Metalized Film Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.01 Billion |

| Market Size (2031) | USD 5.09 Billion |

| Growth Rate (2026 - 2031) | 4.92% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

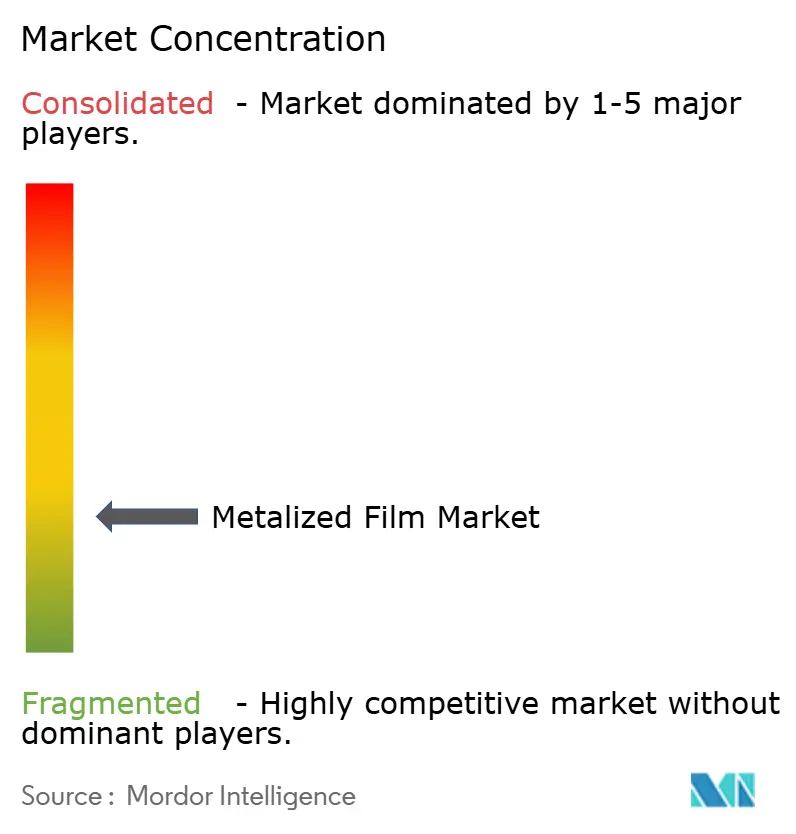

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Metalized Film Market Analysis by Mordor Intelligence

Metalized Film market size in 2026 is estimated at USD 4.01 billion, growing from 2025 value of USD 3.82 billion with 2031 projections showing USD 5.09 billion, growing at 4.92% CAGR over 2026-2031. Rising demand for lightweight barrier packaging, rapid electrification of vehicles, and expanding printed electronics output are the main forces lifting the metalized film market. Established converters are investing in wider, faster coating lines to gain scale and contain cost inflation, while material innovators focus on recycling-ready structures that meet tightening regulatory targets. Copper coatings for battery pouches and high-frequency circuitry are growing quickly, yet aluminum retains a clear cost and supply advantage in most food and consumer goods uses. Asia-Pacific retains the largest production and consumption base, and its policy support for renewable energy and electric mobility widens the regional demand gap over North America and Europe.

Key Report Takeaways

- By metal type, aluminum led with 78.10% of the metalized film market share in 2025; copper is the fastest-growing metal at a 5.55% CAGR through 2031.

- By film type, polyethylene held 66.70% of the metalized film market share in 2025, whereas other film types are projected to expand at a 5.72% CAGR to 2031.

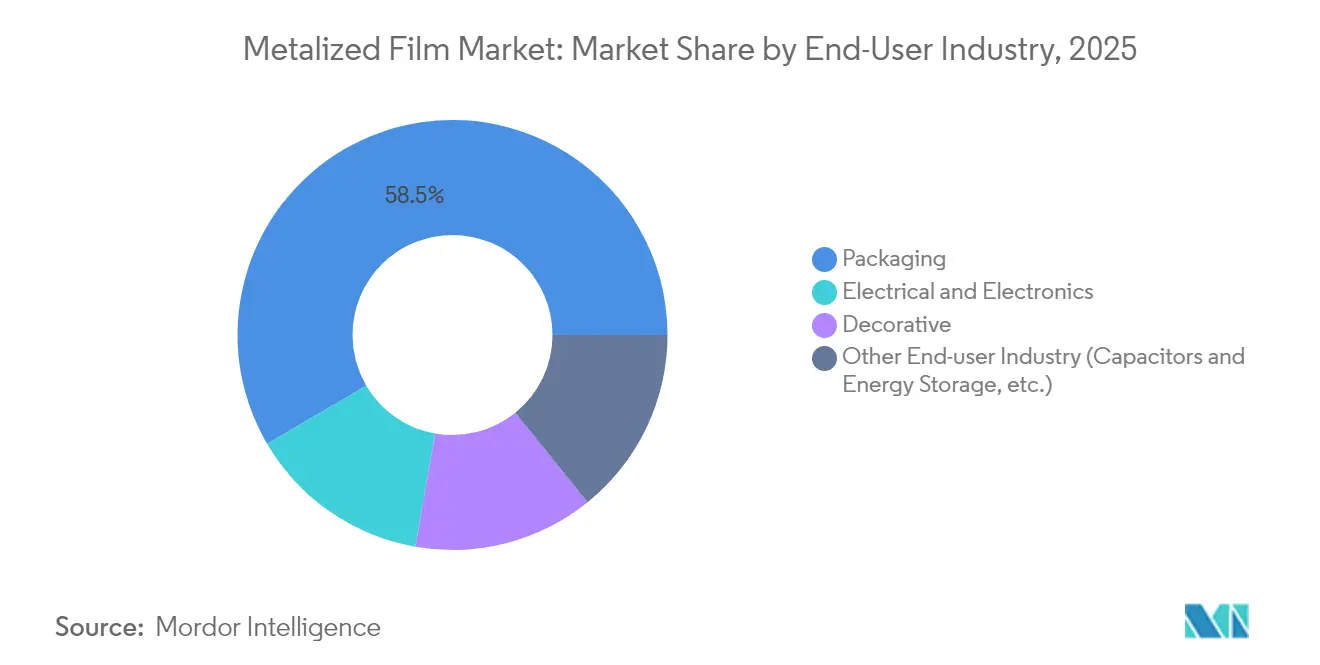

- By end-user industry, packaging commanded 58.45% of the metalized film market size in 2025; energy storage and capacitor applications are advancing at a 5.78% CAGR to 2031.

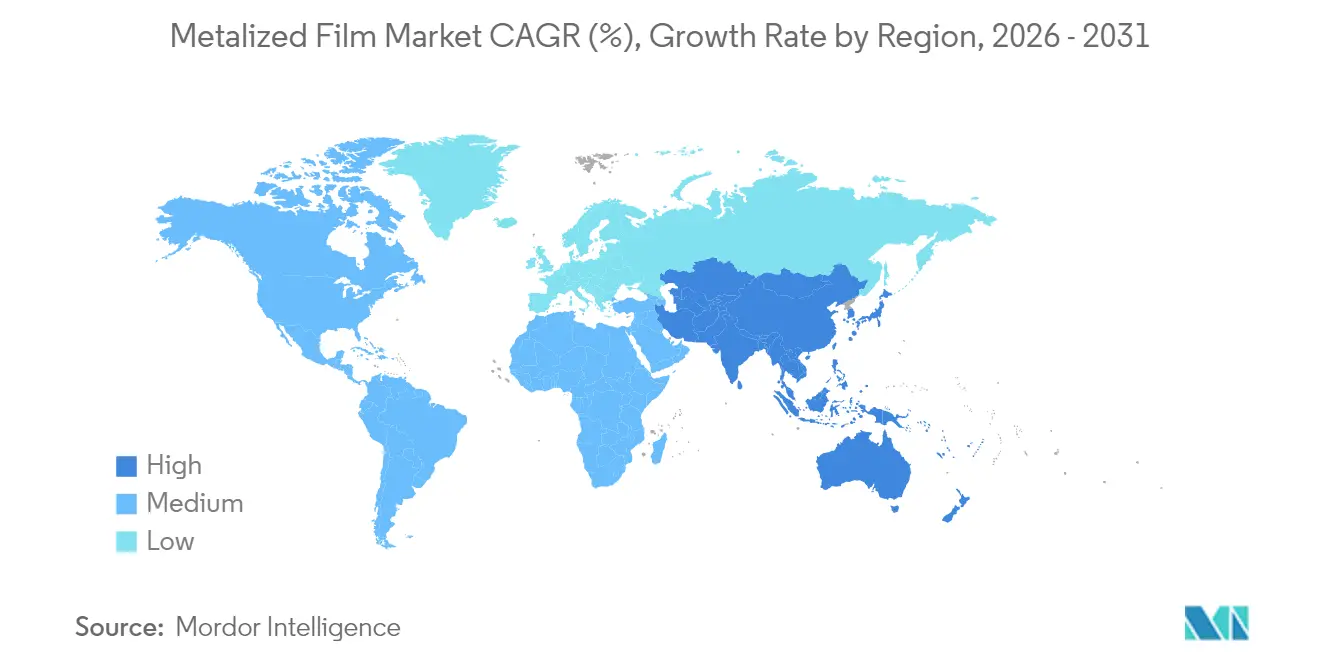

- By geography, Asia-Pacific captured 53.20% of the metalized film market share in 2025 and is set to grow at the highest regional CAGR of 5.61% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Metalized Film Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for high-barrier flexible food packaging | +1.20% | Global, with strongest growth in APAC and emerging markets | Medium term (2-4 years) |

| Rapid substitution of aluminium foil with lightweight metallized films | +0.80% | North America & EU, expanding to APAC manufacturing | Short term (≤ 2 years) |

| Expansion of EV battery insulation and pouch cell applications | +0.60% | Global, concentrated in China, US, and Germany | Long term (≥ 4 years) |

| Growth of smart labels and printed electronics on flexible substrates | +0.40% | APAC core, spill-over to North America and EU | Medium term (2-4 years) |

| Adoption in solar‐backsheet and reflective insulation products | +0.30% | Global, with early gains in China, India, and southwestern US | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for High-Barrier Flexible Food Packaging

Food brands are switching from rigid containers to flexible packs that deliver long shelf life, lower transport emissions, and premium shelf appeal. Aluminum-coated polyethylene and polypropylene films supply the oxygen and moisture barriers needed to keep ready-to-eat meals safe during lengthy global supply chains. Retailers in Europe and North America set aggressive food waste reduction targets that favor barrier laminates produced in the metalized film market. Asian processors benefit from high-speed vapor deposition lines that cut coating costs without sacrificing performance. Government food-safety rules also push converters to adopt metalized structures that resist contamination while remaining lightweight.

Rapid Substitution of Aluminum Foil with Lightweight Metallized Films

Vehicle makers and aircraft suppliers pursue weight reduction to comply with carbon regulations. Vapor-deposited aluminum films provide barrier levels close to foil at a fraction of the mass and can wrap contoured parts easily. Their roll-to-roll coating process boosts throughput, lowering unit costs for converters active in the metalized film market. Battery pack builders prefer these films for thermal pads because the material conforms around prismatic cell edges without cracking. Producers that control both polymer extrusion and metallization gain resilience against primary aluminum price swings.

Expansion of EV Battery Insulation and Pouch Cell Applications

Electric-vehicle battery pouches rely on aluminum-coated polymer films to manage heat and stop short circuits[1]SK Nexilis, “Battery Copper Foil Expansion Update 2025,” sknexilis.com . Surging EV output in China and the United States drives large-volume contracts that lock in metallized substrate demand to 2030. Copper-coated films show promise as high-current collectors that improve energy density, though moisture stability remains a design hurdle. Film makers are entering joint-development programs with battery OEMs to refine adhesion layers and functional coatings. Strong safety rules enforced by German authorities further accelerate the uptake of flame-retardant metallized laminates in European gigafactories.

Growth of Smart Labels and Printed Electronics on Flexible Substrates

Brands now embed RFID antennas, freshness sensors, and QR-based engagement tags on package surfaces. Silver or copper grid traces printed on aluminum-coated PET enable these circuits without major tooling changes, and roll-to-roll printing keeps unit economics attractive. Asian display makers leverage the same substrate know-how to produce foldable screens, adding another pull on the metalized film market. Logistics companies adopt temperature-logging labels to monitor cold-chain performance, reinforcing demand for conductive yet transparent coatings. As internet-connected packaging moves mainstream, converters with electronics-grade cleanliness stand to capture premium margins.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recycling complexity of multi-layer metallized laminates | -0.70% | EU and North America, expanding globally due to regulations | Medium term (2-4 years) |

| Aluminium price volatility squeezing converter margins | -0.50% | Global, with highest impact in cost-sensitive markets | Short term (≤ 2 years) |

| Copper-layer reliability issues in high-frequency electronics | -0.30% | APAC core (China, Japan, South Korea), spill-over to North America and EU electronics hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Recycling Complexity of Multi-Layer Metallized Laminates

European regulators require packaging to reach 70% recyclability targets, yet thin aluminum layers fused to polymers remain difficult to separate. Waste sorters often misclassify shiny films as paper-plastic composites, sending valuable material to landfill[2]WRAP, “Plastics Recycling Market Situation Report 2025,” wrap.org.uk . Brands respond by testing clear-coat barrier films, but performance still trails conventional vapor-deposited structures. Chemical delamination pilot plants operate in Germany and the Netherlands, yet scale economics are unproven. Until reliable recovery routes emerge, environmental scrutiny will curb growth in regions with strict extended producer responsibility fees.

Aluminum Price Volatility Squeezing Converter Margins

Spot aluminum prices spiked in 2024 and 2025, catching mid-size converters with limited hedging capacity. Packaging contracts fixed for 12 months expose suppliers to sizeable cost swings, prompting margin erosion. High-energy smelting costs in Europe are transmitted rapidly to thin-gauge coil feedstock used in the metalized film market. Manufacturers respond by localizing material sourcing and raising automation levels to offset raw-material risk. Persistent volatility may spur further consolidation as scale becomes critical for purchasing leverage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Metal Type: Aluminum Dominance Faces Emerging Copper Growth

Aluminum accounted for 78.10% of the metalized film market in 2025, reflecting its balanced barrier, cost, and recycling profile. The segment’s large installed vacuum-coating base secures a predictable supply to food and personal-care packers. Copper, however, is on a 5.55% CAGR trajectory through 2031 as high-power battery packs and 5G devices need superior conductivity. The metalized film market size for copper coatings in battery pouches is projected to increase, supported by gigafactory investments in China and the US. Although copper films risk corrosion in humid environments, multilayer adhesion promoters are improving durability.

Technological refinements such as plasma-assisted vapor deposition deliver tighter thickness tolerances that enhance electrical performance in fine-line circuits. Aluminum remains favored for decorative wraps and capacitor foils because of its oxide layer stability and ample scrap recycling infrastructure. Niche metals such as silver and aluminum oxide serve optical filters and antimicrobial wraps, where value per square meter outruns raw metal cost. Producers balancing a dual-metal portfolio can hedge demand shifts and maintain utilization rates across diverse end-uses in the metalized film market.

By Film Type: Polyethylene Leadership Challenged by Innovation

Polyethylene held 66.70% of the metalized film market in 2025, thanks to regulatory clearance for direct food contact and compatibility with heat-seal lines. The polymer’s low melting point supports energy-efficient processing, which keeps total conversion costs competitive. Yet high-temperature electronics and electric drives call for films that retain dimensional stability above 150 °C. Consequently, other film types, including polyimide and others, are growing at a 5.72% CAGR to 2031.

Barrier enhancements applied through atomic-layer deposition now bring water vapor transmission rates below 0.05 g/m²/day, closing the gap with aluminum foil. Polypropylene, while entrenched in capacitor and label uses, faces slower growth as converters shift to recyclable mono-PE laminates favored by brand owners targeting circularity metrics. Bio-based PLA and cellulose films with vacuum-deposited aluminum coatings are under early commercialization, signaling future competition for incumbent polyolefins. Film makers that master both commodity and engineered resins will defend share across fast-changing customer specifications.

By End-User Industry: Packaging Dominance Amid Electronics Expansion

Packaging absorbed 58.45% of the metalized film market in 2025, reflecting steady consumer demand for snack foods, confectionery, and ready meals that need a moisture-oxygen barrier. Shelf-life extension cuts wastage and supports retail category growth, locking in baseline volume for aluminum-coated PE and PP laminates. Meanwhile, the energy storage and capacitor cluster is accelerating at a 5.78% CAGR to 2031 as global EV output tops 20 million units and solar farms add higher-voltage inverters.

Electronics assembly requires ever-thinner dielectric barriers to fit into wearable devices and foldable screens. Metallized PET and PEN films under 8 µm thickness answer that need, pushing coating uniformity limits once thought impractical. Decorative wraps for appliances and car interiors still book reliable volume, yet growth is modest because OEM styling cycles are lengthening. The rise of smart packaging blurs lines between traditional packaging and electronics, encouraging converters to offer integrated barrier and circuit-printing services under one roof.

Geography Analysis

Asia-Pacific generated 53.20% of the metalized film market revenue in 2025, backed by China’s dominance in both polymer extrusion and thin-film vacuum deposition. Annual capacity additions across Jiangsu and Zhejiang provinces keep unit costs low through economies of scale and captive aluminum coil. India’s consumer packaged goods sector expands fast, lifting domestic demand and inviting upstream investment in new BOPP and BOPET lines. South Korea and Japan focus on high-precision copper and silver coatings for semiconductor carriers, sustaining premium export niches. The region’s policy emphasis on electric mobility further propels the consumption of battery-grade metallized films.

North America remains a key regional block, led by US food and beverage brands that specify high-barrier pouches for frozen entrees and pet foods. Incentives under the Inflation Reduction Act spur battery plant construction, which raises local sourcing requirements for metallized separators and insulation wraps. Canada’s abundant clean energy and rising aluminum billet production provide a stable supply base for converters operating in Ontario and Quebec. Mexico benefits from near-shoring trends as electronics and auto suppliers move assembly closer to US consumers, creating fresh pull for metallized packaging and capacitor films.

Europe’s stringent circular-economy directives accelerate R&D into de-lamination technologies and mono-material barrier structures. Germany is leading in high-speed capacitor film slitting for industrial drives and wind turbines. France and the United Kingdom prioritize recyclable food wraps and have launched retailer-led collection pilots for shiny snack packs. Nordic countries champion bio-based substrates paired with thin aluminum oxide coatings to lower total carbon intensity. However, elevated power prices in continental Europe challenge profit margins for energy-intensive metallization plants, prompting some capacity relocation to Eastern Europe, where electricity tariffs are lower.

Competitive Landscape

The metalized film market shows moderate fragmented concentration, with the top five converters estimated to hold roughly 33% of global capacity. Large players integrate backward into polymer resin and upstream aluminum to cushion commodity swings and ensure quality traceability. Capital expenditure in 2025 favors wider, 10.5 m vacuum coaters that raise throughput by 20% versus earlier lines. Firms such as Cosmo Films and JPFL commission greenfield lines in India aimed at both export and booming domestic food brands. In Europe, Treofan and Innovia test plasma-enhanced reactors that deposit ultra-thin aluminum oxide layers for transparent barrier applications.

Strategic partnerships emerge along the battery value chain, where film makers cooperate with cell producers to tailor substrate roughness and thermal conductivity. Patent filings covering adhesion-promoter chemistry and sputtered copper layer stacks have risen 18% year-on-year, suggesting a technology race for next-generation EV designs. Niche specialists concentrate on antimicrobial silver coatings for medical packaging and on laser ablation patterns for in-mold labeling, carving high-margin pockets outside commodity snack food wraps.

Competitive intensity also surfaces in sustainability claims. Converters publish life-cycle assessments to prove lower greenhouse-gas footprints than rigid alternatives. Facilities in Asia install rooftop solar and waste-heat recovery to meet multinational brand procurement standards. Recycling alliances such as CEFLEX enroll multiple film producers to design compatible barrier structures. Smaller regional participants may struggle to fund these upgrades, leading to further consolidation or joint ventures with resin majors that can underwrite technology shifts.

Metalized Film Industry Leaders

Cosmo Films

JPFL Films Private Limited

Polyplex

Taghleef Industries

UFlex Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: JPFL Films Pvt Ltd is set to invest INR 7,000 million to boost capacity at its Nashik plant. The move aims to ramp up production across all current product lines, such as Biaxially Oriented Polypropylene (BOPP), Polyethylene Terephthalate (PET), and Cast Polypropylene (CPP), significantly enhancing the metalized film market.

- June 2025: Cosmo Films commissioned a new BOPP (Biaxially Oriented PolyPropylene) film production line at its Aurangabad plant in Maharashtra, India. This development is expected to strengthen its position in the metalized film market by enhancing production capacity and meeting growing demand.

Global Metalized Film Market Report Scope

Metalized films are polymer films that have a thin coating of metal over them, often aluminum. They look shiny and metal-like like aluminum foil, but they are lighter and cheaper. Metalized films are often used as decorations and for food packaging. They are also used for more specific things like insulation and electronics. The metalized film market is segmented by metal type, film type, end-user industry, and geography. By metal type, the market is segmented into aluminum, copper, and other metal types. By film type, the market is segmented into polypropylene, polyethylene terephthalate, and other film types. By end-user industry, the market is segmented into packaging, electrical and electronics, decorative, and other end-user industries. The report also covers the market sizes and forecasts for metalized film in 15 countries across major regions. For each segment, market sizing and forecasts have been done on the basis of revenue (USD million).

| Aluminium |

| Copper |

| Other Metal Types (Aluminium-Oxide-coated (AlOx), Silver, etc.) |

| Polypropylene |

| Polyethylene |

| Other Film Types (Polyimide, etc) |

| Packaging |

| Electrical and Electronics |

| Decorative |

| Other End-user Industry (Capacitors and Energy Storage, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Metal Type | Aluminium | |

| Copper | ||

| Other Metal Types (Aluminium-Oxide-coated (AlOx), Silver, etc.) | ||

| By Film Type | Polypropylene | |

| Polyethylene | ||

| Other Film Types (Polyimide, etc) | ||

| By End-user Industry | Packaging | |

| Electrical and Electronics | ||

| Decorative | ||

| Other End-user Industry (Capacitors and Energy Storage, etc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the metalized film market?

The metalized film market is valued at USD 4.01 billion in 2026 and is set to reach USD 5.09 billion by 2031.Film Market is projected to register a CAGR of 4.92% during the forecast period (2026-2031)

Which segment holds the largest metalized film market share?

Aluminum-based films led with 78.10% of the metalized film market share in 2025.e Inc, Clifton Packaging Group Limited, Flex Films, Polinas and Jindal Films are the major companies operating in the Metalized Film Market.

Which region is growing fastest in the metalized film market?

Asia-Pacific is expanding at a 5.61% CAGR through 2031 and already represents 53.20% of global revenue.

How is the metalized film market addressing recycling challenges?

Producers are developing delamination technologies and mono-material barrier structures to meet circular-economy rules, particularly in Europe.

Why is copper metallization gaining interest?

Copper coatings deliver superior electrical conductivity, attracting battery and high-frequency electronics makers, and are projected to grow at 5.55% CAGR.

Page last updated on: