Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

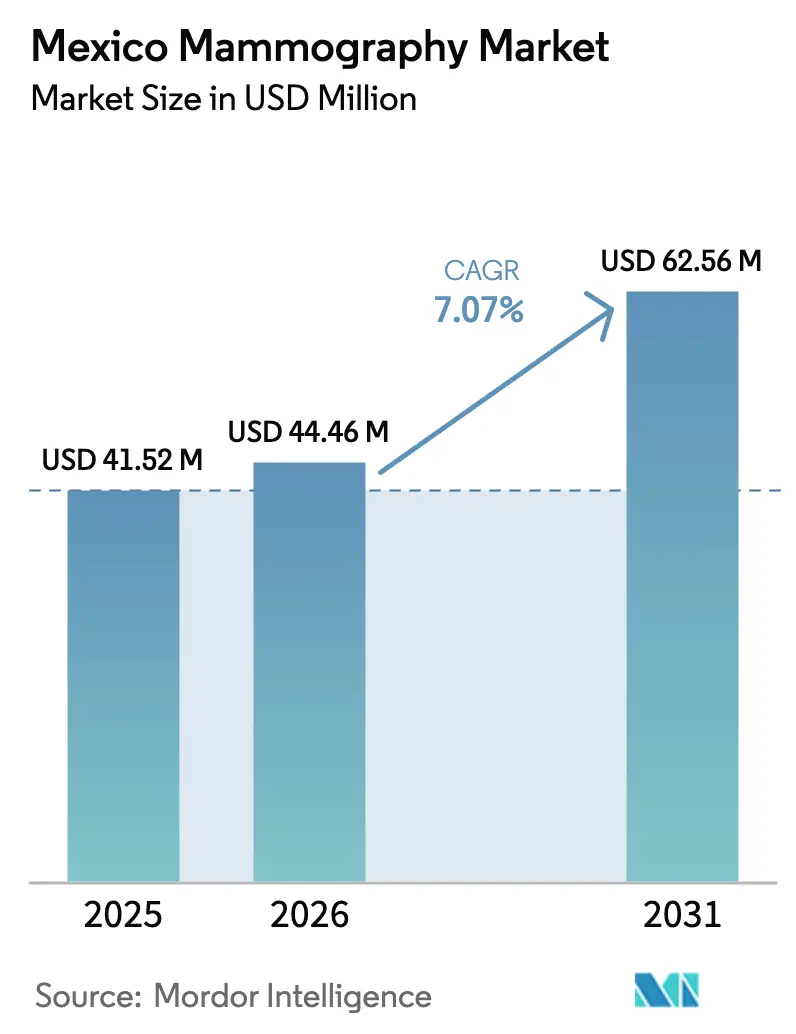

| Base Year Market Size (2025) | USD 41.52 Million |

| Market Size (2026) | USD 44.46 Million |

| Market Size (2031) | USD 62.56 Million |

| Growth Rate (2026 - 2031) | 7.07% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Mammography Market Analysis by Mordor Intelligence

Mexico mammography market size in 2026 is estimated at USD 44.46 million, growing from 2025 value of USD 41.52 million with 2031 projections showing USD 62.56 million, growing at 7.07% CAGR over 2026-2031. A strong export-oriented medical-device ecosystem, the country’s position as the world’s eighth-largest device manufacturer, and more than 150,000 sector jobs collectively underpin demand for advanced breast-imaging solutions. Digital penetration accelerates because analog replacement cycles coincide with government procurement of full-field digital units for the vast IMSS-BIENESTAR hospital network, which manages over 10,500 primary health establishments and 576 hospitals across 23 states. Meanwhile, cross-border medical tourism from Central America funnels additional screening patients to northern clinics, and mobile units extend services to rural communities that lack resident radiologists. Artificial-intelligence integration remains nascent—only 9% of physicians currently employ AI tools—yet high-profile deployments such as Lunit’s roll-out across Salud Digna’s 230-plus sites point to wider adoption through 2030. Simultaneously, COFECE’s investigation into alleged cartel behavior in radiological equipment introduces pricing uncertainty that may reshape tender dynamics and spur new entrants.

Key Report Takeaways

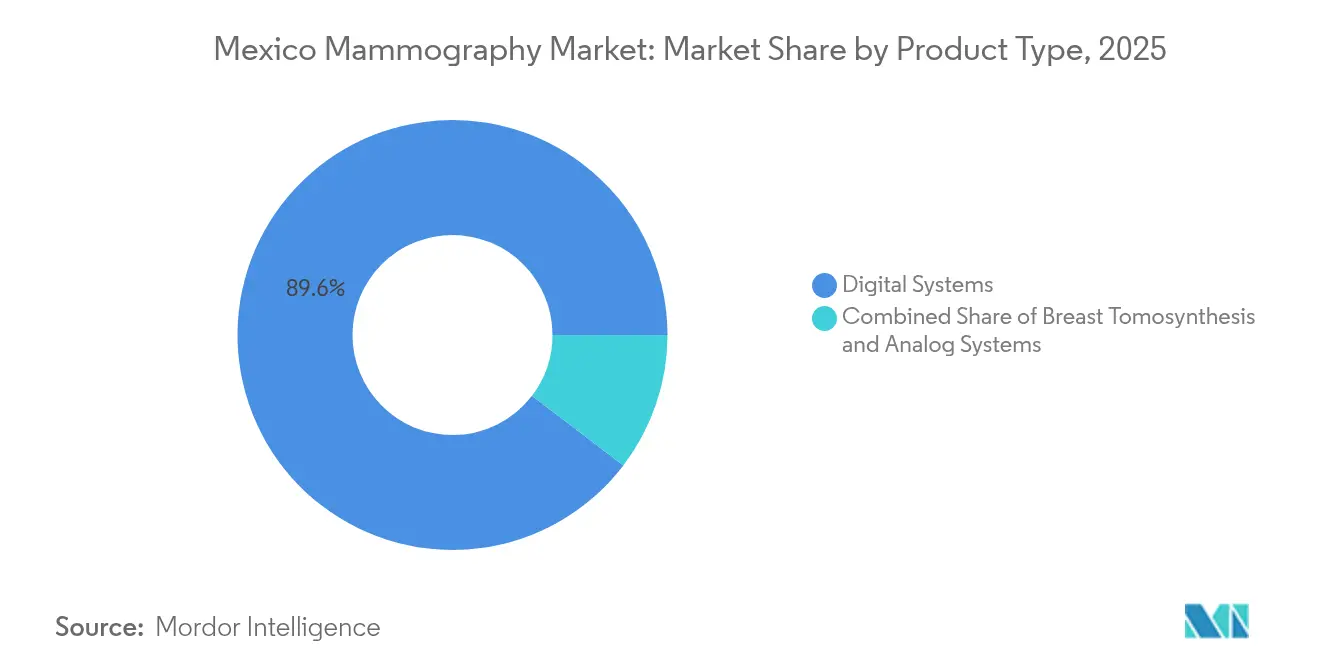

- By product type, digital systems captured 89.62% Mexico mammography market share in 2025 while breast tomosynthesis is advancing at an 7.78% CAGR through 2031.

- By technology, 2-D platforms accounted for 54.02% of the Mexico mammography market size in 2025 whereas 3-D mammography leads growth at 7.64% CAGR to 2031.

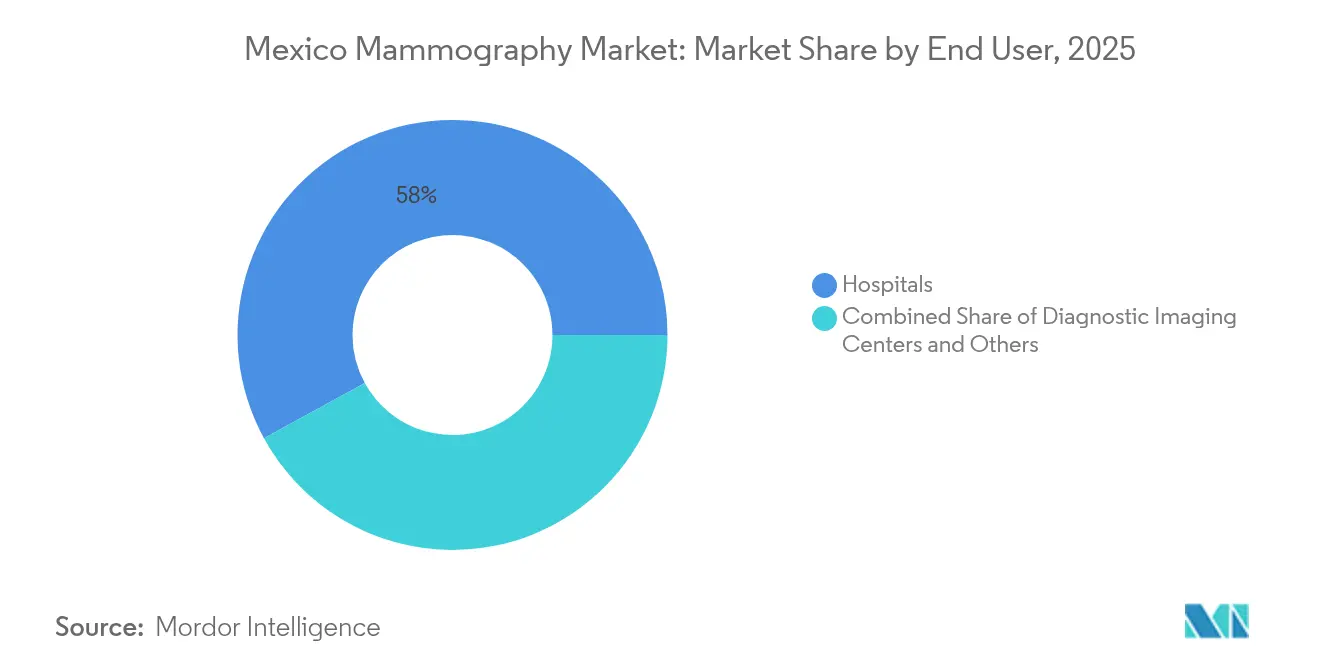

- By end user, hospitals held 57.98% Mexico mammography market share in 2025; diagnostic imaging centers record the highest projected CAGR at 7.95% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Mammography Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence Of Breast Cancer Among Women ≥40 Years | +1.8% | National, concentrated in urban centers | Long term (≥ 4 years) |

| Rapid Replacement Of Analog By Full-Field Digital Systems | +1.1% | National, prioritizing public hospitals | Medium term (2-4 years) |

| Government's Expanding Mobile-Screening Programs | +1.2% | Rural states, northern border regions | Medium term (2-4 years) |

| Private-Sector Investment In AI-Powered Workflow Tools | +1.5% | Mexico City, Guadalajara, Monterrey metropolitan areas | Medium term (2-4 years) |

| Growing Availability Of CESM For Under-Served Dense-Breast Cohorts | +0.9% | Major urban hospitals, specialized imaging centers | Long term (≥ 4 years) |

| Cross-Border Medical Tourism From Central America | +0.6% | Northern border states, major metropolitan areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence Of Breast Cancer Among Women ≥40 Years

Nationwide demographic shifts elevate the screening pool as age-period-cohort analyses reveal mortality increases beyond earlier projections, stimulating continuous demand for diagnostic capacity. Multidisciplinary treatment guidelines that now require genetic counselors intensify imaging needs for precise staging and surveillance. Survival disparities surface between states, with Guerrero registering 73% five-year survival despite high poverty, whereas younger women post poorer outcomes, underscoring the necessity for broader age inclusion in regular screening. Indigenous Otomí women cite cultural norms and discrimination as core barriers, confirming the importance of culturally sensitive outreach. The phased termination of welfare programs such as Prospera reduced subsidized care, encouraging private providers to design alternative access pathways. Regulatory standard NOM-229-SSA1-2002 ensures radiation safety compliance across expanding screening sites[1]COFEPRIS, “COFEPRIS-05-024-A,” catalogonacional.gob.mx .

Rapid Replacement Of Analog By Full-Field Digital Systems

Analog units persist mainly in rural outposts; nevertheless, economic evaluations confirm digital systems’ superior lifetime cost-effectiveness when throughput exceeds 3,000 exams yearly, catalyzing systemic upgrades. Government tenders for consumables point to sustained operating budgets even where capital constraints slow replacement. Foreign direct investment of USD 126 million in 2022 expanded financing options for private clinics upgrading to digital suites. COFEPRIS labeling mandates under NOM-137-SSA1-2008 amplify confidence in imported detectors. Combined, these factors accelerate the Mexico mammography market’s digital transformation trajectory.

Government's Expanding Mobile-Screening Programs

State health authorities deploy mobile caravans such as Michoacán’s free unit visits to remote municipalities, closing physical-distance gaps and driving episodic demand spikes. Private-public collaborations like ADO’s 32% expansion of the Caravana Rosa widen outreach logistics. Fujifilm’s training hubs enhance technologist skills, increasing utilization of installed units. Federal coordination agreements guarantee budget transfers that underpin free exams in underserved zones. AI-enabled portable devices under evaluation promise workflow efficiencies, though evidence from Latin American settings remains limited.

Private-Sector Investment In AI-Powered Workflow Tools

Lunit’s partnership with Salud Digna introduces Insight MMG algorithms over a 10-million-image dataset, positioning Mexico as Latin America’s largest AI mammography incubator. Domestic developer HERA-MI’s Breast-Slim View screens positioning quality and density metrics, supporting quality assurance protocols. Grupo RIO’s adoption of deepc’s platform illustrates aggregator models that bundle over 70 AI applications within a unified PACS interface. Cost–utility studies predict AI-human task sharing can cut screening program costs by up to 30.1%, provided false-positive management remains controlled. Physician adoption lags due to infrastructure and training gaps, but industry partnerships with academic centers aim to close skill deficits.

Growing Availability Of CESM For Dense-Breast Cohorts

Contrast-enhanced spectral mammography offers higher contrast-to-noise ratios for malignant lesions versus conventional imaging, improving detection in dense tissue. Validation of the Mirai risk-prediction model in Mexican clinics achieved a C-index of 0.63, informing stratified screening that channels high-risk women toward CESM. Technical assessments confirm malignant tumors exhibit distinct enhancement patterns, enabling earlier intervention. Brazilian cost-effectiveness evidence for tomosynthesis plus synthetic views supports regional transferability of combined CESM–DBT workflows. Implementation challenges center on contrast agents and training, yet high-risk population benefits justify capital outlays for referral centers.

Restraints Impact Analysis*

| Restraint | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost For 3-D/DBT Units In Public Hospitals | -1.3% | National public health system, rural hospitals | Long term (≥ 4 years) |

| Limited Number Of Certified Radiologists In Rural States | -0.8% | Northern and southern border states, rural municipalities | Medium term (2-4 years) |

| Risk Of Radiation Over-Exposure In Opportunistic Screening | -0.5% | National, particularly unregulated private facilities | Medium term (2-4 years) |

| Fragmented Reimbursement Rules Between IMSS, ISSSTE & Private Payors | -0.7% | National, affecting all healthcare sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost For 3-D/DBT Units In Public Hospitals

Economic analyses calculate an additional 5.4 million peso investment for each DBT system versus computed radiography units, straining public budgets despite available operating funds. The domestic device market valued at USD 15.6 billion in 2023 expands at 8.3% CAGR in local currency, which encourages vendor financing yet tender complexity delays roll-outs. IMSS purchases of consumables show utilization growth even where new-equipment procurement stalls [2]Diario Oficial de la Federación, “Acuerdo de Coordinación,” dof.gob.mx . Retrofittable flat-panel detectors like the RSM-2430C provide interim digitalization options. Cross-border leasing and vendor-managed inventory agreements emerge as alternative pathways for capital-constrained facilities.

Limited Number Of Certified Radiologists In Rural States

Workflow bottlenecks persist because 80% of hospitals still rely on outdated archiving systems that extend reading queues. Physician surveys note delays exceeding 90 days for breast-cancer care in 18% of public hospitals, with many clinicians unaware of standardized referral protocols. Fujifilm’s technology centers supply modular training, yet scaling remains insufficient for nationwide coverage. AI triage tools such as Eden Creator promise workload mitigation, though rural bandwidth constraints impede cloud-based model deployment. Regional collaboration with the Pan American Health Organization advocates tele-radiology hubs to pool expertise across Latin America.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Digital Dominance Accelerates Tomosynthesis Adoption

Digital systems led the Mexico mammography market size for product type at USD 37.21 million in 2025, translating to a 89.62% share. Analog units remain in legacy public clinics yet decline swiftly as budget allocations prioritize image-quality gains and workflow integration. The Mexico mammography market benefits from detector innovations such as Fujifilm’s direct-conversion selenium panels that deliver full-resolution previews in 10 seconds, improving daily throughput. Retrofit panels like Rose-M permit cost-efficient digital migration, sustaining digital share growth. Breast tomosynthesis, either as stand-alone or upgrade kits, gains successive tender wins because clinical evidence shows superior detection for architectural distortions, supporting its 7.78% CAGR trajectory. Vendors bundle extended warranties, software‐upgrade pathways, and technologist training to justify higher acquisition prices. Demand tails in analog peripherals signal an imminent shift where secondary resale markets absorb decommissioned units, further consolidating digital primacy. Overall, the Mexico mammography market expects digital equipment revenues to surpass USD 53.47 million by 2031 as analog installs fall below 2% of total inventory.

Second-generation DBT systems create differentiated value propositions in high-volume imaging centers where reimbursement differentials offset capital costs. Innovative detector materials reduce dose while maintaining resolution, reinforcing physician confidence amid patient safety priorities. Hybrid product lines that support synthetic 2-D reconstruction enable facilities to meet screening guidelines without additional exposures, aligning with NOM-012-NUCL-2016 radiation requirements. Vendor-hosted PACS packages, inclusive of AI licences, bolster arguments for comprehensive digital system procurement. Consequently, digital platforms remain the cornerstone of Mexico mammography market revenue, with tomosynthesis leading performance-driven adoption curves.

By Technology: 3-D Innovation Challenges 2-D Incumbency

Technology segmentation shows 2-D platforms contributing USD 22.43 million for a 54.02% share of Mexico mammography market size in 2025, but growth moderates as 3-D systems advance at 7.64% CAGR. Siemens Healthineers’ Mammomat B.brilliant improves abnormality detection while cutting scan time by 35%, demonstrating dual emphasis on clinical efficacy and patient comfort. Healthcare providers adopt phased strategies, integrating synthetic 2-D from 3-D datasets to minimize per-exam radiation. CAD and AI-assisted modules overlay decision support, reducing reading times and false positives. Regulatory alignment with NOM-229 ensures dose-tracking logs, which strengthens quality management compliance.

Contrasted against entrenched 2-D fleets, 3-D units command premium pricing yet secure reimbursement in private insurance policies, promoting wider penetration in urban centers. Deployment of cloud-based AI models linked to 3-D datasets enhances clinical value, encouraging tele-diagnostic collaboration that compensates for radiologist shortages. CESM complements 3-D modalities in dense-breast cohorts, fostering a multi-technology ecosystem that maximizes detection accuracy across patient profiles. As a result, 3-D’s revenue contribution is projected to nearly equal 2-D by 2030, redefining the competitive playing field within the Mexico mammography market.

By End User: Imaging Centers Capitalize On Hospital Constraints

Hospitals generated USD 24.07 million, equal to 57.98% Mexico mammography market share in 2025, reflecting the state network’s breadth. Nonetheless, diagnostic imaging centers exhibit 7.95% CAGR due to shorter appointment windows and bundled value-added services. Private centers such as CMQ Hospital deploy advanced screening suites in tourism corridors like Riviera Nayarit, tapping expatriate and traveling patient segments. Established specialists like CEDIMMONT leverage two-decade reputations to attract local referrals within Yucatán.

Fragmented reimbursement between IMSS, ISSSTE, and private payors burdens hospital billing workflows, driving some beneficiaries to pay-per-service imaging centers for faster diagnostics. Centers differentiate through extended operating hours, AI-augmented reporting, and ancillary ultrasound or biopsy on the same visit. Mobile-unit operators enter employer wellness programs, offering on-site screening for maquiladora workforces, thereby broadening the other-users segment. Collectively, the end-user mix evolves toward a hybrid service landscape that balances public hospital capacity with agile private offerings, sustaining diversified demand across the Mexico mammography market.

Geography Analysis

Regional dispersion creates distinct procurement patterns. Northern border states leverage cross-border medical tourism, which supplies cash patients to private clinics equipped with advanced 3-D systems that align with United States screening standards. Proximity to U.S. distributors reduces delivery lead times for spare parts, strengthening uptime for high-throughput centers. Mid-continent urban clusters—Mexico City, Guadalajara, and Monterrey—concentrate tertiary hospitals and academic research hubs that pilot AI algorithms under vendor-academic collaborations, spurring early adoption curves. Metropolitan density also supports CESM adoption where dense-breast prevalence intersects with higher socioeconomic levels.

In contrast, southern and mountainous states confront limited road connectivity and low specialist density. Mobile units fill this gap, supported by federal resource-transfer agreements and state outreach campaigns that schedule rotating visits to remote municipalities. Indigenous regions require culturally tailored awareness messaging; bilingual technologists improve attendance among Otomí, Mixe, and Zapotec communities. Geography influences reimbursement complexities, as cross-state referrals often trigger insurance pre-authorization hurdles that dampen demand in border areas of Chiapas and Oaxaca.

Central states like Jalisco enjoy greater fiscal autonomy after the 2019 health-system reforms, enabling flexible equipment purchases responsive to local epidemiology . This empowerment fosters competitive bidding that includes emerging AI-enabled vendors, further diversifying the supplier base. Overall, geographic heterogeneity demands multi-pronged strategies ranging from high-tech urban centers with integrated AI worklists to resource-optimized mobile caravans in sparsely populated districts, ensuring Mexico mammography market growth remains inclusive.

Competitive Landscape

Global manufacturers—Hologic, GE HealthCare, Siemens Healthineers, and Fujifilm—anchor the market with comprehensive portfolios, local service teams, and compliance readiness under NOM-241-SSA1-2025 quality-system mandates. AI specialists such as Lunit, HERA-MI, and deepc cultivate strategic partnerships to embed decision-support software inside multivendor PACS environments, differentiating on algorithm accuracy and cloud-scalability. Domestic innovators exploit familiarity with COFEPRIS processes, tailoring interfaces and documentation to Spanish-speaking radiologists.

COFECE’s ongoing cartel investigation heightens scrutiny over public-tender pricing, potentially leveling the playing field for mid-size entrants. Vendor responses include transparent cost-breakdowns and expanded training packages to demonstrate value beyond initial price tags. White-space remains in rural deployment where leasing models, portable detectors, and mobile configurations offer scalable penetration paths. Strategic moves in 2024-2025 include Lunit’s Latin America–wide AI roll-out with Salud Digna and Siemens’ FDA-cleared Mammomat B.brilliant marketing push, illustrating technology-plus-service integration as a winning formula.

Competitive intensity also manifests in after-sales support. Companies open regional parts depots and training academies to meet uptime SLAs demanded by large diagnostic chains. Platform ecosystems emerge, where equipment, AI plug-ins, and tele-radiology modules interoperate, enhancing switching costs for clients. Overall, the Mexico mammography market tilts toward moderate concentration as leading players defend share through bundled offerings while agile AI start-ups capture niche segments, balancing consolidation with innovation.

Mexico Mammography Industry Leaders

Siemens AG

Hologic Inc.

GE Healthcare

Planmed OY

Fujifilm Holdings Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Lunit will deploy Insight CXR and Insight MMG across Salud Digna’s network of over 230 clinics in Mexico and Central America.

- September 2024: Medical Scientific and CARCAL supply breakthrough mammography technology to FUCAM, one of Latin America’s most prominent breast-cancer centers.

- May 2023: Johnson & Johnson Impact Ventures invests in Mamotest to expand digital screening access for Latin American women.

Mexico Mammography Market Report Scope

As per the scope of the report, mammography refers to a standard diagnostic and screening technique that is used to screen breast tissues to check the presence of a malignant tumor. The process involves the usage of low-energy X-rays for the early detection of breast cancer. Mexico Mammography Market is segmented by Product Type (Digital Systems, Analog Systems, Breast Tomosynthesis, and Other Product Types), End Users (Hospitals, Specialty Clinics, and Diagnostic Centers). The report offers the value (in USD million) for the above segments.

By Product Type

| Digital Systems |

| Analog Systems |

| Breast Tomosynthesis (Stand-alone) |

By Technology

| 2-D Mammography |

| 3-D Mammography |

| CAD & AI-Assisted Mammography |

By End User

| Hospitals |

| Diagnostic Imaging Centers |

| Others |

| By Product Type | Digital Systems |

| Analog Systems | |

| Breast Tomosynthesis (Stand-alone) | |

| By Technology | 2-D Mammography |

| 3-D Mammography | |

| CAD & AI-Assisted Mammography | |

| By End User | Hospitals |

| Diagnostic Imaging Centers | |

| Others |

Key Questions Answered in the Report

How big is the Mexico Mammography Market?

The Mexico Mammography Market size is expected to reach USD 44.46 million in 2026 and grow at a CAGR of 7.07% to reach USD 62.56 million by 2031.

Which product category dominates sales?

Digital mammography systems account for 89.62% of 2025 revenue thanks to their superior image quality and integration features.

Who are the key players in Mexico Mammography Market?

Siemens AG, Hologic Inc., GE Healthcare, Planmed OY and Fujifilm Holdings Corporation are the major companies operating in the Mexico Mammography Market.

How fast is breast tomosynthesis growing?

Breast tomosynthesis is expanding at an 7.78% CAGR, the fastest among product categories, propelled by better detection of subtle lesions.

Page last updated on: