MEMS Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

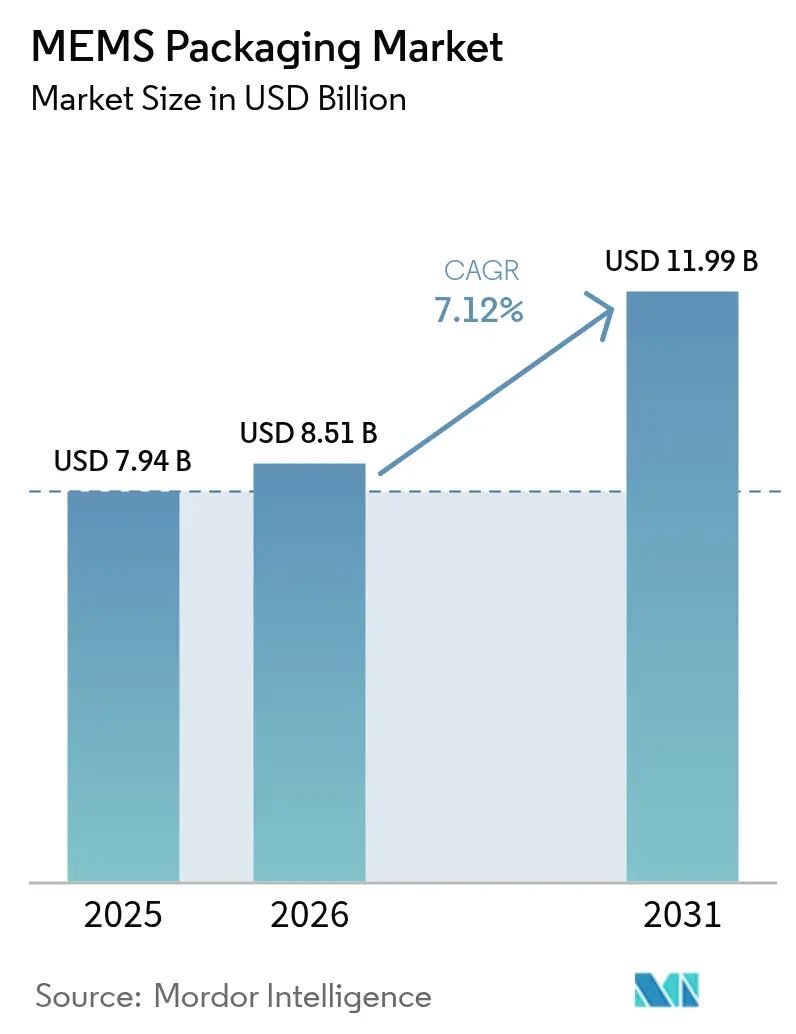

| Market Size (2026) | USD 8.51 Billion |

| Market Size (2031) | USD 11.99 Billion |

| Growth Rate (2026 - 2031) | 7.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

MEMS Packaging Market Analysis by Mordor Intelligence

MEMS packaging market size in 2026 is estimated at USD 8.51 billion, growing from 2025 value of USD 7.94 billion with 2031 projections showing USD 11.99 billion, growing at 7.12% CAGR over 2026-2031. This expansion reflects the structural shift from cloud-centric data processing to edge intelligence, where latency-sensitive automotive safety features, on-device AI in smartphones, and hermetically sealed implantable monitors require sub-micron packaging tolerances. Growth is therefore driven less by unit volume and more by the complexity of co-packaging heterogeneous die such as MEMS accelerometers with ASIC signal processors or CMUT ultrasound arrays bonded to CMOS readout chips within footprints that automobile Tier-1 suppliers and phone OEMs now specify in single-digit millimeter dimensions. Asia Pacific leads adoption as 12-inch foundries ramp, while public subsidies in North America and Europe de-risk advanced-packaging investments. On the materials side, glass and ceramic substrates are gaining favor because they match silicon’s thermal expansion and sustain hermetic seals needed for RF MEMS and implantable medical devices.

Key Report Takeaways

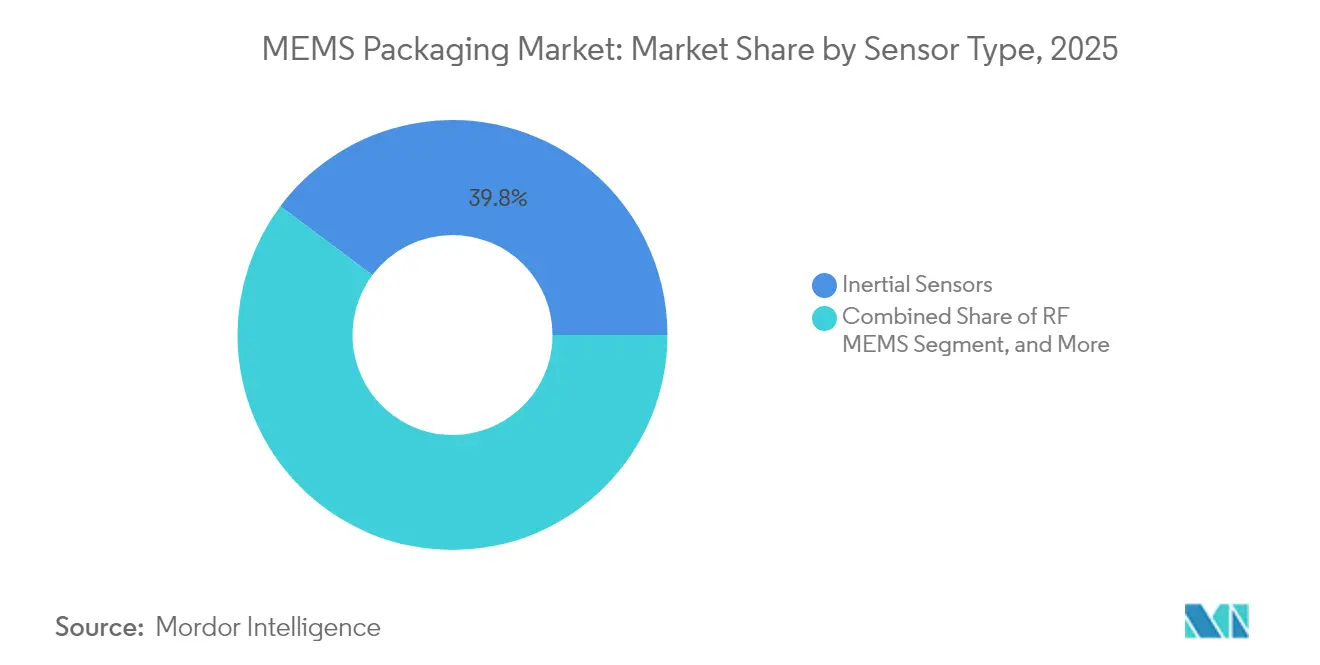

- By sensor type, inertial sensors led with 39.78% of 2025 revenue, while RF MEMS is forecast to grow at an 8.05% CAGR through 2031.

- By packaging platform, wafer-level chip-scale packages captured 44.25% revenue in 2025, and System-in-Package is advancing at a 9.22% CAGR to 2031.

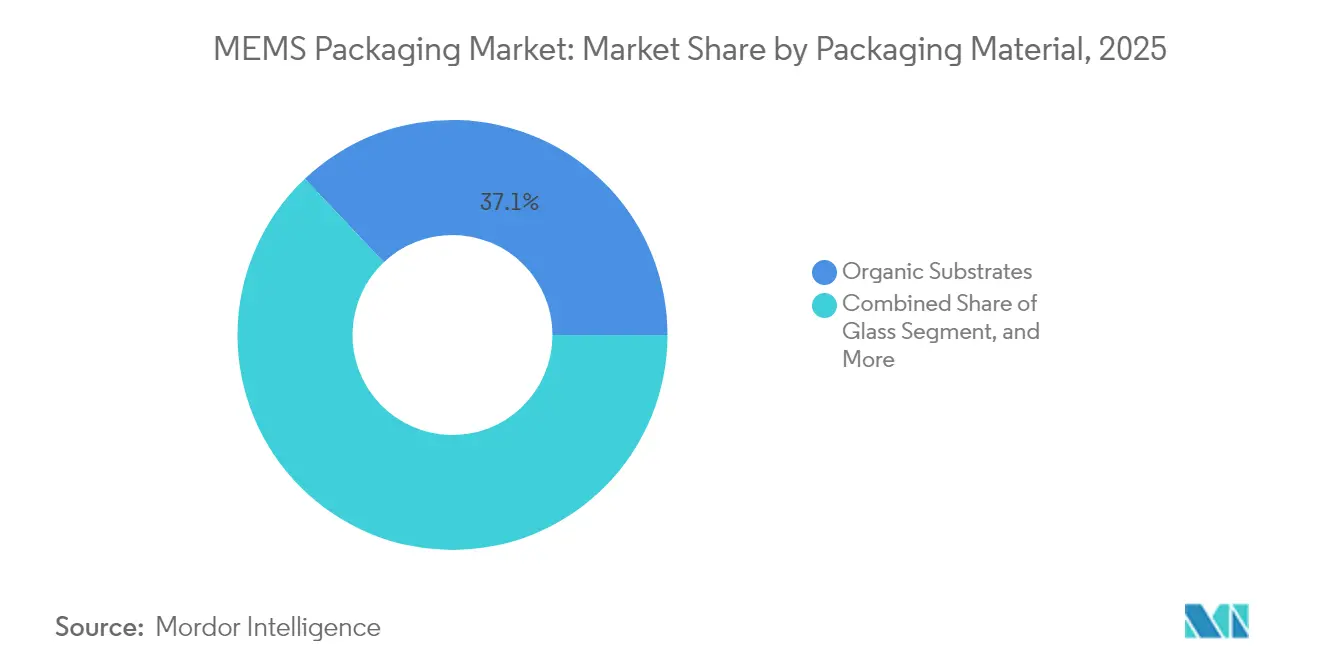

- By packaging material: organic substrates lead, glass substrates surge, and organic laminates captured 37.05% of 2025 revenue due to low material cost and compatibility with flip-chip flows. glass substrates are forecast to grow 10.3% through 2031.

- By geography, Asia Pacific commanded 47.30% of 2025 revenue; North America records the fastest projected CAGR at 9.78% through 2031.

- By end user, mobile phones held a 34.65% share in 2025, whereas medical systems are expanding at an 8.32% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global MEMS Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Smart Automotive Market | +1.8% | Global, early adoption in North America, Europe, China | Medium term (2-4 years) |

| Increasing Smartphone Adoption and Connected Devices | +1.5% | Asia Pacific core, spill-over to Middle East and Africa | Short term (≤ 2 years) |

| Expanding Sensor Usage in Industrial Automation | +1.2% | Europe and North America, expanding to Asia Pacific | Medium term (2-4 years) |

| Demand for IoT-Enabled Consumer Electronics | +1.0% | Global, led by Asia Pacific manufacturing hubs | Short term (≤ 2 years) |

| Adoption of Heterogeneous Integration in MEMS to Reduce Footprint | +1.3% | Global, concentrated in Taiwan, South Korea, United States | Long term (≥ 4 years) |

| Rise of MEMS in Implantable Medical Devices Requiring Hermetic Vacuum Packaging | +0.9% | North America and Europe, emerging Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Smart Automotive Market

Automotive OEMs are embedding multi-axis inertial units, pressure sensors, and optical stabilization modules that must meet AEC-Q100 Grade 1 from −40 °C to +125 °C. Bosch introduced the BHI385 sensor in 2024, an integrated 6-axis IMU with on-chip AI that enables predictive vehicle-dynamics analysis.[1]Robert Bosch GmbH, “BHI385 Smart Connected Sensor,” bosch.com Murata expanded Finnish and Japanese lines to supply hermetically sealed accelerometers that survive chassis vibration. Automakers now specify sensor fusion at the package level, pushing System-in-Package modules combining gyroscopes, magnetometers, and pressure sensors into zone-controller PCBs. Infineon’s XENSIV and STMicroelectronics’ LIS2DU12 families illustrate this shift toward pre-calibrated modules. Qorvo’s 77 GHz radar modules integrate MEMS-based phase shifters to enable 4D imaging in premium sedans. As vehicle platforms move to centralized compute, packaging suppliers that deliver edge-ready, automotive-qualified MEMS assemblies are capturing design wins that elevate the MEMS packaging market.

Adoption of Heterogeneous Integration in MEMS to Reduce Footprint

Smartphone and wearable designers demand sub-5 mm² sensor modules. The IEEE International Roadmap projects flip-chip bumps shrinking to 10-20 µm by 2030, enabling MEMS die to be hybrid-bonded directly onto CMOS readouts. STMicroelectronics has committed new back-end capex in Calamba, Kirkop, Shenzhen, and Muar to scale this capability. Fraunhofer ENAS demonstrated silicon-to-glass bonding with 5 µm pitches, validating process paths to sub-1 µm interconnects for next-gen RF MEMS. U.S. federal strategy now channels USD 3 billion into advanced packaging, focusing on 3D stacking and chiplet ecosystems that trim latency and power for edge AI. Intel’s work on glass-core substrates and SCHOTT’s hermetic glass solutions both aim to resolve thermal-mismatch fatigue between silicon die and organic laminates. Collectively, these advances compress form factors and fuel long-run growth for the MEMS packaging market.

Expanding Sensor Usage in Industrial Automation

Industry 4.0 programs rely on MEMS accelerometers, gyroscopes, and environmental sensors for predictive maintenance. The IEC’s smart-sensing guidelines stress on-chip diagnostics, driving demand for System-in-Package MEMS nodes that include analog front-ends, DSPs, and wireless radios in single hermetic housings. NAMUR guidelines released in 2024 echo this push toward self-calibrating sensors that minimize downtime. Bosch and STMicroelectronics launched accelerometers with ATEX-rated ceramic packages for explosive atmospheres. TDK’s AXO314 digital accelerometer reached volume production in 2024, packaged in a hermetic ceramic J-LEAD housing and targeting industrial navigation. Rising brownfield retrofits create packaging challenges around energy harvesting and RF transparency, reinforcing long-term demand in the MEMS packaging market.

Rise of MEMS in Implantable Medical Devices Requiring Hermetic Vacuum Packaging

Implantable devices increasingly integrate MEMS pressure sensors, accelerometers, and CMUT ultrasound arrays. Infineon introduced CMUT technology co-packaged with CMOS readouts in glass or ceramic housings to block moisture ingress. Fraunhofer ENAS validated parylene encapsulation with leak rates below 10⁻⁷ mbar·ℓ/s, meeting ISO 13485 hermeticity targets. Analog Devices’ iSensor family delivers factory-calibrated IMUs in ceramic and wafer-level housings for pacemakers and neurostimulators. The FDA’s 510(k) requirements simulate 10 years of in-vivo exposure, encouraging glass-frit sealing and reactive bonding. Flexible hybrid electronics blend stretchable polymers with MEMS, necessitating atomic-layer-deposited alumina barriers that open new niches within the broader MEMS packaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex Manufacturing Process | −0.7% | Global, acute where advanced packaging is scarce | Medium term (2-4 years) |

| High Capital Expenditure for Advanced Packaging Lines | −0.9% | Global, affecting new entrants and smaller OSATs | Long term (≥ 4 years) |

| Reliability Challenges in Wafer-Level Vacuum Packaging for RF MEMS | −0.5% | North America, Europe, Asia Pacific centers | Medium term (2-4 years) |

| Supply Chain Bottlenecks for Specialty Low-CTE Packaging Materials | −0.6% | Global, shortages in glass and ceramic carriers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure for Advanced Packaging Lines

A single MEMS packaging line can require more than USD 200 million for bonding, hybrid alignment, PECVD, and advanced inspection gear. Lam Research positions its SABRE, Syndion, and Coronus platforms expressly for these flows. ASE Technology raised 2025 capex by over 60% to expand bumping, flip-chip, and SiP capacity. Amkor’s Peoria, Arizona plant secured USD 400 million in CHIPS Act grants and USD 200 million in loans, underscoring the subsidy scale needed to localize such facilities. Treasury’s 48D tax credit lowers after-tax cost but excludes brownfield upgrades, leaving existing plants to self-fund retrofits. Reliance on a small pool of well-capitalized OSATs extends lead times and moderates growth for the MEMS packaging market.

Supply Chain Bottlenecks for Specialty Low-CTE Packaging Materials

Borosilicate glass wafers, alumina substrates, and kovar lids remain concentrated among a few suppliers. SCHOTT’s capacity additions trail demand, stretching lead times beyond 20 weeks in 2024. LPKF’s laser-etched through-glass vias are still pilot-scale, not yet replacing incumbents. Intel’s data-center glass-core roadmap consumes the same borosilicate feedstock that MEMS packages require, tightening availability. Ceramic substrate providers Kyocera and Murata must pass lengthy reliability screening, limiting throughput. Export controls complicate Chinese expansions, forcing Shenzhen and Suzhou foundries to import glass from Japan and Germany, inflating costs across the MEMS packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sensor Type: Inertial Sensors Anchor Volume, RF MEMS Capture Premium Growth

Inertial sensors accounted for 39.78% of 2025 revenue, underpinning smartphones, wearables, and automotive stability modules that demand high-volume, low-cost wafer-level housings. RF MEMS is forecast to expand at an 8.05% CAGR as 6G roadmaps incorporate MEMS phase shifters and tunable filters into multi-band antenna arrays, a trend lifting the MEMS packaging market size for high-frequency modules. The price premium associated with millimeter-wave hermeticity elevates average selling prices and offsets lower unit counts. Optical MEMS actuators for image stabilization and LiDAR mirrors add incremental share, while environmental sensors and ultrasonic devices broaden industrial and automotive opportunities. A strategic shift is emerging toward System-in-Package assemblies that integrate a 6-axis IMU, pressure sensor, and magnetometer on a single substrate, reducing PCB area by 60% and further expanding the MEMS packaging market.

Smartphone OEMs increasingly order combo-modules rather than discrete dies. Bosch and STMicroelectronics both released wafer-level optical image-stabilization actuators with z-heights below 2.5 mm, illustrating how tight form-factor constraints steer demand toward advanced packaging. Qorvo’s phase-shifter SiP for automotive radar combines power amplifiers and MEMS tuning elements in one cavity, commanding a price premium that lifts MEMS packaging market share in RF front-ends. As integration deepens, package-level test complexity rises, nudging suppliers toward modular SiP architectures that streamline final test and burn-in.

By Packaging Platform: Wafer-Level Dominates, System-in-Package Accelerates

Wafer-level chip-scale packages held 44.25% of 2025 revenue thanks to size-on-die efficiency and cost leadership in wearables and phones. System-in-Package is set to grow 9.22% through 2031 as co-integration of MEMS die, ASICs, passives, and antennas becomes essential for edge-AI and automotive safety. STMicroelectronics’ planned USD 950 million purchase of NXP’s MEMS operations adds SiP know-how and underscores industry appetite for vertically integrated solutions. Flip-chip BGAs maintain relevance in under-hood automotive environments where copper-pillar bumps enable -40 °C to +150 °C performance and bolster MEMS packaging market share in safety-critical modules.

Package-in-Package formats serve telecom infrastructure, stacking MEMS oscillators atop RF amplifiers to trim signal paths. Ceramic packages remain the gold standard for implantables and aerospace; Kyocera and Murata supply gold-plated alumina lids that meet 1,000-hour high-temperature life tests. Fraunhofer ENAS demonstrated glass-frit bonding for CMUT arrays with leak rates below 10⁻⁷ mbar·ℓ/s, signaling future cost reductions once scaled. The bifurcation is clear: consumer electronics prize wafer-level cost efficiency, while medical and automotive markets justify higher SiP and ceramic outlays, collectively expanding the MEMS packaging market size across varied performance tiers.

By Packaging Material: Organic Substrates Lead, Glass Substrates Surge

Organic laminates captured 37.05% of 2025 revenue due to low material cost and compatibility with flip-chip flows. Glass substrates are forecast to grow 10.3% through 2031 as their thermal expansion aligns with silicon and their low dielectric loss improves RF performance, fueling incremental MEMS packaging market growth. Intel’s glass-core adoption in data-center CPUs validates scale potential. LPKF’s laser-induced deep etching reached 50 µm via diameters with 10:1 aspect ratios, enabling vertical routing without wire bonds.

Ceramic substrates dominate implantable and aerospace segments, offering hermetic seals and high-temperature resilience. Kyocera and Murata remain principal suppliers, but competition from glass-based lids is intensifying. Silicon interposers enable 2.5D stacking of MEMS with processors for automotive radar, while Kovar and copper-tungsten alloys serve as lids and heat spreaders. DuPont’s ElectronicsCo spin-off supplies die-attach films and underfills optimized for low-CTE assemblies, strengthening supply-chain depth. Material choice thus maps directly to the target market, reinforcing the stratification of the MEMS packaging market.

By End User Industry: Mobile Phones Dominate, Medical Systems Accelerate

Mobile phones held 34.65% of 2025 demand, driven by multi-axis IMUs, MEMS microphones, and OIS actuators that rely on high-volume wafer-level production. Medical systems are projected to grow 8.32% through 2031 as implantable glucose monitors and neurostimulators demand leak-rate guarantees below 10⁻⁷ mbar·ℓ/s, expanding the MEMS packaging market size for hermetic solutions. Syntiant’s 2024 acquisition of Knowles’ microphone business highlights vertical integration around voice-AI modules for wearables.

Automotive applications span stability control, TPMS, radar, and LiDAR, each adding to MEMS packaging market share for ceramic and SiP solutions. Industrial users adopt closed-loop accelerometers like TDK’s AXO314 for vibration monitoring, increasing demand for ATEX-qualified ceramic packages. Aerospace and defense rely on radiation-hard ceramic packages that survive >10,000 g shock loads. The correlation between end-user reliability needs and package cost defines revenue pools within the broader MEMS packaging market.

Geography Analysis

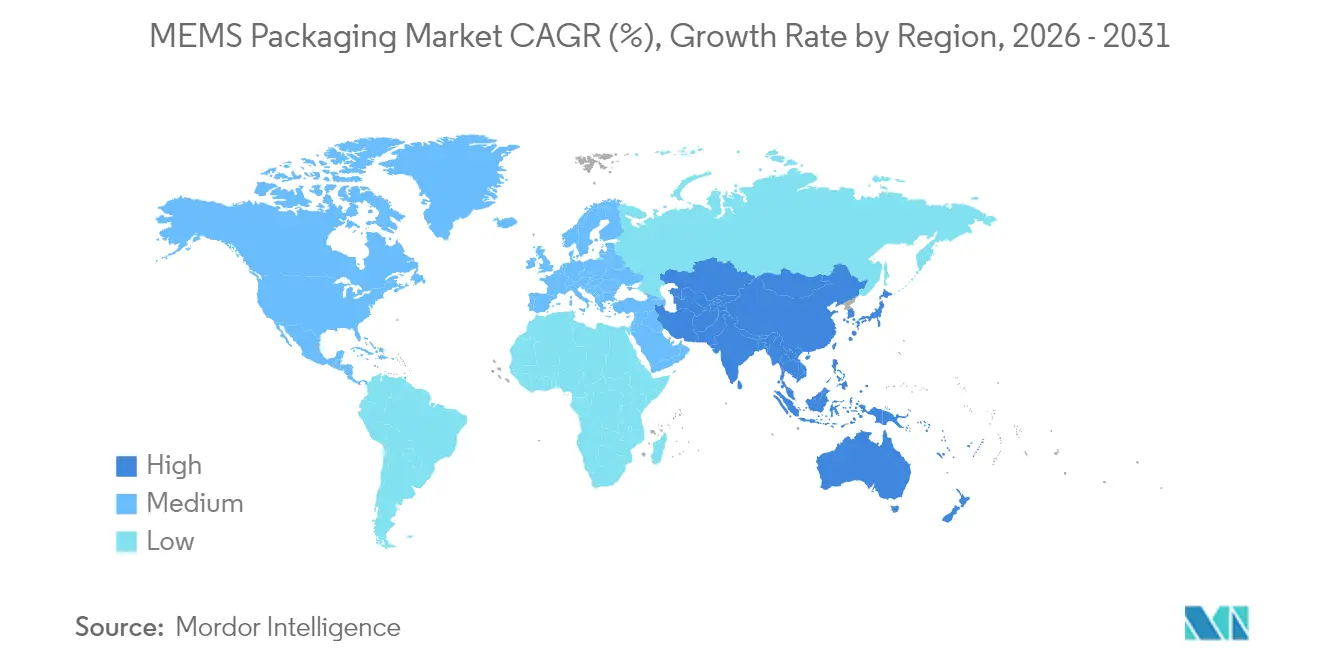

Asia Pacific controlled 47.30% of 2025 revenue and is forecast to grow at 9.78% through 2031 as China ramps 12-inch MEMS foundries and Japan funds the Kyushu cluster. Beijing Silex hit 20,000 wafers per month after a RMB 7 billion investment. Sony earmarked ¥1.5 trillion for CMOS and MEMS packaging lines. South Korea and Taiwan host ASE and Amkor, providing wafer-level and SiP capacity that sustains the MEMS packaging market.

North America’s share is rising as the CHIPS and Science Act channels USD 3 billion into the National Advanced Packaging Manufacturing Program, de-risking hybrid bonding and glass-core flows. Rogue Valley Microdevices will ship 300 mm MEMS wafers from Florida in early 2025, diversifying supply. Europe leverages Bosch, STMicroelectronics, and Infineon leadership but depends on Taiwan OSATs; Amkor’s Porto facility opens in 2025 to localize some capacity. South America and the Middle East, and Africa remain nascent, importing packaged sensors from Asia Pacific and North America. Policy and capacity moves, therefore, redraw regional contributions to the MEMS packaging market. The geographic landscape is bifurcating: Asia Pacific will retain volume leadership through foundry scale and cost competitiveness, while North America and Europe leverage public subsidies and regulatory mandates to build domestic advanced-packaging capacity that reduces supply-chain risk and secures access to automotive and defense applications.

Regulatory Landscape

MEMS packaging suppliers operate under a compliance stack that combines safety and reliability qualification with evolving trade and export-control rules that can affect packaging materials, equipment, and cross-border assembly flows. On the technical side, IEC continues to expand MEMS-specific standards used by qualification teams and customer audits, including IEC 62047-49:2025 (reliability testing methods for piezoelectric MEMS cantilevers) and the generic MEMS specifications covered under IEC 62047-4:2026.

Policy scrutiny increasingly extends to back-end processes and inputs used in advanced packaging. In the United States, trade actions and controls published via the Federal Register and related presidential actions in January 2026 added another layer of import and licensing complexity for semiconductor-related articles defined by technical parameters, reinforcing the need for product-level compliance mapping across packaged sensor modules and their derivative products.

Value Chain Analysis

The MEMS packaging value chain starts with substrate and consumable inputs (organic laminates, ceramics, glass wafers, lids, underfills, and metallization chemicals), then moves to front-end MEMS fabrication at IDMs and foundries, and finally to back-end assembly and test performed by OSATs and captive packaging lines. Core packaging process steps include wafer bonding (including vacuum and hermetic sealing for RF MEMS and implantables), thinning and singulation, interconnect formation (wire bond, flip-chip, TSV/TGV where applicable), encapsulation, and final test that often requires application-specific stimulation (pressure, flow, acoustic, vibration, or IR) with tight metrology.

Value capture and bottlenecks concentrate in process integration and test, where yield loss and reliability screening drive cost and cycle time. Deep reactive ion etching (DRIE), copper plating for TSV-related flows, and wafer-level bonding quality are recurring pinch points, while constrained availability of low-CTE glass and ceramic carriers can stretch lead times. As heterogeneous integration expands (MEMS plus ASICs, passives, and antennas in SiP), the chain increasingly relies on a small set of advanced OSATs (for wafer-level and SiP) alongside IDMs such as Bosch, STMicroelectronics, and Texas Instruments that invest in wafer-scale packaging to control qualification, calibration, and supply assurance.

Competitive Landscape

The MEMS packaging market is moderately fragmented. ASE Technology and Amkor hold significant wafer-level and SiP volume, yet face potential backward integration from Bosch, STMicroelectronics, and TDK, each with captive lines.[3]Amkor Technology Inc., “CHIPS Act Funding for Peoria Plant,” amkor.com STMicroelectronics’ USD 950 million bid for NXP’s MEMS unit underscores the premium on automotive-qualified packaging IP. Emerging disruptors include Syntiant, integrating edge-AI into MEMS audio modules post-acquisition of Knowles, and Rogue Valley Microdevices, building 300 mm capacity in Florida.

Technology differentiation now centers on hybrid bonding, TSVs, and glass-core interposers enabling <5 µm pitches. ASE filed 6,433 patents by 2024, spanning wafer-level MEMS to fan-out Sip. Lam Research supports the ecosystem with SABRE plating and Syndion DRIE systems tailored for MEMS, posting USD 14.9 billion revenue in fiscal year 2024. Ceramic-package incumbents face competition from glass and parylene encapsulation, validated by Fraunhofer ENAS.

Consumer devices still emphasize cost and scale, rewarding OSATs, while automotive and medical clients prize vertical integration that streamlines compliance with AEC-Q100 and ISO 13485, allowing IDMs to command higher margins. This bifurcation informs strategic positioning across the MEMS packaging market.

MEMS Packaging Industry Leaders

AAC Technologies Holdings Inc.

Robert Bosch GmbH

Infineon Technologies AG

Texas Instruments Incorporated

Analog Devices Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Whitespace is forming around localized capacity additions and application-specific advanced packaging modules that reduce dependence on concentrated Asia-based back-end supply. Government-backed programs and grants are actively financing new microsystems and packaging capacity, highlighted by X-FABs Fab4Micro support for its Erfurt site (grant notification of EUR 127.4 million from the German federal government and the Free State of Thuringia in June 2026). At the same time, company actions to add regional manufacturing footprints, including Silex Microsystems' binding agreement in July 2026 to acquire an 8-inch fab in Mountain Top, Pennsylvania, point to efforts to place MEMS production closer to end markets that demand automotive- and medical-grade traceability and shorter qualification loops.

Opportunity also sits in scaling packaging technologies that enable higher integration density and improved thermo-mechanical stability, especially wafer-level bonding, through-glass via approaches, and glass or ceramic-based hermetic solutions used in RF MEMS and implantable devices. Work on MEMS sensor integration through the IEEE Electronics Packaging Society technical roadmap (May 2026) underscores continued industry focus on heterogeneous integration and modular packaging building blocks rather than a single universal standard. Large, adjacent advanced-packaging investments, including SK Hynix's July 2026 plan for a USD 12.85 billion advanced packaging plant in Cheongju with dedicated wafer-level lines, add momentum to equipment and process ecosystems that MEMS packaging providers can leverage for materials readiness, metrology, and high-throughput bonding and inspection.

Recent Industry Developments

- July 2026: Silex Microsystems signed a binding agreement to acquire an 8-inch semiconductor fab in Mountain Top, Pennsylvania, creating its first manufacturing footprint in the United States. The move supports domestic MEMS supply options and can shorten qualification cycles for customers that require tighter control over back-end packaging and traceability.

- August 2025: STMicroelectronics announced the acquisition of NXP Semiconductors MEMS sensor business for USD 950 million. The deal strengthens STMicroelectronics vertical integration around MEMS devices and associated packaging know-how, supporting higher-value System-in-Package and automotive-qualified module roadmaps.

- June 2024: Qorvo unveiled RF multi-chip modules integrating MEMS phase shifters for 4D imaging radar. This product direction raises the packaging requirement for high-frequency, hermetic, and tightly co-integrated RF front-end assemblies, reinforcing demand for advanced SiP and cavity-style packaging capabilities.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the MEMS packaging market covers revenues earned from packaging solutions used to protect and interconnect MEMS devices, including wafer-level and package-level formats that enable electrical, thermal, and mechanical performance in end products.

Scope exclusions: Pure MEMS device revenue, test equipment sales, and outsourced wafer fabrication services are excluded unless they are sold as part of a packaging service or packaged unit price.

Segmentation Overview

- By Sensor Type

- Inertial Sensors

- Optical Sensors

- Environmental Sensors

- Ultrasonic Sensors

- RF MEMS

- Other Sensor Types

- By Packaging Platform

- Wafer-Level Chip-Scale Package (WLCSP)

- System-in-Package (SiP)

- Package-in-Package (PiP)

- Flip-Chip Ball Grid Array (FC-BGA)

- Ceramic Packages

- By Packaging Material

- Organic Substrates

- Ceramics

- Silicon

- Glass

- Metals and Alloys

- By End User Industry

- Automotive

- Mobile Phones

- Consumer Electronics

- Medical Systems

- Industrial

- Other End User Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Kenya

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with building a clear demand-and-supply map for MEMS packaging, so unit drivers and pricing logic stayed separated from MEMS device shipments. Public sources such as USITC trade statistics for electronics and related components were used, UN Comtrade was used to cross-check trade flows, and OECD and World Bank macro indicators helped as electronics output proxies. We also used patent databases to understand where packaging processes and reliability improvements were being emphasized.

To anchor the model in industry signals, we used company annual reports, 10-K style filings, investor presentations, and technical publications from IEEE and similar peer-reviewed venues that discuss wafer-level packaging, hermeticity, and reliability. In a few places, paid subscriptions for company financials and intelligence, news and financials, and patent databases were used to speed up identification of active packaging players and recent capacity moves. These examples are not exhaustive, and many other public and paid sources were also reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary checks were run with packaging engineers, operations leaders, and commercial teams across OSATs, MEMS-focused fabs, and packaging material and substrate suppliers, so our assumptions on package mix and pricing were tested against real programs. We also spoke with demand-side stakeholders in automotive, mobile devices, and industrial sensing to validate adoption timing, qualification cycles, and how packaging choices change when volumes scale across regions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 13% | APAC: 46% |

| Mid tier: 53% | Functional/Unit leaders: 30% | EMEA: 35% |

| Smaller Players: 14% | Managers: 57% | Americas: 19% |

Market-Sizing & Forecasting

Sizing was built with a top-down approach, reconstructing MEMS end-market demand from device shipment signals and converting it into packaging value using package-type mix and typical price bands. Because packaging revenue can shift simply due to format changes, we corroborated the results with selective bottom-up approximations, including supplier roll-ups for sampled programs and channel checks on average selling price by package platform.

Key model inputs included MEMS unit volumes by major sensor families, the share of wafer-level packages versus system-in-package and ceramic formats, typical yields and rework rates that affect effective packaged output, and pricing progression as packaging moves from mature to higher reliability requirements. Regional electronics manufacturing activity and automotive build trends were treated as demand anchors, and packaging material availability was monitored as a practical limiter in tight periods. For forecasting, we used scenario analysis supported by expert consensus on adoption curves, with a base case reflecting expected qualification timelines and capacity additions. When bottom-up visibility was thin, gaps were handled by applying conservative ranges on package mix and then narrowing them through follow-up interview re-contacts.

Data Validation & Update Cycle

Outputs were checked against independent signals such as MEMS shipment direction, packaging platform penetration, and region-level electronics manufacturing momentum, so large jumps could be explained before sign-off. When the model produced unusual mix or price movements, assumptions were reviewed in steps and re-tested with additional expert feedback until the variance became logical.

Each draft went through multi-stage internal reviews, including consistency checks across sensors, end uses, and regions, followed by a final analyst pass right before delivery. The dataset is refreshed annually, and interim updates are triggered when material events occur, such as large capacity expansions, policy-led localization moves, or sharp changes in packaging material constraints.

Mordor Intelligence's Mems Packaging Market Sizing Compared With Other Published Estimates

Published market sizes for MEMS packaging can vary a lot because different teams count different revenue pools and apply different timing for price and mix changes. Differences show up most when wafer-level versus package-level formats are treated inconsistently, or when adjacent services are pulled into the total without being called out.

In this study, the main gap drivers were whether estimates include only packaging revenue versus also counting MEMS device value, how the package platform mix is translated into pricing over time, and whether the base year aligns to the same calendar-year currency assumptions. The spread can also be explained by refresh cadence, since new automotive qualification wins and capacity additions tend to shift package mix in steps rather than smoothly, and the 2026 size is tracked as packaging-only revenue with platform mix checks, a choice applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 8.51 B (2026) | |

| Global Research Publisher A | USD 2.82 B (2024) | Uses an earlier base year and appears to apply a narrower revenue capture, which can undercount higher-value packaging formats and later-stage automotive and industrial volume ramps. |

| Industry Analyst Group B | USD 6.04 B (2025) | Starts from a different base year and does not clearly separate packaging-only revenue from adjacent MEMS value or services, which can shift totals depending on what gets bundled. |

Looking across the three figures, the differences are mainly tied to year alignment and how packaging value is separated from nearby revenue pools, not just growth expectations. By keeping variables like package mix, price bands, and end-market volume anchors visible in the model, our estimate stays traceable and can be re-run when new capacity or qualification signals appear.

Key Questions Answered in the Report

How large is the MEMS packaging market in 2026 and what is its growth rate?

The market stands at USD 8.51 billion in 2026 and is on track to grow at a 7.12% CAGR to 2031.

Which region contributes the most revenue to MEMS packaging?

Asia Pacific accounts for 47.30% of 2025 revenue and is expanding faster than any other region at a 9.78% CAGR.

What packaging platform is gaining momentum beyond wafer-level solutions?

System-in-Package configurations are forecast to expand at a 9.22% CAGR as designers co-package MEMS, ASICs, and passives in compact modules.

Which sensor category is expected to grow fastest?

RF MEMS devices, used in emerging 6G and automotive radar systems, are projected to grow at an 8.05% CAGR through 2031.

What is the main supply-chain bottleneck for MEMS packaging materials?

Limited capacity for borosilicate glass and alumina ceramic substrates, both essential for hermetic sealing, has stretched lead times beyond 20 weeks.

How are public policies influencing MEMS packaging capacity in North America?

The CHIPS and Science Act directs USD 3 billion toward advanced packaging programs, subsidizing hybrid bonding, TSVs, and glass-core interposers to localize production.

Page last updated on: