Insulated Gate Bipolar Transistors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

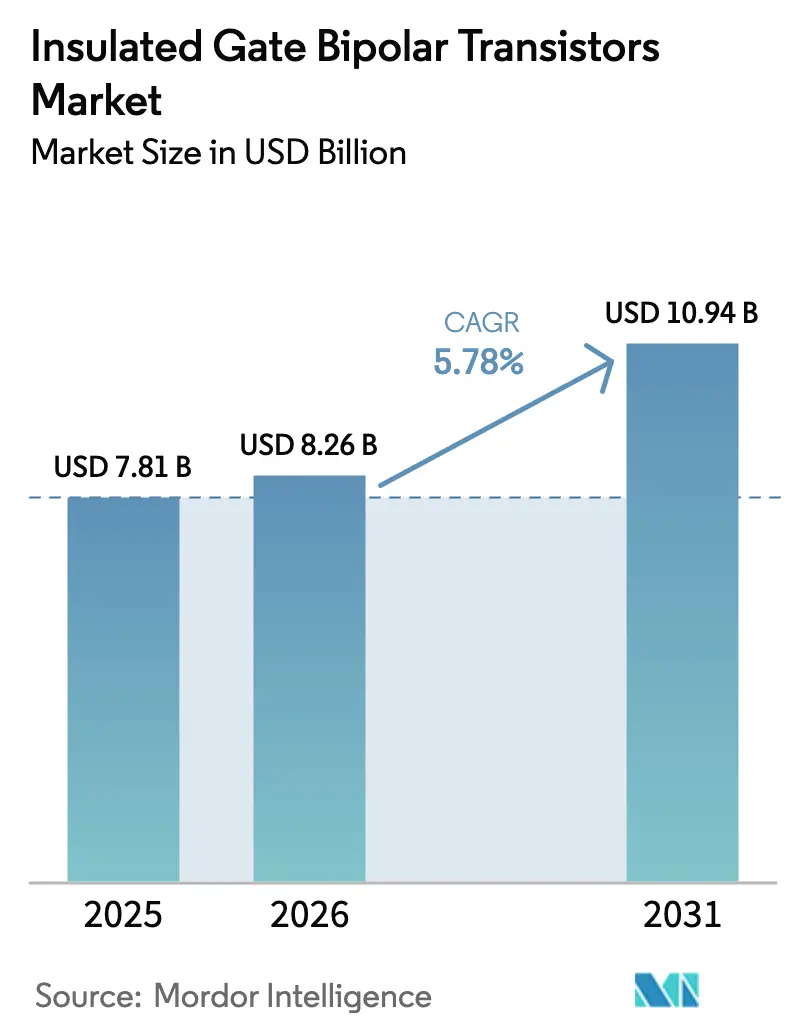

| Market Size (2026) | USD 8.26 Billion |

| Market Size (2031) | USD 10.94 Billion |

| Growth Rate (2026 - 2031) | 5.78% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Insulated Gate Bipolar Transistors Market Analysis by Mordor Intelligence

The insulated gate bipolar transistors market size was valued at USD 7.81 billion in 2025 and estimated to grow from USD 8.26 billion in 2026 to reach USD 10.94 billion by 2031, at a CAGR of 5.78% during the forecast period (2026-2031). This expansion is underpinned by rapid electrification of transport, renewable energy build-outs, and continuous efficiency gains in industrial motor control. Electric vehicle (EV) traction inverters now favor 1,200 V and 1,700 V automotive-grade devices, while utility-scale solar operators demand megawatt-class modules that maximise energy throughput. Railroad electrification programmes in Southeast Asia and Africa add another layer of volume growth as public agencies invest in low-loss traction stacks. At the same time, moderate substitution by silicon-carbide MOSFETs in premium EVs creates pricing pressure, keeping the insulated gate bipolar transistors market highly cost-competitive. Supply chain resilience, especially around 300 mm wafers, is therefore emerging as a strategic differentiator for leading producers.

Key Report Takeaways

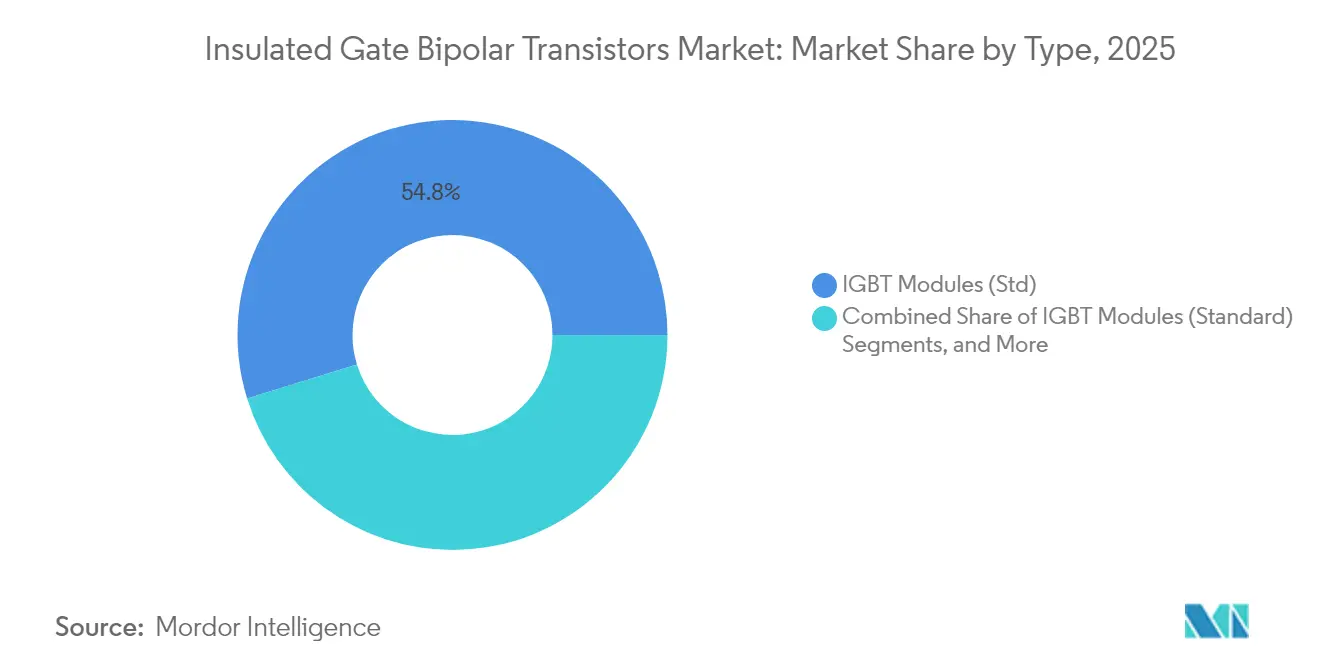

- By product type, IGBT modules held 54.78% of the insulated gate bipolar transistors market share in 2025, while intelligent power modules are projected to grow at 7.05% CAGR through 2031.

- By voltage class, 651-1,200 V devices dominated with 46.25% revenue share in 2025; ultra-high-voltage devices above 1,700 V are forecast to advance at an 7.72% CAGR to 2031.

- By power rating, high-power devices above 20 kW accounted for 43.65% of the insulated gate bipolar transistors market size in 2025, whereas the 1-20 kW category is expanding at 5.98% CAGR.

- By application, industrial motor drives commanded 29.35% share of the insulated gate bipolar transistors market size in 2025; EV traction inverters record the fastest 8.74% CAGR through 2031.

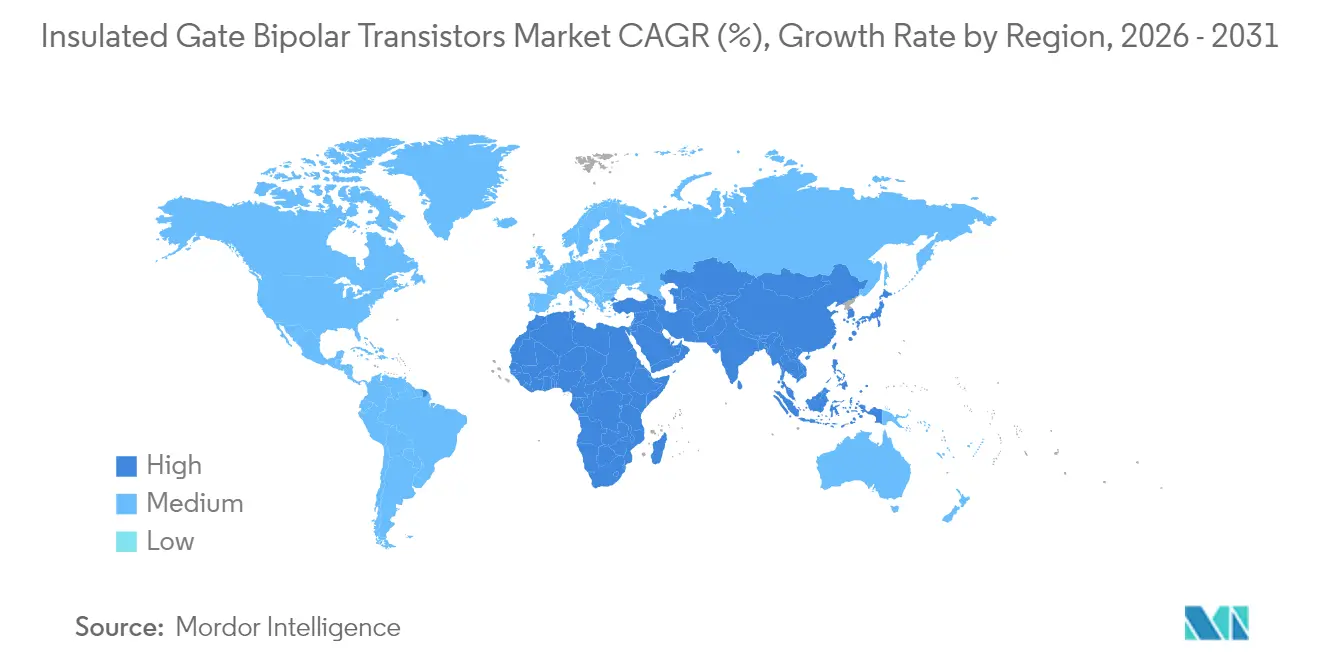

- By geography, Asia-Pacific led with 61.25% revenue share in 2025, while the Middle East is on track for the highest 6.63% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Insulated Gate Bipolar Transistors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in 800-V Battery EV Platforms Elevating 1200-V and 1700-V Automotive IGBT Demand | +1.8% | Global, with early gains in Europe, China, and premium EV segments | Medium term (2-4 years) |

| Utility-Scale Solar and Wind Build-out in India and MENA Requiring High-Power IGBT Modules | +1.2% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Railroad Electrification in SE-Asia and Africa Boosting Low-Loss Traction IGBT Stacks | +0.9% | Southeast Asia, Africa, with expansion to Latin America | Long term (≥ 4 years) |

| Shift to Trench-Field-Stop IGBTs for EU Residential Heat-Pumps | +0.7% | Europe, with adoption spreading to North America | Medium term (2-4 years) |

| 5G Macro-Site Roll-outs Driving 650-V RF-Optimised IGBTs | +0.5% | Global, with concentration in urban centers | Short term (≤ 2 years) |

| United States IRA Incentives Spurring New Domestic IGBT Fabs | +0.4% | North America, with supply chain benefits globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in 800 V Battery EV Platforms Elevating 1,200 V and 1,700 V Automotive IGBT Demand

Automakers are moving from 400 V to 800 V battery packs, cutting charging times and enabling thinner cabling. Semikron Danfoss introduced its 1,700 V IGBT E7 module family in 2024 with 20% lower forward voltage, directly addressing conduction-loss constraints. Higher pack voltages, however, raise partial-discharge risks, so automakers demand enhanced encapsulation resins and advanced thermal pads to maintain insulation integrity during rapid charging cycles. These packaging upgrades increase average selling prices, offsetting the volume-driven margin squeeze in the insulated gate bipolar transistors market.

Utility-Scale Solar and Wind Build-out in India and MENA Requiring High-Power IGBT Modules

India’s 280 GW solar roadmap and Gulf state giga-projects now specify medium-voltage inverters that reduce transformer count. Fraunhofer ISE’s 1,500 VAC string inverter proves that higher AC outputs trim copper by 25%, a direct cost saving for developers.[4]Fraunhofer ISE, “Medium Voltage for Resource Efficiency in PV Plants,” ise.fraunhofer.de Such designs use multi-chip IGBT half-bridge assemblies that combine current sharing with built-in gate drivers. Module makers respond with sintered die-attach layers that improve thermal cycling capability, maintaining junction temperatures under 150 °C even in desert climates. This performance uplift sustains premium pricing and secures the insulated gate bipolar transistors market against near-term SiC substitution for multi-megawatt projects.

Railroad Electrification in Southeast Asia and Africa Boosting Low-Loss Traction IGBT Stacks

Public transit operators in Thailand, Vietnam, and Kenya specify three-level neutral-point-clamped inverters to cut harmonic distortion and increase regenerative braking efficiency. ABB’s HES580 traction platform demonstrates up to 75% lower harmonic losses than two-level designs, lengthening service intervals for pantograph-fed locomotives. Field studies confirm that closed-loop junction-temperature control extends device life by 45% in humid, high-vibration railcar. Demand therefore concentrates on press-fit module formats that support interchangeable stacks, reinforcing aftermarket revenues for leading vendors.

Shift to Trench-Field-Stop IGBTs for EU Residential Heat Pumps

Heat-pump adoption accelerated after revised EU energy-efficiency targets came into force in 2024. Variable-speed compressors require IGBTs switching above 20 kHz, so manufacturers favour trench-field-stop structures offering lower saturation voltage and reduced electromagnetic emissions. Shared-loop ground-source installations in the United Kingdom report 3% energy savings relative to air-source units, creating a niche for compact inverter boards in multi-dwelling retrofits. Suppliers answer with epoxy-gel-filled dual-in-line packages that withstand condensation cycles, opening a long-tail opportunity within the insulated gate bipolar transistors market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Silicon-Carbide MOSFET Penetration in Premium EVs | -1.4% | Global, with concentration in premium EV segments | Medium term (2-4 years) |

| 300 mm Wafer Shortage Constraining Module Supply | -0.8% | Global, with acute impact in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Thermal-Cycling Reliability Issues in Press-Pack IGBTs | -0.6% | Industrial applications globally, particularly in harsh environments | Long term (≥ 4 years) |

| EU Eco-Design Rules Curtailing Legacy Low-Power IGBTs | -0.4% | Europe, with potential expansion to other regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Silicon-Carbide MOSFET Penetration in Premium EVs

SiC MOSFETs slash switching losses by up to 60% compared with silicon IGBTs, enabling extended EV range. Toshiba benchmark tests show 41% lower power loss under identical duty cycles. ON Semi’s EliteSiC M3e further cuts turn-off losses by 50% in 400-A modules. SiC device pricing remains a hurdle for mass-market EVs, yet premium marques increasingly absorb the extra bill-of-materials cost, diverting revenue away from the insulated gate bipolar transistors market in high-end segments.

300 mm Wafer Shortage Constraining Module Supply

Demand for 300 mm wafers outstrips capacity because high-voltage dies require larger guard rings and have lower line-yield percentages. Wolfspeed’s upgrade to 200 mm SiC at Mohawk Valley illustrates the industry’s shift toward bigger diameters to improve economies of scale. In the interim, module makers prioritise automotive contracts, lengthening lead times for industrial customers and creating spot-market price volatility for the insulated gate bipolar transistors market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Modules Dominate Through Integration Advantages

IGBT modules generated 54.78% of the insulated gate bipolar transistors market in 2025, reflecting OEM preference for turnkey thermal and electrical integration. Standard half-bridge packs integrate multiple chips on direct-bond-copper substrates, shortening assembly cycles for inverter builders. Press-fit pins and intelligent gate drivers further cut external component count, lowering system error rates. Intelligent power modules add digital protection features and are growing at a 7.05% CAGR, driven by HVAC and servo drives that demand predictive fault analytics. Discrete devices remain cost-effective for appliance motor boards, yet their share is eroding as power densities rise. Press-pack modules hold a small but strategic niche in offshore converters where low thermal resistance offsets longer assembly times. Life-cycle tests report stable junction-plate thermal resistance after 220,000 power cycles, confirming suitability for long-haul rail traction.

Second-generation sintered-silver die attach pushes module overload ratings to 175 °C, a boost that shields the insulated gate bipolar transistors market from immediate substitution by SiC in multi-megawatt duty. Meanwhile, flexible substrate layouts now accept mixed silicon and SiC chips, allowing hybrid power stages that capitalise on each technology’s strengths without redesigning entire inverter housings. Vendors use this roadmap to keep module ASPs resilient despite a steady drop in discrete pricing.

By Voltage Class: Medium Voltage Leads with Ultra-High Growth

Devices rated 651-1,200 V held 46.25% revenue share in 2025 thanks to their versatility across industrial drives, residential PV inverters, and commercial EV chargers. Epitaxial trench architectures in this class cut saturation voltage below 1.6 V at 150 A, delivering a favourable conduction-to-switching loss ratio. Adoption of 800 V drivetrains propels the 1,201-1,700 V class, where turn-off loss optimisation remains the main design focus. Toshiba’s dual-side multi-gate structure achieves 34% lower turn-off energy than conventional planar gates, meeting emerging automotive specifications

Ultra-high-voltage devices above 1,700 V, although niche, are set for 7.72% CAGR because HVDC grids and wind-farm interconnects demand higher blocking voltages. These modules often incorporate soft-punch-through designs that stabilise collector-emitter voltage during fault conditions, a prerequisite for grid codes mandating ride-through capability. At the bottom end, ≤ 650 V parts face tightening EU eco-design rules that oblige manufacturers to publish digital product passports covering recyclability metrics. Suppliers respond by shifting R&D budgets to higher-voltage segments, reinforcing the revenue dominance of the mid-voltage band within the insulated gate bipolar transistors market.

By Power Rating: High Power Segments Drive Industrial Applications

Modules rated over 20 kW commanded 43.65% of the insulated gate bipolar transistors market size in 2025, anchored by wind-turbine converters, grid-tied battery storage, and metro rail traction. Direct liquid cooling and double-sided substrates raise continuous current capacity without enlarging footprints. Researchers demonstrated multi-condition junction-temperature estimation that keeps ΔT below 20 °C under pulsed overloads, trimming unexpected shutdowns in critical infrastructure. Medium-power brackets between 1 kW and 20 kW are on track for a 5.98% CAGR, fuelled by residential solar inverters and workplace EV chargers that standardise on 15 kW three-phase topologies.

Low-power devices under 1 kW now lose sockets to gallium nitride FETs in fast-charger adapters, yet they retain a foothold in induction cookers and motor-control boards for white goods. The shift in revenue mix encourages vendors to rationalise low-current product lines, freeing clean room capacity for medium-power die that enjoy higher margins. This capacity rebalance fortifies profitability as the insulated gate bipolar transistors market migrates toward applications where switching loss dominates total cost of ownership

By Application: Industrial Motors Lead with EV Traction Fastest Growing

Industrial motor drives represented 29.35% of the insulated gate bipolar transistors market size in 2025 because factories retrofit variable-speed drives to curb energy bills amid escalating power tariffs. Modern vector-control algorithms call for high PWM frequencies, pushing IGBT gate-charge optimisation to the forefront of design roadmaps. In regenerative cranes and conveyors, 15 kHz switching frequency balances acoustic noise and efficiency, validating module-level thermal spreaders that disperse hotspot gradients.

EV/HEV traction inverters provide the highest 8.74% CAGR through 2031. Tier-one suppliers deploy 1,200 V half-bridge modules in stacked layouts to hit 300 kW peak output, integrating negative temperature coefficients for parallel sharing. Renewable-energy inverters follow closely, with Indian and MENA plant operators specifying 1,500 V DC arrays that align with medium-voltage AC outputs. UPS systems for data centres remain a steady niche, but high-frequency telecom rectifiers now lean toward gallium nitride, narrowing IGBT addressable value. The broad application map assures resilient demand, ensuring that the insulated gate bipolar transistors market maintains a diversified revenue base even amid competitive substitution threats.

Geography Analysis

Asia-Pacific held 61.25% revenue share in 2025, reflecting China’s high-volume module assembly, Japan’s technology leadership, and India’s renewable-energy surge. Chinese vendors leverage government support to scale 300 mm wafer fabs, buffering domestic EV makers from external supply shocks. Japanese companies such as Mitsubishi Electric focus on process shrinks and copper sinter attach, exporting premium devices for offshore wind converters. India’s solar-tender pipeline now tops 50 GW, amplifying import demand for high-power stacks compliant with Bureau of Indian Standards grid codes.

Europe is the second-largest region, driven by EV mandates and stringent ecodesign law. German automakers’ adoption of 800 V drivetrains pulls demand for 1,700 V automotive-grade modules, while Nordic heat-pump installations underpin medium-power discrete sales. The EU’s digital product passport requirement reshapes bill-of-materials choices, as OEMs shift to materials with higher recyclability indices. European rail electrification upgrades also specify three-level inverters, boosting demand for press-pack devices with enhanced fault-ride-through.

North America benefits from the CHIPS Act, which grants a 25% investment tax credit for advanced fabs. Infineon and Wolfspeed announced capacity additions that will bring domestic 200 mm lines online, lowering lead times for automotive and renewables customers. Mexico’s industrial corridor is emerging as a near-shoring hub for inverter assembly, further strengthening regional demand.

The Middle East and Africa show the fastest 6.63% CAGR. Mega-projects like Saudi Arabia’s NEOM integrate gigawatt-scale solar and wind capacity, necessitating high-power IGBT stacks for HVDC links. Hitachi Energy’s Grid-enSure portfolio illustrates the focus on grid-friendly power electronics that stabilise fluctuating renewable inputs. Africa’s electrification of commuter rail boosts traction inverter orders, and localisation incentives in Egypt and South Africa spur module packaging investments.

Latin America maintains mid-single-digit growth as Brazil and Chile extend net-metering rules, incentivising rooftop and industrial PV systems. Rail retrofit programmes in Argentina use standard 1,200 V modules, underpinning baseline demand. Although the absolute market is smaller, currency depreciation in several economies raises import costs, nudging local contract manufacturers to partner with Asian die suppliers to manage pricing volatility.

Competitive Landscape

The insulated gate bipolar transistors market is moderately concentrated. Infineon, Mitsubishi Electric, and Semikron-Danfoss anchor the top tier with vertically integrated wafer-to-module operations. Infineon launched 15 A and 20 A EiceDRIVER isolated gate drivers in 2025, enabling traction inverters above 300 kW without external booster stages.[1] Infineon Technologies AG, “EiceDRIVER Isolated Gate Drivers,” infineon.com Mitsubishi Electric sampled its XB series 3.3 kV, 1,500 A module that cuts switching loss by 15%, targeting railway and large industrial drives. Semikron-Danfoss rounded out its Generation 7 family with 1,200 V SEMiX 6 modules rated to 175 °C junction, widening service intervals for wind-turbine converters.

Strategic partnerships define mid-tier competition. ROHM’s 2 kV SiC MOSFETs now ship inside Semikron-Danfoss hybrid modules for SMA Solar’s central inverters, blending SiC high-side switches with silicon IGBT low-sides to balance cost and efficiency.[2]ROHM Semiconductor, “2 kV SiC MOSFET Module for SMA Solar,” rohm.com Infineon signed long-term supply agreements with Stellantis covering smart power switches and silicon-carbide dies, securing volume visibility until 2030. ABB’s planned acquisition of Gamesa Electric’s power-electronics arm strengthens its renewables inverter portfolio and expands its serviceable base by 40 GW.

Smaller specialists focus on packaging innovations such as top-side cooling and wire-bond-free interconnects that push power density without shifting to SiC. Licensing deals around double-sided cooled substrates are accelerating, as EPC-class data-centre PSUs adopt IGBTs in intermediate-bus designs to reach 97.5% efficiency. These incremental advances collectively reinforce the competitive moat of incumbents even as SiC substitution intensifies.

Insulated Gate Bipolar Transistors Industry Leaders

Infineon Technologies AG

Renesas Electronics Corporation

Texas Instruments Incorporated

Microchip Technology Inc.

ABB Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Mitsubishi Electric began sampling its XB Series 3.3 kV / 1,500 A HVIGBT module featuring 15% lower switching loss and a 25% larger reverse-recovery safe-operating area for rail and heavy-industrial inverters

- February 2025: Infineon rolled out first 200 mm SiC products at its Kulim facility, paving the way for higher-throughput manufacturing of high-voltage devices used in renewable energy and traction

- January 2025: Infineon released new AEC-qualified EiceDRIVER isolated gate drivers rated for >300 kW traction inverter designs

- January 2025: FORVIA HELLA chose Infineon’s 1,200 V CoolSiC automotive MOSFETs with top-side cooling for next-generation 800 V DC-DC converters aimed at fast chargers

Global Insulated Gate Bipolar Transistors Market Report Scope

Insulated gate bipolar transistors are semiconductor devices with three terminals. It has been developed by combining the best qualities of both BJT and power MOSFETs. It provides a steady electricity supply by reducing the congestion in the power supply, which leads to optimized power utilization. The market study focuses on the trends affecting the market for applications in multiple regions. The study tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry. Further, the study also tracks the impact of COVID-19 on the overall insulated gate bipolar transistor industry and its performance.

The insulated gate bipolar transistor (IGBT) market is segmented by type (discrete IGBT and modular IGBT), power rating (high power, medium power, low power), application (automotive and EV/HEV, consumer, renewables, UPS, rail, industrial/motor drives), and geography (North America, Europe, Asia Pacific, and the rest of the world). The market sizes and forecasts are provided in terms of value (USD billion) for all the above segments.

| Discrete IGBT |

| IGBT Modules (Standard) |

| Intelligent Power Modules (IPM) |

| Press-Pack IGBT |

| High Power |

| Medium Power |

| Low Power |

| Upto 650 V (Low) |

| 651 - 1200 V (Medium) |

| 1201 - 1700 V (High) |

| Above 1700 V (Ultra-High) |

| EV/HEV Traction Inverters |

| Industrial Motor Drives |

| Renewable Energy Inverters (PV and Wind) |

| Uninterruptible Power Supplies (UPS) |

| Rail Traction |

| HVDC and FACTS |

| Consumer Appliances |

| Other Applications (Welders, Induction Heating) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Nordics | ||

| Rest of Europe | ||

| South America | Brazil | |

| Rest of South America | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Type | Discrete IGBT | ||

| IGBT Modules (Standard) | |||

| Intelligent Power Modules (IPM) | |||

| Press-Pack IGBT | |||

| By Power Rating | High Power | ||

| Medium Power | |||

| Low Power | |||

| By Voltage Class | Upto 650 V (Low) | ||

| 651 - 1200 V (Medium) | |||

| 1201 - 1700 V (High) | |||

| Above 1700 V (Ultra-High) | |||

| By Application | EV/HEV Traction Inverters | ||

| Industrial Motor Drives | |||

| Renewable Energy Inverters (PV and Wind) | |||

| Uninterruptible Power Supplies (UPS) | |||

| Rail Traction | |||

| HVDC and FACTS | |||

| Consumer Appliances | |||

| Other Applications (Welders, Induction Heating) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Nordics | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Rest of South America | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the insulated gate bipolar transistors market?

The market is valued at USD 8.26 billion in 2026 and is projected to grow to USD 10.94 billion by 2031 at a 5.78% CAGR

Which product type leads the insulated gate bipolar transistors market?

IGBT modules lead with 54.78% revenue share in 2025 due to their integration benefits in industrial and renewable applications.

How fast is the automotive segment expanding?

EV and HEV traction inverters are advancing at a 8.74% CAGR through 2031 on the back of 800 V battery architectures.

Why are ultra-high-voltage IGBTs gaining attention?

Devices above 1,700 V post the strongest 7.72% CAGR because HVDC links and large wind farms require higher blocking voltages for grid-code compliance.

Page last updated on: