Poultry Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.82 Billion |

| Market Size (2031) | USD 4.79 Billion |

| Growth Rate (2026 - 2031) | 4.64% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

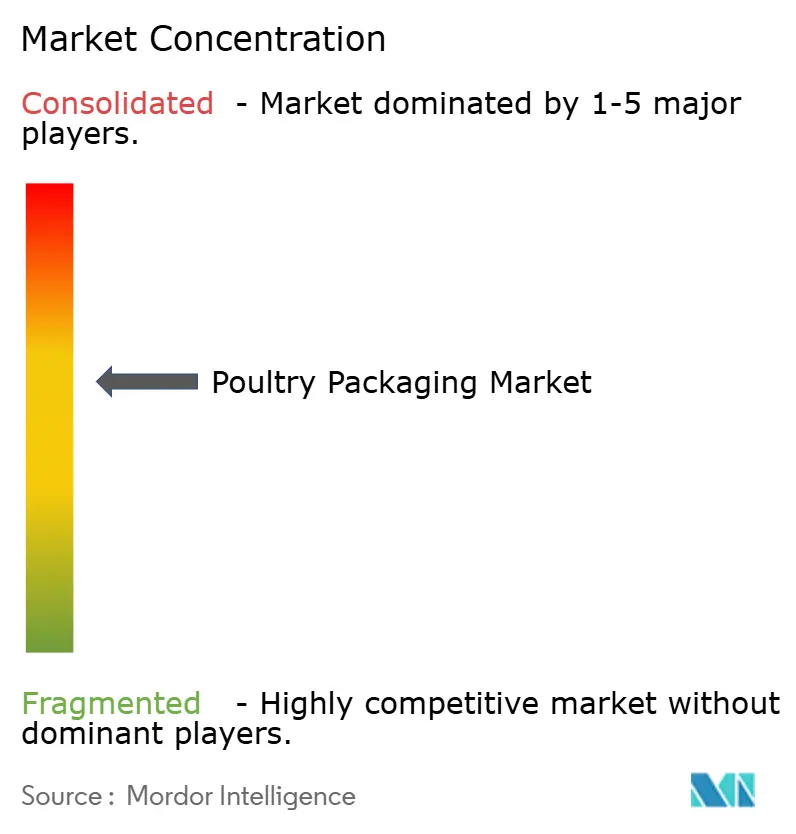

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Poultry Packaging Market Analysis by Mordor Intelligence

The poultry packaging market size is expected to grow from USD 3.65 billion in 2025 to USD 3.82 billion in 2026 and is forecast to reach USD 4.79 billion by 2031 at 4.64% CAGR over 2026-2031. Rising demand for case-ready poultry, new modified-atmosphere solutions, and sustainability regulations underpin this steady growth. Retailers prefer shelf-stable chicken trays that reduce shrink and labor. E-commerce adds volume for insulated formats that survive multi-day transit. Material shifts toward paper-based laminates press producers to innovate barrier layers without losing throughput. Meanwhile, merger activity is altering bargaining power between converters and processors, and technology firms are embedding sensors that warn of temperature abuse at every link in the chain.

Key Report Takeaways

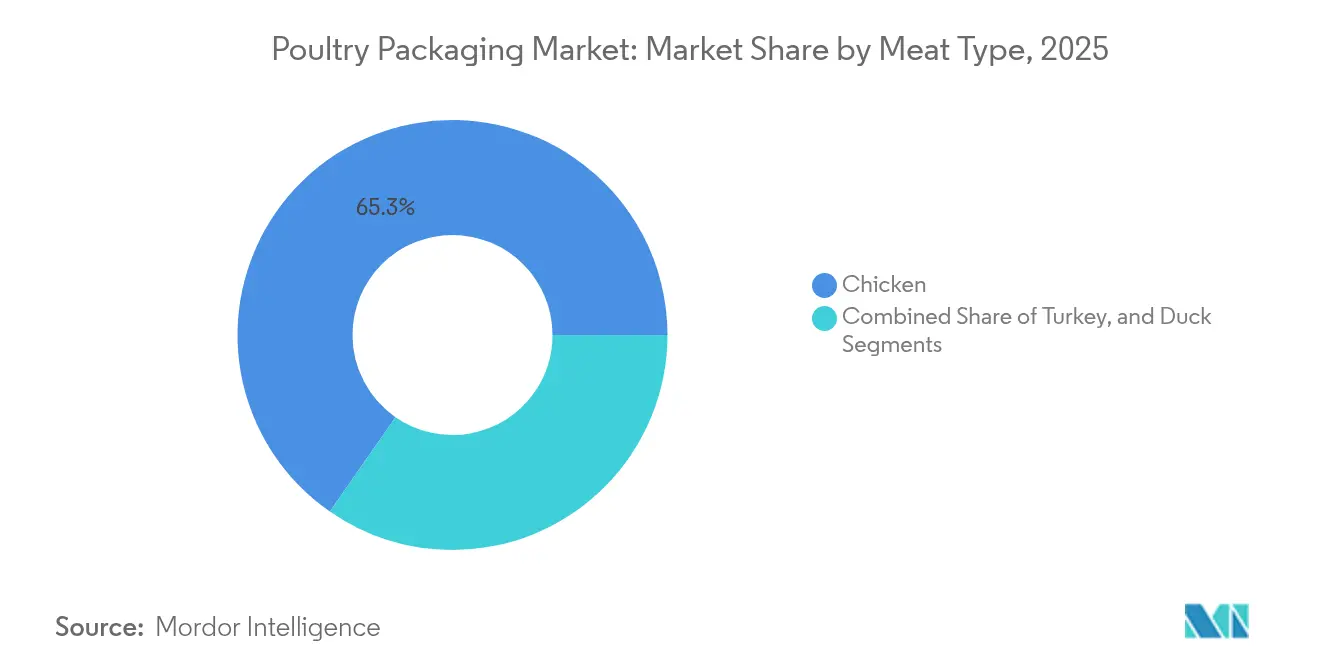

- By meat type, chicken led with 65.34% poultry packaging market share in 2025, while duck is projected to expand at a 5.45% CAGR to 2031.

- By packaging format, flexible solutions commanded 62.45% of the poultry packaging market size in 2025; the same format is forecast to grow at 5.27% through 2031.

- By material, plastics retained 67.02% share of the poultry packaging market size in 2025, whereas paper and paperboard is expected to post the fastest 5.31% CAGR to 2031.

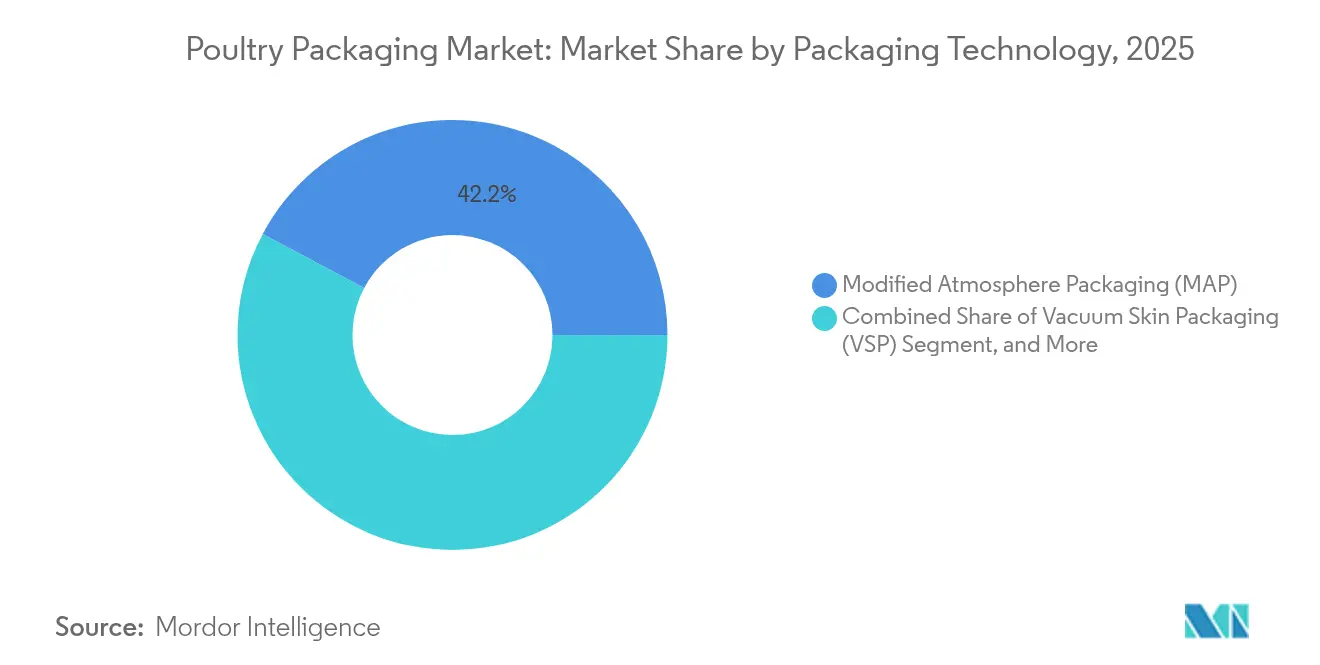

- By packaging technology, modified-atmosphere systems accounted for 42.21% of the poultry packaging market size in 2025; active and intelligent formats are set to advance at 5.18% CAGR.

- By distribution channel, retail captured 56.98% share of the poultry packaging market in 2025, while e-commerce retail is projected to grow at 5.14% through 2031.

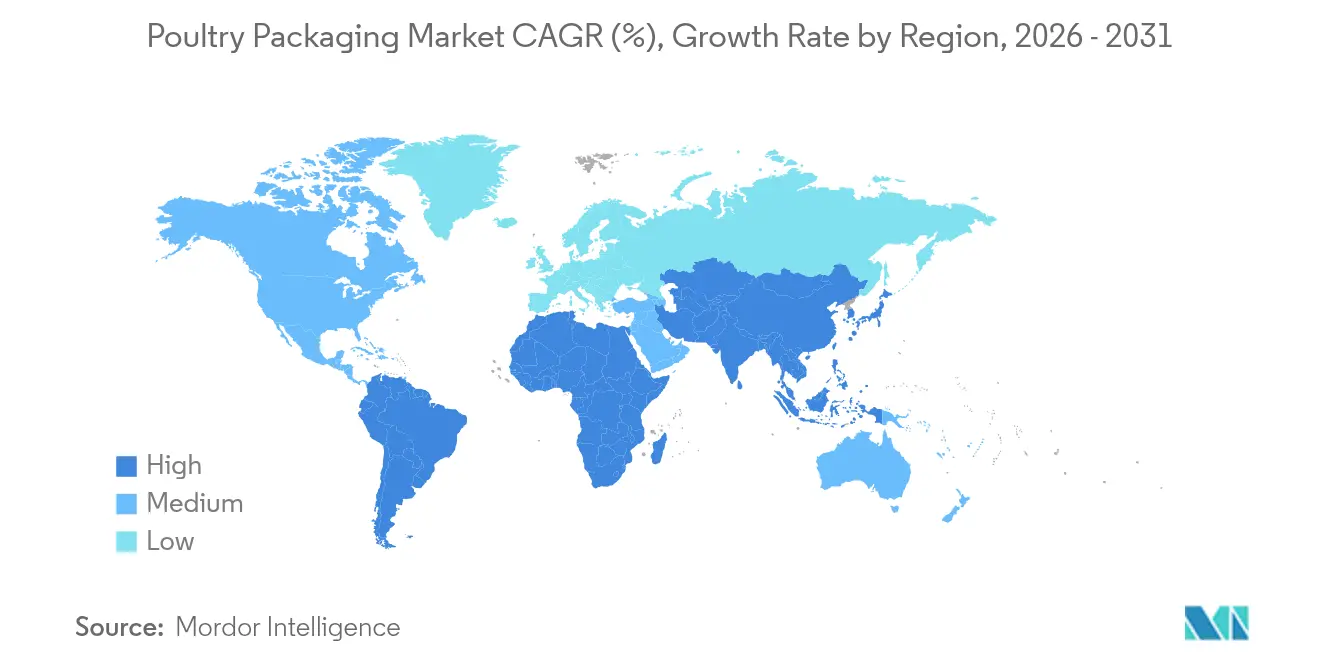

- By geography, Asia-Pacific held 38.45% of the poultry packaging market in 2025 and is expected to grow the fastest at a 5.11% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Poultry Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for convenience and case-ready | +1.2% | North America, EU | Medium term (2-4 years) |

| Surge in MAP and vacuum-skin technologies | +0.8% | Developed markets | Short term (≤2 years) |

| Shift toward bio-based and recyclable input | +0.7% | EU, expanding to North America | Long term (≥4 years) |

| E-commerce cold-chain expansion | +0.6% | Global, led by Asia-Pacific | Medium term (2-4 years) |

| Adoption of intelligent freshness sensors | +0.4% | Developed markets | Long term (≥4 years) |

| Recycled-content mandates | +0.5% | EU, California | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Convenience and Case-Ready Poultry

Millennial and Generation Z shoppers favor quick, no-mess poultry meals that arrive in easy-peel trays or ovenable pouches. Large retailers therefore specify centralized case-ready programs that cut in-store labor and improve product consistency. Tray producers now integrate absorbent pads and gas-flush valves that extend freshness by several days. Equipment vendors such as G.Mondini supply modular lines that blend precise portioning with lower film gauge, trimming material use without sacrificing visual appeal. Foodservice chains mirror this shift by ordering pre-marinated, vacuum-skin packs that move from cooler to grill in one step. Premium meal-kit platforms exploit the same packaging to boost shelf life during shipping, capturing higher margins that offset advanced film costs.

Surge in MAP and Vacuum-Skin Technologies

Modified-atmosphere packaging improves shelf life by slowing microbial growth, yet early high-oxygen blends accelerated lipid oxidation and color shifts. Converters now trial carbon-monoxide adjuncts that stabilize bloom without raising safety concerns. Vacuum-skin films from firms like Duropac prevent purge and withstand puncture, making them attractive for bone-in cuts. Plasma-treated trays that create in-pack ozone cut Campylobacter by 90% and Salmonella by 60% without chemicals. Equipment makers such as MULTIVAC pair MAP valves with micro-perforated lids so processors can tune gas ratios to each SKU.

Shift Toward Bio-Based and Recyclable Materials

The EU Packaging and Packaging Waste Regulation mandates 30% recycled PET by 2030 and 100% recyclability by the same year, pushing converters toward mono-material films [1]European Commission, “Regulation 2025/40 on Packaging and Packaging Waste,” europa.eu. Amcor’s AmFiber papers mimic plastic barrier while allowing curbside recycling. In the United States, polylactic-acid blends secured FDA food-contact clearance, but limited composting slows uptake. Chitosan coatings add natural antimicrobial activity yet require allergen assessment. Accredo Packaging’s sugarcane-based pouches sequester 43 g CO2 per unit while matching mechanical strength.

E-Commerce Cold-Chain Expansion

Direct-to-consumer poultry kits travel farther and encounter more hand-offs than retail loads. Fiber-based insulation such as DS Smith’s TailorTemp replaces styrene coolers and maintains temperature for 36 hours. Reusable containers with GPS loggers from Candor Food Chain hold safe temperatures for nine days and remove the need for dry ice. Smart labels report excursion events by reading color change, letting brands refund only affected boxes rather than entire shipments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Avian-influenza supply disruptions | -0.9% | Global, North America focus | Short term (≤2 years) |

| Stringent food-contact compliance costs | -0.6% | EU, North America | Medium term (2-4 years) |

| Feedstock-price volatility for polyolefins | -0.4% | Global commodity markets | Short term (≤2 years) |

| Consumer skepticism toward high-O₂ MAP | -0.3% | Educated markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Avian-Influenza Supply Disruptions

The 2024–2025 HPAI wave removed millions of birds from supply chains, unsettling production schedules and altering tray demand by weight class. USDA spent USD 1.8 billion on indemnities, but barns need up to 24 weeks to repopulate, prolonging volume instability. Rapid biosensors from Washington University now detect H5N1 in five minutes, enabling earlier lockdowns and targeted culls. Shorter flock cycles force processors to order more flexible sizes and adjust brand mix, which in turn influences run-length planning for converters.

Stringent Food-Contact Compliance Costs

Thirty-five PFAS notifications lost FDA clearance, obliging converters to reformulate grease barriers by June 2025. The EU further bans PFAS outright under Regulation 2025/40, adding lab certification for each new structure. The USDA now considers Salmonella an adulterant in raw poultry, triggering mandatory recalls and increasing liability for packers. New migration testing protocols add USD 50,000–100,000 to development cycles, disadvantaging smaller converters and encouraging alliances with labs that specialize in extractables work.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Meat Type: Chicken Retains Scale, Duck Accelerates Premiumization

The chicken category owns 65.34% of the poultry packaging market, thanks to broad consumer acceptance and streamlined deboning lines. High throughput lets processors negotiate film cost and spur experimentation with peel-reseal lids that cut food waste. Duck, despite its modest base, grows at a 5.45% CAGR as upscale retailers introduce portion-controlled breasts in sleek vacuum-skin trays. Here, the poultry packaging market size for duck is forecast to climb steadily as exotic proteins move into mainstream freezers. Enhanced barrier bags from Amcor prevent grease migration and preserve dark-meat color, meeting premium presentation standards.

Duck’s rise compels converters to integrate oil-resistant coatings while keeping clarity for retail appeal. Automation now portions duck to weight specs, enabling case-ready rollouts similar to chicken. Turkey holds share through seasonal whole-bird formats, yet value-added roasts and sliced deli packs sustain year-round demand. Each protein therefore demands tailored barrier, puncture strength, and silhouette, nudging film suppliers to broaden portfolios without inflating SKU count.

By Packaging Format: Flexible Films Drive Material Efficiency

Flexible structures delivered 62.45% of the poultry packaging market in 2025, supported by lower material intensity and high graphics that elevate shelf presence. The format will remain the growth leader, advancing 5.27% each year as mono-PET and PE laminates become store-drop recyclable. Within the poultry packaging market size, rigid trays retain roles in premium oven-ready SKUs and whole-bird presentations that benefit from stacking stability.

Equipment such as GEA’s PowerPak 1000 lets mid-scale plants swing between vacuum, MAP, and skin variants on a single frame, cutting change-over downtime . Flexible pouches now embed freshness sensors that change color when pH rises, turning the wrapper into a quality monitor. These upgrades defend price points in a cost-sensitive protein category and satisfy retailers that push for longer coded life to lower shrink.

By Material: Plastics Dominate but Paperboard Gains Ground

Plastics covered 67.02% of the poultry packaging market in 2025 due to unrivaled moisture and oxygen barriers. Yet paper and paperboard post a 5.31% CAGR as new dispersion coatings hit required grease resistance while enabling curbside recycling. The poultry packaging market share for plastics therefore declines gradually, though volumes still rise with protein output.

Amcor’s AmFiber Performance Paper secures over 80% fiber recovery during recycling and matches polyethylene’s water vapor barrier, illustrating rapid R&D gains. Hybrid structures that pair a thin PE sealant with heavyweight kraft are entering tray sealers without tooling change. Metal cans persist in military and remote catering uses, but their contribution to overall volume remains marginal.

By Packaging Technology: MAP Prevails as Intelligent Layers Emerge

Modified-atmosphere lines captured 42.21% of the poultry packaging market in 2025, offering processors a cost-efficient route to 7-14-day shelf life. Meanwhile, active and intelligent formats climb at a 5.18% CAGR as price of sensors and scavengers declines. The poultry packaging market size for MAP will still grow but cede share to smart variants that cut recalls and provide analytics.

Iron-based scavenger sachets extend refrigerated chicken life by nine days, reducing markdowns . Color-changing inks based on polyaniline nanotubes give a visual cue to consumers whenever spoilage triggers pH shift. IoT-enabled data loggers now cost under USD 0.10 per pack when amortized over large runs, making continuous cold-chain metrics feasible for mainstream brands.

By Distribution Channel: Retail Dominates but E-Commerce Surges

Traditional grocery generated 56.98% of revenue for the poultry packaging market in 2025, leveraging established planograms and just-in-time restocks. Nevertheless, e-commerce parcels will register a 5.14% CAGR as meal-kit and direct-farm websites multiply. The poultry packaging market size attributed to online channels thus expands quickly yet still relies on the same core converter base.

Retailers demand tamper-evident trays that showcase product color, whereas parcel shippers prefer vacuum-skin pouches nestled in fiber insulation to reduce dimensional weight. Institutional feeders and foodservice maintain consistent volume but challenge packers to balance toughness with ease of opening in busy kitchens. Converters offer modular tooling that swaps cavity depth, letting one base film serve multiple channel specifications.

Geography Analysis

Asia-Pacific controlled 38.45% of the poultry packaging market in 2025 and is projected to expand at a 5.11% CAGR to 2031. Rapid urban migration and rising disposable income in China and India lift chilled-poultry demand, while Thailand strengthens its export position. National circular-economy rules spur adoption of recyclable laminates, and local processors engage global machinery firms to meet export hygiene codes. Multinational retailers entering Indonesia and Vietnam specify case-ready programs, unlocking new business for regional converters.

North America ranks second in value. Federal regulation remains stable, but states such as California and Oregon add producer-responsibility fees that reward mono-material formats . Consumers display strong willingness to pay for antibiotic-free and sustainability-certified packs, encouraging brands to pilot compostable trays. Canada’s updated Zero Plastic Waste agenda echoes EU targets, further accelerating the shift to paper-polymer hybrids. Intelligent labels see early uptake as big-box stores test on-pack QR codes for traceability.

Europe shows low headline growth yet high innovation density. Regulation 2025/40 enforces 100% recyclability by 2030 and bans PFAS, forcing converters into rapid material substitution. Retailers collaborate with suppliers to validate fully fiber trays that keep poultry fresh for 21 days, exemplified by Coveris’ new BarrierFresh line. Smart-sensor pilots in Germany track time-temperature abuse, delivering data that informs dynamic discounting to curb waste.

Competitive Landscape

The poultry packaging market remains moderately fragmented, though recent deals signal a tilt toward consolidation. Amcor’s USD 8.4 billion purchase of Berry Global scales film extrusion and thermoforming under one roof, promising customers worldwide SKU harmonization. Sonoco’s EUR 3.615 billion acquisition of Eviosys expands metal and rigid paperboard capability, positioning the group to offer multi-material solutions.

Large groups invest heavily in sustainability science. Amcor’s Moda automated bagging line integrates AI vision that adjusts vacuum pull in real time, reducing leakers while cutting film usage. Mondi’s FlexStudios hub partners with poultry processors to co-create recyclable laminates suited to high-speed fill lines. Meanwhile, mid-tier specialists carve niches in intelligent packaging. Several have launched printed electronics that deliver temperature logs via NFC at checkout.

Technology startups become acquisition targets. Sensor-developers that perfected carbon-dot indicators now license know-how to laminate suppliers seeking differentiation. E-commerce growth lures insulation innovators who replace expanded polystyrene with molded-fiber pads. Competitive pressure therefore hinges on innovation pace as much as scale. Companies able to prove regulatory compliance across global jurisdictions gain access to multinational processors’ supplier lists, cementing long-term contracts.

Poultry Packaging Industry Leaders

Amcor plc

Mondi Group

Sealed Air Corporation

Sonoco Products Company

Berry Global Group Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Coveris unveiled BarrierFresh MAP trays that cut plastic by 90% while offering a 21-day shelf life.

- February 2025: The European Union issued Regulation 2025/40 mandating 100% recyclability by 2030 and banning PFAS in food-contact materials.

- January 2025: Cirkla launched molded-fiber MAP trays following successful meat-packer trials in the United States.

- November 2024: Mondi opened FlexStudios, an innovation hub for sustainable flexible packaging focused on poultry applications.

Global Poultry Packaging Market Report Scope

Thepoultry packaging market gives a detailed analysis of packaging materials used for packagingdifferent poultry meat such as duck,chicken, and turkey. The report talks about fixed packaging materials such as trays and bowls, and cardboard whereas in flexibles, pouches, bags, and films are considered. On the basis of geography, North America, Europe, Asia-Pacific, Middle East & Africa, and Latin America are included in the report.

| Chicken |

| Turkey |

| Duck |

| Fixed / Rigid |

| Flexible |

| Plastics |

| Paper and Paperboard |

| Metals |

| Modified Atmosphere Packaging (MAP) |

| Vacuum Skin Packaging (VSP) |

| Active and Intelligent Packaging |

| High-Pressure and Others |

| Retail |

| Foodservice / HORECA |

| Industrial and Institutional |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Meat Type | Chicken | ||

| Turkey | |||

| Duck | |||

| By Packaging Format | Fixed / Rigid | ||

| Flexible | |||

| By Packaging Material | Plastics | ||

| Paper and Paperboard | |||

| Metals | |||

| By Packaging Technology | Modified Atmosphere Packaging (MAP) | ||

| Vacuum Skin Packaging (VSP) | |||

| Active and Intelligent Packaging | |||

| High-Pressure and Others | |||

| By Distribution Channel | Retail | ||

| Foodservice / HORECA | |||

| Industrial and Institutional | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the poultry packaging market?

The poultry packaging market reached USD 3.82 billion in 2026.

Which region offers the fastest growth?

Asia-Pacific is forecast to expand at a 5.11% CAGR to 2031, driven by urbanization and rising protein consumption.

What packaging format dominates the market?

Flexible structures hold 62.45% share and will remain the leading format due to material-efficiency and graphics advantages.

How are regulations reshaping material choices?

EU Regulation 2025/40 mandates 100% recyclability and PFAS bans by 2030, prompting a shift toward mono-material and paper-based solutions.

Page last updated on: