Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

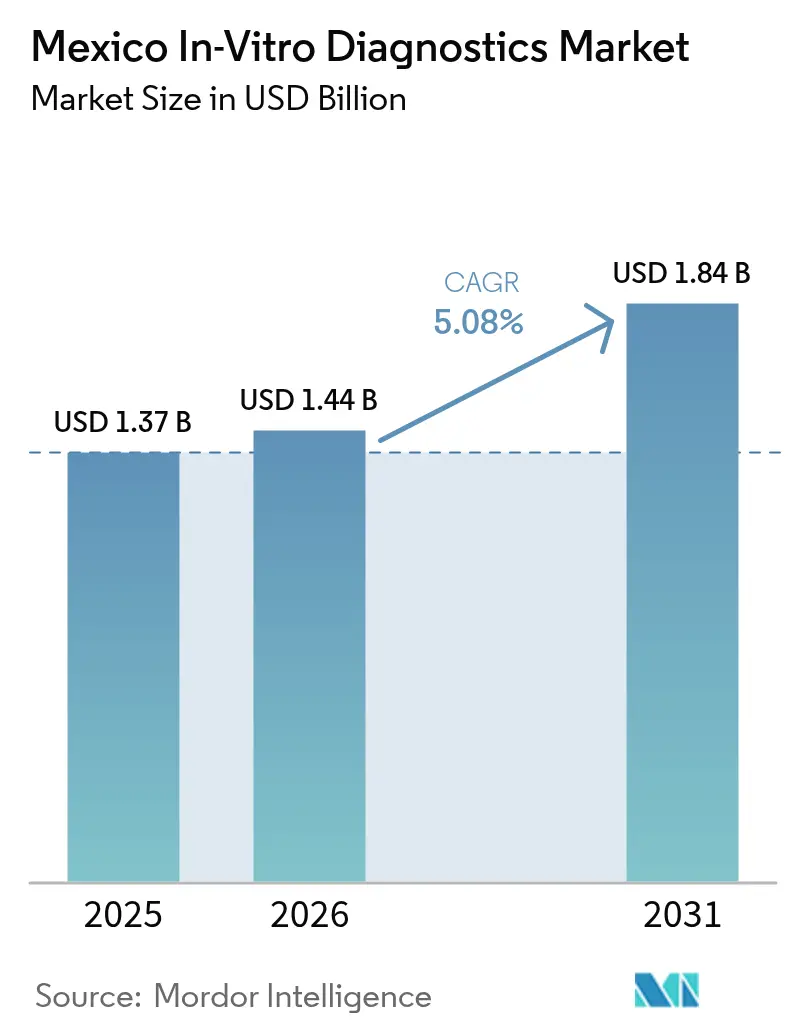

| Base Year Market Size (2025) | USD 1.37 Billion |

| Market Size (2026) | USD 1.44 Billion |

| Market Size (2031) | USD 1.84 Billion |

| Growth Rate (2026 - 2031) | 5.08% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico In-Vitro Diagnostics Market Analysis by Mordor Intelligence

The Mexico In-Vitro Diagnostics Market size was valued at USD 1.37 billion in 2025 and estimated to grow from USD 1.44 billion in 2026 to reach USD 1.84 billion by 2031, at a CAGR of 5.08% during the forecast period (2026-2031).

Regulatory convergence via the 30-day equivalency route is streamlining launch cycles for multinational suppliers, driving consolidated public tenders toward companies with FDA 510(k) or CE Mark approvals. Centralized federal procurement through BIRMEX is reducing reagent prices while enabling volume-based contracts that prioritize closed-system platforms. Nearshoring initiatives in Querétaro and Baja California are attracting new investments in medical devices, though the majority of funding continues to focus on cardiovascular hardware rather than core diagnostic consumables. Additionally, the adoption of AI-ready laboratory information systems, fueled by NOM-240-SSA1-2024 technovigilance regulations, is creating a high-growth opportunity in the software and services segment within Mexico's in-vitro diagnostics market.

Key Report Takeaways

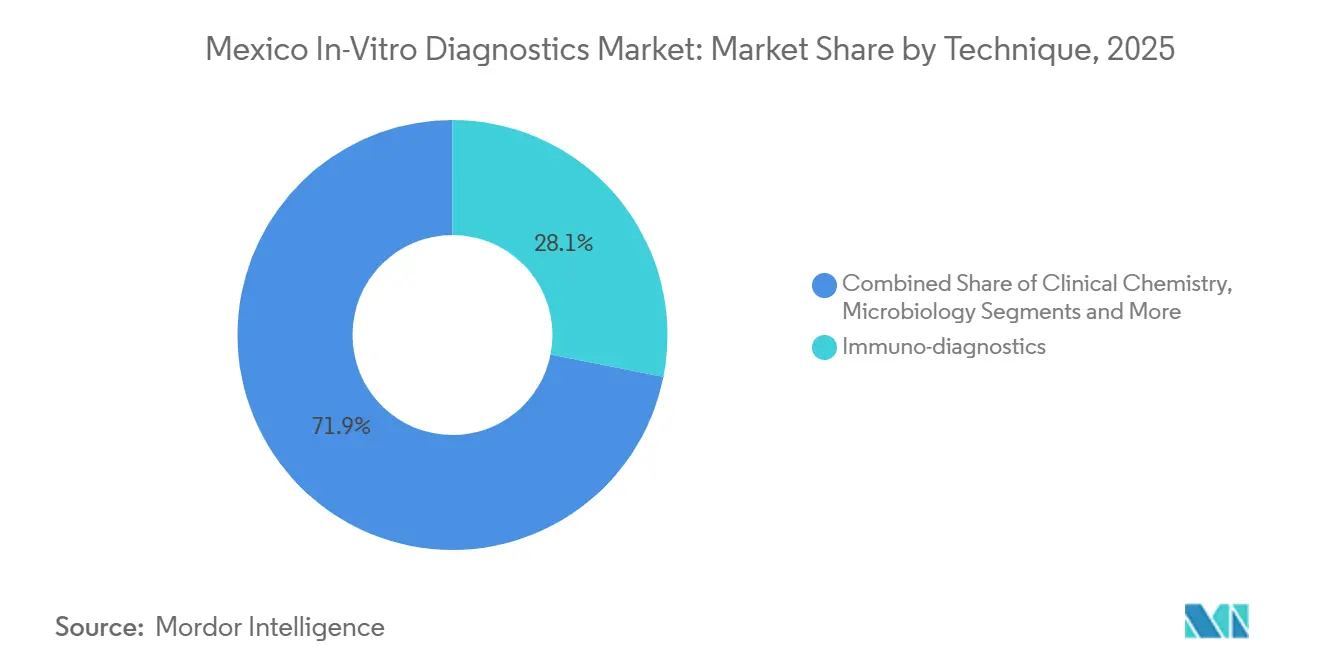

- By test type, Immuno-Diagnostics held 28.11% of 2025 revenue, while Molecular Diagnostics is projected to expand at a 7.65% CAGR from 2026 to 2031.

- By product category, Reagents & Kits captured 54.88% of the 2025 total; Software & Services is expected to post the quickest rise at an 8.32% CAGR through 2031.

- By usability, Disposable IVD Devices commanded 57.08% of 2025 sales, whereas Re-Usable Equipment is forecast to grow at a 7.83% CAGR between 2026 and 2031.

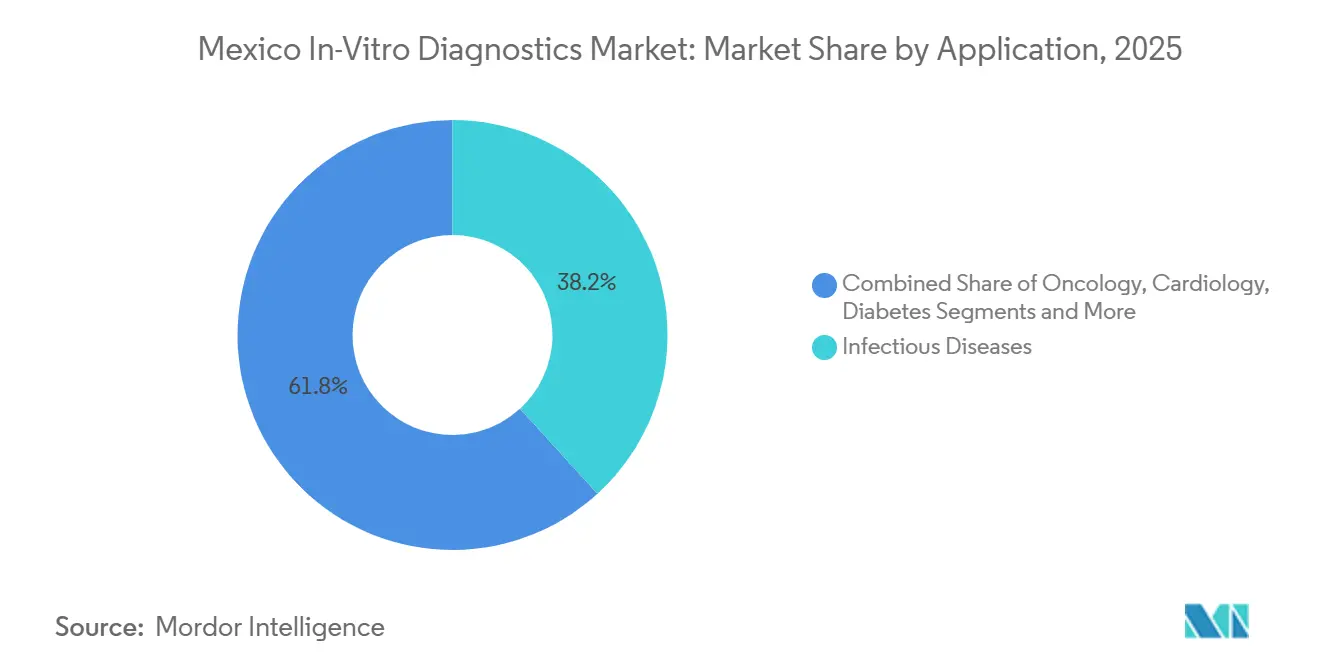

- By application, Infectious Diseases generated 38.21% of 2025 revenue; Oncology testing is on track to increase at an 8.54% CAGR over 2026-2031.

- By end user, Hospital-Based Laboratories accounted for 38.15% of 2025 demand, and Home-Care & Self-Testing Users are set to advance at a 6.54% CAGR during the same forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico In-Vitro Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence Of Chronic And Infectious Diseases | +1.2% | National, highest burden in Estado de México, Jalisco, Veracruz | Medium term (2-4 years) |

| Growing Penetration Of Point-Of-Care Testing Across Rural Areas | +0.8% | National, early gains in Estado de México, Colima, Veracruz via IMSS Bienestar | Short term (≤ 2 years) |

| Expansion Of Public Healthcare Funding And Insurance Coverage | +0.9% | National, concentrated in federal procurement via BIRMEX | Medium term (2-4 years) |

| Accelerated Regulatory Approvals Via COFEPRIS Fast-Track Pathway | +0.6% | National, benefits FDA/CE/PMDA-cleared products | Short term (≤ 2 years) |

| Increasing Localization Of IVD Manufacturing Under Near-Shoring | +0.5% | Querétaro, Baja California, Ciudad Juárez | Long term (≥ 4 years) |

| Technological Advancements In High-Throughput And Digital Diagnostics | +0.7% | Mexico City, Monterrey, Guadalajara | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic and Infectious Diseases

Mexico’s 73.4% adult overweight rate, 11.2% diabetes prevalence, and continuing tuberculosis and HIV incidence enlarge routine screening demand within the Mexico in-vitro diagnostics market[1]World Health Organization, “Mexico Noncommunicable Disease Profile 2025,” who.int. Diabetes alone generated a domestic glucose testing spend that surpassed USD 41 million in 2024 and is slated to reach USD 51 million by 2030, much of it through retail pharmacy strips purchased by informal-sector workers. Infectious diseases remained the largest application, accounting for 38.21% of revenue in 2025, yet the epidemiological shift toward non-communicable disorders is accelerating the uptake of oncology and cardiology panels. The Pediatric ALL Bridge Project demonstrated that a hub-and-spoke model can move 600+ molecular specimens nationally within budget constraints, suggesting broader scalability if federal oncology budgets rise. Still, a median 113-day diagnosis lag signals that laboratory capacity must grow in parallel with test menu expansion to capture the full potential of the Mexican in-vitro diagnostics market.

Growing Penetration of Point-Of-Care Testing Across Rural Areas

IMSS Bienestar’s “La Muestra Viaja” began in 2025 by shuttling samples from 606 clinics to 11 regional labs, serving 9 million uninsured residents and expanding to Colima, Veracruz, and Mexico City within 4 months. The model circumvents the capital burden of installing analyzers at every rural site, rewarding reagent suppliers that provide cold-chain-stable kits and modular leases rather than outright instrument sales. Roughly one-quarter of Mexicans live in rural areas, creating latent demand for rapid POC panels that remains unmet, as reimbursement still prioritizes the lowest unit price over turnaround time. Continuous glucose monitors illustrate the ceiling: devices promise tighter glycemic control yet face slow uptake because public payers omit them from formularies, and tele-health infrastructure is sparse outside large metros. Syndromic molecular panels approved by COFEPRIS in 2024 stand ready for deployment once funding and staff training converge, underscoring medium-run upside for the Mexico in-vitro diagnostics market.

Expansion of Public Healthcare Funding and Insurance Coverage

The 2025-2026 BIRMEX mega-tender pooled MXN 130 billion (USD 6.34 billion) across 3,900 codes, transforming fragmented state buys into single federal auctions that tilt bargaining power toward high-volume incumbents. While price compression hits routine reagents, award winners lock in multiyear consumable pull-through on closed platforms, fortifying their stake in the Mexico in-vitro diagnostics market. Public procurement currently accounts for roughly three-quarters of diagnostic spend, magnifying the impact of any budget swing. Yet 54-55% workforce informality holds back private insurance penetration, leaving out-of-pocket expenditure at 41.37% of total health spending and sustaining a parallel retail cash market for advanced assays that fail to secure reimbursement. Products lacking standard approvals from the FDA, EMA, or other IMDRF peers remain ineligible for fast-track, limiting smaller innovators’ near-term share gains.

Accelerated Regulatory Approvals Via COFEPRIS Fast-Track Pathway

COFEPRIS affiliation with the International Medical Device Regulators Forum in 2024 and the June 2025 equivalency guideline reduced clearance for FDA-510(k) or CE-marked devices to 30 days. Multinationals leverage that window to participate in tenders without waiting for traditional 60-day Class III reviews, shortening revenue ramp cycles inside the Mexico in-vitro diagnostics market. Digital tools such as Digipris now allow 24-hour priority lanes for transfer-of-rights filings, signaling further paperwork relief. Compliance costs do climb under NOM-240-SSA1-2024 post-market vigilance rules, yet larger players already operate global technovigilance teams. By contrast, regional firms without recognized approvals confront longer reviews plus documentation in Spanish with apostilles, delaying entry and reinforcing market concentration.

Restraints Impact Analysis*

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent And Evolving Regulatory Compliance Requirements | –0.4% | National, highest burden on Class III filings | Medium term (2-4 years) |

| Inadequate Reimbursement For Advanced Molecular Tests | –0.6% | National, acute in oncology and autoimmune panels | Long term (≥ 4 years) |

| Supply-Chain Volatility And Import Dependency For Reagents | –0.5% | National, exposure to U.S. and China | Short term (≤ 2 years) |

| Uneven Laboratory Infrastructure Beyond Major Urban Centers | –0.3% | Rural zones and secondary cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent and Evolving Regulatory Compliance Requirements

ISO-13485-aligned GMP under NOM-241-SSA1-2021 now covers export-only IMMEX plants, adding audits and documentation burdens that weigh heaviest on contract manufacturers. New labeling rule NOM-137-SSA1-2024 mandates Spanish e-labels plus QR codes, prompting packaging redesigns and extra cost per SKU. The post-market vigilance draft standard further obliges technovigilance teams to report adverse events within tight timeframes, heightening back-office spend across the Mexico in-vitro diagnostics market. Although the 30-day equivalency path accelerates launches, it excludes emergency-use authorizations, delaying pandemic-response assays. A 12,000-file backlog in 2022 shows that even with Digipris, resource constraints can extend Class III reviews, adding timeline risk for novel platforms.

Inadequate Reimbursement for Advanced Molecular Tests

HER2, BRCA, and PD-L1 remain outside public coverage, shifting oncology test costs to patients or pharma-sponsored programs that distort competition and restrict independent labs’ volumes. BIRMEX tenders reward the lowest net price, disincentivizing high-complexity panels unless suppliers demonstrate clear cost offsets. Out-of-pocket spending already accounts for 41.37% of total health expenditure, so private-pay capacity is finite. Newborn screening pilots show that NGS panels cost 3-5× U.S. prices due to import tariffs, suppressing uptake even among affluent families. Without a statutory pricing framework, private insurers apply strict prior authorization, further narrowing the addressable demand and tempering the Mexico in-vitro diagnostics market growth trajectory.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: Molecular Platforms Outpace Legacy Assays

Immuno-diagnostics retained 28.11% of the Mexico in-vitro diagnostics market share in 2025, while Molecular Diagnostics is forecast to expand at a 7.65% CAGR through 2031, the highest among all test categories. Installed immunoassay analyzers remain workhorses for diabetes and lipid panels in public hospitals, yet oncology biomarkers and infectious-disease syndromic panels are redirecting capital budgets toward PCR, isothermal, and digital PCR systems[2]. Cepheid GeneXpert modules already support tuberculosis and HIV programs, and BioMérieux BIOFIRE pipes respiratory and sepsis panels into emergency departments where rapid turnaround shortens antibiotic courses. Commoditization pressure on routine chemistry reagents keeps prices flat, but closed-system molecular cartridges remain priced at a premium, sustaining revenue growth despite smaller test volumes.

Molecular adoption also benefits from the 30-day COFEPRIS equivalency route, letting FDA-cleared assays enter consolidated tenders without lengthy local trials. Laboratories pursuing ISO 15189 accreditation favor high-throughput PCR cyclers that lock in reagent rental contracts over ten-year horizons, deepening vendor stickiness. Rapid panel uptake, combined with entrenched immuno demand, positions the test-type segment as a dual-engine driver of the broader Mexico in-vitro diagnostics market.

By Product: Software and Services Accelerate Amid Digitization

Reagents & kits accounted for 54.88% of the Mexico in-vitro diagnostics market in 2025, reflecting the consumable intensity of glucose monitoring strips, immunoassay reagents, and molecular cartridges. However, Software & Services is projected to grow at an 8.32% CAGR through 2031 as laboratories deploy middleware, LIMS, and AI-enabled error-tracking to meet NOM-240-SSA1-2024 technovigilance mandates. Public hospitals bundle equipment leases with cloud analytics, turning service fees into an embedded component of annual operating budgets.

The shift toward digital platforms is accelerated by a talent gap; only 4.7% of surveyed lab staff had formal AI training, yet 75.4% expressed support for automation, driving demand for turnkey software that simplifies adoption. Instrument sales remain aligned with seven-to-ten-year replacement cycles, but vendors increase stickiness by embedding predictive-maintenance algorithms and remote calibration inside service contracts. As compliance rules tighten, software subscriptions outpace hardware in margin contribution, further diversifying revenue streams within the Mexico in-vitro diagnostics market.

By Usability: Disposables Dominate but Reusables Gain Traction

Disposable IVD devices held a 57.08% share in 2025, buoyed by single-use rapid antigen kits and glucose strips sold through 650,000 pharmacy outlets nationwide. Yet Re-Usable Equipment is advancing at a 7.83% CAGR as federal procurement channels concentrate high-throughput analyzers inside hub laboratories that amortize capital costs over large test volumes. The “La Muestra Viaja” sample-transport program validates this pivot by moving specimens from rural clinics to regional centers outfitted with reusable platforms rather than scattering disposables widely.

Labeling rule NOM-137-SSA1-2024, requiring QR-coded electronic instructions, slightly raises per-unit costs for disposables, while having a negligible impact on larger instruments that already include digital documentation. Cold-chain fragility and customs delays expose single-use biologics to spoilage risk, nudging procurement officers toward durable analyzers with locally stored reagents. Together, these forces rebalance the Mexico in-vitro diagnostics market toward a mixed model in which capital equipment growth softens but does not eclipse large-volume consumable demand.

By Application: Oncology Testing Rises Against Infectious-Disease Based

Infectious disease assays contributed 38.21% of application revenue in 2025, cementing their role in tuberculosis, HIV, and dengue surveillance programs. Oncology panels, however, are projected to increase at an 8.54% CAGR through 2031 as hospitals seek BRCA, HER2, and PD-L1 status to inform targeted therapy choices despite current reimbursement gaps. Median diagnostic delays of 113 days have motivated tertiary centers to adopt multiplex PCR and NGS panels that condense work-ups into a single encounter, improving care pathways even in self-pay scenarios.

Pharma-sponsored testing offsets some public-funding shortages, channeling companion diagnostic volumes to reference labs that meet strict quality criteria. Cardiology and metabolic panels grow more slowly yet maintain baseline demand given 19.7% hypertension and 11.2% diabetes prevalence. These dynamics keep infectious testing as the volume backbone, while oncology supplies incremental, high-margin growth within the Mexico in-vitro diagnostics market narrative.

By End User: Home Self-Testing Expands Alongside Hospital Labs

Hospital-based laboratories accounted for 38.15% of 2025 revenue, anchored by tertiary centers that run high-complexity molecular and immunopanel tests under multiyear reagent rental agreements. Home-care and self-testing users are expected to grow at a 6.54% CAGR, driven by glucose meters and pharmacy-dispensed respiratory antigen tests that appeal to the 54-55% of the informal workforce lacking employer insurance. Stand-alone reference labs, numbering over 18,000 registered units, fill regional gaps but face price pressure from consolidated public tenders that steer bulk volumes toward hospital hubs.

Digital health apps are beginning to link self-test results to telemedicine consults, reinforcing demand for Bluetooth-enabled meters even without formal reimbursement. Point-of-care outposts in rural clinics lean on sample-transport programs rather than on-site analyzers, preserving their role as collection nodes rather than full laboratories. Interplay among these channels sustains a diversified customer base, ensuring that no single end user dominates the wider Mexico in-vitro diagnostics market share equation.

Competitive Landscape

Abbott, Roche, Siemens Healthineers, and BD collectively anchor high-volume public tenders by pairing regulatory equivalency with broad test menus and deep field service. Roche Diagnostics Mexico recorded MXN 5.75 billion (USD 287 million) sales in 2024, a year-over-year rise of 8.4%, buoyed by cobas pro immuno-chemistry placements despite budget hold-ups. BD operates 12 plants that employ 17,000 staff, chiefly fabricating syringes and Vacutainer tubes, giving it leverage in specimen-collection contracts that feed analyzer reagent sales. Siemens Healthineers exploits installed ADVIA and Atellica bases to secure consumable pull-through, while its middleware enables compliance with NOM-240-SSA1-2024 technovigilance rules, deepening account stickiness.

Mid-tier challengers target white spaces. QIAGEN markets digital PCR dengue and monkeypox assays cleared by COFEPRIS in 2024, carving a niche in syndromic respiratory and tropical disease panels. BioMérieux rides BIOFIRE SPOTFIRE and VITEK REVEAL to accelerate antimicrobial-resistance testing turnaround from 24 hours to six, appealing to tertiary centers battling nosocomial infections. Thermo Fisher’s Ion Torrent line and Illumina’s NextSeq instruments see limited public uptake due to reagent cost but retain a foothold in private oncology labs that handle pharma-sponsored sequencing.

Strategic moves reveal intensifying rivalry. Seegene formed a technology-sharing joint venture with Werfen in late 2024, a template that could port to Mexico once local talent and incentives align. Shimadzu inaugurated a Mexico subsidiary in September 2024, with a demo lab slated for 2025, signaling that growing analytical-instrument demand is spilling over into medical systems. Meanwhile, smaller domestic reagent blenders face uphill battles: lacking FDA or CE marks, they must traverse 60-day Class III reviews and cannot bid on BIRMEX fast-track tenders, squeezing margins and encouraging consolidation within the Mexico in-vitro diagnostics market.

Mexico In-Vitro Diagnostics Industry Leaders

Bio-Rad Laboratories, Inc.

Thermo Fisher Scientific Inc.

bioMerieux SA

Abbott Laboratories

F. Hoffmann-La Roche AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Abbott announced a USD 200 million electrophysiology device plant in Querétaro aimed at 1 000+ new jobs, reinforcing medical-device nearshoring though not yet covering IVD reagents

- October 2024: Seegene and Werfen created a Spain-based NewCo to localize syndromic PCR R&D, a model under evaluation for Mexico to serve regional pathogen panels

- June 2024: QIAGEN launched 35 digital-PCR assays, including dengue serotypes 1-4 and chikungunya, following COFEPRIS clearance to support endemic-disease surveillance.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the Mexico in-vitro diagnostics (IVD) market as all revenue generated within the country from reagents, analyzers, data-management tools, and associated services used to test human blood, urine, tissue, and other specimens in laboratories or at the point of care for diagnosis, screening, or monitoring of disease.

Scope exclusion: revenue from research-only assays, contract manufacturing, and veterinary tests falls outside this study.

Segmentation Overview

- By Test Type

- Clinical Chemistry

- Immuno-Diagnostics

- Molecular Diagnostics

- Hematology

- Coagulation

- Microbiology

- Other Test Types

- By Product

- Instruments

- Reagents & Kits

- Software & Services

- By Usability

- Disposable IVD Devices

- Re-Usable Equipment

- By Application

- Infectious Diseases

- Diabetes

- Oncology

- Cardiology

- Auto-Immune Disorders

- Nephrology

- Other Applications

- By End User

- Stand-Alone Laboratories

- Hospital-Based Laboratories

- Point-Of-Care Settings

- Home-Care & Self-Testing Users

Detailed Research Methodology and Data Validation

Primary Research

Our team interviewed laboratory directors, hospital buyers, regional distributors, and regulators across northern, central, and southern states. The exchanges validated average selling prices, menu-mix shifts, and realistic uptake curves for molecular point-of-care kits.

Desk Research

We first mapped the demand pool by reviewing open datasets from Mexico's National Epidemiological Surveillance System, COFEPRIS import logs, OECD Health Data, and World Bank health-spend tables. Trade digests from the Mexican Association of Clinical Laboratories and technical papers from IFCC clarified test volumes and reagent consumption. Company 10-Ks, investor decks, and government tender notices guided local price corridors. When sub-segment detail was scarce, Mordor analysts pulled installed-base clues from D&B Hoovers, Dow Jones Factiva, and Questel patent trends. These named sources are illustrative; many additional documents were checked to verify every datapoint.

Market-Sizing & Forecasting

We built a top-down model that converts import, production, and procedure data into annual spend. We then cross-checked totals with selective bottom-up supplier roll-ups. Key inputs include diabetes prevalence, elective surgery rebounds, private insurance enrollment, public reimbursement updates, analyzer installed base, and point-of-care penetration. Multivariate regression links test volumes and price trajectories to GDP per capita and health expenditure, and expert consensus bounds scenario spreads. Gaps in granular data are bridged with normalized reagent-per-test factors obtained during interviews.

Data Validation & Update Cycle

Model outputs face variance checks against historical import values and insurer claim files. Senior analysts examine anomalies and, if material events arise, re-contact sources before the scheduled annual refresh so clients always receive an up-to-date view.

Why Mordor's Mexico In-Vitro Diagnostics Baseline Commands Reliability

Published estimates often diverge because firms apply different product baskets, data vintages, and currency treatments.

Our 2025 base year, wider inclusion of software fees, and yearly refresh cadence keep the Mordor baseline current and decision-ready. Key gaps arise when other studies omit ancillary services, rely on older 2024 customs data, or project growth with single-factor methods.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.22 B (2025) | Mordor Intelligence | - |

| USD 2.41 B (2024) | Global Consultancy A | Excludes software and services, uses 2024 prices without inflation adjustment |

| USD 2.20 B (2024) | Trade Journal B | Narrower test menu and single-factor growth, limited primary validation |

These contrasts show that our disciplined variable selection, fresh pricing checks, and multi-step reviews deliver a transparent baseline that end users can trust.

Key Questions Answered in the Report

How large will Mexico's in-vitro diagnostics sector be by 2031?

It is forecast to reach USD 1.84 billion by 2031, expanding at a 5.08% CAGR from 2026.

Which test category is expanding fastest in Mexico?

Molecular diagnostics is projected to grow at 7.65% CAGR through 2031 due to oncology biomarkers and syndromic infectious panels.

What product area is seeing the quickest revenue rise?

Software & Services leads with an 8.32% CAGR as labs install LIMS and AI-driven quality tools to meet NOM-240-SSA1-2024 rules.

How is nearshoring affecting diagnostics supply?

New plants in Querétaro and Baja California improve hardware availability, yet most high-value reagents remain import-dependent.

Why do oncology assays face adoption hurdles?

Public reimbursement omits HER2, BRCA, and PD-L1 tests, transferring costs to patients or pharma programs and limiting volume growth.

Which regions hold the greatest growth potential outside Mexico City?

Monterrey, Guadalajara, and border states such as Nuevo León show opportunity thanks to larger hospitals and cross-border logistics advantages.

Page last updated on: