Metal Oxide Varistors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

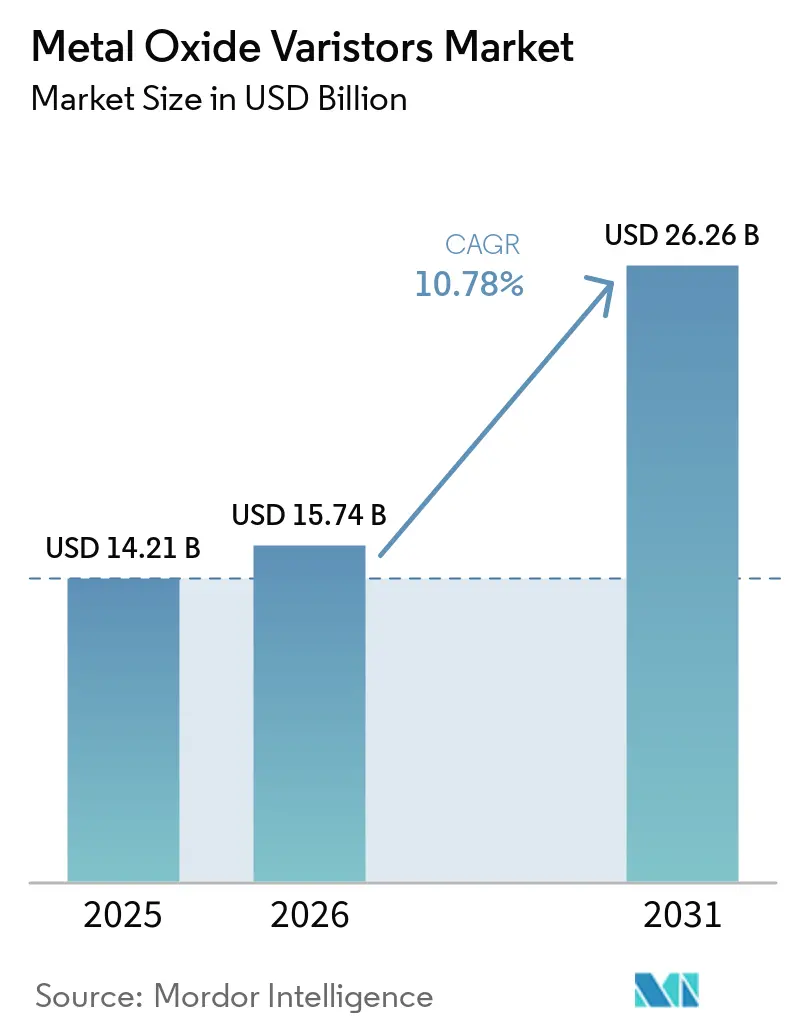

| Market Size (2026) | USD 15.74 Billion |

| Market Size (2031) | USD 26.26 Billion |

| Growth Rate (2026 - 2031) | 10.78% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Middle East |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Metal Oxide Varistors Market Analysis by Mordor Intelligence

The metal oxide varistors market size is projected to expand from USD 14.21 billion in 2025 and USD 15.74 billion in 2026 to USD 26.26 billion by 2031, registering a CAGR of 10.78% between 2026 to 2031. Momentum is shifting from cyclical consumer hardware refresh cycles toward structural demand, as surge-protection compliance becomes obligatory for electric-vehicle chargers, 5G base stations, and grid-edge power-quality systems. Medium-voltage devices dominate residential and light-commercial protection because they match 230 V to 1,000 V mains, while high-voltage parts now track the rapid adoption of 800 V EV architectures and 1,500 V photovoltaic strings. Supply chains remain tight; lead times for specialized MOV chips stretched from eight weeks to six months through 2025, and zinc-oxide feedstock price swings have compressed margins despite healthy revenue growth. Competition is moderate yet intense, with six global suppliers holding slightly below two-thirds of aggregate sales but facing cost pressures from raw-material volatility and substitution threats from silicon TVS diodes.

Key Report Takeaways

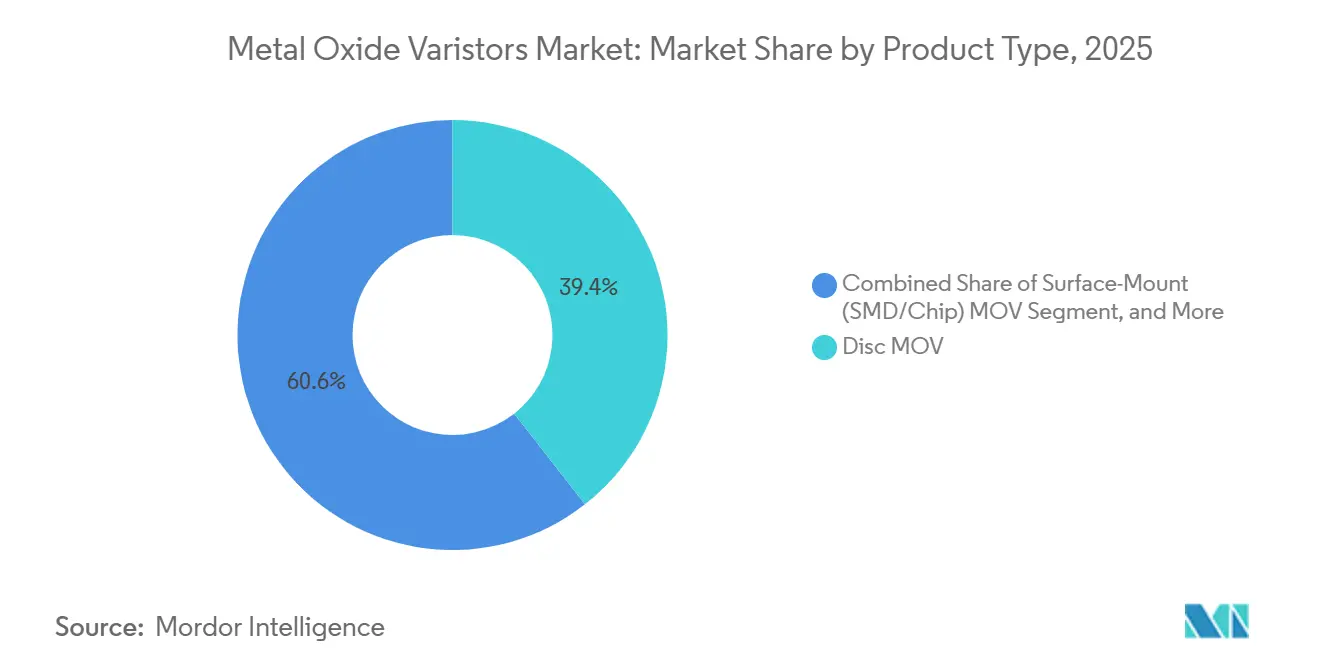

- By product type, disc devices accounted for 39.43% of revenue in 2025, while surface-mount variants are expanding at a 11.58% CAGR through 2031.

- By voltage rating, medium-voltage parts (230 V-1,000 V) commanded 44.59% of the metal oxide varistors market share in 2025; high-voltage devices above 1,000 V are the fastest-growing tier at an 11.38% CAGR.

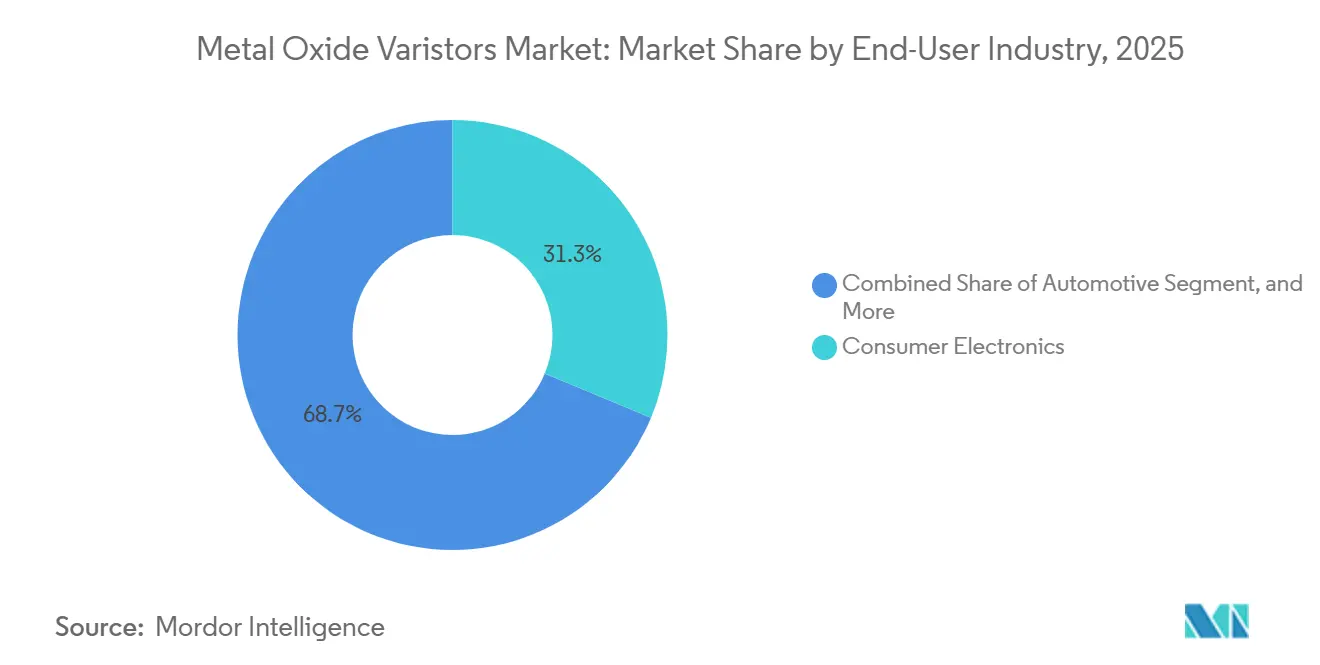

- By end-user industry, consumer electronics accounted for 31.29% revenue in 2025, whereas automotive electronics is advancing at an 11.98% CAGR.

- By application, surge-protective devices held 46.81% of 2025 revenue; automotive-electronics protection is pacing ahead with an 11.78% CAGR.

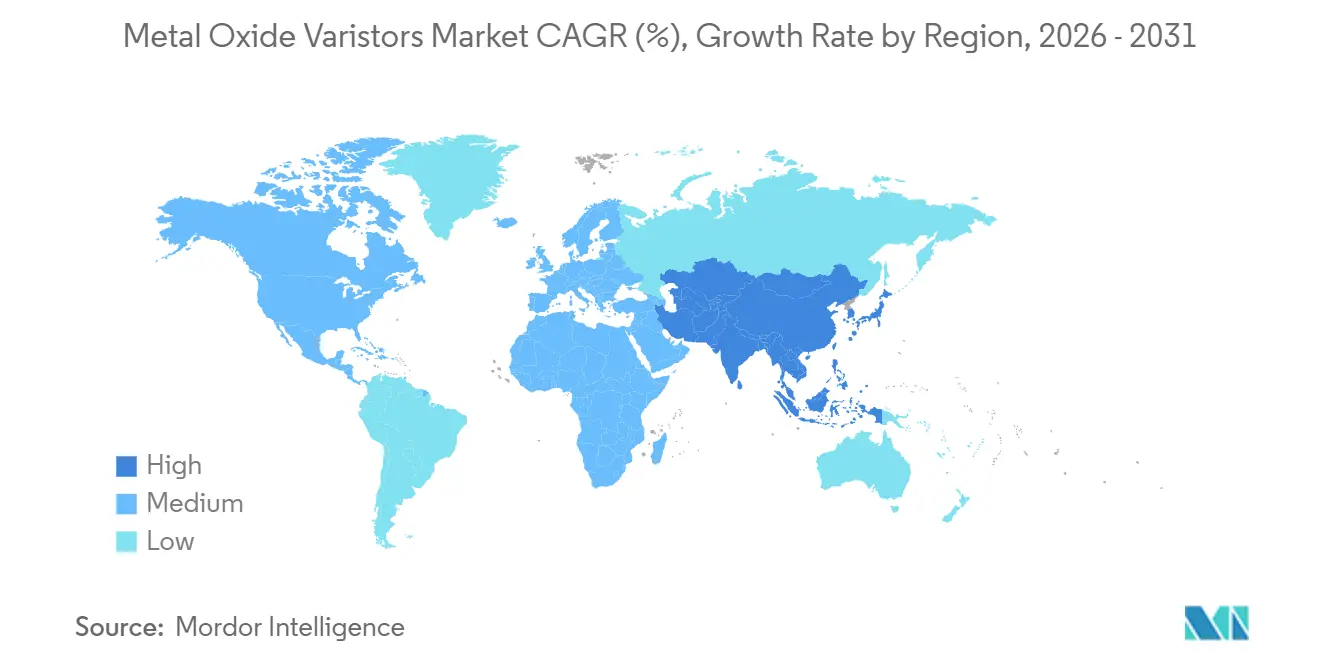

- By geography, Asia-Pacific led with 38.48% of 2025 demand and is growing at 11.69% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Metal Oxide Varistors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Proliferation of Electric Vehicle Charging Infrastructure | +2.1% | Global, concentrated in China, Europe, North America | Medium term (2-4 years) |

| Heightened Adoption of Smart Home Surge Protection | +1.8% | North America and Europe, expanding to Asia-Pacific urban centers | Medium term (2-4 years) |

| 5G Network Roll-outs Requiring Robust Surge Suppression | +1.6% | Asia-Pacific core, spill-over to Middle East and Africa | Short term (≤ 2 years) |

| Industrial IoT Expansion in Harsh-Power Environments | +1.4% | Global industrial corridors; Asia-Pacific manufacturing hubs, North America and Europe retrofits | Long term (≥ 4 years) |

| Grid-Edge Power Quality Initiatives in Developing Economies | +1.2% | India, Brazil, Southeast Asia, Sub-Saharan Africa | Long term (≥ 4 years) |

| Insurance-Driven Mandates for Lightning Protection in Commercial Buildings | +0.9% | North America and Europe; emerging in Latin America and Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Proliferation Of Electric Vehicle Charging Infrastructure

Global public EV chargers exceeded 5 million units in 2024, and IEC 61851-23:2023 now mandates DC-side surge-protective devices with a 2.5 kV protection level. These rules push coordinated Type 1 and Type 2 architectures that pair MOVs with gas-discharge tubes at AC inputs and dedicated MOV-based DC arresters at outputs. IEEE Std C62.230-2022 further codifies protection up to 1,500 V DC, favoring high-energy MOV absorption over semiconductor-only options. Field reliability matters, 46% of fast-charge users cite downtime linked to electrical faults, and a failed charger can cost more than USD 40,000 in repair and lost revenue. Component makers responded; Raycap’s 2025 ProTec T2 DCGU 3Y provides pluggable 1,000 V and 1,500 V modules rated to 100 kA, illustrating the shift to high-voltage, serviceable MOV platforms.[1]Raycap, “Surge Protection for Public and Commercial DC Charging Infrastructure in Accordance With IEC 61851-23,” raycap.com

Heightened Adoption of Smart Home Surge Protection

Homes now host roughly 30 connected devices, and NEC 2023 Article 230.67 requires surge protection on all U.S. dwelling service entrances. Whole-house MOV-based devices mitigate lightning strikes and grid fluctuations, which increased by 18% and 17%, respectively, over the past decade. Makers such as Mersen expanded premium lines in 2025 with 75 kA residential units that bundle thermal-disconnect MOV cores, remote status LEDs, and connected-equipment warranties, pushing average selling prices higher. Supply tension persists; however, lead times for AEC-Q200-grade MOV chips lengthened to nine months for select values, forcing builders and installers to pre-stock. IoT-enabled SPDs, such as Weidmüller’s VARITECTOR PU IoT AC, now stream overvoltage events to cloud dashboards, allowing homeowners to schedule replacements before failure.

5G Network Roll-Outs Requiring Robust Surge Suppression

Outdoor 5G macro cells experience high surge exposure because antennas are mounted atop steel towers, where lightning strike density is high. Design guides from Bourns urge MOV-GDT cascades at 230/400 V AC feeds and 48 V DC back-up lines. MOVs offer symmetrical, bidirectional energy capability that semiconductor diodes cannot match at the tens-of-kiloampere levels specified in UL 1449. Product innovation zeroes in on footprint, multilayer MOVs in 2220 SMD now replace four radial-lead parts, reducing board area by roughly 30% and shrinking tower-top power units.

Industrial IoT Expansion In Harsh-Power Environments

Edge-connected factories deploy thousands of sensors tied to variable-speed drives that generate frequent switching surges. Siemens and others supply DIN-rail MOV SPDs that combine replaceable cartridges, remote alarms, and performance logs to support predictive maintenance. Bourns introduced a multilayer varistor in 2025 that handles 4,500 A in a 2220 package and operates from -55 °C to +125 °C, making it suitable for compact industrial modules. Real-time telemetry on surge counts and thermal stress now feeds asset-health models, helping facilities avoid unscheduled shutdowns.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Zinc Oxide Raw-Material Prices | -1.3% | Global, acute in regions dependent on imports from China and India | Short term (≤ 2 years) |

| Miniaturization Limits on Peak Energy Handling | -0.8% | Global, concentrated in consumer electronics and IoT segments | Medium term (2-4 years) |

| Substitution Threat from Transient Voltage Suppressors (TVS Diodes) | -0.7% | North America, Europe, and Asia-Pacific high-speed data applications | Medium term (2-4 years) |

| Counterfeit Components in Gray-Market Supply Chains | -0.5% | Global, elevated risk in price-sensitive and rapidly relocating supply chains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatility In Zinc Oxide Raw-Material Prices

Zinc oxide is the functional ceramic base of an MOV, and feedstock cost spikes can wipe out quarterly margins. Spot prices ranged between USD 3.11 kg and USD 3.46 kg during late 2025, roughly 25% above pre-pandemic norms. Smaller Asian suppliers with thin balance sheets struggle to hedge, prompting some to ration deliveries or impose surcharges. Vertical integration by top-tier vendors partially offsets volatility; several negotiated multi-year ore contracts and invested in closed-loop recycling of kiln scrap.[2]Cybersecurity and Infrastructure Security Agency, “Critical Manufacturing Sector: Introduction to the Gray Market,” cisa.gov

Miniaturization Limits On Peak Energy Handling

Compact IoT boards often allocate less than 3 mm² for surge protection, limiting MOV diameter and, thus, energy capacity. Silicon TVS diodes claim ground in these sockets because their sub-nanosecond switching and low capacitance preserve high-speed signaling integrity. Comparative Texas Instruments tests showed a 24 V MOV clamping nearly 1,500 V under IEC 61000-4-2 stress, whereas a matching TVS diode limited the peak to 400 V, well within CAN bus transceiver tolerance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Surface-Mount Designs Propel Board-Level Integration

Disc devices retained the largest 39.43% slice of the metal oxide varistors market share in 2025, a position secured by their high-energy handling in service-entrance and appliance surge protectors. Surface-mount variants, however, deliver the fastest 11.58% CAGR through 2031 as automotive and telecom boards migrate to reflow-solderable components. This shift is evident in AEC-Q200-qualified multilayer offerings that halve placement time compared to radial leads. Strap-and-block formats continue to shield utility transformers and rail drives, where tens of kiloamperes per impulse are common, but they represent a niche in overall value terms. Other geometries such as ring MOVs occupy specialty cable-wrap roles, sustaining moderate demand without altering the hierarchy.

Over the forecast horizon, the metal oxide varistors market size for surface-mount parts expands as OEMs consolidate protection at the board level, embedding miniaturized MOVs next to power controllers to meet ISO 7637 and IEC 61000-4-5. Higher layer counts in multilayer ceramics increase joule capacity by roughly 30%, closing the gap with 14 mm discs while preserving sub-nanosecond response. Disc devices still dominate price-sensitive white goods and UPS designs, where through-hole assembly remains prevalent. Suppliers differentiate by adding polymer thermal fuses and conformal coatings to disc parts, extending cycle life in damp environments. The coexistence of both formats ensures a balanced portfolio for manufacturers that can flex ceramic kilns across diameters and stack heights.

By Voltage Rating: High-Voltage Tier Surges With EV and Solar Growth

Medium-voltage devices between 230 V and 1,000 V captured 44.59% of the 2025 metal oxide varistors market share, reflecting their fit with residential split-phase and three-phase commercial mains. High-voltage parts above 1,000 V post the leading 11.38% CAGR, fueled by 800 V traction batteries and 1,500 V photovoltaic strings. Low-voltage MOVs remain essential on consumer boards and data ports yet face direct competition from silicon TVS diodes. Product roadmaps now emphasize 1,500 V continuous-operation modules that slot into DC fast-charger output stages without derating. Field-replaceable cartridges help operators avoid full-cabinet shutdowns during maintenance.

As renewable-energy capacity scales, utilities specify high-voltage MOV-GDT hybrids to satisfy IEC 61643-41 temporary-overvoltage tests, pulling demand toward the top end of the curve. The metal oxide varistor market size, linked to high-voltage ratings, therefore grows faster than the overall average, even though absolute unit volumes remain lower than on medium-voltage lines. Manufacturers are improving thermal disconnect mechanisms that trip below 180 °C, preventing catastrophic rupture under sustained faults. Meanwhile, medium-voltage products receive incremental updates, laser-marked traceability codes, and IoT contact points that lock them into smart-panel ecosystems. Low-voltage MOVs will persist in LED drivers and laptop adapters where a single 2 kA pulse is the design target, but volume uplift remains modest.

By End-User Industry: Automotive Electrification Rewrites Demand Patterns

Consumer electronics maintained its 31.29% share of end-user revenue in 2025, driven by smartphones, TVs, and home appliances that embed MOVs on AC inputs. Automotive electronics record the strongest 11.98% CAGR, as every battery-electric vehicle integrates dozens of board-level varistors to withstand load-dump and lightning-induced surges. Industrial equipment, telecommunications, and energy storage installations round out demand, each requiring ruggedized packages and long maintenance intervals. Cost-down pressure is intense in legacy consumer applications, whereas automotive Tier-1s accept premium pricing for AEC-Q200 compliance and -40 °C to +150 °C endurance.

The metal oxide varistor market size attributable to automotive systems is expected to expand further as 800 V drivetrains proliferate, raising surge amplitudes that only MOVs with multilayer stacks can absorb. Battery management units deploy arrays rated for 60 J pulse energy yet measuring only 1210 in footprint, balancing space and robustness. Consumer electronics, conversely, push toward smaller-diameter discs or polymer resettable fuses to shave pennies per unit. Industrial drives and PLC cabinets maintain steady volume for radial-lead 20 mm parts capable of 40 kA on an 8/20 µs wave. Telcos, finally, favor multilayer MOVs that combine bidirectional protection with compact SMD footprints at tower-top power converters.

By Application: Surge-Protective Devices Retain Leadership, Automotive Electronics Catch Up

Surge-protective devices (SPDs) accounted for 46.81% of 2025 application revenue, the largest share in the metal oxide varistors market, because building codes mandate Type 1 and Type 2 arresters at service entrances. Automotive electronics protection is growing at an 11.78% CAGR, driven by stringent ISO 7637 and IEC 61000-4-5 test levels in electric-vehicle powertrains. Line-voltage protection for industrial gear sits in the middle, with modest but stable uptake as factories digitize. Renewable inverters and battery storage systems also specify MOV-based DC arresters, but their combined share remains secondary.

Forward uptake centers on multi-pole SPDs that integrate MOV, GDT, and TVS elements within snap-in cartridges, offering real-time status contacts for predictive maintenance. The overall metal oxide varistor market for SPDs thus grows in line with widespread code enforcement across North America and Europe. Automotive on-board chargers increasingly deploy coordinated MOV-SIDACtor cascades that clamp below 1 kV during 6 kV surges, a requirement that is impossible with MOVs alone. Industrial line-voltage filters rely on 275 V to 320 V discs to tame motor-switching spikes, ensuring PLC uptime. Renewable-energy installers specify 1,500 V MOV arresters at DC combiner boxes, but elevated voltage stress narrows the supplier pool to vendors with proven high-voltage ceramics.

Geography Analysis

Asia-Pacific leads the metal oxide varistors market, accounting for 38.48% of revenue in 2025 and an 11.69% CAGR outlook. China’s policy goal of 70% domestic content in core components fuels joint ventures, while India’s Electronics Components Manufacturing Scheme, expanded to INR 400 billion (USD 4.8 billion), has attracted pledged investments topping USD 13.9 billion.[3]Government of India, Ministry of Electronics and Information Technology, “Electronics Components Manufacturing Scheme Press Release, Feb 2026,” meity.gov.in Local capacity reduces logistics risk but surfaces counterfeit exposure, as 43% of relocated plants reported suspect parts within six months of moving production.

North America follows as a significant market, driven by U.S. code mandates and the rapid expansion of the electric vehicle (EV) industry. The CHIPS Act, which allocates USD 52 billion in incentives, is playing a crucial role in encouraging domestic fabrication of passive components and reducing reliance on imports. Additionally, the implementation of Section 301 tariffs has significantly impacted the cost of Metal Oxide Varistors (MOVs) imported from China, effectively doubling their prices starting in 2025. This has prompted distributors to diversify their supply chains to mitigate risks and manage costs effectively. Meanwhile, Canada and Mexico are witnessing increased installations of Type 1 Surge Protective Devices (SPDs), particularly on wind farms and data centers. These installations are concentrated in lightning-prone prairie corridors, where the need for robust surge protection is critical to ensure the reliability and safety of infrastructure in these regions.

Europe benefits from stringent EMC rules under EN 61643 and the push toward renewable energy. Germany and France accelerate DC bus protection in 1,500 V solar arrays, while the United Kingdom requires SPDs on EV charger circuits unless a formal risk exemption is filed. Regional initiatives to underground distribution lines dampen lightning exposure but heighten demand for networked surge logging to support asset-health audits. South America expands steadily, led by Brazil’s solar build-out and Mexico’s automotive assembly clusters that source AEC-Q200 MOVs.The Middle East and Africa are adopting surge protection in utility and oil installations; the United Arab Emirates is promoting smart-grid pilots that instrument SPDs with IoT status beacons.

Competitive Landscape

Industry concentration is moderately fragmented. TDK, Littelfuse, Vishay, Panasonic, Eaton, and Bourns collectively control nearly 60% of the metal oxide varistors market revenue, benefiting from proprietary ceramic recipes and broad regulatory certifications. Littelfuse posted a 370-basis-point EBITDA margin lift in Q4 2025 on robust passive-product demand, despite a goodwill impairment tied to weaker power semiconductors.[4]Littelfuse Inc., “Littelfuse Reports Fourth Quarter and Full Year 2025 Results,” littelfuse.com Bourns launched four new varistor or hybrid surge families within 18 months, signaling an aggressive cadence aimed at automotive and 5G infrastructure.

Strategic trends emphasize vertical integration and portfolio breadth. Market leaders co-fire multilayer stacks in-house, incorporate thermal-disconnect links, and bundle MOV cores with gas-discharge tubes and TVS diodes in hybrid modules. Compliance with UL 1449 5th Edition and IEC 61643-41:2025 imposes significant engineering barriers, as each new product family can cost USD 100,000 in certification fees and year-long testing. Disruptive threats come from government-backed Chinese entrants scaling volume quickly, though they trail on high-end automotive qualifications.

IoT-enabled SPDs represent emerging value. Weidmüller and Schneider Electric integrate Bluetooth or Ethernet telemetry that logs surge counts and residual life, opening service-contract revenue. Insurance firms now discount policies for properties that report real-time SPD status, monetizing data collected by such devices. Hybrid MOV-GDT-TVS structures gain favor because they merge high-energy absorption, low standby leakage, and precise clamping, reducing the component count in compact chargers and base stations.

Metal Oxide Varistors Industry Leaders

TDK Corporation

Vishay Intertechnology, Inc.

Panasonic Holdings Corporation

Littelfuse, Inc.

Bourns, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Bourns introduced the GDT225HE series, high-voltage gas-discharge tubes rated 1,000 V-2,000 V DC with a maximum discharge of 60 kA, targeting EV chargers and battery storage.

- January 2026: Littelfuse reported Q4 2025 electronics sales of USD 345.15 million, up 20.7% year over year, led by 23% growth in passive surge-protection products.

- December 2025: Raycap unveiled the ProTec T2 DCGU 3Y pluggable DC SPD for 1,000 V and 1,500 V EV chargers, compliant with IEC 61851-23 and UL 1449 5th Edition.

- October 2025: Mersen expanded its Surge-Trap STXH family with a 75 kA residential model featuring TPMOV cores and a USD 50,000 connected-equipment warranty.

Global Metal Oxide Varistors Market Report Scope

The Metal Oxide Varistor (MOV) market is the global industry that designs, manufactures, distributes, and applies voltage-dependent resistive components to protect electrical and electronic systems from transient voltage surges and overvoltage events. Metal oxide varistors are nonlinear semiconductor devices, primarily composed of zinc oxide-based ceramic materials, that rapidly change resistance in response to excessive voltage, thereby diverting surge currents and safeguarding sensitive circuits and equipment.

The Metal Oxide Varistors Market Report is Segmented by Product Type (Disc MOV, Surface-Mount MOV, Strap/Block MOV, and Other Product Types), Voltage Rating (Low ≤230 V, Medium 230-1,000 V, and Above 1,000 V), End-User Industry (Consumer Electronics, Industrial Equipment, Automotive, Energy and Power, Telecommunications, and Other End-User Industries), Application (Surge-Protective Devices, Line-Voltage Protection, Automotive Electronics, Industrial Power Electronics, and Other Applications), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Disc MOV |

| Surface-Mount (SMD/Chip) MOV |

| Strap / Block MOV |

| Other Product Types |

| Low (≤230 V) |

| Medium (230 - 1,000 V) |

| High (Above 1,000 V) |

| Consumer Electronics |

| Industrial Equipment |

| Automotive |

| Energy and Power |

| Telecommunications |

| Other End-User Industries |

| Surge-Protective Devices (SPDs) |

| Line-Voltage Protection |

| Automotive Electronics |

| Industrial Power Electronics |

| Other Applications |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Product Type | Disc MOV | ||

| Surface-Mount (SMD/Chip) MOV | |||

| Strap / Block MOV | |||

| Other Product Types | |||

| By Voltage Rating | Low (≤230 V) | ||

| Medium (230 - 1,000 V) | |||

| High (Above 1,000 V) | |||

| By End-User Industry | Consumer Electronics | ||

| Industrial Equipment | |||

| Automotive | |||

| Energy and Power | |||

| Telecommunications | |||

| Other End-User Industries | |||

| By Application | Surge-Protective Devices (SPDs) | ||

| Line-Voltage Protection | |||

| Automotive Electronics | |||

| Industrial Power Electronics | |||

| Other Applications | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the metal oxide varistors market?

The metal oxide varistors market size reached USD 15.74 billion in 2026 and is forecast to hit USD 26.26 billion by 2031, tracking a 10.78% CAGR.

Which product type is expanding fastest?

Surface-mount MOVs post the quickest growth, advancing at 11.58% annually on rising adoption in automotive boards and 5G radios.

Why are MOVs critical for EV chargers?

IEC 61851-23:2023 caps DC output let-through at 2.5 kV, so high-energy MOV-based SPDs are mandatory to absorb lightning and switching surges that threaten charger uptime.

How does zinc-oxide price volatility affect suppliers?

Spot zinc-oxide costs rose about 25% over pre-pandemic benchmarks, squeezing margins for MOV makers that lack long-term ore contracts.

Which region leads demand growth?

Asia-Pacific commands the largest share and the highest growth, propelled by China's localization drive and India's INR 400 billion (USD 4.8 billion) incentive program for component production.

Are TVS diodes replacing MOVs?

TVS diodes win in low-voltage, high-speed lines because of faster response and lower capacitance, but MOVs remain dominant for high-energy AC and DC power protection due to superior joule absorption.

Page last updated on: