Mechanical Keyboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

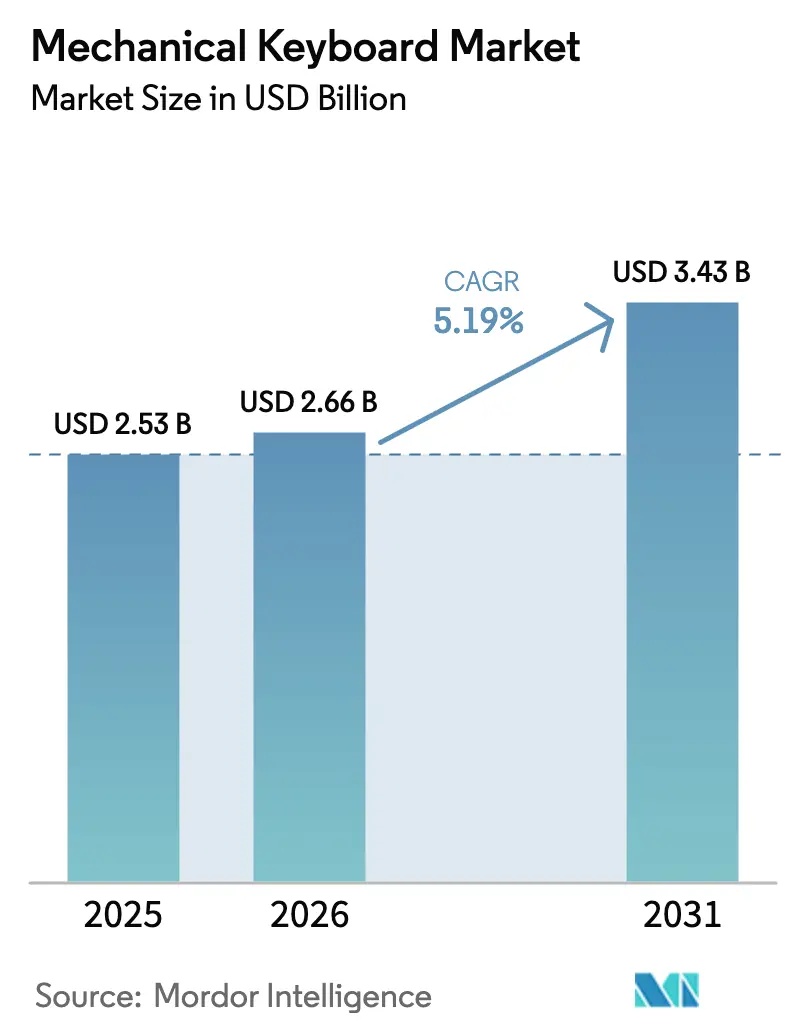

| Market Size (2026) | USD 2.66 Billion |

| Market Size (2031) | USD 3.43 Billion |

| Growth Rate (2026 - 2031) | 5.19% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

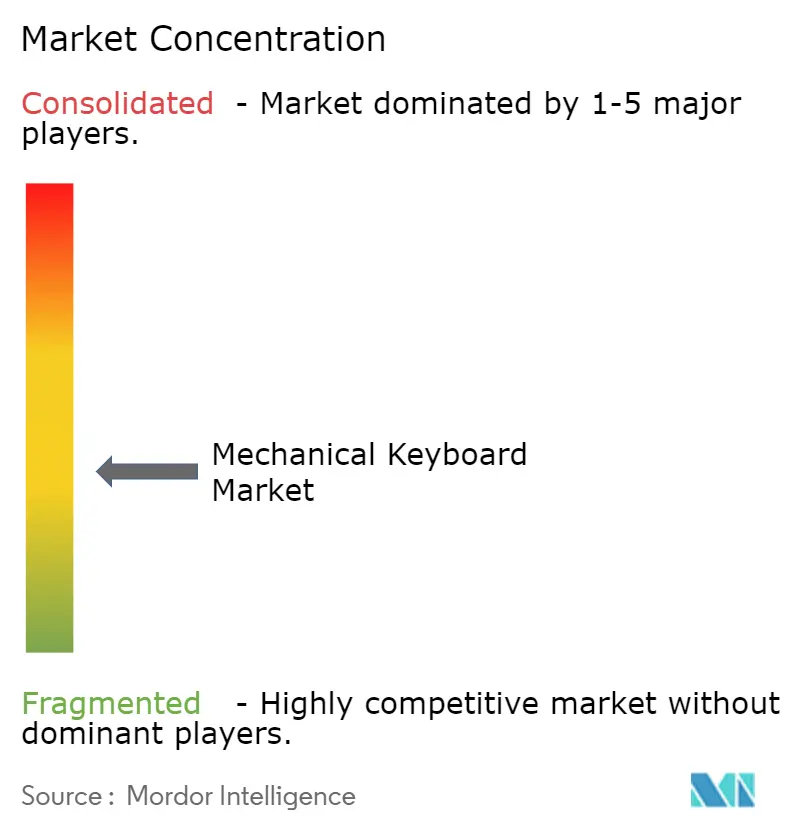

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mechanical Keyboard Market Analysis by Mordor Intelligence

Mechanical keyboard market size in 2026 is estimated at USD 2.66 billion, growing from 2025 value of USD 2.53 billion with 2031 projections showing USD 3.43 billion, growing at 5.19% CAGR over 2026-2031. Rising hybrid-work adoption, continued esports investment and switch miniaturization collectively reposition the category from gaming niche to mainstream productivity accessory. Demand for compact 65% and low-profile layouts intensifies as home offices shrink and workers seek ergonomic upgrades. Component innovation led by optical and hall-effect designs sustains premium pricing while keeping performance front-of-mind for competitive gamers. Asia-Pacific production scale, Europe’s strict ergonomics rules and North America’s high refresh-rate gaming culture together create a balanced global growth profile.

Key Report Takeaways

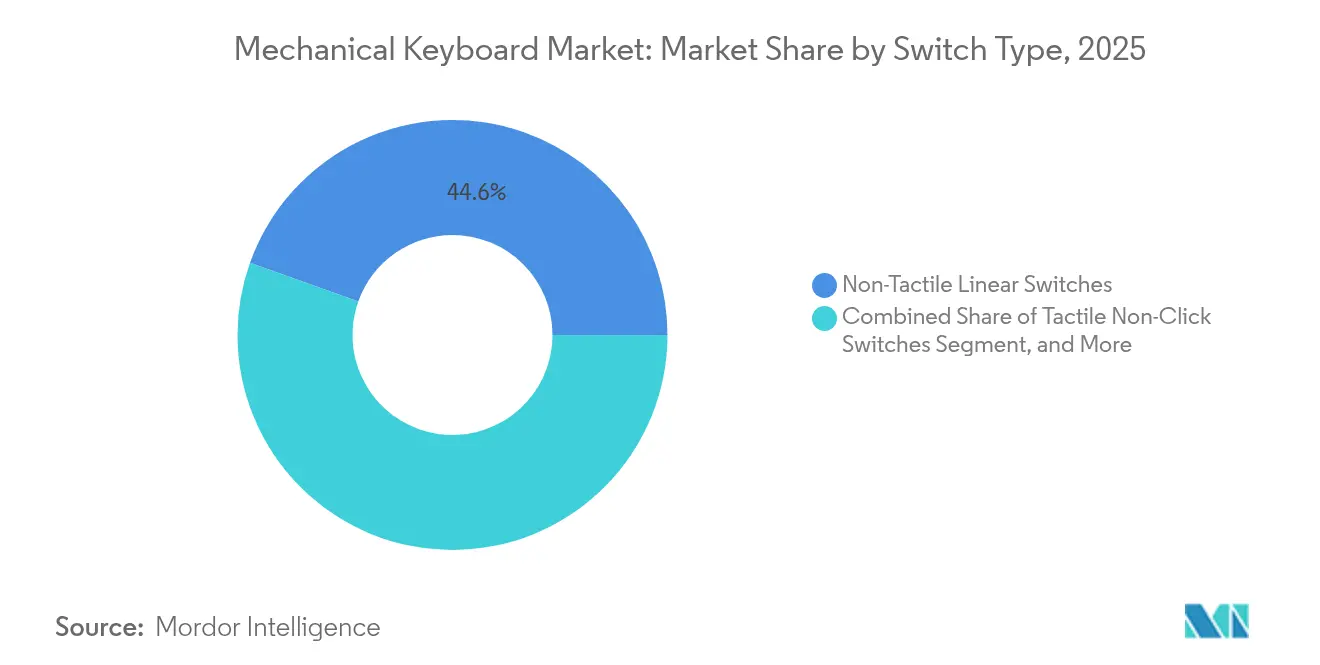

- By switch type, non-tactile linear switches held 44.55% of the mechanical keyboard market share in 2025 while optical and hall-effect switches are forecast to grow at 7.62% CAGR through 2031.

- By connectivity, wired models retained 69.05% of the mechanical keyboard market size in 2025; 2.4 GHz wireless solutions are projected to expand at 6.32% CAGR to 2031.

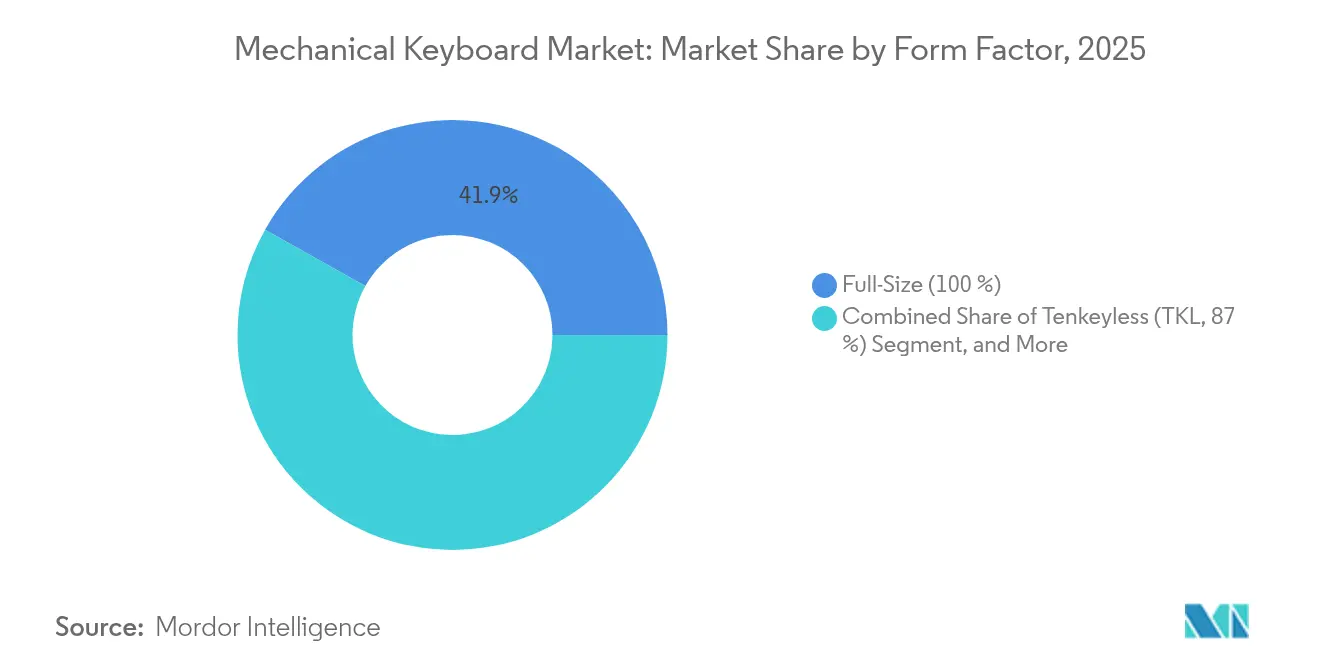

- By form factor, full-size layouts led with 41.85% revenue share in 2025; the 65% segment is advancing at an 8.23% CAGR through 2031.

- By keycap material, ABS dominated with 57.95% share in 2025 while PBT double-shot variants are expected to grow 7.75% annually to 2031.

- By application, gaming and esports commanded 59.75% of the mechanical keyboard market size in 2025; enthusiast/DIY use cases post the highest 8.55% CAGR through 2031.

- By geography, Asia-Pacific captured 38.15% revenue in 2025 and is set to record the fastest 5.96% CAGR during the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Mechanical Keyboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Esports-led expansion of high-refresh-rate gaming monitors | +0.8% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Rise of hybrid work culture | +0.6% | North America & Europe | Short term (≤ 2 years) |

| Rapid growth of DIY/enthusiast communities | +0.9% | Asia-Pacific core; spill-over global | Long term (≥ 4 years) |

| Switch miniaturization for 60% & 65% layouts | +0.7% | Global | Medium term (2-4 years) |

| Optical & hall-effect switch adoption | +0.5% | Esports hubs worldwide | Short term (≤ 2 years) |

| Corporate ergonomics programs | +0.4% | Europe expanding to North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Esports-led Expansion of High-Refresh-Rate Gaming Monitors

High-performance displays running at 240 Hz and above let competitive players realize benefits only when every peripheral responds equally fast. Professional teams now specify sub-1 ms keyboards and brands such as Corsair saw peripheral revenue climb in tandem with monitor upgrades.[1]Corsair Gaming Inc., “Corsair Gaming Reports Strong First Quarter 2025 Growth in Revenue, EBITDA and Gross Margin,” ir.corsair.com Tournament organizers bundle keyboards in sponsorship packages, while monitor makers cross-promote certified boards alongside new panels. Content creators echo the requirement during livestreams, reinforcing consumer demand. The feedback loop pushes premium boards beyond gaming circles into mainstream buyers seeking “tournament grade” assurance.

Rise of Hybrid Work Culture Intensifying Home-Office Upgrades

Permanent remote work turned mechanical keyboards into daily productivity essentials. Logitech’s keyboards and combos category grew 20% in Q1 2025 as businesses supplied employees with higher-quality input devices. IT budgets now earmark ergonomic peripherals, elevating wireless, multi-device boards that switch between work laptop and personal PC. Corporate insurance programs classify mechanical boards under health-related spend, accelerating bulk procurement. Durable PBT keycaps gain traction with professionals who value longevity over RGB aesthetics.

Rapid Growth of DIY/Enthusiast Keyboard Communities

Influencer-driven teardown videos on YouTube and Twitch repositioned keyboards as customizable art pieces. Asia-Pacific hobbyists benefit from proximity to factories, turning Shenzhen-origin parts into globally shipped kits. Direct-to-consumer switch makers recorded robust 2025 web-store growth as builders bypassed OEMs. Viral trends-from gasket mounts to latent sound-dampening mods-spread via social networks, compressing product cycles and letting small brands crowdsource design feedback in real time. The community’s appetite for experimentation fosters continuous component innovation.

Switch Miniaturization Enabling Ultraportable Layouts

Thin mechanical switch platforms introduced by CHERRY in 2025 allow boards as slim as 22 mm while preserving 4 mm travel.[2]CHERRY, “CHERRY Leads the Revolution from Mechanical to Smart Switches,” cherry.de Compact 65% designs remain travel-friendly yet keep arrow keys, meeting a wide user spectrum from coders to creatives. Portability aligns with mobile-first professionals who alternate between coffee shops and co-working spaces. Manufacturers leverage miniaturization to produce split or ergonomic variants without bulk, broadening addressable demand.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price inflation of PBT keycaps & custom PCBs | -0.9% | Global | Short term (≤ 2 years) |

| Supply-chain concentration in China | -0.6% | Global; acute in North America | Medium term (2-4 years) |

| Limited battery life & latency in esports wireless | -0.8% | Competitive gaming markets | Long term (≥ 4 years) |

| Environmental scrutiny over ABS keycaps | -0.3% | Europe; expanding | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Inflation of Niche Components Limiting Mass Adoption

Premium parts such as double-shot PBT keycaps cost 40-60% more than ABS, inflating final retail prices beyond casual budgets. Custom PCB runs remain small, driving per-unit expenses higher and raising warranty overheads for brands. Material shortages amplify volatility, making limited-edition releases even pricier and keeping mainstream penetration subdued.

Supply-Chain Concentration in China Exposing Brands to Tariff Risks

Recent 45% tariffs forced Qwertykeys and Keyboardio to halt US shipments, spotlighting overreliance on Guangdong production clusters.[3]Wes Davis, “Qwertykeys halts keyboard shipments to US over tariff costs and confusion,” theverge.com Diversifying tooling outside China proves costly and time-intensive. Larger vendors absorb duties via slimmer margins; smaller labels risk exit. Component sourcing-from switches to stabilizers-faces the same geographic bottleneck, compounding exposure whenever trade policies tighten.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Switch Type: Linear Dominance Faces Contactless Innovation

Non-tactile linear technology held 44.55% of the mechanical keyboard market in 2025, cementing its leadership among gamers demanding smooth keystrokes. Optical and hall-effect designs, however, chart a 7.62% CAGR, propelled by sub-1 ms latency benefits that resonate with esports professionals. CHERRY’s IK inductive platform exemplifies the turn toward contactless actuation, promising infinite adjustability and extended lifespan. Hot-swappable PCBs further encourage experimentation, letting users shift from linear to optical sets without buying new boards. The mechanical keyboard market size for contactless categories is projected to swell as cost premiums narrow by 2031.

Linear switches will still dominate office settings where quiet operation pairs well with productivity demands, but rising DIY communities accelerate broader uptake of advanced mechanisms. Esports organizations now standardize on singular switch SKUs to guarantee practice consistency, influencing consumer emulation. Component manufacturers cultivate tiered lineups-traditional MX, optical and hall-effect-to serve segmented price points while defending share.

By Connectivity: Wired Reliability Versus Wireless Convenience

Wired variants controlled 69.05% of 2025 revenue thanks to zero-latency assurance critical for tournaments. Yet 2.4 GHz models deliver a 6.32% CAGR, bolstered by low-profile battery advances and tri-mode keyboards like Logitech’s G515, which offers 36-hour life at 1,000 Hz polling. Enterprises champion wireless to de-clutter desks and enable flexible seating. The mechanical keyboard market size for wireless segments will expand as fast-charge and detachable cable options ease battery anxiety.

Competitive gamers remain tethered due to interference bans at LAN events. However, mid-tier players accept microsecond delays for cable-free comfort, pushing brands to engineer swappable batteries and purpose-built tournament dongles. Bluetooth remains secondary for multi-device convenience but trails in pure performance metrics. Dual-mode boards future-proof purchases against evolving user profiles.

By Form Factor: Compact Layouts Gain Momentum

Full-size units accounted for 41.85% of 2025 shipments, underscoring continued spreadsheet and data-entry relevance. The 65% category, though, tops growth at 8.23% CAGR as mobile professionals and gamers appreciate arrow-key retention within a minimized footprint. Mechanical keyboard market share patterns illustrate this shift, with desk-space optimization aligning to multi-monitor setups.

Manufacturers exploit switch miniaturization to keep typing feel consistent despite reduced chassis height. Tenkeyless and 75% formats further diversify choices, targeting gamers and coders, respectively. Extreme 60% and 40% boards stay niche yet drive creative layout experimentation, feeding enthusiast culture while informing mainstream design.

By Keycap Material: Premium PBT Builds Brand Equity

ABS options dominated 57.95% share in 2025 for cost and color flexibility. PBT grows 7.75% annually, valued for shot-resistant texture and environmental optics amid Europe’s plastics regulations. The mechanical keyboard market size for PBT lines will swell as economies of scale emerge and corporate buyers prioritize durability.

Double-shot molding secures legends against wear, while artisan demand fuels exotic composites like POM blends. Regulatory pushes toward circular materials could accelerate innovation in bio-plastics, providing differentiation levers for early adopters.

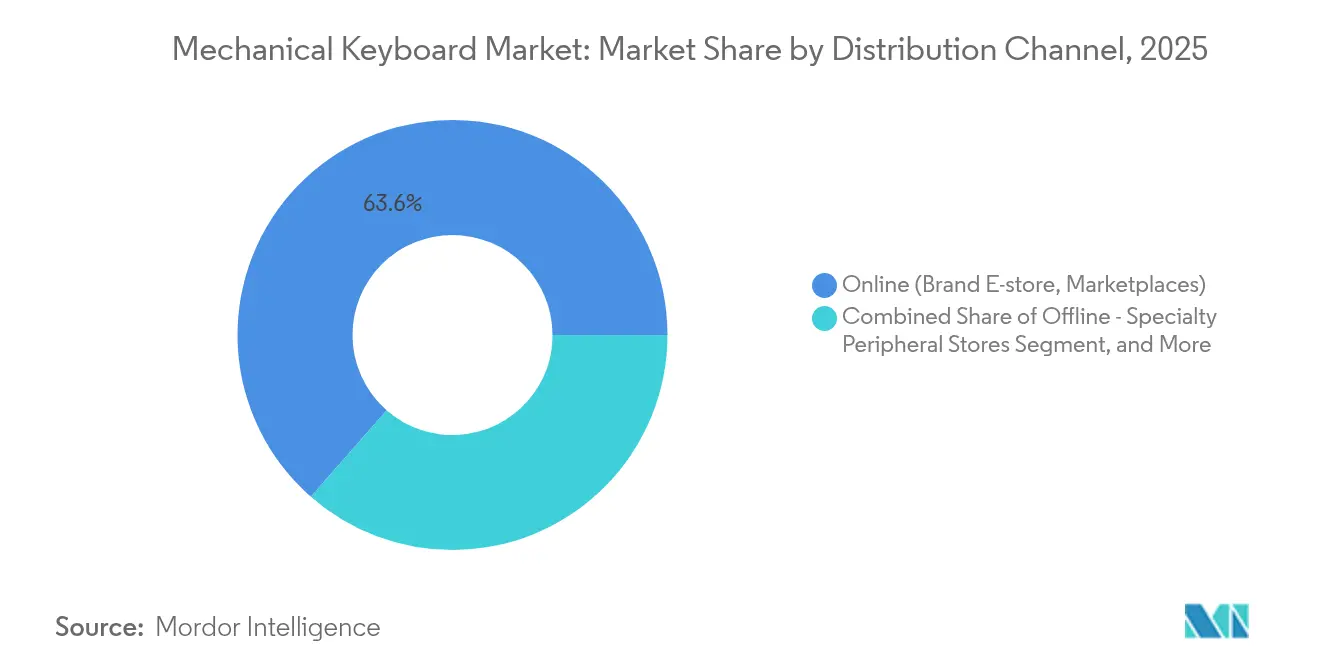

By Distribution Channel: Online Leads, Experiential Retail Resurges

E-commerce captured 63.55% of 2025 volumes, reflecting global reach and wide SKU availability. Direct brand storefronts lift margins and gather customer feedback loops, whereas marketplaces assure traffic and logistics. Specialty peripheral shops, posting 6.08% CAGR, let consumers test switches, a tactile requirement absent online.

Retailers offer hybrid “click-and-collect” models to merge convenience and experience. As mechanical keyboard market growth pushes into mainstream, big-box electronics chains stock curated selections, introducing casual shoppers to premium typing.

By Application and End-User: Gaming Holds, Enthusiast DIY Accelerates

Gaming and esports preserved 59.75% revenue in 2025, supported by streamer culture that elevates keyboard aesthetics into on-camera props. Enthusiast/DIY builders forecast an 8.55% CAGR as hobbyists chase self-expression. Corporate offices adopt split and low-profile units within ergonomics budgets, while developers value programmability for code macros.

Industrial settings request sealed boards for dusty or chemical zones, proving mechanical robustness transcends consumer perception. The mechanical keyboard market continues to diversify, with each segment driving tailored innovation cycles.

Geography Analysis

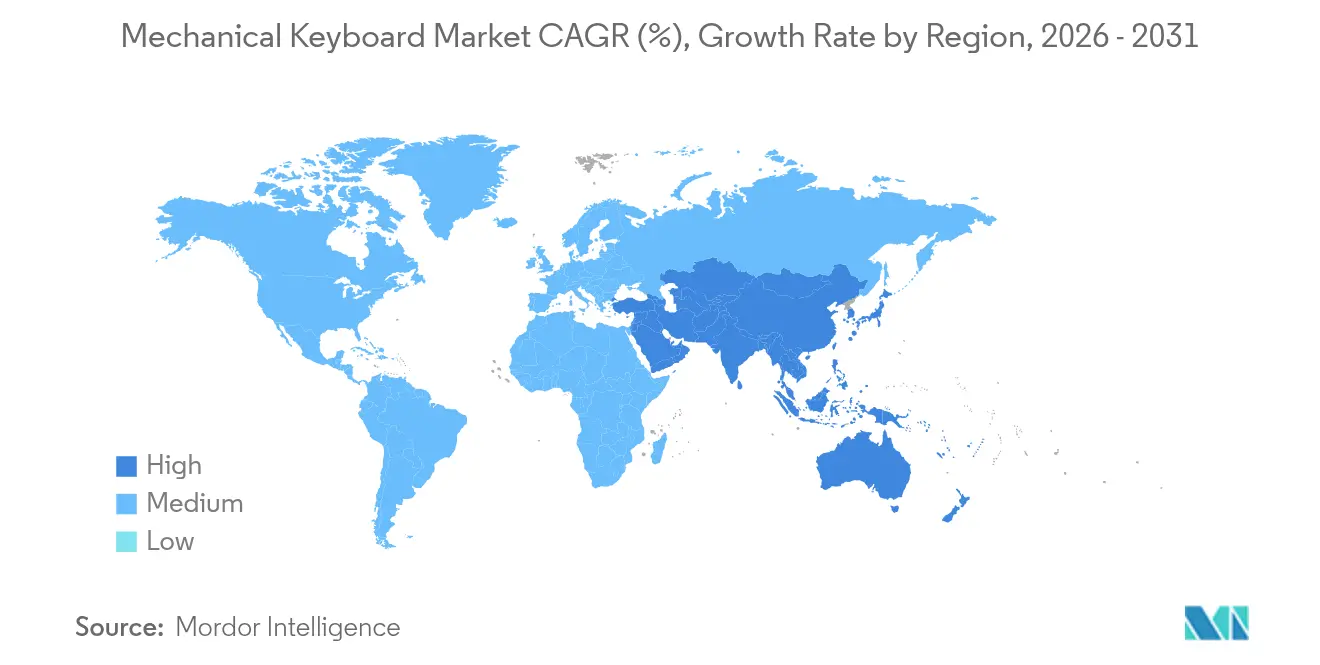

Asia-Pacific led with 38.15% revenue in 2025 and is forecast to grow at 5.96% CAGR, anchored by Guangdong’s production clusters and vibrant gaming scenes in China, Japan and South Korea. Local DIY forums translate factory proximity into rapid prototype-to-market cycles, while export-oriented brands leverage cost advantages. Regulatory uncertainties such as US tariffs, however, expose the region’s over-concentration risk.

North America trails yet enjoys high per-capita accessory spend and mature esports infrastructure. Hybrid-work upgrades propel enterprise demand for wireless ergonomic models. Tariff volatility spurs exploratory shifts to Mexican assembly, though scale remains limited. Canada sees rising enthusiast adoption fueled by cross-border e-commerce that skirts domestic distribution gaps.

Europe grows steadily under ergonomic and environmental legislation. Germany’s engineering culture and UK’s content-creator landscape support premium board sales, while Nordic countries pioneer split designs aligned with workplace wellness ethos. EU plastic waste directives pressure brands to pivot from ABS to recyclable alternatives, pushing regional differentiation in sustainable materials.

Competitive Landscape

Market concentration is moderate: global giants such as Logitech, Corsair and Razer coexist with agile specialists including Keychron, DuckyChannel and Varmilo. Logitech posted 20% year-over-year keyboard revenue growth to USD 1.1 billion in Q1 2025, reaffirming leadership. Larger vendors harness broad retail reach and proprietary software ecosystems, whereas niche entrants court enthusiasts via hot-swappable kits and crowd-funded launches.

Component makers wield strategic influence; CHERRY’s multi-technology switch portfolio enables OEM partners to refresh lines without full redesign, sustaining differentiation momentum. Supply-chain shocks encourage co-manufacturing deals outside China, yet only tier-one brands currently absorb associated costs.

Competitive tactics emphasize technology, not price: low-profile chassis, contactless switches and AI-enhanced macros headline 2025 launches. Sustainability promises an emerging battlefield as EU rules tighten. Partnerships with esports organizations and content creators remain critical brand-building levers, while B2B ergonomics contracts unlock incremental volumes.

Mechanical Keyboard Industry Leaders

Logitech International SA.

Dell Technologies Inc.

Huawei Technologies Co. Ltd.

Lenovo Group

Samsung Electronics Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: CHERRY unveiled IK inductive, MK magnetic and new MX switch families at COMPUTEX 2025, signaling a shift toward contactless and multi-sensor solutions for keyboards.

- May 2025: Corsair Gaming reported Q1 2025 net revenue of USD 369.75 million, up from USD 337.26 million in Q1 2024, with Gamer & Creator Peripherals contributing strongly.

- April 2025: Keyboardio suspended US shipments after tariffs raised costs to unsustainable levels, illustrating geopolitical exposure.

- April 2025: Logitech introduced the Logi AI Prompt Builder software alongside the Signature AI Edition Mouse, embedding generative-AI access into peripherals.

Global Mechanical Keyboard Market Report Scope

Mechanical keyboards feature individual mechanical switches for each key. Each switch consists of a keycap, a spring, and a mechanism that detects a key press when activated. Known for their tactile feedback, distinct key presses, and long-lasting durability, mechanical keyboards have established a strong presence in the market.

The study tracks the revenue accrued through the sale of mechanical keyboards by various players across the globe. it also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

The mechanical keyboard market is segmented by product type (non-tactile linear switches, tactile non-click switches, and tactile click switches), connectivity (wired and wireless), application (gaming, and office/industrial), and geography (North America, Europe, Asia Pacific, Middle East and Africa, and Latin America). The market sizes and forecasts regarding value (USD) for all the above segments are provided.

| Non-Tactile Linear Switches |

| Tactile Non-Click Switches |

| Tactile Click Switches |

| Optical and Hall-Effect Switches |

| Low-Profile Mechanical Switches |

| Wired |

| Wireless (2.4 GHz, Bluetooth, Dual-Mode) |

| Full-Size (100 %) |

| Tenkeyless (TKL, 87 %) |

| 75 % Layout |

| 65 % Layout |

| 60 % and Below |

| Ergonomic/Split |

| ABS |

| PBT (Single and Double-Shot) |

| POM and Others |

| Online (Brand E-store, Marketplaces) |

| Offline - Specialty Peripheral Stores |

| Offline - Mass Retail and Consumer Electronics Chains |

| Gaming and Esports |

| Office and Industrial |

| Programming/Developer Workstations |

| Enthusiast/DIY Modders |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Nordics | ||

| Rest of Europe | ||

| South America | Brazil | |

| Rest of South America | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Switch Type | Non-Tactile Linear Switches | ||

| Tactile Non-Click Switches | |||

| Tactile Click Switches | |||

| Optical and Hall-Effect Switches | |||

| Low-Profile Mechanical Switches | |||

| By Connectivity | Wired | ||

| Wireless (2.4 GHz, Bluetooth, Dual-Mode) | |||

| By Form Factor | Full-Size (100 %) | ||

| Tenkeyless (TKL, 87 %) | |||

| 75 % Layout | |||

| 65 % Layout | |||

| 60 % and Below | |||

| Ergonomic/Split | |||

| By Keycap Material | ABS | ||

| PBT (Single and Double-Shot) | |||

| POM and Others | |||

| By Distribution Channel | Online (Brand E-store, Marketplaces) | ||

| Offline - Specialty Peripheral Stores | |||

| Offline - Mass Retail and Consumer Electronics Chains | |||

| By Application and End-User | Gaming and Esports | ||

| Office and Industrial | |||

| Programming/Developer Workstations | |||

| Enthusiast/DIY Modders | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Nordics | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Rest of South America | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the mechanical keyboard market?

The market is worth USD 2.66 billion in 2026 and is projected to reach USD 3.43 billion by 2031.

Which switch type leads global sales?

Non-tactile linear switches dominate with 44.55% revenue share in 2025.

Why are 65% keyboards gaining popularity?

They balance compact size with functional arrow keys, supporting mobile professionals and gamers without requiring full-size desks.

How do tariffs affect mechanical keyboard availability in the United States?

Recent 45% duties forced several niche brands to suspend US shipments, highlighting supply-chain dependence on Chinese factories.

Which region grows fastest in this market?

Asia-Pacific records the highest 5.96% CAGR thanks to manufacturing concentration and vibrant gaming culture.

Are wireless keyboards suitable for esports?

Latency and battery constraints still keep top-tier players on wired models, though 2.4 GHz advances continue to narrow the gap.

Page last updated on: