Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

High Frequency Circuit Inductors Market is Segmented by Product Type (Core-/Wire-Wound Inductors, Multilayer Stacked Inductors, and More), Core Material (Ferrite, Iron Powder, and More), Mounting Technology (Surface-Mount Device, and More), Frequency Range (HF (3-30 MHz), and More), End-User Industry (Automotive, and More), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

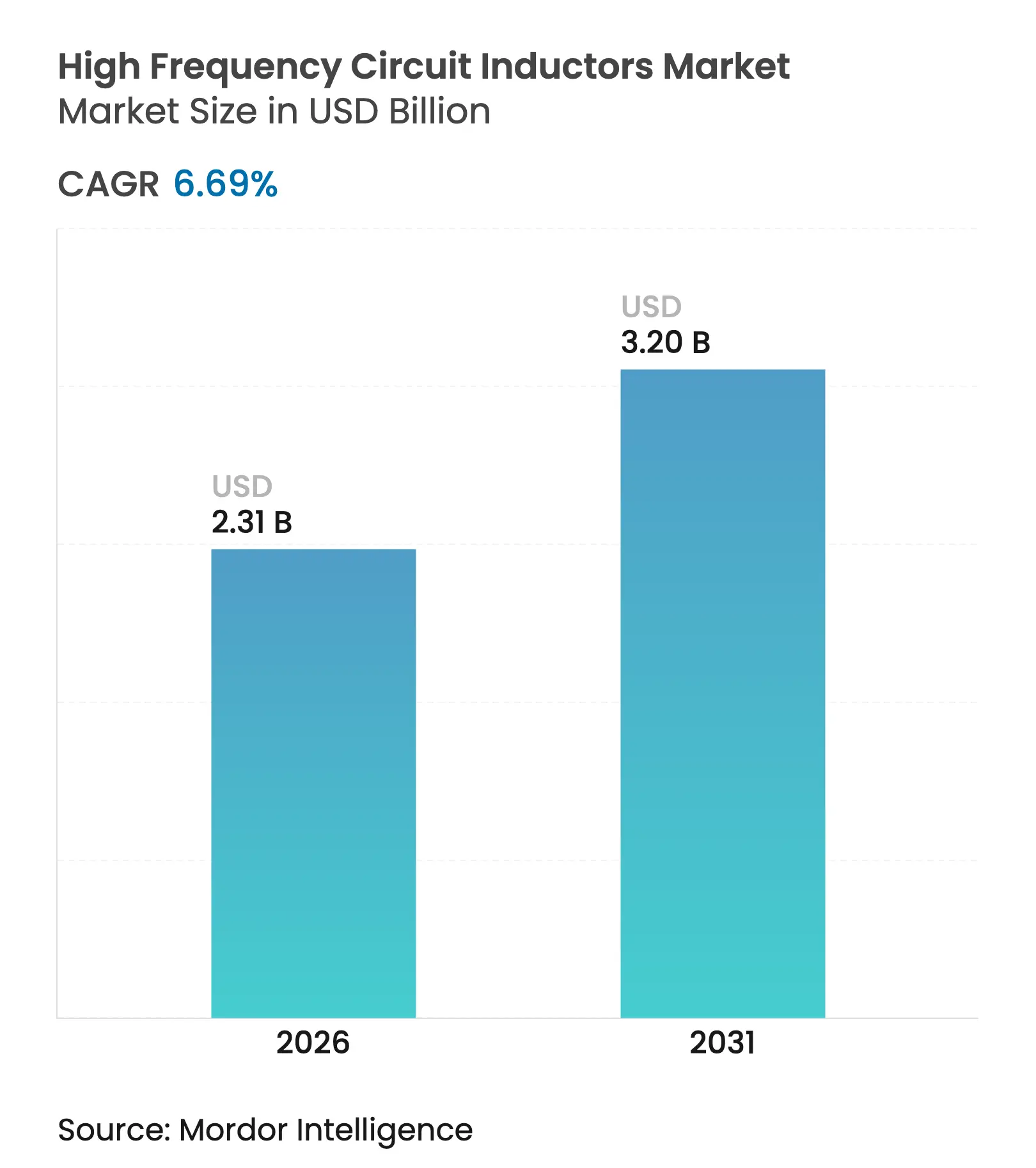

| Market Size (2026) | USD 2.31 Billion |

| Market Size (2031) | USD 3.2 Billion |

| Growth Rate (2026 - 2031) | 6.69 % CAGR |

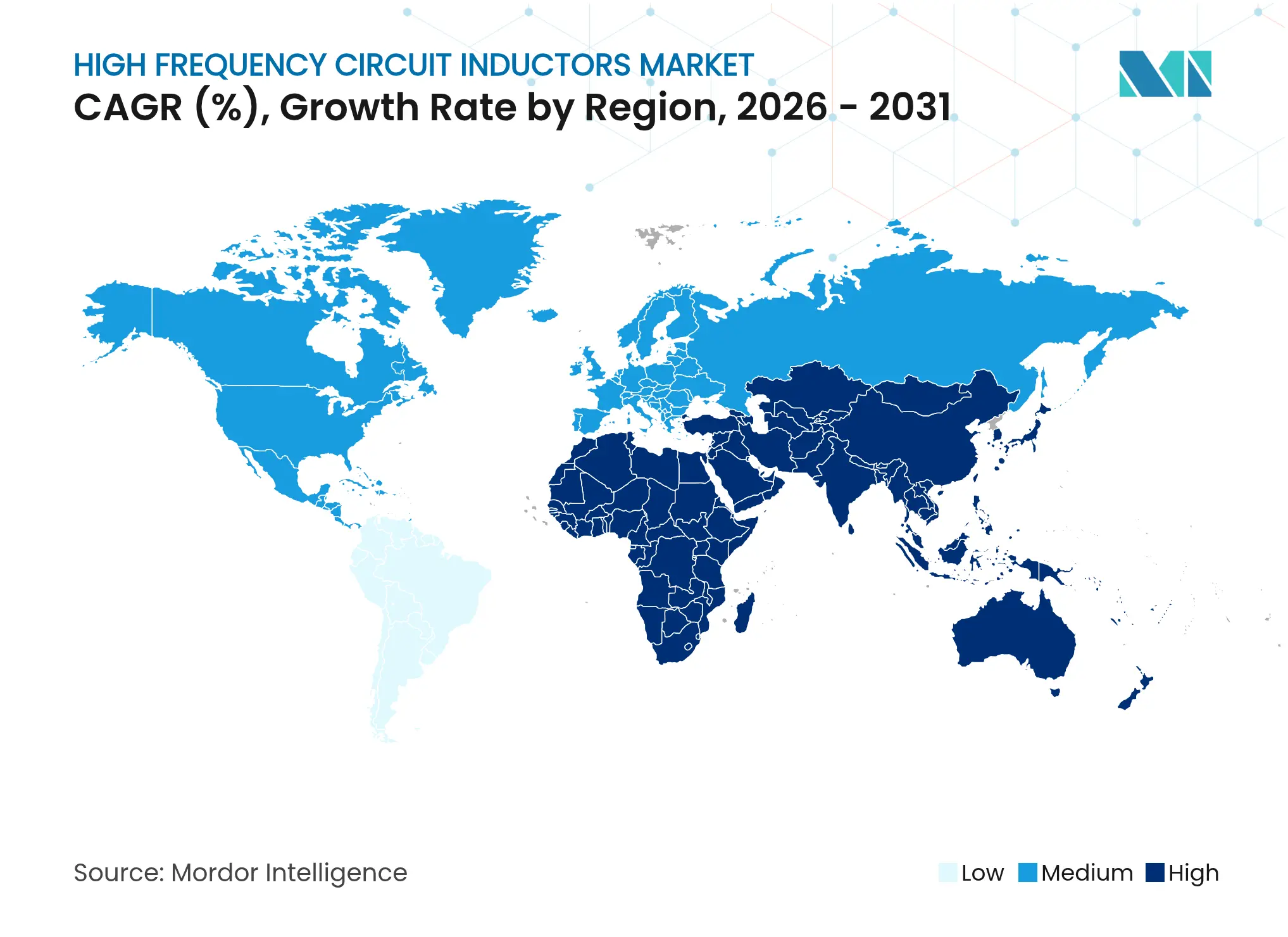

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

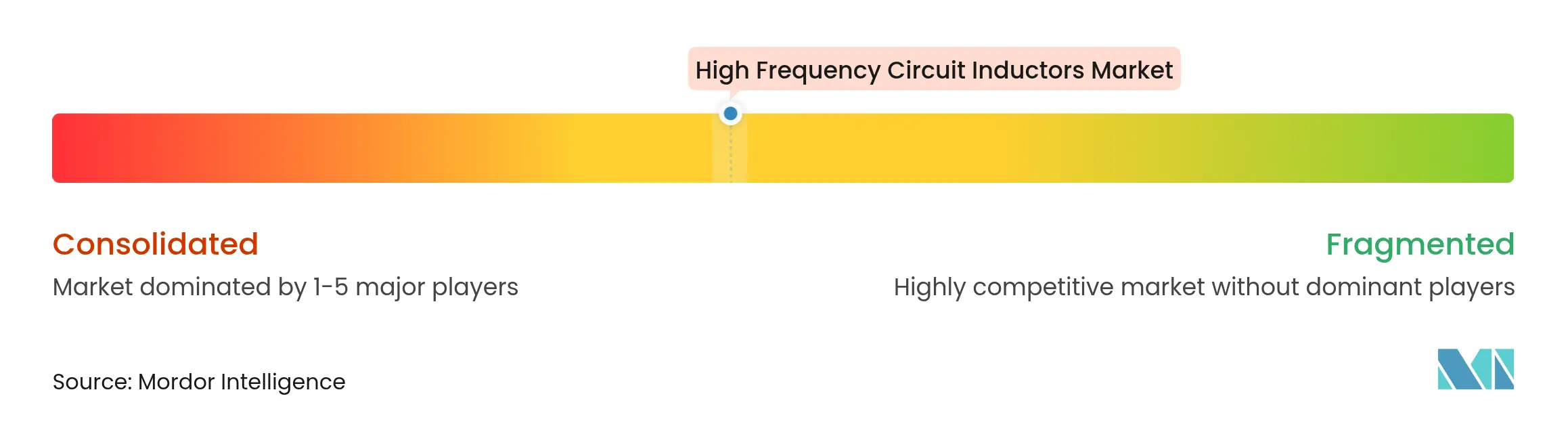

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The high-frequency circuit inductors market size was valued at USD 2.17 billion in 2025 and estimated to grow from USD 2.31 billion in 2026 to reach USD 3.2 billion by 2031, at a CAGR of 6.69% during the forecast period (2026-2031). Rising adoption of wide-bandgap semiconductors has pushed switching frequencies higher, which, in turn, has increased demand for compact inductors that minimize core losses. Multilayer-stacked technologies dominated because they balanced performance, cost, and automated assembly needs. Nanocrystalline cores gained traction as designers sought higher saturation flux densities and lower losses at 500 kHz and above. Asia-Pacific remained the production and consumption hub, while automotive electrification emerged as the single fastest growth vector, lifting value share for vehicular power-train magnetics. Supply chain risks around ferrite powders, however, encouraged substitution with alternative core chemistries and accelerated factory automation. Consequently, the high-frequency circuit inductors market continued to reward suppliers that combined material science breakthroughs with flexible, yield-oriented manufacturing investments.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

5G / mmWave roll-out accelerating ultra-miniature RF

inductor demand

5G / mmWave roll-out accelerating ultra-miniature RF

inductor demand

| +2.5% | Global, notably North America, East Asia, Western Europe | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+2.5%

|

Geographic Relevance

:

Global, notably North America, East Asia, Western Europe

|

Impact Timeline

:

Medium term (2-4 years)

|

EV power-train DC-DC converters driving high-frequency

magnetics

EV power-train DC-DC converters driving high-frequency

magnetics

| +1.8% | North America, Europe, China, Japan | Medium term (2-4 years) | |||

Wearables and IoT miniaturization requiring chip-level

high-Q inductors

Wearables and IoT miniaturization requiring chip-level

high-Q inductors

| +1.2% | Global, early adoption in North America, East Asia | Short term (≤2 years) | |||

Wide-bandgap (GaN/SiC) adoption raising

switching-frequency ceiling

Wide-bandgap (GaN/SiC) adoption raising

switching-frequency ceiling

| +0.9% | North America, Europe, Japan, South Korea | Medium term (2-4 years) | |||

Radar and sat-com modernization boosting UHF/SHF inductor

consumption

Radar and sat-com modernization boosting UHF/SHF inductor

consumption

| +0.6% | North America, Europe, China | Long term (≥4 years) | |||

| Source: Mordor Intelligence | ||||||

5G / mmWave Roll-out Accelerating Ultra-Miniature RF Inductor Demand

Millimeter-wave 5G base stations require inductors with Q-factors 40% higher than 4G radios to retain signal integrity at 24–100 GHz. Thin-film air-core devices with self-resonant frequencies above 20 GHz became the default in radio front-end modules. Murata expanded multilayer liquid-crystal-polymer lines to address this niche, focusing on smaller footprints and automated optical inspection yields.[1]Murata Manufacturing, “High Frequency Devices and Communications Modules,” murata.com South Korea’s densification phase confirmed volume pull-through, as each 64-T/R antenna panel integrated more than 120 high-frequency inductors.

EV Power-Train DC-DC Converters Driving High-Frequency Magnetic Components

Electric-vehicle power stages migrated toward 500 kHz and beyond to shrink magnetics and boost efficiency. Tesla’s Model S Plaid DC-DC modules used 10 kHz inductors, trimming magnetic mass 15% while exceeding 95% efficiency. GaN traction inverters operating from 800 V batteries cut power loss 25% versus SiC, pushing inductor designs toward lower core losses and tighter stray-field control.

Wearables and IoT Miniaturization Requiring Chip-Level High-Q Inductors

Smartwatches, fitness bands, and hearables demanded sub-0201 inductors with Q values above 60 at 2.4 GHz. These parts had to survive high pick-and-place forces and reflow cycles without cracking. Rapid gains in multilayer electrode metallurgy raised current limits by 35% in the same package envelope. Early volume shipments clustered in North American and East-Asian branded devices, validating demand elasticity for ultra-miniature passives.

Wide-Bandgap (GaN/SiC) Adoption Raising Switching-Frequency Ceiling

GaN switches displayed lower switching energy than SiC below 10 kW, enabling MHz-class converters. The U.S. Department of Energy projected GaN power-device unit growth at a 75% CAGR through 2030, catalyzing inductor redesign for MHz operations. Designers gravitated toward nanocrystalline tape-wound cores that offered 30% lower losses than ferrite at 1 MHz.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Ferrite powder price volatility pressuring margins

Ferrite powder price volatility pressuring margins

| −1.2% | Global, acute in Asia-Pacific | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

−1.2%

|

Geographic Relevance

:

Global, acute in Asia-Pacific

|

Impact Timeline

:

Medium term (2-4 years)

|

Yield losses in ≤0201-size SMD lines raising production

costs

Yield losses in ≤0201-size SMD lines raising production

costs

| −0.8% | Asia-Pacific, notably Taiwan, Japan, South Korea | Short term (≤2 years) | |||

EMI/EMC regulations pushing designers toward alternative

filtering topologies

EMI/EMC regulations pushing designers toward alternative

filtering topologies

| −0.5% | Europe, North America, Japan | Medium term (2-4 years) | |||

Lengthening automotive PPAP cycles delaying revenue

realization

Lengthening automotive PPAP cycles delaying revenue

realization

| −0.3% | Global automotive supply chain | Short term (≤2 years) | |||

| Source: Mordor Intelligence | ||||||

Ferrite Powder Price Volatility Pressuring Margins

Ferrite spot prices fluctuated 25–30% in 2024 after geopolitical tensions disrupted Asian ore flows. Manufacturers whose bill of materials was 40% ferrite by value faced direct margin compression, prompting substitution with nanocrystalline powders and more procurement hedging. Acme Electronics confirmed a 22% sales-volume drop in ferrite cores and posted a USD 6.6 million net loss in 2023.[2]Acme Electronics, “Annual Report for the Year Ended December 31, 2023,” acme-ferrite.com.tw

Yield Losses in ≤0201-Size SMD Lines Raising Production Costs

Ultra-miniature production lines reported scrap rates near 8% in 2024 because of micro-cracking and electrode delamination. Each one-point yield loss added roughly USD 0.03 to the per-unit cost in consumer-device volumes. Leading Japanese and Taiwanese fabs accelerated optical-metrology upgrades and reel-to-reel defect mapping to recapture profitability.

By Product Type: Multilayer Stacked Inductors Sustain Leadership

Multilayer stacked devices captured 38.62% of the high-frequency circuit inductors market share in 2025, reflecting their mature ceramic-lamination economics and GHz-grade Q-factors. Vendors increased electrode conductivity and layer-to-layer alignment precision, lifting current ratings 40% within unchanged footprints. High-density smartphones, true-wireless stereo earphones, and VR headsets continued to anchor demand. Thin-film inductors, while only 12.15% of the 2025 volume, advanced at a 12.1% CAGR on the back of 5G phased-array modules that needed 20 GHz resonance margins.

Wire-wound formats retained relevance wherever peak currents topped 3 A, notably in notebook computing VRMs and 48 V industrial DC-DC stages. Planar etched spirals addressed aerospace radars that prized controlled inductance tolerances at 10–18 GHz. Air-core spirals remained indispensable above 30 GHz, where magnetic cores suffered serious loss spikes. Across all formats, the high-frequency circuit inductors market reiterated that form-factor innovation goes hand-in-hand with assembly-line yield engineering, as even minor electrode burrs can halve Q in the millimeter-wave band.

By Core Material: Nanocrystalline Alloys Accelerate Penetration

Ferrite still delivered 43.75% of 2025 revenue because it offered the lowest cost-per-millihenry. Yet, nanocrystalline ribbons advanced at a 12.6% CAGR, supported by studies that showed 50–80% volume reduction when filtering 100 kHz–100 MHz common-mode noise. Induction cooktops, wireless-power pads, and EV chargers embraced these alloys to unlock higher power densities.

Iron-powder cores, valued for distributed-gap behavior, stayed entrenched in cost-sensitive LED drivers. Ceramic and air cores served microwave and mmWave downstream bands where hysteresis must be virtually zero. As GaN drove switching frequencies upward, core-loss slopes favored nanocrystalline even more, reinforcing structural tailwinds for the material segment inside the broader high-frequency circuit inductors market.

By Mounting Technology: Embedded IPD Designs Gain Ground

Surface-mount devices accounted for 77.92% of 2025 shipments, underscoring SMT’s line-beat cost advantage. Vendors supplemented base metals with high-temperature insulation to survive lead-free reflow. However, embedded and IPD formats expanded at a 14.7% CAGR because they shaved parasitic inductance and delivered superior electromagnetic compatibility inside RF modules. Self-rolled-up membrane coils hit 40–53 GHz resonance, offering substrate-integrated alternatives for future 6G arrays.

Through-hole products, though declining in relative share, persisted in telecom rectifiers where 5–10 A continuous currents and airflow cooling dictated tall structures. The ongoing pivot toward substrate-level passives signals that the high-frequency circuit inductors market will see growing overlap with advanced packaging ecosystems as system-in-package architectures proliferate.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By Frequency Range: EHF Momentum Builds

The SHF band (1–30 GHz) supplied 44.65% of revenue in 2025, thanks to 5G new-radio deployments and 77 GHz automotive radars. Component designers optimized Q-factor flatness across 2–18 GHz so that a single inductor code could span multiple radio variants. EHF applications (>30 GHz) soared at an 17.4% CAGR, tied to exploratory 6G links beyond 100 GHz and satellite back-haul modems.

HF and VHF ranges maintained stable utility in industrial converters, induction heating, and long-wave communications. UHF inductors found repeat sales in smart-meter rollouts and asset-tracking beacons. Across every band, the high-frequency circuit inductors market illustrated a direct correlation between frequency climb and demand for air-core or low-loss ceramic solutions.

By End-User Industry: Automotive Outsprints the Pack

Consumer electronics retained 30.98% of 2025 billings, reflecting the sheer shipment scale of phones and wearables. Nonetheless, automotive demand climbed at a 12.7% CAGR, powered by battery electric-vehicle penetration, ADAS feature proliferation, and zonal-architecture transitions. Each premium EV now integrates more than 200 high-frequency inductors in traction inverters, on-board chargers, domain controllers, and sensor fusion modules.

Aerospace and defense, while niche, delivered outsized ASPs because of extended-temperature and radiation-hardening requirements. Telecom infrastructure continued to absorb SHF-grade parts for massive-MIMO radios and coherent optical line cards. Industrial and IoT nodes broadened the customer base as factory-automation vendors embedded sub-GHz and 2.4 GHz radios into motor drives. Taken together, these patterns underpin a diversified high-frequency circuit inductors market that taps both volume consumer cycles and high-specification professional verticals.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

Asia-Pacific supplied 54.78% of 2025 shipments, with Japan, South Korea, Taiwan, and mainland China anchoring multilayer and thin-film capacity. Strong local ecosystems for MLCCs, sensors, and assembly services enabled cost leadership and rapid scale-up. Government incentives in China’s Guangdong and Jiangsu provinces further encouraged fab expansions, fortifying the region’s grip on the high-frequency circuit inductors market.

North America ranked second by value, underpinned by aerospace, defense, and data-center investments. The CHIPS Act steered USD 52 billion to domestic wafer fabs, indirectly reinforcing local passive-component demand as integrated-device manufacturers sought regionalized supply chains. Europe retained a technology-driven share through German automotive Tier-1s and French satellite integrators that mandated stringent EMC compliance.

The Middle East and Africa posted the fastest CAGR at 13.6% from a modest base. Gulf smart-city blueprints required millions of sensor nodes, each embedding several high-frequency inductors. Sub-Saharan solar micro-grids also pulled in DC-DC magnetics for power electronics. South America, led by Brazil, advanced gradually as local content rules in automotive and telecom stimulated regional assembly. Across all zones, the high-frequency circuit inductors industry faced a common challenge: balancing competitive landed cost with resilience against geopolitical shocks.

Market Concentration

The sector displayed moderate concentration; the top five vendors acquired the majority of 2024 sales. TDK, Murata, and Taiyo Yuden enjoyed vertically integrated powder-processing and ceramic-tape assets, enabling quicker material pivots. R&D outlays prioritized nanocrystalline metallurgies, sub-0201 stacking accuracy, and real-time X-ray inspection. Murata projected fiscal-2025 revenue of JPY 1.75 trillion (USD 11.7 billion) on a JPY 261.14 billion (USD 1.75 billion) profit, underscoring solid execution despite raw-material turbulence.[4]Eulerpool, “Murata Manufacturing Co. Stock,” eulerpool.com

Strategic alliances proliferated. Integrated-passive-device specialists partnered with substrate makers to embed coils in glass and organic packages, eroding the addressable market for discrete SMD inductors. Japanese incumbents licensed winding recipes to automotive Tier-1s to secure design-in positions during PPAP cycles. Meanwhile, Taiwanese and Chinese challengers narrowed technology gaps and leveraged cost advantages to penetrate mid-range smartphones, intensifying pricing pressure in commoditized codes.

Future competition will likely hinge on mastering hybrid assembly—combining lithography-defined micromagnetic with traditional wire-winding—to serve multiband 6G radios and 48 V boardnet converters. In that environment, the high-frequency circuit inductors market will reward firms that can orchestrate global powder sourcing, automated vision analytics, and co-design platforms linking system architects with magnetic-model libraries.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

High-frequency circuit inductors typically exhibit increased resistance and reduced current ratings, making them appropriate for high-frequency circuits operating within the range of 10 MHz to several GHz.

The study tracks the revenue accrued through the sale of high frequency circuit inductors by various players in the global market. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

The High Frequency Circuit Inductors Market Report is segmented by type (core wound inductors, multilayer stacked inductors, planar etched inductors, and other types), by end user industry (automotive, aerospace & defense, power systems, communications, consumer electronics and computing, and other end-user industries), and by geography (North America, Europe, Asia Pacific, and Rest of the World). The report offers values terms in USD for the above mentioned segments.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

US Market Entry for Taiwanese Machine Tool Manufacturers

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.