Market Overview

| Study Period | 2020 - 2031 |

|---|---|

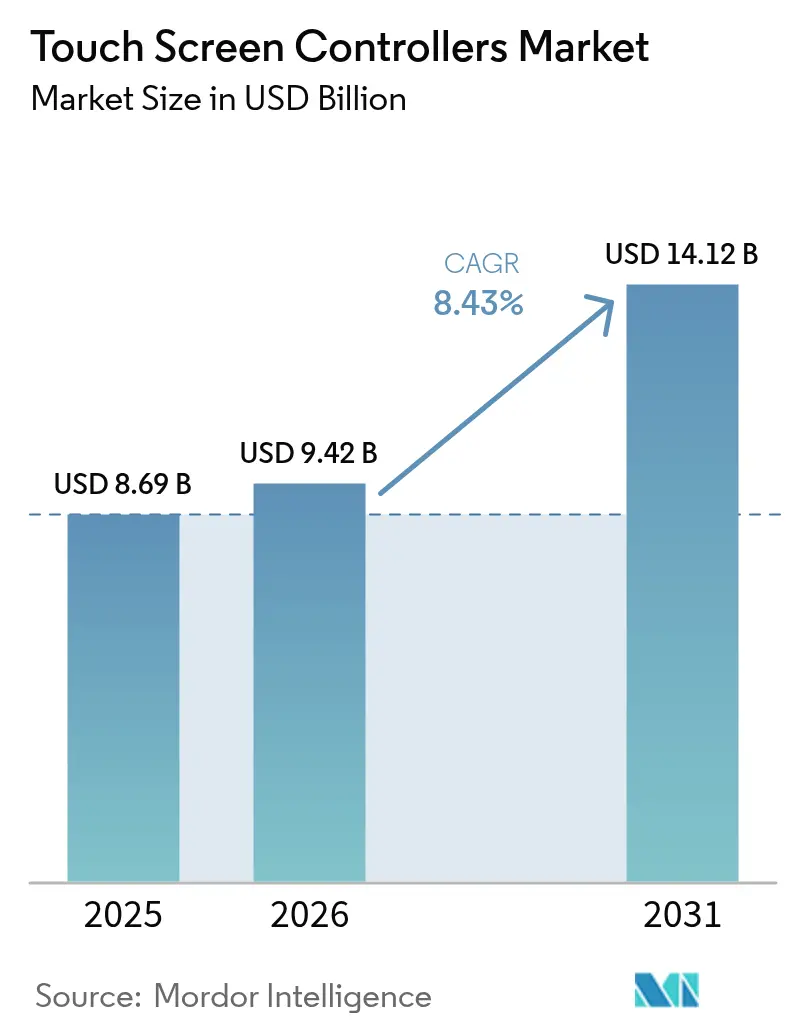

| Market Size (2026) | USD 9.42 Billion |

| Market Size (2031) | USD 14.12 Billion |

| Growth Rate (2026 - 2031) | 8.43% CAGR |

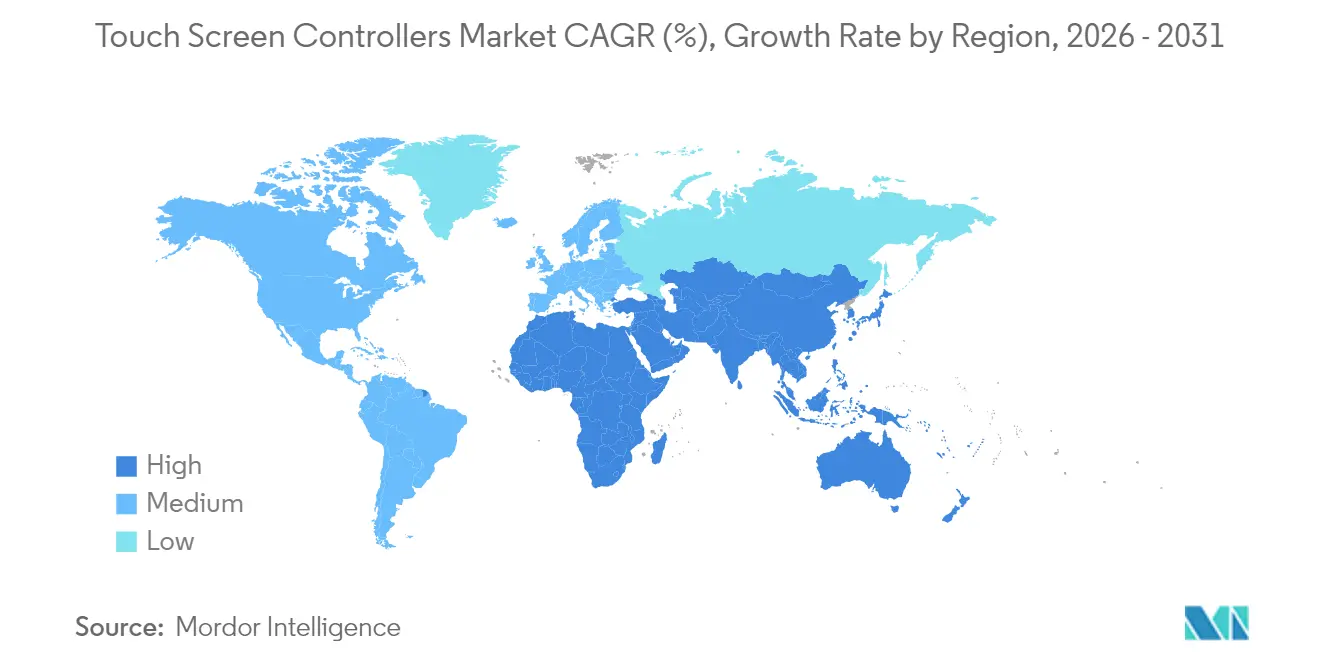

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

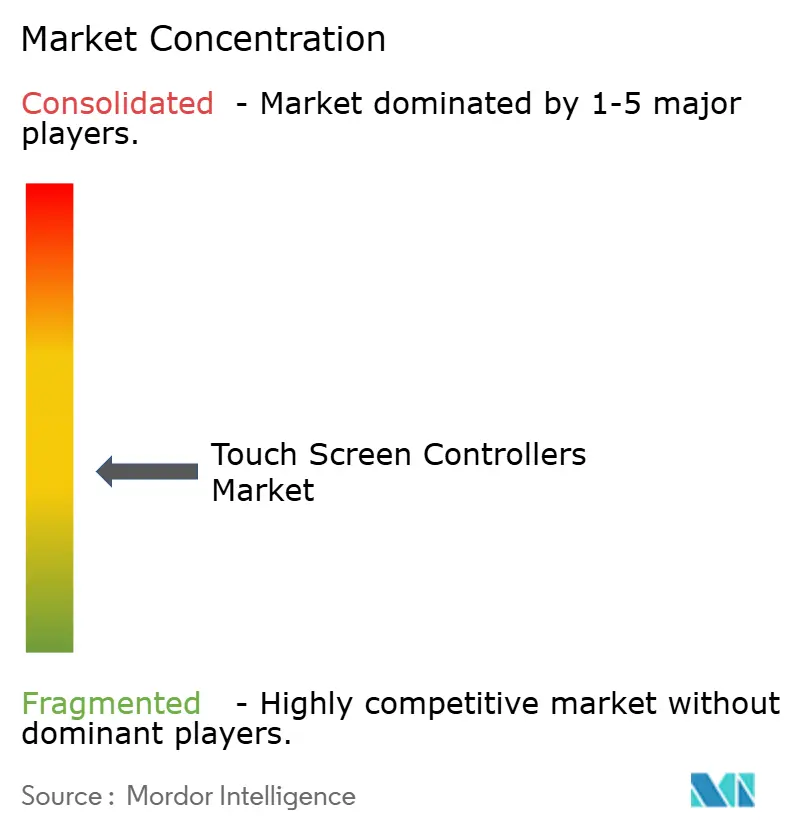

| Market Concentration | Medium |

Major Players.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Touch Screen Controllers Market Analysis by Mordor Intelligence

The touch screen controllers market size is expected to grow from USD 8.69 billion in 2025 to USD 9.42 billion in 2026 and is forecast to reach USD 14.12 billion by 2031 at 8.43% CAGR over 2026-2031. Growth is propelled by rising adoption of multi-touch interfaces in smartphones, larger in-vehicle displays, and industrial migration to projected capacitive (PCAP) panels. On the supply side, integrated touch-and-display driver ICs (TDDI) are trimming component counts and enabling thinner device profiles, while ongoing wafer-level constraints encourage premium-priced automotive and medical solutions. Demand is reinforced by retail automation, wearables that require ultra-low-power 32-bit controllers, and expanding use of flexible OLED screens that push controller algorithms toward complex edge detection and palm rejection. Regional momentum is greatest in Asia Pacific because of its dense electronics manufacturing base, with incremental opportunities building in the Middle East and Africa through smart-city projects and self-checkout deployments.

Key Report Takeaways

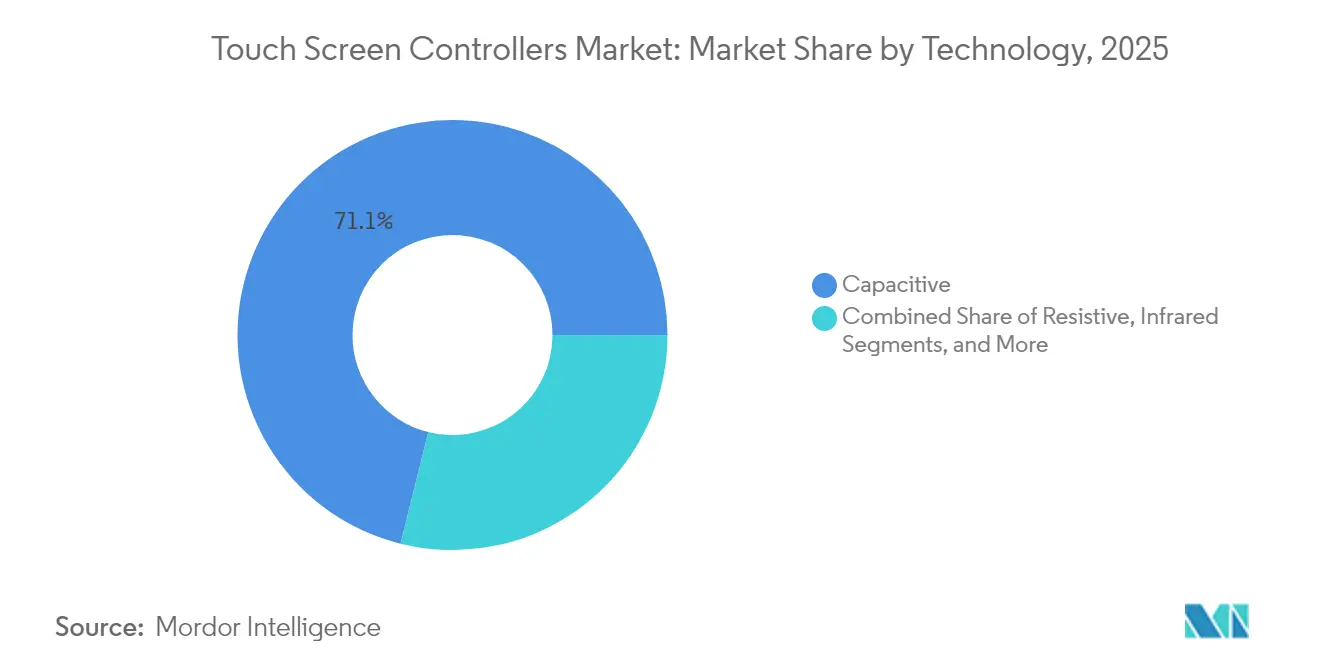

- By technology, capacitive solutions led with 71.12% of the touch screen controllers market share in 2025, whereas infrared is set for the fastest 10.45% CAGR to 2031.

- By interface, I2C held 42.65% revenue share in 2025; USB is forecast to advance at a 9.05% CAGR through 2031.

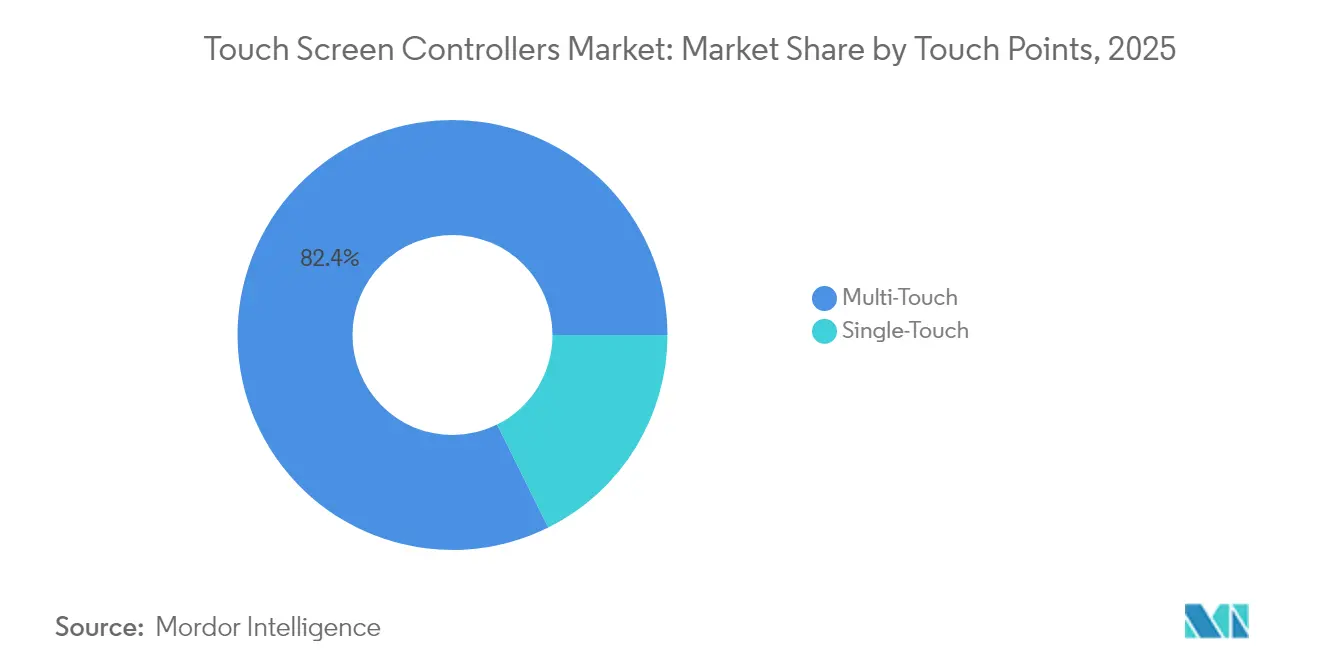

- By touch points, multi-touch accounted for 82.35% of the touch screen controllers market size in 2025, and remains on an 8.56% growth path.

- By display size, the 5–10 inch class captured 38.40% of the touch screen controllers market size in 2025, while panels above 10 inches expand at a 10.05% CAGR to 2031.

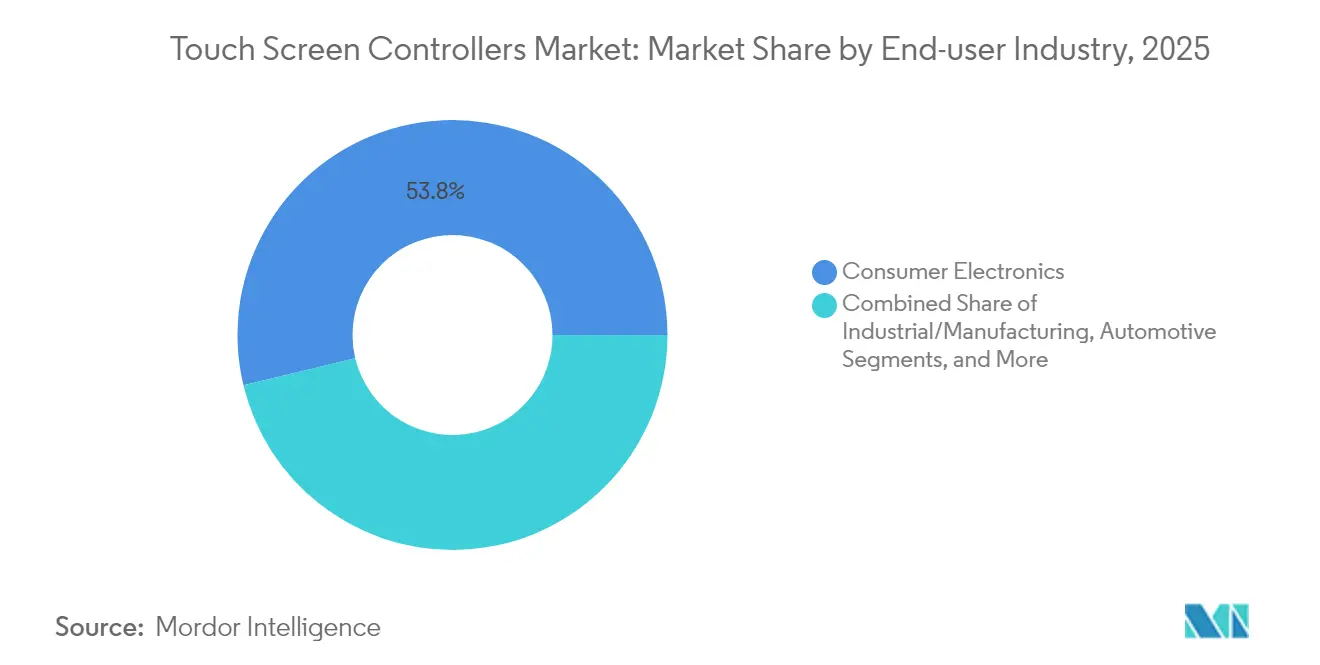

- By end-user industry, consumer electronics led with 53.75% revenue in 2025, but automotive registers the strongest 11.05% CAGR through 2031.

- By geography, Asia Pacific commanded 61.25% revenue in 2025, whereas the Middle East and Africa region is on a 10.03% CAGR trajectory to 2031.

- The top five companies together controlled 44.30% global share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Touch Screen Controllers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Multi-Touch Capacitive Adoption in Flexible OLED Smartphone Displays | +2.3% | Global, with concentration in China, South Korea, and Japan | Medium term (2-4 years) |

| In-Vehicle Infotainment Upgrades with Level-2 ADAS in Europe | +1.8% | Europe, North America, with spillover to premium segments in APAC | Medium term (2-4 years) |

| Self-Checkout POS Proliferation amid North-American Labor Shortages | +1.2% | North America, with adoption spreading to Europe and developed APAC | Short term (≤ 2 years) |

| Hand-held Medical Imaging Devices Miniaturization | +0.8% | North America, Europe, and developed APAC markets | Medium term (2-4 years) |

| Industry 4.0 Rugged PCAP Panels Replacing Membrane Keypads in China | +1.5% | Asia Pacific, primarily China, with gradual adoption in other manufacturing hubs | Medium term (2-4 years) |

| Touch-Enabled Smartwatch Shift Driving Low-Power 32-bit Controllers | +1.1% | Global, with early adoption in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Multi-touch Capacitive Adoption in Flexible OLED Smartphone Displays

Smartphone makers are stretching displays over curved edges and foldable hinges, raising complexity for touch-channel routing and palm-rejection logic. Controllers must process variable pressure inputs over irregular surfaces while minimizing parasitic capacitance. Oxide-based panels showcased in 2025 demonstrated integrated touch paths that sustain signal-to-noise ratios at narrow bezels above 90% screen-to-body levels. Patent portfolios around edge shielding and localized drive waveforms create a premium tier inside the touch screen controllers market, where suppliers monetize specialized IP against high-volume flagship handsets.

In-Vehicle Infotainment Upgrades with Level-2 ADAS in Europe

Car dashboards now host curved 34-inch panels that merge cluster, navigation, and media controls. Controllers, therefore, need wide operating temperatures, stringent EMI resilience, and fault-tolerant firmware. Devices such as the ATMXT3072M1 adopt 112 reconfigurable channels and proprietary mutual-cap acquisition schemes that raise SNR by 15 dB, ensuring reliable detection under electromagnetic stress from powertrains and ADAS radars.[1]Microchip Technology, “maXTouch Touchscreen Controllers,” microchip.com Haptic knobs embedded atop displays restore tactile feedback, improving driver attention scores and placing additional latency constraints on the controller’s scan loop.

Self-Checkout POS Proliferation amid North-American Labor Shortages

Retailers deploy high-duty-cycle kiosks that must reject liquid splashes, adapt to dynamic lighting, and safeguard payment credentials. Controllers with extended voltage drive eliminate water-induced false touches and integrate hardware crypto accelerators for secure PIN entry. The advanced PCAP 9200 series exemplifies these features and positions vendors to ride the swelling installed base of unattended checkout lanes. Volume demand for kiosks brings incremental units into the touch screen controllers market within a two-year window.

Industry 4.0 Rugged PCAP Panels Replacing Membrane Keypads in China

Factory operators migrate to glass-front PCAP screens that tolerate chemicals and glove usage. This shift expands controller unit volumes beyond consumer handhelds into production lines, pushing suppliers to build firmware that filters conductive noise from drive motors. Domestic Chinese OEMs have begun standardizing on these rugged modules, accelerating share gain for regional fabs and stimulating local tooling investments across the touch screen controllers market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 55 nm Mixed-Signal Wafer Supply-Chain Tightness | -0.7% | Global, with particular impact on Asian manufacturing | Short term (≤ 2 years) |

| EMI/ESD Compliance Issues for >24″ Capacitive Automotive Displays | -0.5% | Global automotive supply chain, primarily affecting European and North American OEMs | Medium term (2-4 years) |

| Controller-IP Litigation with Indian White-Box Tablet Makers | -0.3% | India, with potential spillover to other emerging markets | Medium term (2-4 years) |

| ASP Erosion from Panel-Maker Vertical Integration | -0.6% | Asia Pacific, primarily affecting Chinese and Taiwanese supply chains | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

55 nm Mixed-Signal Wafer Supply-Chain Tightness

Foundry allocations at key 55 nm nodes remain strained because automotive MCU and industrial IoT demand compete with consumer touch chips. Controller makers increasingly sign multi-year take-or-pay contracts to guarantee capacity, diverting working capital and elongating design cycles. Some firms are redesigning products for 65 nm or 40 nm bulk CMOS, though such porting introduces requalification costs and can raise die size. NXP’s disclosure of limited allocation windows underscores near-term supply risk across the touch screen controllers market.[2]NXP Semiconductors, “IFRS 2024 Q4,” nxp.com

EMI/ESD Compliance Issues for >24″ Capacitive Automotive Displays

Large cockpit screens magnify antenna effects that attract EMI and elevate ESD stress. Controller vendors must integrate guard channels, advanced filtering, and on-chip transient suppression, increasing the bill-of-materials and certification timelines. Synaptics markets automotive-grade solutions that address these demands through proprietary spread-spectrum drive schemes and robust shielding layouts. Compliance complexity tempers growth potential for oversized panels within the touch screen controllers market until design tools and material stacks mature.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Capacitive Dominates While Infrared Scales Up

Capacitive solutions captured 71.12% of the touch screen controllers market share in 2025, reflecting strong adoption in phones, tablets, and vehicle cockpits. Their ability to sense through cover-glass and to support ten-plus touch points secures design wins where durability, optical clarity, and gesture richness matter. The segment benefits from ongoing migration to integrated TDDI chips that lower bezel count and shrink module thickness. Conversely, resistive products continue serving glove-based factory consoles and point-of-sale terminals, though incremental volumes decline as PCAP pricing falls.

Infrared controllers post the highest 10.45% CAGR to 2031. Bezel-mounted emitter-receiver arrays let integrators scale beyond 100 inches at moderate cost, a key advantage for classrooms, digital signage, and heavy-duty kiosks. Efficiency gains in IR LED drivers combined with refined line-of-sight algorithms are reducing latency and improving ambient light immunity, prompting education boards and corporate meeting rooms to consider interactive walls. This dynamic keeps technology diversity alive inside the touch screen controllers market, encouraging vendors to maintain parallel product lines across PCAP, IR, and niche acoustic or optical imaging solutions.

By Interface: I2C Retains Lead While USB Accelerates

The I2C protocol delivered 42.65% revenue in 2025 thanks to its two-wire simplicity, low pin count, and multi-master capability, catering to system-on-chip environments. Smartphones, wearables, and many automotive displays rely on I2C for low-noise, low-power communication between the controller and host processor. SPI holds steady in panel PCs and higher-resolution tablets where bandwidth requirements rise, while UART persists in legacy industrial terminals seeking minimal firmware updates.

USB emerges as the fastest-growing at a 9.05% CAGR given its plug-and-play nature and high throughput that supports stylus data and hover sensing. ODMs targeting kiosks, medical carts, and detachable monitors appreciate the standard connector and host-agnostic enumeration process. White-box PC makers also favor USB touch due to the cost avoidance of additional bridge ICs. This interface flexibility widens application reach, adds volumes to the touch screen controllers market, and pressures vendors to supply multi-interface firmware capable of seamless field reconfiguration.

By Touch Points: Multi-Touch Sets the Experience Benchmark

Multi-touch occupied 82.35% revenue in 2025, confirming its status as a baseline expectation in interactive products. Controllers now decode 10 to 20 separate contacts with high linearity and sub-1 mm precision, empowering pinch-zoom and three-finger swipe gestures that dominate modern UX design. Industrial HMIs exploit five-finger recognition for simultaneous operability with gloves. Hover detection and pressure gradation extend capabilities, positioning high-resolution multi-touch as the standard for creative tools and automotive telematics.

Single-touch retains relevance where cost and ruggedness outweigh gesture needs. Medical infusion pumps, elevator panels, and basic thermostats often adopt single-point controllers tuned for fluid rejection and EMI immunity. Embedded firmware emphasizes consistent debounce timing rather than complex pattern recognition. This coexistence ensures the touch screen controllers market accommodates an array of price and specification brackets, supporting long-tail applications even as multi-touch growth persists.

By Display Size: Mid-Range Screens Dominate Yet Large Panels Surge

Panels measuring 5–10 inches delivered 38.40% of the touch screen controllers market size in 2025. The format balances portability and readability, serving mid-sized tablets, rugged handhelds, and infotainment head units. Designers leverage edge-to-edge glass and mini-LED backlights, which elevate EMI and thermal hurdles that controllers must resolve through adaptive drive waveforms and temperature compensation.

Displays above 10 inches register the strongest 10.05% CAGR moving toward 2031. Full-dashboard automotive screens, interactive kiosks, and collaborative flat panels demand high channel counts and robust frequency hopping to mitigate large-panel noise. Snowmobile consoles outfitted with 10.25-inch touch displays illustrate spillover into recreational vehicles, broadening applications. Below 5 inches, wearables and specialized sensors persist but cede revenue share to expanding midsize and large formats, sustaining multiple growth nodes inside the touch screen controllers market.

By End-User Industry: Consumer Electronics Tops While Automotive Gains Pace

Consumer electronics contributed 53.75% revenue in 2025, anchored by handset and tablet economies of scale. Laptop penetration is rising as OEMs introduce 2-in-1 designs with stylus input, while smartwatches ask for micro-footprint controllers drawing single-digit milliwatts in sleep mode. Tight design cycles spur demand for readily available reference boards and software toolkits.

Automotive rises fastest at 11.05% CAGR, propelled by cockpit digitization and the transition to software-defined vehicles. Large curved clusters require extended operating temperature and functional-safety diagnostics, steering controller roadmaps toward AEC-Q100 qualification. Industrial factories, healthcare devices, and retail kiosks together expand a robust second tier, where environmental robustness and regulatory compliance drive premium ASPs that cushion margin compression across the broader touch screen controllers market.

Geography Analysis

Asia Pacific held 61.25% revenue in 2025, supported by dense component supply chains, skilled labor, and government incentives for semiconductor self-sufficiency. China hosts major controller IC fabs plus downstream module assemblers that feed local smartphone and appliance giants. Regional suppliers such as FocalTech continue to innovate with integrated display-and-touch solutions that meet automotive reliability goals. South Korea and Japan contribute leading OLED and oxide TFT expertise, fueling high-value controller sockets in flexible and foldable devices.

North America ranks second, driven by platform innovation in automotive electronics, medical imaging, and industrial automation. Silicon Valley design centers emphasize AI-enhanced signal processing that filters complex noise environments. Retail chains accelerate self-checkout installations, securing additional controller unit demand. Robust cybersecurity requirements in this region elevate interest in hardware-accelerated encryption embedded within touch controllers.

Europe follows closely and relies heavily on automotive production clusters in Germany, France, and Sweden. Stringent functional-safety and electromagnetic-compatibility norms lengthen design timelines yet create defendable niches for certified suppliers. EU-wide push toward Level-2 and Level-3 ADAS drives larger cockpit displays that utilize high-channel-count controllers, enriching application diversity in the touch screen controllers market.

The Middle East and Africa region posts the fastest 10.03% CAGR through 2031. Smart-city programs in Gulf economies order touch-enabled kiosks, digital signage, and payment terminals. Retail and hospitality segments adopt interactive systems that shorten service queues. Smaller domestic integrators procure controllers via global distributors, raising local design activity.

South America shows gradual expansion, with Brazil and Argentina upgrading banking ATMs and classroom technology. Currency volatility and tariff structures influence procurement cycles, yet growing smartphone penetration nourishes aftermarket demand for repair-grade touch modules. Collective regional progress broadens the geographic footprint of the touch screen controllers market, mitigating overreliance on Asia-based output.

Regulatory Landscape

Touch screen controllers are governed primarily through electromagnetic compatibility (EMC), radio equipment, and functional-safety requirements that vary by end-use. In the United States, electronic devices that can be treated as unintentional radiators are commonly brought to market under FCC Part 15 (47 CFR), supported by lab testing and a Supplier Declaration of Conformity or certification workflow, while international EMC test practices often reference IEC 61000 immunity methods (including IEC 61000-4-2 for ESD) alongside emissions frameworks such as CISPR.

In Europe, products with wireless connectivity in the host device intersect with the Radio Equipment Directive (RED). Delegated Regulation (EU) 2026/339 entered into force in February 2026, repealing Delegated Regulation (EU) 2022/30 that was tied to RED, and shifting the compliance backdrop for software and radio-related requirements in connected devices. For higher-reliability verticals, controller vendors and OEMs typically align designs with automotive standards such as ISO 26262 (often targeting ASIL-B allocations at the system level) and CISPR-25 Class 5 emission limits for in-vehicle electronics. Appliance-oriented touch interfaces also often reference IEC/UL 60730 Class B functional-safety expectations.

Value Chain Analysis

The touch screen controller value chain runs from mixed-signal IC definition and design to wafer fabrication at mature nodes (often constrained around mixed-signal processes), followed by OSAT packaging and test and then downstream touch subsystem manufacturing. On the touch side, glass or film substrates are sourced and processed, electrodes are patterned, and the stack is laminated with OCA/LOCA before integration into a display module or device. Key commercial participants include controller IC suppliers (such as Goodix, NXP, Renesas, and Synaptics), touch-module specialists and integrators, and glass and materials suppliers such as Corning and Schott.

Downstream production and quality gates shape controller attach rates and rework costs, particularly where robust noise immunity is required. Documented practices in 2026 include tighter module QA with 100% functional touch testing using automated simulation for multi-touch accuracy and linearity, alongside industrial OEM and ODM workflows that formalize pilot runs and bill-of-materials verification to reduce material-shortage risk and batch variability. In-cell architectures that integrate electrodes into TFT backplanes to reduce thickness increase co-engineering needs between display makers and controller vendors. Bottlenecks remain tied to FPC attachment precision (ACF bonding), lamination yields, and maintaining stable touch reporting in harsh EMI environments such as automotive cockpits and factory floors.

Competitive Landscape

The touch screen controllers market displays moderate concentration. Roughly 45% revenue rested with the top five vendors in 2024, led by NXP Semiconductors, Renesas Electronics, and Synaptics. These firms leverage mixed-signal design heritage and large automotive engagement to sustain competitive moats. Mid-tier Asian companies integrate forward into display driver ICs, forming TDDI packages that cut the bill-of-materials for handset OEMs and intensify price competition in high-volume segments.

Value-chain integration is altering power dynamics. Panel makers in China and Taiwan co-develop controller silicon to retain margin amid LCD commoditization, creating cost pressure on standalone IC suppliers. In response, pure-play controller firms pivot to specialized verticals where regulatory compliance or environmental constraints elevate entry barriers. Examples include medical-grade controllers qualified under IEC 60601 or industrial parts with chemical-resistant cover-glass calibration.

Innovation is active. SigmaSense introduced ShareTouch for secure data transfer and Who Touch for personalized user recognition, exploiting advanced digital signal processing to sample full analog waveforms instead of traditional peak detection. Microchip’s knob-on-display concept embeds rotary encoders on glass, merging tactile and touch input in one module. Patent disclosures on multi-point capacitive sensing with integrated drive and readout circlets indicate continuing efforts to heighten noise immunity while shrinking die area.[4]Steven P. Hotelling et al., “US8279180B2 – Multipoint Touch Surface Controller,” google.com

Touch Screen Controllers Industry Leaders

NXP Semiconductors

STMicroelectronics

Renesas Electronic Corporation

Texas Instruments Incorporated

Microchip Technology Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Automotive cockpits and larger-format HMIs are expanding the addressable requirement set for touch controllers, which is creating demand around high-channel-count sensing, EMC robustness, and packaging that reduces board area. Microchip expanded its maXTouch M1 family in January 2026 with parts positioned for free-form widescreen displays up to 42 inches, including an ATMXT288M1 variant highlighted with a smaller PCB footprint via TFBGA packaging. This aligns directly with the report theme of larger in-vehicle displays and industrial migration to PCAP, and it highlights whitespace for suppliers that can combine high SNR sensing with automotive-grade validation and integration hooks for haptics and safety diagnostics.

IT-sized OLED touch integration is also expanding beyond smartphones, especially where active stylus support and larger touch matrices are required. In February 2026, Himax initiated mass production of its HX85200 on-cell OLED touch controller series for 13- to 16-inch laptop displays with active stylus protocol support, pointing to commercial pull for controller solutions tuned to OLED electrical noise and thin-stack integration. Separately, Goodix disclosed a flexible OLED touch controller launch (GT9926) entering commercial use in an OPPO gaming smartphone in April 2026, reinforcing ongoing opportunity for premium algorithms such as noise suppression, palm rejection, and edge handling as flexible OLED form factors increase sensing complexity. On the supply side, migration to smaller process nodes such as 40 nm HV CMOS is being cited by industry sources as a practical route to improve power efficiency while easing dependence on constrained legacy wafer capacity, which supports opportunity for vendors that can port mixed-signal touch IP without long requalification cycles in regulated end markets.

Recent Industry Developments

- April 2026: Microchip Technology announced the SAM9X75D5M hybrid MCU System-in-Package with integrated maXTouch technology for automotive HMIs. The integration pairs application processing with touch capability in a compact solution, supporting cockpit designs that prioritize reduced board space and simpler qualification for larger, feature-rich displays.

- March 2026: Cirque Corporation introduced Gen6-powered GlidePoint Circle Trackpad development kits. The kits lower prototyping friction for circular and gesture-centric touch interfaces, supporting OEM experimentation with differentiated touch input formats alongside conventional rectangular touchscreens.

- January 2026: Microchip Technology expanded the maXTouch M1 touchscreen controller series with new devices positioned for automotive OLED and microLED displays and broader display-size coverage. The release strengthens controller options for free-form and widescreen designs, aligning with the industry shift toward larger, curved in-vehicle screens that demand higher noise immunity and robust sensing.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers touch screen controller integrated circuits that process touch sensor signals and convert them into digital inputs for a connected display system across major device categories.

Scope exclusions: We exclude touch and display driver combo modules, and we also exclude legacy 4-bit resistive controller chips.

Segmentation Overview

- By Technology

- Resistive

- capacitive (Projected and Surface)

- Surface Acoustic Wave

- Infrared

- Optical Imaging

- By Interface

- I2C

- SPI

- USB

- UART

- By Touch Points

- Single-Touch

- Multi-Touch

- By Display Size

- Less than 5 Inch

- 5 - 10 Inch

- Above 10 Inch

- By End-user Industry

- Consumer Electronics

- Industrial and Manufacturing

- Healthcare and Medical Devices

- Retail and POS Terminals

- Automotive

- Banking and Financial Kiosks

- Others (Aviation, Education)

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Nordics (Denmark, Sweden, Norway, Finland)

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Southeast Asia

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East

- Gulf Cooperation Council Countries

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the basic demand and supply picture around touch-enabled devices and the controller IC value chain, before any sizing assumptions were finalized. We relied on non-paywalled sources such as USITC and UN Comtrade trade statistics, US Census and Eurostat electronics indicators, and patent databases to track filing intensity and technology directions.

To keep the model grounded, we also reviewed company filings and investor presentations, standards and guidance from bodies such as IEC and ISO (where relevant to electronics interfaces), and selected peer-reviewed journal papers on capacitive and resistive sensing. In parallel, paid subscriptions for company financials and intelligence and news and financials were used to confirm revenue splits, shipment commentary, and major product transitions without overfitting the model. These desk sources are illustrative rather than exhaustive, and we also checked additional public references for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what is actually shipped and adopted, and pressure-testing pricing and mix assumptions that are hard to observe in public datasets. We spoke with a mix of component-side stakeholders, channel participants, and device-side buyers across Americas, EMEA, and APAC, so differences in interface choices, touch points, and screen-size demand were captured.

Interview inputs were used to confirm controller attach rates in target devices, typical multi-touch requirements by use case, and the pace of technology substitution, then the numbers were reconciled back to desk indicators before final sign-off.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 12% | APAC: 42% |

| Mid tier: 45% | Functional/Unit leaders: 32% | EMEA: 35% |

| Smaller Players: 17% | Managers: 56% | Americas: 23% |

Market-Sizing & Forecasting

The sizing starts with a top-down reconstruction of the addressable controller demand pool by linking touch-enabled device shipments and installed-base refresh cycles to controller attach rates and interface-level requirements, then translating that demand into value using observed average selling price ranges. To keep the totals from being purely assumption-driven, we corroborated them with selective bottom-up approximations, including sampled supplier revenue splits, channel checks on controller ASP bands, and volume cross-checks for high-usage device categories.

Key inputs that move the model include global shipments of touch-enabled smartphones, tablets, and HMI panels, the mix shift between capacitive and resistive solutions, multi-touch adoption by end use, common interface preferences such as I2C and SPI, and screen-size mix that affects controller complexity and pricing. Where direct data was sparse, gaps were handled by using conservative ranges from interviews and then narrowing them through consistency checks against trade flows, patent trend signals, and publicly discussed design transitions.

For forecasting, scenario analysis was used and then anchored with a multivariate regression layer that links market value to device shipment growth, touch penetration in emerging applications, and the expected ASP progression as integration and node changes play out. Assumptions were kept explainable so each step can be traced back to a small set of measurable indicators.

Data Validation & Update Cycle

Outputs are checked through triangulation across independent signals, and any large variance between shipment-driven demand, pricing logic, and supplier-side commentary is flagged and reworked. Before finalization, anomalies are reviewed by another analyst who checks year-over-year movements, regional splits, and whether the implied unit economics still make sense.

If a gap cannot be explained with available evidence, re-contact is triggered with relevant interviewees and the assumption is either revised or bounded more tightly. Reports are refreshed annually, and interim updates are done when major events materially change device shipment outlooks, interface transitions, or pricing trends. Right before delivery, a fresh pass is completed so the latest public releases and market signals are reflected.

Mordor Intelligence's Touch Screen Controllers Market Market Size Compared Against Other Published Estimates

Published market sizes for touch screen controllers do not always match because the scope and the value counted can shift in small but important ways, and then the forecast math amplifies those differences over time. Common gap areas include whether the estimate tracks controller ICs only or blends in adjacent modules, how multi-touch complexity is priced, and how quickly older technologies are assumed to phase out.

Some public figures appear to include broader touch-related electronics content, and they do not clearly separate controller IC revenue from integrated touch and display driver modules. In Mordor Intelligence, value is counted only for standalone touch screen controller integrated circuits, and the totals exclude touch plus display driver combos and legacy 4-bit resistive chips, which keeps the number aligned to a repeatable device-shipment and attach-rate model.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 9.42 B (2026) | |

| Industry Research Publisher A | USD 14.10 B (2025) | The estimate is presented at a higher level with broad segment coverage, and it does not clearly state exclusions for integrated controller plus driver modules, which can inflate the value counted versus controller ICs only. |

| Global Research Publisher B | USD 11.06 B (2025) | The scope is described mainly through device applications and touch types, with limited visibility on pricing logic and whether mixed module content is removed, so ASP progression and included bill-of-material items can differ. |

Looking across the three numbers, the spread is largely explained by scope clarity and how adjacent touch electronics are treated, followed by differences in pricing build-up and the assumed speed of mix shift. By tying value to device demand signals, attach rates, and an interview-validated ASP range, the estimate stays transparent and can be replicated when new shipment or technology data comes in.

Key Questions Answered in the Report

What is the current value of the touch screen controllers market?

The touch screen controllers market is valued at USD 9.42 billion in 2026.

How fast is the touch screen controllers market expected to grow?

It is projected to expand at an 8.43% CAGR, reaching USD 14.12 billion by 2031.

Which technology holds the largest share in the touch screen controllers market?

Capacitive technology leads with 71.12% share in 2025.

Why are infrared touch controllers gaining traction?

Infrared solutions scale cost-effectively to very large screens, driving a 10.45% CAGR from 2026 to 2031.

Why are infrared touch controllers gaining traction?

Infrared solutions scale cost-effectively to very large screens, driving a 10.45% CAGR from 2026 to 2031.

What regions show the strongest growth potential?

The Middle East and Africa region is projected to record a 10.03% CAGR between 2026 and 2031, the fastest worldwide.

Page last updated on: