Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

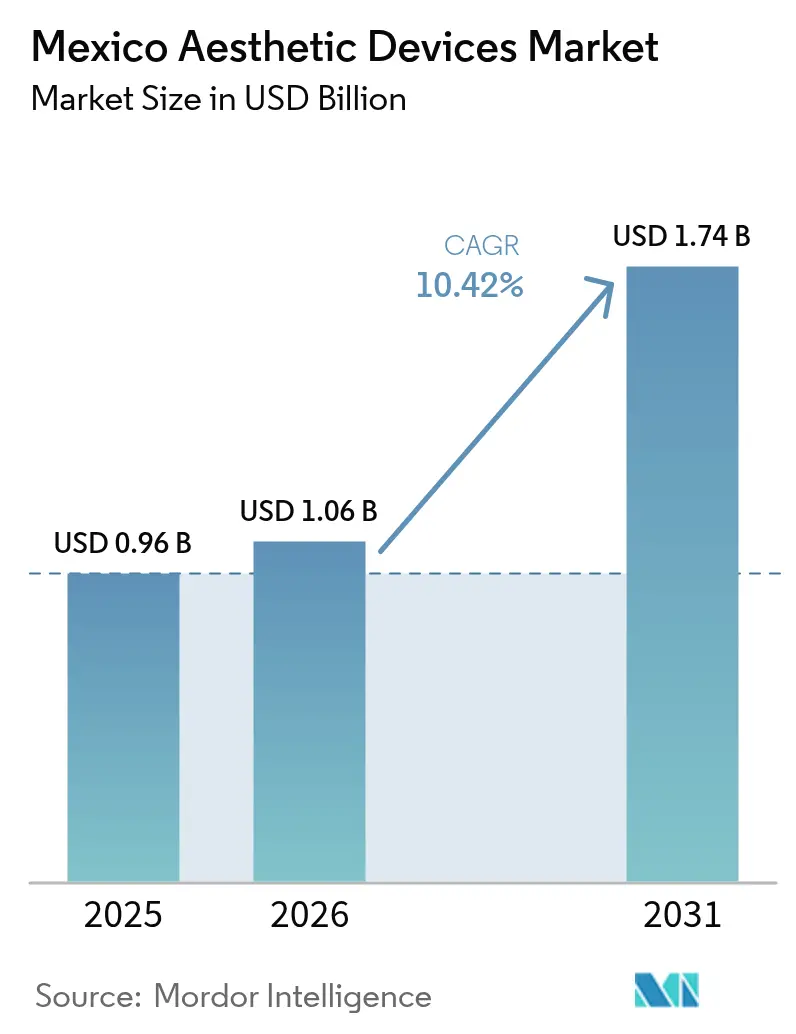

| Base Year Market Size (2025) | USD 0.96 Billion |

| Market Size (2026) | USD 1.06 Billion |

| Market Size (2031) | USD 1.74 Billion |

| Growth Rate (2026 - 2031) | 10.42% CAGR |

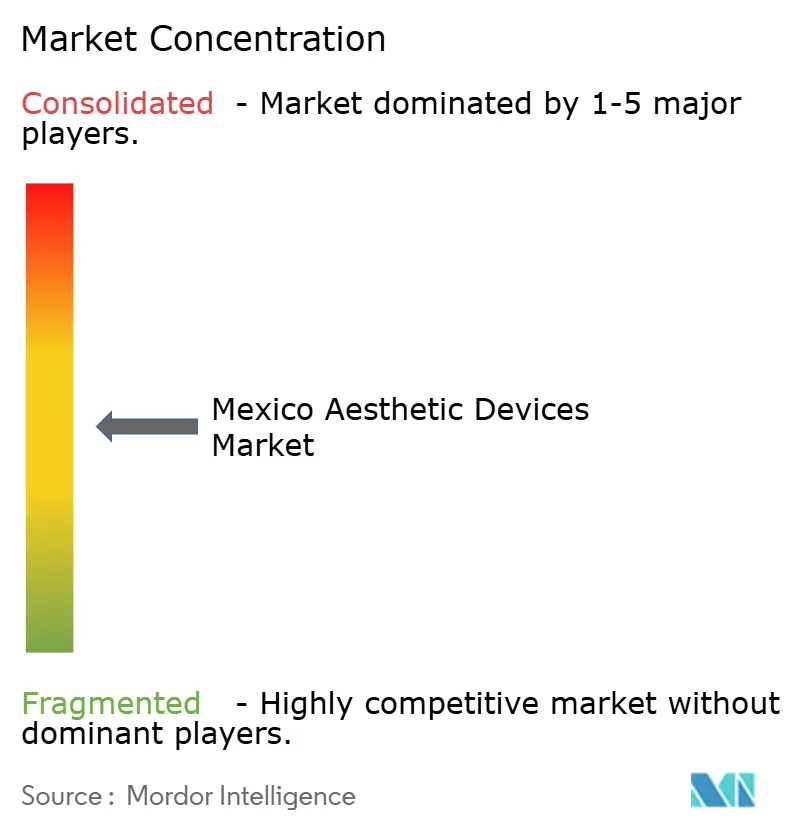

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Aesthetic Devices Market Analysis by Mordor Intelligence

Mexico aesthetic devices market size in 2026 is estimated at USD 1.06 billion, growing from 2025 value of USD 0.96 billion with 2031 projections showing USD 1.74 billion, growing at 10.42% CAGR over 2026-2031.

Favorable regulatory pathways, a booming medical-tourism sector, and rising interest in minimally invasive procedures combine to keep the Mexico aesthetic devices market on a strong growth track. Energy-based technologies maintain leadership because they are versatile, quick to adopt under COFEPRIS equivalency rules, and well suited to address skin-tightening needs that follow weight-loss drug uptake. Hair-removal platforms continue to capture steady year-round demand, while body-contouring devices accelerate as post-GLP-1 patients seek solutions for residual laxity. Domestic utilization remains dominated by urban clinics, yet the home-use channel is expanding rapidly, supported by e-commerce and fintech payment options that lower up-front costs.

Key Report Takeaways

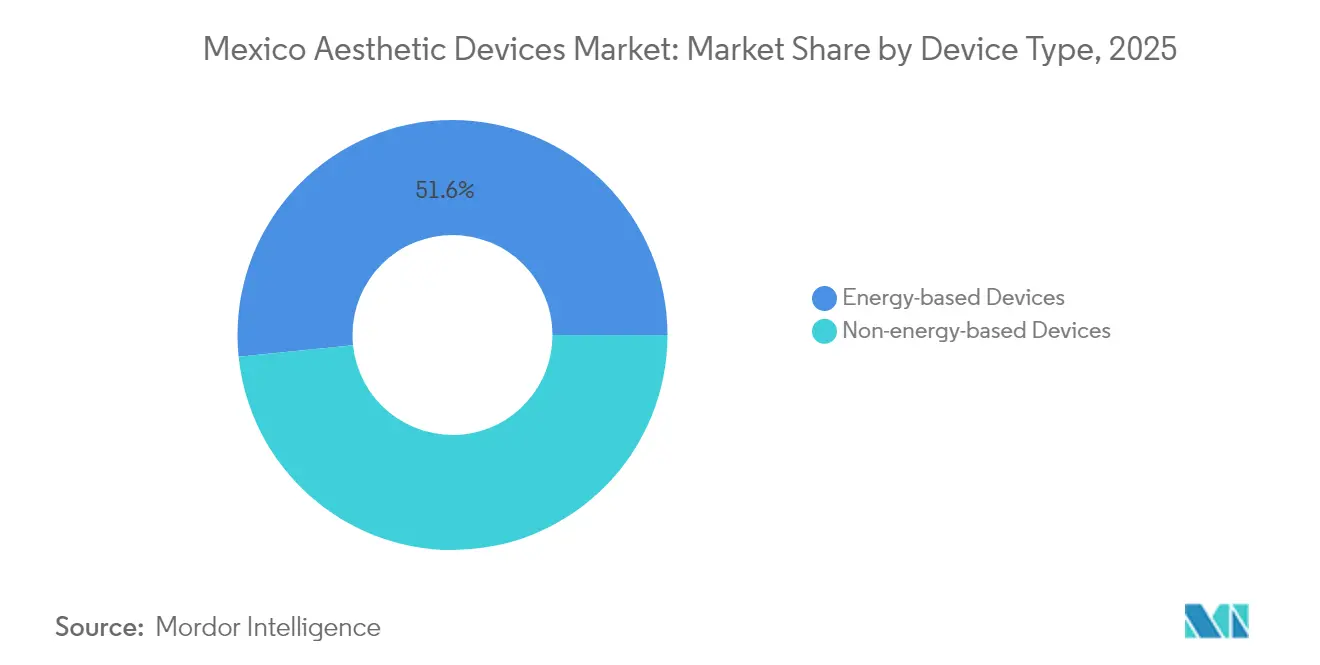

- By device type, energy-based platforms captured 51.62% of the Mexico aesthetic devices market share in 2025, and radio-frequency systems are advancing at a 13.45% CAGR through 2031.

- By application, hair-removal treatments held 30.08% share of the Mexico aesthetic devices market size in 2025, while body-contouring procedures are set to grow at a 12.18% CAGR through 2031.

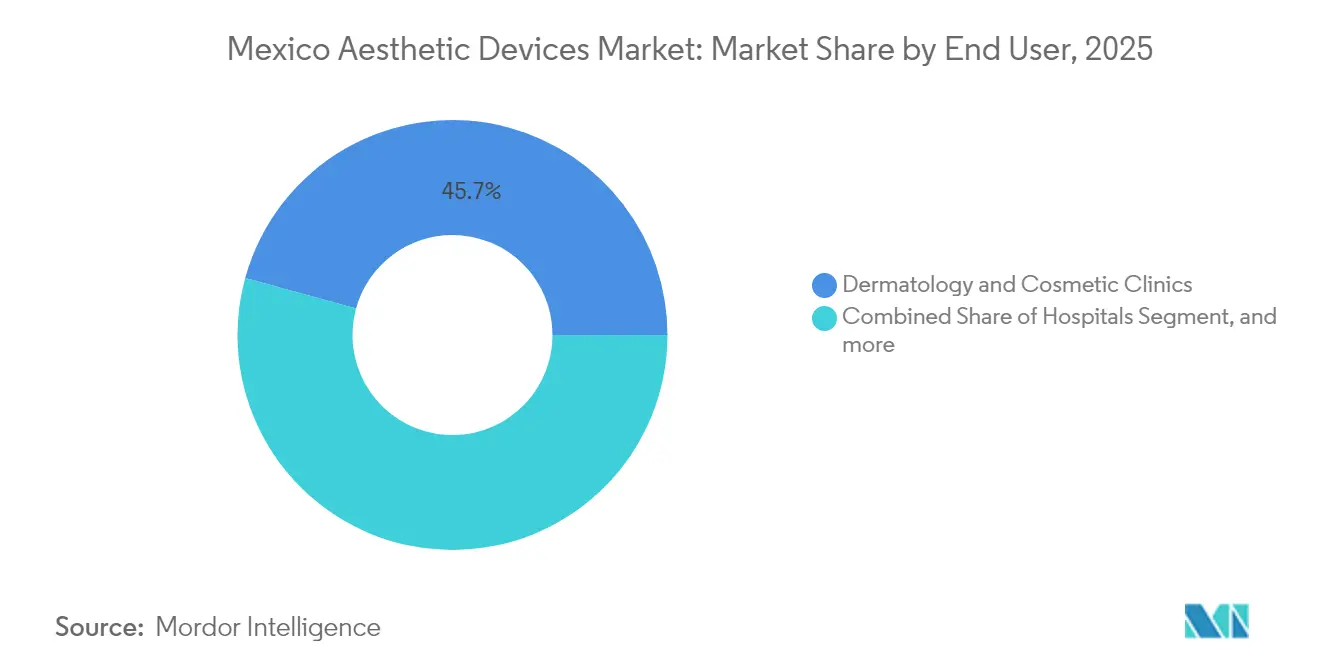

- By end user, dermatology and cosmetic clinics commanded 45.73% revenue in 2025, whereas home-use devices represent the fastest growing channel with an 11.3% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Aesthetic Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Aesthetic Consciousness & Obesity Prevalence | +3.2% | National, with concentration in major metropolitan areas | Medium term (2-4 years) |

| Demand For Minimally-/Non-Invasive Procedures | +2.8% | Global trend with strong adoption in Mexico's tier-1 cities | Short term (≤ 2 years) |

| Growth In Inbound Medical Tourism | +2.1% | Border states and major cities, spillover to coastal regions | Medium term (2-4 years) |

| COFEPRIS "Equivalency" Fast-Track For FDA-Approved Devices | +1.5% | National regulatory framework | Short term (≤ 2 years) |

| Social-Media Micro-Influencers in Tier-2 Cities | +0.8% | Tier-2 cities with expanding digital infrastructure | Long term (≥ 4 years) |

| Fintech BNPL Financing for Cosmetic Treatments | +0.6% | Urban centers with established fintech penetration | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Aesthetic Consciousness & Obesity Prevalence

Obesity rates above 35% in many Mexican states have heightened public awareness of body image, encouraging patients to pair pharmacological weight-loss solutions with post-reduction skin-tightening therapies. Surgeons report a consistent uptick in combination treatments that address volume loss and tissue laxity after rapid weight change. Social-media platforms amplify this trend by showcasing before-and-after outcomes and by normalizing aesthetic intervention among younger age groups. Device makers respond with multipolar radio-frequency systems marketed for flexible use on face and body, allowing clinics to widen service menus without heavy incremental spending. The combined clinical need and cultural acceptance is expected to keep skin-tightening platforms in double-digit growth across the forecast window.

Demand For Minimally/Non-Invasive Procedures

Patient preference continues to migrate toward procedures that require no general anesthesia, minimal downtime, and limited follow-up. CO2 laser resurfacing, fractional radio-frequency microneedling, and low-intensity ultrasound collectively anchor this shift by achieving visible results in one or two sessions. Smaller-format devices help providers run leaner operating models, giving clinics higher throughput and faster returns on investment. Price-sensitive local consumers view non-surgical treatments as incremental steps rather than once-a-decade events, boosting procedural frequency per patient. The same-day-return appeal is particularly important for medical tourists whose stays average 3–5 days.[1]Medical Tourism Review Team, “Health Tourism in Mexico,” medicaltourism.review

Growth in Inbound Medical Tourism

Total medical-tourism revenue reached USD 8 billion in 2024, with aesthetic interventions accounting for 40% of receipts.[2]Verónica M. Garrido, “México, destino mundial del bisturí: luces y sombras del turismo estético,” El País, elpais.com Cross-border price gaps north of 50% versus U.S. providers underpin this flow, while Joint Commission International accreditations give foreign patients confidence to book. High-demand procedures such as liposuction and “mommy makeovers” require multi-modality equipment that blends suction-assisted fat removal with thermal skin contraction, driving capital expenditure on bundled energy platforms. Border clinics market rapid-turnaround packages that match U.S. postoperative standards, reinforcing Mexico’s position as the second-ranked global destination for plastic-surgery travel.

COFEPRIS “Equivalency” Fast-Track For FDA-Approved Devices

The 2024 equivalency agreement cuts average registration times from 10–18 months to 6–12 months, slashing holding-cost risk for global manufacturers entering the Mexico aesthetic devices market.[3]Pure Global, “COFEPRIS Mexico Medical Device Regulations,” pureglobal.com Reduced wait times improve product-refresh cycles, letting clinics acquire latest-generation devices sooner and retire obsolete units faster. Equivalency also lowers legal uncertainty; providers can advertise FDA-cleared performance claims without running afoul of domestic labeling rules. As renewals stay valid for five years, well-capitalized players gain a compliance edge that smaller importers struggle to match.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Procedure Cost & Limited Reimbursement | -2.3% | National, with greater impact in lower-income regions | Long term (≥ 4 years) |

| Shortage of Trained Dermatologists Beyond Metros | -1.8% | Tier-2 and tier-3 cities, rural areas | Long term (≥ 4 years) |

| COFEPRIS Backlog Delaying New Device Approvals | -1.2% | National regulatory framework | Short term (≤ 2 years) |

| Counterfeit Injectables Eroding Patient Trust | -0.9% | Border regions and unregulated clinic areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Procedure Cost & Limited Reimbursement

Aesthetic devices are almost always funded out-of-pocket, and average treatment courses can equal two months of median household income outside major cities. Although fintech “buy now, pay later” platforms offer installment plans, usage remains clustered in Mexico City, Monterrey, and Guadalajara. Public insurers exclude elective aesthetics, which caps uptake among younger professionals balancing multiple debt obligations. Clinics therefore rely on discount bundles and loyalty programs to retain cost-conscious customers. Up-front fees also deter rural residents from traveling for treatments, slowing penetration rates in secondary markets.

Shortage of Trained Dermatologists Beyond Metros

Specialist density skews heavily toward urban centers, leaving many states below half the OECD benchmark for dermatology coverage. Energy-based systems require certified operators to avoid burns and pigmentary complications, so under-served regions depend on periodic visiting specialists rather than full-time staff. Nurse-led medical spas help bridge the gap but face varying state-level scope-of-practice rules. The supply imbalance limits device sales to clinics able to recruit or retain qualified supervisors, creating pockets of latent demand that remain untapped until workforce pipelines expand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Energy-Based Technologies Lead Innovation

Energy-based platforms generated 51.62% of the Mexico aesthetic devices market in 2025 and are expected to outpace non-energy counterparts through 2031 as radio-frequency systems alone expand at a 13.45% CAGR. Providers value software-driven parameter libraries that shorten staff training and reduce adverse-event risk. Laser hair-removal units remain entry-level staples, while fractional CO2 lasers command premium price points among high-volume practices.

Market momentum is reinforced by COFEPRIS equivalency rules that permit quicker import clearance for FDA-listed devices, sparing suppliers redundant clinical testing. Non-energy devices, which accounted for 48.38% revenue in 2025, stay relevant in injectables and implants but face longer product-refresh cycles. Botulinum toxin continues to dominate the wrinkle-relaxer category, yet counterfeit threats compel reputable brands to invest in serialization and tamper-evident packaging. Chemical peels and microdermabrasion systems serve price-sensitive segments but show single-digit growth given limited differentiation potential.

By Application: Body Contouring Accelerates Post-GLP-1 Adoption

Hair-removal retained 30.08% of the Mexico aesthetic devices market share in 2025 thanks to consistent demand in a warm climate where year-round skin exposure drives grooming habits. Nevertheless, body-contouring is the star performer, advancing at a 12.18% CAGR through 2031 as patients who lose weight via GLP-1 medications seek non-surgical skin retraction. The Mexico aesthetic devices market size for body-contouring treatments is on track to more than double by 2030, aided by devices that merge thermal and mechanical effects for deeper tissue remodeling. Combination protocols bundle fat-reduction sessions with RF skin tightening, leading clinics to favor multi-handpiece consoles to maximize room turnover.

Skin-resurfacing and tightening also enjoy robust adoption as urban millennials aim for preventive maintenance rather than late-stage correction. Tattoo-removal platforms earn higher margins per pulse but remain geographically concentrated in entertainment and industrial hubs. Breast-augmentation device demand is steady in border surgery centers, where U.S. patients can schedule implant procedures and postoperative device-assisted lymphatic drainage in a single visit. Acne-scar therapies pick up speed among teenagers and working adults, propelled by social-media filter-free photo trends that spotlight skin texture.

By End User: Home-Use Devices Disrupt Traditional Models

Dermatology and cosmetic clinics commanded 45.73% revenue in 2025, benefiting from centralized specialist talent and the ability to finance high-ticket capital equipment. Hospital-based aesthetics represent a niche focused on complex reconstructive work but concede ground to outpatient facilities that offer shorter waiting lists. Home-use platforms, however, are the fastest mover, charting an 11.3% CAGR through 2031 as connected devices with AI-guided treatment modes win regulatory clearances.

Device makers increasingly design safety overrides into consumer units, such as skin-tone sensors and auto-dimming power controls, to meet COFEPRIS standards. Subscription refill models for LED masks and microcurrent probes create recurring revenue, while retail pharmacies expand shelf space for compact devices under the national “Pharmacies for Well-being” program. Medical spas ride the crossover wave by selling take-home kits that complement in-clinic courses, thus extending patient engagement beyond the appointment.

Geography Analysis

Border states including Baja California, Chihuahua, and Nuevo León dominate cross-border patient inflow, leveraging proximity to the U.S. and streamlined customs handling for imported devices. Clinics in these corridors market same-day body-contouring and injectables bundles that fit within a weekend itinerary, pushing device utilization rates above the national average. Certification under international hospital-quality regimes gives operators pricing power without dampening volume, sustaining a premium sub-segment within the broader Mexico aesthetic devices market.

Coastal destinations such as Quintana Roo capture longer-stay tourists who combine elective surgery with leisure, resulting in bundled accommodation and recovery packages. Municipal incentives for medical “clusters” provide tax relief on new equipment, encouraging rapid adoption of radio-frequency body-shaping consoles that suit post-operative care paths. Mexico City, Monterrey, and Guadalajara remain the largest domestic markets by virtue of dense dermatologist populations and higher per-capita disposable income. The Mexico aesthetic devices market size in these metros is forecast to expand at a compound 8.8% clip, marginally below the national rate due to a higher maturity base.

Tier-2 cities like Puebla and León are emerging growth pockets as social-media campaigns translate aesthetic awareness into first-time consultations. Nonetheless, specialist scarcity restrains procedure throughput, motivating clinics to deploy devices featuring pre-set protocols that nursing staff can run under remote supervision. Rural regions lag both in purchasing power and in specialist access; however, home-use laser epilators are beginning to close the gap, supported by greater mobile-payment adoption and nationwide courier networks. Public-sector procurement guidelines that allow federal agencies to import FDA-cleared devices without separate local authorization may widen future geographic reach for entry-level units.

Regulatory Landscape

Aesthetic devices in Mexico are regulated as medical devices and generally require COFEPRIS sanitary registration (registro sanitario) before commercialization, with registrations valid for five years. Foreign manufacturers typically work through a Mexico Registration Holder (MRH) to manage the registration locally, while manufacturing and quality compliance are tied to mandatory GMP requirements under NOM-241-SSA1-2021.

In 2025, COFEPRIS made process changes that affect time-to-market and compliance workloads. An abbreviated regulatory pathway became effective on September 1, 2025, enabling reliance on prior approvals from recognized reference regulators for certain submissions, and COFEPRIS issued GMP documentation submission guidelines in March 2025 for new registrations, extensions, and modifications. On the standards side, NOM-137-SSA1-2025 updated medical device labeling requirements with enhanced traceability elements and broader symbol usage, with mandatory compliance set for May 14, 2027, which pushes suppliers to plan packaging and IFU transitions in advance.

Competitive Landscape

The competitive field is moderately concentrated: the top five multinationals control a significant market share of the Mexican aesthetic devices market. AbbVie’s Allergan Aesthetics continues to lead in neuromodulators and dermal fillers, offsetting a recent global revenue dip with targeted promotions for combination therapies. Galderma posts double-digit growth in injectable lines and leverages its distribution alliance to extend reach into tier-2 cities. Cutera’s restructuring under Chapter 11 opens share for contenders in energy-based acne platforms, while Venus Concept eyes market gaps with newly approved multipurpose systems.

Local distributors like Invasix Mexico and Deleo Mexico sharpen their value propositions by bundling regulatory consulting and after-sales service, a must-have for foreign suppliers unfamiliar with NOM-137-SSA1-2024 labeling rules. COFEPRIS enforcement against counterfeit devices further incentivizes clinics to source from authorized channels, indirectly favoring established brands. Strategic alliances between device makers and financing partners help clinics mitigate capital barriers, a model gaining traction as interest rates stabilize. M&A activity is buoyant; private-equity investors closed more than a dozen minority stakes in specialized clinic chains during 2025, betting on procedural volume scaling as workforce constraints ease.

Mexico Aesthetic Devices Industry Leaders

Abbvie (Allergan Inc.)

Bausch Health Companies (Solta Medical)

Johnson & Johnson Inc.

Galderma SA

Hologic Inc. (Cynosure)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Operational simplification at COFEPRIS, along with the abbreviated pathway in effect from September 2025, creates room for faster product refresh cycles and broader portfolio rollouts, particularly for multinational suppliers with prior approvals from recognized reference regulators. This supports adoption in energy-based platforms, which already account for a major share of device-type revenue in Mexico, and in home-use devices where clearer compliance tools can support channel expansion. COFEPRIS also provides a self-verification guide for aesthetic medical establishments, which can improve clinic readiness and standardize procurement toward compliant systems.

Beyond regulatory process, manufacturing and contract manufacturing investments in Mexico point to a deeper medtech industrial base, which can improve service levels, parts availability, and localization options for device makers and distributors. For example, Abbott inaugurated a US$200 million electrophysiology facility in Queretaro in January 2026 and reaffirmed an MXN 3.5 billion investment plan tied to the same state in May 2026, while Domico Med-Device opened a 23,000 sq ft facility in Celaya, Guanajuato in January 2026. Although these initiatives are not aesthetic-specific, they reinforce the broader medtech footprint in the Bajio corridor and can support opportunities for aesthetic OEMs and importers to leverage Mexico-based manufacturing and QA capabilities as labeling and GMP expectations tighten.

Recent Industry Developments

- May 2026: Abbott reaffirmed an MXN 3.5 billion investment project linked to its Queretaro manufacturing footprint. The announcement indicates continued scaling of Mexico-based medtech production and a maturing supplier base that can support localized quality, logistics, and technical capabilities for device makers.

- July 2025: COFEPRIS closed 97 illegal aesthetic clinics nationwide as part of enhanced enforcement actions. The crackdown raised the compliance bar for providers and strengthened the position of authorized clinics and distributors relying on registered devices and formal after-sales service networks.

- June 2024: Merz Aesthetics expanded access to its educational platform for aesthetic healthcare professionals, including in Mexico. Training-led initiatives support safer adoption of advanced aesthetic technologies and help clinics standardize protocols as procedure volumes shift toward minimally invasive treatments.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues generated in Mexico from aesthetic devices used to deliver cosmetic and appearance-improvement procedures in clinical and supervised settings, covering both face and body treatments. The sizing approach starts from device sales and then uses the installed-base driven demand for follow-on aesthetic procedures.

Scope exclusions: We exclude purely topical products, OTC cosmetics, and service-only procedure revenues that do not involve the sale of an aesthetic device.

Segmentation Overview

- By Device Type

- Energy-based Devices

- Laser-based

- Light-based (IPL)

- Radio-frequency-based

- Ultrasound-based

- Cryolipolysis & Plasma-based

- Non-energy-based Devices

- Botulinum Toxin

- Dermal Fillers & Threads

- Chemical Peels

- Microdermabrasion

- Implants

- Mesotherapy & Others

- Energy-based Devices

- By Application

- Skin Resurfacing & Tightening

- Body Contouring & Cellulite Reduction

- Hair Removal

- Tattoo & Pigmentation Removal

- Breast Augmentation

- Acne & Scar Treatment

- Other Applications

- By End User

- Hospitals

- Dermatology & Cosmetic Clinics

- Home-use Settings

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the fact base for Mexico around procedure demand, healthcare delivery capacity, and the regulatory pathways that shape how quickly devices can be adopted. Public and official sources reviewed include COFEPRIS guidance and registration information, INEGI health and demographic indicators, OECD health spending tables, UN Comtrade trade statistics, and peer-reviewed clinical literature that tracks procedure trends and technology outcomes.

We also screened manufacturer annual reports, investor presentations, press releases, and distributor and clinic websites to understand product positioning, pricing bands, and common use cases. Where public disclosures were thin, we relied on paid subscriptions for company financials and news, and we also used a patent database to cross-check technology focus and the cadence of innovation. The sources listed are illustrative only, and additional public and paid references were used to collect, validate, and clarify data points.

Primary Interviews and Surveys

Primary work focused on confirming which device categories are actually purchased in Mexico, how replacement cycles play out in practice, and what typical price ranges look like after distributor margins and financing terms. We spoke with a mix of clinics, hospitals, distributors, and service providers across Mexico, then used structured surveys to stress-test adoption assumptions and the split between energy-based and non-energy-based device demand.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 13% | |

| Mid tier: 51% | Functional/Unit leaders: 34% | |

| Smaller Players: 16% | Managers: 53% |

Market-Sizing & Forecasting

Sizing starts from a top-down demand pool, where procedure volumes and the active base of dermatology and cosmetic clinics are used to reconstruct device need, and then totals are translated into value using typical system prices and replacement timing. To keep the estimate practical, the model is cross-checked through selective bottom-up approximations using a roll-up of visible supplier revenues, distributor channel checks, and sampled ASP-by-unit assumptions for core modalities.

Key inputs that shape the Mexico model include the share of non-invasive and minimally invasive procedures, the mix of energy-based systems versus implants and other non-energy devices, average selling price bands by modality, utilization per installed device, and replacement or upgrade cycles driven by new features and maintenance costs. COFEPRIS registration and local availability were also treated as gating factors, since they affect when newer platforms can scale beyond early adopter clinics.

For forecasting, we applied scenario analysis supported by expert feedback. Scenarios were anchored to macro and healthcare indicators plus expected procedure growth in major urban centers. When bottom-up visibility was incomplete for smaller providers, we used conservative gap fills based on clinic counts, typical device-per-clinic ranges, and validated price bands, then reconciled back to the demand-led total.

Data Validation & Update Cycle

Validation is done in several passes so the output stays tied to real-world signals, not just spreadsheet calculations. We compare model totals with independent indicators such as import trends for relevant device categories, changes in clinic footprints, and observed pricing shifts, and then we re-check any outliers before sign-off.

If interview feedback or new public releases suggest a material change, assumptions are revisited and respondents are re-contacted to confirm what changed and why. Reports are refreshed annually, with interim updates when major regulatory, pricing, or demand events materially move the market. Before delivery, an analyst performs a final review so the view reflects the latest available information.

Mordor Intelligence's Mexico Aesthetic Devices Market Size Measured Against Other Published Estimates

Published market sizes for Mexico aesthetic devices often disagree because the scope is not kept consistent, and the counting method can shift between device revenues, procedure service revenues, and injectables that are not devices. Differences also come from how firms handle pricing over time, what they assume for the installed base and replacement cycles, and how frequently the numbers are refreshed.

In practice, the biggest gaps usually come from whether energy-based capital systems are combined with non-energy categories like implants and other procedure-linked device sales, and whether the estimate is constrained to Mexico or blended with broader regional patterns. Currency timing and inflation handling matter as well, especially when list prices are mixed with transacted prices that include distributor terms and promotions. The spread below is largely explained by category inclusions and how procedure demand is translated into device units, which is kept consistent and rechecked in the approach applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.96 B (2025) | |

| Industry Publisher A | USD 0.10 B (2025) | This estimate appears to sit on a narrower value base that is closer to select device categories. It may also include non-device items like injectables, which can compress the device-only total when definitions are blended. |

| Market Bulletin B | USD 0.31 B (2026) | The starting year differs, and the scope emphasizes a limited set of energy-based modalities. This can undercount implants and other non-energy device categories, and it also shifts totals based on the assumed ASP progression into 2026. |

Looking across the figures, the gap is mainly driven by what is counted as a device market in Mexico and how procedure activity is converted into unit demand before pricing is applied. By keeping the conversion logic tied to procedure mix, clinic capacity, and realistic price bands, the resulting number stays traceable to inputs that can be reviewed and repeated.

Key Questions Answered in the Report

What is the current value of the Mexico aesthetic devices market?

It is valued at USD 1.06 billion in 2026 and is projected to reach USD 1.74 billion by 2031.

Which device category leads sales?

Energy-based platforms hold 51.62% share, led by radio-frequency and laser systems.

How fast is body-contouring demand growing?

Body-contouring applications are forecast to expand at a 12.18% CAGR through 2031.

Why does medical tourism matter for aesthetic devices in Mexico?

Foreign patients generate 40% of medical-tourism revenue, driving high-end device adoption in border and coastal clinics.

What regulatory change most benefits manufacturers?

COFEPRIS equivalency now lets FDA-approved devices secure Mexican clearance in as little as six months, accelerating market entry.

Page last updated on: