Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

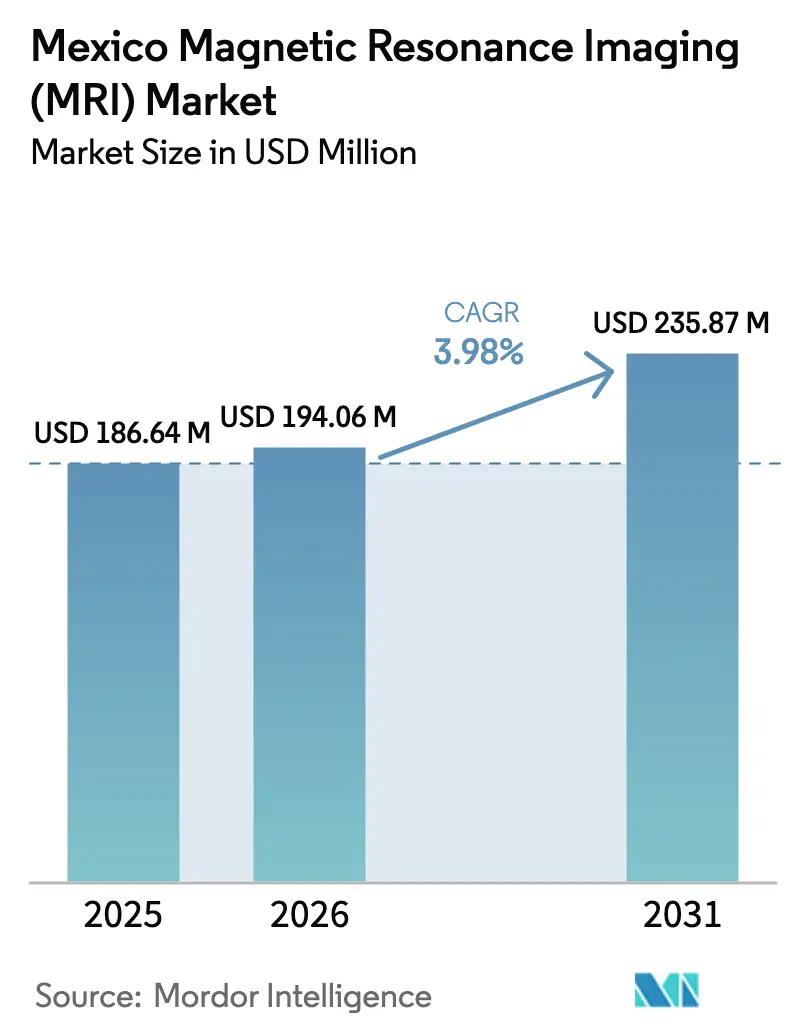

| Base Year Market Size (2025) | USD 186.64 Million |

| Market Size (2026) | USD 194.06 Million |

| Market Size (2031) | USD 235.87 Million |

| Growth Rate (2026 - 2031) | 3.98% CAGR |

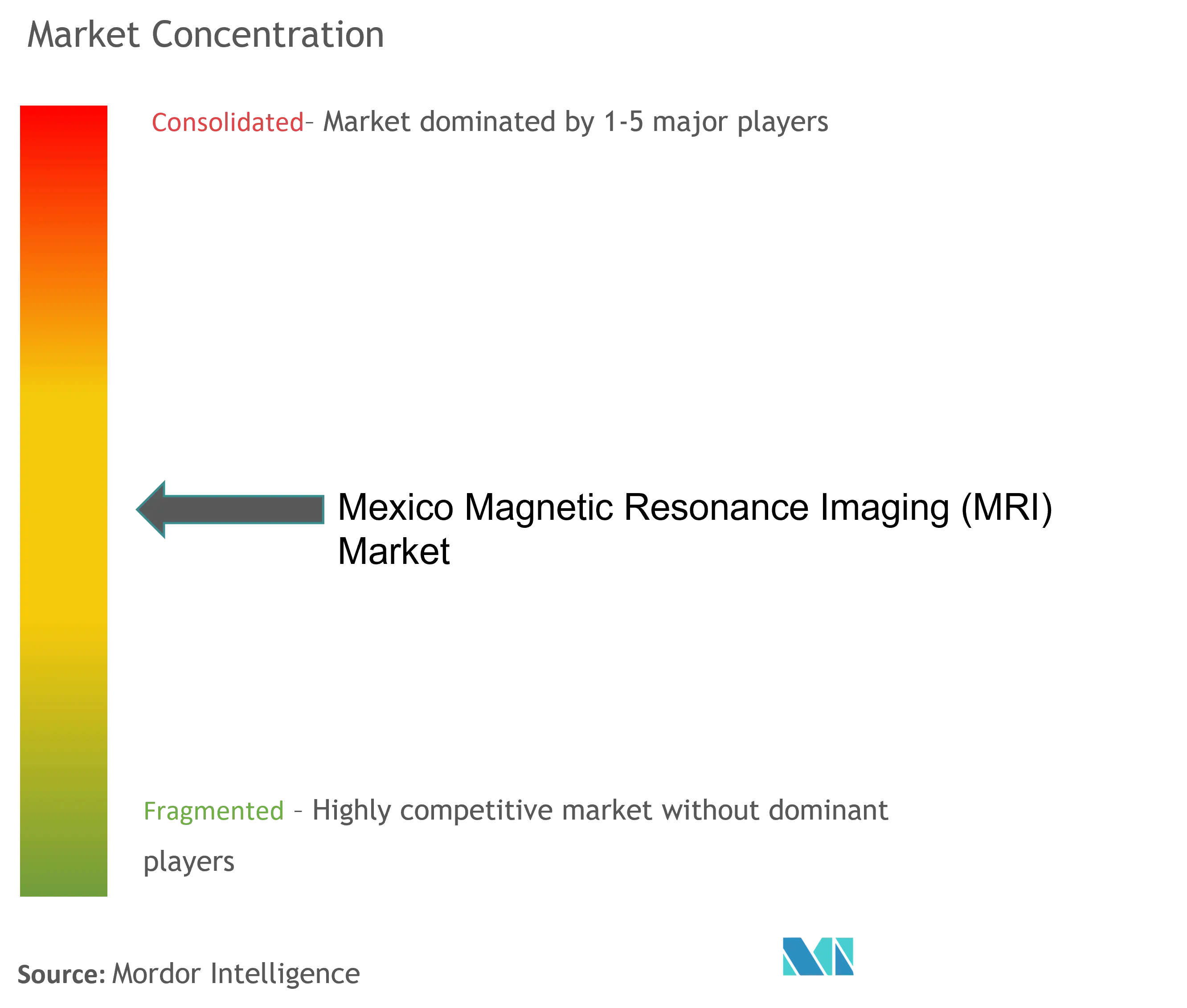

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Magnetic Resonance Imaging (MRI) Market Analysis by Mordor Intelligence

The Mexico MRI market size is expected to grow from USD 186.64 million in 2025 to USD 194.06 million in 2026 and is forecast to reach USD 235.87 million by 2031 at 3.98% CAGR over 2026-2031. Public-sector modernization programs, rising private-hospital spending and USMCA-enabled equipment imports are expanding diagnostic imaging capacity in every major metropolitan area, while AI-enabled scanners reinforce throughput and lower per-study costs. Steady chronic-disease growth, particularly diabetes and cardiovascular conditions, elevates routine MRI utilization rates, and Mexico’s USD 11 billion medical-tourism stream brings incremental demand from 1.4 million international patients who opt for lower-cost scans in Tijuana, Los Cabos and Mexico City. Global vendors are localizing coil and magnet sub-assemblies to capture USMCA origin benefits, while helium-free technologies alleviate cost pressures from peso volatility and supply-chain shocks. Persistent radiologist shortages remain a structural headwind, but nationwide teleradiology roll-outs and AI-driven reporting platforms are beginning to bridge interpretation gaps.

Key Report Takeaways

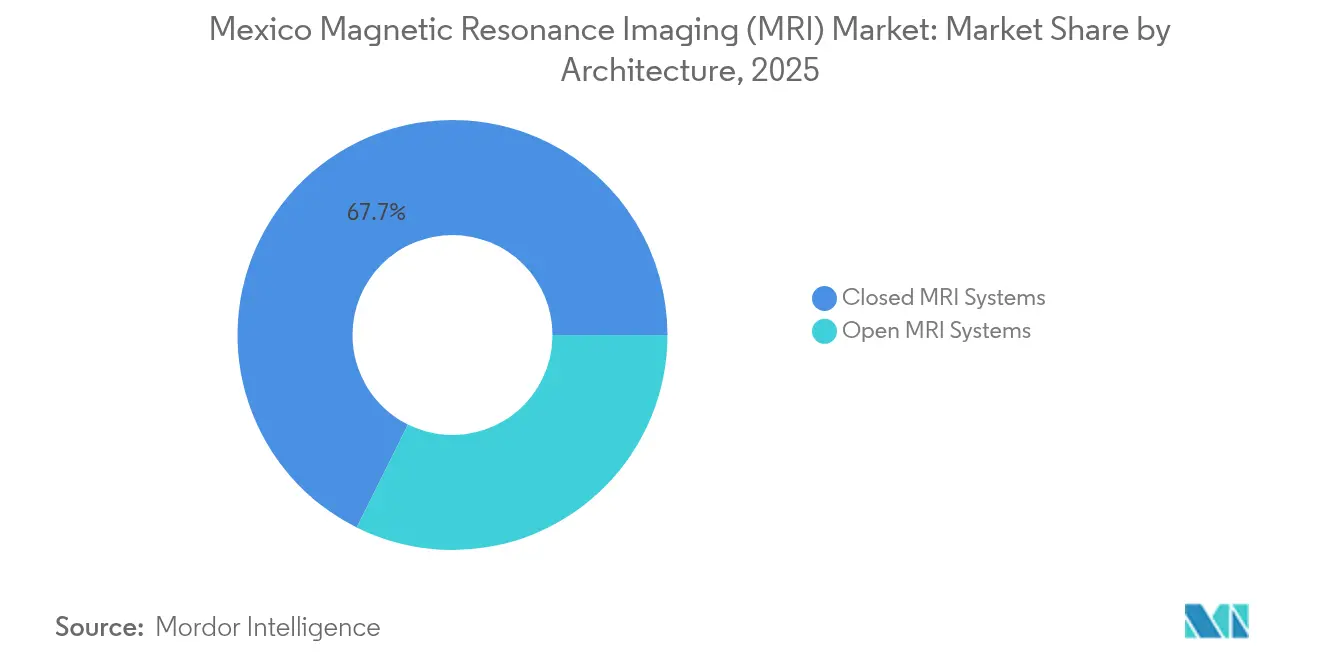

- By architecture, closed systems led with 67.65% of Mexico MRI market share in 2025; open systems are projected to advance at a 4.65% CAGR through 2031.

- By field strength, 1.5 T scanners held 54.55% share of the Mexico MRI market size in 2025, while 3 T and ≥7 T platforms are poised to expand at a 4.60% CAGR to 2031.

- By application, neurology captured 31.85% revenue share in 2025; oncology imaging is forecast to post a 5.05% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Magnetic Resonance Imaging (MRI) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advancements in MRI System Hardware & AI-Enabled Software | +0.8% | National, with early adoption in Mexico City, Guadalajara, Monterrey | Medium term (2-4 years) |

| Rising Burden of Chronic & Oncological Diseases | +1.2% | National, with higher concentration in urban centers | Long term (≥ 4 years) |

| Expansion of Private Hospitals & Medical-Tourism Clusters | +0.9% | Regional clusters in Los Cabos, Tijuana, Mexico City, Guadalajara | Medium term (2-4 years) |

| Federal Tax Breaks & USMCA Import Incentives for Imaging Devices | +0.6% | National, with manufacturing benefits in border states | Short term (≤ 2 years) |

| Rapid Roll-Out of Teleradiology & PACS Across Secondary Cities | +0.5% | Secondary cities and rural areas nationwide | Medium term (2-4 years) |

| OEM Near-Shoring of Coil & Magnet Sub-Assembly Lines | +0.4% | Northern Mexico manufacturing corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Advancements in MRI Hardware and AI-Enabled Software

Rapid algorithmic innovation is shrinking scan times by up to 50%, allowing facilities to raise daily throughput without adding scanners. Siemens Healthineers’ AI-Rad Companion and Philips’ SmartSpeed Precise platforms sharpen images while trimming protocol length, which directly offsets the radiologist shortfall by reducing repeat studies[1]Siemens Healthineers, “Artificial Intelligence for MRI,” siemens-healthineers.com. Helium-free magnet designs such as Philips BlueSeal systems curb lifetime operating expenses by removing volatile cryogen inputs, and more than 1,000 units have been installed worldwide [2]USA Philips, “Philips Extends Leadership in Virtually Helium-Free MRI,” usa.philips.com . Mexico’s universal electronic-health-record program positions facilities to exploit AI workflow engines that draw on integrated data lakes for automated triage, further lifting scanner productivity. FDA-cleared software such as SwiftMR is vendor-agnostic, enabling hospitals to retrofit legacy fleets instead of replacing entire systems.

Rising Chronic and Oncological Disease Burden

Diabetes affected 16.9% of Mexican adults in 2022 and is projected to climb steadily through 2050, necessitating periodic renal, cardiac and neurologic imaging follow-ups. Cardiovascular mortality increased from 96.7 to 111.7 per 100,000 between 2011-2015, making MRI pivotal for ischemic and structural heart assessments. Cancer incidence stands at 140.9 per 100,000, with breast and prostate leading new-case tallies, and oncology MRI volumes are growing fastest as screening guidelines widen. Chronic kidney disease linked to diabetes impacts 14.5 million residents, driving repeat abdominal MRI studies for disease-progress tracking. Long COVID affects 37% of survivors, adding respiratory and neurologic MRI demand for lingering complications.

Expansion of Private Hospitals and Medical-Tourism Clusters

Hospitales MAC secured USD 160 million to build MRI-equipped hospitals in 17 cities and targets a value-for-money positioning that matches domestic demand with tourist inflows. CHRISTUS Health’s USD 84 million Cabo San Lucas facility will integrate AI-assisted imaging across 75 beds, exemplifying destination-care models focused on comprehensive diagnostics. Los Cabos, Tijuana and Mexico City advertise MRI scans at 60% cost savings versus U.S. rates, drawing 1.4 million annual visitors and fueling out-of-pocket imaging volumes. The Mexican Council for Medical Tourism is harmonizing quality standards, further legitimizing cross-border care and embedding premium MRI packages into bundled surgery offerings. Private providers distinguish themselves with whole-body MRI options priced between USD 273-826, which remain significantly below U.S. cash prices while still supporting healthy margins.

Federal Tax Breaks and USMCA Import Incentives

The USMCA eliminates tariffs on compliant imaging systems, trimming acquisition costs, and it streamlines regulatory definitions, cutting redundant certification expenses. Mexico’s PROSEC scheme further reduces duties on MRI components destined for export, encouraging global vendors to near-shore coil and magnet assembly lines in northern industrial zones. A March 2025 tariff suspension covers half of all USMCA-qualified imports, reducing scanner list prices during public-hospital procurement cycles. However, policymakers have floated 10% tariff surcharges for fully-built scanners, which could add USD 100,000-200,000 to high-end systems and stall replacement schedules. December 2024 regulations allow public buyers to import MRI units without local marketing authorization through BIRMEX, accelerating fleet upgrades but raising intellectual-property concerns among established suppliers.

Restraints Impact Analysis*

| Restraint | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront & Lifecycle Cost of MRI Scanners | -1.1% | National, with greater impact on smaller facilities | Long term (≥ 4 years) |

| Lengthy COFEPRIS Device-Registration & Reimbursement Delays | -0.7% | National regulatory bottleneck | Medium term (2-4 years) |

| Peso Volatility Inflating Lease-Financing Costs | -0.5% | National, with higher impact on import-dependent facilities | Short term (≤ 2 years) |

| Shortage & Uneven Distribution of Trained Radiologists | -0.9% | Rural and secondary cities disproportionately affected | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront and Lifecycle Cost of MRI Scanners

Premium 3 T platforms require capital outlays above USD 2 million, and facility modifications, helium refills and annual service contracts can double total ownership cost over ten years [3]PAHO, “Mexico – Country Profile,” paho.org. With 41.37% of health spending paid out of pocket, many mid-size hospitals postpone upgrades or resort to refurbished imports that carry shorter warranties. Peso volatility magnifies budgeting risk because most coils, gradients and electronics are priced in U.S. dollars, causing leasing rates to swing alongside exchange-rate shifts. Public institutions face multi-year budget cycles that delay tender launches and prolong replacement of aging 1 T fleets. Helium-free magnets offer energy savings of 40 MWh per year per system, trimming operating expenses yet still demand high sticker prices that challenge cash-constrained providers.

Shortage and Uneven Distribution of Trained Radiologists

Mexico employs roughly 4,000 radiologists for 124 million inhabitants, equating to fewer than one specialist per imaging facility. Urban clusters attract the majority of talent, leaving secondary cities and rural zones reliant on general practitioners or outsourced teleradiology, which raises turnaround times and constrains MRI throughput. Average salaries sit near USD 73,000, which competes poorly with private-practice earnings in the United States and drives emigration of subspecialists. International training collaborations through the World Health Organization provide live case reviews and virtual fellowships, but sustainable knowledge transfer depends on local residency expansions and scholarship funding. Remote-operation platforms enable technologists to steer scanners from centralized hubs while cloud PACS route images to metropolitan readers, yet roll-out momentum hinges on broadband quality and cybersecurity investments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Architecture: Closed Leadership and Open-System Momentum

Closed scanners delivered 67.65% of Mexico MRI market revenue in 2025, reflecting hospital preference for higher field strengths and multi-sequence versatility that support complex neuro, cardiac and oncologic protocols. Facilities catering to medical tourists use closed platforms to advertise comprehensive head-to-toe packages that rival premium U.S. imaging centers. Patient-centric design pressures, however, underpin a 4.65% CAGR for open systems through 2031, as claustrophobic, bariatric and pediatric cohorts seek more comfortable environments.

Open platforms led by Fujifilm Aperto Lucent add motion-compensating sequences and permanent magnets that lower energy use, making them attractive for mid-size regional hospitals. Closed systems evolve in parallel; Canon Medical’s Vantage Galan 3 T Supreme Edition integrates AI protocols that slash scan times and minimize helium usage. As facility portfolios widen, executives mix open units for outpatient comfort with closed units for high-throughput tertiary care, anchoring balanced long-term demand across both architectures.

By Field Strength: 1.5 T Sweet Spot with Ultra-High Research Upside

1.5 T platforms captured 54.55% of Mexico MRI market share in 2025, offering cost-effective coverage across neuro, musculoskeletal and body imaging without specialized infrastructure demands. Public insurers favor 1.5 T fleets for standardization, spares interchangeability and reimbursement baselines, solidifying the modality’s entrenched position.

Ultra-high 3 T and ≥7 T units post a 4.60% CAGR to 2031, driven by academic centers and oncology institutes that require diffusion, spectroscopy and functional mapping capabilities unattainable on lower-field magnets. Siemens Healthineers’ MAGNETOM Flow 1.5 T introduces helium-light technology and AI-boosted sequences that blur the line between mid and high field strengths, extending 1.5 T viability. GE HealthCare’s head-only MRI for neuroscience research demonstrates niche demand in cognitive science that relies on ultra-high gradients for microstructural insights. Low-field ≤0.4 T units persist in pediatric wards and mobile trailers, but limited SNR confines their role to adjunct imaging in resource-restricted settings.

By Application: Neurology Dominance with Oncology Acceleration

Neurology retained 31.85% revenue in 2025, supported by aging demographics, stroke prevalence and pioneering psychiatric research such as Dr. Camilo de la Fuente-Sandoval’s glutamate-mapping studies that rely heavily on spectroscopy. Routine brain, spine and peripheral-nerve protocols drive predictable daily volumes and stable scanner revenue streams.

Oncology leads the growth curve with a 5.05% CAGR through 2031 as national screening campaigns expand MRI indications for breast, prostate and liver lesions. Multispectral techniques, dynamic contrast and whole-body diffusion sequences, coupled with emerging manganese-based contrast agents under development by GE HealthCare, deepen oncologic utility. Musculoskeletal studies remain steady due to sports-injury management and orthopedic pre-surgical planning. Cardiac and vascular applications gain momentum from rising atherosclerotic disease, while functional MRI usage spreads in academic psychology departments and pharma trials, diversifying the installed-base workload mix.

Geography Analysis

Greater Mexico City, Guadalajara and Monterrey host most MRI capacity, anchored by flagship public institutes and premium private networks that together conduct the majority of reimbursed scans. These metropolitan regions present the largest clusters of subspecialized radiologists, enabling advanced protocols like cardiac stress MRI and functional neuroimaging. Border cities such as Tijuana leverage physical proximity to California to attract outbound U.S. patients seeking scans at 40-60% price discounts, converting cross-border flows into steady equipment-utilization gains.

Coastal tourist corridors, especially Los Cabos and Cancún, integrate MRI suites into poly-specialty hospitals that package imaging with elective surgery for international clients. Northern industrial hubs benefit from employer-sponsored health plans that reimburse MRI rapidly, reinforcing procurement pipelines for private diagnostic centers. Secondary interior cities, including León and Puebla, receive new IMSS-Bienestar hospitals featuring MRI as the government inaugurates nine hospitals and six Family Medicine Units across 12 states in 2025.

Rural states in the south still depend on mobile MRI programs and periodic teleradiology support due to sparse specialist density. Government broadband initiatives promise higher bandwidth that can support cloud-based PACS and remote operation, gradually narrowing the urban-rural imaging gap. While travel times remain a barrier for some populations, shared-service agreements among regional hospitals are emerging, ensuring that newly acquired scanners generate sustainable case volumes despite distributed demand patterns.

Competitive Landscape

Global manufacturers dominate the Mexico MRI market through longstanding distributor alliances and established COFEPRIS dossiers that shorten registration timelines. Siemens Healthineers invests USD 314 million in new MRI production lines aimed at fulfilling USMCA origin thresholds, ensuring competitive pricing while bolstering local after-sales parts availability. GE HealthCare focuses on AI-enhanced workflow ecosystems, complementing hardware with predictive maintenance platforms that minimize downtime. Philips leverages helium-free BlueSeal magnets to advertise lower lifecycle costs, courting public buyers sensitive to operational expense overruns.

Canon Medical and Fujifilm capture share in mid-price segments by coupling patient-friendly designs with modular upgrade paths; their emphasis on open and low-noise configurations appeals to outpatient centers. United Imaging, Neusoft and Hyperfine are selectively entering secondary-city tenders with competitively priced bundles that include five-year service plans, although COFEPRIS approval cycles and reimbursement uncertainties temper rapid expansion.

Vendor rivalry increasingly centers on AI software ecosystems, sustainable magnet technology and turnkey teleradiology solutions that offset staffing shortages. Partnerships with local universities for research deployments of ≥7 T systems are strengthening brand visibility in the academic segment, while mobile service providers contract refurbished 1.5 T trailers to rural municipalities to widen population coverage. Across the board, suppliers now bundle remote-scanner operation and cloud PACS to mitigate the radiologist gap and secure long-term service revenues.

Mexico Magnetic Resonance Imaging (MRI) Industry Leaders

FUJIFILM Holdings Corporation

Koninklijke Philips N.V.

GE HealthCare

Siemens Healthcare GmbH

Canon Inc. (Canon Medical Systems Corporation)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Hospital Angeles Health System introduced AISHA MRI, an AI-based platform that embeds magnetic-resonance imaging into routine preventive check-ups.

- July 2025: AIRS Medical partnered with Simbioxia in Mexico to roll out SwiftMR across private radiology networks, accelerating adoption of AI-driven scan-time reduction technology.

- May 2024: Medis sponsored a hands-on Medis Suite MR workshop during the Mexican Society of Echocardiography and Cardiovascular Imaging’s three-day course, giving 40 clinicians direct experience with advanced cardio-MRI analytics.

Mexico Magnetic Resonance Imaging (MRI) Market Report Scope

As per the scope of the report, magnetic resonance imaging is a medical imaging technique used in radiology to produce pictures of the anatomy and the physiological processes of the body. These pictures are further used to diagnose and detect the presence of abnormalities in the body. The Mexico Magnetic Resonance Imaging (MRI) Market is Segmented by Architecture (Closed MRI Systems and Open MRI Systems), Field Strength (Low Field MRI Systems, High Field MRI Systems, Very High Field MRI Systems, and Ultra-high MRI Systems), Application (Oncology, Neurology, Cardiology, Gastroenterology, Musculoskeletal, and Other Applications). The report offers the value (in USD) for the above segments.

By Architecture

| Closed MRI Systems |

| Open MRI Systems |

By Field Strength

| Low-Field (≤0.4 T) |

| High-Field (1.5 T) |

| Very-High (3 T) & Ultra-High (≥7 T) |

By Application

| Neurology |

| Oncology |

| Musculoskeletal |

| Cardiology & Vascular |

| Other Clinical Applications |

| By Architecture | Closed MRI Systems |

| Open MRI Systems | |

| By Field Strength | Low-Field (≤0.4 T) |

| High-Field (1.5 T) | |

| Very-High (3 T) & Ultra-High (≥7 T) | |

| By Application | Neurology |

| Oncology | |

| Musculoskeletal | |

| Cardiology & Vascular | |

| Other Clinical Applications |

Key Questions Answered in the Report

What CAGR is forecast for the Mexico MRI market through 2031?

The market is projected to grow at a 3.98% CAGR between 2026-2031, reaching USD 235.87 million by the end of the period.

Which MRI architecture is growing fastest in Mexico?

Open systems are advancing at a 4.65% CAGR as hospitals target patient comfort and lower operational complexity.

Why are 1.5 T scanners still prevalent in Mexican hospitals?

They balance diagnostic versatility and acquisition cost, holding 54.55% of 2025 revenue and fitting most reimbursement schedules.

How is medical tourism influencing MRI demand in border regions?

Facilities in Tijuana and Los Cabos attract U.S. patients with 60% lower scan prices, sustaining high scanner utilization rates.

Page last updated on: