Operating Room Integration Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

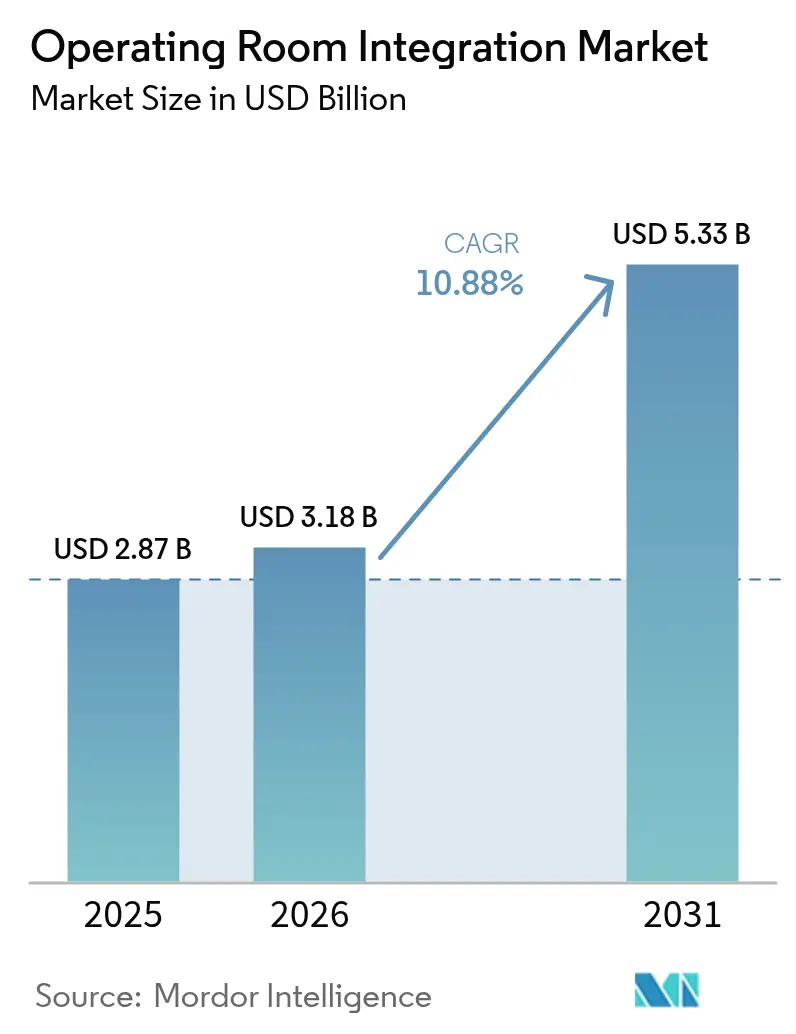

| Market Size (2026) | USD 3.18 Billion |

| Market Size (2031) | USD 5.33 Billion |

| Growth Rate (2026 - 2031) | 10.88% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Operating Room Integration Market Analysis by Mordor Intelligence

The operating room integration market size is expected to grow from USD 2.87 billion in 2025 to USD 3.18 billion in 2026 and is forecast to reach USD 5.33 billion by 2031 at 10.88% CAGR over 2026-2031. The growth reflects hospitals’ shift from isolated device purchases toward fully connected surgical suites that orchestrate imaging, video, robotics, and data analytics in real time.[1]American Hospital Association, “Tackling the Surgical Backlog,” aha.org Fast-tracked recovery plans for elective procedures, rising adoption of minimally invasive surgery, and the push to eliminate avoidable delays in the peri-operative pathway underpin the expansion trajectory. Software platforms now eclipse hardware as the value driver, while hybrid operating rooms gain favor for accommodating complex therapies in a single setting. Simultaneously, Asia-Pacific’s modernization programs position the region as the fastest riser, even as North America maintains the largest installed base. Amid these dynamics, vendors pivot from selling standalone equipment to delivering outcome-oriented digital partnerships that blend software, services, and AI.

Key Report Takeaways

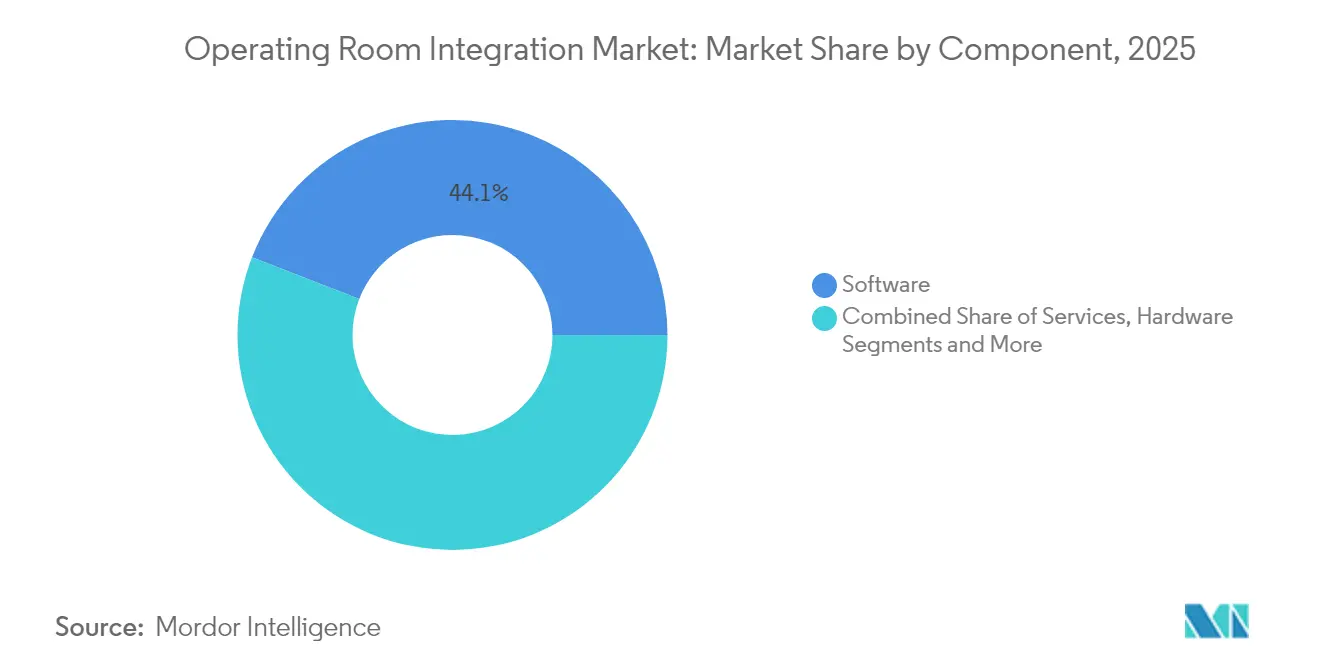

- By component, software solutions led with a 44.12% revenue share in 2025; services are projected to post the highest 14.57% CAGR through 2031.

- By application, general surgery commanded 36.25% of the operating room integration market share in 2025, while neurosurgery is set to advance at a 13.22% CAGR to 2031.

- By end-user, large hospitals held 57.92% share of the operating room integration market size in 2025; ambulatory surgical centers (ASCs) will expand fastest at a 13.98% CAGR.

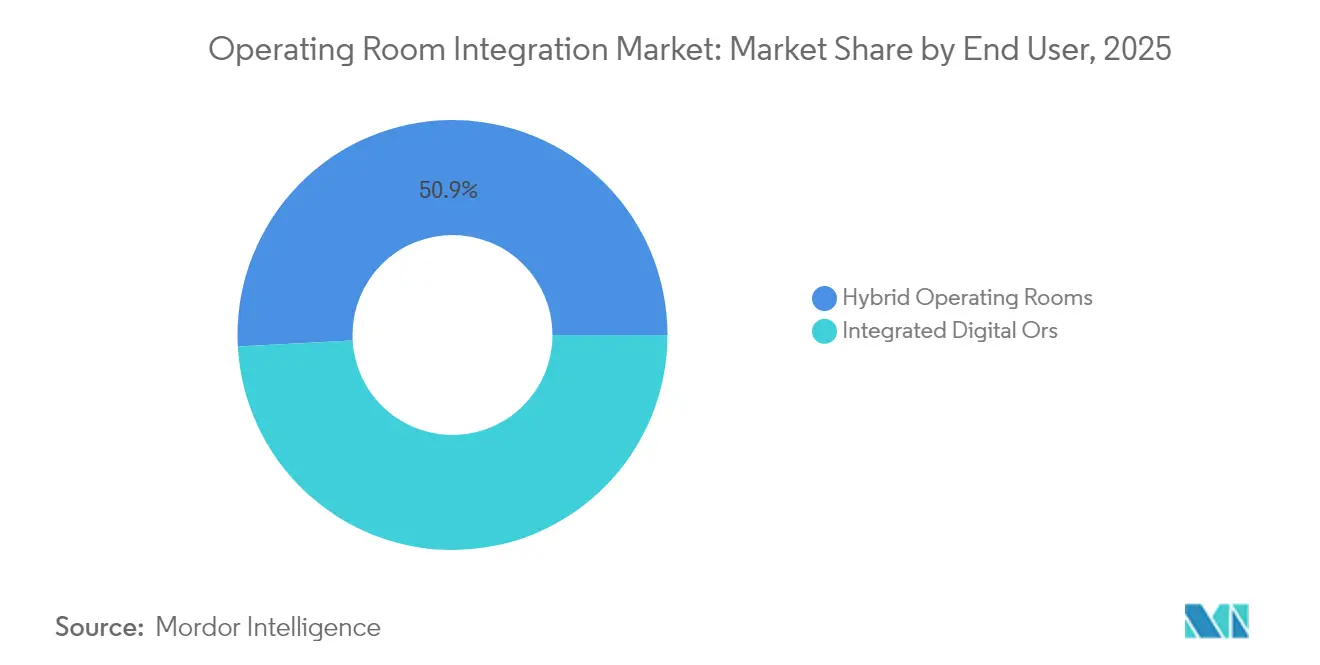

- By OR type, hybrid rooms accounted for 50.86% of 2025 revenue and are poised to grow at a 15.02% CAGR.

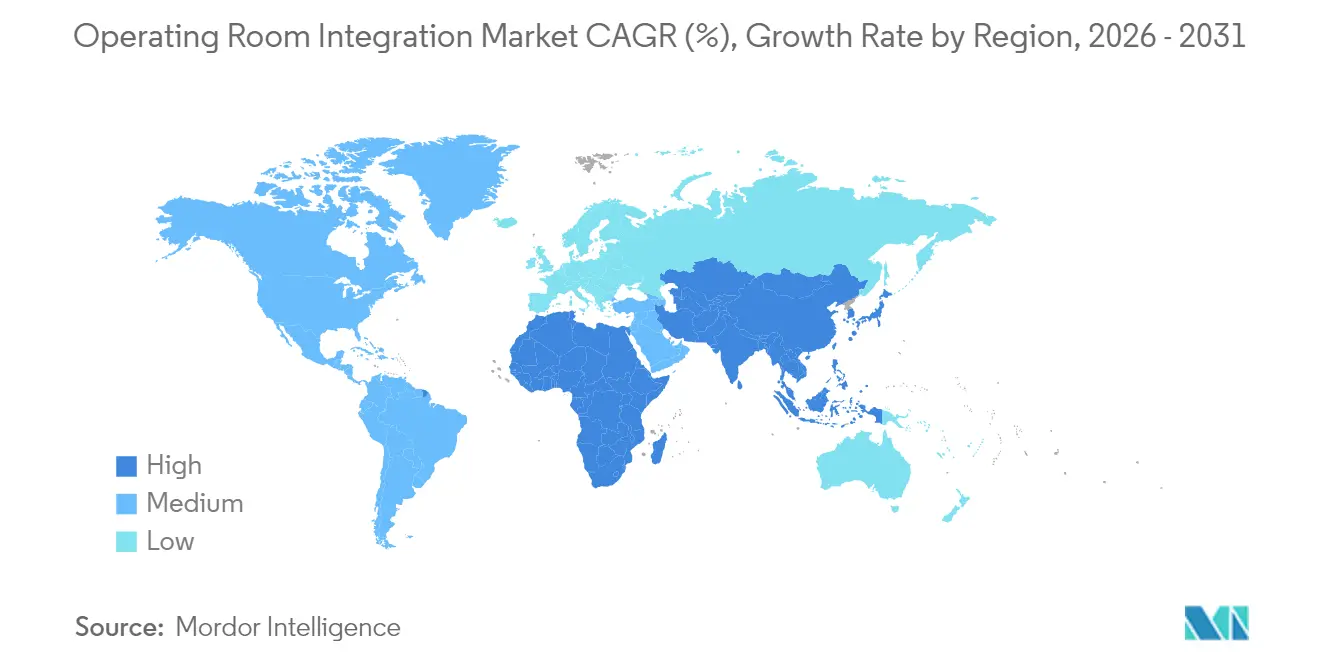

- By geography, North America retained 39.12% market share in 2025; Asia-Pacific is projected to register a 13.94% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Operating Room Integration Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in number of surgical procedures | +2.8% | Global (notably NA & APAC) | Medium term (2-4 years) |

| Uptake of minimally invasive & image-guided surgery | +2.1% | North America & Europe; expanding in APAC | Short term (≤ 2 years) |

| Hospital investments in digital/IoT-enabled ORs | +1.9% | Global; led by North America & Europe | Medium term (2-4 years) |

| Post-pandemic backlog reduction programs | +1.6% | North America & Europe | Short term (≤ 2 years) |

| IP-based 4K/8K video routing for collaboration | +1.4% | Early uptake in developed markets | Long term (≥ 4 years) |

| ESG-driven demand for energy-efficient ORs | +1.0% | Europe & North America; emerging in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rise in Number of Surgical Procedures

Hospitals worldwide are booking fuller operating schedules as aging populations and chronic conditions fuel procedure demand. Integrated workflow software helps teams turn over theatres faster, allocate instruments efficiently, and shorten anesthesia times. The payoff is clearest in robot-assisted cases where platforms such as da Vinci Xi achieve accuracy above 90%, sharply reducing costly revisions and freeing capacity for additional patients.[2]Luthfi Gatam et al., “Robotic Pedicle Screw Placement for Minimal Invasive Thoracolumbar Spine Surgery,” Frontiers in Surgery, frontiersin.org These throughput gains make operating room integration market implementations financially attractive, particularly for systems facing strained staffing and reimbursement pressures.

Rapid Uptake of Minimally Invasive & Image-Guided Surgeries

Laparoscopic and endovascular techniques require simultaneous visualization of high-resolution video, fluoroscopy, and navigation data. Augmented-reality overlays have improved precision in microsurgical fields and neurosurgery, streamlining complex instrument maneuvers.[3]James Zhang et al., “The Impact of Extended Reality on Surgery: A Scoping Review,” Springer, springer.comHospitals therefore prioritize interoperable video routing, low-latency image processing, and sterile touch interfaces, all of which propel the operating room integration market.

Hospital Investments in Digital/IoT-Enabled OR Platforms

Three-quarters of executives label OR digitization “critical,” yet many still underfund it. Systems now monitor device usage and environmental variables, generating analytics that flag idle assets or abnormal workflow bottlenecks. Cybersecurity spending has risen to as much as 10% of IT budgets as ransomware attacks highlight risks to connected theatres. The drive to safeguard data while unlocking predictive insights strengthens demand for integrated, standards-based architectures.

Post-Pandemic Backlog Reduction Programs

North American and European health networks extended OR hours, created high-intensity theatre lists, and redirected lower-risk cases to ASCs. Reinforcement-learning scheduling engines outperformed manual block-allocation methods in clearing backlogs efficiently.[4]Sam M. Wiseman and Jason M. Sutherland, “Improving the Quality of Care of Canadians Waiting for Elective Surgery,” Canadian Journal of Surgery, canjsurg.ca These experiences cemented the role of centralized scheduling dashboards and digital case carts, further lifting the operating room integration market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & lifecycle maintenance costs | -1.8% | Global; acutely felt by smaller hospitals | Medium term (2-4 years) |

| Lengthy procurement cycles & budget freezes | -1.2% | Europe & Canada; select US public systems | Short term (≤ 2 years) |

| Shortage of biomedical IT personnel | -0.9% | Global; severe in rural areas | Long term (≥ 4 years) |

| Cybersecurity & data-privacy risks | -0.7% | Global; regulation varies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital & Lifecycle Maintenance Cost of OR Integration

Beyond initial hardware, hospitals must fund software licenses, patch management, and staff retraining, often surpassing upfront spend over a decade. Smaller campuses with limited surgical throughput struggle to clear return-on-investment thresholds, slowing penetration in community settings.

Lengthy Procurement Cycles & Budget Freezes in Public Hospitals

Compliance with multi-year capital plans and competitive tender laws can push installations 18–24 months beyond initial scope. European facilities face additional scrutiny on interoperability and sustainability, prolonging bid evaluations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Leads an Analytics Revolution

Software accounted for 44.12% of 2025 revenue, underscoring the migration from cabling and routers toward data orchestration, workflow guidance, and AI-based predictive alerts. Service contracts are forecast to rise at a 14.57% CAGR as customers recognize that every upgrade introduces change-management and cybersecurity tasks best handled by specialists. In contrast, commoditized hardware such as ceiling booms and monitor arms delivers solid but slower growth. The operating room integration market size for services is projected to expand from USD 1.28 billion in 2025 to USD 2.9 billion by 2031, mirroring the industry’s pivot to recurring revenue. AI-enabled platforms, including KARL STORZ’s Artisight collaboration, reveal how real-time analytics lower turnover times and elevate staff satisfaction.

Purpose-built middleware integrates multi-vendor imaging, anesthesia records, and pathology reports into a unified timeline that surgeons can query intra-operatively. Hospitals cite automated preference-card management and predictive device servicing as the top two software benefits. These capabilities reinforce the view that the operating room integration market will reward vendors that deliver open APIs, granular cybersecurity controls, and intuitive dashboards rather than isolated display routers.

By Application: Neurosurgery Complexity Drives Demand

General surgery commanded 36.25% revenue share in 2025 due to sheer case volume, yet neurosurgery will grow fastest at a 13.22% CAGR as frameless navigation, robotic scaffolds, and intra-operative CT imaging become routine. The operating room integration market size associated with neurosurgery is projected to nearly double by 2031. Integrated guidance systems have already pushed pedicle-screw placement accuracy to 99% in hybrid rooms, slashing revision operations and radiation exposure.

Cardiovascular, orthopedics, and urology maintain healthy shares, but their growth hinges on procedure migration to outpatient and catheter-based labs. Neurosurgery’s insistence on zero-latency imaging, redundant power, and vibration control makes it the bellwether for next-generation suite specifications. Hospitals aligning early with this trajectory future-proof their investment and solidify referral pipelines, supporting wider growth in the operating room integration market.

By End-User: ASCs Accelerate Outpatient Integration

Large tertiary hospitals held 57.92% of revenue in 2025, but ASCs represent the fastest 13.98% CAGR as policymakers lift inpatient-only restrictions on joint arthroplasty and other high-value procedures. The operating room integration market share for ASCs is set to climb steadily as outpatient volumes approach 44 million cases by 2034.

ASCs demand compact, cloud-managed consoles that minimize floor space and simplify infection control. Vendors that package video routing, anesthesia charting, and remote proctoring into subscription bundles gain traction by lowering upfront capital. For small hospitals, managed-service contracts that outsource IT maintenance become the entry point to advanced integration, broadening the operating room integration market footprint.

By OR Type: Hybrid Rooms Lead Innovation

Hybrid theatres combined interventional radiology, CT, or angiography with open surgery tools to capture 50.86% revenue in 2025 and to log the strongest 15.02% CAGR. The operating room integration market size for hybrid rooms benefits from their ability to support stroke thrombectomy, endovascular aortic repair, and complex spine fusion in a single session. Sites in challenging geographies, such as Tibet, report meaningful reductions in complication rates after installing hybrid suites equipped with robot-assisted positioning and real-time fluoroscopy.

While classic integrated digital ORs suffice for high-volume general surgery, forward-looking hospitals view hybrid configurations as an essential hedge against case-mix shifts. The higher ticket size also attracts vendors eager to bundle software, imaging, and robotics, further concentrating the operating room integration market opportunity.

Geography Analysis

North America retained 39.12% of 2025 revenue on the back of entrenched hospital networks, reimbursement clarity, and early adoption of digital health mandates. Systems leverage predictive scheduling tools to recapture elective volumes that fell during the pandemic. The operating room integration market size in the United States alone surpassed USD 1.1 billion in 2025. Canada’s publicly funded model adds momentum through national backlog-reduction funds that earmark capital for integrated theatres.

Europe remains a mature yet innovative cluster. Sustainability directives spur replacement of legacy halogen lighting with LED arrays and demand life-cycle assessments for every large capital project. High-profile programs such as Germany’s Hospital Future Act disburse grants for interoperability upgrades, sustaining steady adoption. Meanwhile, stringent procurement laws lengthen decision cycles, tempering the operating room integration market’s growth rate relative to North America.

Asia-Pacific represents the breakout region with a forecast 13.94% CAGR. China’s public hospitals scale AI-enabled smart wards and adopt hybrid theatres to handle rising vascular and oncology caseloads. Japan advances showcase projects like Sapporo Kashiwabakai Hospital, where Siemens Healthineers engineered a fully digital, patient-centric “Smart‐OR” that shortens emergency transfer times. India and Southeast Asia emphasize modular, cost-optimized suites suited to constrained budgets but high procedure growth, broadening the operating room integration market.

Latin America and the Middle East & Africa post modest uptake impeded by currency volatility and infrastructure gaps. Nonetheless, selected private groups invest strategically to attract medical tourism and retain top surgical talent, laying the groundwork for future expansion.

Competitive Landscape

The operating room integration industry is moderately fragmented. Legacy device makers such as Stryker, KARL STORZ, and STERIS pivot toward platform-centric portfolios combining software orchestration, managed services, and cybersecurity. Stryker bundles its iSuite offering with voice-activated control, AI-enhanced surgical video analytics, and robotics to reinforce account stickiness. KARL STORZ’s alliance with NVIDIA and Artisight exemplifies the shift from proprietary hardware toward cloud-native AI ecosystems.

Emerging software specialists emphasize vendor-agnostic connectivity, offering lightweight subscription models that appeal to ASCs and mid-tier hospitals. Olympus teamed with Proximie to deliver secure, real-time video collaboration, extending its presence beyond endoscopes to encompass virtual mentoring and digital asset management. Brainlab’s planned Frankfurt IPO aims to finance expansion of its digital surgery platform across orthopedics and cardiovascular applications, signaling investor confidence in service-heavy revenue streams.

Partnerships predominate as firms recognize that no single vendor can supply imaging, navigation, robotics, cybersecurity, and analytics at scale. The resulting ecosystem approach nurtures cross-licensing and white-label arrangements, progressively tightening interoperability standards and accelerating consolidation within the operating room integration market.

Operating Room Integration Industry Leaders

Stryker Corporation

Olympus Corporation

KARL STORZ SE & Co. KG

STERIS plc

Getinge AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Brainlab AG filed for a Frankfurt Stock Exchange IPO to raise EUR 200 million for global rollout of integrated OR solutions.

- May 2025: Altera Digital Health activated an integrated operating theater at Latrobe Regional Health, leveraging Microsoft Azure for enterprise-wide EHR interoperability.

- April 2024: LEM Surgical obtained FDA 510(k) clearance for its Dynamis Robotic Surgical System, expanding robotic options for hard-tissue procedures.

- March 2025: Artisight, NVIDIA, and KARL STORZ announced a collaboration to deliver AI-enabled “Smart ORs,” integrating automation and analytics.

Global Operating Room Integration Market Report Scope

As per the scope of the report, integrated operating rooms are designed to lessen the complexity of the most intricate environments inside a hospital, a private clinic, or a medical institute. The operating room integration market is segmented by component (software and services), application (general surgery, orthopedic surgery, cardiovascular surgery, neurosurgery, and others), and geography (North America, Europe, Asia-Pacific, Middle-East and Africa, and South America). The market report also covers the estimated market sizes and trends of 17 countries across major regions globally. The report offers values (in USD million) for the above-mentioned segments

| Software |

| Services |

| Hardware (AV management, surgical displays, OR booms, lights) |

| General Surgery |

| Orthopedic Surgery |

| Cardiovascular Surgery |

| Neurosurgery |

| Urology & Gynecology |

| Large Hospitals (≥500 beds) |

| Small & Mid-size Hospitals (<500 beds) |

| Ambulatory Surgical Centers (ASCs) |

| Hybrid Operating Rooms |

| Integrated Digital ORs (non-hybrid) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software | |

| Services | ||

| Hardware (AV management, surgical displays, OR booms, lights) | ||

| By Application | General Surgery | |

| Orthopedic Surgery | ||

| Cardiovascular Surgery | ||

| Neurosurgery | ||

| Urology & Gynecology | ||

| By End-User | Large Hospitals (≥500 beds) | |

| Small & Mid-size Hospitals (<500 beds) | ||

| Ambulatory Surgical Centers (ASCs) | ||

| By OR Type | Hybrid Operating Rooms | |

| Integrated Digital ORs (non-hybrid) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current operating room integration market size?

The operating room integration market size reached USD 3.18 billion in 2026.

How fast is the operating room integration market expected to grow?

It is forecast to register a 10.88% CAGR, climbing to USD 5.33 billion by 2031.

Which component segment is expanding the quickest?

Services are projected to rise at a 14.57% CAGR because hospitals seek ongoing optimization and support for integrated suites.

Why are hybrid operating rooms gaining momentum?

Hybrid rooms combine surgical and interventional capabilities, capturing 50.86% revenue in 2025 and growing fastest at 15.02% CAGR due to their versatility in complex procedures.

Which region presents the highest growth potential?

Asia-Pacific is poised for a 13.94% CAGR as governments invest in healthcare modernization and procedure volumes climb.

Page last updated on: