Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

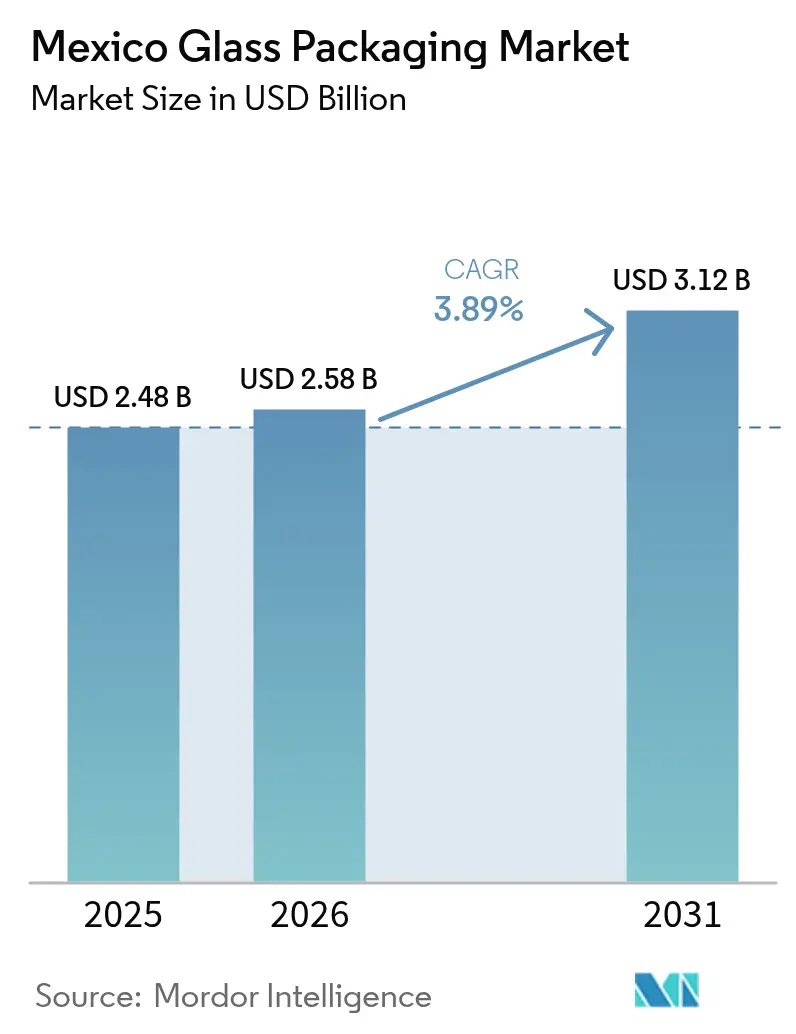

| Base Year Market Size (2025) | USD 2.48 Billion |

| Market Size (2026) | USD 2.58 Billion |

| Market Size (2031) | USD 3.12 Billion |

| Growth Rate (2026 - 2031) | 3.89% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Mexico Glass Packaging Market Analysis by Mordor Intelligence

The Mexico glass packaging market size is expected to grow from USD 2.48 billion in 2025 to USD 2.58 billion in 2026 and is forecast to reach USD 3.12 billion by 2031 at 3.89% CAGR over 2026-2031. This steady trajectory is underpinned by the country’s position as a manufacturing bridge between North and Latin America, near-shoring of premium beverage production, and policy shifts that favor infinitely recyclable materials. Rising disposable incomes spur premiumization in alcoholic beverages, while the 2027 Extended Producer Responsibility (EPR) rules channel investment into cullet recovery networks that expand domestic feedstock. Pharmaceutical export growth further widens demand for Type I borosilicate vials, and furnace electrification pilots built around hydrogen firing promise cost relief in a volatile energy environment. Competitive strategies revolve around lightweighting, recycled-content integration, and joint ventures that secure scale economies in high-growth niches.

Key Report Takeaways

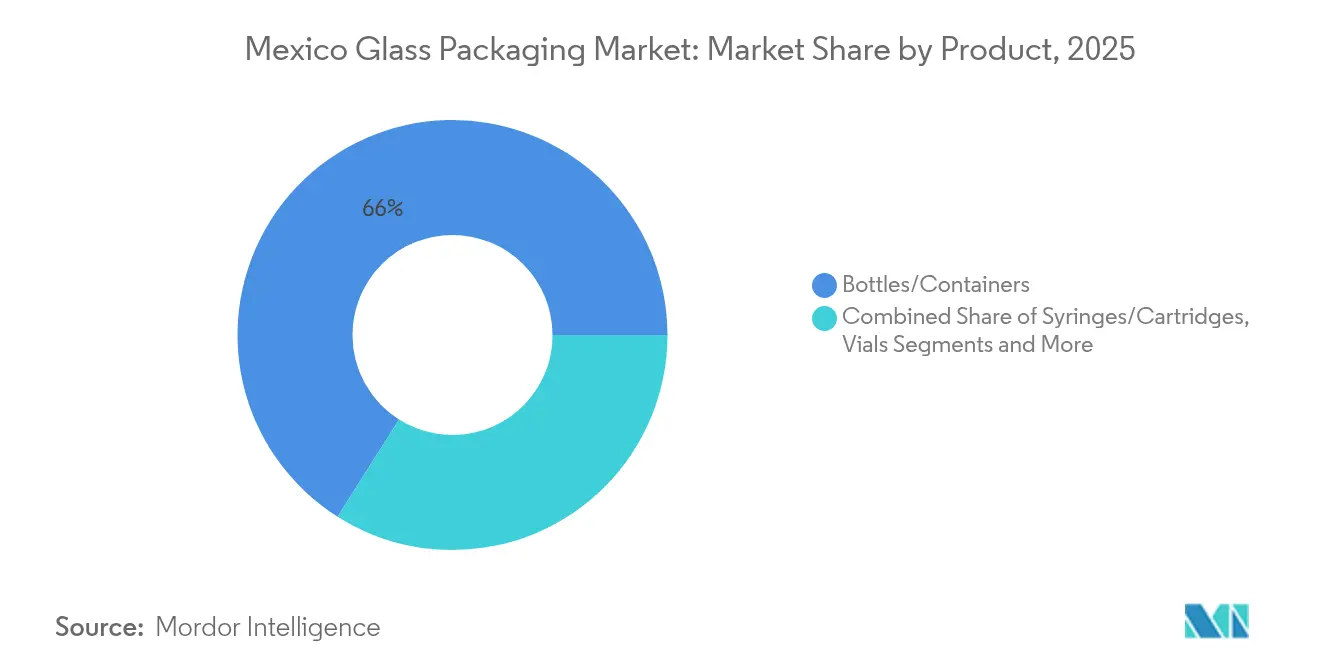

- By product, consumer bottles and containers captured 66.02% of the Mexico glass packaging market share in 2025, and vials are projected to grow at a 4.36% CAGR between 2026-2031.

- By glass type, the Mexico glass packaging market for Type I (Borosilicate) is projected to grow at a 4.58% CAGR between 2026 and 2031, and Type III soda-lime glass captured 57.62% of the Mexico glass packaging market share in 2025.

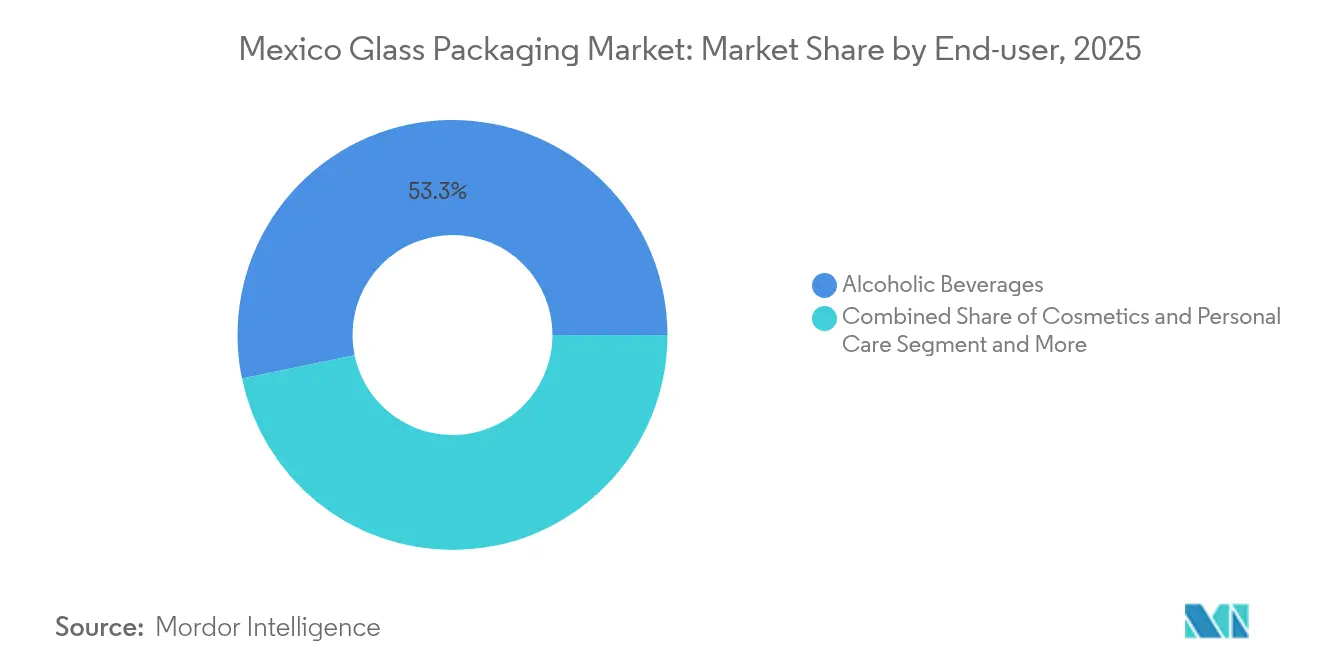

- By end-user, alcoholic beverages captured 53.25% of the Mexico glass packaging market share in 2025, while pharmaceutical applications are projected to grow at a 4.55% CAGR between 2026-2031.

- By capacity range, the Mexico glass packaging market for <30 ml is projected to grow at a 4.12% CAGR between 2026 and 2031, and 100–500 ml accounted for 37.72% share of the Mexico glass packaging market size in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Glass Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher disposable income and premiumization | +0.8% | National strongest in Mexico City, Monterrey, Guadalajara | Medium term (2-4 years) |

| Growing demand due to recyclability mandates | +0.7% | National early adoption in Mexico City and resort corridors | Short term (≤ 2 years) |

| Pharmaceutical export-led vial demand surge | +0.9% | Querétaro, Guadalajara, border maquiladoras | Medium term (2-4 years) |

| The 2027 EPR regulation accelerates collections | +0.6% | Nationwide, with state-level variations | Short term (≤ 2 years) |

| Near-shoring of craft-spirit brands | +0.5% | Jalisco, Guanajuato | Long term (≥ 4 years) |

| Hydrogen-fired furnace adoption | +0.4% | Sites linked to emerging hydrogen corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Higher Disposable Income and Premiumization

Mexico’s expanding middle class boosts demand for premium tequila, mezcal, and craft gin packaged in ornate bottles that project authenticity and quality. Producers such as Komos Tequila commission handcrafted flint and colored containers that raise unit margins and reinforce brand storytelling. Near-shoring lets distilleries cut lead times into the United States, and aesthetically refined glass has become a prerequisite for shelf differentiation in duty-free and e-commerce channels. The same spending upgrade ripples into cosmetics and personal-care items, where clear glass jars communicate purity and sustainability.

Growing Demand Due to Recyclability Mandates

Plastic bans enacted in Durango, Quintana Roo, Zacatecas, and Michoacán push retailers toward materials that meet circular-economy criteria. Mexico City’s “Basura Cero” ordinance elevates refill and returnable schemes, reinforcing consumer familiarity with glass bottles’ infinite recyclability. Beverage majors leverage returnable-glass fleets that already exceed 40 reuse cycles, cutting Scope 3 emissions and meeting corporate net-zero milestones. FEMSA’s 2025 sale of plastics assets underscores the pivot toward glass as the lower-regulatory-risk path forward.

Pharmaceutical Export-Led Vial Demand Surge

COFEPRIS streamlined import licensing in March 2025, shortening approval cycles for medicinal components and easing market entry for foreign contract manufacturers. Multinationals now treat Mexico as a secondary fill-finish hub supporting biologics launches in North America, driving demand for 2-50 ml borosilicate vials that withstand freeze-thaw and lyophilization. Local converters scale isolator-based sterile-fill lines, and SCHOTT Pharma’s adaptiQ ready-to-use platform accelerates adoption by reducing validation steps for small-batch therapies.

2027 EPR Regulation Accelerates Glass Collection Rates

Draft federal EPR rules obligate producers to finance take-back systems and hit glass-specific collection targets. Ardagh Group’s April 2025 joint venture with CAP Glass pre-emptively doubles cullet processing capacity, securing color-sorted feed for its Baja facilities.[1]Ardagh Group-Comms, “AGP and CAP Glass invest in recycling,” ardaghgroup.com Analogous frameworks in Europe show that glass achieves >75% recovery under EPR, translating into lower virgin-raw-material needs and insurance against silica price volatility.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Alternate materials and logistical concerns | −0.6% | Nationwide strongest where last-mile freight costs dominate | Medium term (2-4 years) |

| Complexities in proposed bottle-deposit system | −0.3% | Rural communities lacking reverse-logistics nodes | Short term (≤ 2 years) |

| Volatile natural-gas prices and transition fees | −0.4% | Central industrial corridors linked to LNG infrastructure | Short term (≤ 2 years) |

| Skilled labor shortages in mold maintenance | −0.2% | Northeast automotive-glass clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Alternate Materials and Logistical Concerns

PET and aluminum compete aggressively in price-sensitive beverage tiers where payload weight dictates freight outlays. PetStar’s network collected 5.5 billion PET bottles in 2024, giving plastic converters a closed-loop narrative that resonates with low-income consumers. Mexico’s geography compounds freight distance, and glass’s higher tare weight inflates per-kilometer costs, challenging its position in value water and RTD tea.

Complexities in Proposed Bottle-Deposit System

Federal legislators are studying a Quebec-style refund framework, but the Canadian province’s rollout illustrates pitfalls: only 47 of 200 return depots were operational by March 2025 thanks to funding shortfalls. Mexico faces added hurdles in rural areas dominated by informal retail, delaying infrastructure build-out. This uncertainty can postpone furnace investment decisions and chill financing for cullet-sorting upgrades.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Vials Drive Pharmaceutical Expansion

Mexico glass packaging market size for bottles and containers remained dominant at USD 1.64 billion in 2025, translating into 66.02% share of overall value. Vials, although smaller in absolute revenue, post the steepest trajectory at a 4.36% CAGR through 2031 owing to export-oriented fill-finish contracts for injectable biologics. Mexico's glass packaging market share gains in ampoules follow closely in ophthalmic drugs, while syringes and cartridges capture demand from insulin and GLP-1 therapeutics.

The growth curve for vials is reinforced by the SCHOTT-Gerresheimer-Stevanato alliance that standardizes RTU formats, trimming validation lead times for contract development organizations and driving scale procurement. Bottles and containers continue benefiting from tequila premiumization, with limited-edition variants using embossing, punted bases, or heavy flint to evoke craft heritage and justify price uplift. Meanwhile, anti-counterfeiting inks printed on ampoules, such as SCHOTT Pharma’s August 2024 launch, bolster integrity in export lanes.

By Glass Type: Borosilicate Gains on Quality Demands

Type III soda-lime kept its 57.62% Mexico glass packaging market share in 2025 on the back of beverage mass volume. Nevertheless, Type I borosilicate records the highest 4.58% CAGR to 2031 as pharmaceutical regulations tighten. Amber glass secures niches where UV shielding is required for liquid botanicals and IPA-based injectables.

SGD Pharma’s 20% post-consumer recycled (PCR) content trial underscores how sustainability blends with performance, achieving clarity standards while lowering carbon intensity. Future EPR credits could further tilt economics in favor of PCR-rich soda-lime, yet parenteral drugs will still need borosilicate’s alkaline extractables profile. Mexico's glass packaging industry converters hedge by reserving tank blocks for Type I and leveraging modular batch furnaces.

By End-user: Pharmaceutical Segment Accelerates

Alcoholic beverages represented USD 1.32 billion of the Mexico glass packaging market size in 2025, equal to a 53.25% share. Pharmaceuticals, valued at USD 0.39 billion that same year, are projected to outpace all other segments at 4.55% CAGR. Cosmetics follow, supported by indie brands tapping urban eco-conscious consumers.

COFEPRIS labeling standard NOM-137-SSA1-2024, published in April 2024, obliges tamper-evident finishes and manufacturer codes, circumstances that favor glass suppliers equipped with laser-etch capability. Spirits maintain momentum with export contracts: O-I Glass and Constellation Brands run a USD 160 million plant in Nava dedicated to flint whiskey bottles. Pharmaceutical vendors, meanwhile, are investing in ISO Class 5 filling suites that seamlessly integrate RTU vials.

By Capacity Range: Small Formats Lead Growth

Containers between 100 ml and 500 ml dominated at 37.72% of Mexico's glass packaging market share in 2025 because they fit mainstream beer, soda, and cough syrup SKUs, yet sub-30 ml formats display the fastest 4.12% CAGR. These micro-volumes serve biologics, high-value serums, and ophthalmics.

Increased biologic potency means dosing volumes fall, reinforcing small-format demand. Meanwhile, 30–100 ml glass gains traction in premium fragrance samplers marketed to Gen-Z buyers. Mexico's glass packaging market size for ≥500 ml containers stays stable in foodservice growlers and bulk sauces, buffered by the restaurant sector’s rebound after pandemic-era restrictions.

Geography Analysis

Mexico's glass packaging market revenues cluster along the industrialized Bajío and northern corridors, where rail links speed exports into Texas and Arizona. Guadalajara hosts multi-furnace complexes with rail-served cullet yards, providing cost advantages on silica procurement. Querétaro has emerged as a pharma-packaging enclave, funneling vials through Laredo into U.S. distribution centers within 36 hours.

Monterrey anchors heavy-gauge bottle output tied to regional beer giants, leveraging abundant natural-gas pipelines but facing price volatility that erodes energy cost predictability. Central Mexico City remains the largest demand node thanks to dense population and hospitality spend; local returnable systems feed cullet back to Toluca plants. States such as Jalisco enjoy tequila appellations, where craft distillers prioritize thick-walled, custom molds made in nearby mold workshops. Investment inflows continue: BA Glass’s 60% stake in Vidrio Formas secures two Lerma furnaces and EUR 125 million of sales (USD 136 million) that anchor regional perfume-bottle supply. Vitro’s April 2024 USD 100 million term loan funds rebuilds of regenerative furnaces designed for oxy-fuel upgrades. EPR-driven collection grants are expected to favor underserved southern states, balancing cullet supply across geography.

Regulatory Landscape

Mexico glass packaging suppliers operate under mandatory Normas Oficiales Mexicanas (NOMs) administered through the federal standards system, with conformity assessment tracked via the Comprehensive Standards and Conformity System (SINEC) under the Secretaría de Economía. For packaged food and beverages, NOM-051-SCFI/SSA1-2010 sets commercial labeling requirements, influencing decoration, traceability, and pack communication decisions for both domestic sales and imports.

For food-contact safety, the Secretaría de Salud and COFEPRIS provide sanitary oversight of packaging, including limits on heavy metals for materials in contact with food, using parameters such as those in NOM-010-SSA1-1993 for lead and cadmium. Imported glass packaging and packaged products must meet the same sanitary and labeling requirements as domestic production, keeping compliance documentation and testing readiness central for converters serving beverage, food, and pharmaceutical customers.

Competitive Landscape

Mexico's glass packaging market exhibits a moderate concentration, with the top five participants holding roughly 65% of the value. Vitro leverages vertical integration across flat and container glass, giving it cross-business in sand procurement and capital deployment. O-I Glass’s Fit to Win cost-reduction program delivered USD 61 million in savings in Q1 2025, freeing funds for lightweighting R&D. Gerresheimer focuses on high-margin pharma vials, recently tripling isolator capacity in Querétaro.

Ardagh Group acts as the sustainability front-runner, piloting hydrogen-boosted melters at its Baja line and launching a 300 g lightweight Bordeaux bottle in July 2025 that undercuts the 400 g incumbent by 25% without compromising wall pressure.[3]Ardagh Group-Comms, “Ardagh launches 300 g glass wine bottle,” ardaghgroup.com Competitive threats arise from aluminum-can entrants courting craft beer, yet deposit-return success in spirits keeps loyalty to glass.

Strategic alliances multiply: Vitro supplies flint to Patrón’s new Atotonilco distillery under a multi-year take-or-pay deal; Gerresheimer pairs with Becton Dickinson for RTU syringe components. Technology barriers, namely hot-end vision inspection and narrow-neck press-and-blow, shield incumbents from small-scale entrants. Nonetheless, mold-maintenance talent shortages prompt automation spend that could level efficiency gaps.

Mexico Glass Packaging Industry Leaders

-

O-I Glass, Inc.

-

Gerresheimer Querétaro S.A

-

Verallia México S.A. de C.V.

-

Saverglass SAS

-

Ardagh Group S.A.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Near-term opportunity centers on scaling domestic, color-sorted cullet supply ahead of the draft federal EPR framework referenced for 2027. With collection and take-back funding obligations shifting to producers, companies are already positioning investment toward recycling infrastructure and the networks needed to deliver furnace-ready cullet across Mexico's long freight lanes. O-I Mexico and SILICE inaugurated a recycling hub in Chihuahua designed to process 300 tons of glass per month (feeding O-I Monterrey), and Ardagh Group and CAP Glass moved to double cullet processing capacity through a new sorting line announced in April 2025. This combination supports roles for collection operators, MRF upgrades, and logistics providers that can maintain reliable cullet quality.

Capacity additions aimed at premium beverages, cosmetics, and pharma-grade packaging also broaden demand for specialty molds, decoration, and quality systems. Vitro began operations of Furnace 4 at its Toluca plant in February 2025, adding 230 tons per day for spirits and cosmetics-oriented production, while Gerresheimer is expanding in Querétaro with a project disclosed as about EUR 100 million to add glass forming and ready-to-fill processing lines for pharmaceutical syringes. Alongside Mexico City and state-level waste-reduction measures that favor refill and returnable models, these moves support a clearer route for lightweight returnable glass, higher recycled-content runs where specifications allow, and primary pharma packaging backed by ISO-aligned quality management and validated RTU formats.

Recent Industry Developments

- January 2026: Mexico continued implementing mandatory technical regulations (NOMs) for packaged goods and food-contact materials under the Secretaría de Economía standards system and COFEPRIS sanitary oversight. This sustained compliance emphasis keeps labeling, traceability, and testing capabilities as key differentiators for glass packaging suppliers serving multinational beverage, food, and pharmaceutical customers.

- April 2025: Ardagh Group and CAP Glass announced an investment in a new cullet-sorting line in Mexico that doubled recycled-glass throughput to support container production. The added sorting capacity strengthens domestic cullet availability ahead of draft federal EPR rules referenced for 2027 and supports recycled-content integration and cost control amid raw-material volatility.

- July 2024: O-I Mexico and SILICE inaugurated a glass recycling hub in Chihuahua designed to process 300 tons of glass per month and ship cullet to O-I's Monterrey plant. The project improves local cullet capture in northern corridors and tightens the loop between collection and furnace feedstock for container production serving beverage and other end users.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the market covers the value of glass packaging sold in Mexico for use as primary packs, mainly bottles, jars, vials, and ampoules supplied to end-use industries.

Scope exclusions: It excludes secondary shipping packaging, metal and plastic packaging formats, and equipment or services linked to glassmaking and filling lines.

Segmentation Overview

-

By Product

- Bottles / Containers

- Vials

- Ampoules

- Syringes / Cartridges

-

By Glass Type

- Type I (Borosilicate)

- Type II (Treated Soda-lime)

- Type III (Soda-lime)

- Amber

-

By End-user

- Food

- Soft-drink Beverages

- Alcoholic Beverages

- Cosmetics and Personal Care

- Pharmaceutical

-

By Capacity Range

- <30 ml

- 30 – 100 ml

- 100 – 500 ml

- 500 – 1,000 ml

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was used to set the base structure of the model and to anchor Mexico-specific demand signals. We used public datasets and publications such as Mexico trade statistics, UN Comtrade, and production or industrial indicators from sources such as INEGI, which help us understand manufacturing activity and import-export movements tied to glass containers.

We also reviewed sources such as customs tariff chapter notes for glass containers, government environment and waste rules where relevant to recycled content and collection, and trade bodies linked to packaging and beverages. Company filings, investor presentations, and reputable press were checked to understand capacity changes, plant utilization commentary, and pricing direction. Where needed, paid subscriptions for company financials and intelligence, news and financials, and shipment-level import-export views were used to cross-check the direction of key inputs. The sources listed here are not exhaustive, and many other public documents and references were also used for data collection and validation.

Primary Interviews and Surveys

Primary discussions were used to validate how demand is split across key end users such as beverages, food, and pharmaceuticals, and to confirm practical assumptions like lightweighting, returnable share, and typical price movements. We also used these interactions to sanity-check desk assumptions on capacity utilization, lead times, and the effect of imports versus local supply, so the model reflects what market participants are reporting.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 14% | |

| Mid tier: 52% | Functional/Unit leaders: 32% | |

| Smaller Players: 21% | Managers: 54% |

Market-Sizing & Forecasting

Market sizing starts from a top-down build where Mexico glass container demand is reconstructed using end-use consumption signals and trade flows, then aligned to packaging intensity by application. To keep the outputs grounded, selective bottom-up checks were applied using sampled supplier revenue ranges, typical average selling prices by format (such as bottles versus vials), and volume cues from capacity and utilization commentary.

Key inputs used in the model include container mix by end use (beverage, food, pharma), the returnable versus one-way share in beverages, cullet availability and recycled content direction, import penetration trends, and energy and freight-related cost pass-through that influences pricing. Forecasts were built using scenario analysis so shifts in beverage mix, premiumization, and pharma demand can be stress-tested, and then the final path was confirmed through what interviewees expect for volumes and pricing. Where coverage gaps exist in smaller applications, those were handled through share-based allocations tied to the closest comparable end-use patterns, then rechecked against totals.

Data Validation & Update Cycle

Model outputs are checked against independent signals such as trade balances for glass containers, industrial production direction, and visible capacity additions or shutdowns in Mexico. If an input creates an abnormal jump in volume or price, it is flagged, reviewed, and corrected through a second analyst pass and, where needed, a follow-up with an industry respondent.

Reports are refreshed annually, and interim updates are done when a material event changes supply, pricing, or demand. Before delivery, a fresh review is completed so the latest public releases and market events are reflected in the final numbers.

Mordor Intelligence's Mexico Glass Packaging Market Estimate Compared With Other Published Estimates

Published market sizes for Mexico glass packaging can differ even when they use similar labels, because the counted product set and the year used as the anchor are not always the same. Differences also show up when one study relies mainly on broad packaging splits, while another leans more on application interviews and local trade checks.

Secondary transport packaging and logistics services sit outside Mordor Intelligence's scope, which can pull the value lower versus estimates that blend primary packs with wider packaging spend. The spread can also come from price logic, since some studies assume faster premium-price expansion for beverages, and from refresh timing, since currency conversion dates and inflation updates move value numbers quickly in this market.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.48 B (2025) | |

| Global Research Publisher A | USD 2.80 B (2024) | Uses an earlier base year and a broader product framing that may mix in wider packaging spend, which can lift the value when compared to primary glass packs only. |

| Global Research Publisher B | USD 1.28 B (2024) | Appears to apply narrower quality or application filters and may undercount higher-value pharma formats, which can reduce the total in value terms. |

Overall, the comparison shows that year selection, what is treated as primary glass packaging, and how prices are progressed across formats are the main reasons totals move. Our sizing keeps the scope tied to primary glass packs and then checks totals against trade and end-use demand signals, which makes the output easier to trace and repeat year after year.

Key Questions Answered in the Report

What is the forecast value of the Mexico glass packaging market in 2031?

The market is projected to reach USD 3.12 billion by 2031.

Which glass type is growing fastest in Mexico?

Type I borosilicate is on track for a 4.58% CAGR through 2031.

Why are vials in high demand?

Export-oriented pharmaceutical production and stringent drug-quality rules lift demand for 2–50 ml borosilicate vials.

How do 2027 EPR rules affect glass packaging?

They push producers to finance nationwide collection systems, boosting cullet supply and favoring materials with high recyclability.

Which capacity range dominates Mexico’s glass packaging sales?

Containers between 100 ml and 500 ml lead with 37.72% share in 2025.

Which regions host the bulk of glass production facilities?

Guadalajara, Querétaro, Monterrey, and Toluca concentrate furnace capacity close to rail and export corridors.

Page last updated on: