Meat, Poultry & Seafood Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

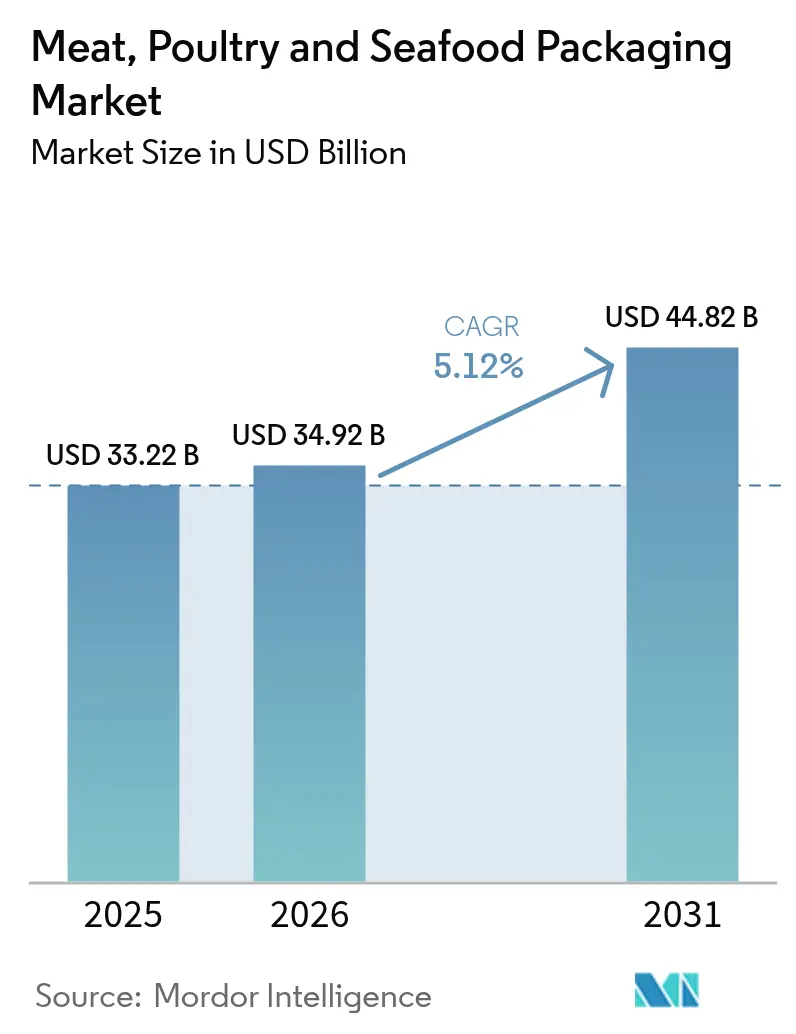

| Market Size (2026) | USD 34.92 Billion |

| Market Size (2031) | USD 44.82 Billion |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Meat, Poultry & Seafood Packaging Market Analysis by Mordor Intelligence

The meat, poultry and seafood packaging market size was valued at USD 33.22 billion in 2025 and estimated to grow from USD 34.92 billion in 2026 to reach USD 44.82 billion by 2031, at a CAGR of 5.12% during the forecast period (2026-2031). Global appetite for animal protein keeps rising, and processors are turning to advanced materials and automation to protect margins while complying with ever-stricter food-safety and environmental rules. Flexible formats, mono-material developments, and smart labels are now standard considerations at every plant retrofit or greenfield project. Labor shortages intensify capital spending on robotics, and regulatory convergence across the European Union, Japan, and North America is encouraging harmonized designs that travel smoothly across borders. Sustainability ambitions are steering purchasing away from multi-layer laminates toward recyclable or compostable constructions, yet cost volatility in polymers and metals continues to squeeze profitability for converters and brand owners alike.

Key Report Takeaways

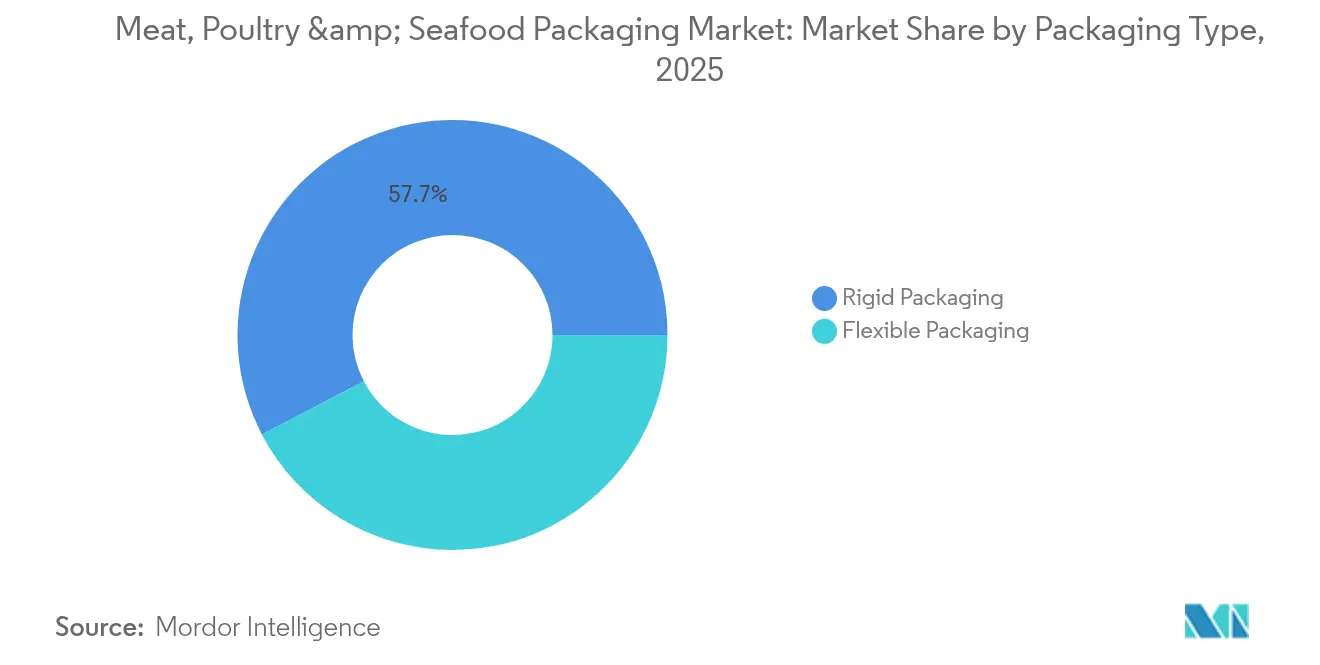

- By packaging type, flexible solutions held 42.35% of the meat, poultry, and seafood packaging market share in 2025, while rigid alternatives lagged but remained essential for portion-controlled SKUs.

- By product type, coated films commanded 36.12% revenue share in 2025; pre-made bags and pouches are forecast to expand at a 4.73% CAGR through 2031.

- By material type, polypropylene accounted for 50.85% of the meat, poultry and seafood packaging market size in 2025, whereas polyester is poised for the fastest 5.41% CAGR to 2031.

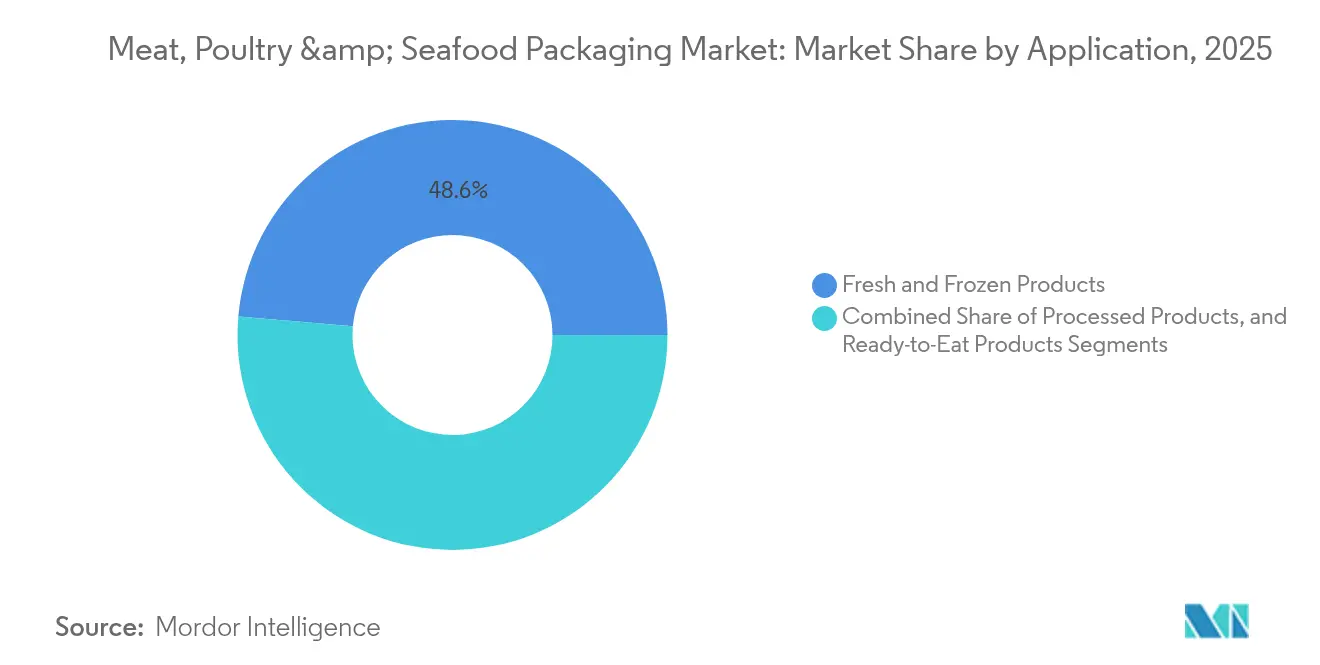

- By application, fresh and frozen items represented 48.62% of 2025 demand; ready-to-eat formats are advancing at a 5.19% CAGR.

- By technology, modified-atmosphere formats led with 44.30% revenue share in 2025, and active or intelligent formats are set to grow at 5.22% through 2031.

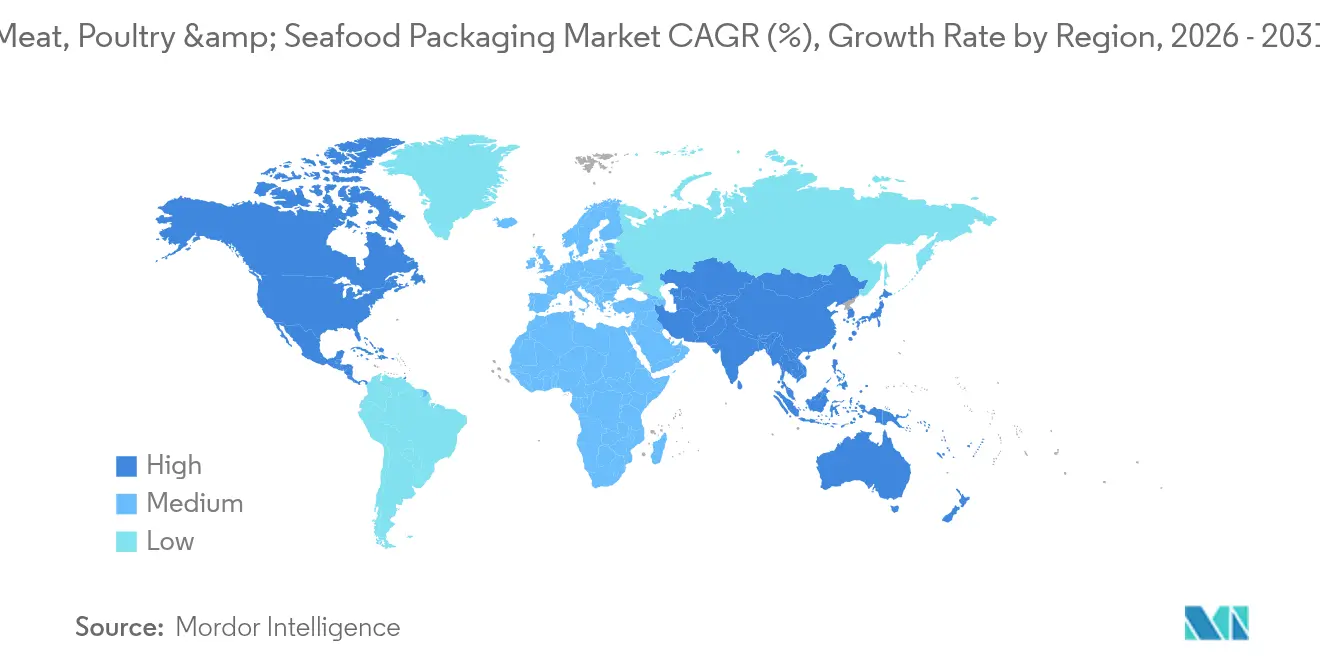

- By geography, Asia-Pacific captured 34.32% market share in 2025 and is projected to rise at a 5.92% CAGR thanks to booming e-commerce and rising disposable incomes.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Meat, Poultry & Seafood Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging global per-capita protein consumption | +1.2% | Global, with Asia-Pacific leading growth | Medium term (2-4 years) |

| Growing stringency of food-safety and labelling legislation | +0.8% | North America and EU, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Retail migration to case-ready and high-throughput tray systems | +0.9% | North America and Europe primarily | Medium term (2-4 years) |

| Rise of direct-to-consumer chilled-meal e-commerce channels | +0.7% | Global urban centers, Asia-Pacific acceleration | Short term (≤ 2 years) |

| Adoption of mono-material films to hit recyclability targets | +0.6% | EU leading, North America following | Long term (≥ 4 years) |

| Automation demand from labour-short meat-processing plants | +1.1% | North America and Europe primarily | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Global Per-Capita Protein Consumption

Rapid income growth across Asia and urbanization in Africa are keeping meat, poultry, and seafood demand high even as alternative proteins enter mainstream discussion. Higher cold-chain penetration enables retailers to extend distribution into once-inaccessible hinterlands, amplifying packaging unit volumes. Processors race to secure materials that prevent drip loss and color shift because quality lapses translate directly into brand erosion. Meanwhile, premiumization in mature markets prompts retailers to specify high-clarity vacuum skin formats that showcase marbling and freshness. As consumption accelerates, the meat, poultry, and seafood packaging market must balance throughput with shelf-life performance, and suppliers that can validate barrier claims quickly win specifications.

Growing Stringency of Food-Safety and Labeling Legislation

Japan’s positive-list system, effective June 2025, narrows acceptable resins to 21 families and 827 additives, forcing converters to validate every input against a common global library. In Europe, the Packaging and Packaging Waste Regulation bans PFAS and mandates recyclability by 2030, reshaping material road maps for global suppliers. North American retailers pre-emptively align SKUs to meet these same criteria to avoid costly pack revisions later. Uniform rules also reduce testing duplication, letting multinationals scale one compliant structure across continents. The meat, poultry, and seafood packaging market, therefore, sees faster roll-outs of mono-material solutions as legal uncertainty fades.

Retail Migration to Case-Ready and High-Throughput Tray Systems

Supermarkets increasingly eliminate in-store butchery to cut labor and cross-contamination risk. Case-ready lines use modified-atmosphere trays and lidding films that extend shelf life by up to seven days compared with over-the-counter options[1]Tyson Fresh Meats, “Case-Ready Efficiency Metrics,” tysonfoods.com. Younger shoppers accept bar-coded packs that provide traceability and allow self-checkout. Tray sealers now exceed 120 packs per minute, driving demand for films with precise thickness tolerances and easy- peel seals that survive distribution shocks. This trend enlarges the meat, poultry and seafood packaging market as each primal can be divided into more individual portions, raising pack counts.

Automation Demand from Labor-Short Meat-Processing Plants

Fifty-six percent of processors still struggle to recruit staff, so collaborative robots now conduct repetitive tasks such as placement, weighing, and sealing. To prevent machine jams, film friction and flex-crack properties receive unprecedented scrutiny during specification. JBS Prepared Foods invested USD 200 million in a Missouri site that runs automated guided vehicles and smart conveyors, validating the business case for end-to-end automation. As throughput climbs, predictive maintenance sensors on sealing jaws signal operators before failures can trigger downtime. Suppliers able to bundle films, equipment, and on-site service gain share within the meat, poultry and seafood packaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile polymer and aluminium input prices | -0.9% | Global, with North America most exposed | Short term (≤ 2 years) |

| Food-contact compliance hurdles for recycled plastics | -0.5% | EU and North America primarily | Medium term (2-4 years) |

| Accelerating EPS and multi-layer laminate bans | -0.4% | EU leading, expanding globally | Long term (≥ 4 years) |

| Long-term volume risk from alt-protein penetration | -0.3% | Developed markets primarily | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Polymer and Aluminium Input Prices

Resin tariffs scheduled for 2025 could lift North American polypropylene and polyethylene costs by 12-20%, forcing converters to pass on surcharges or redesign packs. Aluminum premiums may double to 50%, pressuring suppliers of foil lidding and retortable cans. Dynamic pricing clauses are becoming standard in converter contracts, signaling structural rather than temporary volatility. Smaller regional firms without hedging instruments face margin erosion that leads to consolidation. This cost turbulence caps near-term profitability for the meat, poultry and seafood packaging market and tempers capital spending on novel lines.

Food-Contact Compliance Hurdles for Recycled Plastics

Circular-economy pledges hinge on food-grade recycled content, yet migration protocols require exhaustive challenge-testing that can exceed six months per SKU. Approvals are slower for multi-layer laminates, nudging suppliers toward single-polymer films that fit existing disinfection processes. Early adopters must fund high sampling volumes, adding up-front expense before scale benefits emerge. Until recyclate validation pipelines accelerate, virgin resins will remain dominant, limiting immediate CO₂ reduction within the meat, poultry and seafood packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Type: Flexible Solutions Drive Automation Integration

Flexible formats contributed USD 14,068.67 million to the meat, poultry and seafood packaging market size in 2025 and are forecast to climb at a 4.22% CAGR through 2031. Gravure-printed barrier flow wraps protect fresh poultry on high-speed lines while reducing pack weight by up to 75% compared with rigid trays. Processors value the cube efficiency that enables more packs per pallet, easing freight cost pressure. Consumer preference studies also reveal that clear stand-up pouches help shoppers quickly check product quality, reinforcing trust at the point of sale.

Rigid trays and tubs still dominate bulk club formats because they stack well in distribution, but upcoming bans on expanded polystyrene accelerate trials of bio-based options such as sugar-cane molded pulp. Sealed Air’s compostable tray maintains the stiffness needed for robotic pick-and-place while meeting ASTM D6400 requirements. The segment’s resilience therefore hinges on updating material recipes rather than defending outdated substrates. By 2031, multi-material barrier trays will likely migrate to mono-PET cousins that align with deposit-return systems in Europe, anchoring their relevance within the broader meat, poultry and seafood packaging market.

By Product Type: Pre-Made Solutions Accelerate Growth

Coated films generated the largest slice of the meat, poultry and seafood packaging market share at 36.12% in 2025, underpinning modified-atmosphere and vacuum skin packs that appear in chilled cabinets worldwide. These films incorporate EVOH or silicon oxide layers to curb oxygen ingress below 0.1 cc/m²/day, safeguarding color retention on beef rib-eye cuts for up to 28 days. Rising e-commerce volumes are, however, tilting momentum toward pre-made bags and pouches, which are forecast to record the briskest 4.73% CAGR through 2031.

Warehouse pickers favor gusseted pouches because their uniform shape avoids miscounts during automated induction. Brand owners exploit the larger printable area to relay cooking instructions and QR codes that trace farms of origin. Food cans, although mature, enjoy renewed stocking in emergency kits, and containers remain vital in institutional catering. Across formats, specification choices concentrate on drop-strength ratings and puncture resistance to withstand robotic depalletizing, keeping performance metrics central to competition within the meat, poultry and seafood packaging market.

By Material Type: Polyester Gains Momentum

Polypropylene’s 50.85% slice of the meat, poultry and seafood packaging market size in 2025 stems from its favorable stiffness-to-weight ratio and hermetic sealing on vertical form-fill-seal lines. Processors appreciate the resin’s high heat-deflection temperature, which tolerates microwave reheating without distortion. Nevertheless, polyester films are accelerating at a 5.41% CAGR because their intrinsic barrier and recycling pedigree align with new European Commission rules.

Recyclers now accept PET/PE mono-structures that bypass delamination steps, shortening reprocessing cycles and cutting Scope 3 emissions. In contrast, polystyrene usage is sliding because legislative calendars in France, Spain, and Germany include explicit bans on foam meat trays. Thermoform-grade PVC/PET co-extrusions persist for premium smoked salmon extensions requiring crystal-clear windows. Aluminum lidding commands niche share for long-shelf-life tuna salads that travel lengthy export routes. Bio-based PLA and PHA resins are debuting in low-acid charcuterie wraps, hinting at future diversification but not yet scaling materially within the meat, poultry and seafood packaging market.

By Application: Ready-to-Eat Segment Accelerates

Fresh and frozen proteins, covering chilled chicken breasts, whole turkeys, and IQF shrimp, account for 48.62% of demand, reflecting legacy eating habits. Their unit volumes remain large, yet growth plateaus as consumers pivot toward ready-to-eat items that remove kitchen prep time. The convenience cohort is forecast to expand at 5.19% through 2031, making it the fastest-moving target audience for pack developers.

Single-serve trays with built-in absorbent pads now reach school canteens and workplace cafeterias, cutting plate waste while meeting portion-control guidelines. Processed meats, such as deli turkey slices, keep steady traction thanks to sandwich culture in North America and Europe. In each sub-application, pack-design variables including oxygen transmission rate, microwave resistance, and easy-open tear lines determine material choice, anchoring differentiation inside the meat, poultry and seafood packaging market.

By Packaging Technology: Intelligence Integration Advances

Modified-atmosphere formats secured 44.30% of sector revenue in 2025, leveraging nitrogen and carbon-dioxide blends to slow microbial growth. Gas-flushed poultry packs lengthen shelf life to 14 days, saving retailers expiration-related shrink. Vacuum and vacuum skin technologies sit right behind, prized for their craft-butcher aesthetics and negligible headspace.

Active and intelligent systems are projected to outpace all peers at 5.22% CAGR. Time-temperature indicators now cost less than USD 0.02 per unit and integrate into label stock, allowing supply-chain partners to reject compromised cartons before customer complaints arise. NFC tags on salmon fillets feed inventory software in real time, improving demand planning. These smart layers transform the meat, poultry and seafood packaging market from passive containment to data-enabled quality assurance.

Geography Analysis

Asia-Pacific led with a 34.32% stake in the meat, poultry and seafood packaging market share during 2025 and maintains the highest 5.92% CAGR outlook to 2031. Rising middle-class incomes in China and Southeast Asia elevate per-capita meat intake, and omnichannel retail booms in urban clusters where same-day chilled delivery requires robust packs. China’s state-backed labs are already experimenting with rice-based scaffolds for cultured meat, calling for ultra-low-migration pouches that satisfy both biotech purity standards and consumer sensory expectations.

North America remains a technology bellwether even as growth moderates. Tariffs on resins and metals could lift input costs sharply, so converters explore lightweight films to preserve gross margin. Mexico’s growing cluster of flexible plants supplies both US grocers and domestic supermarkets, leveraging near-shoring strategies that cut shipping emissions. Regional processors also respond to labor shortages by pairing collaborative robots with vision-guided tray sealers, reinforcing equipment-driven purchases in the meat, poultry and seafood packaging market.

Europe pushes sustainability boundaries through the Packaging and Packaging Waste Regulation, which bans PFAS and demands recyclability. Multinationals pilot chemically recycled polyamide shields for high-barrier beef mince bags, a project led by Südpack, BASF, and Werz. Deposit-return systems for PET trays launch in Germany in 2026, spurring design-for-recycling among exporters aiming to retain shelf presence. Middle East and Africa along with South America register rising protein uptake, yet infrastructure gaps cap refrigerated penetration. Investments in cold-chain corridors are, however, narrowing that deficit, signaling upside for packaging suppliers willing to extend credit to local converters in the meat, poultry and seafood packaging market.

Competitive Landscape

The meat, poultry and seafood packaging market shows moderate concentration. Sealed Air, Amcor, Mondi, and Sonoco all command notable shares through end-to-end material plus equipment portfolios. These firms differentiate by bundling onsite technicians with film rollouts, a service increasingly valued as automation narrows tolerance windows. Sealed Air offers whole-line validation that reduces commissioning times by 20%, giving processors faster payback when labor is scarce.

Consolidation is accelerating. The pending Amcor-Berry Global all-stock merger would create a behemoth with complementary footprints across North America, Europe, and Asia, trimming freight miles from multipoint customer networks. Sonoco’s USD 3.9 billion acquisition of Eviosys brings metal packaging expertise into its broader mix, widening cross-selling opportunities to seafood canners. Coveris focuses on mono-material PE/EVOH pouches, while Tetra Pak adapts retort cartons for shelf-stable soups containing shredded chicken indicating the trend towards niche challengers gravitate toward specialty lanes for enhanced opprtunities.

Technology remains the fiercest battlefront. Mondi has scaled paper-based thermoformable webs that claim a 70% fiber content yet seal at existing line speeds, catering to grocers that want plastic reduction but not throughput loss. Graphic Packaging invests in grease-resistant barrier boards for oven-ready wings. Data-enabled packaging also gains ground as the market vendors such as WestRock through its EverGrow platform embeds sensors that monitor CO₂ build-up, alerting distributors before spoilage. Competitive intensity therefore stems from who delivers verifiable sustainability alongside line efficiency, positioning integrated innovators to capture rising volumes in the meat, poultry and seafood packaging market.

Meat, Poultry & Seafood Packaging Industry Leaders

Berry Global

Mondi Group

Sealed Air

Amcor

Sonoco

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Crown Holdings reported Q1 2025 net sales of USD 2,887 million with efficiency gains in North American food cans

- April 2025: Südpack, BASF, and Werz introduced chemically recycled meat packs supporting circularity goals.

- March 2025: Brazil approved Japanese inspection missions for meat plants, opening new export channels.

- January 2025: Südpack launched recyclable low-carbon flowpacks for fresh pasta, a format transferable to deli meats.

Global Meat, Poultry & Seafood Packaging Market Report Scope

Packaging plays an important role in preserving the meat and extending its shelf-life. The meat can be compromised without packaging as it is contaminated by direct contact with chemical, physical, and biological contaminants.

The meat, poultry & seafood packaging market is segmented by packaging type (flexible and rigid), product type (containers (aluminum foil container, plastic container, and board container), pre-made bags, food cans, coated films, and other product types), material type (polypropylene (PP), polystyrene (PS), polyester (PET) thermoform, and aluminum), application (fresh and frozen products, processed products, and ready-to-eat products), and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa).

The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

| Rigid Packaging |

| Flexible Packaging |

| Containers |

| Pre-made Bags and Pouches |

| Food Cans |

| Coated Films |

| Other Product Types |

| Polypropylene (PP) |

| Polystyrene (PS) |

| Polyester (PET) |

| Thermoform-grade PVC/PET |

| Aluminium |

| Other Material types |

| Fresh and Frozen Products |

| Processed Products |

| Ready-to-Eat Products |

| Vacuum Packaging (VP) |

| Modified-Atmosphere Packaging (MAP) |

| Vacuum-Skin Packaging (VSP) |

| Active and Intelligent Packaging |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordics | ||

| Rest of Europe | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| By Packaging Type | Rigid Packaging | ||

| Flexible Packaging | |||

| By Product Type | Containers | ||

| Pre-made Bags and Pouches | |||

| Food Cans | |||

| Coated Films | |||

| Other Product Types | |||

| By Material Type | Polypropylene (PP) | ||

| Polystyrene (PS) | |||

| Polyester (PET) | |||

| Thermoform-grade PVC/PET | |||

| Aluminium | |||

| Other Material types | |||

| By Application | Fresh and Frozen Products | ||

| Processed Products | |||

| Ready-to-Eat Products | |||

| By Packaging Technology | Vacuum Packaging (VP) | ||

| Modified-Atmosphere Packaging (MAP) | |||

| Vacuum-Skin Packaging (VSP) | |||

| Active and Intelligent Packaging | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Nordics | |||

| Rest of Europe | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| ASEAN | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia-Pacific | |||

Key Questions Answered in the Report

What is the current value of the meat, poultry and seafood packaging market?

The market is valued at USD 34,920.86 million in 2026.

How fast is the meat, poultry and seafood packaging market expected to grow?

It is forecast to expand at a 5.12% CAGR, reaching USD 44,824.21 million by 2031.

Which packaging type holds the largest share?

Flexible formats lead with 42.35% of market share, supported by their compatibility with high-speed lines.

Which region exhibits the strongest growth outlook?

Asia-Pacific commands the highest 5.92% CAGR to 2031 thanks to rising protein demand and e-commerce penetration.

Page last updated on: