Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

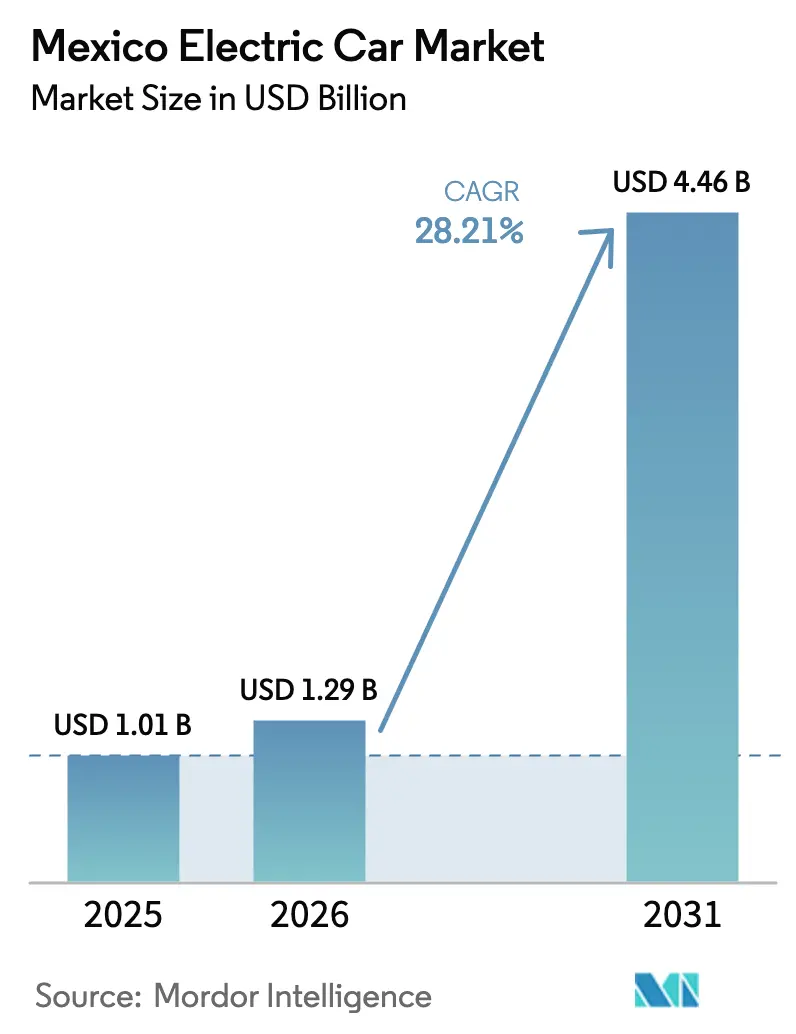

| Base Year Market Size (2025) | USD 1.01 Billion |

| Market Size (2026) | USD 1.29 Billion |

| Market Size (2031) | USD 4.46 Billion |

| Growth Rate (2026 - 2031) | 28.21% CAGR |

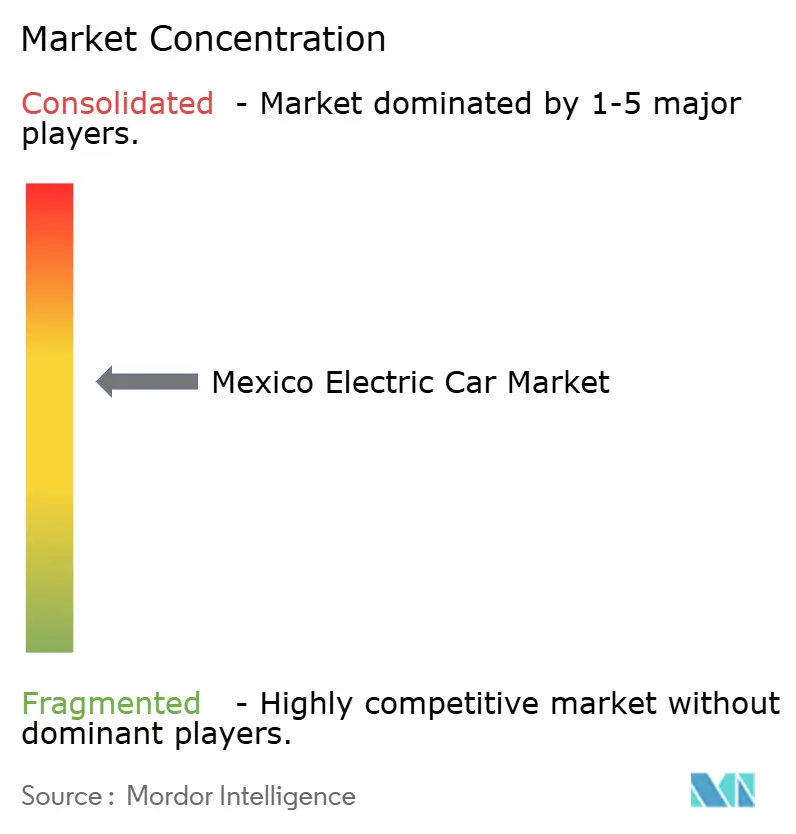

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Electric Car Market Analysis by Mordor Intelligence

The Mexico electric car market size is expected to grow from USD 1.01 billion in 2025 to USD 1.29 billion in 2026 and is forecast to reach USD 4.46 billion by 2031 at a 28.21% CAGR over 2026–2031. Driven by USMCA origin rules promoting battery and power-train localization, a federal tax framework offering substantial deductions on EV manufacturing investments, and the nationalization of lithium resources positioning the nation as a pivotal cell-making hub, the Mexican automotive landscape is witnessing a robust transformation. In response, automakers are committing significant investments to retooling, while cell suppliers are aggressively driving down lithium-iron-phosphate (LFP) pack costs, aiming to reach a more affordable threshold in the near future. While affordability pressures keep hybrids at the forefront today, the approaching cost parity is spurring faster adoption of battery-electric vehicles. Demand remains geographically concentrated, with Mexico City accounting for a substantial share. However, as Tesla's gigafactory comes online, Nuevo León is poised to rise as a significant northern hub. The competitive landscape is moderately intense: Tesla, Nissan, BYD, and General Motors together account for a major share of market volume, yet no single entity commands a dominant position.

Key Report Takeaways

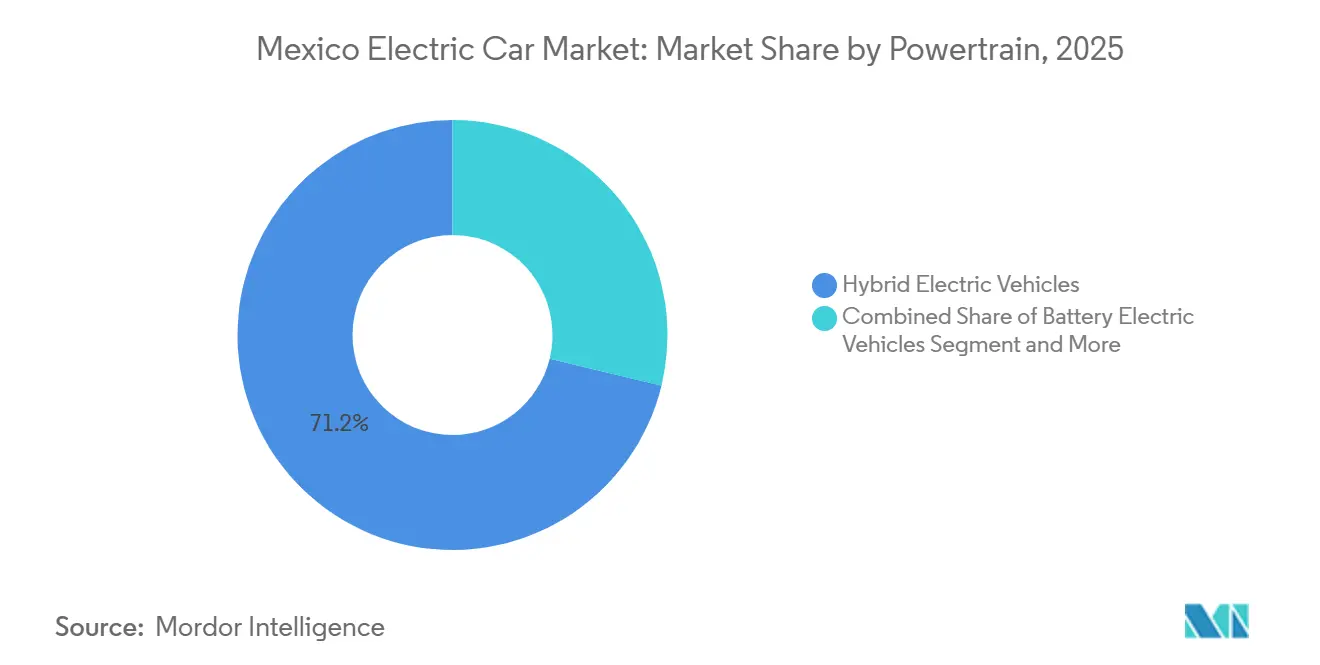

- By powertrain, hybrid electric vehicles led with 71.23% of Mexico's electric car market share in 2025, while battery electric vehicles are expanding at a 28.23% CAGR through 2031.

- By vehicle class, hatchbacks accounted for 35.61% of the Mexican electric car market in 2025, sports utility vehicles are on track for the fastest 28.37% CAGR to 2031.

- By price band, entry-level models captured 41.28% share of the Mexican electric car market in 2025 and are advancing at a 28.29% CAGR through 2031.

- By battery chemistry, lithium-iron-phosphate held 58.73% of the Mexican electric car market size in 2025 and is growing at a 28.38% CAGR to 2031.

- By motor architecture, permanent-magnet synchronous motors led with 53.28% share in 2025, induction solutions are gaining, yet remain below PMSM growth of 28.27% CAGR.

- By range, sub-200 km models captured 45.56% of 2025 registrations, whereas 200–400 km vehicles are the fastest, progressing at a 28.33% CAGR through 2031.

- By customer type, private buyers generated 78.91% of 2025 demand, but fleet and commercial operators recorded the swiftest 28.31% CAGR.

- By state, Mexico City delivered 23.47% of 2025 volumes, while Nuevo León is forecast to record the steepest 28.25% CAGR on the back of a pending gigafactory.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Mexico Electric Car Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Decline in Lithium-Iron-Phosphate Battery | +7.2% | Global, with spillover to Mexican assembly plants sourcing Chinese cells | Medium term (2-4 years) |

| Government Purchase-Tax Incentives | +6.8% | National, with early gains in Mexico City, Guadalajara, Monterrey | Short term (≤ 2 years) |

| Automaker Re-Tooling and Nearshoring | +5.9% | National, concentrated in Nuevo León, Puebla, Guanajuato, Coahuila | Medium term (2-4 years) |

| Expansion of Domestic Charging-Infrastructure | +4.1% | National, prioritizing Mexico City-Guadalajara-Monterrey corridor | Long term (≥ 4 years) |

| National Lithium Resource Nationalization | +3.2% | National, with manufacturing hubs in Sonora, Nuevo León | Long term (≥ 4 years) |

| Elimination of Import Tariffs on EVs | +1.7% | National, temporary effect tapering post-2024 | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Decline in Lithium-Iron-Phosphate Battery Pack Costs

In recent years, LFP pack pricing has experienced a significant decline, with further reductions anticipated in the near future. This trend is primarily driven by CATL's vertical integration strategies and BYD's innovative Blade architecture, which eliminates the need for module-level packaging [1]“Battery Technology Whitepaper 2024,” CATL, catl.com . As a result, entry-level hatchbacks are now being equipped with more affordable battery packs, effectively narrowing the total-cost-of-ownership gap, even before considering fuel savings. Mexican assemblers, who rely on imported cells from China, are benefiting from notable cost reductions in their bill of materials. However, they face margin risks due to the highly volatile nature of lithium-carbonate spot prices, which have shown considerable fluctuations. Additionally, the thermal stability of these packs enables the use of simpler cooling systems, which is particularly advantageous in regions with extremely high summer temperatures.

Government Purchase-Tax Incentives & Zero-Emission-Zone Mandates

Federal and municipal authorities combined a heavy tax deduction for EV manufacturing assets with zero-emission-zone enforcement in Mexico City during 2024. These levers sharply reduced after-tax capital costs for new battery, motor, and power-electronics lines, encouraging ride-hailing and last-mile fleets to electrify in dense corridors where combustion vehicles now face access penalties. The deduction remains contingent on USMCA sourcing thresholds, putting pressure on automakers to localize power-train content or risk audits that have already sparked bilateral disputes. While the policy accelerates near-term demand, its longer-term effect hinges on consistent labor-value-content interpretations and sustained municipal enforcement.

Automaker Re-Tooling and Nearshoring Under USMCA Origin Rules

In 2024, the USMCA's stipulations of a significant regional-value requirement and a labor-value floor spurred substantial retooling commitments worth billions of dollars. Volkswagen, Audi, and Ford each allocated considerable investments to transition their Mexican operations to electric platforms, ensuring eligibility for federal deductions and protection of their U.S. market access. Meanwhile, Tesla's ambitious gigafactory in Nuevo León, which secured permits in late 2023, finds itself in limbo due to tariff uncertainties. The contentious labor-value clause remains a point of contention among negotiators, with potential disputes threatening to stall investments from auxiliary suppliers.

Expansion of Domestic Charging-Infrastructure PPP Projects

In 2024, the Comisión Federal de Electricidad (CFE) rolled out a PPP blueprint, aiming to establish hundreds of fast-charging stations within a few years. These stations will dot the triangle formed by Mexico City, Guadalajara, and Monterrey, as well as key routes leading to the U.S. border. The ambitious plan, supported by significant annual investments through the end of the decade, sees a collaboration between state capital and operators like ChargePoint and Electrify America [2]“Tarifas para Estaciones Públicas de Carga Rápida,” Comisión Reguladora de Energía, gob.mx/cre . However, the rollout has been hampered by a lack of regulatory clarity. The Comisión Reguladora de Energía only set public-charging tariffs in mid-2024, causing a bottleneck in permit approvals. Currently, with a limited number of public chargers available per electric vehicle, Mexico lags behind the ratio seen in more developed markets. This gap highlights the pressing need for swift grid-interconnection approvals and an uptick in renewable capacity additions, as outlined in the National Strategy for Electric Mobility 2024-2030.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Vehicle Price | -4.5% | National, most pronounced in rural and lower-income urban areas | Long term (≥ 4 years) |

| Sparse Inter-City Fast-Charging | -3.8% | National, acute in Bajío, Yucatán, and Pacific coast states | Medium term (2-4 years) |

| Prospective 50% Tariff on Non-FTA Imports | -2.9% | National, affecting imports from China and non-USMCA markets | Short term (≤ 2 years) |

| Mild-Hybrid Classification Diluting Fiscal Incentives | -1.6% | National, regulatory ambiguity at federal and state levels | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Vehicle Price Relative to Average Household Income

In 2024, despite declining pack costs, entry-level BEVs were priced significantly higher than the median household income in Mexico. To mitigate concerns over residual values, banks are pricing EV loans noticeably higher than those for conventional vehicles, and leasing remains at a minimal penetration rate. While total-cost-of-ownership parity now benefits drivers who travel substantial distances annually, most private buyers fall short of this mileage. As a result, automakers are focusing on higher-margin SUV platforms to recover their investments in electrification, which in turn is limiting affordability for the mass market.

Sparse Inter-City Fast-Charging Corridor Coverage

In Mexico, fast chargers are predominantly found in major cities such as Mexico City, Guadalajara, and Monterrey. As a result, the corridor between Mexico City and Guadalajara has a very limited number of charging stations expected by the end of 2024. This insufficient infrastructure discourages long-distance travel and hampers the electrification of fleets, particularly for operators without access to depot charging facilities. While a trilateral plan under the USMCA, announced in 2024, aims to establish frequent charging stops along trade routes, the plan is still awaiting necessary approvals, including funding and land-use permits. Additionally, private operators are facing delays in utility interconnections. This is primarily due to the energy regulator finalizing public-charging tariffs only in mid-2024, which has consequently delayed construction timelines into the following year.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Powertrain: Hybrids Dominate, BEVs Accelerate

Hybrid electric vehicles commanded 71.23% of the 2025 share in the Mexican electric car market, a reflection of range concerns in a country where charging visibility remains low. Battery-electric vehicles, however, are advancing at a swift 28.23% CAGR that outstrips every other drivetrain and will close the gap once LFP costs hit USD 80 per kWh and public chargers proliferate. Toyota and Nissan exploit mature hybrid portfolios to serve urban buyers today, yet the surge in BEV registrations during 2024 demonstrates shifting sentiment. Plug-in hybrids occupy a narrow niche because their dual systems raise maintenance outlays, while fuel-cell models remain sidelined without hydrogen infrastructure. Looking forward, USMCA-compliant pack assembly will determine which brands can sustain margin and qualify for the federal deduction.

Consumer range anxiety explains hybrids’ current prevalence, but the trajectory leans toward full electrification as costs compress and policies tighten. BEV uptake benefits from municipal zero-emission-zone enforcement, and lithium-nationalization initiatives promise a local cathode supply that slots neatly into USMCA rules. Meanwhile, plug-in hybrids may stay relevant for rural owners with sporadic charging access, yet even that position weakens as mid-range BEVs extend beyond 300 km. Overall, rising charger density, falling pack costs, and stricter import duties converge to accelerate the BEV share within the Mexican electric car market.

By Vehicle Class: SUVs Gain as Hatchbacks Hold Urban Share

Hatchbacks held 35.61% of 2025 unit volume in the Mexican electric car market, anchored by Mexico City’s narrow streets and modest parking spaces, whereas SUVs promise the fastest 28.37% CAGR through 2031. Nissan’s Leaf and BYD’s Dolphin dominate entry-level hatchback sales at sub-USD 25,000, leveraging LFP chemistry to keep costs down. Tesla’s Model Y and Ford’s Mustang Mach-E drive SUV enthusiasm among higher-income households in Monterrey and Guadalajara, enabling automakers to amortize battery overhead across richer margins.

As global trends shift towards larger vehicles, automakers are reaping the benefits. These bigger vehicles not only absorb battery costs more efficiently but also command a premium price. Volkswagen is making a significant investment to upgrade its Puebla plant, with a clear focus on electric SUVs. Simultaneously, Audi is rolling out its own substantial initiative, zeroing in on electrifying its Q-series. However, if hatchbacks become unaffordable, it could hinder their widespread adoption, particularly in states with lower incomes. While urban areas still favor compact cars, the growing appeal of SUVs – both for their versatility and status – could alter the market dynamics, especially as charging infrastructure expands.

By Price Band: Entry Segment Leads, Premium Lags

Entry-level cars priced below USD 30,000 captured a 41.28% share of the Mexican electric car market in 2025, underscoring the primacy of affordability. This slice is also growing at 28.29% CAGR, powered by BYD’s Dolphin and Nissan’s Leaf, each equipped with 40-plus kWh LFP packs and priced fairly for the consumers. Mid-range models serve fleet buyers who weigh total-cost-of-ownership more heavily than sticker price, while premium and luxury units remain niche because import tariffs inflate costs for non-USMCA makes.

The entry momentum hinges on deep localization: bringing cell, pack, and drive-unit manufacturing inside Mexico qualifies vehicles for the CapEx deduction, potentially trimming retail prices by up to one-fifth. Tesla toes the premium-entry boundary with the Model 3 at roughly USD 35,000, but uptake concentrates in wealthier metro areas. Luxury nameplates from Audi and BMW focus on brand building rather than volume, anticipating a trickle-down once infrastructure matures.

By Battery Chemistry: LFP Ascends on Cost and Stability

Lithium-iron-phosphate held 58.73% of 2025 installations and leads growth at 28.38% CAGR, due to Chinese suppliers targeting USD 75 per kWh packs and delivering robust thermal safety in Mexico’s hot climate. BYD's Blade pack, achieving a competitive energy density, has streamlined module hardware, positioning entry hatchbacks at retail prices within an affordable range. Due to their cost resilience and temperature tolerance, LFP batteries have emerged as the go-to chemistry for widespread adoption in Mexico's electric car landscape.

Nickel-manganese-cobalt systems are crucial for premium models, ensuring an extended driving range. Both Tesla's high-end variants and Ford's Mach-E prioritize NMC for its superior energy density. However, as LFP batteries close the gap in volumetric density through cell-to-pack assembly, NMC may shift to specialized performance areas, especially if raw material prices remain unstable.

By Motor Architecture: Permanent Magnets Lead, Induction Gains

Permanent-magnet synchronous machines accounted for a 53.28% share in 2025 and are projected to climb at a 28.27% CAGR on the back of peak efficiency figures. BYD, Nissan, and Volkswagen rely on neodymium-iron-boron magnets, but price spikes in rare earths—ranging from USD 60 to USD 160 per kg—fuel supply-chain anxiety. Tesla hedges with a dual-motor approach, pairing a PMSM front unit with an induction motor at the rear.

Induction designs avoid magnets entirely and are gaining interest for cost-sensitive rear-axle deployments. Tesla’s standard-range Model 3 shows the trade-off: a minimal efficiency hit for reduced material exposure. Alternative architectures, such as switched-reluctance, remain in pilot stages, pointing toward a bifurcated future: PMSMs for efficiency-driven premium products and induction motors for frugal entry and fleet offerings within the Mexican electric car market.

By Range: Short-Range Dominates, Mid-Range Ascends

Vehicles rated under 200 km covered 45.56% of 2025 registrations, mirroring urban commuting realities and limited charging coverage. Mid-range 200–400 km models, though, are set to grow at a 28.33% CAGR as CFE’s 200 planned fast chargers come online. BYD’s Dolphin (180 km) and Nissan’s Leaf (226 km) command lower tiers, while Tesla’s Model 3 Long Range and Ford’s Mach-E cater to premium clientele seeking 400 km plus.

The mid-range sweet spot gains relevance once corridor charging improves, enabling ride-hailing and light logistics fleets to run inter-city loops. Long-range (400–600 km) units remain price-limited, and ultra-long (more than 600 km) offerings are niche due to pack costs beyond USD 15,000. Scaling charger density thus becomes pivotal if mid-range formats are to capture volume from short-range incumbents within the Mexican electric car market.

By Customer Type: Private Buyers Lead, Fleets Accelerate

Private buyers generated 78.91% of 2025 demand, reflecting early-adopter enthusiasm in urban centers. Fleet and commercial users, however, should post a 28.31% CAGR as zero-emission zones in Mexico City and forthcoming procurement mandates nudge ride-hailing and delivery operators to electrify. Total-cost-of-ownership parity already exists for duty cycles over 20,000 km annually at commercial electricity rates around MXN 2.00 per kWh. Yet upfront leasing models are scarce, limiting smaller operators that cannot shoulder purchase risks.

Government fleets remain small but symbolically important, as federal guidelines favor USMCA-compliant models. Private financing barriers, notably higher loan rates for EVs, keep fleet managers exploring subscription options, and battery leasing may emerge as a workaround once residual-value clarity improves.

Geography Analysis

Mexico City held 23.47% of the 2025 demand for the Mexican electric car market, empowered by zero-emission corridors that grant electrified fleets unimpeded access to high-traffic boroughs. Estado de México added an estimated one-fifth share, yet sparser suburban charger density tempers further gains. Nuevo León, presently smaller, is primed for a 28.25% CAGR toward 2031 as gigafactory supply chains ripple through local SMEs and 700 public chargers blanket Monterrey highways. The state has already earmarked a vast amount in tax and infrastructure support, envisioning a cross-border logistics hub that links Texas demand with localized Mexican content.

In March 2024, BYD set its sights on Guadalajara, Jalisco, eyeing a substantial manufacturing plant expected to employ thousands of workers. However, the project's momentum hinges on clarity regarding U.S. tariffs. The brand's heavy dependence on Chinese components raises potential USMCA threshold concerns. Meanwhile, Puebla successfully attracted significant investments from Volkswagen and Audi in 2024. This achievement was bolstered by Puebla's extensive network of hundreds of suppliers and advantageous rail connections to U.S. markets. Not to be outdone, Guanajuato welcomed a major drive-unit line from Ford in Irapuato, a decision driven by the region's labor-value compliance. Collectively, these Bajío states are forging a mid-continental EV corridor, positioning themselves as a formidable rival to the northern cluster.

Yet, beyond these hubs, regions like Yucatán, Baja California, and Chiapas are still in the nascent stages of electric mobility. Challenges such as lower income levels, underdeveloped grid infrastructure, and their remoteness from primary supply chains hinder progress. The National Strategy for Electric Mobility sets ambitious targets: a significant portion of electricity from renewable sources and a substantial increase in new capacity. However, lagging transmission upgrades pose a risk of charging congestion. In 2024, a trilateral USMCA corridor was unveiled, aiming to install chargers at regular intervals along key trading routes. Yet, challenges in site acquisition and financing leave inter-city coverage inconsistent, primarily extending only along the Mexico City-Guadalajara-Monterrey route.

Competitive Landscape

In recent years, Tesla, Nissan, BYD, and General Motors have emerged as key players in the Mexican electric car market, collectively holding a significant share of registrations. However, no single company has managed to dominate the market entirely. Tesla's competitive advantage lies in its extensive Supercharger network and direct-sales strategy, which appeals strongly to premium consumers in regions like Nuevo León and Mexico City. Despite this, Tesla's large-scale gigafactory remains inactive as it awaits clarity on tariffs, leaving its imports susceptible to potential increases in U.S. duties. Nissan has streamlined its EV production by consolidating operations at its Aguascalientes facility after closing another plant, which has reduced costs but also limited its ability to expand. General Motors, on the other hand, scaled back operations at its Ramos Arizpe facility due to weak demand for one of its EV models in the U.S.

BYD has set ambitious sales targets in Mexico and is actively shipping vehicles through Lázaro Cárdenas, even as the government considers imposing high tariffs on imports that do not comply with USMCA regulations. Meanwhile, SAIC's MG brand and Great Wall Motor's ORA sub-brand have submitted plans to establish factories but are still awaiting final approvals. There is a notable opportunity in the market for affordable hatchbacks and commercial vans with moderate driving ranges, as these segments remain underserved by established manufacturers who are focusing more on higher-margin SUVs.

Technological advancements are creating a clear divide in the market. Premium brands are integrating advanced features such as over-the-air updates and Level 3 driver assistance systems, while budget competitors are prioritizing cost efficiency by excluding certain features. Recently, patent filings with IMPI have seen a significant increase, particularly in areas like battery thermal management and silicon-carbide inverters, highlighting the growing intensity of research and development efforts within Mexico's electric vehicle industry.

Mexico Electric Car Industry Leaders

Anhui Jianghuai Automobile (JAC)

Bayerische Motoren Werke AG

Daimler AG (Mercedes-Benz AG)

Ford Motor Company

Toyota Motor Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Ford introduced hybrid variants of the Territory SUV in Mexico, pairing a 1.5 L engine with an electric motor to challenge rivals such as Toyota RAV4 and Kia Sportage.

- May 2024: BYD debuted the Shark mid-size hybrid pickup in Mexico, marking its first offshore product launch and targeting entrenched nameplates like Toyota Tacoma and Ford Ranger.

Mexico Electric Car Market Report Scope

The scope of the report includes Powertrain (BEVs, HEVs, and More), Vehicle Class (Hatchback, Sedan, and More), Price Band (Entry, Mid-Range, and More), Battery Chemistry (LFP, NMC, and More), Motor Architecture (PMSM, Induction, and Others), Range (Short, Mid, and More), Customer Type (Private and More), and State.

By Powertrain

| Battery Electric Vehicles (BEVs) |

| Hybrid Electric Vehicles (HEVs) |

| Plug-in Hybrid Electric Vehicles (PHEVs) |

| Fuel Cell Electric Vehicles (FCEVs) |

By Vehicle Class

| Hatchback |

| Sedan |

| Sports Utility Vehicles |

| Multi Purpose Vehicles |

By Price Band

| Entry |

| Mid-Range |

| Premium |

| Luxury |

By Battery Chemistry

| Lithium Iron Phosphate (LFP) |

| Lithium Nickel Manganese Cobalt Oxide (NMC) |

| Lithium Nickel Cobalt Aluminum Oxide (NCA) |

| Others |

By Motor Architecture

| Permanent Magnet Synchronous / Interior Magnet |

| Induction Motors |

| Others (SRM, Axial Flux, etc.) |

By Range

| Short (0–200 km) |

| Mid (200–400 km) |

| Long (400–600 km) |

| Ultra-Long (>600 km) |

By Customer Type

| Private |

| Fleet & Commercial |

| Govt / Municipal |

By State

| Mexico City (CDMX) |

| Estado de México |

| Nuevo León |

| Jalisco |

| Puebla |

| Guanajuato |

| Others |

| By Powertrain | Battery Electric Vehicles (BEVs) |

| Hybrid Electric Vehicles (HEVs) | |

| Plug-in Hybrid Electric Vehicles (PHEVs) | |

| Fuel Cell Electric Vehicles (FCEVs) | |

| By Vehicle Class | Hatchback |

| Sedan | |

| Sports Utility Vehicles | |

| Multi Purpose Vehicles | |

| By Price Band | Entry |

| Mid-Range | |

| Premium | |

| Luxury | |

| By Battery Chemistry | Lithium Iron Phosphate (LFP) |

| Lithium Nickel Manganese Cobalt Oxide (NMC) | |

| Lithium Nickel Cobalt Aluminum Oxide (NCA) | |

| Others | |

| By Motor Architecture | Permanent Magnet Synchronous / Interior Magnet |

| Induction Motors | |

| Others (SRM, Axial Flux, etc.) | |

| By Range | Short (0–200 km) |

| Mid (200–400 km) | |

| Long (400–600 km) | |

| Ultra-Long (>600 km) | |

| By Customer Type | Private |

| Fleet & Commercial | |

| Govt / Municipal | |

| By State | Mexico City (CDMX) |

| Estado de México | |

| Nuevo León | |

| Jalisco | |

| Puebla | |

| Guanajuato | |

| Others |

Market Definition

- Vehicle Type - The category includes passenger cars.

- Vehicle Body Type - This include various body types such as Hatchbacks, Sedans, Sports Utility Vehicles, and Multi-purpose Vehicles.

- Fuel Category - The category exclusively covers electric propulsion systems, including various types such as HEV (Hybrid Electric Vehicles), PHEV (Plug-in Hybrid Electric Vehicles), BEV (Battery Electric Vehicles), and FCEV (Fuel Cell Electric Vehicles).

| Keyword | Definition |

|---|---|

| Electric Vehicle (EV) | A vehicle which uses one or more electric motors for propulsion. Includes cars, buses, and trucks. This term includes all-electric vehicles or battery electric vehicles and plug-in hybrid electric vehicles. |

| BEV | A BEV relies completely on a battery and a motor for propulsion. The battery in the vehicle must be charged by plugging it into an outlet or public charging station. BEVs do not have an ICE and hence are pollution-free. They have a low cost of operation and reduced engine noise as compared to conventional fuel engines. However, they have a shorter range and higher prices than their equivalent gasoline models. |

| PEV | A plug-in electric vehicle is an electric vehicle that can be externally charged and generally includes all-electric vehicles as well as plug-in hybrids. |

| Plug-in Hybrid EV | A vehicle that can be powered either by an ICE or an electric motor. In contrast to normal hybrid EVs, they can be charged externally. |

| Internal combustion engine | An engine in which the burning of fuels occurs in a confined space called a combustion chamber. Usually run with gasoline/petrol or diesel. |

| Hybrid EV | A vehicle powered by an ICE in combination with one or more electric motors that use energy stored in batteries. These are continually recharged with power from the ICE and regenerative braking. |

| Commercial Vehicles | Commercial vehicles are motorized road vehicles designed for transporting people or goods. The category includes light commercial vehicles (LCVs) and medium and heavy-duty vehicles (M&HCV). |

| Passenger Vehicles | Passenger cars are electric motor– or engine-driven vehicles with at least four wheels. These vehicles are used for the transport of passengers and comprise no more than eight seats in addition to the driver’s seat. |

| Light Commercial Vehicles | Commercial vehicles that weigh less than 6,000 lb (Class 1) and in the range of 6,001–10,000 lb (Class 2) are covered under this category. |

| M&HDT | Commercial vehicles that weigh in the range of 10,001–14,000 lb (Class 3), 14,001–16,000 lb (Class 4), 16,001–19,500 lb (Class 5), 19,501–26,000 lb (Class 6), 26,001–33,000 lb (Class 7) and above 33,001 lb (Class 8) are covered under this category. |

| Bus | A mode of transportation that typically refers to a large vehicle designed to carry passengers over long distances. This includes transit bus, school bus, shuttle bus, and trolleybuses. |

| Diesel | It includes vehicles that use diesel as their primary fuel. A diesel engine vehicle have a compression-ignited injection system rather than the spark-ignited system used by most gasoline vehicles. In such vehicles, fuel is injected into the combustion chamber and ignited by the high temperature achieved when gas is greatly compressed. |

| Gasoline | It includes vehicles that use gas/petrol as their primary fuel. A gasoline car typically uses a spark-ignited internal combustion engine. In such vehicles, fuel is injected into either the intake manifold or the combustion chamber, where it is combined with air, and the air/fuel mixture is ignited by the spark from a spark plug. |

| LPG | It includes vehicles that use LPG as their primary fuel. Both dedicated and bi-fuel LPG vehicles are considered under the scope of the study. |

| CNG | It includes vehicles that use CNG as their primary fuel. These are vehicles that operate like gasoline-powered vehicles with spark-ignited internal combustion engines. |

| HEV | All the electric vehicles that use batteries and an internal combustion engine (ICE) as their primary source for propulsion are considered under this category. HEVs generally use a diesel-electric powertrain and are also known as hybrid diesel-electric vehicles. An HEV converts the vehicle momentum (kinetic energy) into electricity that recharges the battery when the vehicle slows down or stops. The battery of HEV cannot be charged using plug-in devices. |

| PHEV | PHEVs are powered by a battery as well as an ICE. The battery can be charged through either regenerative breaking using the ICE or by plugging into some external charging source. PHEVs have a better range than BEVs but are comparatively less eco-friendly. |

| Hatchback | These are compact-sized cars with a hatch-type door provided at the rear end. |

| Sedan | These are usually two- or four-door passenger cars, with a separate area provided at the rear end for luggage. |

| SUV | Popularly known as SUVs, these cars come with four-wheel drive, and usually have high ground clearance. These cars can also be used as off-road vehicles. |

| MPV | These are multi-purpose vehicles (also called minivans) designed to carry a larger number of passengers. They carry between five and seven people and have room for luggage too. They are usually taller than the average family saloon car, to provide greater headroom and ease of access, and they are usually front-wheel drive. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all its reports.

- Step-1: Identify Key Variables: To build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built based on these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. Market revenue is calculated by multiplying the sales volume with their respective average selling price (ASP). While estimating ASP factors like average inflation, market demand shift, manufacturing cost, technological advancement, and varying consumer preference, among others have been taken into account.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms.