Rice Seed Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Market Size (2025) | USD 1.30 Billion |

| Market Size (2030) | USD 1.73 Billion |

| Growth Rate (2025 - 2030) | 5.90% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Rice Seed Treatment Market Analysis by Mordor Intelligence

The rice seed treatment market size is valued at USD 1.30 billion in 2025 and is projected to reach USD 1.73 billion by 2030, reflecting a 5.9% CAGR over the forecast period. Hybrid-seed premiums, climate-driven disease pressure, and regulatory momentum toward low-impact biologicals are reshaping competitive dynamics and elevating demand for precision application technologies within the rice seed treatment market. Seed companies are bundling treatments with certified hybrids to protect growers’ higher upfront seed investments, while digital coating lines improve dosing accuracy and cut application costs. Emerging carbon-credit schemes, government subsidies for methane-mitigation practices, and rapid adoption of direct-seeded rice systems in the Asia-Pacific further accelerate treatment uptake across the rice seed treatment market. Bayer AG's Rice Carbon Program in India has generated 250,000 metric tons of CO₂ equivalent credits through practices that include biological seed priming, demonstrating the commercial viability of carbon-linked seed treatment incentives. Competitive intensity is rising as major agrochemical firms acquire or partner with biological innovators to diversify their portfolios and comply with tightening regulations on neonicotinoids and microplastics.

Key Report Takeaways

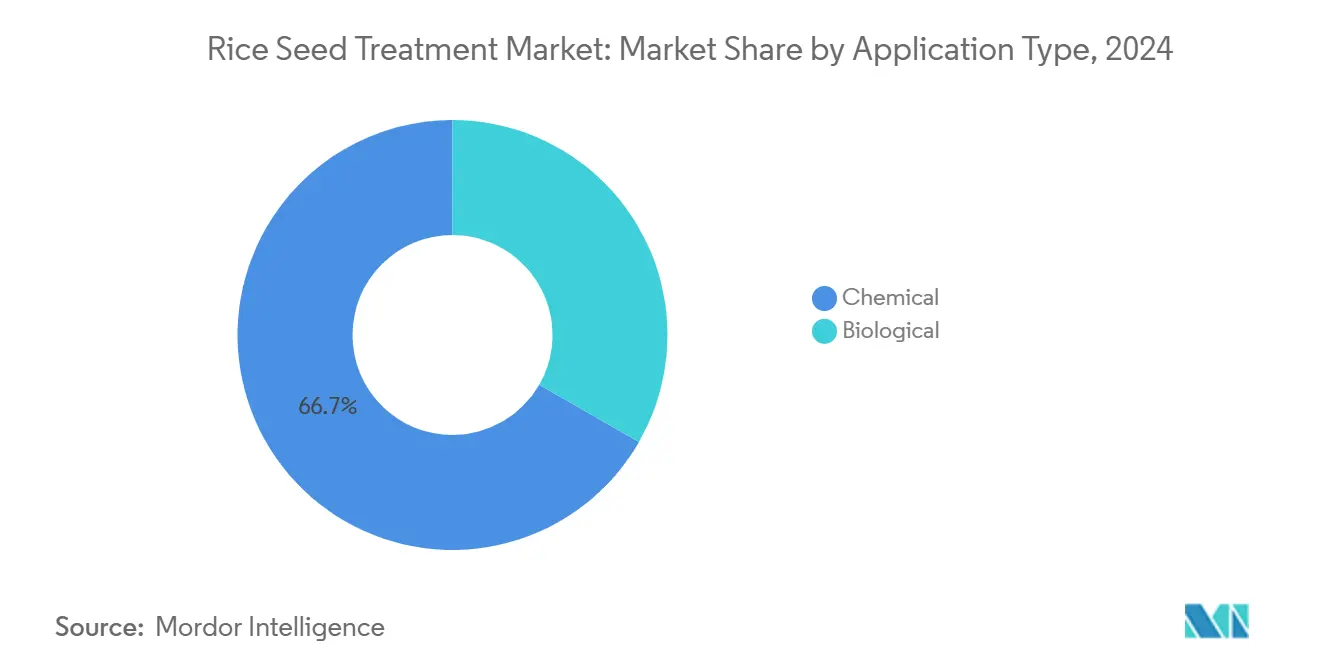

- By application, chemical treatments led with 66.7% rice seed treatment market share in 2024, while biological solutions are projected to expand at an 5.9% CAGR through 2030.

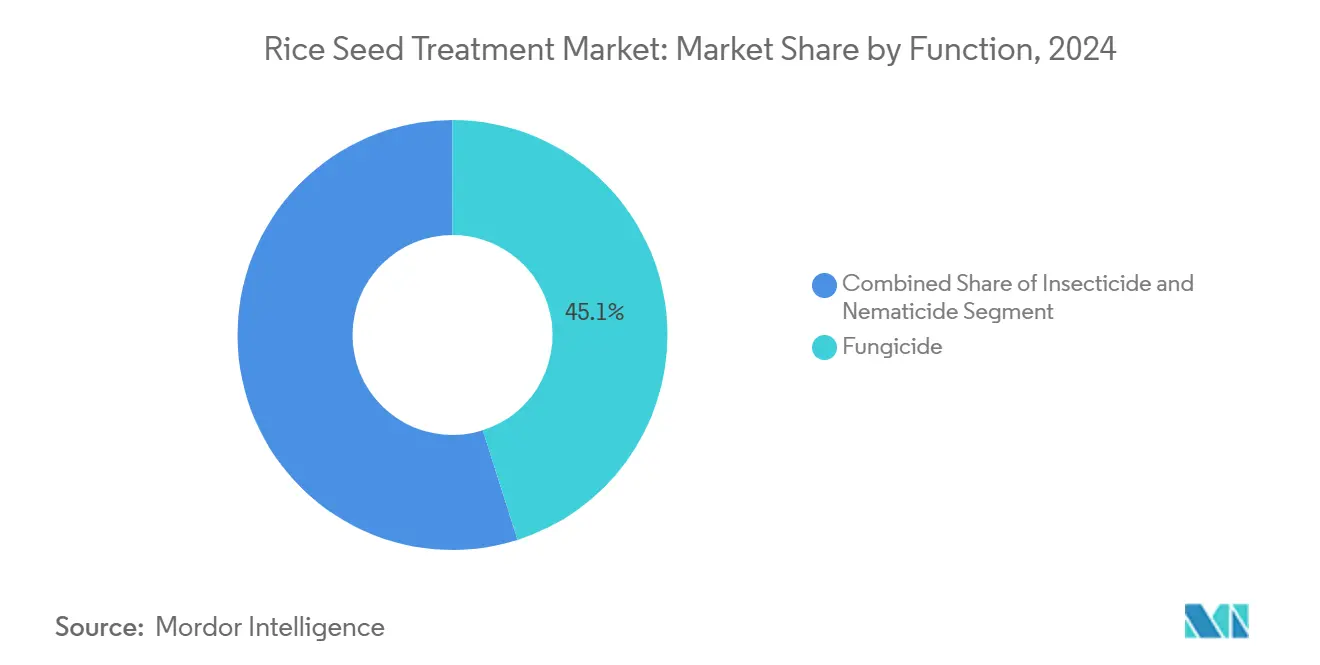

- By function, fungicide accounted for 45.1% of the rice seed treatment market size in 2024, whereas insecticide is advancing at 6.3% CAGR to 2030.

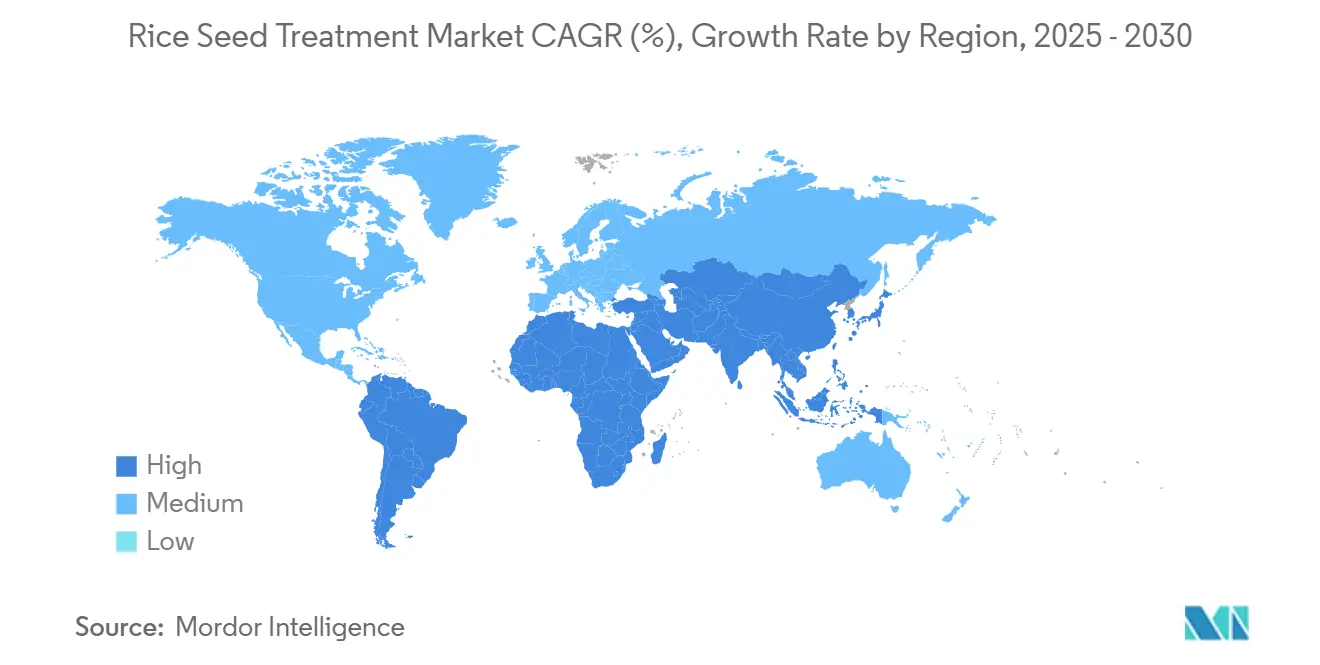

- By geography, Asia-Pacific held a 39.2% share of the market in 2024. The Middle East registers the fastest regional CAGR at 6.2% to 2030.

Global Rice Seed Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium-priced hybrid and certified rice seeds are expanding treated-seed demand | +1.2% | Asia-Pacific core, spillover to North America | Medium term (2-4 years) |

| Rapid replacement of in-furrow chemicals by seed-applied systemic actives | +0.9% | Global, with early adoption in North America and Europe | Short term (≤ 2 years) |

| Government subsidies for low-dose seed treatments to curb paddy methane emissions | +0.8% | Asia-Pacific, with emerging programs in North America | Long term (≥ 4 years) |

| Climate-driven spike in bacterial-leaf-blight and blast outbreaks fueling prophylactic seed coating | +1.1% | Global, particularly monsoon-dependent regions | Short term (≤ 2 years) |

| Digitally dosed film-coating lines lower treatment cost per kilogram | +0.7% | Global, with the fastest adoption in developed markets | Medium term (2-4 years) |

| Carbon-credit schemes rewarding biologically primed rice seedlings | +0.6% | Asia-Pacific and Europe, with pilot programs in other regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premium-priced Hybrid and Certified Rice Seeds Expanding Treated-Seed Demand

Hybrid rice acreage surged in China during 2024, intensifying grower focus on safeguarding higher seed investments through bundled treatments. The trend erodes the farmer-saved-seed practice, widening the commercial base for the rice seed treatment market. Companies such as RiceTec integrate color-coded SQUAD treatment systems to lock in recurring revenues and capture 15-25% price premiums over untreated seed. Certified-seed policies in Vietnam and the Philippines amplify this effect by mandating traceable, treated seed lots at planting. The shift sustains mid-term growth momentum as direct-seeded rice expands across Asia-Pacific and North America.

Rapid Replacement of In-Furrow Chemicals by Seed-Applied Systemic Actives

Labor constraints in mechanized direct-seeding systems are accelerating the pivot from in-furrow sprays to single-pass seed treatments. BASF SE’s Prexio Active delivers season-long pest control with 70–80% less active ingredient per hectare than legacy soil applications. Bayer’s Channel Edge platform further optimizes release kinetics, aligning active availability with early pest windows[1]Source: Bayer AG, “Channel Edge Seed Treatment Platform,” bayer.com. Adoption is strongest in the United States and Spain, where seed-applied formulations simplify logistics and reduce worker exposure. The efficiency gain meets tightening residue thresholds, solidifying short-term demand across the rice seed treatment market.

Government Subsidies for Low-Dose Seed Treatments to Curb Paddy Methane Emissions

Haryana offers USD 48 per acre incentives for direct-seeded rice, contingent upon the adoption of specialized treatment to ensure uniform germination. Vietnam’s Transforming the Rice Value Chain (TRVC) program distributed USD 130,000 in grower bonuses in 2025 to support low-emission seed technologies. Bayer’s Rice Carbon Program monetized 250,000 metric tons CO₂e in credits by bundling biological priming with alternate wetting practices. The Sustainable Rice Platform's Low Carbon Assurance Module, launched in May 2024, provides a standardized framework for measuring and verifying emission reductions from improved seed treatments and cultivation practices.

Climate-Driven Spike in Bacterial-Leaf-Blight and Blast Outbreaks Fueling Prophylactic Coating

Weather volatility elevates pathogen pressure, especially in exposed direct-seeded fields. Ascribe Bioscience’s Phytalix cut bacterial leaf blight incidence in 2025 trials, underscoring the growing role of prophylactic biologicals. The International Rice Research Institute’s Direct-Seeded Rice Consortium identifies disease as the primary obstacle to scaling Direct Seeded Rice (DSR), prompting growers to seek seed-based defenses. BASF SE’s Cevya fungicide addresses the escalating outbreaks of blast disease tied to erratic rainfall patterns. This disease pressure is particularly acute in direct-seeded systems, where seeds lack the protective environment of nursery beds and are exposed to pathogens immediately upon planting.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening neonic regulation in the Asia-Pacific and Europe | -0.8% | Asia-Pacific and Europe primarily | Short term (≤ 2 years) |

| On-farm slurry treatments' poor shelf life and farmer skill gaps | -0.5% | Global, particularly in developing regions | Medium term (2-4 years) |

| Polymer-microplastic regulations targeting conventional film coats | -0.6% | Europe primarily, expanding globally | Medium term (2-4 years) |

| Variability of microbial efficacy across flooded paddy ecologies | -0.4% | Asia-Pacific core rice regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tightening Neonic Regulation in Asia-Pacific and Europe

European Union and Chinese authorities continue to restrict neonicotinoid usage, compelling costly reformulation and re-registration cycles that can exceed USD 2 million per active ingredient[2]Source: European Chemicals Agency, “Restriction on Intentionally Added Microplastics,” echa.europa.eu. The regulatory transition creates market uncertainty as companies invest in alternative active ingredients while managing inventory of restricted formulations. BASF responded with non-neonic Prexio Active, but smaller firms struggle to finance compliance, reducing product diversity and raising prices for the rice seed treatment market. Farmer uncertainty during transition periods slows near-term uptake of new products, dampening growth.

On-farm slurry treatments’ poor shelf life and farmer skill gaps

Basic slurry formulations remain popular among smallholder farmers due to their low cost, but these formulations degrade within weeks and require precise mixing ratios and careful application techniques. The limited availability of agricultural extension services in Africa and South Asia contributes to improper application methods and inadequate storage practices, resulting in inconsistent field performance and farmer doubts about the value of commercial seed treatments. Knowledge gaps in proper handling procedures and application methods hinder the adoption of advanced treatments, particularly biological products that require temperature-controlled storage and transport throughout the distribution chain.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Biologicals Gain Momentum Despite Chemical Dominance

Chemical formulations continued to dominate the rice seed treatment market with a 66.7% share in 2024, underpinned by entrenched distribution networks and proven broad-spectrum efficacy. The biological segment is projected to grow at a 5.9% CAGR through 2030. The rice seed treatment market size for biological products is projected to grow by 2030, driven by the convergence of carbon credit eligibility and residue regulations, which are projected to support increased adoption. Chemical treatments remain essential in regions with high disease pressure and limited access to biological alternatives, particularly in the Asia-Pacific markets, where blast and bacterial leaf blight pose significant yield risks.

Biological uptake began in Western Europe and the United States, but is now accelerating in China and Brazil, where food safety certification and export premiums offset higher product costs. Integrated bio-chem packages pair microbial inoculants with reduced-dose synthetic actives to deliver season-long protection while easing regulatory pressures. Major players, such as Corteva Incorporated, injected USD 25 million into Simbiose Agro to expand its biological treatment capacity, signaling the industry's commitment to this pivot[3]Source: Corteva Inc., “Strategic Partnerships and Investment Announcements,” corteva.com.

By Function: Fungicides Dominate, Insecticides Surge Ahead

Fungicide-based seed treatments comprised 45.1% of the rice seed treatment market share in 2024, reflecting their critical role in managing early-season fungal threats such as Magnaporthe oryzae (rice blast) and Xanthomonas oryzae (bacterial blight). These treatments are used in both transplanted and direct-seeded rice systems, where early pathogen suppression is essential for stand establishment and tiller uniformity. The segment features dual-action formulations combining curative and preventive modes, integrated with micronutrient primers to enhance seedling resilience. In high-humidity regions like Bangladesh and the Mekong Delta, fungicidal coatings are developed for compatibility with polymer carriers and precision sowing technologies to ensure uniform coverage and reduce environmental drift.

The insecticide seed treatment segment projects a CAGR of 6.3% from 2025 to 2030, emerging as the fastest-growing functional category. This growth stems from increasing pest resistance and the spread of vector-borne diseases such as rice ragged stunt and grassy stunt virus, particularly in hybrid rice systems where early vigor is essential. Seed-applied insecticides, notably neonicotinoids and anthranilic diamides, are reformulated for compatibility with drone-based sowing and automated seeders. India, Vietnam, and the Philippines show the highest adoption rates, where high-value rice varieties require consistent emergence and reduced seedling mortality. As farmers implement integrated pest management practices, insecticidal coatings help minimize post-emergence sprays and improve return on investment.

Geography Analysis

Asia-Pacific held 39.2% of the rice seed treatment market share in 2024, driven by intensive rice cultivation across China, India, and Southeast Asia, where changing agricultural practices are creating new treatment demands. China's seed market grew 18% in 2024 according to Syngenta's financial disclosures, with seed treatment adoption accelerating alongside hybrid rice expansion and direct-seeding adoption. The region's dominance reflects both cultivation scale and the rapid adoption of mechanized planting systems that require specialized seed treatments for optimal performance.

The Middle East represents the fastest-growing regional market at 6.2% CAGR through 2030, despite its smaller absolute size, driven by government initiatives to enhance food security and agricultural sustainability. The region's growth is supported by substantial government investments in agricultural technology and water-efficient production systems that rely heavily on advanced seed treatments. North America and Europe maintain steady growth rates supported by regulatory compliance requirements and premium market segments that justify higher treatment costs.

North America and Europe exhibit steady single-digit growth as farmers adopt low-dose systemic actives to satisfy residue ceilings and labor efficiency goals. European regulation around microplastics accelerates migration toward biodegradable coatings, reshaping product portfolios. South America's market development is accelerating through strategic partnerships and technology transfers, with Corteva's USD 25 million investment in Brazilian biological seed treatment development representing a significant commitment to regional market expansion.

Competitive Landscape

The rice seed treatment market exhibits moderate consolidation, with global multinational corporations maintaining dominant positions alongside emerging regional specialists and biological innovators. Bayer AG, Syngenta Group, BASF SE, Corteva Inc., and UPL Ltd. command an estimated top-five, while dozens of regional firms and biological specialists fill niche gaps. Strategic alliances are proliferating as incumbents seek proprietary microbial strains and delivery technologies to future-proof portfolios against regulatory risk.

Technology investment differentiates leaders. BASF SE pilots AI-driven coating lines that recalibrate polymer flow in real time, while Syngenta integrates QR-traceability to verify treatment integrity at the point of sale. FMC Corporation-backed AgroSpheres develops nano-lipid carriers that may reduce dosage rates by half, challenging incumbent economics.

Regional compliance divergence adds complexity. European microplastic bans boost early mover advantage for biodegradable offerings, whereas looser North American regulation allows extended sales of legacy formulations. Companies pairing sustainability credentials with robust field efficacy position themselves to capture premium segments of the rice seed treatment market. The competitive landscape favors companies that can provide comprehensive solutions combining synthetic chemistry, biological alternatives, and application technologies to meet Chile's complex export compliance requirements while maintaining economic viability for growers across diverse production systems.

Rice Seed Treatment Industry Leaders

Bayer AG

UPL Limted

Syngenta Group

BASF SE

Corteva Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Bayer's Rice Carbon Program in India generated 250,000 metric tons of CO2 equivalent credits by implementing sustainable rice cultivation practices, demonstrating the growing adoption of seed treatment solutions in the rice market. The program incorporated biological seed priming and alternative cultivation methods to reduce methane emissions, which is going to drive the demand for advanced seed treatment products in rice cultivation.

- April 2025: The Haryana state government of India plans to expand direct-seeded rice (DSR) cultivation to 300,000 acres, offering USD 120 per acre in subsidies to farmers who adopt DSR technology, which requires specialized rice seed treatments for successful implementation.

- May 2024: Agritech platform Rize secured USD 14 million in Series A funding to scale sustainable rice farming technology across South and Southeast Asia, including seed treatment innovations that support emission reduction goals.

Global Rice Seed Treatment Market Report Scope

According to the International Seed Federation, seed treatment products encompass biological, physical, and chemical agents and techniques applied to seeds to protect and enhance healthy rice crop establishment.

The rice seed treatment market segments include treatment type (chemical and non-chemical/biological), function (seed protection, seed enhancement, and other functions), application techniques (seed coating, seed pelleting, seed dressing, and other application techniques), and geography (North America, Europe, Asia-Pacific, South America, and Africa). The report provides market size and forecasts in USD million for all segments.

| Chemical |

| Biological |

| Fungicide |

| Insecticide |

| Nematicide |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| France | |

| Spain | |

| Italy | |

| Russia | |

| United Kingdom | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| Application | Chemical | |

| Biological | ||

| Function | Fungicide | |

| Insecticide | ||

| Nematicide | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| Spain | ||

| Italy | ||

| Russia | ||

| United Kingdom | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the rice seed treatment market?

The rice seed treatment market size stands at USD 1.30 billion in 2025 and is projected to reach USD 1.73 billion by 2030.

Which region leads adoption of rice seed treatments?

Asia-Pacific holds the largest share at 39.2%, mainly China, India, and Southeast Asia's have intensive rice areas.

How are carbon credits influencing treatment demand?

Verified emission-reduction schemes reward biologically primed seed, creating new revenue streams that offset treatment costs.

What regulatory trends affect polymer seed coatings?

EU and emerging global restrictions on intentionally added microplastics push manufacturers toward higher-cost biodegradable polymers.

Page last updated on: