Ethylene Tetrafluoroethylene (ETFE) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 567.16 Million |

| Market Size (2031) | USD 802.29 Million |

| Growth Rate (2026 - 2031) | 7.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ethylene Tetrafluoroethylene (ETFE) Market Analysis by Mordor Intelligence

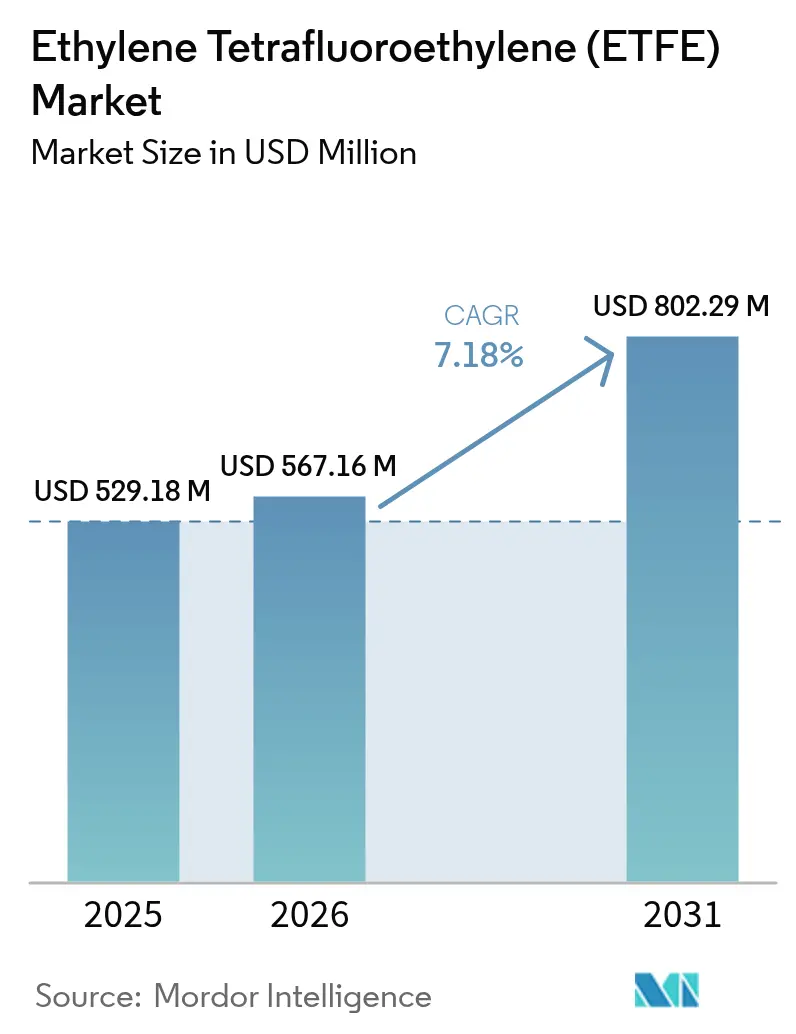

The Ethylene Tetrafluoroethylene Market size was valued at USD 529.18 Million in 2025 and estimated to grow from USD 567.16 Million in 2026 to reach USD 802.29 Million by 2031, at a CAGR of 7.18% during the forecast period (2026-2031). Architectural membranes, aerospace wiring, and transparent photovoltaic laminates are the principal growth engines, as the material’s clarity, chemical inertness, and tensile strength outperform conventional glass and polymer alternatives. Stadium roofing projects across North America and Europe continue to showcase ETFE’s weight savings and daylighting advantages, while airlines and Electric Vertical Take-off and Landing (eVTOL) manufacturers specify ETFE-insulated cables to withstand thermal cycling and hydraulic-fluid exposure. Solar module producers are deploying transparent ETFE laminates that preserve façade aesthetics and convert sunlight into power, expanding the ETFE market into building-integrated photovoltaics. Regional production capacity additions in Asia-Pacific underpin supply security, although Per- and polyfluoroalkyl substances (PFAS) regulations in Europe and North America could redirect investment toward greener chemistries and localized value chains.

Key Report Takeaways

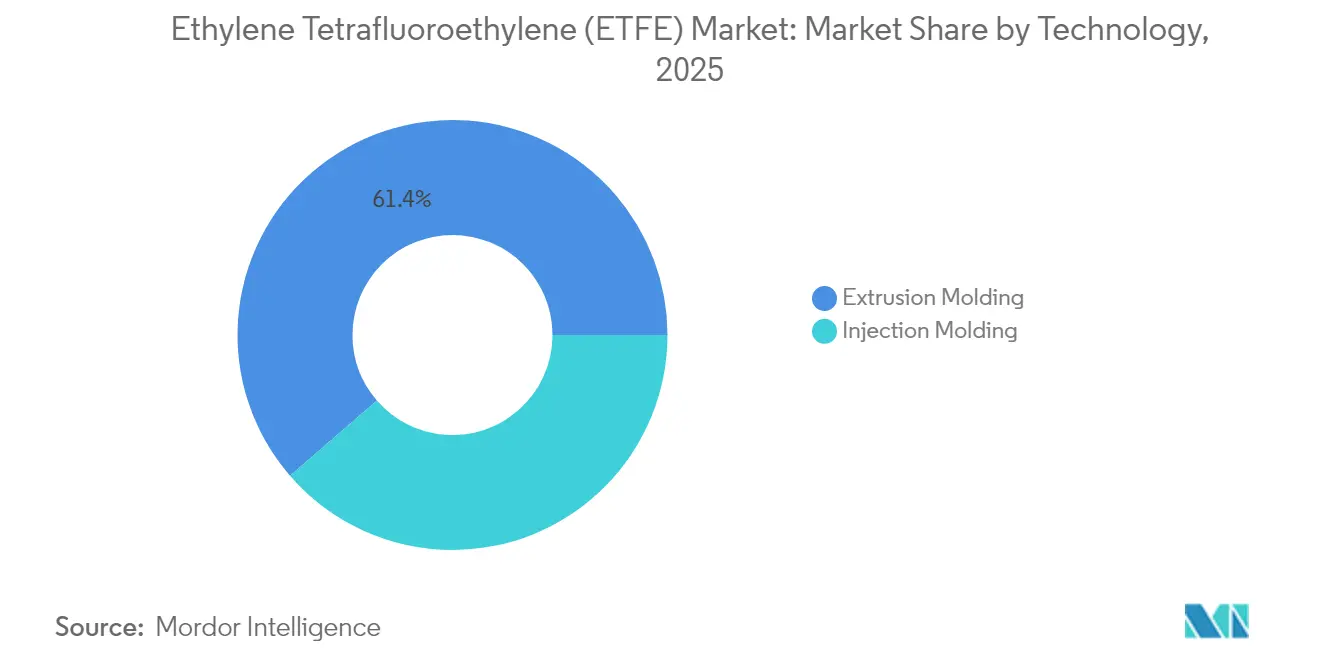

- By technology, extrusion molding captured 61.36% Ethylene Tetrafluoroethylene (ETFE) market share in 2025, whereas injection molding is projected to log an 7.96% CAGR through 2031.

- By product type, granules held 55.62% of the Ethylene Tetrafluoroethylene (ETFE) market size in 2025, while powders are forecast to post an 8.41% CAGR to 2031.

- By application, film and sheet commanded 49.35% revenue in 2025, yet wire and cable is set to advance at a 8.86% CAGR over 2026-2031.

- By end-use industry, buildings and construction led with 42.10% share of the Ethylene Tetrafluoroethylene (ETFE) market size in 2025; solar photovoltaics is poised for the fastest 8.98% CAGR to 2031.

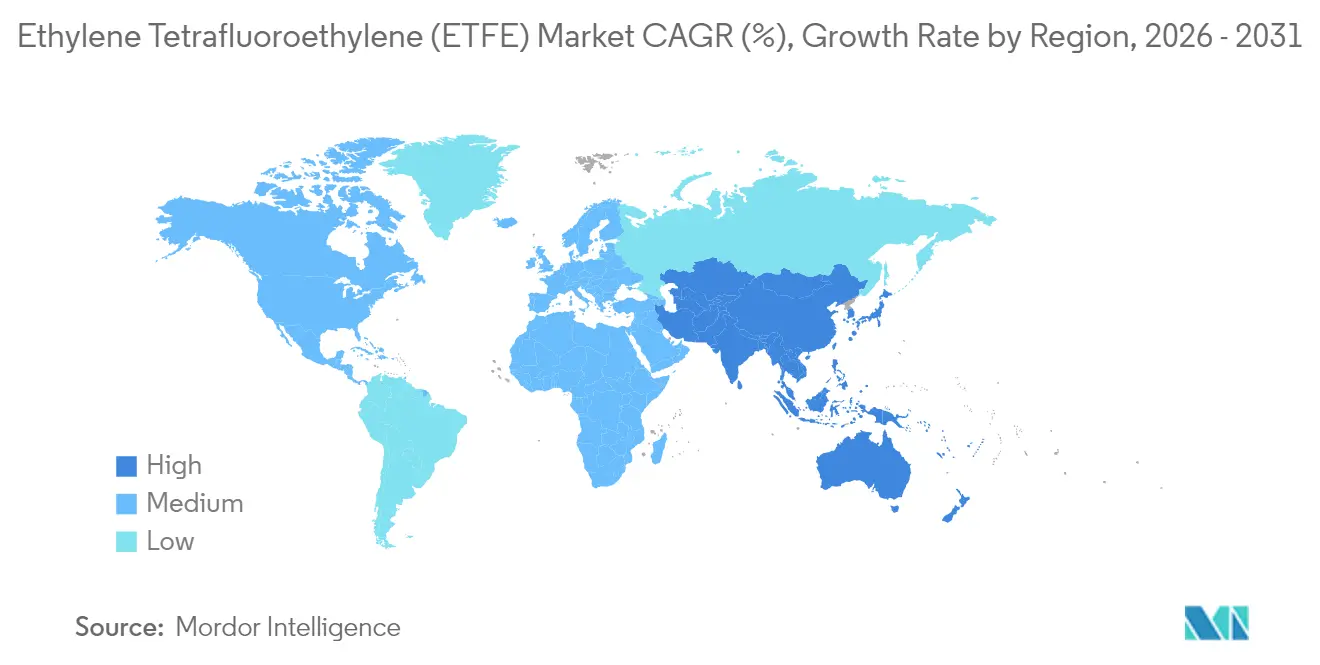

- By geography, Asia-Pacific generated 46.90% of 2025 revenue and is expanding at an 8.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ethylene Tetrafluoroethylene (ETFE) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Gaining Popularity as Roof-cover Material for Stadium-type Structures | +1.8% | Global, early gains in North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Rising Demand for Ethylene Tetrafluoroethylene (ETFE) Cables in Aerospace Wiring | +1.5% | North America & Europe core, spill-over to Asia-Pacific | Long term (≥ 4 years) |

| Light-weight, Durable Facades Replacing Conventional Glass | +1.2% | Global, concentrated in urban construction | Medium term (2-4 years) |

| Emergence of Transparent Ethylene Tetrafluoroethylene (ETFE) Photovoltaic Laminates | +0.9% | Europe & Asia-Pacific, expanding to North America | Long term (≥ 4 years) |

| Chemical-resistant Tubing Demand in Renewable Aviation-fuel Plants | +0.7% | North America & Europe, Asia-Pacific following | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Gaining Popularity as Roof-cover Material for Stadium-type Structures

Stadium architects are increasingly specifying ETFE roofing systems because they deliver natural lighting while eliminating the structural weight penalties of traditional glass canopies. The Intuit Dome's 277,000 square foot diagrid roof structure incorporates clear ETFE membranes that allow natural airflow, eliminating air conditioning requirements in certain areas while achieving Leadership in Energy and Environmental Design (LEED) Platinum certification. The material's self-extinguishing properties address fire safety concerns that have historically limited membrane adoption in high-occupancy venues. Beyond functionality, ETFE's ability to scatter sunlight prevents greenhouse effects while maintaining 95% daylight transmission, creating optimal playing conditions that traditional roofing cannot match. This trend is accelerating as venue operators recognize ETFE's long-term cost advantages, with maintenance requirements limited to cleaning every 2-3 years compared to frequent glass panel replacements.

Rising Demand for Ethylene Tetrafluoroethylene (ETFE) Cables in Aerospace Wiring

Aerospace manufacturers are expanding ETFE cable adoption because the material withstands extreme temperature cycles and chemical exposure that would degrade conventional insulation materials. The 2025 Aerospace and Defense Industry Outlook projects 11.6% growth in global air passenger traffic, with defense spending surpassing USD 2.4 Trillion, creating sustained demand for high-performance wiring solutions. ETFE's resistance to hydraulic fluids and thermal stability make it essential for next-generation aircraft systems, particularly in electric vertical takeoff and landing (eVTOL) aircraft where weight reduction is critical. Military applications drive premium pricing, as ETFE cables meet stringent specifications for combat aircraft and spacecraft thermal control surfaces. The shift toward more electric aircraft architectures is expanding ETFE's role beyond traditional wiring to power management systems, where its thermal stability enables higher current densities without insulation failure.

Light-weight, Durable Facades Replacing Conventional Glass

Building designers are specifying ETFE facades because they achieve transparency goals while reducing structural loads by 95% compared to equivalent glass installations. The material's R-value is three times higher than glass, enabling superior thermal performance that reduces Heating, Ventilation, and Air Conditioning (HVAC) energy consumption while maintaining natural lighting. ETFE's Ultraviolet (UV) transmission can be precisely controlled through printing technologies, allowing architects to customize solar heat gain without compromising visibility. The material's acoustic transparency reduces reverberation in large spaces, creating better interior environments than traditional glass curtain walls. Maintenance advantages are substantial, with ETFE's self-cleaning properties and 50-year lifespan unaffected by Ultraviolet (UV) exposure or urban pollution. The emergence of STFE (Structural Transparent Fluorinated Envelope) by Serge Ferrari Group represents a technological evolution, offering 50% light transmission while being ten times lighter than glass and enabling expansive applications beyond ETFE's traditional pneumatic module limitations.

Emergence of Transparent Ethylene Tetrafluoroethylene (ETFE) Photovoltaic Laminates

Solar panel manufacturers are integrating ETFE laminates because they enable building-integrated photovoltaics that maintain architectural aesthetics while generating clean energy. Research on transparent spectral selective photovoltaics demonstrates that ETFE-based systems can achieve high average visible transmittance while maintaining power conversion efficiency, making them suitable for agrivoltaic applications where crop growth and energy generation must coexist. The material's weatherability ensures long-term performance in outdoor installations, with Daikin's NEOFLON ETFE series specifically designed for roofing membranes and greenhouse films due to its UV resistance. ETFE's optical clarity enables efficient light transmission to underlying photovoltaic cells while protecting them from environmental degradation. The development of luminescent solar concentrators using ETFE substrates allows for color-neutral transparency with 92% average visible transmittance while absorbing 60-90% of harmful UV radiation [1]Journal of Materials Chemistry A, “Transparent Spectral Selective Photovoltaics,” rsc.org. This technology is particularly valuable for architectural applications where traditional opaque solar panels would compromise building aesthetics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental Concerns and Stricter Per- and Polyfluoroalkyl Substances (PFAS)/fluoropolymer Regulations | –2.1% | Europe core, spreading to North America & Asia-Pacific | Short term (≤ 2 years) |

| Fire-safety Scrutiny on Single-skin Ethylene Tetrafluoroethylene (ETFE) Cushions | –1.3% | Global, heightened in Europe post-Grenfell | Medium term (2-4 years) |

| Limited Global Ethylene Tetrafluoroethylene (ETFE)-resin Capacity | –0.8% | Concentrated in Asia-Pacific production centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Environmental Concerns and Stricter Per- and Polyfluoroalkyl Substances (PFAS)/Fluoropolymer Regulations

The European Union's proposed Per- and Polyfluoroalkyl Substances (PFAS) restrictions could ban over 10,000 substances, including ETFE, in concentrations exceeding specified limits, with implementation timelines extending to 2029. This regulatory pressure is forcing manufacturers to develop PFAS management strategies, including supply chain audits and sourcing alternatives, though suitable replacements often underperform or carry higher costs. Daikin has responded by investing over USD 300 Million to capture PFAS emissions, targeting a 99.9% capture rate in process water discharges while transitioning to sustainable manufacturing technologies by 2030. The European Environment Agency emphasizes that PFAS polymers constitute 24-40% of total PFAS volume in European Union (EU) markets, with their persistence and potential toxicity creating pollution throughout their lifecycle from production to disposal. The regulatory fragmentation between Europe's centralized approach and the United States' (US) state-by-state restrictions creates compliance complexities that increase operational costs and limit market access for ETFE products.

Fire-safety Scrutiny on Single-skin Ethylene Tetrafluoroethylene (ETFE) Cushions

Building safety regulators are intensifying scrutiny of single-skin ETFE installations following the Grenfell Tower inquiry, which highlighted systemic failures in building safety and the need for robust fire protection measures [2]UK Parliament, “Grenfell Tower Inquiry Progress Report,” parliament.uk. The pace of unsafe cladding remediation has been slower than expected, with many buildings still requiring safety upgrades, creating uncertainty around membrane material approvals. Manufacturers are responding by developing enhanced fire-resistant formulations and multi-layer cushion systems that provide backup protection if primary barriers fail. The regulatory emphasis on personal evacuation plans for vulnerable residents and robust enforcement of building safety standards is driving more conservative material selection, favoring proven technologies over innovative solutions. This scrutiny is particularly acute in high-occupancy buildings like stadiums and airports, where ETFE's lightweight advantages must be balanced against comprehensive fire safety protocols that may require additional protective measures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Extrusion Dominates Processing Methods

Extrusion molding generated 61.36% of 2025 revenue, highlighting its efficiency for continuous films, sheets, and wire coatings. The ETFE market size for extrusion-grade products is set to grow steadily alongside stadium and greenhouse projects. Injection molding’s 7.96% CAGR reflects rising demand for precision parts such as complex cable connectors and semiconductor chamber components. Hybrid machines capable of both extrusion and injection are gaining traction as converters aim to serve niche aerospace and electronics orders without multiple capital assets.

Optimized resin grades like NEOFLON ETFE-TX strengthen tensile performance for both processes, enabling thinner walls and lower part weight without sacrificing durability. Processing-equipment makers are introducing screw geometries and hot-runner systems tailored to ETFE’s high melt temperature, helping processors avoid degradation and surface defects.

By Product Type: Granules Lead Material Formats

Granules accounted for 55.62% of the 2025 market value share because pelletized form assures consistent flow during extrusion and injection. Wire & cable producers favor granules for precise metering that minimizes dielectric defects. Powder grades, expanding at 8.41% CAGR, cater to spray-coating and additive-manufacturing uses where thin, uniform layers are mandatory. The ETFE market share for powders will rise as aerospace primes qualify powder-bed fusion and cold-spray repairs.

Manufacturers are blending nano-fillers into powder grades to raise surface hardness for process piping and fuel plants. Hybrid formats, micro-granules and high-bulk-density powders bridge the gap between conventional pellets and ultrafine particles, giving converters flexibility to switch between extrusion and coating lines with minimal changeovers.

By Application: Film and Sheet Applications Drive Demand

Film and sheet accounted for 49.35% of the 2025 market demand as roof membranes, façade cushions, and greenhouse covers dominate volume. The ETFE market size for films will remain anchored by marquee sports facilities and transparent Building-Integrated Photovoltaic (BIPV) façades. Wire and cable, the fastest-growing application at 8.86% CAGR, leverages ETFE’s dielectric strength and resistance to Skydrol and JP-8 fuels, opening premium revenue streams in defense and Electric Vertical Take-Off and Landing (eVTOL) fleets.

Coating applications continue to evolve, with powder overlays under 150 micrometer (µm) thick extending asset life in acid plants and seawater desalination. Tubing supports renewable aviation-fuel processing where corrosion resistance and visual inspection capability cut downtime. Additive-manufactured ETFE prototypes in semiconductor tools suggest a pipeline for bespoke, low-volume components.

By End-use Industry: Buildings and Construction Leads Market

Buildings and construction held a 42.10% market share in 2025 as architects exploit ETFE’s daylighting and weight savings to achieve net-zero energy targets. Wire-embedded ETFE cushions integrate Light Emitting Diodes (LEDs) and sensors, transforming façades into dynamic media skins. Solar photovoltaics, growing at 8.98% CAGR, benefits from transparent laminates that merge energy harvesting with aesthetics, pushing the ETFE market into carbon-neutral real-estate projects.

Aerospace and defense adopt ETFE for wiring harnesses and radomes, where weight savings convert directly to fuel burn reductions. Electric-vehicle makers use ETFE high-voltage cable jackets to meet thermal limits in compact power-electronics bays. Chemical processors specify ETFE linings to counter acids and solvents that shorten steel and Polytetrafluoroethylene (PTFE) service lives.

Geography Analysis

Asia-Pacific generated 46.90% of global market revenue in 2025 and is advancing at an 8.54% CAGR through 2031, benefiting from China’s expanding ethylene capacity and Japan’s expertise in high-purity fluoropolymers. Government-backed stadium and high-speed-rail stations frequently adopt ETFE roofs, reinforcing regional construction pull. Local converters scale powder-coating lines to serve semiconductor fabs and lithium-battery plants, deepening domestic value capture.

North America remains a prime consumer as National Football League (NFL) and Major League Soccer venues adopt ETFE membranes that deliver clear sightlines and year-round turf protection Axios. The aerospace cluster from Washington State to Quebec drives wire-insulation demand, while renewable-fuel refineries along the Gulf Coast integrate ETFE tubing for corrosion control. Regional clean-energy incentives funnel capital toward Building-Integrated Photovoltaics (BIPV) façades that capitalize on ETFE’s optical properties.

Europe grapples with PFAS regulation but still embraces ETFE for iconic structures and offshore wind farm cables. German carmakers deploy ETFE wire harnesses in 800-V drivetrains, whereas Nordic countries integrate ETFE-laminated agrivoltaic roofs across greenhouses to stretch production seasons under limited sunlight. Ethylene rationalization tightens supply, yet specialty ETFE grades retain pricing power.

South America and the Middle East & Africa remain nascent, yet stadium upgrades for upcoming tournaments and airport expansions are beginning to spec ETFE façades. Local resin shortages prompt imports, but regional engineering firms partner with established suppliers to accelerate technology transfer and installation expertise.

Regulatory Landscape

ETFE sits within the broader fluoropolymer and PFAS policy debate, with the European Chemicals Agency (ECHA) progressing the EU-wide REACH restriction proposal for PFAS. This has created compliance uncertainty for fluoropolymers used in construction membranes, wire and cable, and industrial linings. Industry bodies have been pushing for differentiated treatment of fluoropolymers: the European Sealing Association highlighted an ITRE Committee study in February 2026 calling for a risk-based approach, and the UK Environmental Audit Committee published a report in April 2026 that acknowledged the role of fluoropolymers in advanced manufacturing while advocating group-based regulation.

In the United States, ETFE use cases that touch food contact are governed under FDA frameworks for food-contact materials, with 21 CFR 177.1550 commonly referenced for perfluorocarbon resin compliance pathways. Separately, Regulation (EU) 2024/573 (effective February 2024) on fluorinated greenhouse gases tightens containment and recovery requirements across parts of the fluorinated materials value chain. The EU also published a voluntary Safe and Sustainable by Design (SSbD) methodology in the Official Journal in 2026, reinforcing lifecycle-based scrutiny even where formal restrictions are not yet finalized.

Value Chain Analysis

The ETFE value chain starts with upstream fluorochemical feedstocks and the production of tetrafluoroethylene (TFE) monomer, followed by copolymerization of TFE with ethylene to produce ETFE resin. Industrial production commonly uses pressurized polymerization, then coagulation (often using salts such as calcium chloride, magnesium sulfate, or aluminum sulfate), washing, drying, and pelletization to deliver commercial forms (granules and powders) that align with extrusion and injection molding requirements.

Integrated fluoropolymer producers such as AGC Inc. (Fluon), The Chemours Company (Tefzel), and Daikin Industries (Neoflon) supply base resins and application-engineered grades. Specialized processors and fabricators, including Zeus Company for tubing and profiles, convert resins into films, sheets, wire coatings, and industrial components that pass through distributors and project-based installers in building-envelope applications. Bottlenecks center on resin availability and qualification cycles for high-spec end uses such as aerospace wiring, semicon, and chemical processing, while downstream value capture increases when converters provide compounding, tight impurity control, and fabrication or installation services for architectural membrane systems.

Competitive Landscape

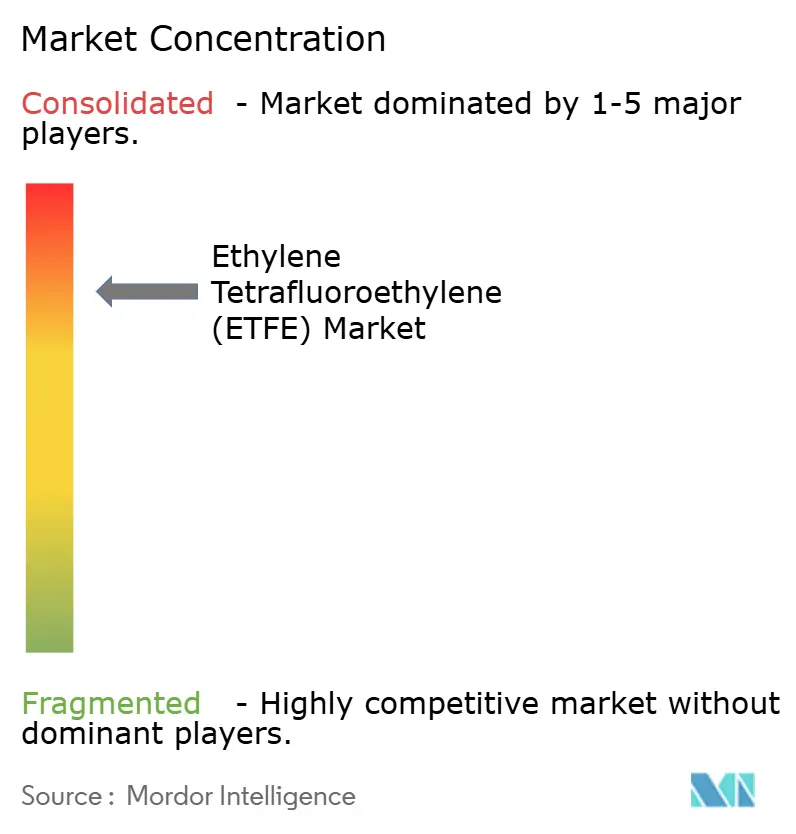

The Ethylene Tetrafluoroethylene (ETFE) market is concentrated, with the global supply concentrated among integrated fluoropolymer producers, including The Chemours Company, DAIKIN INDUSTRIES, Ltd., 3M, Saint-Gobain, and AGC Inc., whose proprietary resins and application engineering provide scale economies and switching barriers. Mid-tier competitors differentiate through fabrication and installation services, while Chinese newcomers leverage cost advantages to target domestic construction and electronics customers. Strategic moves underscore the shifting competitive axis. The Chemours Company’s collaboration with Hibiya Engineering to trial Opteon 2P50 coolant diversifies revenue beyond traditional membranes, mitigating PFAS exposure risk. AGC Inc. supplied Fluon ETFE film for SoFi Stadium and Allianz Arena façades, reinforcing brand visibility in flagship projects.

Ethylene Tetrafluoroethylene (ETFE) Industry Leaders

The Chemours Company

3M

DAIKIN INDUSTRIES, Ltd.

AGC Inc.

Saint-Gobain

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A clear whitespace area is recycling and circularity solutions for fluoropolymers. This has become more commercially relevant as EU REACH-based PFAS policy discussions move forward, and large end-use segments such as building membranes, industrial linings, and cable face tighter documentation and stewardship expectations. Producers and downstream users that pair ETFE performance with verifiable PFAS management practices, audited supply chains, and take-back or recycling pathways have a route to protect specifications in Europe while keeping global programs aligned.

Opportunity also sits in increasing the share of high-performance, qualification-driven applications where ETFE's value proposition is anchored in durability and compliance rather than commodity substitution. This includes aerospace wiring insulation, chemical-resistant tubing in renewable aviation-fuel plants, and transparent photovoltaic laminates for building-integrated use cases. On the supply side, Chinese fluoropolymer manufacturers have been focusing on process optimization to meet certification standards across Europe, the United States, and Southeast Asia, as reported by Shandong Hengyi New Material Technology Co., Ltd. in May 2026. That signals intensifying competition in certified, higher-end ETFE and related fluoropolymer grades, rather than only domestic, volume-led markets.

Recent Industry Developments

- July 2026: 3M and Microsoft announced a strategic partnership to advance AI data center infrastructure and enterprise transformation. The initiative emphasizes scaling data center capabilities and accelerating deployment of advanced infrastructure components, aligning with increasing demand for high-performance materials and connectivity solutions across hyperscale builds. The move strengthens 3M's position in infrastructure supply chains that consume specialty polymers, coatings, and insulating materials.

- August 2025: The Chemours Company signed strategic agreements with SRF Limited in India to increase operational flexibility and strengthen capacity support for fluoropolymers and fluoroelastomers used in essential applications. The agreements broaden Chemours' manufacturing and supply options for high-value fluoromaterial portfolios that share upstream dependencies with ETFE. This supports resiliency in a market characterized by concentrated resin supply and multi-year qualification requirements.

- July 2024: AGC Chemicals Americas' Fluon ETFE film was specified for the roof application at SoFi Stadium in Inglewood, California. The project highlights continued adoption of ETFE architectural membranes in high-visibility venues where daylighting and weight savings are central design drivers. Such flagship installations reinforce downstream demand for premium-grade films and fabrication expertise in building-envelope applications.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the ethylene tetrafluoroethylene (ETFE) market is defined as the global revenue generated from ETFE material sold across common commercial forms and processing routes, and then used in industrial and end-use applications where ETFE is the main performance polymer.

Scope exclusions: Finished assemblies where ETFE is only a minor sub-component, and installation or construction services attached to ETFE-based structures, are kept outside the market value.

Segmentation Overview

- By Technology

- Extrusion Molding

- Injection Molding

- By Product Type

- Powder

- Granule

- Other Product Types (Pellet, etc.)

- By Application

- Film and Sheet

- Wire and Cable

- Tubes

- Coatings

- Other Applications (3D-Printed Components, etc.)

- By End-use Industry

- Building and Construction

- Aerospace and Defense

- Automotive and E-Mobility

- Electrical and Electronics

- Solar Photovoltaics

- Industrial and Chemical Processing

- By Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to build the first version of the demand and supply picture before any sizing assumptions are locked. Public sources are referenced for inputs, including USGS mineral and materials data, USITC and UN Comtrade trade statistics, and International Energy Agency industry and power indicators, plus government statistical agencies that track construction output and industrial production.

In parallel, company annual reports, investor presentations, product brochures, and reputable press releases are reviewed to track capacity additions, application focus, and pricing direction. Patent databases are also checked to see where new ETFE grades and processing routes are being developed, which helps confirm how quickly innovation moves into commercial adoption. For hard-to-find company financials and shipment signals, paid subscriptions for company financials and intelligence, plus shipment-level import and export tracking, are used. These are illustrative sources, and other public references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to stress-test what was built from desk research, and to close the gaps that often show up around split assumptions, pricing movement, and actual adoption by application. Interviews covered a mix of producers, distributors, processors, and large end users across major consuming regions, so regional demand signals and supply constraints could be cross-checked, then reflected back into the final model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 13% | APAC: 42% |

| Mid tier: 54% | Functional/Unit leaders: 39% | EMEA: 36% |

| Smaller Players: 14% | Managers: 48% | Americas: 22% |

Market-Sizing & Forecasting

Sizing starts with a top-down approach where polymer demand pools are reconstructed using application-linked indicators, then translated into ETFE consumption using penetration and substitution assumptions. The inputs that typically matter are construction facade and roofing activity (for film and sheet use), wire and cable output trends, chemical processing investment cycles, and trade flows of ETFE-linked material forms where reporting is available.

After the top line is formed, it is checked using selective bottom-up approximations from the supply side, such as sampled producer capacity and utilization direction, distributor channel checks, and volume-by-application sanity checks using typical price bands. Where country or application splits are thin, gaps are handled by anchoring to the regional mix described by interviewees, then applying conservative adjustment factors until the output aligns with observed trade and end-use signals.

For forecasting, scenario analysis is used because ETFE demand can shift with construction cycles and industrial investment timing. The base case combines short-series trend smoothing with expert-agreed variable outlooks, and upside and downside cases are applied to the same set of drivers so the forecast remains consistent and explainable.

Data Validation & Update Cycle

Model outputs are validated through consistency checks across independent signals such as regional construction indicators, industrial production movement, and reported capacity changes. When an outlier is detected, the assumption trail is reviewed, and follow-up calls are triggered with the relevant respondent group so the driver or split can be corrected before sign-off.

A multi-step review is followed, where the analyst building the model and a second reviewer check calculations, units, currency conversion timing, and year mapping. Reports are refreshed annually, with interim updates when material events occur, such as major plant changes, regulatory shifts, or abrupt demand shocks. Before delivery, a final review pass is completed so clients receive the most current view that matches the latest available evidence.

Mordor Intelligence's Ethylene Tetrafluoroethylene Etfe Market Size Compared Against Other Published Estimates

Published ETFE market values can differ even when the topic name looks the same, because different teams may count different ETFE forms, apply different pricing logic, and select different base years for their growth calculations. The comparison stays practical by focusing on the year being sized, what is counted in-scope, and what checks were used to keep the total tied to real demand.

By tracking application-linked demand drivers and refreshing pricing and mix assumptions with interviews, Mordor Intelligence keeps the ETFE total aligned to where ETFE is actually consumed, rather than letting adjacent fluoropolymer items or service spend spill into the value.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 567.16 M (2026) | |

| Global Consultancy A | USD 500.90 M (2024) | Uses an earlier base year and shorter horizon, and the scope presentation leans more on type-level splits, which can understate newer demand pockets where films and sheets are expanding faster than historical averages. |

| Industry Publisher B | USD 540.00 M (2025) | Starts from a different base year and uses a longer forecast window, where differences in currency timing and how application shares are carried forward can create a higher 2034 trajectory even if near-term demand signals are similar. |

The spread in the table is mainly explained by year selection and how pricing and application mix are carried into the model. When scope boundaries are kept tight and the sizing steps are tied back to visible demand indicators, the result is easier to audit and to update as end markets move.

Key Questions Answered in the Report

What is the current ETFE market size and its expected growth?

The Ethylene Tetrafluoroethylene (ETFE) market size is USD 567.16 Million in 2026 and is projected to reach USD 802.29 Million by 2031, reflecting a 7.18% CAGR.

Which region holds the largest share of the ETFE market?

Asia-Pacific leads with 46.90% revenue share in 2025 and is forecast to grow at an 8.54% CAGR through 2031.

Which ETFE application segment is expanding the fastest?

Wire and cable applications are advancing at a 8.86% CAGR between 2026 and 2031 due to aerospace and renewable-energy infrastructure demand.

How are PFAS regulations affecting the ETFE industry?

Proposed EU PFAS restrictions could reduce ETFE usage above threshold concentrations, prompting manufacturers to invest in emission-capture technologies and alternative chemistries.

Why is ETFE preferred over glass in stadium roofing?

ETFE membranes cut structural weight by up to 95%, transmit 95% daylight, and require cleaning only every two to three years while maintaining fire-safe, self-extinguishing properties.

Page last updated on: