Light Control Switches Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

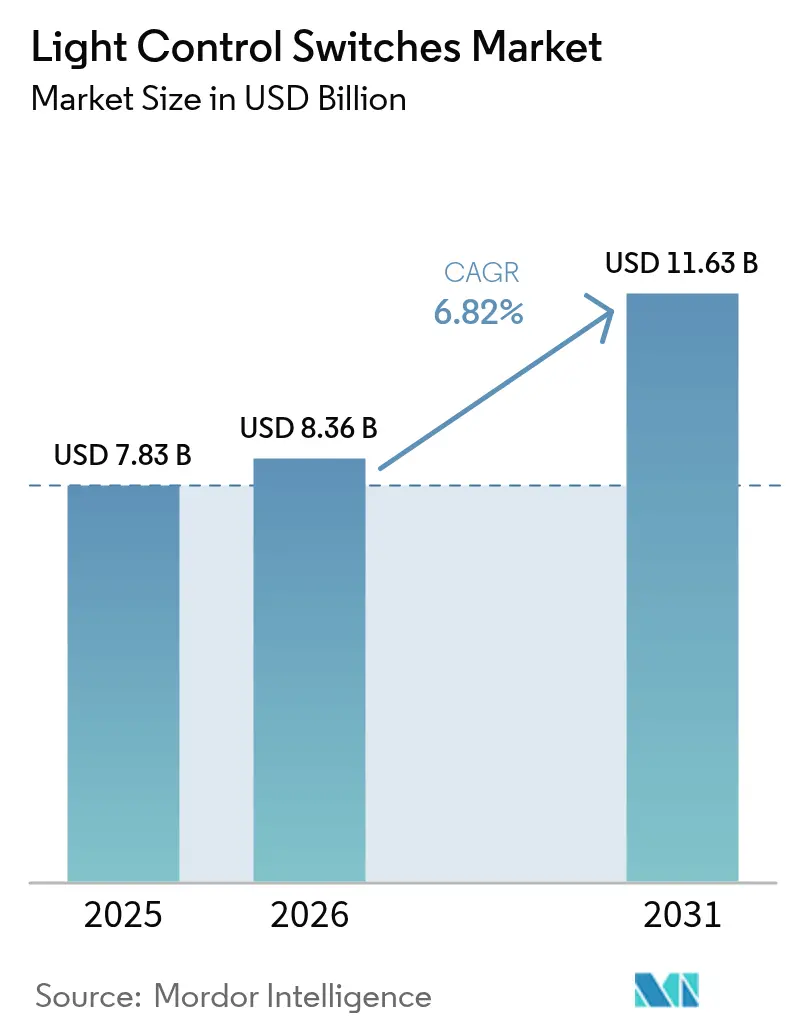

| Market Size (2026) | USD 8.36 Billion |

| Market Size (2031) | USD 11.63 Billion |

| Growth Rate (2026 - 2031) | 6.82% CAGR |

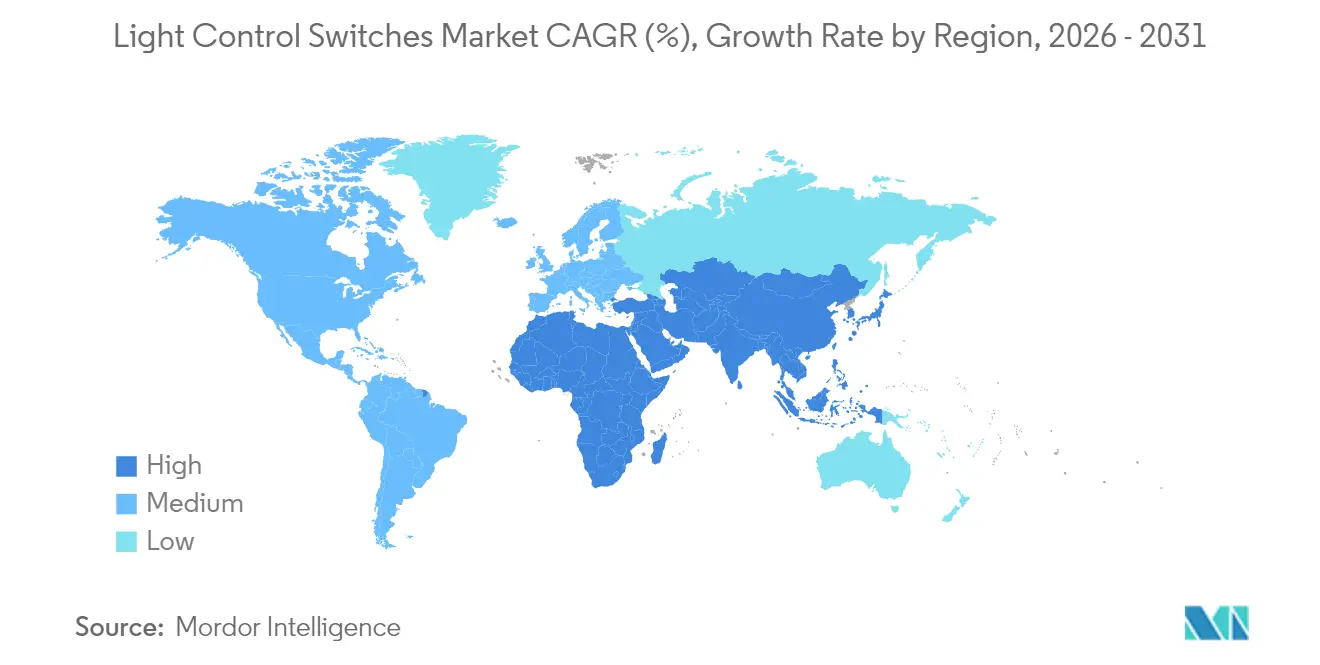

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Light Control Switches Market Analysis by Mordor Intelligence

The light control switches market size was valued at USD 7.83 billion in 2025 and estimated to grow from USD 8.36 billion in 2026 to reach USD 11.63 billion by 2031, at a CAGR of 6.82% during the forecast period (2026-2031). This rise mirrors the migration from mechanical toggles to intelligent, networked controls that sync with building-automation platforms and smart-city grids.[1]U.S. Department of Energy, “General Service Lamps,” energy.gov Mandatory efficiency rules, including the U.S. Department of Energy’s 45 lumens-per-watt requirement for general-service lamps, continue to eliminate incandescent technologies and stimulate demand for compatible digital switches.[2]U.S. Department of Energy, “Energy Conservation Standards for General Service Lamps,” federalregister.gov Asia-Pacific leads adoption on the strength of large-scale LED rollouts such as India’s UJALA program that supplied more than 366 million LED bulbs and 10 million smart streetlights. Simultaneously, Middle East and Africa posts the quickest regional growth as megaprojects like Saudi Arabia’s NEOM and the UAE-based Aion Sentia embed AI-driven lighting networks. Commercial retrofits in North America, falling wireless module prices, and growing voice-control adoption in Europe further propel market expansion.

Key Report Takeaways

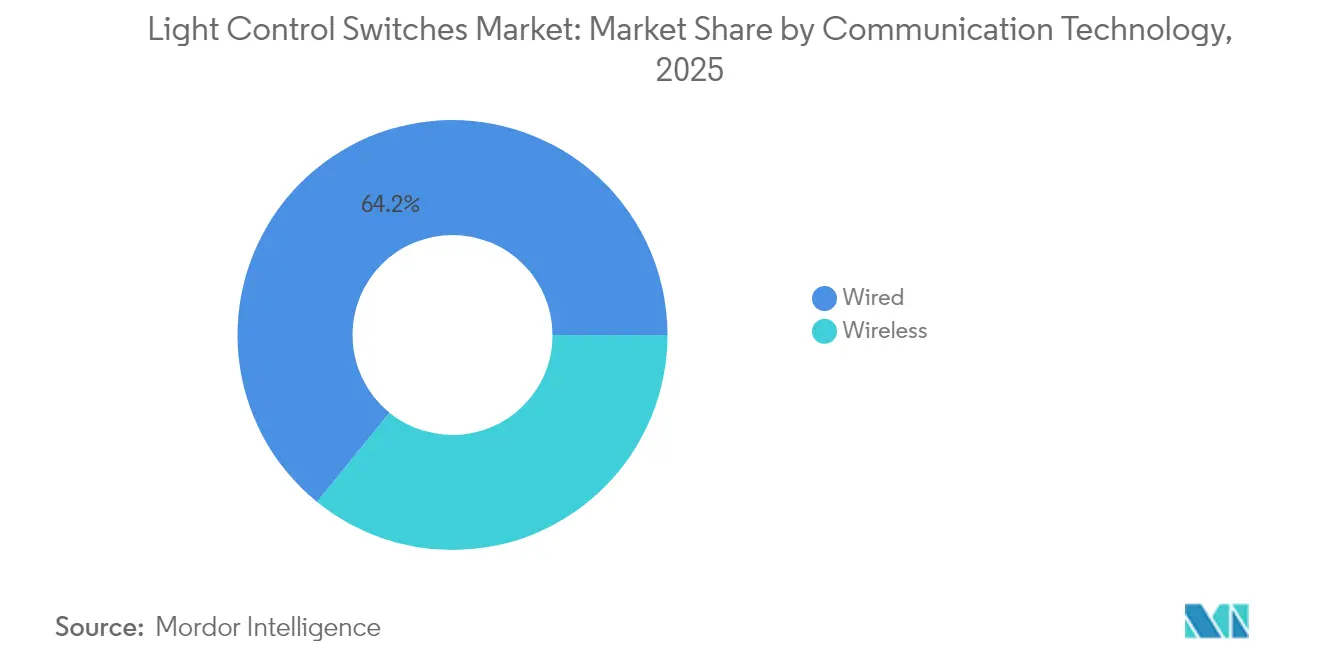

- By communication technology, wired systems held 64.15% of the light control switches market share in 2025, while wireless alternatives are projected to climb at a 10.05% CAGR through 2031.

- By switch type, mechanical toggles led with 39.15% revenue in 2025, as smart multi-function switches are forecast to expand at an 8.31% CAGR to 2031.

- By end-use sector, residential applications captured 47.35% of the light control switches market size in 2025, whereas commercial installations are advancing at a 7.51% CAGR through 2031.

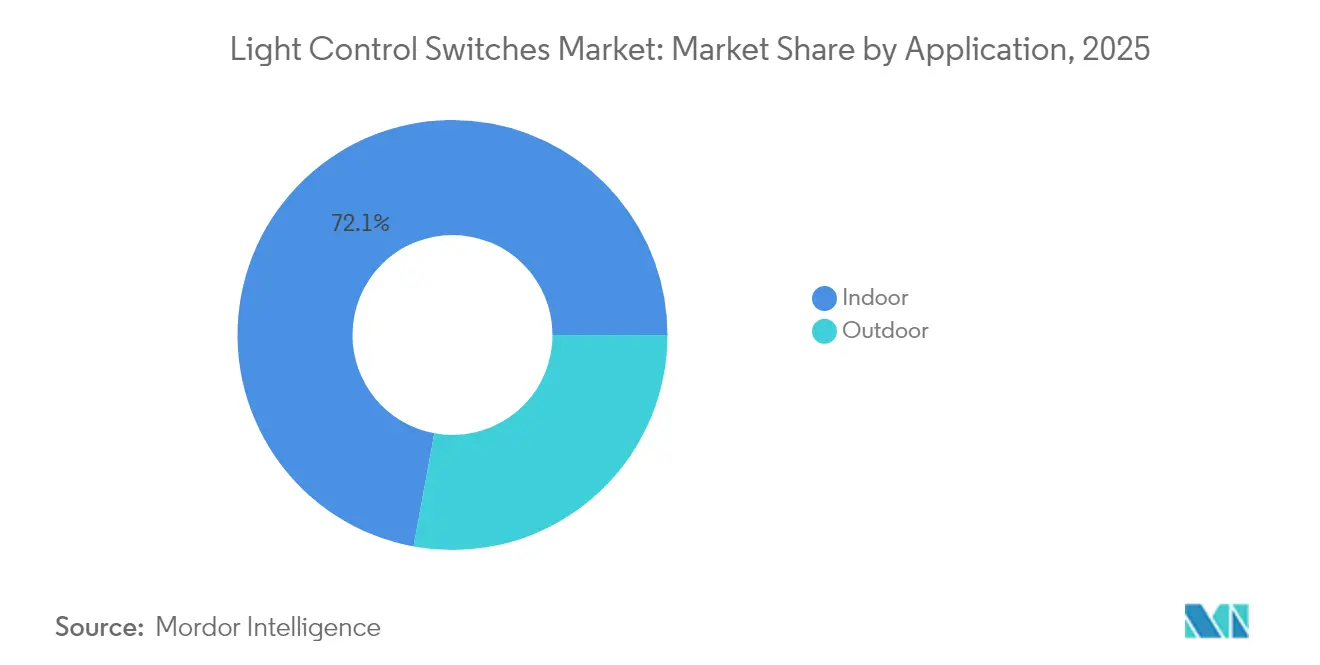

- By application, indoor installations dominated with 72.10% revenue in 2025, while outdoor lighting systems are projected to register the highest 8.09% CAGR through 2031.

- By light source, LED-based switches commanded 81.35% of 2025 sales and remain the fastest-growing category with a 6.88% CAGR forecast to 2031.

- By geography, Asia-Pacific accounted for 37.45% of 2025 revenue, and the Middle East and Africa region is set to post the fastest 7.02% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Light Control Switches Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing retrofitting of smart lighting in North-American commercial real-estate | +1.8% | North America and Europe | Medium term (2-4 years) |

| Policy-driven global phase-out of incandescent lamps accelerating switch upgrades | +1.2% | Global; strongest in developed markets | Short term (≤ 2 years) |

| IoT-enabled voice-control adoption in European residential sector | +0.9% | Europe (Germany, UK, France) | Medium term (2-4 years) |

| Energy-performance contracting in Asia-Pacific boosting adaptive lighting controls | +1.1% | Asia-Pacific core | Long term (≥ 4 years) |

| Smart-city pilot roll-outs in Middle East demanding connected street-lighting switches | +0.7% | Middle East and North Africa | Long term (≥ 4 years) |

| Falling ASP of wireless mesh modules enabling low-cost residential retrofits | +0.8% | Global; strongest in cost-sensitive markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Retrofitting of Smart Lighting in North-American Commercial Real-Estate

Commercial building owners across the United States and Canada now prioritize intelligent lighting upgrades to meet the 2022 ASHRAE 90.1 code, which makes demand-responsive controls obligatory. Energy service companies (ESCOs) bundle these upgrades into performance contracts that deliver 40-70% electricity savings and finance themselves through the avoided utility spend. California’s Title 24 continues to serve as a benchmark; property managers adopt occupancy and daylight sensors to secure compliance and utility rebates. Case evidence such as the KTRK-TV retrofit, which cut annual lighting energy by 70%, reinforces the financial logic behind replacing legacy switches. Beyond savings, new systems offer individualized scene-setting that attracts higher-paying tenants in competitive office markets.

Policy-Driven Global Phase-Out of Incandescent Lamps Accelerating Switch Upgrades

DOE enforcement of 45 lumens-per-watt standards effectively removes incandescent and most halogen lamps from U.S. shelves, compelling households to replace incompatible dimmer circuits alongside lamps. Europe experienced a similar chain reaction after its phased bans, driving a boom in LED-ready dimmers that prevent flicker and premature failure. Canada harmonized its efficiency rules with the United States in 2024, creating a contiguous North-American market for retrofit-friendly switches. The result is a synchronized replacement cycle spanning residential and commercial estates as facility managers pre-empt user complaints related to dimming incompatibility.

IoT-Enabled Voice-Control Adoption in European Residential Sector

Residential consumers increasingly view voice-controlled lighting as the easiest gateway to the broader smart-home ecosystem. Europe’s installed base of 167.7 million smart-home devices is expanding at 13.7% annually, and lighting switches are the first nodes most households deploy. Germany’s strict energy codes encourage intelligent fixtures, while the UK market benefits from near-ubiquitous Alexa and Google Assistant usage that now leverage the Matter protocol to auto-discover compatible switches. Signify, through Philips Hue, augments convenience with AI scene suggestions that interpret natural-language commands. French multi-family developers are even embedding voice-ready controls as standard amenities, citing lower maintenance overhead compared with wall-mounted scene controllers.

Energy-Performance Contracting in Asia-Pacific Boosting Adaptive Lighting Controls

Urbanization across China, India, and Southeast Asia coincides with binding efficiency targets that mandate adaptive lighting controls in new commercial space. Through ESCO contracts, building owners sidestep upfront costs and still capture 30-50% energy savings guaranteed by service providers. India’s Smart Cities Mission allocates capital to smart poles equipped with occupancy sensors and wireless nodes, strengthening domestic demand for advanced switches. Rising distributed-energy resources further heighten the value of demand-responsive lighting that can taper consumption to match rooftop-solar output or grid-price signals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Interoperability issues across Zigbee, BLE-Mesh, Thread and proprietary stacks | -1.4% | Global | Medium term (2-4 years) |

| Building-code heterogeneity in the United States inflating certification cost | -0.8% | United States and Canada | Short term (≤ 2 years) |

| Cybersecurity vulnerabilities in connected lighting networks | -0.7% | Global; heightened in critical facilities | Medium term (2-4 years) |

| Price sensitivity in developing markets limiting premium feature uptake | -0.5% | Asia-Pacific, Africa, Latin America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Interoperability Issues Across Zigbee, BLE-Mesh, Thread and Proprietary Stacks

Despite the headline promise of the Matter standard, professional integrators still report site delays when devices from multiple protocols coexist. Field tests show that mixed-stack networks often require additional hubs, raising cost and complexity.[3]Theodoros Spyridopoulos, “Investigating Radio Frequency Vulnerabilities…,” mdpi.com Security researchers have demonstrated replay attacks that override encryption on Zigbee lighting nodes, underscoring that protocol diversity can also widen the attack surface. End users confronted with confusing setup flows tend to revert to simple on-off solutions, slowing smart-switch penetration in both residential and small-commercial properties.

Building-Code Heterogeneity in the United States Inflating Certification Cost

Manufacturers supplying the light control switches market face a checkerboard of state-level energy codes. California’s Title 24 demands advanced demand-response capability; numerous other jurisdictions still adhere to IECC 2021’s more modest sensor requirements. Achieving compliance across this mosaic can cost more than USD 100,000 per product family due to duplicated testing and documentation.[4]Lutron Electronics, “0-10 V Dimmer Sensor APP NOTE,” lutron.com Smaller firms frequently delay U.S. launches or restrict catalogs to one region, reducing competitive pressure and innovation velocity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Communication Technology: Wireless Protocols Gain Despite Reliability Concerns

Wired architectures controlled 64.15% of the light control switches market in 2025, a testament to the commercial sector’s preference for deterministic performance where lighting downtime equates to safety or revenue risk. However, the wireless cohort is advancing at a 10.05% CAGR as silicon costs fall and mesh algorithms improve resilience. Inside residential projects, Bluetooth Low-Energy Mesh eliminates gateway hardware, offering a streamlined retrofit path attractive to DIY consumers.

Early adopters in hospitality and retail increasingly rely on Thread and Zigbee nodes that auto-commission via Matter, shaving hours off installation labor. Meanwhile, Wi-Fi switches retain a niche in environments where existing access points provide power and backhaul, though higher standby draw still discourages broad deployment. Proprietary sub-GHz solutions remain common in stadium lighting and campus projects where long-range links and battery-free wall stations improve ROI. Heightened cybersecurity attention is spurring vendors to bundle over-the-air key rotation and zero-trust provisioning, signaling that security will be a core purchasing criterion through the forecast horizon.

By Switch Type: Smart Multi-Function Devices Transform User Experience

Mechanical toggles accounted for 39.15% of light control switches market revenue in 2025, showing resilience in cost-driven retrofits where the existing wiring supports only two-wire circuits. Yet smart multi-function models are expanding at an 8.31% CAGR as updated codes require integrated occupancy sensing and demand-response signals that mechanical products cannot deliver. Dimming units keep steady volume, but manufacturers increasingly embed microcontrollers that auto-adapt to constant-current LED drivers, averting flicker complaints common in earlier retrofit waves.

Premium projects now specify capacitive touch plates with scene presets, color-temperature tuning, and short-range voice pickup. Occupancy-based devices featuring dual-element PIR and microphonic detection attain higher accuracy and avoid nuisance activations in open offices. Research into kinetic-energy harvesting promises battery-free, wireless wall controls that can lower retrofit installation costs by 50%, a proposition especially compelling for multifamily housing stock built before conduit requirements. The future roadmap points to switches evolving into edge controllers that locally process sensor data and expose APIs to building-management systems.

By End-Use Sector: Commercial Growth Outpaces Residential Adoption

Residential projects delivered 47.35% of 2025 revenue, underpinned by widespread smart-speaker ownership and the simplicity of plug-and-play switch replacements. Commercial demand is forecast to rise 7.51% annually through 2031 as ESCO-financed retrofits scale across office, healthcare, and education estates. C-PACE financing further accelerates uptake by allowing building owners to amortize upgrades via property-tax assessments that transfer on sale.

Distribution centers and manufacturing plants increasingly specify ruggedized smart switches paired with high-bay LED fixtures to capture energy savings without compromising safety in high-ceiling environments. Municipal infrastructure, exemplified by New York’s program to network 500,000 streetlights, is driving volume in utility-grade controllers that double as sensor gateways. This public-sector push enhances vendor credibility and catalyzes private-sector adoption.

By Application: Outdoor Lighting Controls Surge Through Smart City Initiatives

Indoor suites-spanning homes, offices, factories-still captured 72.10% of 2025 spending, yet outdoor deployments now post an 8.09% CAGR as cities invest in adaptive roadway, façade, and park illumination. Dubai’s early smart-pole deployments illustrated a 25% electricity cut within the first month, providing a showcase for neighboring jurisdictions. AI-enabled controllers that modulate brightness by traffic and weather have been rolled out across 800 North American municipalities, demonstrating scalability.

Sports venues experiment with ultra-responsive DMX-over-IP switches that coordinate light shows with broadcast graphics. Architectural lighting designers employ dynamic color-tuning to elevate urban identity while still meeting strict nighttime luminance caps. The intersection of 5G radios and edge processors integrated into streetlight enclosures lays groundwork for ancillary services including air-quality monitoring and public Wi-Fi.

By Light Source: LED Dominance Drives Control System Evolution

LED technology represented 81.35% of lamps controlled by switches in 2025 and will expand at 6.88% CAGR through 2031. As legacy fluorescent and HID volumes decline, switch makers prioritize deep-dimming performance, flicker mitigation, and driver-level data feedback. Digital drivers facilitate color-temperature tuning and circadian-support profiles now requested in corporate wellness programs.

Embedded sensors in LED fixtures convert every luminaire into a network node transmitting occupancy, temperature, or asset-tracking signals over power-line or wireless links. Li-Fi pilots that piggyback broadband data on visible-light frequencies illustrate future convergence between illumination and communications infrastructure. The net effect is that control intelligence migrates from wall boxes to distributed drivers, reshaping product design and software-integration requirements.

Geography Analysis

Asia-Pacific possessed 37.45% of 2025 revenue, with China’s mandatory adaptive-lighting code and India’s Smart Cities Mission anchoring demand for sophisticated switches. National utility programs that bulk-procure LED lamps create a downstream ecosystem for interoperable dimmers and sensors. Rapid urbanization across Vietnam, Indonesia, and the Philippines further widens the addressable base, although cost sensitivity in these economies occasionally curbs uptake of premium multi-function units.

North America retains a prominent role thanks to stringent building codes, strong rebate frameworks, and mature ESCO financing models that de-risk investment. Ongoing retrofits guided by ASHRAE 90.1 and the constant tightening of Title 24 sustain momentum. Research and pilot projects-including battery-free kinetic switches developed at the University of Alberta-keep the region at the forefront of technology breakthroughs.

The Middle East and Africa generate the strongest 7.02% CAGR as governments allocate multibillion-dollar budgets to build AI-enhanced cities. The UAE-based Aion Sentia and Saudi Arabia’s NEOM showcase large-scale deployments where lighting networks tie into district-wide digital twins that predict energy loads. Off-grid solar streetlight programs in sub-Saharan Africa employ adaptive dimming to stretch battery life, underscoring the region’s unique intersection of electrification and efficiency targets.

Regulatory Landscape

Energy and electrical-safety codes are tightening the compliance envelope for light control switches as regions push higher-efficiency lighting and more granular control strategies. In the United States, the National Electrical Code (NEC) update for 2026 reorganizes requirements for device-type switches, including dimmers and electronic control switches, by moving them from Article 404 to Article 406 (Part III), influencing installation and inspection practices across jurisdictions that adopt the new edition. In parallel, ANSI/ASHRAE/IES Standard 90.1-2025 incorporates updated mandatory lighting-control strategies and refined power density limits, reinforcing demand-response capable and sensor-integrated controls in commercial projects.

Standards and qualification programs are also shaping product design toward connected, interoperable controls. The DesignLights Consortium began accepting applications for SSL Technical Requirements Version 6.0 on January 5, 2026, adding a control options table that affects rebate eligibility for products with integrated controls. In Europe, Regulation (EU) 2024/1781 (Ecodesign for Sustainable Products Regulation, ESPR) sets a transition period through December 31, 2026 for electrical equipment still under the earlier Ecodesign Directive framework, while IEC work such as prEN IEC 60669-2-1:2026 updates requirements for electronic control devices with HBES/BACS integration considerations. For North American product certification, UL 20/CSA C22.2 No. 111 updates for general-use snap switches move toward an effective date of January 31, 2027, adding requirements that affect modular devices such as occupancy sensors and dimmers.

Value Chain Analysis

The value chain covers raw materials and electromechanical parts, electronics design, high-volume assembly, certification, and multi-channel distribution. Upstream inputs include copper and engineered plastics for housings and contacts, plus semiconductors and passives for dimmers, touch interfaces, and connected switches. Manufacturing is heavily concentrated in Asia for cost-competitive mechanical components and contract electronics assembly, while higher value-add sits in firmware, connectivity stacks (for example, Wi-Fi, Zigbee, Thread, BLE mesh), and application-layer integration with building automation and smart-home ecosystems.

Key constraints and risk points include availability and lead times for chips used in wireless modules and control ICs, along with exposure to specialty materials that touch the broader lighting supply chain. China export controls on certain rare earths used in phosphors and related lighting components have been cited as a source of supply uncertainty, contributing to cost volatility that can ripple into switch and control system BOMs. To manage this, suppliers and OEMs are diversifying production footprints toward Southeast Asia and India, adjusting inventory policies for critical electronics, and emphasizing platform interoperability and cybersecurity features to protect margins as channels shift toward retrofit-led replacement cycles across residential and commercial estates.

Competitive Landscape

The light control switches market remains moderately fragmented. Global electrical majors such as Signify, Legrand, Lutron, and Acuity Brands compete alongside IoT specialists and semiconductor providers supplying connectivity chipsets. Acuity’s USD 1.215 billion purchase of QSC broadens its Intelligent Spaces Group into audio, video, and control domains, indicating a strategy of full-stack platform ownership. Signify pairs its Philips Hue line with AI-driven scene-generation software, reinforcing the race to differentiate through services rather than hardware.

Private-equity activity underscores the segment’s attraction: Kingswood Capital merged Kichler and Progress Lighting under the new Coleto Brands umbrella after USD 256 million in acquisitions, targeting synergies in residential channels. Patent disputes, such as Signify’s infringement case against Nanoleaf on RF communication and color-mixing, highlight intensifying competition to control intellectual property.

Cybersecurity capability emerges as a white-space differentiator. Pacific Northwest National Laboratory cataloged 57 threat vectors against connected lighting, most aimed at management software rather than the fixture itselfv. Vendors are responding with local-processing architectures that minimize cloud exposure, positioning security as a purchase-decision lever comparable to energy performance.

Light Control Switches Industry Leaders

Signify BV

Legrand SA

Leviton Manufacturing Company Inc.

Lutron electronics co., Inc.

Eaton Corporation PLC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Rebate and building-performance programs are creating near-term whitespace for networked lighting controls (NLC) that demonstrate interoperability and integrated building benefits beyond lighting energy savings. The DesignLights Consortium released NLC V5.2 requirements in June 2026, with an effective date of August 3, 2026, and the update raises the bar on interoperability while adding thermostat-enabled HVAC integration, which expands the addressable scope for switch vendors that can package lighting control with building-management interfaces. On the codes side, ANSI/ASHRAE/IES Standard 90.1-2025 increases the intensity of mandatory control strategies in commercial buildings, supporting demand for occupancy/vacancy sensing, daylighting control, and demand-response capable devices tied to building automation.

Product and compliance roadmaps also open room for differentiated offerings in smart safety, measurement, and edge intelligence. UL 60335-2-107:2026 introduces RF immunity and thermal runaway tests for smart lighting with an effective date of December 1, 2026, pushing manufacturers toward more robust wireless and thermal designs aimed at enterprise and critical-facility buyers. In parallel, published real-world validation of embedded AI control approaches (for example, office tests demonstrating measurable energy savings from adaptive control on embedded hardware) supports a shift toward switches and controllers that process sensor data locally and coordinate with HVAC via BACnet-compatible building systems. Regionally, Japan METI draft revisions tied to the Energy Conservation Act (released in July 2026) point to a compliance-driven need for smart lighting products that can transmit real-time power data for labeling and monitoring, aligning opportunities with metering-aware switches and integrated energy-management bundles.

Recent Industry Developments

- June 2026: Signify expanded the Philips Hue portfolio with new wired switch products, including a wired on/off switch, wired dimmer switch, and a wired wall switch module for smart control of traditional lighting circuits. The broadened Hue line takes in in-wall control points beyond lamps and wireless accessories, supporting retrofit adoption while strengthening platform positioning at the switch level.

- February 2026: Leviton partnered with Sonos to integrate the Decora Smart Wi-Fi Scene Controller Switch with Sonos audio systems, enabling combined wall control for lighting and music. This frames scene controllers as multi-function home interfaces and differentiates them against standalone smart switches through shared use cases.

- June 2025: Mouser introduced MEAN WELL Matter-ready wireless LED drivers aimed at smart-home integrators. Wider availability of Matter-aligned drivers supports end-to-end compatibility across lamps, drivers, and wall controls, reducing integration friction for switch makers targeting retrofit and new-build smart lighting projects.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue from light control switches used to turn lights on or off, dim, and manage lighting circuits in indoor and outdoor settings across residential, commercial, industrial, and public infrastructure use.

Scope exclusions: We exclude full lighting control systems, luminaires, lamps, and building management software unless they are sold as part of the switch product value.

Segmentation Overview

- By Communication Technology

- Wired

- Wireless

- Proprietary RF

- Zigbee

- Bluetooth Low-Energy Mesh

- Wi-Fi

- Z-Wave

- Thread

- By Switch Type

- Mechanical On/Off Toggle

- Dimmer

- Touch-based capacitive

- Occupancy/Vacancy Sensor

- Smart/Connected Multi-Function

- By End-Use Sector

- Residential

- Commercial

- Industrial

- Public Infrastructure and Utilities

- By Application

- Indoor

- Residential Indoor

- Commercial Indoor

- Industrial Indoor

- Outdoor

- Street and Roadway

- Architectural and Facade

- Sports and Stadium

- Indoor

- By Light Source

- Incandescent

- Fluorescent

- Light-Emitting Diode (LED)

- Other Sources (HID, Halogen)

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Nordics

- Rest of Europe

- South America

- Brazil

- Rest of South America

- Asia-Pacific

- China

- Japan

- India

- South-East Asia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Gulf Cooperation Council Countries

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with mapping where demand comes from, and how much hardware is typically installed per building area or per project type. We used public sources such as the US Energy Information Administration, US Census construction and housing data, Eurostat building indicators, UN Comtrade trade statistics, and IEA energy efficiency publications to anchor activity levels and adoption signals.

Next, supply and pricing context is built using company annual reports, investor presentations, product catalogs, and reputable press coverage on wiring devices and smart home penetration. Where needed, we also referenced paid subscriptions for company financials and intelligence, patent databases, and an import or export shipment-level database to sanity check product flow and pricing direction. These desk sources are illustrative, and other public documents were used to collect data, validate assumptions, and clarify gaps.

Primary Interviews and Surveys

Primary work was used to stress test assumptions that are not visible in public data, especially channel pricing, mix shifts between mechanical switches and dimmers, and the pace of wireless adoption in retrofit projects. We spoke with manufacturers, distributors, electrical contractors, and large facility and project stakeholders across major regions, so the final sizing reflects how buying decisions and installations typically happen.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 12% | APAC: 45% |

| Mid tier: 48% | Functional/Unit leaders: 38% | EMEA: 29% |

| Smaller Players: 14% | Managers: 50% | Americas: 26% |

Market-Sizing & Forecasting

The core model is built using a top-down approach where construction activity, renovation intensity, and building stock upgrades are reconstructed into an addressable switch demand pool, which is then converted into value using region-wise average selling prices. To keep totals realistic, we corroborate the result with selective bottom-up checks, such as sampled supplier revenue splits, distributor channel checks, and a volume times ASP cross-check for a few representative countries.

Key inputs used in the model include building starts and completions, renovation spend direction, electrification and energy efficiency policy signals, indoor versus outdoor lighting upgrade rates, wireless penetration in retrofit jobs, and the mix shift between standard on or off switches and dimming or touch controls. Forecasting is run using scenario analysis, since the market is sensitive to construction cycles and retrofit incentives, and the scenarios are aligned to what interviewees expect for pricing, mix, and project timing. Where bottom-up information is missing for smaller countries, gaps are handled by proxying per-capita building activity and applying validated mix assumptions from comparable markets.

Data Validation & Update Cycle

Outputs are checked against independent signals such as construction indicators, import and export trends, and reported revenue direction in wiring devices, and then variances are investigated before internal sign-off. When a country result looks unusual, we revisit the underlying drivers, re-check price logic, and re-contact sources if the gap cannot be explained by mix or timing.

Reports are refreshed annually, and interim updates are made when material events change demand, pricing, or regulation. Before delivery, an analyst performs a fresh pass across the model and key assumptions so clients receive the latest updated view.

Mordor Intelligence's Light Control Switches Market Size Compared Against Other Published Estimates

Published market values for light control switches can differ because the counted product boundary is not always the same, and because pricing and exchange rate choices move the headline number even when unit demand looks similar. We keep the scope centered on switch hardware value, and we also watch how retrofit and new-build cycles shift the mix across regions.

Key gaps usually come from whether sources blend in broader lighting control systems, how they treat wired versus wireless products, and how they step up ASPs over time when smart features rise. A further driver is refresh timing. Using a different currency conversion month, and not re-checking prices against channel feedback, can change the USD total. This is why refresh cadence and validation checks were emphasized in Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 8.36 B (2026) | |

| Trade Journal A | USD 7.82 B (2024) | Uses an earlier base year and a faster near-term growth frame, and the scope appears to be broader in places, which can blend adjacent lighting control products and inflate unit assumptions versus pure switch value. |

| Industry Portal B | USD 7.59 B (2021) | Relies on an older base year, with limited visibility on how ASP progression and currency timing were handled across regions, which can compress the starting value and create a different long-range path. |

Across the three figures, the spread is mainly explained by base-year choice, scope edges around control systems, and how pricing and FX are updated through the forecast. By keeping inputs tied to observable construction and retrofit indicators, and then validating pricing and mix through interviews, our estimate stays traceable to steps that can be repeated each year.

Key Questions Answered in the Report

What is the current size of the light control switches market?

The light control switches market size stands at USD 8.36 billion in 2026 and is projected to reach USD 11.63 billion by 2031.

Which region leads the light control switches market?

Asia-Pacific holds the largest 37.45% revenue share due to government-backed LED programs and smart-city investments.

How fast are wireless lighting controls growing?

Wireless solutions are expanding at a 10.05% CAGR as component prices fall and Matter improves device interoperability.

Why are commercial buildings adopting smart switches rapidly?

Performance-based ESCO contracts guarantee energy savings of 40-70%, making smart switches a financially attractive retrofit.

What are the main barriers to market growth?

Protocol-level interoperability issues and varied U.S. building codes raise integration and certification costs for manufacturers.

Which companies are most active in strategic acquisitions?

Acuity Brands, Signify, and Kingswood Capital have led recent deals, using acquisitions to build platform depth and channel reach.

Page last updated on: