Market Overview

| Study Period | 2020 - 2031 |

|---|---|

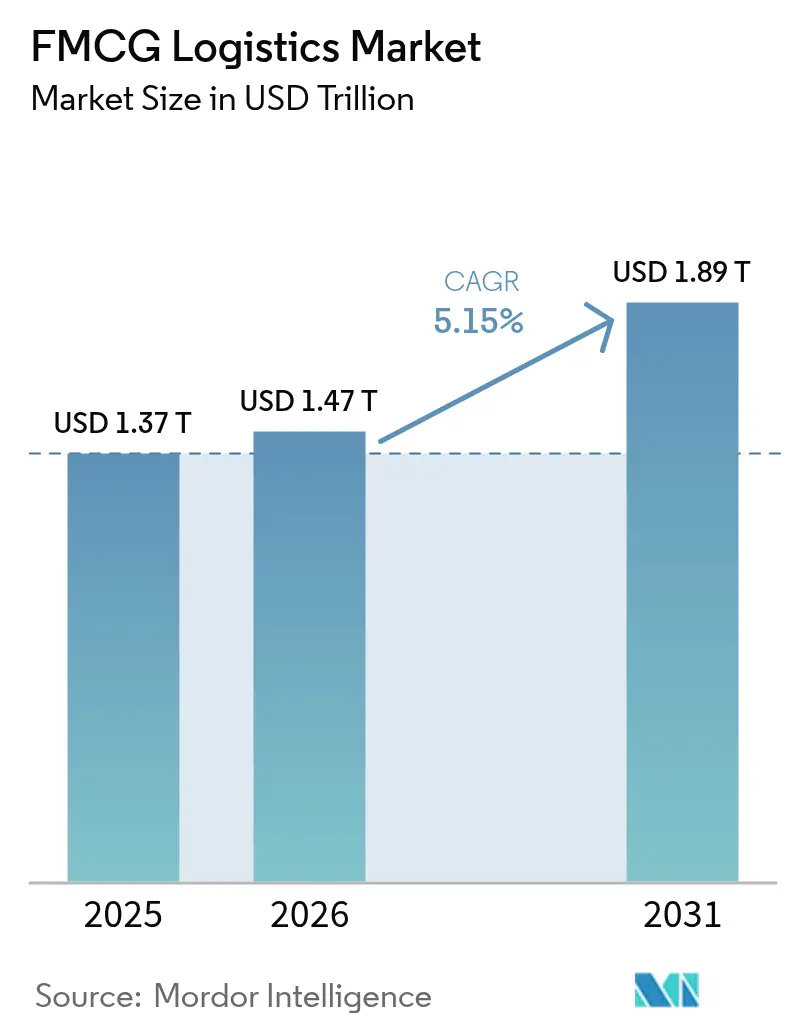

| Market Size (2026) | USD 1.47 Trillion |

| Market Size (2031) | USD 1.89 Trillion |

| Growth Rate (2026 - 2031) | 5.15% CAGR |

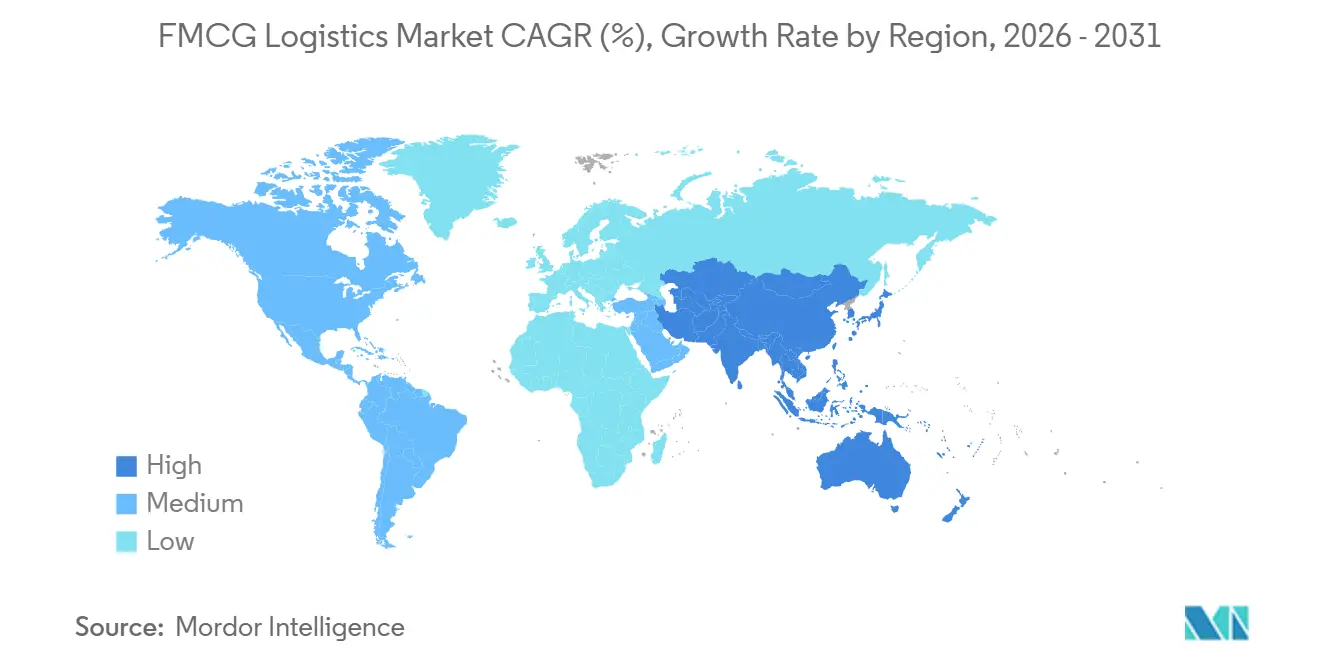

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

FMCG Logistics Market Analysis by Mordor Intelligence

The FMCG Logistics Market size is projected to be USD 1.37 trillion in 2025, USD 1.47 trillion in 2026, and reach USD 1.89 trillion by 2031, growing at a CAGR of 5.15% from 2026 to 2031.

The global FMCG logistics market is growing steadily, supported by the rapid expansion of e-commerce and increasing demand for faster replenishment cycles. Growth is reinforced by rising investments in automation and network optimization, such as Walmart retrofitting 23 distribution centers with automation to improve inventory availability and reduce cycle times, alongside regulatory initiatives like the FDA’s FSMA 204 extension, driving digital traceability adoption. While Asia-Pacific continues to dominate due to strong consumption and infrastructure expansion, the shift toward omnichannel distribution and cold-chain capacity is accelerating growth across regions. At the same time, rising service complexity and demand for speed are pushing logistics providers toward more integrated, technology-driven, and value-added solutions.

Key Report Takeaways

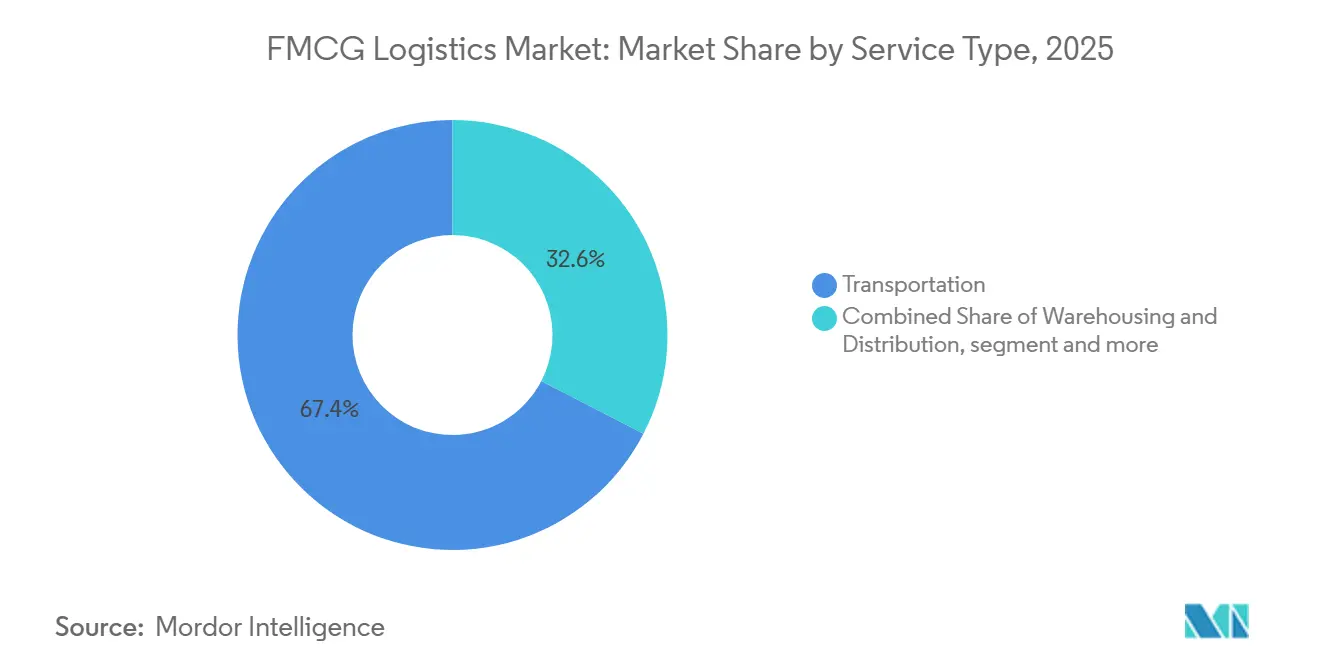

- By service, transportation led the FMCG Logistics Market share with 67.35% in 2025. Value-added services are projected to expand at a 4.8% CAGR through 2026–2031.

- By temperature control, ambient operations accounted for a 63.50% share in 2025. Frozen logistics is forecast to grow at a 5.6% CAGR through 2026-2031, enhancing the FMCG Logistics Market size.

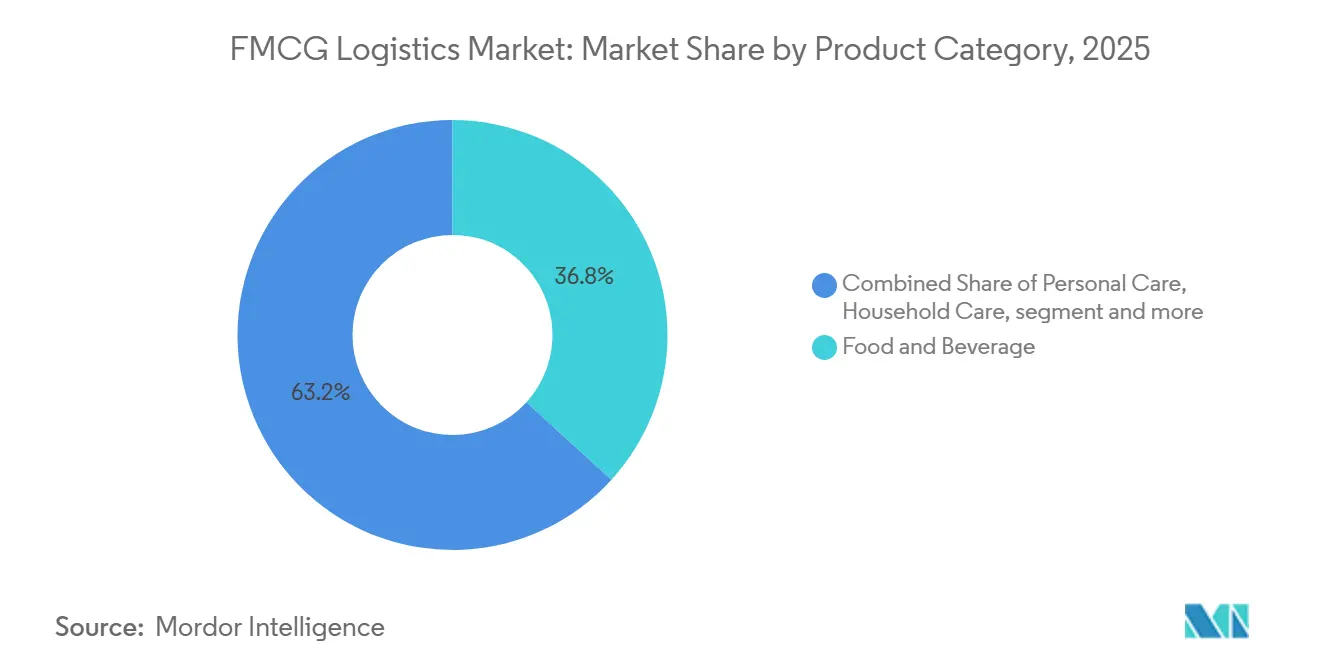

- By product category, food and beverage held a 36.75% share in 2025. OTC and healthcare are projected to advance at a 5.9% CAGR through 2026-2031.

- By distribution channel, offline networks held 69.75% of the 2025 market share. Online channels are projected to grow at a 5.1% CAGR through 2026-2031.

- By geography, Asia-Pacific leads with 37.20% of 2025 revenue and is projected to post the fastest 4.7% CAGR through 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global FMCG Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in E-Commerce FMCG Purchases and Home Delivery | +1.2% | Global, highest in Asia-Pacific and North America | Short term (≤ 2 years) |

| Growth in Modern Warehousing Across Tier-2/3 Cities | +0.8% | Asia-Pacific core, spill-over to South America and MEA | Medium term (2-4 years) |

| Strategic Collaborations Between FMCG Brands and 3PL Providers | +0.7% | Global, strong in Europe and North America, expanding in Asia-Pacific | Medium term (2-4 years) |

| Expansion of Cold Chain Infrastructure for Perishables | +0.7% | Asia-Pacific core, spill-over to South America and MEA | Medium term (2-4 years) |

| Increasing Demand for Fast Replenishment and Short Lead Times | +0.6% | Global, early adoption in North America and Europe, scaling in Asia-Pacific | Short term (≤ 2 years) |

| Rising Demand for Customized Value-Added Logistics Services | +0.5% | Global, premium uptake in North America and Europe, cost-driven in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in E-Commerce FMCG Purchases and Home Delivery

E-commerce continues to expand, boosting parcel, cross-dock, and micro-fulfillment activities in the FMCG logistics market. Amazon shipped over 9 billion same-day or next-day orders in 2025, covering 2,300+ U.S. cities, setting a high standard for grocery and household essentials delivery. Prologis anticipates e-commerce firms will dominate new warehouse leasing in 2026 as online penetration grows. The FDA's FSMA 204 compliance deadline extension to July 2028 is driving digitalization of inventory and batch tracking for high-risk items. Quick-commerce models depend on urban nodes and short-haul loops, increasing picks and tighter replenishment cycles. As these models scale, the FMCG logistics market is adding capacity in dense areas and balancing stock between regional hubs and city spokes to maintain service levels.

Increasing Demand for Fast Replenishment and Short Lead Times

Retailers and brand owners are redesigning replenishment strategies to meet next-day and same-day delivery demands in the FMCG logistics market. Walmart retrofitted 23 of its 42 regional distribution centers with automation, servicing most U.S. stores faster and improving inventory availability. Faster moves require synchronized transportation, labor-light picking, and real-time visibility to position top-moving SKUs closer to dispatch points. Forecasting and store-order orchestration now adapt to network constraints like lane reliability and hub congestion. The FMCG logistics market uses data from store traffic, weather, and promotions to optimize replenishment and reduce costly expedites. Operators combining automation with clear slotting rules report steadier pick productivity and lower shrink, especially in chilled and fresh categories.

Growth in Modern Warehousing Across Tier-2/3 Cities

Inventory is moving closer to consumers in growth corridors with favorable land and labor costs, supporting omnichannel expansion in the FMCG logistics market. Prologis expects strong development in key emerging corridors by 2026 and tight vacancy in established European nodes, indicating continued absorption of modern spaces for robotics and cold-chain fit-outs. Tier-2 and tier-3 cities offer lower capital requirements and proximity to manufacturing and consumption basins, creating buffers for peak seasons and online surges. Providers are standardizing build specifications to switch configurations between product families without extensive retrofits. The market is also adopting ISO 14001-aligned practices in new facilities, linking network contracts with sustainability targets. Investments in secondary cities are paired with route redesigns to improve service coverage and reduce last-mile cycle times.

Strategic Collaborations Between FMCG Brands and 3PL Providers

Logistics partnerships now span inbound planning to last-mile execution, simplifying accountability and enabling variable cost structures in the FMCG logistics market. Retailers and manufacturers co-design SKU assortments, slotting rules, and promotional calendars with 3PL partners to stabilize throughput and maintain high-service commitments. Agreements bundle warehousing with value-added services like kitting, customization, and returns management, reducing handoffs and compressing cycle time. Technology integration is key, with shippers demanding shared analytics for performance and emissions dashboards aligned to Scope 3 accounting. Providers demonstrating audit readiness across ISO 9001, GDP, and HACCP standards gain a competitive edge, positioning 3PLs as strategic operators and enabling brands to focus capital on growth rather than fixed logistics assets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Seasonal Demand Fluctuations and Inventory Imbalances | -0.7% | Global, highest impact where retail peaks are pronounced | Short term (≤ 2 years) |

| Infrastructure Challenges in Rural and Semi-Urban Areas | -0.6% | Asia-Pacific, South America, MEA, rural concentration | Medium term (2-4 years) |

| Limited Skilled Workforce in Warehousing and Distribution | -0.5% | North America, Europe, emerging Asia-Pacific markets | Medium term (2-4 years) |

| Congestion at Distribution Centers During Peak Periods | -0.4% | Global, concentrated at major distribution hubs in Q4 | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Infrastructure Challenges in Rural and Semi-Urban Areas

Rural routes face cost pressures due to low drop densities and long distances, limiting tight delivery windows in the FMCG logistics market. Poor infrastructure, such as road quality and cold-room availability, complicates operations outside major hubs. In Africa, cold-chain gaps and border delays increase lead times and risks, affecting freshness and on-time performance. Informal distribution and channel fragmentation hinder forecasting and reverse logistics in remote areas. Hub-and-spoke designs phase inventory through feeder towns, but higher unit costs persist for low-volume flows. Regional consolidation and shared-user facilities improve utilization, yet service variability and higher costs remain in rural zones.

Seasonal Demand Fluctuations and Inventory Imbalances

Peak seasons and promotional spikes increase order volumes and returns, straining processing capacity and transportation in the FMCG logistics market. Global events like Lunar New Year and year-end holidays compress booking windows and require earlier inventory build-up. Near-capacity carriers and facilities lead to surcharges and longer dwell times, raising logistics costs. Safety stock policies tighten, increasing holding costs and obsolescence risk for short-shelf-life products. Reverse logistics adds complexity, especially in personal care and household consumables, with higher return rates during promotions. The FMCG logistics market addresses these challenges with earlier slotting, cross-dock bypass, and alternative handoffs like parcel lockers to avoid bottlenecks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Transportation Anchors Revenue, Yet Value-Added Growth Outpaces

Transportation accounted for 67.35% of the FMCG logistics market share in 2025, driven by road, rail, sea, and air transport connecting factories to retail and consumers. Warehousing and distribution buffer seasonality and stage inventory closer to demand centers. Value-added services like co-packing, kitting, and reverse logistics are growing as brands aim to compress lead times and refresh displays. Integrated contracts combining transport and in-facility customization are preferred to protect freshness for chilled and frozen items. FDA FSMA 204 drives event-level traceability, embedding batch-tracking into warehouse and transport systems.[1]U.S. Food and Drug Administration, “Food Traceability Final Rule and Compliance Timeline,” U.S. FDA, fda.gov Pure freight brokerage faces margin pressure, while bundled solutions with value-added services sustain pricing power. Operators aligning ISO 9001 with HACCP and GDP ensure quick execution of audits and recalls. Embedded returns processing stabilizes online and quick-commerce experiences, meeting rising consumer expectations. Technology-led differentiation improves visibility, reducing detention, shrink, and errors through exception alerts and dock orchestration.

Value-added services are the fastest-growing segment with a 4.8% CAGR, offering inventory flexibility and campaign agility beyond basic warehousing and transport. The FMCG logistics market increasingly ties promotional execution to on-site capabilities, enabling seasonal bundles and retail-ready formats near ship dates. Walmart’s modernization of 23 regional DCs highlights how automation and inventory placement reduce order-to-shelf time.[2]Walmart Corporate, “How Automation Is Transforming Our Supply Chain,” Walmart, corporate.walmart.com Providers integrate ISO 14001 practices with packaging redesign to meet sustainability targets. Over time, basic transportation’s share declines as integrated operations capture incremental spend.

By Temperature Control: Cold-Chain Outpacing Ambient in Modern FMCG Networks

Ambient operations held 63.50% of the FMCG logistics market share in 2025, driven by shelf-stable foods, personal care, and household products. Chilled capacity supports dairy and fresh items, while frozen capacity handles ready-to-eat meals and premium proteins. Deep-frozen and ultra-low bands cater to specialty foods and pharmaceuticals requiring strict GDP-grade controls. IoT-based monitoring in cold-chain hubs improves energy efficiency and reduces spoilage. The cold-chain cost premium influences network density and capacity staging, especially in mature markets. The FMCG logistics market is balancing ambient dominance with growing frozen and chilled flows as consumption patterns and regulations evolve.

Frozen logistics is the fastest-growing segment, with a projected 5.6% CAGR due to rising demand for frozen meals and temperature-sensitive items. FSMA 204 drives granular traceability and electronic records adoption. Multi-client facilities like Maersk’s Olmos hub integrate IoT for real-time visibility and documentation. Providers with HACCP and GDP-compliant practices are well-positioned in healthcare and high-value food categories. Investments in temperature-controlled capacity are gradually increasing its share within the FMCG logistics market.

By Product Category: Omnichannel Healthcare and Fast-Moving Food

Food and beverage, with a 36.75% revenue share in 2025, leads the FMCG logistics market, driven by packaged foods, beverages, and shelf-stable staples. Personal care sees steady volumes through omnichannel pathways, while OTC and healthcare grow fastest at a 5.9% CAGR due to increased access and compliance frameworks. FSMA 204 boosts traceability, benefiting OTC with GDP-grade execution and serialized handling. Providers combining food safety, GDP, and value-added services are well-positioned for growth.

Category strategies in the FMCG logistics market vary by handling, compliance, and returns needs. Food and beverage require HACCP alignment and short dwell times for freshness. Personal care focuses on packaging integrity and fast cycle times, while household care prioritizes cost-efficient flows and broad retail coverage. Healthcare logistics adapts to omnichannel growth with serialized tracking and lot control. Providers excelling in cold chain and GDP-compliant handling are set to capture above-market growth.

By Distribution Channel: Offline Networks Dominate, Yet Online Expands Fastest

Offline networks accounted for 69.75% of 2025 revenue, driven by supermarkets, hypermarkets, and traditional trade, relying on direct-store delivery and cross-docking. Online channels, holding 30.25%, are growing faster due to rising home delivery demand for essentials. Quick-commerce and marketplace grocery are boosting micro-fulfillment sites, parcel lockers, and last-mile partnerships. Amazon’s same-day and next-day expansion across 2,300+ U.S. cities highlights how network density enhances service for grocery and essentials. Unified inventory and order routing are critical for omnichannel consistency, enabling stores to act as local delivery nodes.

Online growth increases picking intensity and returns, embedding value-added services and reverse logistics into contracts. The FMCG logistics market for online fulfillment grows as brands invest in near-customer nodes and improve data-sharing to reduce shrink and out-of-stocks. Retailers are automating networks to stabilize service during peaks, as seen in Walmart’s retrofit of 23 automated DCs supporting 60% of U.S. stores. AI-enabled planning and predictive routing are also improving consistency and reducing miles. As online momentum continues, the market integrates parcel, less-than-truckload, and final-mile options to meet service commitments.

Geography Analysis

Asia-Pacific led with 37.20% of 2025 revenue and is projected to grow at a 4.7% CAGR through 2031, driven by urbanization, digital payments, and marketplace adoption. Logistics investments in secondary cities improve last-mile efficiency, while cold-chain expansion supports fresh and frozen assortments. Prologis forecasts strong development in emerging markets by 2026, with tight vacancy in Europe influencing global networks.

North America modernizes its network with automation and analytics to enhance speed and availability. Walmart’s automated distribution centers now service most U.S. stores, reducing order-to-shelf time. Cross-border trade remains steady, sustaining demand for ports, rail, and warehousing. Cold-chain reinvestment addresses aging assets and tight utilization, while omnichannel grocery combines regional fulfillment with store-based pick for perishables.[3]U.S. Census Bureau, “U.S. International Trade in Goods and Services, December 2025,” U.S. Census Bureau, census.gov

Europe faces moderate growth due to mature retail, regulatory complexity, and tight vacancy in core hubs. Prologis anticipates a sub-5% vacancy in 2026, requiring long-term site planning. Sustainability efforts focus on EV fleets, renewable-powered warehouses, and green certifications. South America adds modern facilities for perishables and exports, while the Middle East and Africa show potential in urban hubs but face infrastructure challenges in trade corridors. Globally, the FMCG logistics market emphasizes ISO 9001, HACCP, GDP, and ISO 14001 for standardized operations.

Competitive Landscape

The FMCG logistics market features global integrators, regional specialists, and tech-focused providers competing on network breadth, sector depth, and digital capabilities. Global players combine contract logistics, freight forwarding, and last-mile options, while regional specialists excel in niches like cold chain or reverse logistics. Strategic priorities include warehouse automation, data visibility, and emissions accounting. Walmart’s automation across 23 DCs highlights how shippers align technology to improve availability. Prologis anticipates strong demand for modern space in 2026, benefiting 3PLs securing early capacity in tight markets.

Technology adoption drives competition as shippers prioritize analytics, AI, and real-time visibility. FedEx reports high AI adoption for route optimization, while Amazon’s rapid delivery scale raises expectations for speed and coverage. Providers with control towers and digital proof-of-delivery reduce exceptions and shrink. The market emphasizes HACCP and GDP compliance, especially for products with strict regulations.

Cold-chain capability is critical due to rising frozen and chilled demand. High infrastructure costs favor operators sharing capacity and using smart energy systems. New hubs like Olmos, Peru, reduce spoilage and improve reliability for perishables. Sustainability is now essential, with ISO 14001 practices and emissions tracking becoming standard. The FMCG logistics market values providers blending sector expertise, multi-node reach, and value-added services for cost efficiency and service excellence.

FMCG Logistics Industry Leaders

DHL Group

Kuehne + Nagel

DSV

C.H. Robinson

Ceva Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: The U.S. FDA extended the compliance deadline for the Food Traceability Rule (FSMA 204) from January 20, 2026, to July 20, 2028, granting logistics providers and food manufacturers additional time to implement electronic traceability systems for designated high-risk items, including shell eggs, soft cheeses, and finfish.

- December 2025: Target unveiled AI-powered inventory-management system upgrades across its fulfillment network, projecting a reduction in stockouts during peak promotional periods and improving next-day delivery coverage to top metros.

- September 2025: Walmart disclosed that 60% of its U.S. stores are now serviced by automated distribution centers, with 23 of 42 regional DCs retrofitted with robotics and conveyor systems that reduce order-to-shelf cycle times by approximately 30%.

- July 2025: Maersk opened an advanced cold-chain hub in Olmos, Peru, featuring solar-powered refrigeration and IoT-enabled monitoring to address high spoilage rates in the absence of adequate cold-chain infrastructure, with the facility designed to handle significant fresh-produce volumes.

Global FMCG Logistics Market Report Scope

The FMCG Logistics Market Report is Segmented by Service (Transportation, Warehousing & Distribution, Value-Added Services), by Temperature Control (Chilled, Frozen, and More), by Product Category (Food and Beverage, Personal Care, and More), by Distribution Channel (Online, Offline), and by Geography (North America, South America, Asia-Pacific, Europe, Middle East and Africa). Market Forecasts are Provided in Terms of Value (USD).

By Service (Value)

| Transportation | Road |

| Rail | |

| Air | |

| Sea | |

| Warehousing and Distribution | |

| Value-added Services and Others |

By Temperature Control (Value)

| Chilled (0-5 °C) |

| Frozen (-18-0°C) |

| Ambient |

| Deep-Frozen /Ultra-Low (less than-20 °C) |

By Product Category (Value)

| Food and Beverage |

| Personal Care |

| Household Care |

| OTC and Healthcare |

| Others |

By Distribution Channel (Value)

| Online |

| Offline |

By Geography (Value)

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Middle East and Africa | United Arab of Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East And Africa |

| By Service (Value) | Transportation | Road |

| Rail | ||

| Air | ||

| Sea | ||

| Warehousing and Distribution | ||

| Value-added Services and Others | ||

| By Temperature Control (Value) | Chilled (0-5 °C) | |

| Frozen (-18-0°C) | ||

| Ambient | ||

| Deep-Frozen /Ultra-Low (less than-20 °C) | ||

| By Product Category (Value) | Food and Beverage | |

| Personal Care | ||

| Household Care | ||

| OTC and Healthcare | ||

| Others | ||

| By Distribution Channel (Value) | Online | |

| Offline | ||

| By Geography (Value) | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Middle East and Africa | United Arab of Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East And Africa | ||

Key Questions Answered in the Report

What is the current size of the FMCG logistics market, and how fast is it growing?

The FMCG logistics market size was USD 1.37 trillion in 2025 and is projected to reach USD 1.89 trillion by 2031 at a 5.1% CAGR.

Which service segment leads in the FMCG logistics market?

Transportation leads and held 67.35% of 2025 revenue, while value-added services are the fastest-growing as brands pursue agility and shorter cycle times.

Which temperature-control segment is growing fastest within the FMCG logistics market?

Frozen logistics is the fastest-growing, with a projected 5.6% CAGR through 2031 as demand rises for frozen foods and temperature-sensitive items.

Which region holds the largest share of the FMCG logistics market?

Asia-Pacific leads with 37.20% of 2025 revenue and is projected to post the fastest 4.7% CAGR through 2031 as network coverage deepens in secondary cities.

How is e-commerce influencing the FMCG logistics market?

E-commerce is lifting parcel and micro-fulfillment volumes as next-day and same-day expectations expand, supported by rapid-delivery networks and traceability mandates.

What are the key compliance frameworks shaping the FMCG logistics market?

Common frameworks include ISO 9001, ISO 14001, HACCP, ISO 22000, GDP for pharmaceuticals, and FDA FSMA 204 traceability, which guide safety, quality, and environmental performance.

Page last updated on: