Metal Composite Power Inductor Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 1.99 Billion |

| Market Size (2030) | USD 2.85 Billion |

| Growth Rate (2025 - 2030) | 7.46% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

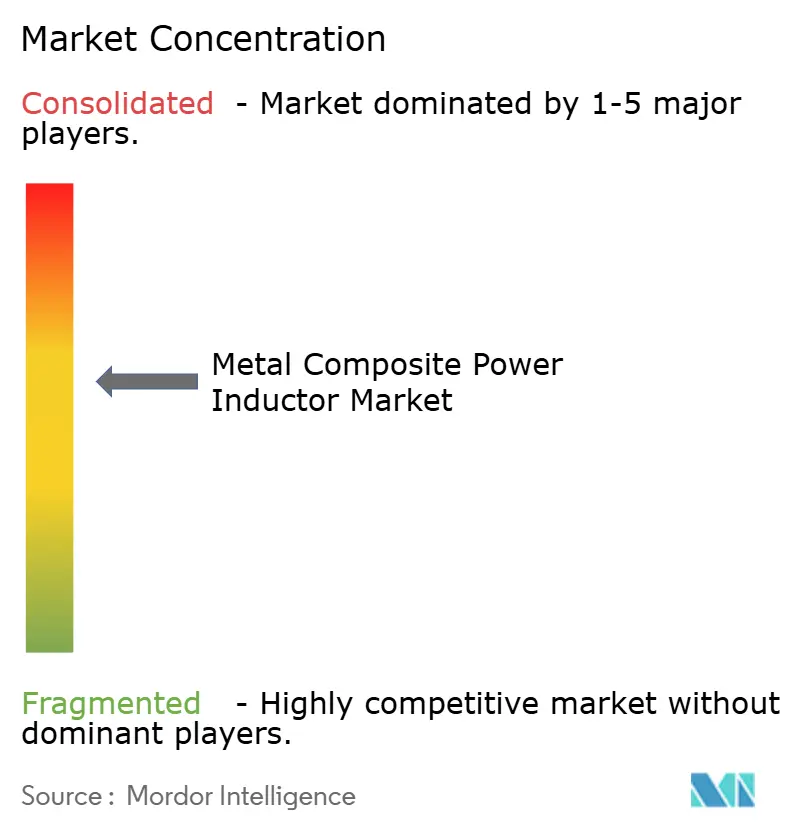

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Metal Composite Power Inductor Market Analysis by Mordor Intelligence

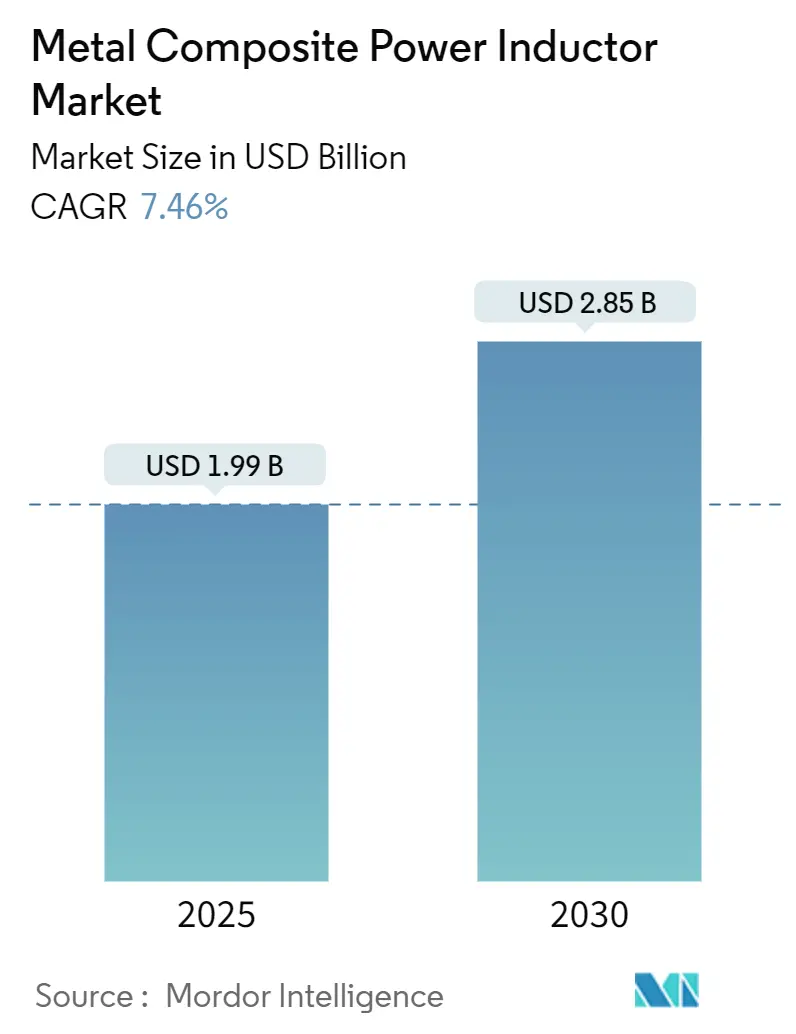

The Metal Composite Power Inductor market size reached USD 1.99 billion in 2025 and is projected to expand to USD 2.85 billion by 2030, translating into a 7.46% CAGR through the forecast period. Robust growth stems from accelerating electrification, the shift toward high-frequency GaN/SiC power stages, and ever-tighter electromagnetic-compatibility regulations. Across end markets, designers favor metal composite cores because they sustain higher saturation currents, exhibit lower core losses, and remain thermally stable at elevated temperatures. The Asia-Pacific region underpins demand thanks to its dense electronics manufacturing base and government-backed electric-vehicle incentives, while North American and European OEMs propel premium adoption through strict board-level EMI mandates. Competitive intensity stays moderate; scale players such as TDK and Murata protect share with deep R&D pipelines, yet niche alloy specialists continue to carve out high-margin applications in fast-switching converters and ultra-thin wearables.

Key Report Takeaways

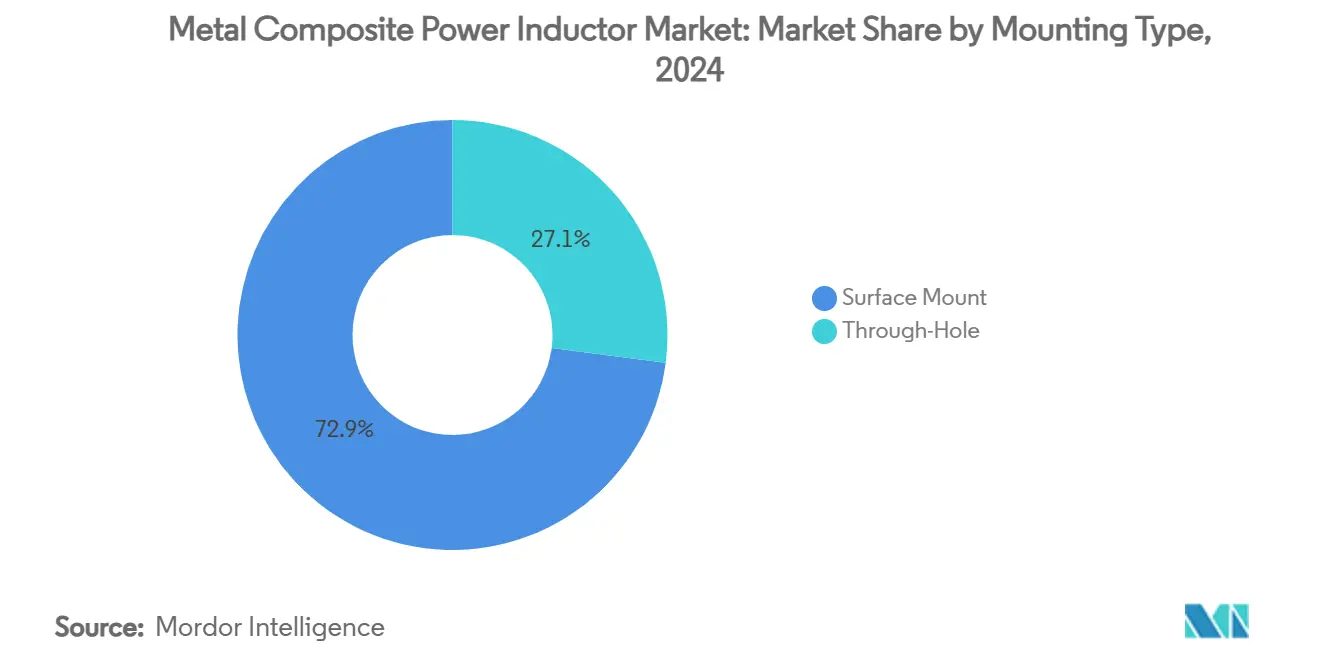

- By mounting type, surface-mount technology held 72.94% of 2024 revenue and is advancing at a 7.76% CAGR to 2030.

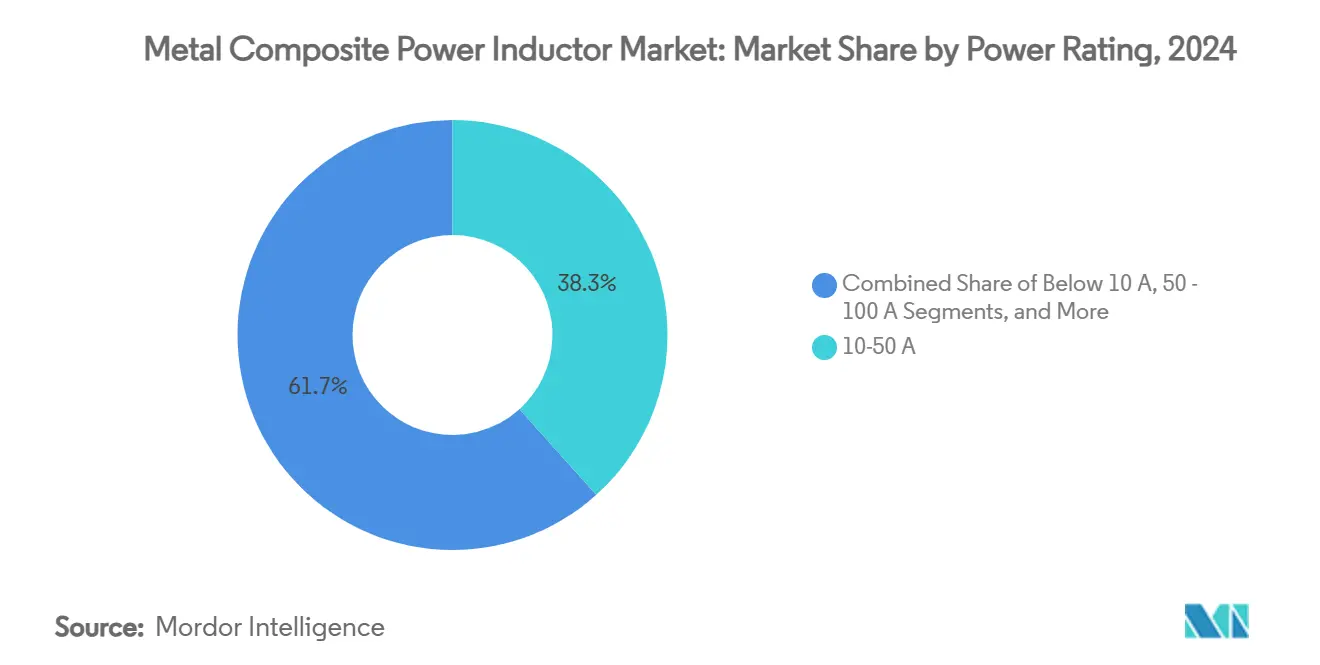

- By power rating, the 10–50 A band commanded 38.34% of 2024 revenue, while the Above 100 A band is projected to expand at 7.56% CAGR.

- By shielding type, shielded variants captured 64.88% share in 2024 and record the highest growth at 7.61% CAGR.

- By core material, alloy cores accounted for the largest 46.83% slice in 2024 and are rising at a 7.81% CAGR.

- By end user, consumer electronics led with 35.73% share in 2024; automotive applications chart the fastest 7.49% CAGR through 2030.

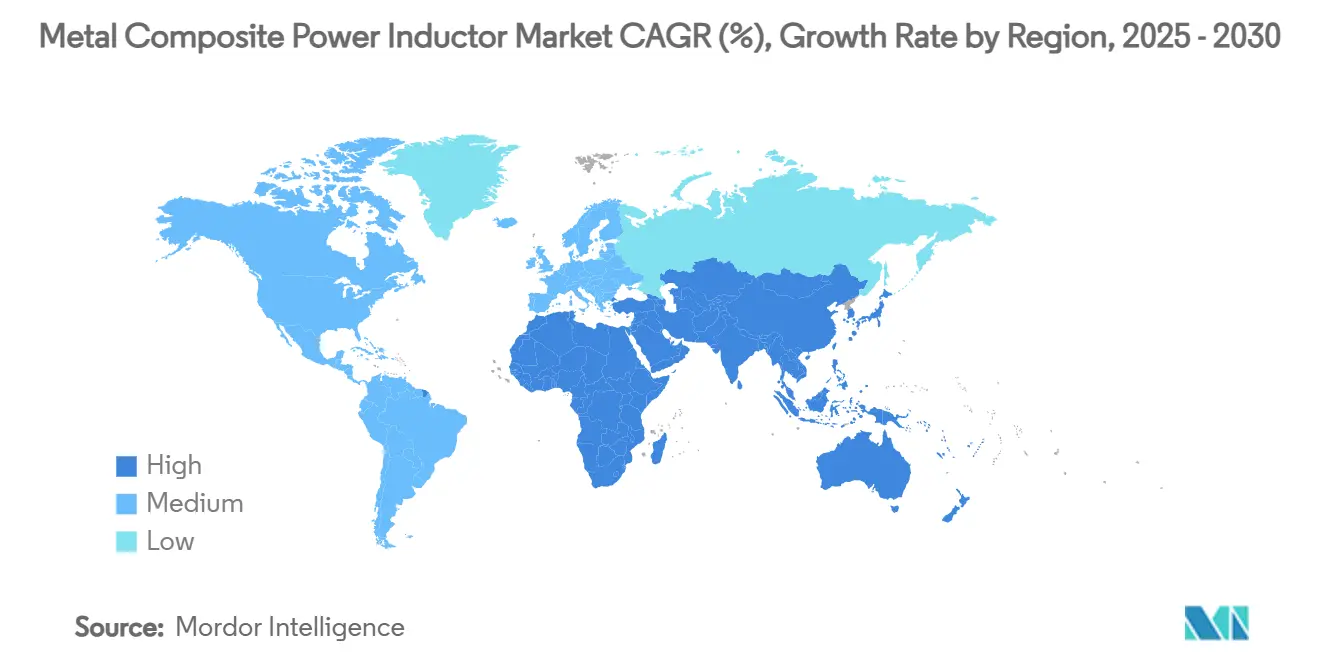

- By geography, Asia-Pacific dominated with a 57.92% share in 2024 and is outpacing all regions at a 7.98% CAGR.

Global Metal Composite Power Inductor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid rise in multi-cell battery architectures for e-mobility | +1.2% | Global, with concentration in China, Europe, North America | Medium term (2-4 years) |

| Proliferation of GaN/SiC fast-switching power stages in consumer and industrial DC-DC converters | +0.8% | Global, led by Asia-Pacific and North America | Short term (≤ 2 years) |

| OEM move toward board-level EMI compliance demanding integrated magnetic shielding | +1.1% | Global, with emphasis on Europe and North America regulatory markets | Medium term (2-4 years) |

| Mainstream demand for ultra-thin SMD inductors in foldable and wearable devices | +0.9% | Asia-Pacific core, spill-over to North America and Europe | Short term (≤ 2 years) |

| Automotive OEM qualification of molded-core alloy inductors for ADAS domain controllers | +0.7% | Global automotive markets, led by Germany, Japan, China, USA | Long term (≥ 4 years) |

| Localized supply-chain incentives for magnetic-component manufacturing in India and Vietnam | +0.6% | Asia-Pacific, with global supply chain implications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid rise in multi-cell battery architectures for e-mobility

Automakers now deploy battery packs with up to 96 cells, and each cell group requires its own DC-DC stage. This architecture multiplies the number of inductors per vehicle ten-fold, pushing specifications toward higher current density and tighter thermal control. Designs such as Tesla’s 4680 pack demand inductor efficiency above 95% during fast charging, driving preference for metal composite cores that avoid saturation under surge currents.

Proliferation of GaN/SiC fast-switching power stages

Wide-bandgap semiconductors operate above 1 MHz and require inductors with extremely low core losses. Metal composite devices paired with GaN converters raise system efficiency by up to 40% in consumer chargers and by several percentage points in data-center supplies. [1]Infineon Technologies, “Switched Mode Power Supplies Applications,” infineon.com Premium pricing of 30–50% over ferrite equivalents is easily justified by the energy savings these stages unlock.

OEM move toward board-level EMI compliance demanding integrated magnetic shielding

Revised EMC rules such as the EU’s Directive 2014/30/EU tighten emission limits between 30 MHz and 1 GHz. Designers increasingly embed shielding into the inductor itself, eliminating discrete filters and saving PCB area. Würth Elektronik’s WE-SHC cabinet delivers up to 80 dB attenuation within the same footprint as a standard inductor. [2]Würth Elektronik, “WE-SHC Shielding Cabinet,” we-online.com

Mainstream demand for ultra-thin SMD inductors in foldable and wearable devices

Smartphones under 7 mm thick and 0.4 mm-high inductors for flexible boards draw on novel winding and molding methods. Murata’s 0603-size lineup demonstrates how suppliers hit mechanical-stress and moisture-survival targets while charging 2–3 times the standard price.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in high-purity iron and amorphous alloy prices | -0.4% | Global, with particular impact on Asia-Pacific manufacturing | Short term (≤ 2 years) |

| Thermal-runaway concerns above 150°C limiting in-cabin EV placement | -0.3% | Global automotive markets, especially in hot climate regions | Medium term (2-4 years) |

| Stringent AEC-Q200 re-qualification cycles slowing new-material adoption | -0.2% | Global automotive markets, with emphasis on Europe, North America, Japan | Long term (≥ 4 years) |

| CapEx-heavy metal-powder molding lines deterring small EMS players | -0.1% | Global, with concentration in Asia-Pacific and emerging manufacturing regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in high-purity iron and amorphous alloy prices

Feedstock accounts for almost half of manufacturing costs, and 25–35% price swings over 12 months force suppliers to rewrite contracts quarterly. Smaller firms lacking long-term agreements struggle to protect margins, accelerating consolidation. [3]Advanced Energy, “Power Supply Thermal Management White Paper,” advancedenergy.com

Thermal-runaway concerns above 150 °C limiting in-cabin EV placement

Most metal composite cores derate rapidly beyond 150 °C. Automotive platforms seeking 175 °C boards must either add cooling hardware or relocate inductors away from heat sources, inflating system cost. Although TDK has qualified variants rated to 1600 mA and enhanced temperature tolerance, broad adoption awaits further material breakthroughs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Rating: High-current designs attract premium margins

Metal Composite Power Inductor market revenue leaned on the 10–50 A class, which controlled 38.34% of 2024 sales and anchors automobile traction inverters and industrial servo drives. The above-100 A tier is the pace-setter, climbing at 7.56% CAGR as fast-charge stations and grid-scale storage specify saturation currents beyond 120 A. Manufacturers battle rising core temperatures through thicker winding conductors, molded heat spreaders, and novel alloy recipes. Bourns’ AEC-Q200-grade lineup reaching 70 A illustrates how suppliers obtain compliance and command 3–4-fold price premiums per ampere.

Spacing constraints in consumer electronics secure the Below 10 A niche, yet consistent volume offsets the segment’s moderate growth. Aerospace and defense designers favor the 50–100 A band for radar and avionic power rails that must tolerate vibration cycles far beyond commercial standards. This breadth of current classes preserves long-tail demand across legacy and emerging systems.

By Shielding Type: EMI mandates push adoption of integrated solutions

Shielded constructions formed 64.88% of 2024 shipments, and the share widens on a 7.61% CAGR as every electronics sub-assembly faces tougher emission ceilings. Automotive ADAS modules and industrial robotics place PCBs within compact enclosures where stray flux endangers neighboring sensors. The incremental bill-of-material cost is eclipsed by the savings from eliminating discrete ferrite beads and copper shielding cans.

Unshielded alternatives hold traction in isolated power bricks and low-noise analog instrumentation where enclosure-level Faraday cages already exist. Nevertheless, thin-film magnetic covers and nanocrystalline laminations are shrinking the cost delta between the two families, accelerating the flow toward shielded dominance.

By Core Material: Alloy technology underwrites performance leadership

Alloy cores delivered 46.83% of 2024 sales and post a 7.81% CAGR as efficiency targets rise. The Metal Composite Power Inductor market share of ferrite has been stable in low-power, high-frequency roles, yet its high-loss profile beyond 500 kHz restricts relevance in next-generation GaN supplies. Iron-powder variants stay popular in cost-critical consumer gadgets, but even here miniaturization forces gradual alloy substitution.

Material scientists integrate amorphous powders with nanocrystalline flakes to widen bandwidth and saturation thresholds, enabling <1% core-loss slopes at >1 MHz switch frequencies. These hybrids remain a specialty today, though the learning curve promises broader commercialization once molding yields and raw material logistics mature.

By Mounting Type: Automation cements surface-mount leadership

Surface-mount assemblies represented 72.94% of 2024 shipments and accelerate on a 7.76% CAGR as factories push straight-through reflow lines to cut labor costs. Direct-to-board heat paths permit higher power density, pivotal for 100 W USB-C chargers and miniature LED drivers. Taiyo Yuden’s micro-MCOIL series epitomizes performance gains achieved via low-profile lead frames and optimized pad geometries.

Through-hole devices persist wherever vibration, shock, or current levels exceed surface-mount staples. Defense avionics, railway traction, and mining automation value the mechanical anchoring offered by pin-in-paste joints. Even here, selective-solder robotics and reinforced gull-wing terminals are closing the reliability gap, suggesting a gradual but steady swing to full surface mounting over the decade.

By End User: Automotive electrification overtakes volume leader consumer electronics

Consumer brands remain the largest outlet at 35.73% of 2024 demand, but slowing handset refresh cycles temper unit growth. Automotive applications race forward at a 7.49% CAGR as every EV integrates traction inverters, DC-DC converters, on-board chargers, and ADAS domain controllers—collectively exceeding 70 inductors per vehicle in premium trims.

Industrial drives and factory automation contribute predictable baseline demand at mid-single-digit growth, while healthcare capitalizes on high-margin diagnostic imaging and patient-monitoring gear requiring ultra-low noise inductors. Aerospace and defense, though cyclical, underpin the highest average selling prices thanks to extended temperature and shock ratings.

Geography Analysis

Asia-Pacific anchored 57.92% of 2024 revenue and is accelerating at 7.98% CAGR on the back of China’s EV boom, Japan’s ADAS leadership, and India’s new incentive schemes for passive-component fabrication. Localization in Vietnam further diversifies the supply base, mitigating geopolitical risk while sustaining cost competitiveness.

North America captures a sizable slice through stringent EMI norms and the onshoring push supported by the CHIPS and Science Act. Advanced fabs in Arizona and Texas invite co-located passive suppliers, enhancing domestic resilience and commanding premium pricing for automotive-grade and data-center-class parts.

Europe sustains demand via Germany’s carmakers and continent-wide carbon-neutrality mandates. Tight EMC rules spur adoption of shielded, alloy-core designs, and niche suppliers in Austria and Switzerland excel in high-reliability segments. The Middle East and Africa remain emergent, with renewable-energy rollouts and 5G networks offering selective growth pockets once macroeconomic stability returns.

Competitive Landscape

The Metal Composite Power Inductor market features a balanced structure where three leaders—TDK, Murata, Vishay—retain scale advantages, yet dozens of mid-sized specialists thrive in performance-driven niches. Large groups cross-sell capacitors and EMC materials to lock in design wins, while newcomers differentiate on novel alloy chemistries, extreme-temperature ratings, or ultra-compact form factors.

R&D pipelines emphasize hybrid powder blends, advanced molding resins, and inductor-on-leadframe topologies that combine low DCR with thin profiles. Patent filings cluster around wireless power-transfer coils and board-embedded magnetics, highlighting future adjacencies. Consolidation continues: Bel Fuse’s Enercon acquisition and Delta Electronics’ purchase of Alps Alpine’s inductor unit enlarge industrial and automotive footprints, respectively.

Automotive qualification remains the most formidable barrier; AEC-Q200 testing spans temperature cycling, vibration, and bias-humidity stress over 1,000 hours. Suppliers that clear this hurdle lock in multiyear revenue streams, whereas consumer-focused vendors chase volume at lower margins. Specialized alloy core producers, often based in Japan or Taiwan, secure high-end share by selling powders to multiple winding houses, blurring traditional supply-chain boundaries.

Metal Composite Power Inductor Industry Leaders

TDK Corporation

Murata Manufacturing Co., Ltd.

Vishay Intertechnology, Inc.

TAIYO YUDEN Co., Ltd.

Bourns, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: TDK released power-over-coax inductors rated to 1600 mA for ADAS cameras.

- May 2025: Kitagawa rolled out new EMI shielding sheets tailored for power electronics.

- April 2025: TDK debuted 10 µF, 100 V MLCCs in 3225 case, complementing its inductor suite for 48 V EV subsystems.

- March 2025: Bel Fuse closed the USD 320 million Enercon deal, doubling its magnetic-component revenue base.

Global Metal Composite Power Inductor Market Report Scope

| Below 10 A |

| 10 – 50 A |

| 50 – 100 A |

| Above 100 A |

| Shielded |

| Unshielded |

| Iron Powder Core |

| Ferrite Core |

| Alloy Core |

| Surface Mount |

| Through-Hole |

| Consumer Electronics |

| Aerospace and Defense |

| Industrial |

| Healthcare |

| Automotive |

| Other End Users |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Power Rating | Below 10 A | ||

| 10 – 50 A | |||

| 50 – 100 A | |||

| Above 100 A | |||

| By Shielding Type | Shielded | ||

| Unshielded | |||

| By Core Material | Iron Powder Core | ||

| Ferrite Core | |||

| Alloy Core | |||

| By Mounting Type | Surface Mount | ||

| Through-Hole | |||

| By End User | Consumer Electronics | ||

| Aerospace and Defense | |||

| Industrial | |||

| Healthcare | |||

| Automotive | |||

| Other End Users | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the Metal Composite Power Inductor market in 2025?

It stands at USD 1.99 billion and is forecast to reach USD 2.85 billion by 2030.

Which region leads demand?

Asia-Pacific holds 57.92% of 2024 revenue and grows fastest at a 7.98% CAGR.

Which segment grows quickest by power rating?

The Above 100 A band rises at 7.56% CAGR thanks to fast-charge and storage uses.

Why are shielded inductors gaining share?

Stricter EMC rules make integrated shielding cost-effective versus discrete filters.

What is the key raw-material risk?

High-purity iron and amorphous alloy price swings cut manufacturer margins.

Who are the market leaders?

TDK, Murata, and Vishay dominate through scale production and broad portfolios.

Page last updated on: