Bipolar Power Transistor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

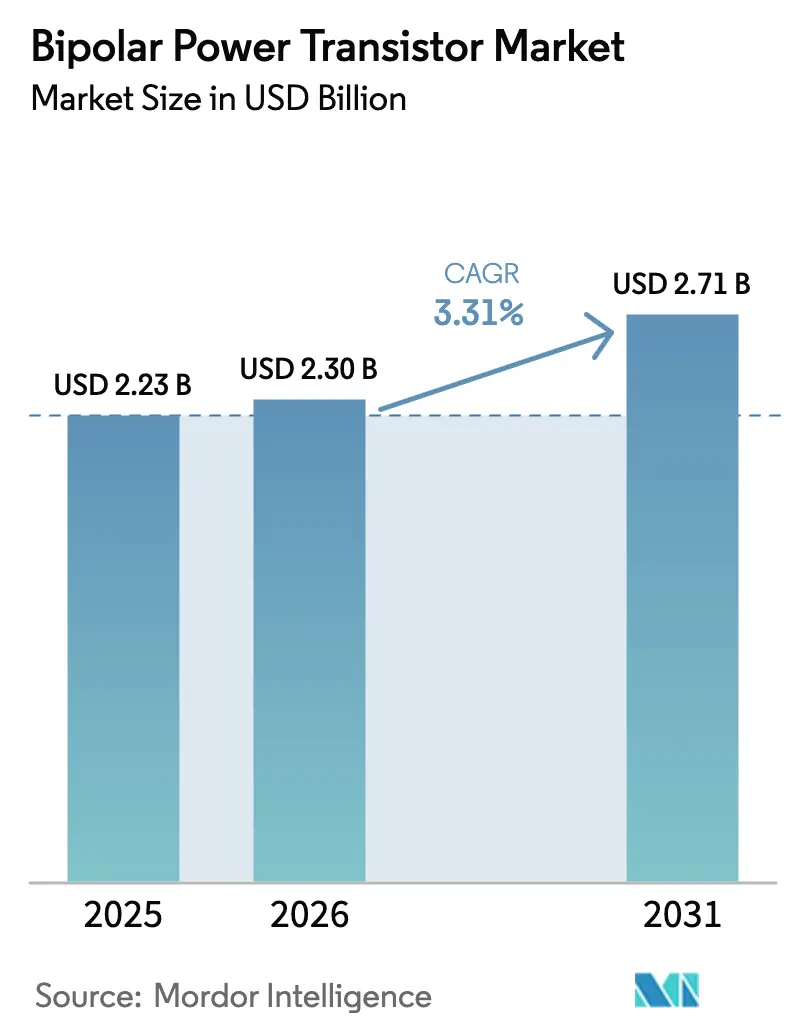

| Market Size (2026) | USD 2.3 Billion |

| Market Size (2031) | USD 2.71 Billion |

| Growth Rate (2026 - 2031) | 3.31% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Bipolar Power Transistor Market Analysis by Mordor Intelligence

The bipolar power transistor market size in 2026 is estimated at USD 2.3 billion, growing from 2025 value of USD 2.23 billion with 2031 projections showing USD 2.71 billion, growing at 3.31% CAGR over 2026-2031. Steady revenue expansion masks the disruptive shift from legacy silicon toward silicon carbide as automotive electrification, renewable energy, and 5G infrastructure raise performance requirements. Silicon keeps volume leadership through mature fabrication lines and cost advantages, yet wide-bandgap materials capture critical design wins where thermal headroom, switching speed, and power density outweigh price sensitivities. Asia-Pacific leads shipments on the strength of China’s scale and Japan’s precision manufacturing, while Europe’s stringent efficiency rules and North America’s high-reliability niches shape differentiated demand. End-use focus migrates from consumer electronics toward renewable energy, EV powertrains, and industrial automation, steering suppliers to higher value applications as discrete device volumes plateau.

Key Report Takeaways

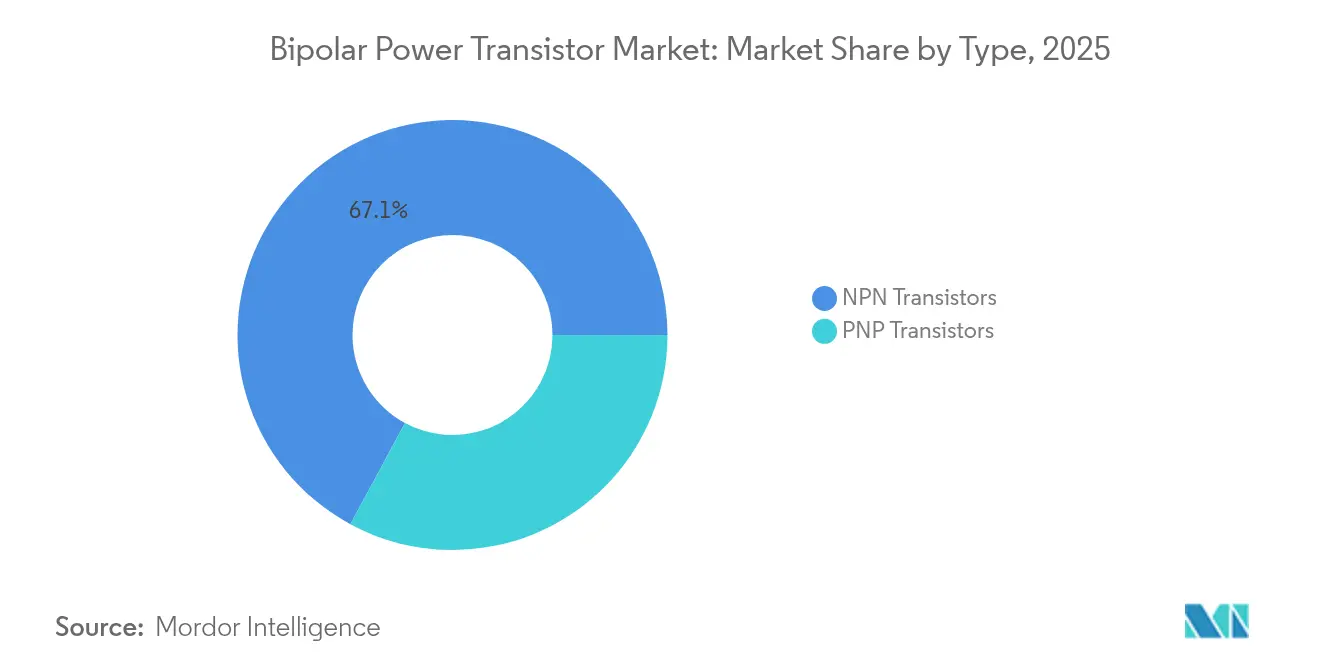

- By type, NPN devices held 67.12% of the bipolar power transistor market share in 2025, while silicon carbide BJTs register the fastest 4.71% CAGR to 2031.

- By material, silicon dominated revenue with 80.76% in 2025, and silicon carbide is set for the highest 4.71% CAGR through 2031.

- By package, surface-mount formats accounted for 61.75% of the bipolar power transistor market size in 2025, and power modules plus hybrid ICs are growing at a 5.11% CAGR.

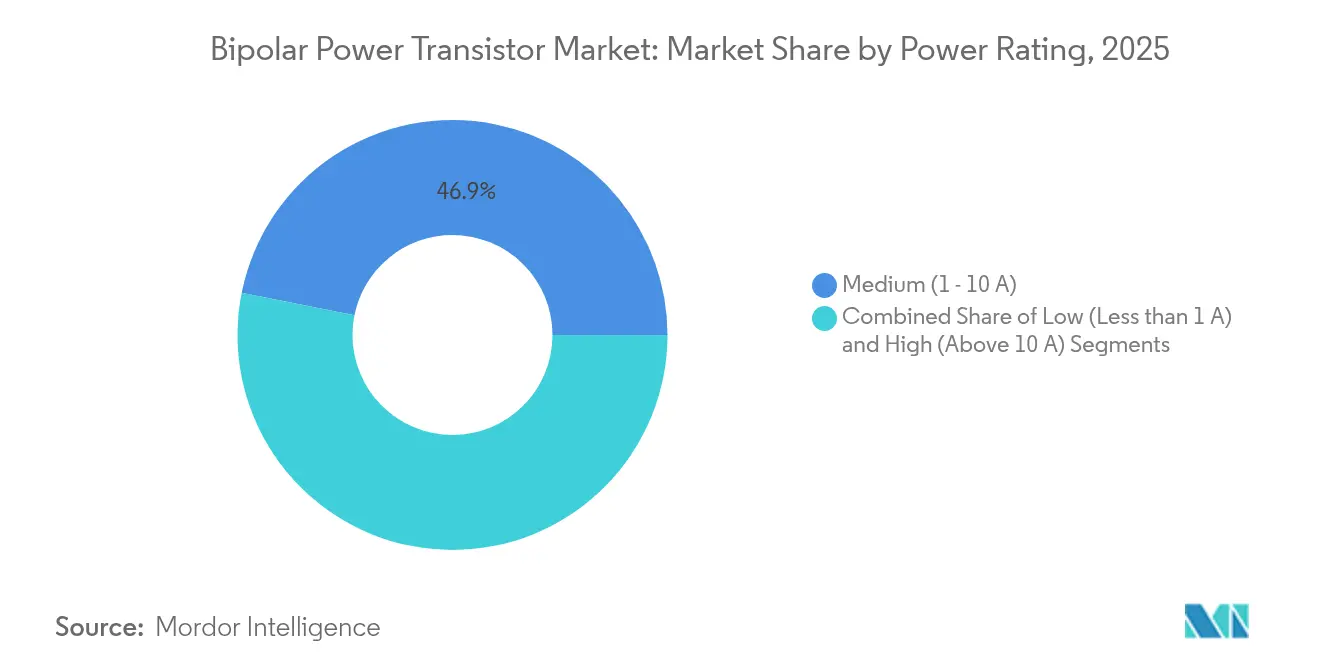

- By power rating, medium-power (1–10 A) devices led with 46.85% share in 2025, while high-power (>10 A) units expand at 4.02% CAGR.

- By end-user, consumer electronics generated 28.94% revenue in 2025, and renewable energy registers the quickest 3.55% CAGR to 2031.

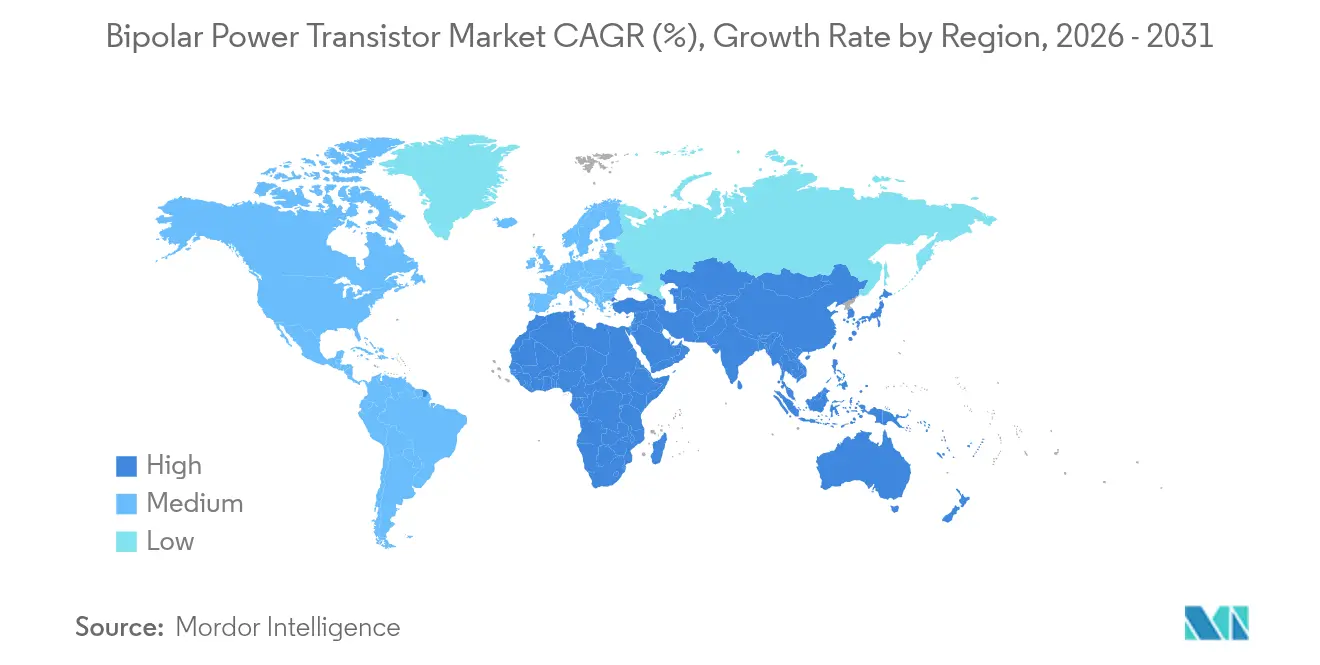

- By region, Asia-Pacific captured 50.65% revenue in 2025; the Middle East and Africa show the highest 3.63% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bipolar Power Transistor Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electrification of 48 V mild-hybrid powertrains in European vehicles | +0.8% | Europe, spillover to North America | Medium term (2-4 years) |

| Proliferation of silicon carbide BJTs in solar micro-inverters across Asia | +0.6% | Asia-Pacific core, expanding to MEA | Long term (≥ 4 years) |

| Demand for cost-optimised discrete switches in low-power IoT wearables | +0.4% | Global, Asia-Pacific concentration | Short term (≤ 2 years) |

| High-reliability needs for avionics power control units in North America | +0.3% | North America, global defence | Long term (≥ 4 years) |

| Roll-out of mmWave 5G macro base-stations in South Korea and Japan | +0.5% | Asia-Pacific, developed markets | Medium term (2-4 years) |

| Retrofit of legacy industrial motor drives in South America mining | +0.2% | South America, other emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Electrification of 48 V Mild-Hybrid Powertrains in European Vehicles

European OEMs are scaling 48 V systems to meet emissions rules and lower electrification bills. Belt starter generators, integrated starter generators, and electric turbochargers rely on efficient bipolar switching to handle 10–20 kW bursts while maintaining compatibility with 12 V architectures. Molex indicates connector redesign tackles electromagnetic interference at elevated voltages. Onsemi’s APM21 module combines multiple switches and thermal enhancements for compact layouts.[1]Onsemi, “48-Volt Systems for Mild Hybrid Electric Vehicles and Beyond,” onsemi.comReliability and low BOM cost keep bipolar devices central to these subsystems, supporting a +0.8% uplift in the bipolar power transistor market CAGR through 2030.

Proliferation of Silicon Carbide BJTs in Solar Micro-Inverters across Asia

Asia-Pacific utility-scale and rooftop solar additions drive micro-inverter uptake, and SiC BJTs cut switching losses up to 50% versus silicon. ROHM and Semikron Danfoss integrated 2 kV SiC MOSFETs into SMA systems for 1500 V DC links that raise yield.[2]ROHM Semiconductor, “Semikron Danfoss' Module with ROHM's latest 2kV SiC MOSFETs,” rohm.com China’s economies of scale and Japan’s quality focus underpin cost and reliability improvements, giving SiC a long-term tailwind and adding +0.6% to growth prospects for the bipolar power transistor market.

Demand for Cost-Optimised Discrete Switches in Low-Power IoT Wearables

Smartwatches, health bands, and sensor tags need sub-1A switches that maximise battery life and fit small footprints. Research on hetero-dielectric gate-all-around devices shows better subthreshold swings that lift efficiency for wearable nodes.[3]MDPI, “Low-Power Energy-Efficient Hetero-Dielectric Gate-All-Around MOSFETs,” mdpi.comAsia-Pacific fabrication hubs deliver cost structures aligned with high-volume consumer pricing. Packaging miniaturisation ensures discrete bipolar transistors remain favoured for size-constrained boards, contributing +0.4% to sector growth.

High-Reliability Requirements for Avionics Power Control Units in North America

Mission-critical avionics demand transistors qualified for radiation and temperature extremes. Microchip’s BJTs meet Joint Army-Navy specifications after enhanced low-dose-rate sensitivity testing. Wide-bandgap devices promise future density gains, yet adoption lags in defence contracts due to lengthy validation cycles. Premium pricing offsets lower volumes, lifting the bipolar power transistor market via a +0.3% CAGR boost.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Share loss to power MOSFETs in high-frequency DC-DC converters | -0.7% | Global, developed markets | Short term (≤ 2 years) |

| Thermal runaway risk above 150°C in EV traction inverters | -0.5% | Global automotive | Medium term (2-4 years) |

| Tightened EU ecodesign regulations on standby losses | -0.3% | Europe, global spillover | Long term (≥ 4 years) |

| Supply instability of high-purity germanium for SiGe BJTs | -0.4% | Global high-performance segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Share Loss to Power MOSFETs in High-Frequency DC-DC Converters

Efficient MOSFET gate control enhances switching above 300 kHz, making them preferred within data centre and telecom converters. Infineon’s CoolGaN integrates Schottky diodes, trimming deadtime losses and shrinking designs.[4]Infineon Technologies AG, “Infineon launches world's first industrial gallium nitride transistor family,” infineon.comBipolar suppliers focus on cost-sensitive or lower frequency grids, facing a -0.7% drag on market CAGR.

Thermal Runaway Risk above 150°C Limits Adoption in EV Traction Inverters

IGBT and SiC modules with double-sided cooling mitigate heat better than bipolar counterparts. MDPI research underlines advanced junction temperature estimation for safe operation. EV charging heat flux has already risen tenfold since 2024. The thermal ceiling subtracts -0.5% from growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: NPN Dominance Drives Circuit Standardization

NPN transistors controlled 67.12% revenue in 2025, and the bipolar power transistor market size for this category is forecast to expand at 3.33% CAGR to 2031. Positive-rail system designs in automotive ECUs, industrial drives, and consumer power supplies favour NPN polarity, anchoring demand even as new materials emerge. PNP units retain complementary roles in push-pull stages and negative-rail circuits, yet economies of scale keep NPN cost leadership intact. Continuous library reuse shortens design cycles, making NPN the default choice when engineers weigh part sourcing and validation schedules.

Migration to silicon carbide preserves NPN conventions. STMicroelectronics maps familiar pin-outs onto SiC structures, easing qualification and widening the bipolar power transistor market footprint in EV charging, renewable inverters, and 5 G power boards. This coherence ensures sustained revenue even if overall discrete volumes moderate.

By Material: Silicon Carbide Emerges Despite Silicon Leadership

Silicon delivered 80.76% revenue in 2025 due to high wafer throughput and decades-old fab lines. Yet, silicon carbide devices book a 4.71% CAGR and increasingly crowd high-voltage sockets, capturing a rising slice of the bipolar power transistor market share. SiC’s wider bandgap shrinks conduction losses and allows 175 °C junctions, cutting heat-sink mass in EVs and string inverters. Infineon’s 200 mm wafer ramp at Kulim underwrites future supply and narrows cost gaps.

Silicon’s entrenched ecosystem shields high-volume consumer and IoT segments, but multi-kilowatt designs pivot toward SiC for range and efficiency gains. Hybrid boards blending both materials blossom, allowing designers to match the right die to each stress zone, which lifts overall bipolar power transistor market flexibility.

By Power Rating: High Current Designs Propel Premium Mix

Medium-power (1-10 A) parts held a 46.85% share in 2025, feeding automotive auxiliaries, appliance motors, and broad industrial use. The bipolar power transistor market size for high-power (>10 A) devices posts a 4.02% CAGR to 2031 as EV chargers, solar string inverters, and factory robotics standardise on higher bus currents to curb conductor bulk. Low-power (<1 A) switches remain staples in wearables and IoT remotes, but their dollar value plateaus as consumer devices consolidate functions into SOCs.

High-current designs demand tighter thermal paths and advanced packaging. ROHM’s molded SiC modules in HSDIP20 deliver triple the power density of older frames, proving that packaging innovation, not die size, governs performance at 20 A+ levels. As system voltages climb from 400 V to 800 V in fast-charge EV stacks, current per device still swells, channelling fresh revenue into the high-power end of the bipolar power transistor market.

By Frequency Range: RF Upswing Challenges Low-Frequency Comfort Zone

Applications below 300 kHz still command 64.65% revenue in 2025, spanning motor drives, UPS units, and conventional switch-mode supplies. Radio-frequency and microwave tiers between 300 kHz and 6 GHz notch a 3.74% CAGR as 5 G macro sites, phased-array radar,s and V2X links proliferate. mmWave cells push gain, linearity, and ruggedness requirements that favour specialised bipolar topologies.

NXP and other RF houses pair SiGe front ends with GaN power stages, yet driver and pre-driver slots often retain silicon BJTs for predictable biasing. Certification for telecom adds complexity, but premium ASPs lift revenue density inside the bipolar power transistor market. Legacy low-frequency categories remain durable as grid-tied assets age slowly, preserving a wide base that funds R&D for RF growth.

By Package Type: Integration Drives Surface-Mount and Modules

Surface-mount packages such as SOT-223 and DPAK represented 61.75% shipments in 2025 because automated pick-and-place lines cut labour cost and boost board reliability. Power modules and hybrid ICs outpace at 5.11% CAGR, combining multiple dies, drivers and sometimes passive layers in a single enclosure that trims footprint while boosting thermal conduction. Through-hole cans like TO-220 persist where heat spread and bolt-down force outweigh solderability, for example in industrial welders and locomotive drives.

Rising EV voltages and server power densities fuel module growth. Onsemi’s Czech plant will vertically integrate boule to finished module, illustrating how supply control underpins cost and delivery surety. Thermal interface materials, direct-bonded copper substrates and leadframe alloy tweaks become differentiators, steering buyers to vendors that package innovation into bipolar power transistor market offerings.

By End-User Industry: Renewable Infrastructure Outspeeds Consumer Volumes

Consumer electronics accounted for 28.94% 2025 revenue, but shipments inch forward as smartphones and TVs saturate. Renewable-energy systems expand at 3.55% CAGR to 2031, lifting the bipolar power transistor market as governments chase decarbonisation goals. Data-intensive 5 G and edge servers keep ICT spending robust, whereas industrial automation gains momentum from retrofits and smart factory rollouts.

EV powertrains and on-board chargers are the showpiece growth engines. Silicon carbide BJTs in traction inverters add range while curbing cooling mass, making them integral to regulatory compliance and customer acceptance. Aerospace and defence remain a steady yet limited slice, characterised by decade-long lifecycles and tight qualification rules that stabilise cash flow inside the bipolar power transistor market.

Geography Analysis

Asia-Pacific generated 50.65% of 2025 revenue, and the bipolar power transistor market size in the region is forecast to widen as China channels subsidies into renewables and EVs, Japan pushes precision IC packaging, and South Korea scales 5G macro sites. Domestic material policies, including China’s gallium and germanium export controls, raise input volatility and spur localization projects, influencing sourcing and pricing strategies.

Europe’s OEMs enforce 48 V mild-hybrid penetration and adhere to EU eco-design rules that penalize standby losses, directing R&D toward efficiency upgrades. STMicroelectronics’ planned Sicily SiC fab, backed by EUR 5 billion (USD 5.88 billion) in aid, exemplifies reshoring momentum. Regional alignment around clean mobility and industrial decarbonization sustains demand for advanced bipolar power devices.

North America relies on aviation, defense, and industrial automation, where lifetime reliability offsets low shipment counts. Long qualification cycles stabilize revenue streams and favor entrenched suppliers. Middle East and Africa post the swiftest 3.63% CAGR as utility-scale solar farms and grid-expansion projects dominate capex. South America’s mines refit motor drives, creating niche demand pockets underpinned by commodity export cashflows.

Competitive Landscape

Market concentration is moderate. STMicroelectronics owns 32.6% of silicon carbide revenue after early capacity bets, while Infineon, onsemi, and Wolfspeed expand through acquisitions and greenfield fabs. Onsemi secured Qorvo’s SiC JFET assets for USD 115 million, targeting AI data center power stages. Infineon added GaN Systems for USD 830 million to deepen wide-bandgap coverage. Capital intensity is rising, illustrated by onsemi’s USD 2 billion Czech SiC project that achieves vertical integration from boule to module.

Technology rivalry focuses on thermal interfaces, module integration, and material purity. Supply-chain control provides cost savings and resilience amid critical mineral restrictions. Specialists carve niches in extreme environments, such as Microchip’s radiation-hardened BJTs. Overall, top suppliers balance scale and specialty portfolios to address divergent cost and performance criteria across the bipolar power transistor market.

Bipolar Power Transistor Industry Leaders

-

STMicroelectronics

-

TT Electronics

-

Nexperia

-

Sanken Electric Co., Ltd.

-

ON Semiconductor (onsemi)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: ROHM introduced 4-in-1 and 6-in-1 SiC molded modules in HSDIP20 packages for onboard chargers with triple power density.

- April 2025: ROHM introduced 4-in-1 and 6-in-1 SiC molded modules in HSDIP20 packages for onboard chargers with triple power density.

- February 2025: Infineon launched its first 200 mm SiC devices from Kulim, Malaysia, targeting renewable and EV platforms.

- January 2025: Onsemi completed the acquisition of Qorvo’s SiC JFET technology business for USD 115 million, broadening its EliteSiC lineup.

Global Bipolar Power Transistor Market Report Scope

A bipolar power transistor is a semiconductor device commonly used for amplification. The device can amplify analog or digital signals. It can also switch DC or function as an oscillator. Physically, a bipolar power transistor amplifies large voltage and current, but it can be connected to circuits designed to amplify voltage or power. The study covers Bipolar power transistor that includes PNP Transistor, NPN Transistor, and usage of Bipolar Power Transistor across major end-users such as consumer electronics, communication and technology, automotive, manufacturing, energy, and power. The study also covers demand across various regions and considers the impact of COVID-19 on the market.

| NPN Transistors |

| PNP Transistors |

| Silicon (Si) |

| Silicon-Germanium (SiGe) |

| Silicon Carbide (SiC) |

| Gallium Arsenide (GaAs) |

| Low (Less than 1 A) |

| Medium (1 - 10 A) |

| High (Above 10 A) |

| Low-Frequency (Less than 300 kHz) |

| Radio-Frequency and Microwave (300 kHz - 6 GHz) |

| Through-Hole (TO-220, TO-3) |

| Surface-Mount (SOT-223, DPAK) |

| Power Modules and Hybrid ICs |

| Consumer Electronics |

| ICT and 5G Infrastructure |

| Automotive and EV Powertrain |

| Industrial Motor Drives and Automation |

| Renewable Energy and Power (Solar, Wind) |

| Aerospace and Defense |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Nordics (Denmark, Sweden, Norway, Finland) | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | Gulf Cooperation Council Countries |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Type | NPN Transistors | |

| PNP Transistors | ||

| By Material | Silicon (Si) | |

| Silicon-Germanium (SiGe) | ||

| Silicon Carbide (SiC) | ||

| Gallium Arsenide (GaAs) | ||

| By Power Rating | Low (Less than 1 A) | |

| Medium (1 - 10 A) | ||

| High (Above 10 A) | ||

| By Frequency Range | Low-Frequency (Less than 300 kHz) | |

| Radio-Frequency and Microwave (300 kHz - 6 GHz) | ||

| By Package Type | Through-Hole (TO-220, TO-3) | |

| Surface-Mount (SOT-223, DPAK) | ||

| Power Modules and Hybrid ICs | ||

| By End-User Industry | Consumer Electronics | |

| ICT and 5G Infrastructure | ||

| Automotive and EV Powertrain | ||

| Industrial Motor Drives and Automation | ||

| Renewable Energy and Power (Solar, Wind) | ||

| Aerospace and Defense | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordics (Denmark, Sweden, Norway, Finland) | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Southeast Asia | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | Gulf Cooperation Council Countries | |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the bipolar power transistor market?

The bipolar power transistor market is valued at USD 2.3 billion in 2026.

How fast will the bipolar power transistor market grow through 2031?

Revenue is forecast to increase at a 3.31% CAGR, reaching USD 2.71 billion by 2031.

Which region leads demand for bipolar power transistors?

Asia-Pacific holds 50.65% revenue share, driven by China’s manufacturing ecosystems and Japan’s precision electronics sector.

Why are silicon carbide devices important for future growth?

Silicon carbide offers higher voltage tolerance and lower switching losses, enabling efficiency gains in EV powertrains and solar inverters and therefore delivers the fastest 4.71% CAGR.

Which end-user segment shows the quickest growth?

Renewable energy and power applications record the highest 3.55% CAGR as solar and wind installations expand.

Page last updated on: