Location-Based Entertainment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

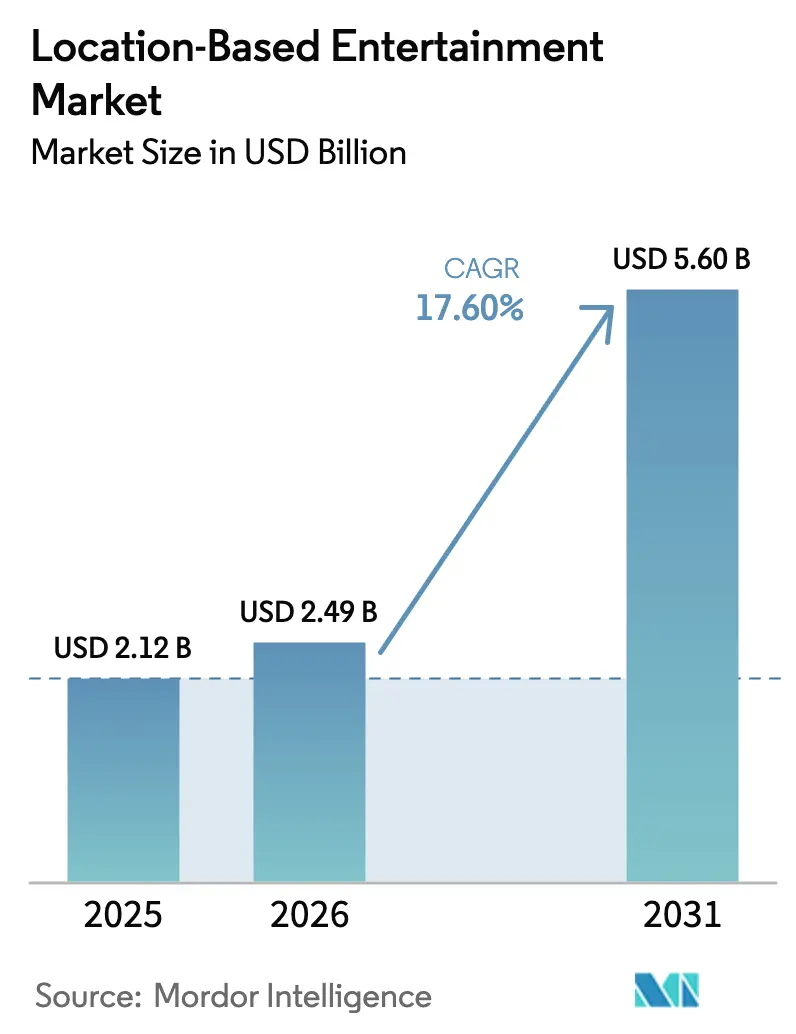

| Market Size (2026) | USD 2.49 Billion |

| Market Size (2031) | USD 5.6 Billion |

| Growth Rate (2026 - 2031) | 17.60% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Location-Based Entertainment Market Analysis by Mordor Intelligence

The location-based entertainment market size in 2026 is estimated at USD 2.49 billion, growing from 2025 value of USD 2.12 billion with 2031 projections showing USD 5.6 billion, growing at 17.6% CAGR over 2026-2031. Momentum stems from widespread 5G coverage, generative-AI content pipelines, and blockbuster intellectual-property (IP) tie-ins that make premium, in-venue experiences difficult to replicate at home. Operators command higher average spend per visit by bundling merchandise, food, and event programming alongside immersive attractions. Hardware suppliers continue reducing headset weight and cost, smoothing adoption for both consumers and venues. Simultaneously, cloud-rendered content lowers on-site compute needs, unlocking new pop-up formats in shopping districts and travel hubs. Competitive rivalry centers on securing exclusive IP rights and forging edge-compute partnerships that can cut latency to sub-20 milliseconds, a threshold that supports multi-user mixed-reality arenas in compact footprints.

Key Report Takeaways

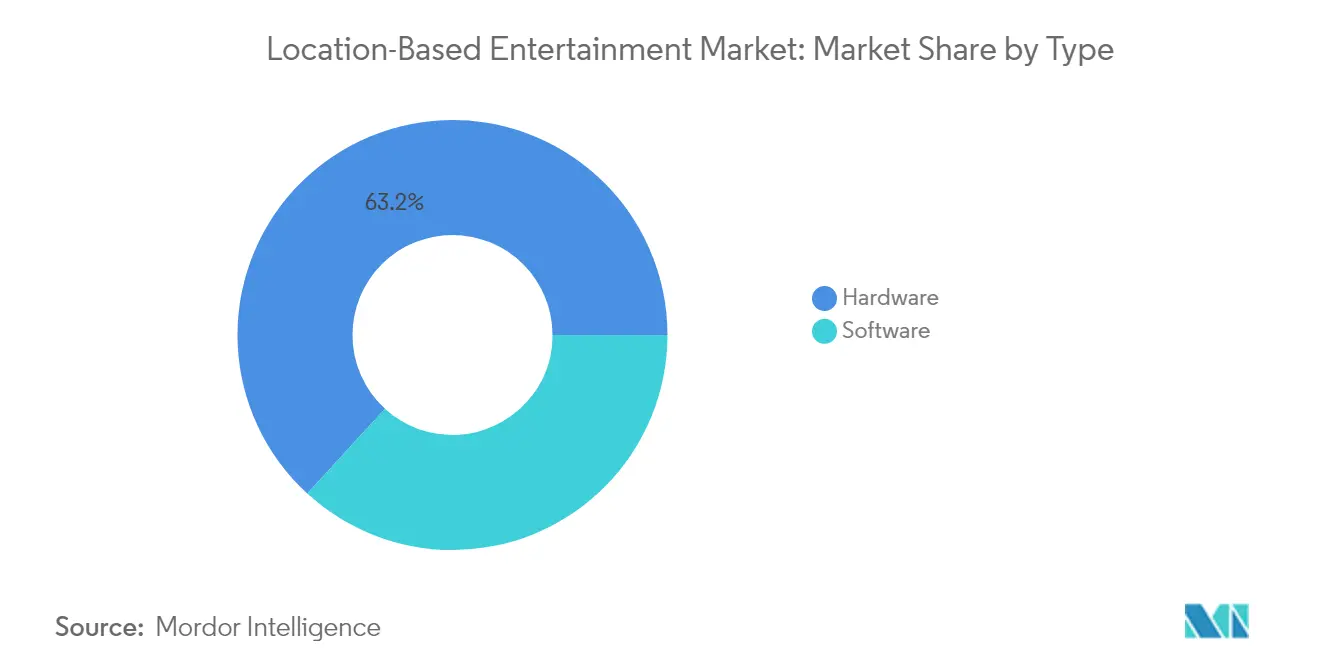

- By type, hardware led with 63.20% of location-based entertainment market share in 2025, while software and platforms are forecast to expand at a 23.10% CAGR through 2031.

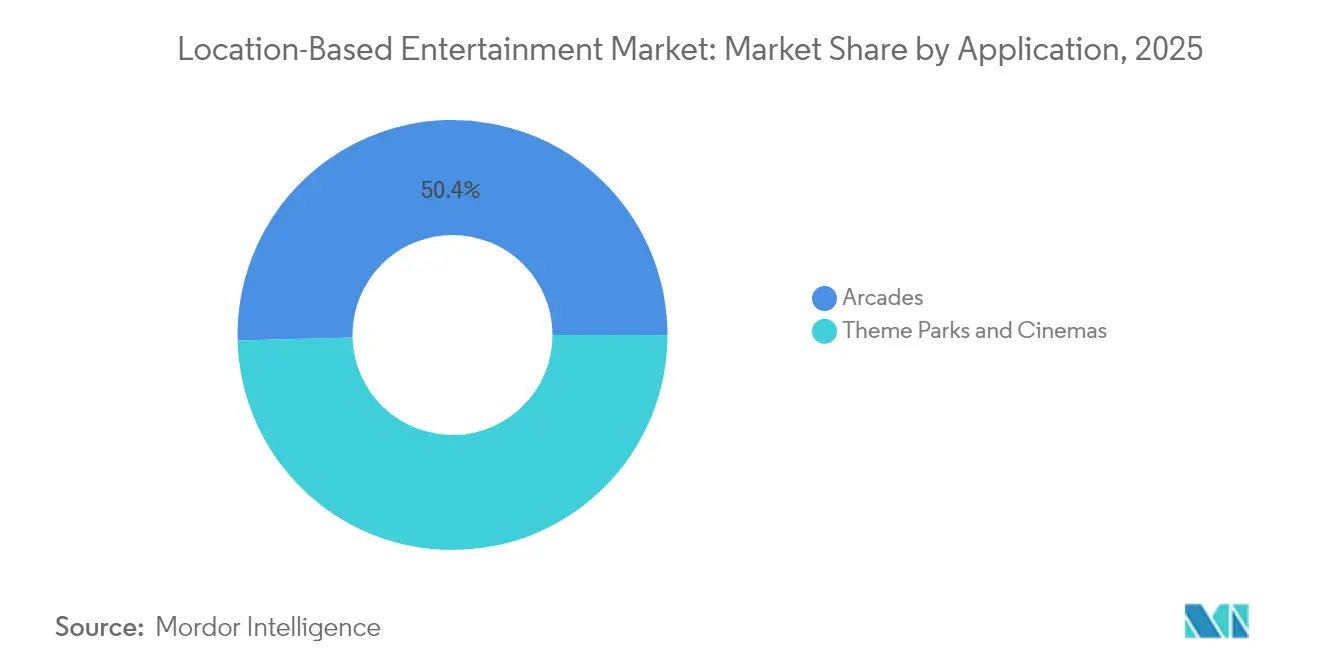

- By application, arcades held 50.40% of the location-based entertainment market share in 2025; theme parks are projected to grow at a 22.40% CAGR to 2031.

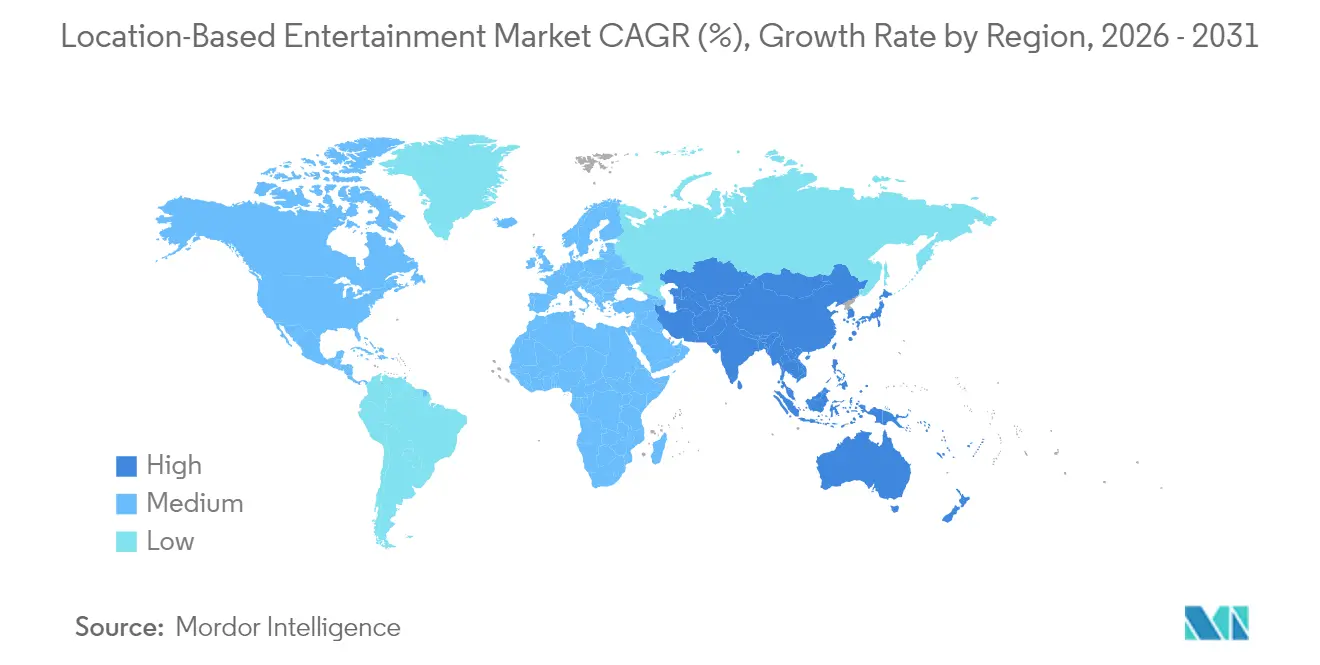

- By geography, the United States accounted for 35.55% of location-based entertainment market share in 2025, whereas China is poised for a 24.00% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Location-Based Entertainment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising spend per capita at amusement venues | +3.2% | Global; concentrated in North America and Europe | Medium term (2-4 years) |

| Rapid roll-out of turnkey LBVR franchise pods | +4.1% | North America, Europe, expanding to APAC | Short term (≤ 2 years) |

| 5G/edge-compute partnerships | +3.8% | Urban centers worldwide, led by US, China, South Korea | Medium term (2-4 years) |

| Generative-AI tools cutting content costs | +2.9% | Global; early adoption in developed markets | Long term (≥ 4 years) |

| Mixed-reality attractions tied to blockbuster IP | +2.7% | North America, Europe, expanding to China | Medium term (2-4 years) |

| Growing corporate team-building budgets | +1.8% | Developed markets, urban business districts | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising spend per capita at amusement venues

Consumers continue to premiumize out-of-home entertainment, paying more for differentiated multi-sensory attractions than for legacy arcade cabinets. Operators boost average transaction values by bundling exclusive merchandise, themed food, and VIP queue access. The trend aligns with younger cohorts prioritizing experiences over goods, sustaining footfall even in macro-economic slowdowns. Flexible pricing algorithms further lift yields during peak evening and weekend slots. As a result, location-based entertainment market revenue per square foot now rivals indoor trampoline parks and boutique cinemas.

Rapid roll-out of turnkey LBVR franchise pods

Standardized “store-in-a-box” packages compress venue launch cycles from months to weeks by bundling motion-tracked headsets, modular play-areas, and evergreen content libraries. Franchisees focus on local marketing and guest throughput, while the franchisor handles firmware, content updates, and remote diagnostics. Sandbox VR expanded from 8 to 25 franchise operators during 2024, targeting 200 active sites by 2027.[1]Katie Jones, “Sandbox VR Raises $6.8 Million,” Zawya, zawya.com The model de-risks technology refresh costs for small business owners and drives network effects that attract third-party developers to a unified distribution platform.

5G/edge-compute partnerships enabling heavy-content streaming

Telco alliances with venue chains offload rendering tasks to nearby edge nodes, eliminating backpack PCs and tethered cables. In a joint showcase, Ericsson, AT&T, Dreamscape Immersive, NVIDIA, Qualcomm, and Wevr delivered an untethered, six-player experience with sub-20 ms round-trip latency.[2]Ericsson Editorial Team, “5G and Edge Compute Power Untethered VR,” Ericsson, ericsson.com Lower in-venue hardware costs open high-footfall sites such as airports and malls, while carriers monetize premium network slices during evening and weekend peaks.

Generative-AI tools cutting content production costs

Procedural world-building, character animation, and sound-design tools shorten concept-to-launch timelines and extend IP life cycles. Meta introduced AI-generated Horizon Worlds templates that convert text prompts into interactive environments within minutes. Independent studios can now refresh storylines quarterly, aligning with consumer demand for novelty and reducing licensing fees for off-the-shelf titles. Cost reductions of 40-60% redirect budget toward marketing and guest services, strengthening venue profitability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront CAPEX for multi-user arenas | -2.8% | Global; smaller operators disproportionately | Short term (≤ 2 years) |

| Content refresh cycle < 12 months inflating OPEX | -1.9% | Global; intense in competitive urban markets | Medium term (2-4 years) |

| Patchy insurance and safety regulations | -1.2% | Developed markets with strict liability rules | Long term (≥ 4 years) |

| Consumer hygiene concerns with shared HMDs | -0.8% | Global; heightened in health-conscious groups | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High upfront CAPEX for multi-user free-roam arenas

Fully immersive arenas require motion-capture arrays, reinforced flooring, and specialized fire-safety systems that push startup budgets well above USD 500,000. Premium head-mounted displays still cost several hundred dollars each to procure, and micro-OLED screens account for 21% of the Vision Pro bill of materials.[3]Hanson Ho, “Micro-OLED Cost Breakdown for Vision Pro,” Panox Display, panoxdisplay.com These capital hurdles favor franchise chains with franchisor financing or entertainment giants able to amortize costs across wider portfolios, leaving independent entrants to target smaller-scale booth formats.

Content refresh cycle < 12 months inflating OPEX

Frequent experience turnover is now a competitive necessity, yet licensing popular titles can absorb 15-25% of monthly operating spend. The gap between an average six-month consumer appetite for “something new” and the longer development calendars of bespoke experiences forces operators to license larger libraries than optimal. Subscription-based platforms soften the pain, but the lack of standardized royalty structures keeps margins thin. Operators that cannot sustain regular refreshes risk negative word-of-mouth and declining repeat visitation, constraining the location-based entertainment market’s addressable capacity in highly competitive cities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Hardware Dominance Faces Software Disruption

Hardware held 63.20% of 2025 revenue, benefiting from continuous display-resolution gains and lighter form-factors that improve guest comfort. At the same time, the segment’s gross margins face headwinds as component prices remain elevated; Vision Pro displays alone cost USD 456 per unit. Hardware makers counter margin compression by bundling maintenance contracts and exclusive content.

Software and platforms are the fastest-growing layer, advancing at a 23.10% CAGR from 2026-2031. Cloud streaming and AI-driven toolsets shift value toward recurring licensing, analytics, and community management fees. The location-based entertainment market size for software providers is projected to reach parity with hardware revenue before 2030, underpinned by demand for cross-venue leaderboards and personalized content playlists. Subscription bundles lower up-front cash burn for venues, while data dashboards optimize session scheduling, raising utilization by as much as 15%.

By Application: Theme Parks Accelerate Past Arcade Leaders

Arcades accounted for 50.40% of 2025 revenue thanks to low floor-area requirements and flexible site selection. Franchised concepts average USD 1.7 million annual sales per US location. Nevertheless, arcades face intensifying competition from mall-based pop-ups and cinematic cross-overs.

Theme parks are the fastest-growing application, set for a 22.40% CAGR through 2031. Large operators integrate headline IPs, allowing premium ticket surcharges and multi-hour dwell times. Merlin Entertainments committed USD 110 million to Minecraft-themed attractions opening from 2026. Universal’s Epic Universe anchors its Dark Universe land around classic monster franchises, raising per-capita guest spend via collectible merchandise and themed dining. The location-based entertainment market size for theme parks is forecast to double as blockbuster IPs lure both domestic visitors and international tourists.

Geography Analysis

The United States remains the largest national market with 35.55% of 2025 revenue. Mature transport links and venture-capital funding enable rapid trials of new formats, while corporate off-sites fill weekday slots. Universal’s proposed Bedfordshire park underscores sustained investor appetite for large-scale projects in high-income regions.

China delivers the highest growth, a 24.00% CAGR to 2031, buoyed by government smart-city initiatives and a pipeline of more than 100 large VR complexes launched in 2024.. Aggressive 5G roll-out allows cloud rendering, trimming hardware costs for operators. Domestic studios merge folklore narratives with cutting-edge effects, creating culturally resonant attractions that draw repeat visitation.

Europe shows steady progress as historic sites deploy immersive overlays to deepen visitor engagement. German operator Karls Erlebnis-Dorf invested EUR 30 million in new adventure zones during 2025.. Meanwhile, Rest-of-World growth clusters in Southeast Asia and the Middle East, where tourism authorities court franchise chains such as Singapore-based Neon Group, posting 20% annual sales gains and announcing new sites in Tokyo, Bangkok, and Paris.

Competitive Landscape

Market structure remains moderately fragmented, with hardware builders, content studios, and operators pursuing hybrid strategies to secure wallet share across the value chain. Meta’s Reality Labs lost USD 4.2 billion in Q1 2025 despite USD 412 million in sales, signaling the scale of R&D outlays needed to shape standards. Venue chains such as Sandbox VR sidestep hardware risk, surpassing USD 200 million in lifetime revenue through franchise fees and central content sourcing. Traditional entertainment majors diversify into immersive formats: Disney negotiates to adapt MuppetVision 3D to Apple Vision Pro, while Meow Wolf layers augmented reality onto physical art installations for hybrid engagement.

Strategic alliances focus on edge-compute nodes, consumer-safe headsets, and proprietary IP pipelines. Early-mover advantages accrue to firms controlling both compelling content and the technical stack that delivers it cost-effectively. White-space applications in enterprise training and healthcare therapy attract new entrants, yet customer-acquisition economics still hinge on leisure-segment footfall volumes.

Location-Based Entertainment Industry Leaders

-

Meta

-

HTC

-

Samsung Electronics Co., Ltd.

-

Sony Interactive Entertainment Inc.

-

DPVR

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Meta unveiled AI-generated Horizon Worlds scene-building, slashing environment-creation timelines.

- June 2025: Disney opened talks with Jim Henson Company to translate MuppetVision 3D to next-gen headsets.

- June 2025: Meow Wolf announced augmented-reality extensions for its immersive art venues

- April 2025: Sandbox VR exceeded USD 200 million lifetime revenue with 127 new sites in the pipeline.

Global Location-Based Entertainment Market Report Scope

The Global Location-Based Entertainment Market is Segmented By Type (Hardware, Software), By Application (Arcade, Theme Parks, Cinemas), and Geography.

| Hardware (Headsets) |

| Software / Platforms |

| Arcades |

| Theme Parks |

| Cinemas |

| North America |

| Europe |

| Asia-Pacific |

| Rest of World |

| By Type | Hardware (Headsets) |

| Software / Platforms | |

| By Application | Arcades |

| Theme Parks | |

| Cinemas | |

| By Geography | North America |

| Europe | |

| Asia-Pacific | |

| Rest of World |

Key Questions Answered in the Report

What is the current size of the location-based entertainment market?

The market generated USD 2.49 billion in 2026 and is projected to reach USD 5.6 billion by 2031 at an 17.60% CAGR.

Which segment holds the largest location-based entertainment market share?

Hardware accounted for 63.20% of revenue in 2025, reflecting continued demand for high-performance headsets and tracking systems.

Which application is expanding the fastest?

Theme parks are forecast to grow at a 22.40% CAGR from 2026-2031, driven by blockbuster IP integrations and premium guest spending.

Why is China the fastest-growing region?

Government smart-city initiatives, rapid 5G deployment, and the launch of more than 100 large-scale VR projects in 2024 support a 24.00% regional CAGR through 2031.

How are 5G and edge computing affecting the industry?

Low-latency edge nodes eliminate the need for bulky on-site PCs, lowering capital costs and enabling untethered multi-user experiences that raise venue throughput and guest satisfaction.

What challenges limit near-term growth?

High upfront capital requirements for free-roam arenas and the need to refresh content in less than 12 months strain cash flow, especially for independent operators.

Page last updated on: