Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

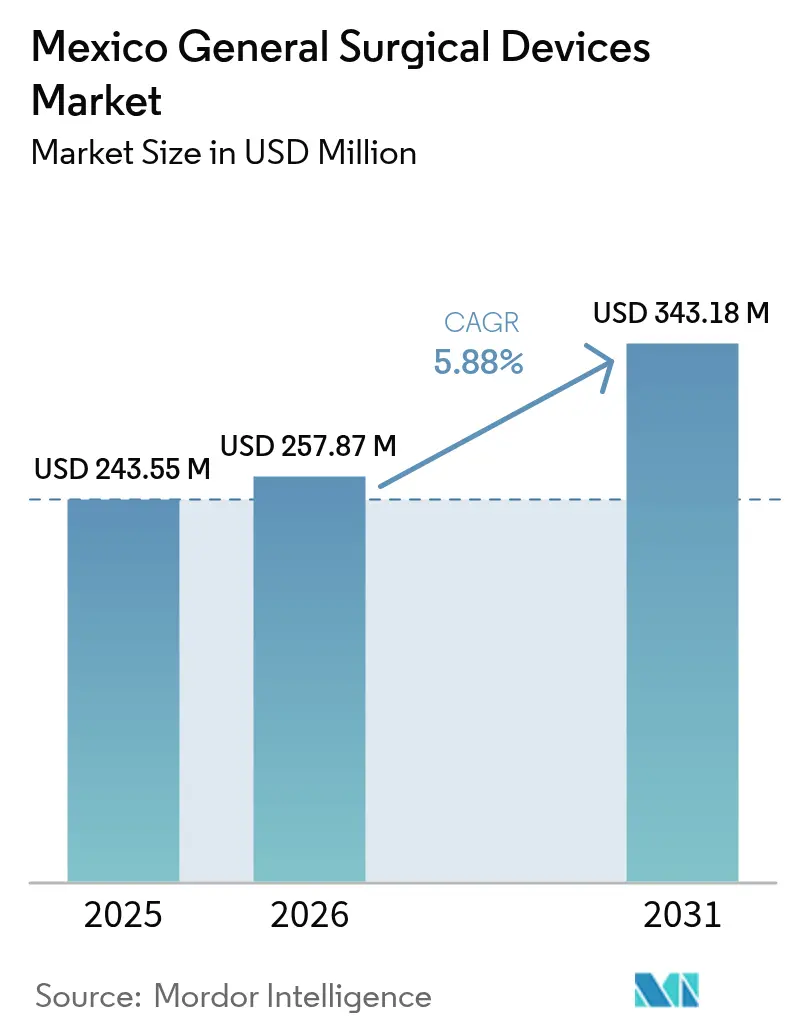

| Base Year Market Size (2025) | USD 243.55 Million |

| Market Size (2026) | USD 257.87 Million |

| Market Size (2031) | USD 343.18 Million |

| Growth Rate (2026 - 2031) | 5.88% CAGR |

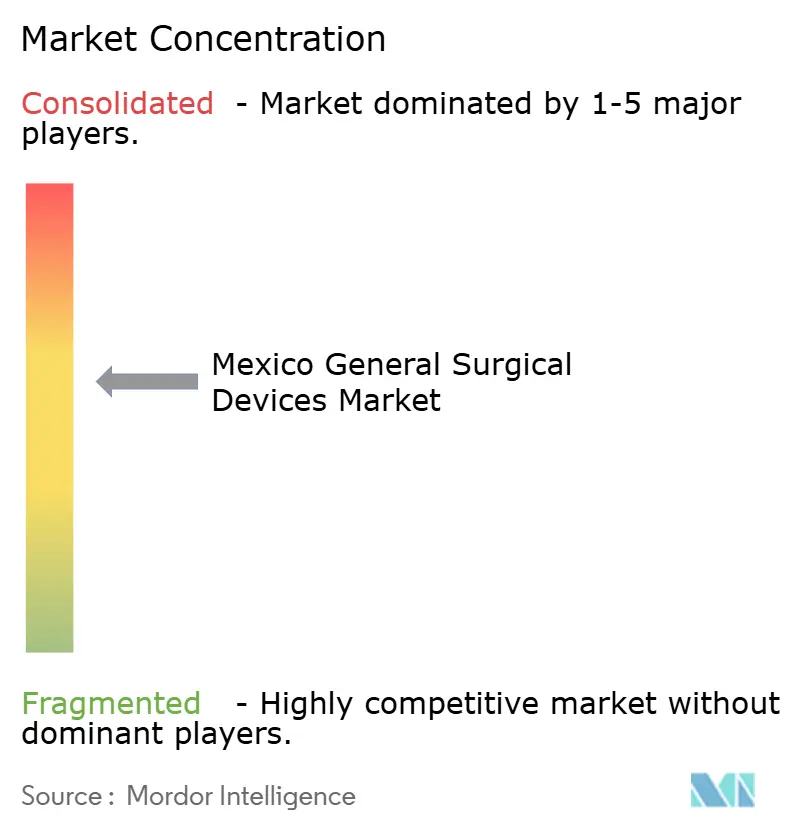

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico General Surgical Devices Market Analysis by Mordor Intelligence

The Mexico General Surgical Devices Market size is expected to grow from USD 243.55 million in 2025 to USD 257.87 million in 2026 and is forecast to reach USD 343.18 million by 2031 at 5.88% CAGR over 2026-2031. Hospitals, private clinics, and border health centers continue to adopt technology that enables shorter recovery times, which has accelerated demand for minimally invasive and robotic systems. The market benefits from near-shoring strategies that position Mexico as a manufacturing hub for North American supply chains, reducing lead times and import costs for critical components. Continued growth in medical tourism underpins premium demand for advanced visualization, imaging, and robotic platforms in border cities. Government hospital-modernization spending and private sector investment in ambulatory surgery centers add further momentum, even as fiscal constraints encourage cost-effective device configurations.

Key Report Takeaways

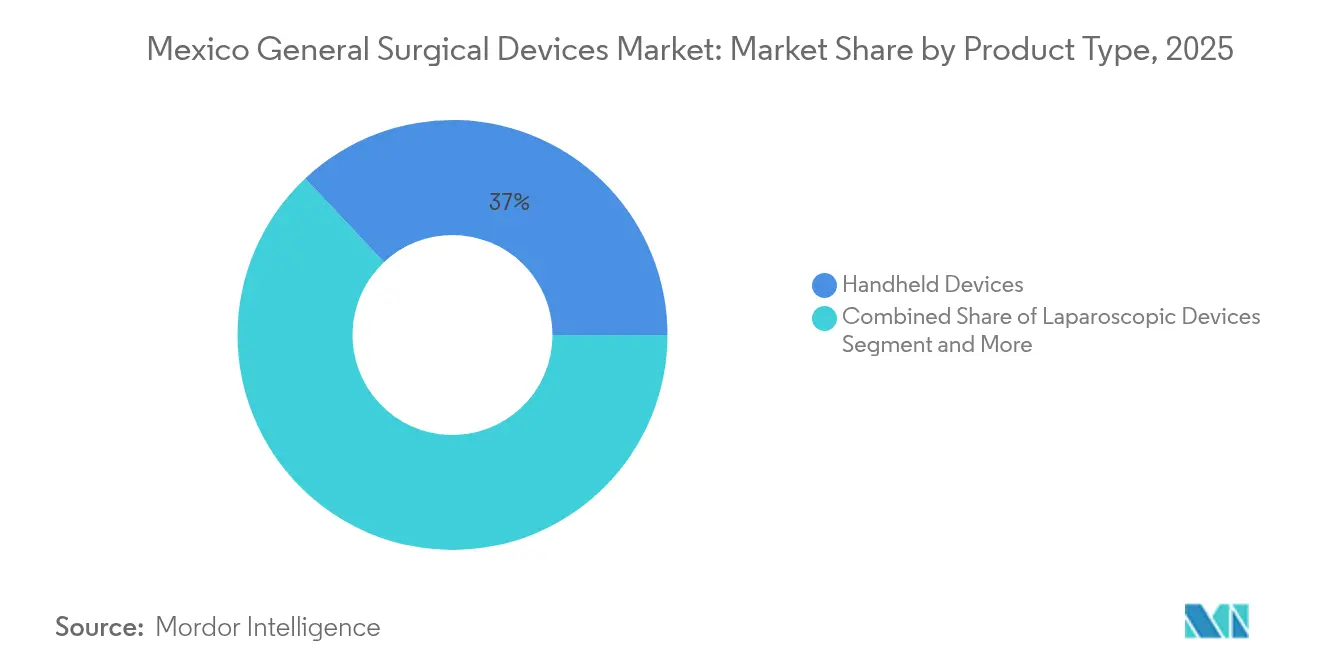

- By product type, handheld devices led with 37.02% of the Mexico general surgical devices market share in 2025, while robotic and computer-assisted systems posted the fastest 6.61% CAGR through 2031.

- By procedure approach, minimally invasive surgery captured 71.24% revenue share in 2025; the segment is expanding at a 6.05% CAGR to 2031.

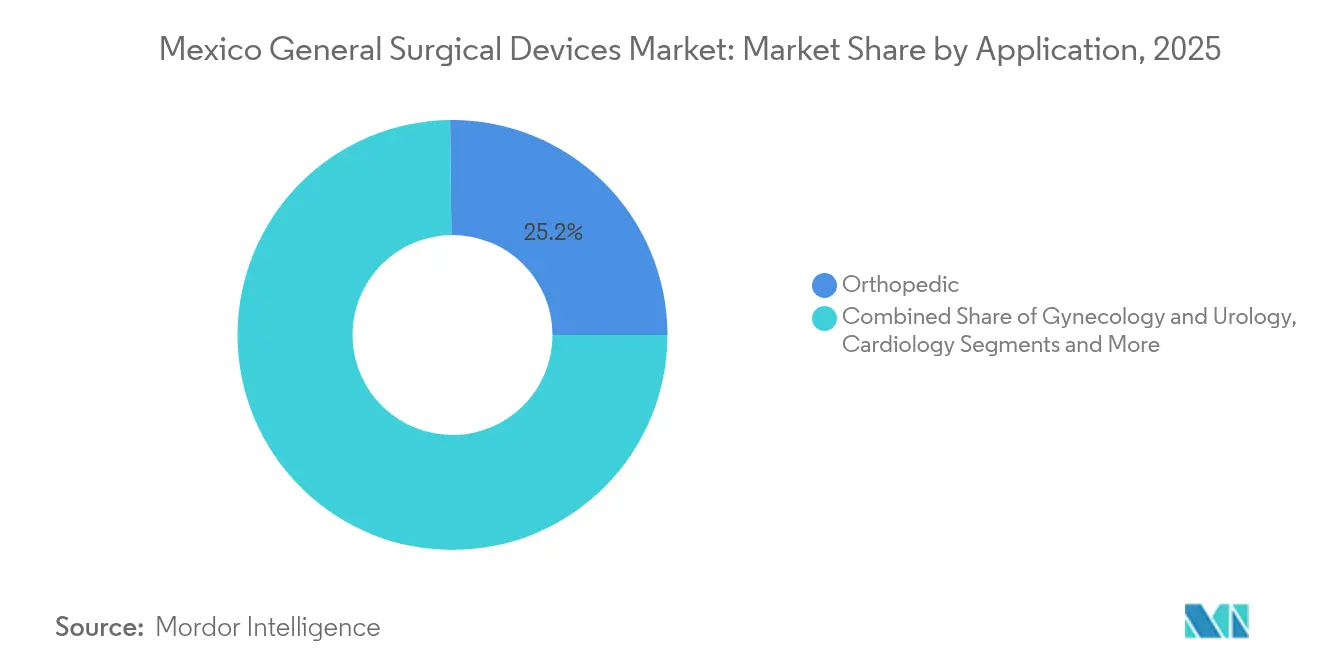

- By application, orthopedic procedures accounted for 25.18% of the Mexico general surgical devices market size in 2025, while cardiology is projected to rise at a 6.02% CAGR through 2031.

- By end user, hospitals held 70.86% share of the Mexico general surgical devices market size in 2025, whereas ambulatory surgery centers are forecast to post a 6.78% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico General Surgical Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Minimally-Invasive Surgery | +1.2% | National, with concentration in border cities and major metropolitan areas | Medium term (2-4 years) |

| Technological Advances in Laparoscopic & Robotic Systems | +0.9% | National, with early adoption in private hospitals and medical tourism centers | Long term (≥ 4 years) |

| Growing Surgical Burden from Obesity & Metabolic Diseases | +0.8% | National, with higher prevalence in northern and urban regions | Long term (≥ 4 years) |

| Government Hospital-Modernization (INSABI) Programs | +0.6% | National, focusing on underserved rural and urban areas | Medium term (2-4 years) |

| Near-Shoring of Device Manufacturing Boosts Local Supply | +0.4% | Regional, concentrated in Baja California, Sonora, Jalisco manufacturing clusters | Medium term (2-4 years) |

| Expansion of Private Border Hospitals for Medical Tourism | +0.3% | Regional, primarily US-Mexico border cities including Tijuana, Ciudad Juárez | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Minimally Invasive Surgery

Mexican surgeons increasingly favor laparoscopic and endoscopic techniques that shorten recovery and reduce postoperative pain, especially in gynecology and bariatric care. Comparative studies show robotic-assisted laparoscopy lowers conversion rates and complications in complex cases such as endometriosis, prompting investment in visualization systems and advanced handheld devices. Ambulatory surgery centers are scaling capacity which further supports demand for portable minimally invasive platforms.[1]Source: Health Industry Distributors Association, “Ambulatory Surgery Center Market Report,” hida.org Artificial-intelligence guidance, already demonstrating sub-millimeter tracking accuracy, is poised to enhance surgeon confidence and accelerate adoption. Collectively, these factors reinforce the dominance of minimally invasive devices across the Mexico general surgical devices market.

Technological Advances in Laparoscopic & Robotic Systems

Launches such as Intuitive Surgical’s da Vinci 5 and Johnson & Johnson’s Velys Spine platform provide Mexico-based hospitals access to smaller footprints, improved imaging, and ergonomic enhancements that overcome earlier cost and training hurdles. Partnerships like Medtronic-Siemens integrate 3D imaging with robotic navigation, enabling precise vertebrae measurement during spine procedures. Domestic training capacity is rising as SAGES rolls out iLAP master programs in nine Mexican centers, standardizing skills and broadening the talent pool available for advanced therapies. Enhanced hardware and educational infrastructure position the Mexico general surgical devices market to sustain long-term technological upgrading.

Growing Surgical Burden from Obesity & Metabolic Diseases

With obesity prevalence among the highest worldwide, bariatric procedures surge, requiring advanced stapling, closure, and imaging systems that withstand complex abdominal anatomy. Diabetes complications are also driving wound-care device consumption, particularly in northern states. An aging population—8.2% over 65—adds knee and cataract surgery volumes under new government programs, widening orthopedic device demand. Robotic bariatric techniques, though capital intensive, deliver lower length-of-stay metrics, improving hospital economics and boosting adoption in tertiary centers.

Government Hospital-Modernization (INSABI) Programs

INSABI’s mandate to reduce care gaps has allocated multiyear budgets for surgical suites, though procurement delays have created pent-up demand for essential devices. Recent bids centralize purchasing to secure scale discounts, saving MX$30 billion while requiring suppliers to prove value over total cost of ownership. Public-private hospital projects in rural districts open channels for vendors that can align training and maintenance packages with modernization targets. Although health budgets fell 11% in 2025, the program still stimulates device demand where clinical need is acute

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost of Advanced Surgical Equipment | -0.8% | National, with greater impact on public hospitals and smaller private facilities | Medium term (2-4 years) |

| COFEPRIS Registration Timelines & Documentation Burden | -0.6% | National, affecting all device manufacturers and importers | Short term (≤ 2 years) |

| Rural Surgeon Shortage Limits Device Penetration | -0.4% | Regional, concentrated in rural and underserved areas | Long term (≥ 4 years) |

| Peso Volatility Inflates Imported Component Prices | -0.3% | National, with greater impact on import-dependent manufacturers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Advanced Surgical Equipment

Public hospitals face tighter budgets after a 14.3% spending decline in 2025, limiting acquisition of premium robotic systems despite proven clinical benefits. Smaller private providers also struggle to justify multimillion-dollar outlays without scale efficiencies, pushing them toward refurbished or shared-service models. Consolidation deals in healthcare M&A highlight the search for capital synergies capable of funding next-generation platforms. Consequently, cost remains a ceiling on penetration for high-value systems within the Mexico general surgical devices market.

COFEPRIS Registration Timelines & Documentation Burden

Standard device approvals take 10-18 months, and deficiency letters can extend the process by another half-year, delaying launches of innovative tools.[2]Source: Pure Global, “COFEPRIS Mexico Medical Device Registration,” pureglobal.com Detailed technical dossiers, ISO 13485 evidence, and local holder requirements add to expense, with single registrations often costing USD 5,000-10,000 before testing fees. Smaller innovators find these hurdles particularly challenging, which slows technology refresh cycles inside the Mexico general surgical devices industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Handheld Dominance amid Rapid Robotic Uptake

Handheld devices generated 37.02% of the Mexico general surgical devices market in 2025, underscoring their ubiquity across every specialty and procedure complexity level. Public institutions appreciate reusable scalpels, forceps, and needle holders that withstand sterilization while private centers pair premium handheld electrosurgical pencils with high-definition screens for delicate work. Demand also rises for energy instruments compatible with minimally invasive ports. The Mexico general surgical devices market size for robotic and computer-assisted systems is projected to climb at 6.61% CAGR, supported by da Vinci 5 and Velys Spine launches that improve haptic feedback and imaging clarity.

Robotic uptake remains highest in spine, bariatric, and urology programs catering to international patients who research technology specifications before travel. Electrosurgical consoles that integrate with AI-guided video feeds show steady volume gains because they shorten procedure times. Trocars and access systems grow in tandem with laparoscopic volumes, particularly in gynecology where spinal anesthesia protocols cut recovery by full days. Wound-closure demand stays resilient with IMSS-Bienestar planning around 1 million surgeries despite budget pressure, locking in baseline consumption of sutures and staplers. Emerging AI-enhanced handhelds capable of real-time tissue identification signal the next frontier for product differentiation within the Mexico general surgical devices market.

By Procedure Approach: Minimally Invasive Supremacy

Minimally invasive surgery held 71.24% share in 2025 and is expanding at 6.05% CAGR through 2031, reflecting nationwide surgeon retraining and patient preference for faster discharge. Many private centers position minimally invasive care as a differentiator for US and Canadian medical tourists, prompting acquisitions of 4K laparoscopes, articulating staplers, and 3 mm ports that minimize scarring.

Open surgery persists for trauma and emergent pathology but its proportion continues sliding as ambulatory centers win case mix from inpatient wards. The Mexico general surgical devices market size tied to minimally invasive platforms benefits from government cataract and knee programs that specify arthroscopy and phacoemulsification techniques. SAGES training hubs further integrate simulation into curriculum, ensuring a pipeline of residents proficient in laparoscopy, which supports downstream device consumption. Robust data that show lower complication rates in robotic endometriosis surgery reinforce physician confidence and fuel procurement budgets in tertiary centers.

By Application: Orthopedic Scale and Cardiovascular Momentum

Orthopedic procedures captured 25.18% of the Mexico general surgical devices market in 2025, led by knee and spine interventions that address aging demographics and rising obesity. President Sheinbaum’s 2025 knee replacement initiative allocates funding for implants and navigation systems, drawing competitive bids from global suppliers.

Cardiology’s 6.02% CAGR stems from device-imaging convergence that streamlines valve, bypass, and hybrid interventions. Medtronic’s cardiovascular portfolio milestone of USD 3.1 billion in Q2 FY25 global revenue provides confidence for Mexican distributors to widen inventory. Gynecological and urological volumes increase through cross-border fertility and prostate programs, requiring fine-bore instruments and laser lithotripters. Neurosurgical adoption of robotic positioning arms drives sales of frameless navigation probes, benefiting from AI-assisted tremor suppression technologies. The Mexico general surgical devices market share associated with bariatric suites rises in parallel with obesity surgery growth, a trend evident in tertiary centers that report shorter stays and lower complication rates after robotic gastric bypass.

By End User: Hospitals Rule yet ASCs Accelerate

Hospitals retained 70.86% revenue dominance in 2025 as they manage trauma, obstetric, and complex oncology cases that demand full operating theater capabilities. Teaching centers in Mexico City and Guadalajara deploy robotic suites to attract residency candidates and to meet accreditation metrics for advanced procedure volumes.

Ambulatory surgery centers grow at 6.78% CAGR, propelled by insurer reimbursement policies that favor outpatient settings and by patient preference for shorter admissions. Border ASCs earn premium returns servicing international clientele who bundle vacation packages with elective surgeries, justifying investments in compact intraoperative CT scanners and high-definition endoscopy. Specialty clinics sharpen focus on single-service lines, leveraging modular surgical towers that reduce floor space. Collective shifts in care sites support diversified channel strategies for suppliers within the Mexico general surgical devices market.

Geography Analysis

Northern border cities concentrate premium surgical demand because proximity to the United States attracts 1.4 million medical tourists per year, fostering high adoption of robotic systems, 4K imaging, and single-use instruments that meet international expectations. Baja California alone accounts for 36% of Mexico’s medical device exports, enabling rapid replenishment of components and streamlined service support, which benefits hospitals in Tijuana and Mexicali.

Central Mexico—especially Mexico City and Guadalajara—hosts national reference hospitals and manufacturing R&D clusters. Guadalajara’s high-tech corridor now mirrors Silicon Valley’s device prototyping culture, encouraging joint ventures where design iterations proceed alongside clinical pilots, reducing time to market for laparoscopic accessories and neurosurgical probes.

Southern and rural regions lag in device penetration due to surgeon shortages and infrastructure gaps, yet INSABI reforms channel grants for modular theaters and tele-surgery pilots that could decentralize access. These programs create future opportunities for rugged handhelds and portable imaging systems tailored to intermittent power conditions. Overall, geographic diversity necessitates multi-tier distribution and after-sales models across the Mexico general surgical devices market.

Competitive Landscape

Multinationals such as Johnson & Johnson, Medtronic, and Stryker dominate high-value specialties through integrated platforms that combine hardware, software, and training packages. Johnson & Johnson’s MedTech division invested USD 1.3 billion in surgical instruments development, underscoring a commitment to next-generation systems that differentiate on ergonomics and AI analytics. Medtronic’s partnership with Siemens showcases ecosystem strategies that lock in imaging and navigation workflows under unified service contracts, raising switching costs for hospitals.

Local production gains momentum as tariff changes add 4-8% duties to imported finished goods, motivating companies like ThermoFab to build enclosures and single-use components in Mexicali where labor costs undercut Asian benchmarks. Olympus Latin America expanded its bipolar energy line and launched the Visera Elite III endoscopic tower, broadening mid-price options for public hospitals.

Emerging innovators develop AI-guided handhelds capable of delivering real-time tissue characterization, threatening to leapfrog legacy vendors reliant on incremental hardware updates. Regulatory expertise remains a strategic asset; firms that navigate COFEPRIS efficiently achieve earlier revenue booking and can reinvest in localized after-sales teams. The Mexico general surgical devices industry therefore balances scale advantages of global incumbents with agile entrants positioned to serve niche clinical needs.

Mexico General Surgical Devices Industry Leaders

Boston Scientific Corporation

Stryker Corporation

Johnson & Johnson (Ethicon)

Medtronic plc

B. Braun SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Olympus Latin America expanded its POWERSEAL advanced bipolar sealer-divider portfolio in Mexico.

- January 2025: ThermoFab announced a Mexicali facility opening mid-2025 to support near-shore molding for medical device enclosures.

- March 2024: Olympus Latin America introduced the VISERA ELITE III endoscopic visualization platform in Mexico.

Mexico General Surgical Devices Market Report Scope

As per the scope of the report, general surgical devices are tools or devices for performing specific actions or carrying out desired effects during surgery. These include tools for cutting and dissecting, such as scalpels, scissors, and saws; tools for grasping and holding, including forceps and clamps; and hemostatic tools, which are used to stop bleeding.

The Mexico general surgical devices market is segmented by product (handheld devices, laparoscopic devices, electro surgical devices, wound closure devices, trocars and access devices, and other products) and application (gynecology and urology, cardiology, orthopedic, neurology, other applications). The report offers the value (in USD million) for the above segments.

By Product Type

| Handheld Devices |

| Laparoscopic Devices |

| Electrosurgical Devices |

| Wound-Closure Devices |

| Trocars and Access Systems |

| Robotic and Computer-Assisted Systems |

| Other Devices |

By Procedure Approach

| Open Surgery |

| Minimally Invasive Surgery |

By Application

| Gynecology and Urology |

| Cardiology |

| Orthopedic |

| Neurology |

| Other Applications |

By End User

| Hospitals |

| Ambulatory Surgical Centres |

| Specialty Clinics |

| By Product Type | Handheld Devices |

| Laparoscopic Devices | |

| Electrosurgical Devices | |

| Wound-Closure Devices | |

| Trocars and Access Systems | |

| Robotic and Computer-Assisted Systems | |

| Other Devices | |

| By Procedure Approach | Open Surgery |

| Minimally Invasive Surgery | |

| By Application | Gynecology and Urology |

| Cardiology | |

| Orthopedic | |

| Neurology | |

| Other Applications | |

| By End User | Hospitals |

| Ambulatory Surgical Centres | |

| Specialty Clinics |

Key Questions Answered in the Report

What is the current value of the Mexico general surgical devices market?

The market is valued at USD 257.87 million in 2026 and is projected to reach USD 343.18 million by 2031, growing at 5.88% CAGR.

Which product segment leads the market?

Handheld devices hold the top spot with a 37.02% share of 2025 revenue.

Why is minimally invasive surgery so prominent in Mexico?

It delivers faster recovery, supports medical tourism competitiveness, and now accounts for 71.24% of procedures with a 6.05% CAGR.

How does COFEPRIS regulation affect device launch timelines?

Standard approvals take 10-18 months, and additional requests can prolong entry, which impacts smaller innovators the most.

Which region generates the highest demand for advanced surgical technology?

Northern border cities such as Tijuana and Mexicali lead because of strong medical tourism inflows and proximity to US patients.

Page last updated on: