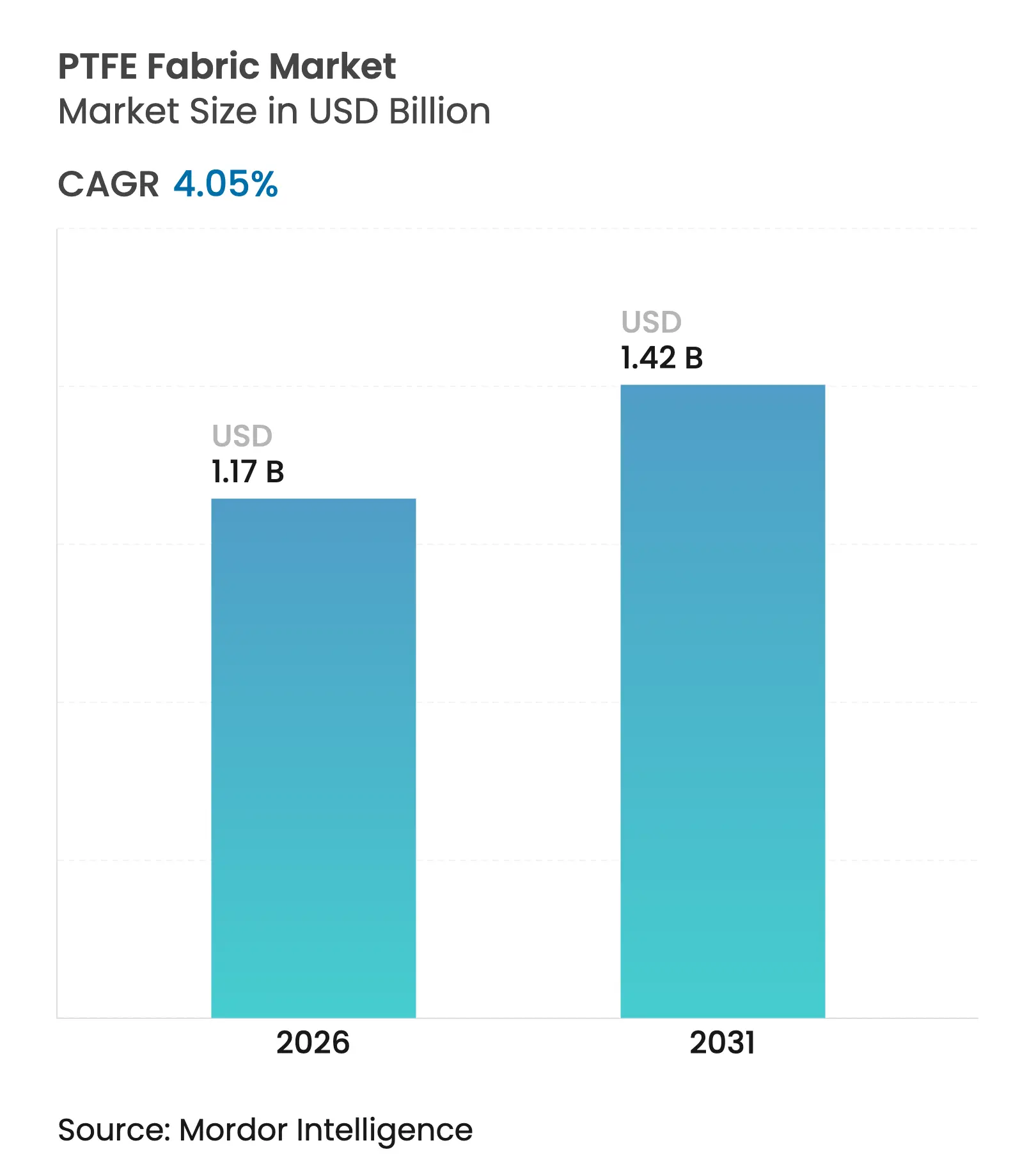

| Market Size (2026) | USD 1.17 Billion |

| Market Size (2031) | USD 1.42 Billion |

| Growth Rate (2026 - 2031) | 4.05 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

PTFE (polytetrafluoroethylene) Fabric Market size in 2026 is estimated at USD 1.17 billion, growing from 2025 value of USD 1.12 billion with 2031 projections showing USD 1.42 billion, growing at 4.05% CAGR over 2026-2031. This steady expansion reflects a market that is moving from rapid uptake to a more mature phase while still benefiting from recurring demand across critical industrial processes that require extreme chemical resistance and high-temperature stability. A principal growth driver is the installed base of filtration systems, where PTFE media can deliver 99.99% particle removal efficiency in Ultra Low Particulate Air (ULPA)-grade cleanroom and dust-collection retrofits. Buyers also value the fabric’s low friction and non-stick surface, which supports higher throughput in food packaging, textile printing, and precision electronics assembly. Vertical integration among leading resin suppliers has helped stabilize raw-material availability, even as Chinese fluorspar export controls tighten supply and elevate feedstock prices. On the demand side, ongoing electrification across automotive, consumer, and industrial sectors is encouraging new applications such as expanded Polytetrafluoroethylene (ePTFE) acoustic liners for battery casings and high-temperature wire insulation, broadening the scope of the PTFE Fabric Market.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rise in Industrial Dust Collection Retrofits Rise in Industrial Dust Collection Retrofits | +0.8% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+0.8%

|

Geographic Relevance

:

North America, Europe, Asia-Pacific

|

Impact Timeline

:

Medium term (2-4 years)

|

Expansion of Advanced Heating, Ventilation, and Air Conditioning (HVAC) Clean-room Projects Expansion of Advanced Heating, Ventilation, and Air Conditioning (HVAC) Clean-room Projects | +0.6% | Asia-Pacific core; spill-over to North America | Short term (≤ 2 years) | |||

Growing Demand for Non-stick Conveyor Belts in Food Packaging Growing Demand for Non-stick Conveyor Belts in Food Packaging | +0.5% | Global | Medium term (2-4 years) | |||

Adoption of Expanded Polytetrafluoroethylene (ePTFE) Acoustic Fabrics in Electric Vehicle (EV) Battery Casings Adoption of Expanded Polytetrafluoroethylene (ePTFE) Acoustic Fabrics in Electric Vehicle (EV) Battery Casings | +0.4% | Asia-Pacific and North America | Long term (≥ 4 years) | |||

Surge in Small-scale Solvent-free Textile Printing Lines Surge in Small-scale Solvent-free Textile Printing Lines | +0.3% | Europe and North America; global diffusion | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rise in Industrial Dust Collection Retrofits

Manufacturing plants are replacing legacy baghouses with PTFE-lined filter elements to meet stricter emission rules and to lower maintenance costs. Facilities handling cement, lime, and metal powders report 2–3 years filter-life extensions because PTFE fibers retain pore integrity above 200°C. New expanded Polytetrafluoroethylene (ePTFE) stretching techniques now limit in-service shrinkage to below 2% at 200°C, allowing stable differential pressure and energy savings over multiple cleaning cycles [1]T. Johnson, “High-Temperature Shrinkage Behaviour of ePTFE Felts,” Journal of The Textile Institute, textileinstitute.org. As regulators ratchet particulate limits below 5 mg/m³ stack gas, many operators are planning multiyear retrofits, supporting a healthy aftermarket for PTFE replacement fabrics. The retrofit opportunity is large because a high proportion of existing dust collectors in North America and Europe still run aramid or fiberglass media that struggle with weak acids and alkalis common in combustion exhaust.

Expansion of Advanced Heating, Ventilation, and Air Conditioning (HVAC) Clean-room Projects

Semiconductor fabs and injectable-drug plants demand stringent International Organization for Standardization (ISO) 3–ISO 5 air classes, pushing heating, ventilation, and air conditioning (HVAC) suppliers to specify PTFE laminar-flow filters with hydrophobic and low-outgassing properties. Compared with glass-fiber high efficiency particulate air (HEPA) mats, PTFE membranes demonstrate a 35% lower pressure drop at equivalent efficiency, cutting fan energy use and extending filter life. New fab corridors in China, Taiwan, and the United States that come online before 2027 will add an estimated 660 thousand m² of cleanroom space, translating into sizable first-fit volumes for PTFE filter rolls. Consumer-electronics brands are also integrating mini-cleanrooms inside assembly lines to minimize micro-scratches on high-resolution displays, a step that favors fine-fiber PTFE cartridges.

Growing Demand for Non-stick Conveyor Belts in Food Packaging

Continuous bake lines for snack foods, tortillas, and ready-meals increasingly specify PTFE-coated glass fabrics because the smooth surface eliminates release sprays and withstands repeated 260°C sanitizing cycles. Food and Drug Administration (FDA) compliance simplifies audits, while the material’s chemical inertness tolerates aggressive alkaline cleaners that manufacturers use to comply with zero-salmonella protocols. Case studies from packaging plants in the United States show that belt-change intervals doubled from six to twelve months after switching to PTFE-coated meshes, saving an estimated USD 80,000 in downtime per line. Adhesion-promoter advances now achieve bond strengths 30% higher than earlier generations, broadening installation on modular belt systems without risk of delamination.

Adoption of Expanded Polytetrafluoroethylene (ePTFE) Acoustic Fabrics in Electric Vehicle (EV) Battery Casings

Vehicle makers face strict noise, vibration, and harshness targets as the absence of an internal-combustion engine makes electric drivetrain sounds more noticeable. Expanded PTFE combines a microporous structure with high thermal tolerance to simultaneously damp sound and vent gas during thermal runaway events. Prototype packs using ePTFE liners survived 2,000 charge–discharge cycles at 70°C without pore collapse, maintaining less than 5 decibel (dB) noise-attenuation loss. Uptake began with premium European brands in 2024, yet Chinese OEMs now embed ePTFE vents in mainstream compact cars, accelerating volume demand in Asia-Pacific.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Volatile Polytetrafluoroethylene (PTFE) Resin Prices Tied to Fluorspar Supply Volatile Polytetrafluoroethylene (PTFE) Resin Prices Tied to Fluorspar Supply | -1.2% | Global; acute in North America and Europe | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:

-1.2%

|

Geographic Relevance

:

Global; acute in North America and Europe

|

Impact Timeline

:

Short term (≤ 2 years)

|

Competition From Aramid and Polyether Ether Ketone (PEEK) High-temp Fabrics Competition From Aramid and Polyether Ether Ketone (PEEK) High-temp Fabrics | -0.8% | Global; core industrial sectors | Medium term (2-4 years) | |||

Rising Carbon-tax Penalties on High-emission Sintering Furnaces Rising Carbon-tax Penalties on High-emission Sintering Furnaces | -0.4% | Europe and North America; emerging in Asia-Pacific | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Volatile Polytetrafluoroethylene (PTFE) Resin Prices Tied to Fluorspar Supply

China controls over 60% of mined fluorspar and has periodically capped exports to protect local downstream production. Acid-grade fluorspar arriving at United States ports averaged USD 450 per t in Q4 2024 versus USD 423 in Q2, adding direct cost pressure for Western PTFE resin plants [2]U.S. Geological Survey, “Mineral Commodity Summary: Fluorspar 2025,” usgs.gov. Mexican sources cover only 74% of the United States needs and lack volumes needed for sudden surges, so converters are exposed to price spikes whenever Chinese inspections truncate mine output. Resin producers such as DAIKIN INDUSTRIES, Ltd. and The Chemours Company have attempted multi-year offtake deals, yet contractual premiums still track spot volatility, forcing fabric coaters to adopt quarterly surcharges. Large buyers offset some risk through inventory hedging but small, specialty-fabric mills struggle to absorb rapid price shifts, creating uncertain margin outlooks for the PTFE fabric market.

Competition From Aramid and Polyether Ether Ketone (PEEK) High-temp Fabrics

Aramid and Polyether Ether Ketone (PEEK) suppliers pitch melt-processable or inherently strong fibers that match PTFE’s thermal window while offering superior abrasion resistance. PEEK belts, for instance, show 50% higher flexural strength after 1,000 heat-cool cycles at 260°C, making them attractive for continuous food frying lines. Aramid felts impregnated with silicone resist boiler chemicals and carry lower density, helping reduce filter-cage weight in large baghouses. End users are running side-by-side trials in aluminum smelters and turbine plants, and the early results are narrowing the performance gap that once insulated PTFE. A growing push to phase out certain PFAS compounds accelerates the shift because neither aramid nor PEEK relies on fluorinated chemistry.

By Type: Coated Fabrics Drive Traditional Applications

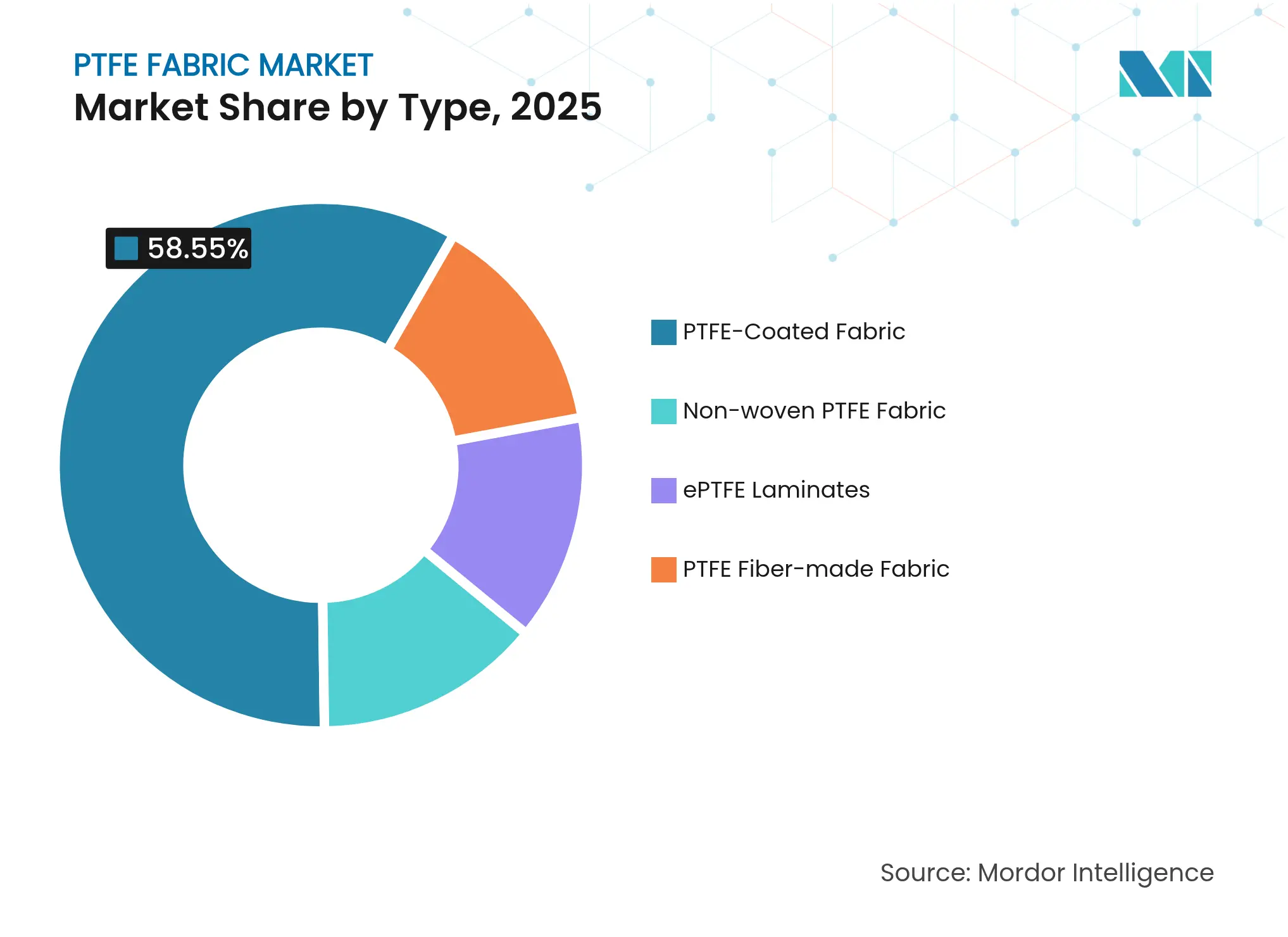

PTFE-coated fabric commanded 58.55% of the PTFE Fabric Market in 2025, underscoring the long-standing preference for glass-fiber substrates impregnated with fluoropolymer resin in filtration and release-liner duties. This dominant slice of the PTFE fabric market size is anchored in proven manufacturing lines that produce rolls up to 3.4 m wide for industrial baking belts and architectural tension structures. Fabricators report stable order books from legacy chemical processors, and the segment benefits from the continuous replacement cycle of baghouse socks that rarely exceed three-year service intervals. Market share may slip modestly as alternative substrates gain ground, yet installed capacity, wide global distribution, and price competitiveness give coated fabrics durable staying power.

Other Types, which include expanded Polytetrafluoroethylene (ePTFE) foams, biaxially stretched membranes, and specialty braid constructions, are on track for a 4.92% CAGR through 2031. This outperformance reflects niche but rapidly scaling uses in electric vehicle (EV) battery separators, cryogenic insulation wraps, and personal protective equipment where breathability and chemical inertness must coexist. Expanded PTFE vents form a microscopic lattice that releases gases while blocking water ingress, a property critical for lithium-ion cell safety. Suppliers expanding into these value-added niches can command margins 20–30% points above commodity coated fabrics, a factor that draws new entrants and pushes research and development (R&D) spending.

Note: Segment shares of all individual segments available upon report purchase

By Application: Filtration Leadership Faces Emerging Competition

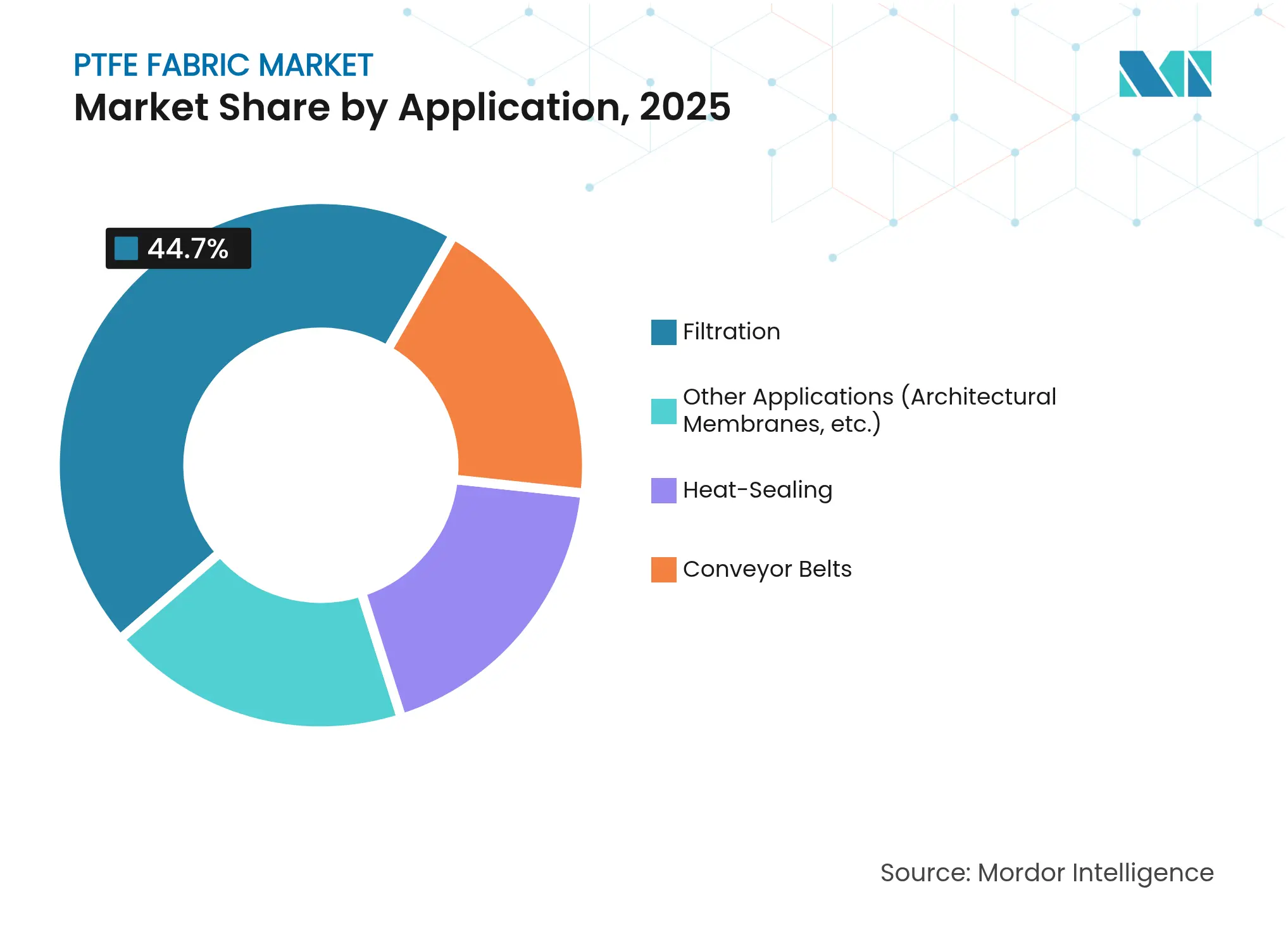

Filtration dominated 44.70% of the total 2025 market revenue, confirming that environmental compliance remains a linchpin for the PTFE fabric market. The PTFE fabric market size tied to filtration will keep rising as cement kilns, biomass boilers, and pharmaceutical dryers add tertiary air-quality controls. In baghouse retrofits, operators choose PTFE felts because they withstand persistent acid dew points and abrasive dust with minimal delamination risk.

Other Applications, although representing a smaller revenue base, clock the fastest 4.97% CAGR through 2031. Architectural membranes coated with high-light-transmission PTFE now appear in stadium roofs across Asia-Pacific, while medical device makers specify ePTFE vascular grafts that integrate fabric-like sleeves. Acoustic dampers inside EV battery modules, flexible printed circuits, and solvent-free textile press plates are further expanding the portfolio. These spaces reward suppliers that deliver precise porosity control, pushing the PTFE fabric market toward higher purity resins and tightly engineered microstructures.

Note: Segment shares of all individual segments available upon report purchase

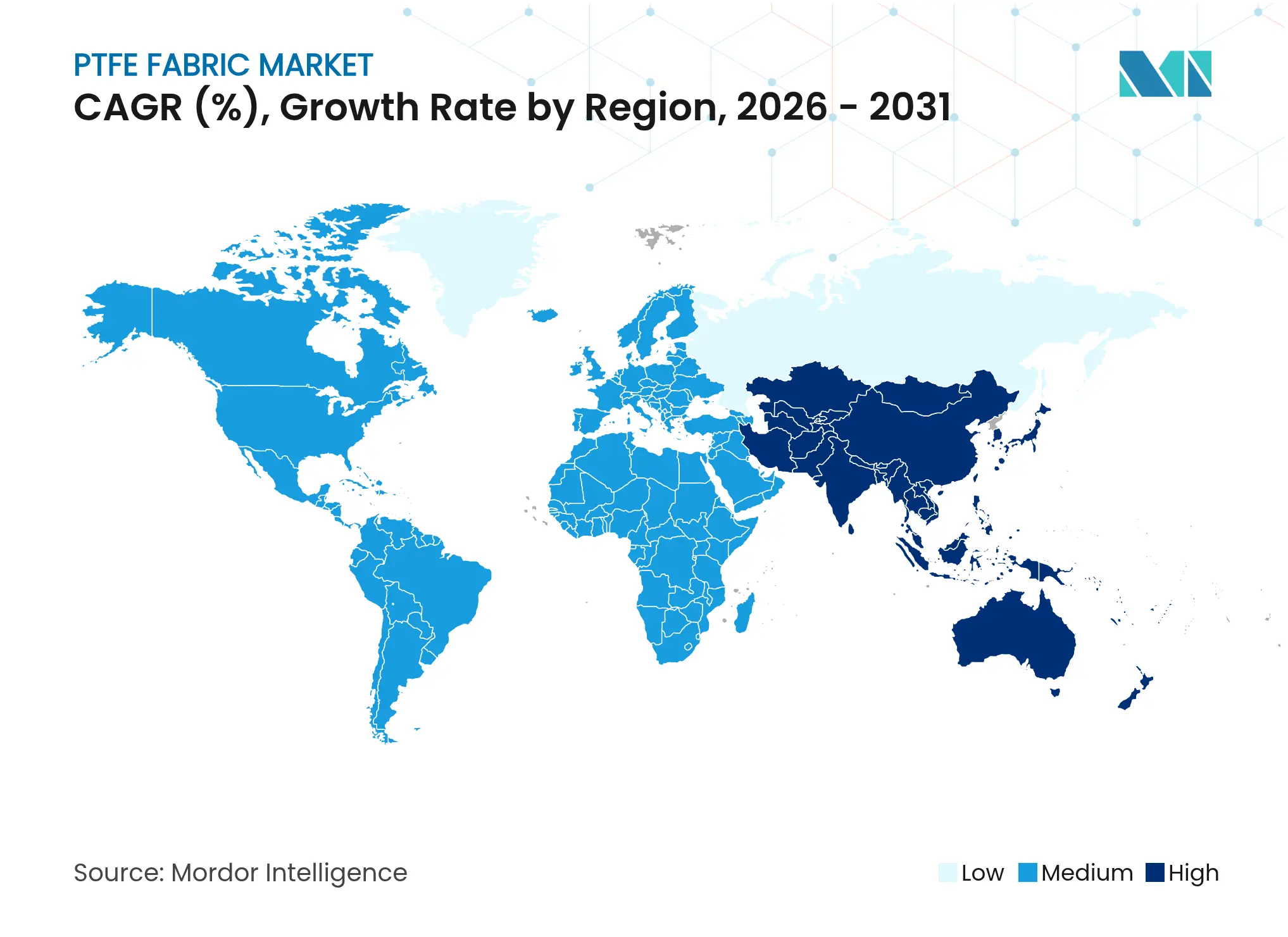

Asia-Pacific led the PTFE Fabric Market with 47.35% revenue share in 2025 and is pacing the field with a 4.75% CAGR to 2031. Strong integration from upstream fluorspar mining through downstream coating plants underpins cost advantages, particularly in China, which controls nearly the entire domestic supply chain. Japanese and Korean firms complement this dominance with high-precision ePTFE vents for electronics and battery casings, leveraging local high-tech clusters. The region also enjoys robust infrastructure spending, spurring demand for PTFE expansion joints and architectural fabrics. Ongoing regulatory scrutiny of per- and polyfluoroalkyl substances (PFAS) is beginning to shape product portfolios, but government grants for advanced-material exports help offset the compliance burden, keeping Asian converters competitive.

North America occupies the second-largest share of the PTFE fabric market, supported by stringent Occupational Safety and Health Administration limits that fuel demand for ultra-low particulate air (ULPA)-grade dust-collection sleeves and cleanroom consumables. Semiconductor expansions in Arizona, Texas, and New York will maintain strong order flow for large-surface PTFE filtration panels needed in Class 100 or better areas. Mexico’s position as a dominant United States fluorspar supplier brings strategic security, though recent droughts and rail bottlenecks have highlighted logistic vulnerabilities and drove spot-freight premiums to 30-year highs in 2024. Resin producers in Louisiana and Kentucky are studying onsite Hydrogen Fluoride (HF) plants to reduce external dependencies, a step expected to secure long-term resin supply for downstream fabric coaters.

Europe ranks third, yet its growth outlook is tempered by evolving PFAS restrictions that could narrow allowable use cases for PTFE except in vital applications such as medical implants and aerospace seals. Producers contend with rising carbon charges on gas-fired sintering ovens, prompting a pivot toward recycled PTFE powder or hybrid laminates that reduce fluoropolymer mass without sacrificing performance. Pilot recycling projects in Germany and Sweden have demonstrated 80% resin recovery through mechanical shredding and re-sintering, fostering a localized circular economy. South America and the Middle East & Africa remain comparatively small, but infrastructure modernization and emerging pharmaceutical hubs in Brazil, Saudi Arabia, and Egypt offer sites for first-wave adoption of PTFE filter fabrics. Limited domestic coating capacity in these regions means imports account for more than 70% of supply, a situation that could shift when Asian suppliers begin to localize cut-and-sew operations nearer to end users.

Market Concentration

The PTFE Fabric Market is moderately consolidated, with the major players such as W. L. Gore & Associates, Inc., Saint-Gobain, DAIKIN INDUSTRIES, Ltd., Taconic, and 3M accounting for a major portion of the overall market revenue. 3M, Saint-Gobain, and DAIKIN INDUSTRIES, Ltd. wield scale advantages in upstream resin production and often secure long-term fluorspar contracts that shield them from abrupt spot-market shocks. Their vertical integration extends to captive sintering and coating lines, allowing tighter process control and consistent surface energy, which is crucial for demanding ULPA filter builds. Mid-tier players such as W.L. Gore & Associates emphasize differentiated ePTFE membranes and acoustic fabrics that fetch premium margins in automotive and electronics channels.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size and Growth Forecasts (Value)

6. Competitive Landscape

7. Market Opportunities and Future Outlook

The PTFE Fabric market report include:

Strategic Expansion of Floor Coatings in the MEIA Region

4 Min Read

Unlocking Supplier Partnerships in the Africa Lubricants Market

5 Min Read

Unlocking Growth in India’s Luxury Beauty & Skincare Market

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.