Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.27 Billion |

| Market Size (2026) | USD 1.36 Billion |

| Market Size (2031) | USD 1.89 Billion |

| Growth Rate (2026 - 2031) | 6.84% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico LED Lighting Market Analysis by Mordor Intelligence

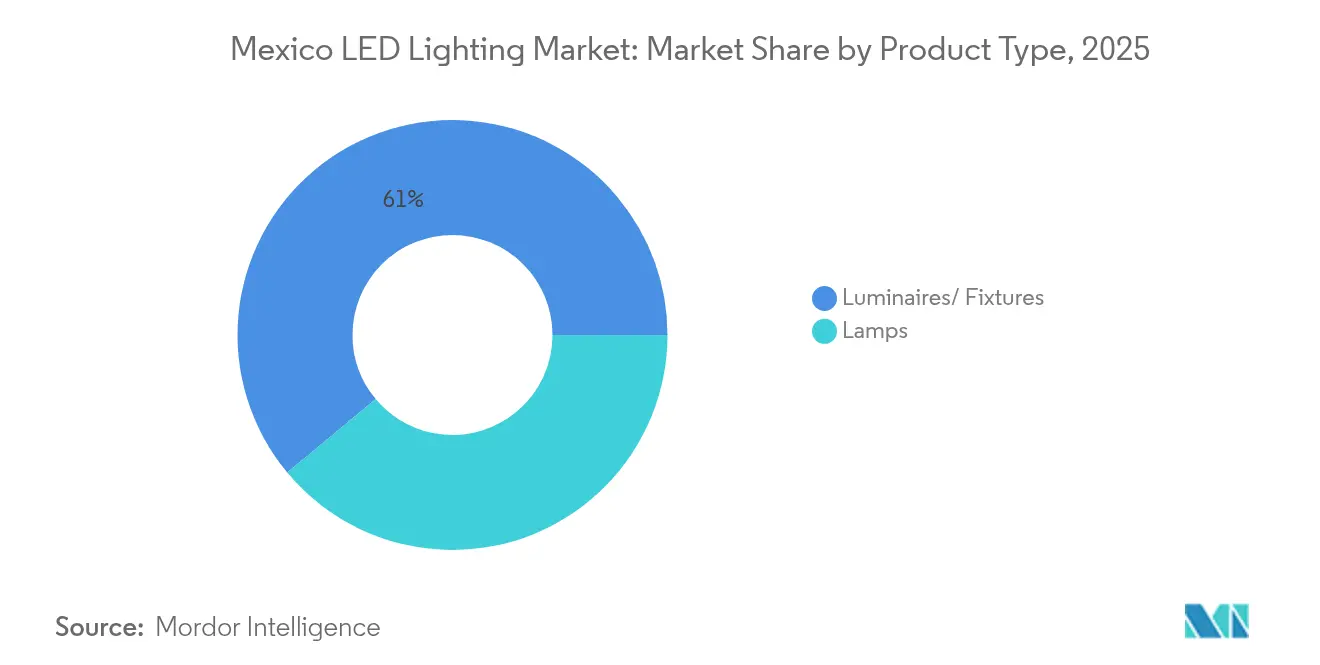

The Mexico LED lighting market size is expected to grow from USD 1.27 billion in 2025 to USD 1.36 billion in 2026 and is forecast to reach USD 1.89 billion by 2031 at 6.84% CAGR over 2026-2031. Sustained growth is tied to industrial modernization linked with near-shoring programs, federal energy-efficiency mandates, and large-scale municipal retrofits. Luminaires and fixtures, which integrate optics, heat sinks, and drivers, accounted for 61.70% of 2024 revenue, underscoring the market’s preference for system-level upgrades over basic lamp swaps. Retrofit activity dominates because legacy fluorescent and HID installations still blanket warehouses, production halls, and street corridors. Meanwhile, e-commerce procurement is growing rapidly as commercial buyers adopt online catalogs and direct-to-site delivery, challenging Mexico’s traditionally wholesale-centric hardware trade. Competitive differentiation is shifting toward control software, warranty scope, and NOM-031 compliance as price competition intensifies.

Key Report Takeaways

- By product type, luminaires commanded 61.05% of the Mexico LED lighting market share in 2025, while lamps posted the fastest growth rate of 7.35% through 2031.

- By application, the residential segment accounted for 20.12% of the Mexico LED lighting market size in 2025 and is projected to advance at an 8.58% CAGR to 2031.

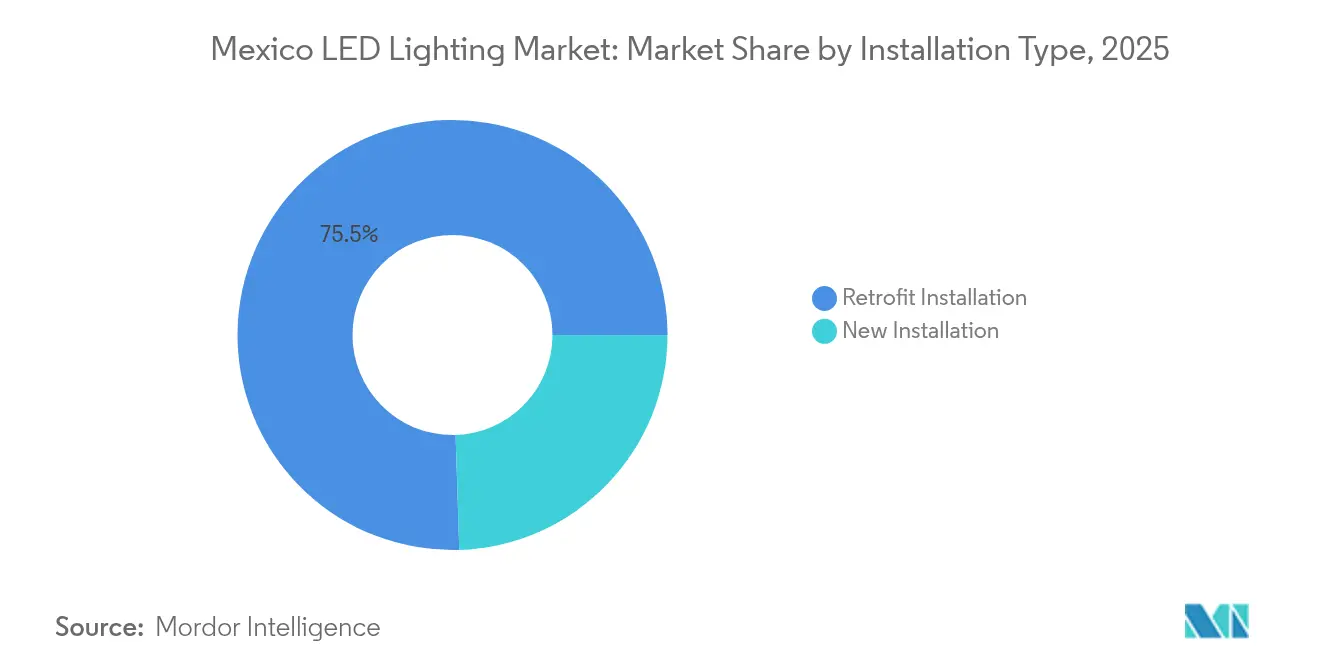

- By installation, retrofit solutions represented 75.50% of 2025 revenue; new builds are projected to register the highest 6.56% CAGR over the forecast horizon.

- By distribution channel, wholesale retained a 52.05% share in 2025, whereas e-commerce orders are rising at a 7.74% CAGR.

- By end user, indoor environments led spending in 2025; horticultural deployments are poised for the quickest expansion, albeit from a small base.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico LED Lighting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid decline in LED component prices | +1.2% | National, higher in northern industrial states | Short term (≤ 2 years) |

| Mandatory NOM-031-ENER enforcement | +1.8% | National, led by large municipalities | Medium term (2-4 years) |

| Near-shoring boom and warehouse retrofits | +1.5% | Northern border states; central manufacturing corridors | Medium term (2-4 years) |

| Growing tele-managed street-lighting tenders | +0.9% | Urban centers and coastal tourist zones | Long term (≥ 4 years) |

| Dark-sky rules in resort districts | +0.6% | Coastal tourist areas and archaeological sites | Medium term (2-4 years) |

| Rising horticultural LED demand | +0.4% | Michoacán, Jalisco, Baja California | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid decline in LED component prices

Global overcapacity has cut packaged LED die costs by roughly 15-20% each year since 2024, compressing payback periods on retrofits to under two years for many commercial users. Mexico fixture makers now source higher-performance chips without inflating BOM costs, helping them compete with uncertified imports while retaining profitability. SMEs that previously delayed projects due to capital constraints are proceeding with upgrades financed by short internal-rate-of-return thresholds. Margin erosion, however, prompts suppliers to seek scale economies, service contracts, and bundled controls to maintain earnings.

Mandatory NOM-031-ENER efficiency standard enforcement

NOM-031 requires roadway and public-area luminaires to meet specific luminous-efficacy benchmarks verified by ANCE- or NYCE-accredited labs. Systematic enforcement, strengthened in 2024, now appears prominently in municipal bid documents. Certified suppliers can price at a premium, confident that non-compliant stock will be barred from formal tenders. Private-sector buyers increasingly require the same seal to ensure access to utility rebates and to align with ESG guidelines. Compliance costs-product testing, documentation, and labeling-create a barrier to entry that raises the quality baseline across the Mexico LED lighting market.

Near-shoring boom driving industrial retrofits

Contract manufacturers shifting from Asia have accelerated LED conversions at assembly plants, distribution hubs, and logistics parks. EnTrans International retrofitted 1,609 high-bay fixtures across a 400,000 sq ft site in Ciudad Juárez, resulting in an annual reduction of more than 3.4 million kWh and a savings of USD 400,000 per year. Similar projects across Nuevo León and Coahuila require robust drivers that are tolerant of voltage swings common on industrial feeders. Certified suppliers offering extended warranties gain an edge with foreign investors who require long service contracts for environmental performance audits.

Growing municipal “tele-managed” street-lighting tenders

Cities such as Playa del Carmen and Mexico City incorporate cloud-connected nodes that relay failure alerts and enable adaptive dimming.[1]Corporate Communications, “Tele-managed Public Lighting Solutions in Mexico,” Signify, signify.com Remote control typically delivers an incremental 30-40% energy cut on top of LED baseline savings, shortening amortization to under five years even for cash-strapped councils. Integrators offering turnkey financing, network commissioning, and operator training are winning bundled concessions that include long-term operations and maintenance (O&M) clauses.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ultra-low-cost non-certified imports | −1.1% | National, strongest in price-sensitive retail | Short term (≤ 2 years) |

| Up-front CAPEX barrier for SMEs | −0.9% | National, acute in rural and developing regions | Medium term (2-4 years) |

| Limited e-waste and LED recycling capacity | −0.8% | National, more severe outside major metros | Long term (≥ 4 years) |

| Grid harmonics and voltage spikes | −0.7% | Industrial belts with aging distribution infrastructure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent presence of ultra-low-cost non-certified imports

LED bulbs shipped from Chinese ports at USD 0.50-1.50 FOB circumvent NOM testing through small-lot, multimodal distribution. Labels often misstate wattage or lumen output, and failure rates of 25-30% within 18 months are common, eroding consumer confidence. Informal retailers on border corridors and central open-air markets move high volumes of these products, undermining compliant brands that invest in accredited testing.

Up-front CAPEX barrier for small and medium enterprises

Although operating savings are clear, SMEs still struggle to finance whole-facility upgrades in a single fiscal cycle. Traditional bank loans carry high interest, and energy-service-company (ESCO) contracts remain limited outside top-tier cities. These liquidity constraints slow penetration, especially for industrial micro-enterprises that account for a large share of Mexico’s manufacturing base.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Luminaires Anchor Infrastructure Modernization

The Mexico LED lighting market size for luminaires reached USD 0.78 billion in 2025, accounting for 61.05% of the overall revenue. Integrated fixtures dominate major industrial and municipal retrofits, as buyers prefer turnkey units that bundle optics, thermal management, and controls. Demand accelerates near automotive clusters where multinational OEMs retrofit high-bay spaces to meet ISO 14001 energy targets. In parallel, the lamps subsegment records the fastest 7.35% CAGR, as residential users progressively replace screw-based bulbs as retail prices fall.

Luminaires are increasingly integrating wireless mesh radios and Bluetooth beacons, transforming lighting grids into sensing networks. Vendors such as Acuity Brands embed Atrius-ready chips for asset-tracking and HVAC interfacing. These capabilities justify premium pricing and heighten vendor lock-in; however, they also expose projects to compatibility risks if the vendor discontinues firmware support. The lamps category benefits from standardized bases that simplify DIY installation, appealing to homeowners and small shops that are less willing to hire contractors.

By Application: Residential Uptake Outpaces Commercial Growth

The residential segment captured 20.12% of 2025 revenue, while posting an 8.58% CAGR that outstrips every other application class. Lower bulb prices, broader supermarket assortments, and federal publicity on energy savings underpin household adoption of energy-efficient bulbs. For a typical urban apartment, full LED adoption can cut lighting bills by 60-80%, delivering clear pocketbook benefits.

Commercial offices, hotels, and big-box retailers retain a considerable slice of the Mexico LED lighting market, but many large chains are already undergoing second-cycle replacements, trimming annual growth. Industrial applications benefit from fresh capex tied to reshoring, though project timelines align with broader plant commissioning. Horticultural deployments, though embryonic, command premium ASPs due to narrow-band chips and corrosion-resistant housings, attracting niche specialists.

By Distribution Channel: E-commerce Nibbles at Wholesale Dominance

Wholesale outlets held 52.05% share in 2025, sustained by 100,000-plus ferreterías that serve contractors nationwide. These stores rely on multi-tier distributors that stock mixed baskets of electrical goods. Nevertheless, the e-commerce route is rising fastest, with 7.74% CAGR forecast through 2031, as corporate buyers appreciate the traceability and SKU depth of online catalogs.

Digital channels empower manufacturers to tell product stories through spec sheets, photometric files, and installation videos, features difficult to convey on crowded store shelves. Yet online marketplaces are also rife with uncertified imports, prompting savvy buyers to filter listings by NOM compliance badges.

By Installation Type: Retrofits Still Dominate but Greenfield Projects Gain Pace

Retrofit activity accounted for 75.50% of the 2025 value owing to Mexico’s vast stock of aging fluorescent and HID luminaires. Facility managers often stage upgrades zone by zone to align with maintenance budgets. Savings from occupancy sensors and daylight harvesting add incremental ROI, making retrofits one of the quickest payback measures for energy.

New-build installations are projected to climb at a 6.56% CAGR as industrial park development surges and residential construction recovers. Architects increasingly specify LED-ready track and troffer systems during design freeze, reducing later re-work. The market shift indicates the normalization of LED as the default technology rather than a premium upgrade.

By End User: Indoor Environments Present Lowest Barriers

Indoor settings such as offices, malls, and homes account for the majority of spending because climate-controlled interiors maximize LED lifetime and simplify maintenance. Industrial interiors require high-CRI options to support quality control tasks, while retail chains favor tunable-white fixtures to enhance the presentation of their merchandise.

Outdoor deployments are subject to greater thermal cycling, moisture, and surge events. Utilities and DOTs, therefore, demand rigorous ingress-protection ratings and surge-withstand documentation, lengthening procurement cycles. Automotive LEDs reside at the intersection of photometric precision and stringent AEC-Q101 reliability standards, limiting participation to globally experienced vendors such as OSRAM and Valeo.

Geography Analysis

Northern border states-Nuevo Leon, Chihuahua, Coahuila, and Tamaulipas-lead in revenue generation due to their dense manufacturing corridors that serve U.S. supply chains. Plants in Monterrey and Ciudad Juárez often specify high-bay LED fixtures with motion sensors to reduce idle-time energy consumption, thereby fostering concentrated demand for industrial-grade luminaires. Voltage anomalies in these corridors, however, necessitate reinforced driver topology and surge-protection design to safeguard warranty terms.

Central Mexico, anchored by Mexico City, Guadalajara, and Querétaro, forms the largest contiguous consumption cluster in the region. Urban municipalities have already replaced much of their sodium street lighting with LED arrays and are now pivoting toward tele-management nodes that report outages in real-time. The Bajío’s automotive supply chain sparks further indoor demand; ZKW’s USD 102 million expansion in Silao adds 15,700 m² of floor space geared for headlamp assembly lines deploying daylight-mimicking fixtures.

Coastal tourist zones such as Cancún, Playa del Carmen, and Los Cabos pursue dark-sky policies to retain pristine night views, commissioning warm-white, full-cutoff luminaires with amber or 2,700 K color temperatures. Suppliers able to fuse aesthetic lighting with turtle-friendly photometry secure premium contracts. Rural southern states lag in adoption because of lower disposable income and weaker distribution, yet they offer prospects for off-grid solar-LED kits where grid extension is uneconomical.

Competitive Landscape

The Mexico LED lighting market is moderately fragmented, with the top five brands holding under 50% of the revenue, while numerous regional firms fill the price gaps. International majors such as Signify, OSRAM, LEDVANCE, and Acuity Brands lean on dealer networks for municipal and industrial bids, bundling financing and multi-year warranties to offset higher sticker prices. Local champions-Grupo Construlita Iluminación, Optima Energia, and Illux-address budget-conscious segments with NOM-certified yet cost-efficient SKUs, leveraging proximity to expedite production tweaks.

Strategic moves reveal a pivot toward specialized niches. Acuity Brands’ acquisition of Arize horticulture assets expands reach into controlled-environment agriculture via Hort Americas distribution. Cree LED partnered with IDC Componentes to replace the streetlights in downtown Querétaro, combining U.S. chipsets with local project management. Ruggedized supplier Red Sky Lighting partnered with SUPRA Desarrollos in Monterrey, targeting heavy-duty industrial bays prone to vibration and high ambient temperatures.

Component cost erosion increases pressure on commoditized bulb makers, prompting consolidation, such as Kuzco Lighting’s 2025 buyout of Insight Lighting, which bolsters its architectural line. Automotive lighting investments-USD 45 million by SL MEX in San Luis Potosí and MXN 600 million by UTAS-NOVA in Aguascalientes-underscore Mexico’s ascent as a regional hub for advanced headlamp modules.[4]Corporate Update, “Aguascalientes Investment,” UTAS-NOVA, utas-nova.com

Mexico LED Lighting Industry Leaders

Signify N.V.

Osram Licht AG

Samsung Electronics Co., Ltd.

Acuity Brands Lighting, Inc.

Grupo Construlita Iluminación S.A. de C.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: SL MEX invested USD 45 million for a 1 million-unit headlight assembly line in San Luis Potosí.

- June 2025: OSRAM introduced PSX auxiliary automotive bulbs with extended durability for Mexico

- May 2025: Lumitex scaled medical-device LED manufacturing in Celaya, Guanajuato.

- January 2025: Kuzco Lighting acquired Insight Lighting, broadening architectural and commercial ranges for North America, including Mexico.

Mexico LED Lighting Market Report Scope

The LED (light-emitting diode) is one of the most energy-efficient and fast-developing lighting technologies. LED light bulbs manage to last longer, are more enduring, and offer adequate light quality than many other types of lighting.

Mexico's LED lighting market is segmented by product type (lamps and luminaires) and end-user vertical (residential, commercial, urban, street lighting, and industrial).

The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Product Type

| Lamps |

| Luminaires / Fixtures |

By Distribution Channel

| Direct Sales |

| Wholesale Retail |

| E-commerce |

By Application

| Commercial Offices |

| Retail Stores |

| Hospitality |

| Industrial |

| Highway and Roadway |

| Architectural |

| Public Places |

| Hospitals |

| Horticulture Gardens |

| Residential |

| Automotive |

| Others (Chemicals, Oil and Gas, Agriculture) |

By Installation Type

| New Installation |

| Retrofit Installation |

By End User

| Indoor |

| Outdoor |

| Automotive |

| By Product Type | Lamps |

| Luminaires / Fixtures | |

| By Distribution Channel | Direct Sales |

| Wholesale Retail | |

| E-commerce | |

| By Application | Commercial Offices |

| Retail Stores | |

| Hospitality | |

| Industrial | |

| Highway and Roadway | |

| Architectural | |

| Public Places | |

| Hospitals | |

| Horticulture Gardens | |

| Residential | |

| Automotive | |

| Others (Chemicals, Oil and Gas, Agriculture) | |

| By Installation Type | New Installation |

| Retrofit Installation | |

| By End User | Indoor |

| Outdoor | |

| Automotive |

Key Questions Answered in the Report

How large is the Mexico LED lighting market in 2026?

The Mexico LED lighting market size is USD 1.36 billion in 2026.

What is the forecast CAGR through 2031?

Revenue is projected to grow at a 6.84% CAGR between 2026 and 2031.

Which product category leads sales?

Integrated luminaires hold 61.05% of 2025 revenue due to preference for turnkey upgrades.

Why are retrofits so prominent?

Legacy fluorescent and HID fixtures remain widespread, giving retrofits a 75.50% revenue share in 2025.

What regulation drives public-sector demand?

Mandatory NOM-031-ENER sets minimum efficacy rules for roadway and outdoor luminaires.

Which distribution channel is growing fastest?

E-commerce orders are expanding at 7.74% CAGR as buyers embrace digital procurement.

Page last updated on: