Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

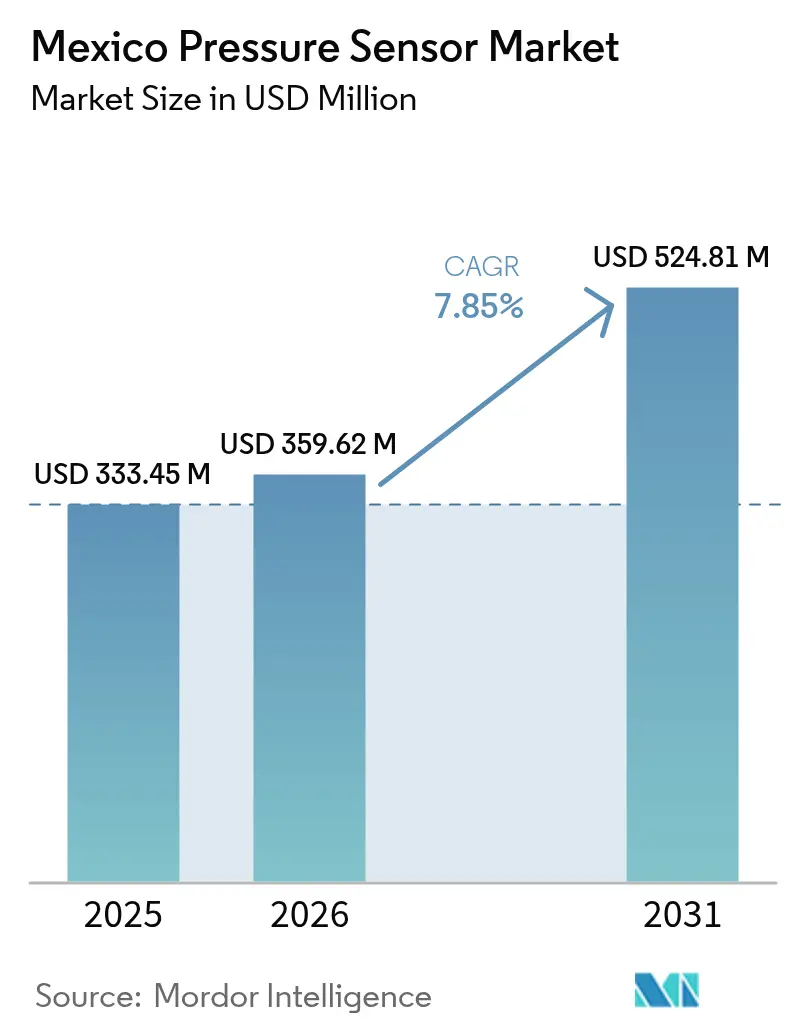

| Base Year Market Size (2025) | USD 333.45 Million |

| Market Size (2026) | USD 359.62 Million |

| Market Size (2031) | USD 524.81 Million |

| Growth Rate (2026 - 2031) | 7.85% CAGR |

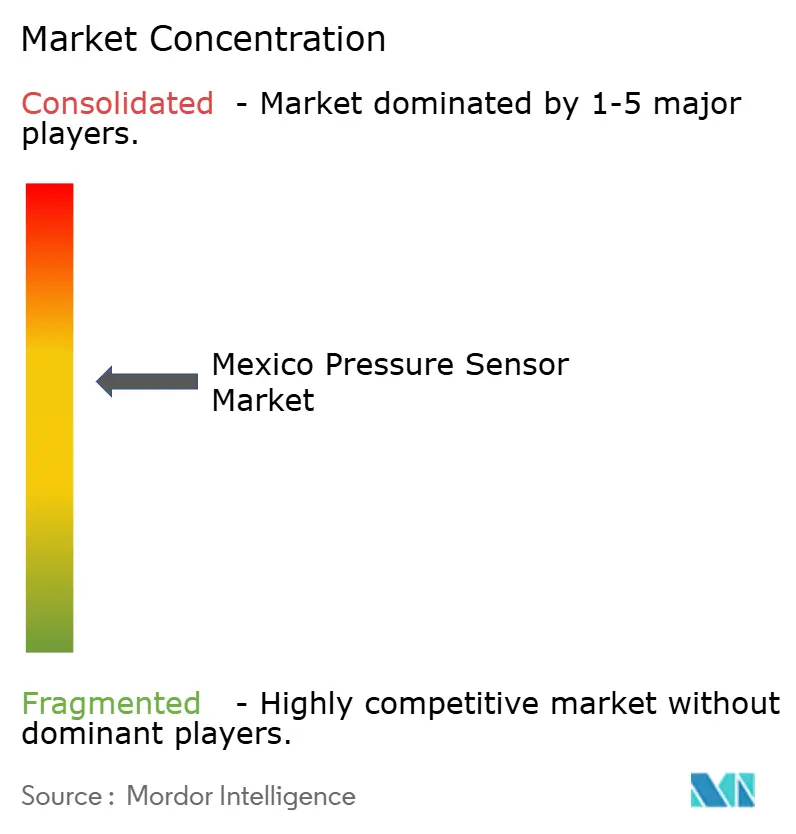

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Pressure Sensor Market Analysis by Mordor Intelligence

The Mexico pressure sensors market size was valued at USD 333.45 million in 2025 and estimated to grow from USD 359.62 million in 2026 to reach USD 524.81 million by 2031, at a CAGR of 7.85% during the forecast period (2026-2031). The upward trajectory mirrors the country’s position as Latin America’s most competitive manufacturing economy, with manufacturing contributing 18% of national GDP in 2024. Mandatory tire-pressure monitoring, healthcare digitization, and Industry 4.0 adoption underpin sustained demand, while the nation’s integration in North American semiconductor supply chains reduces structural risk. Automotive applications dominate spend, yet medical, optical, and differential sensing technologies record the fastest growth as Mexico pressure sensors market participants diversify into precision healthcare, building automation, and offshore energy. Central Mexico leads volumes, Southern Mexico and the Yucatán Peninsula provide the highest growth curve, and established multinationals compete alongside regional MEMS specialists in a moderately fragmented field.

Key Report Takeaways

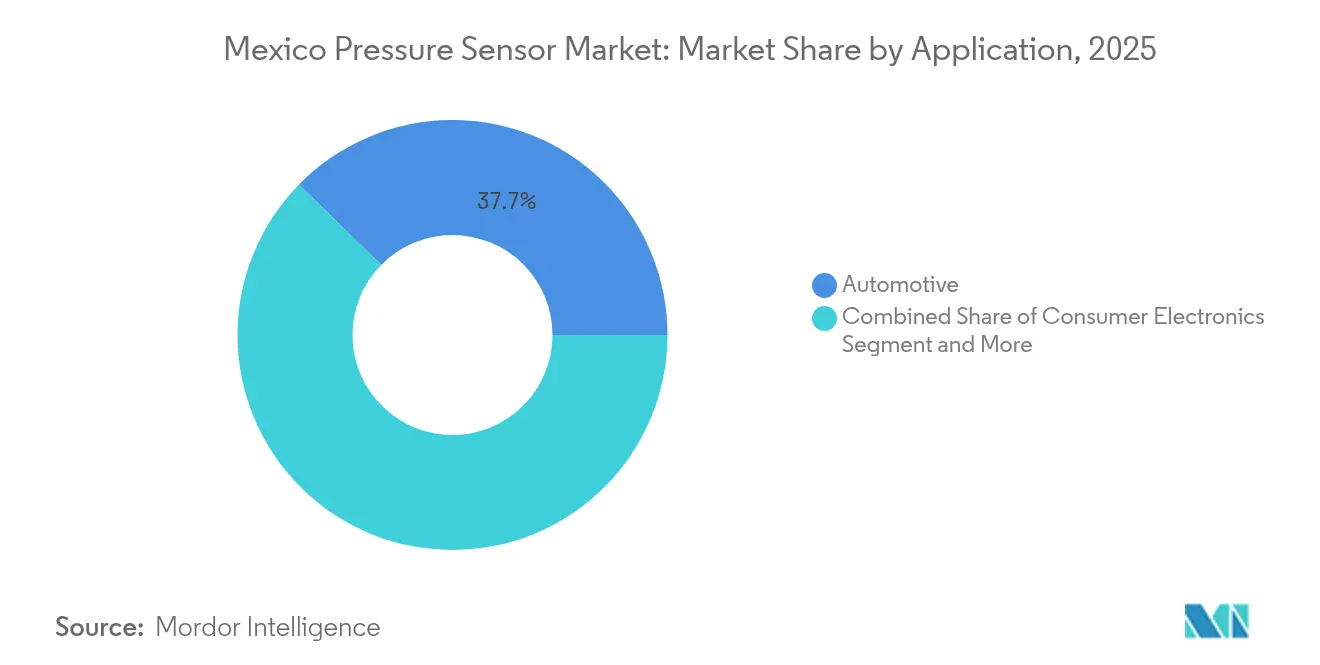

- By application, automotive captured 37.65% of Mexico pressure sensors market share in 2025; medical applications are projected to expand at a 9.05% CAGR through 2031.

- By technology, MEMS commanded 41.75% share of the Mexico pressure sensors market size in 2025, while optical technology is forecast to grow at an 8.15% CAGR through 2031.

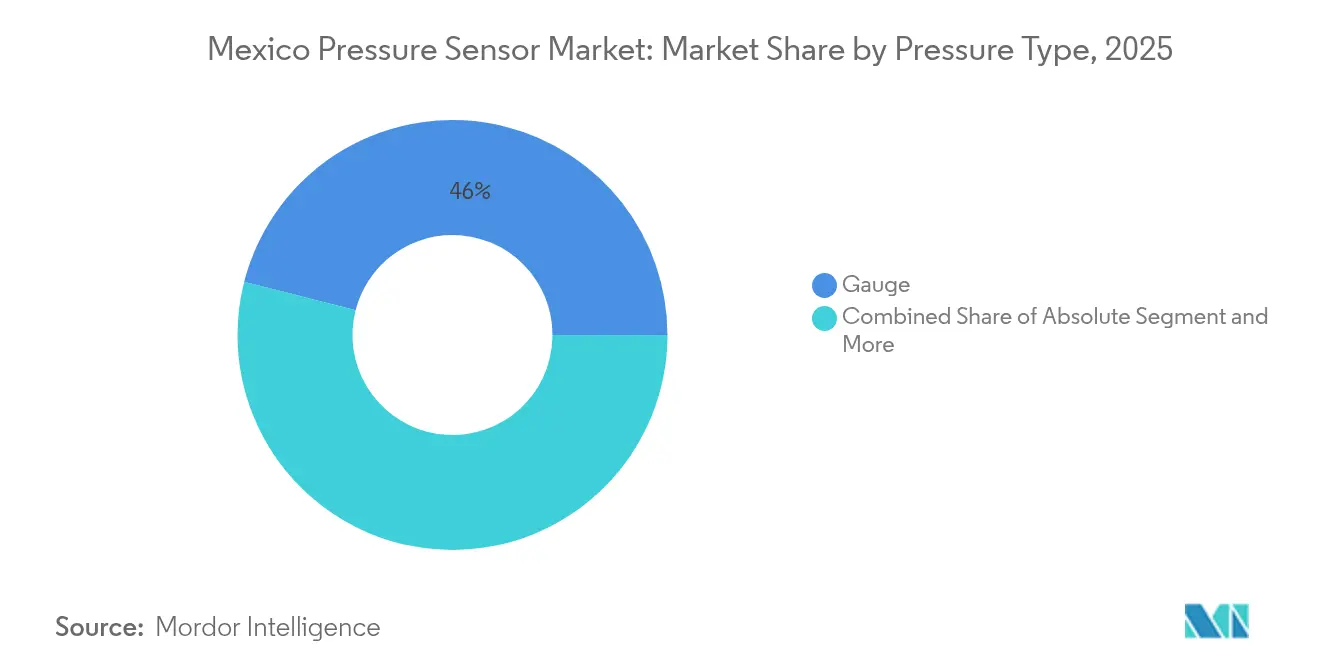

- By pressure type, gauge sensors held 46.02% of the Mexico pressure sensors market size in 2025; differential pressure sensors register the highest projected CAGR at 8.65% through 2031.

- By output type, digital sensors accounted for 53.55% revenue share of the Mexico pressure sensors market size in 2025 and are advancing at a 8.95% CAGR through 2031.

- By region, Central Mexico led with 50.65% Mexico pressure sensors market share in 2025, while Southern Mexico and the Yucatán Peninsula expand at a 9.55% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Pressure Sensor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Automotive and Healthcare production expansion | +2.1% | Central Mexico, Northern Mexico | Medium term (2-4 years) |

| Accelerating MEMS/NEMS adoption | +1.8% | Central Mexico, Jalisco | Long term (≥ 4 years) |

| Industry 4.0-driven factory automation | +1.5% | Northern Mexico, Bajío region | Medium term (2-4 years) |

| Mandatory TPMS under NOM-194-SCFI-2015 | +1.2% | National | Short term (≤ 2 years) |

| Smart-agro greenhouse sensing demand | +0.9% | Southern Mexico, Central Mexico | Long term (≥ 4 years) |

| Offshore Oil and Gas pressure-monitoring projects | +0.8% | Southern Mexico, Gulf Coast | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Automotive and Healthcare Production Expansion

Mexico pressure sensors market demand rises as engine-management, exhaust control, and TPMS roll into every locally built vehicle; at the same time, oxygen concentrators and respiratory monitors require higher-accuracy pressure chips for compliance with COFEPRIS labeling standard NOM-137-SSA1-2024.[1]Emergo by UL, “Mexico COFEPRIS Announces Revised Labeling Standard,” emergobyul.com EV battery packs introduce new cooling and safety loops, adding incremental sensor nodes while nearshoring relocates North American Tier-1 suppliers to Central and Northern clusters. The parallel boom in medical device exports multiplies use cases—from blood pressure monitors to infusion pumps—further reinforcing sensor volumes. Capacity expansion in Sonora and Nuevo León reduces lead times for local OEMs, and cross-licensing agreements with US fabs speed knowledge transfer.

Accelerating MEMS/NEMS Adoption

A regional ecosystem anchored in Jalisco funnels venture funding, university talent, and Bosch’s expanded R&D footprint into MEMS prototypes and small-batch runs.[2]Le Monde, “Mexican State of Jalisco Dreams of Becoming the New Silicon Valley,” lemonde.fr Mexico pressure sensors market participants align with micro-foundry partners to convert legacy piezoresistive designs into wafer-level packages that cut cost per die. Projects financed by the Secretariat of Energy prove MEMS down-hole gauges viable for shale well profiling, broadening the technology’s TAM into oil and gas. Cooperative agreements with Guadalajara universities streamline material characterisation, shortening time-to-market for next-generation devices.

Industry 4.0-Driven Factory Automation

Retrofitting legacy machine tools with information-processing kits places digital pressure transducers at each pneumatic cylinder, enabling cloud dashboards and predictive maintenance loops. Automotive stamp-press lines in Coahuila adopt sensor clusters that feed SPC algorithms and reduce unplanned downtime. Textile mills in the Bajío region integrate compressed-air leak detection to cut utility cost by 8%, evidencing tangible ROI for mid-sized factories. Government mapping through the ‘Prospective Territorial-Industrial Atlas’ channels fiscal incentives to sensor-rich brownfield upgrades, accelerating replacement cycles for analog gauges.

Mandatory TPMS Under NOM-194-SCFI-2015

Federal rules mirror U.S. FMVSS performance thresholds, obliging every new light vehicle sold to trigger an under-inflation warning within 20 minutes.[3]Federal Register, “Federal Motor Vehicle Safety Standards; Tire Pressure Monitoring Systems,” federalregister.gov Local assemblers synchronize ECU firmware with ISO 21750 diagnostics, pushing OEMs to lock long-term agreements with sensor makers. Mexico pressure sensors market growth accelerates because TPMS units migrate from optional trim to base trim, elevating average sensor content per vehicle. Independent aftermarket demand adds a replacement tier as the light-duty fleet ages.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High unit cost of precision sensors | -1.1% | National, with higher impact in Southern Mexico | Medium term (2-4 years) |

| Low-price Asian imports intensifying competition | -0.9% | National, concentrated in Central Mexico | Short term (≤ 2 years) |

| MEMS chip supply-chain disruptions | -0.7% | Northern Mexico, Central Mexico | Short term (≤ 2 years) |

| Shortage of calibration and metrology talent | -0.6% | National, acute in emerging regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Unit Cost of Precision Sensors

Certification under Mexico’s Quality Infrastructure Law elevates CapEx as manufacturers pay for NOM testing, metrology services, and periodic audits. Procurement teams in Chiapas citrus plants often postpone upgrades when ROI falls below internal hurdle rates, limiting Mexico pressure sensors market penetration outside premium tiers. Suppliers counter with localized assembly in Querétaro that reduces import duties and with value-engineered SKUs targeting ±1% FS accuracy instead of ±0.1% in cost-sensitive lines.

Low-Price Asian Imports Intensifying Competition

Commodity gauge transmitters priced 15–20% below regional averages reach the aftermarket via gray-market channels, squeezing margins for domestic distributors. Mexico pressure sensors market incumbents respond by bundling on-site calibration, bilingual technical support, and warranty extensions to justify price premiums. Nearshoring rationales—shorter lead times, USMCA duty preferences—temper but do not erase price gaps, especially in analog vacuum sensors for packaging equipment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Automotive Dominance Drives Market Growth

Automotive applications account for 37.65% of Mexico pressure sensors market share in 2025, underscoring the country’s status as a regional vehicle-production powerhouse. Engine control, TPMS, and emissions subsystems together shape baseline demand. Mexico pressure sensors market size for medical devices is projected to expand at a 9.05% CAGR as tele-med and in-hospital diagnostic equipment proliferate under COFEPRIS oversight. Industrial automation sequences drive consistent replacement of obsolete pneumatic monitors, and smart-home gadgets enlarge the consumer slice by embedding miniaturized gauges in HVAC controllers and air purifiers.

High-growth verticals benefit from value pools beyond unit shipments. Medical-device OEMs require traceability and MDR-style documentation, prompting bundled offerings with digital calibration certificates. In automotive, the EV transition adds battery safety circuits that need absolute micro-barometric sensors, increasing BOM value per unit. Offshore operators widen the industrial envelope, procuring sapphire-diaphragm assemblies rated for 15,000 psi. Collectively, these vectors reinforce the diversified resilience of the Mexico pressure sensors market.

By Technology: MEMS Leadership Accelerates Innovation

MEMS holds 41.75% share of the Mexico pressure sensors market size in 2025 as die-level integration reduces package footprint and cost while sustaining automotive-grade repeatability. Optical technology registers the fastest 8.15% CAGR because non-contact interrogation thrives in corrosive offshore and sterile bioprocess settings. Piezoresistive chips retain incumbency in most gauge and absolute variants, whereas capacitive structures capture niches demanding sub-Pa resolution.

Mexico pressure sensors market suppliers leverage Jalisco’s micro-electronics corridor to co-develop ASICs that process MEMS outputs in-package, cutting board real estate for vehicle ECUs. Optical OEMs partner with Veracruz shipyards to trial fiber Bragg pressure arrays in subsea risers. Resonant sensing, albeit niche, enters barometric drones where frequency drift offers self-calibration advantages. Technology diversification enables portfolio risk management ahead of the next semiconductor cycle.

By Pressure Type: Gauge Sensors Lead Diverse Applications

Gauge devices contribute 46.02% share to the Mexico pressure sensors market size, valued for versatility from TPMS to industrial compressors. Differential sensors outpace the field with 8.65% CAGR, fueled by HVAC energy-saving mandates that rely on duct airflow balancing. Absolute transducers serve altitude corrections in avionics, whereas vacuum units underpin sputtering chambers at Chihuahua semiconductor back-end lines.

Future demand clusters around energy-efficiency retrofits. Smart-building integrators specify dual-port differential transmitters with BACnet over IP to fine-tune VAV boxes, directly lowering electricity spend. Agriculture startups adopt differential configurations to manage irrigation filters and avoid clogging. The Mexico pressure sensors market thus demonstrates depth across price tiers, ranging from low-cost anodized brass gauges to hermetically welded stainless units for LNG loading arms.

By Output Type: Digital Transformation Drives Adoption

Digital sensors represent 53.55% of 2025 shipments, advancing at a 8.95% CAGR powered by Industry 4.0 connectivity. I²C, SPI, and CANopen interfaces slot directly into control buses, enabling timestamped data for machine-learning diagnostics. Mexico pressure sensors market buyers migrate away from analog 4-20 mA loops except where legacy DCS infrastructure persists.

In greenhouses, LoRaWAN-enabled digital nodes broadcast pressure data every minute to cloud dashboards, supporting rule-based vent actuation. Automotive plants in Saltillo deploy EtherCAT ring networks linking up to 1,000 digital pressure points across stamping presses. Analog sensors continue in furnace atmospheres where high EMI challenges digital interfaces; however, multiplexed A/D converter modules increasingly supplement them, reducing the installed gap.

Geography Analysis

Central Mexico holds 50.65% of Mexico pressure sensors market share owing to dense automotive, electronics, and medical-device corridors serving US trade lanes. Southern Mexico and the Yucatán Peninsula expand at a 9.55% CAGR as deepwater projects mandate ruggedized subsea assemblies. Northern Mexico benefits from nearshoring, absorbing feeder-plant investment that lifts baseline sensor demand across border-adjacent value networks.

Regional government schemes direct funding toward technology parks in Tabasco and Campeche to service offshore mega-projects, enhancing downstream opportunities for calibration houses. Nuevo León’s auto-parts SMEs accelerate ISO 9001 and IATF 16949 certifications to penetrate OEM sourcing lists, widening Mexico pressure sensors market volume potential. Balanced growth across regions diversifies country-level risk.

Competitive Landscape

The Mexico pressure sensors market features moderate fragmentation. Honeywell, Sensata, and TE Connectivity headline the field, flanked by regional specialists and fledgling MEMS startups. Honeywell’s USD 37 billion 2023 revenue underscores scale advantages in industrial automation and building controls. Sensata leverages powertrain pedigree to preserve OEM contracts, whereas TE Connectivity concentrates on harsh-environment interfaces tailored to offshore and EV thermal systems.

Strategic moves focus on securing upstream silicon and expanding downstream service wraps. Bosch’s Jalisco expansion aligns R&D co-location with wafer-level packaging, squeezing time-to-market for MEMS pressure dice. TE Connectivity pilots additive-manufactured stainless sensor housings to cut weight by 30% for deepwater modules. Regional newcomers concentrate on application-specific products, such as IP68 digital sensors approved for greenhouse fertigation lines, differentiating through agile customization and local service loops. Market participants increasingly pursue ecosystem alliances—OEM-tier data-platform integration, university joint labs—to embed lock-in beyond price competition.

Mexico Pressure Sensor Industry Leaders

ABB Ltd

All Sensors Corp.

Bosch Sensortec GmbH

Endress+Hauser AG

GMS Instruments BV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: McDermott won a FEED contract with Repsol for Polok-Chinwol, covering subsea umbilicals, risers, and flowlines requiring comprehensive pressure monitoring.

- May 2024: McDermott won a FEED contract with Repsol for Polok-Chinwol, covering subsea umbilicals, risers, and flowlines requiring comprehensive pressure monitoring.

- March 2024: Quantified Sensor Technology won the GreenTech Americas challenge with wireless greenhouse sensors that lower water use, illustrating agri-innovation pull.

- February 2024: Woodside Energy selected Dril-Quip for 24 BigBore IIe subsea wellheads for the Trion field, solidifying demand for HPHT pressure sensing in Southern Mexico.

Mexico Pressure Sensor Market Report Scope

The pressure sensor detects, measures, and transmits the information, which helps analyze the performance of a device. Pressure sensors are used in numerous applications, which include medical, automotive, industrial, aerospace and defense, consumer electronics, food and beverage, HVAC, etc.

The market also covers the qualitative and quantitive performance of pressure sensors in the region. It also covers the study of the impact of Covid-19 in the market.

By Application

| Automotive |

| Medical |

| Consumer Electronics |

| Industrial |

| Aerospace and Defence |

| Food and Beverage |

| HVAC |

By Technology

| Piezoresistive |

| Capacitive |

| Resonant |

| Optical |

| MEMS |

By Pressure Type

| Absolute |

| Gauge |

| Differential |

| Vacuum |

By Output Type

| Analog |

| Digital |

By Region (Mexico)

| Northern Mexico |

| Central Mexico |

| Southern and Yucatn Peninsula |

| By Application | Automotive |

| Medical | |

| Consumer Electronics | |

| Industrial | |

| Aerospace and Defence | |

| Food and Beverage | |

| HVAC | |

| By Technology | Piezoresistive |

| Capacitive | |

| Resonant | |

| Optical | |

| MEMS | |

| By Pressure Type | Absolute |

| Gauge | |

| Differential | |

| Vacuum | |

| By Output Type | Analog |

| Digital | |

| By Region (Mexico) | Northern Mexico |

| Central Mexico | |

| Southern and Yucatn Peninsula |

Key Questions Answered in the Report

What is the current value of the Mexico pressure sensors market?

The market stands at USD 359.62 million in 2026 and is forecast to rise to USD 524.81 million by 2031.

Which application segment leads demand in Mexico?

Automotive applications lead with 37.65% market share in 2025, driven by vehicle safety mandates and powertrain controls.

Why are digital output sensors growing faster than analog versions?

Digital sensors integrate seamlessly with Industry 4.0 networks, supporting predictive maintenance and cloud analytics, which accelerates adoption at a 8.95% CAGR.

Which Mexican region shows the highest growth rate for pressure sensors?

Southern Mexico and the Yucatán Peninsula expand at a 9.55% CAGR thanks to offshore oil and gas projects and greenhouse agriculture

Page last updated on: