Master Data Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

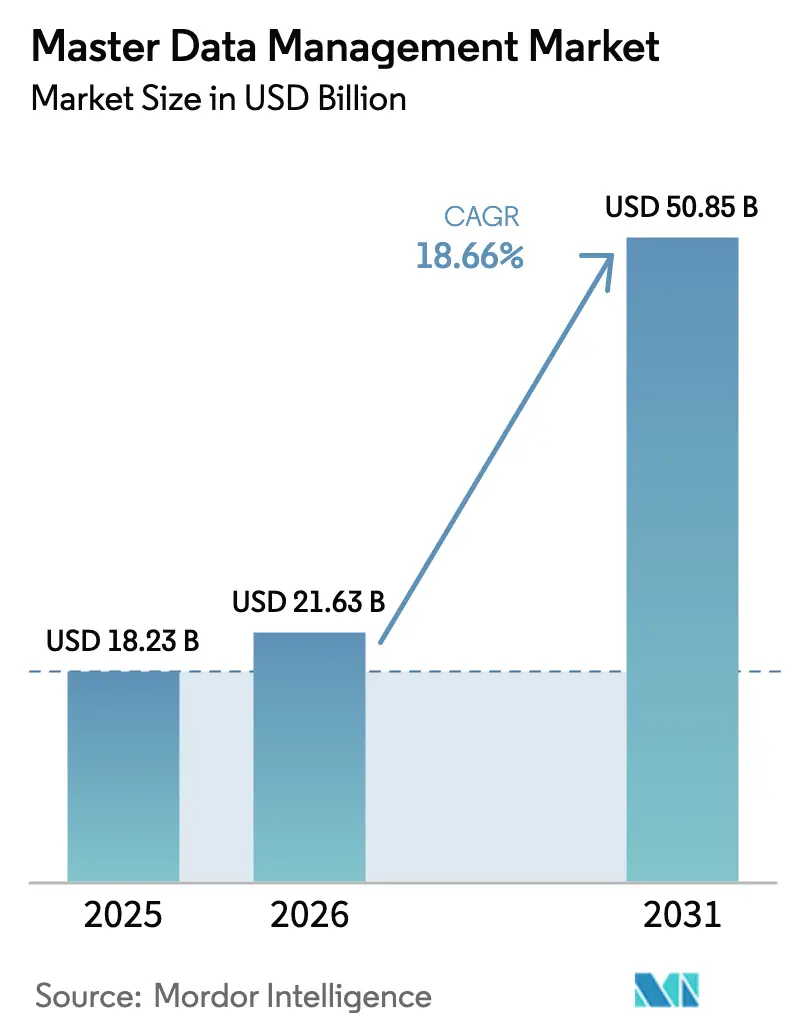

| Market Size (2026) | USD 21.63 Billion |

| Market Size (2031) | USD 50.85 Billion |

| Growth Rate (2026 - 2031) | 18.66% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Master Data Management Market Analysis by Mordor Intelligence

Master Data Management market size in 2026 is estimated at USD 21.63 billion, growing from 2025 value of USD 18.23 billion with 2031 projections showing USD 50.85 billion, growing at 18.66% CAGR over 2026-2031.

Enterprise priorities around generative-AI readiness, mandatory real-time ESG reporting, and cyber-resilience are accelerating demand for unified, high-quality data layers that feed analytics, automation, and risk engines. Software still dominates revenues, yet services are expanding faster as organizations seek design, change-management, and governance expertise to unlock value from increasingly complex deployments. Cloud implementations already deliver 61% of new installations, reflecting mid-market ERP migrations and the appeal of elastic, pay-per-use models that speed time-to-value. [1]Stibo Systems, “Cloud MDM Adoption Trends 2025,” stibosystems.com North America retains leadership with 39% share, while Asia Pacific is advancing at 19.52% CAGR on the back of data-localization laws and rapid digitalization.

Key Report Takeaways

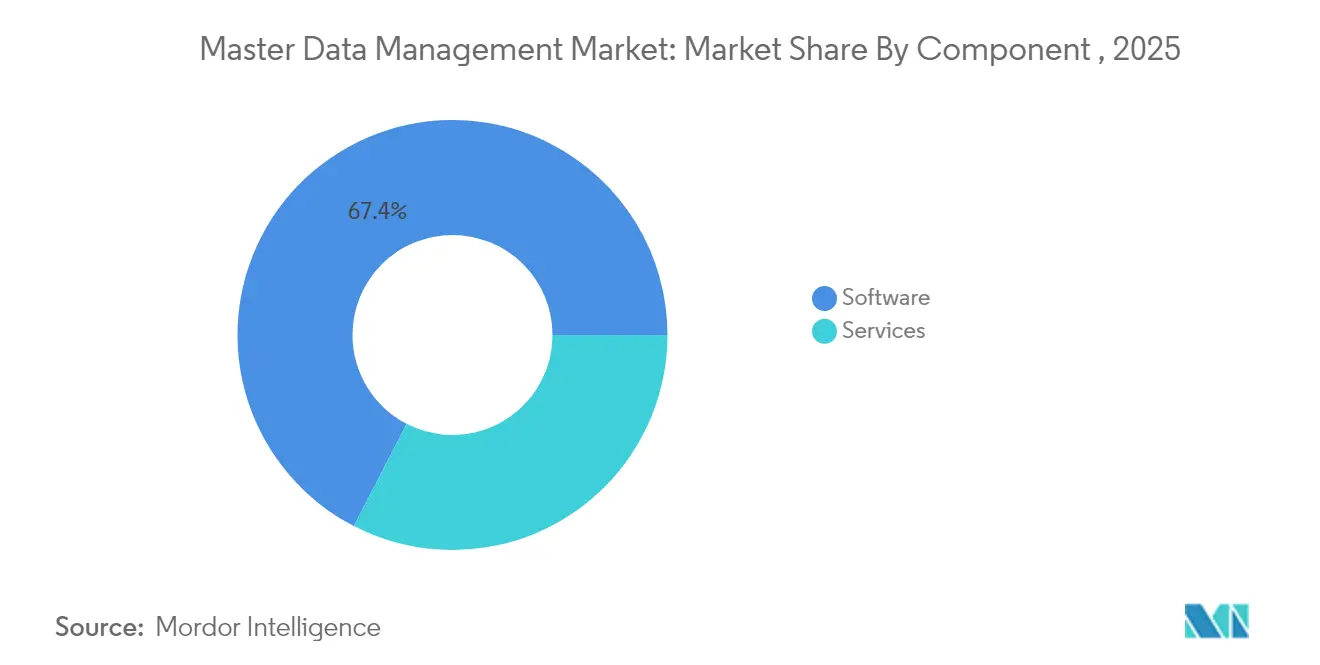

- By component, software captured 67.42% of the Master Data Management market share in 2025, while services are expanding at a 19.26% CAGR through 2031.

- By deployment model, cloud deployments accounted for 60.35% of the Master Data Management market size in 2025 and are advancing at a 20.88% CAGR.

- By enterprise size, large enterprises held 63.25% share in 2025, whereas SMEs are projected to grow at a 19.74% CAGR to 2031.

- By application, customer-360 solutions led with 41.35% revenue share in 2025; finance & reference data management is expected to accelerate at a 22.06% CAGR.

- By industry vertical, BFSI commanded 20.58% of 2025 revenue, while healthcare is forecast to expand at a 18.73% CAGR.

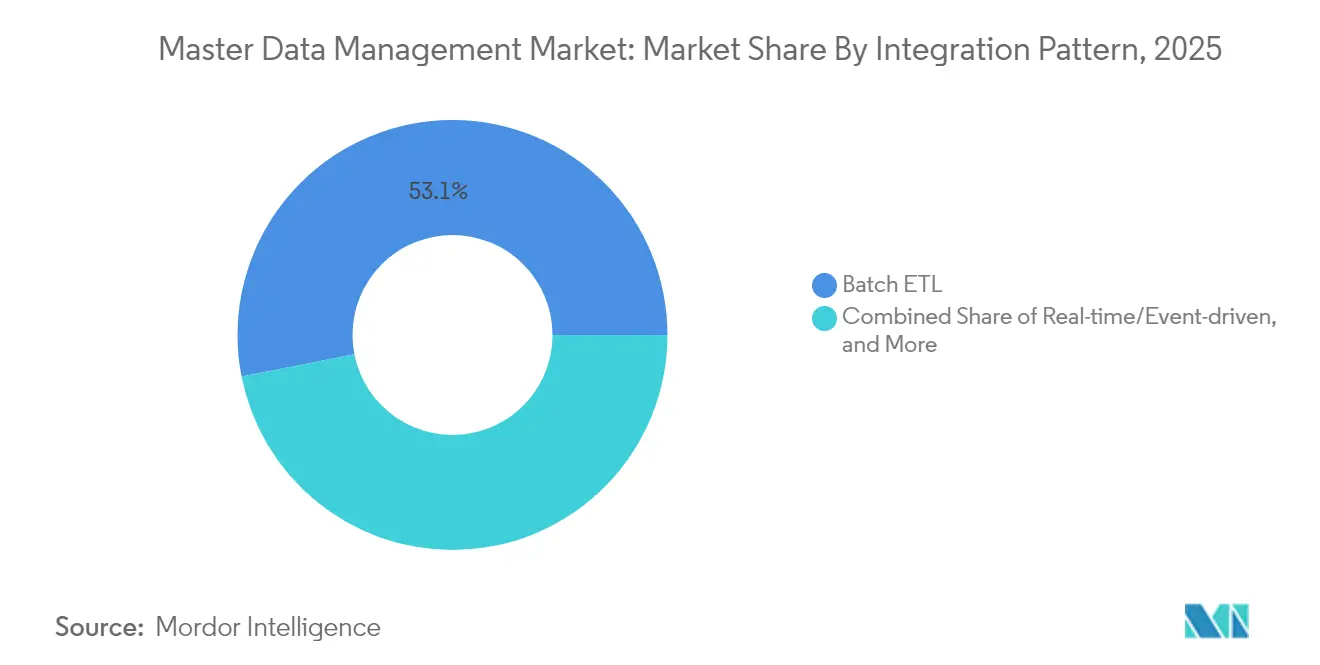

- By integration pattern, batch ETL retained 53.10% share in 2025, whereas real-time event-driven architectures are rising at an 18.72% CAGR.

- By cloud deployment type, multi-tenant SaaS represented 41.30% of cloud implementations in 2025; hybrid architectures are growing at a 21.32% CAGR.

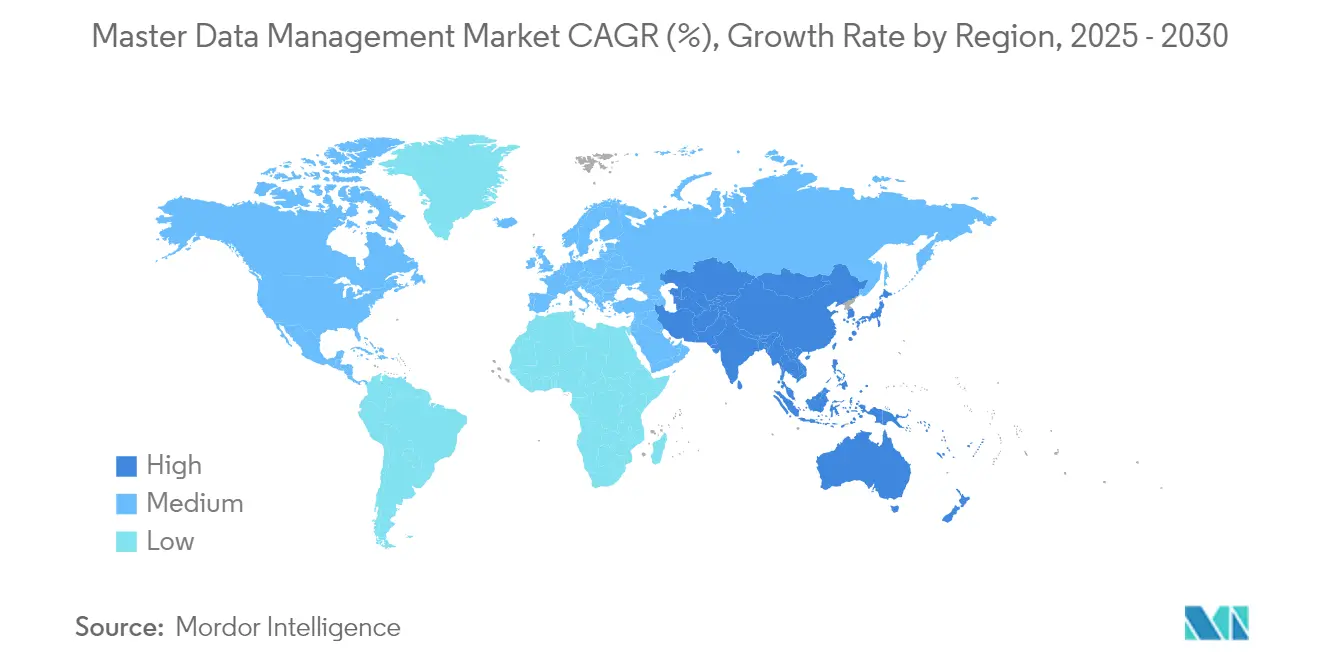

- By geography, North America led with 38.55% market share in 2025, and Asia Pacific is advancing at a 19.14% CAGR

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Master Data Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Gen-AI readiness drives need for high-quality training data | +4.2% | Global, led by North America & EU | Medium term (2-4 years) |

| Regulatory shift to real-time ESG disclosures | +3.1% | EU primary, expanding to North America & APAC | Short term (≤ 2 years) |

| Data-fabric & data-mesh architectures mainstreaming | +2.8% | Global, large-enterprise focus | Medium term (2-4 years) |

| Rapid cloud ERP migrations in mid-market firms | +3.5% | North America & EU core, growing in APAC | Short term (≤ 2 years) |

| Expansion of industry-specific 360-MDM SaaS (e.g., Retail, Life Sciences) | +2.9% | Global, sector-specific adoption patterns | Medium term (2-4 years) |

| Cyber-resilience mandates for critical infrastructure (NIS2, DORA) | +2.7% | EU primary (NIS2/DORA), spreading globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Gen-AI Readiness Drives Need for High-Quality Training Data

Generative-AI projects expose the direct link between model accuracy and master data consistency. Informatica’s AI-enhanced cloud processed 86 trillion transactions, helping customers cut data-program time-to-value by 40%[2]Informatica, “Informatica Cloud Logs 86 Trillion Transactions,” informatica.com . Healthcare and financial services adopters are blending ChatGPT-style enrichment with MDM to raise data-matching accuracy to 80%, turning data quality from a compliance checkbox into a competitive edge. Continuous validation, enrichment, and lineage tracking are therefore moving from optional add-ons to core platform requirements inside the Master Data Management market.

Regulatory Shift to Real-Time ESG Disclosures

The EU’s Digital Operational Resilience Act obliges financial entities to maintain exhaustive ICT risk controls, including auditable master data governance that supports real-time ESG reporting. Traditional quarterly cycles cannot supply investors with carbon-footprint or supply-chain-ethics metrics at the required granularity, pushing enterprises toward platforms that reconcile sustainability data with the rigor of financial ledgers. Multi-jurisdictional operations must additionally accommodate differing data-sovereignty rules, complicating centralization strategies and fuelling hybrid-MDM demand.

Data-Fabric & Data-Mesh Architectures Mainstreaming

Capital One and the U.S. Centers for Medicare & Medicaid Services each deployed federated data-mesh patterns that hand domain teams ownership of master data while preserving enterprise standards. The approach reduces bottlenecks, shortens development cycles, and fits large manufacturers seeking to govern sprawling product hierarchies. MDM vendors are responding with decentralized stewardship workflows, fine-grained access controls, and shared semantics registries that align with mesh principles.

Rapid Cloud ERP Migrations in Mid-Market Firms

Two-thirds of 2024 ERP projects selected cloud delivery, creating urgent need for MDM to reconcile data during migrations and future hybrid states. Early-stage SAP S/4HANA programs that embed MDM cut cutover timelines and system complexity, proving that data quality determines ERP ROI. Subscription pricing and template-based deployments make enterprise-grade governance attainable for mid-market manufacturers and distributors seeking agility without ballooning IT overhead.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of MDM-skilled data stewards | -2.1% | Global, acute in emerging markets | Medium term (2-4 years) |

| Hidden technical debt in legacy source systems | -1.8% | North America & EU legacy enterprises | Long term (≥ 4 years) |

| Access-control conflicts under emerging data sovereignty laws | -1.5% | APAC primary, expanding globally | Short term (≤ 2 years) |

| Rising hyperscaler egress fees inflating total cost of ownership | -1.3% | Global cloud deployments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortage of MDM-Skilled Data Stewards

Seventy-five percent of manufacturers reported difficulty filling data-steward roles in 2024, reflecting demand for professionals who blend domain expertise with AI and governance fluency. While automation eases repetitive cleansing, human oversight remains vital for policy definition and exception handling. Managed-service and embedded-governance offerings are therefore rising as stop-gaps, especially in emerging markets where skill pipelines lag digital-transformation ambitions.

Hidden Technical Debt in Legacy Source Systems

Decades of custom logic, undocumented transformations, and inconsistent schemas double timelines and budgets once MDM discovery phases surface surprise dependencies inside financial-services and manufacturing estates. Organizations now insist on platforms offering deep data-lineage visualization and adaptive integration that can respect idiosyncratic legacy rules while establishing forward-looking standards.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Growth Outpaces Software Dominance

Software delivered 67.42% of 2025 revenue, but services are accelerating at 19.26% CAGR, signalling that the Master Data Management market is no longer technology-first. Enterprises in healthcare and banking invest in advisory, data-architecture design, and change management to navigate complex compliance landscapes. Professional services now encompass governance framework development and cross-domain policy harmonization, extending far beyond initial system integration.

Managed-service adoption among mid-market organizations shows that outsourcing stewardship and platform operations can balance limited internal capacity with quality expectations. As vertical regulations tighten, service partners with domain credentials become pivotal to monetizing software capabilities, reinforcing a shift where value lies in sustained governance outcomes.

By Deployment Model: Cloud Acceleration Reshapes Market Dynamics

Cloud deployments commanded a 60.35% share in 2025 and are scaling at a 20.88% CAGR, redefining vendor selection criteria inside the Master Data Management market. Elastic scaling, automated patching, and usage-based pricing lower entry barriers, while pre-built connectors shorten time-to-insight for analytics teams.

Even highly regulated sectors now blend on-premise controls with cloud agility through containerized or SaaS edge nodes. The Master Data Management industry benefits as platforms integrate natively with cloud AI services, enabling real-time enrichment without heavyweight data-movement pipelines. Hybrid patterns thus satisfy sovereignty, latency, and economics in one architecture.

By Enterprise Size: SME Adoption Accelerates Through Cloud Accessibility

Large enterprises still hold a 63.25% share, yet SMEs are growing at a 19.74% CAGR as subscription models democratize the Master Data Management market. Smaller firms typically target single-domain wins—customer data unification or product catalog clarity—before expanding scope.

Cloud-native vendors supply template libraries and guided workflows that cut configuration effort, letting SMEs realize 15% revenue uplift and 20% lower risk exposure from better analytics. These proof points reinforce the business-case narrative that robust master data is no longer a luxury reserved for global conglomerates.

By Application Domain: Finance & Reference Data Drives Regulatory Compliance

Customer-360 use cases held 41.35% share in 2025, proving that unified customer experiences remain the prime catalyst for Master Data Management market investments. Yet, finance & reference data is projected to climb at 22.06% CAGR as real-time reporting mandates sweep across accounting standards and ESG frameworks.

Unifying supplier, product, and risk attributes under one governance umbrella equips CFOs to meet immediate audit requests and close books faster, converting compliance spending into decision-support value. Convergence toward multi-domain platforms is therefore accelerating, with asset and location data next in line as IoT digitizes physical operations.

By Industry Vertical: Healthcare Transformation Accelerates Growth

BFSI contributed 20.58% of 2025 revenue, but healthcare is moving fastest at 18.73% CAGR, pushing the Master Data Management market toward patient-centric innovation. Verato’s identity-resolution cloud allows providers to match electronic records across institutions, lowering duplicate charts and enhancing clinical insights, Healthcare IT News. Regulatory incentives tied to care-quality metrics make robust provider and patient master data a non-negotiable foundation.

Retail, manufacturing, and telecom also expand footprints, each seeking domain-specific gains—digital-shelf accuracy, supply-chain resiliency, and converged customer-device profiles—underscoring that sector specialization is becoming a key vendor differentiator.

By Integration Pattern: Real-Time Architectures Challenge Batch Dominance

Batch ETL still represents 53.10% of integrations, yet event-driven designs are leaping forward at 18.72% CAGR as instant personalization and fraud-detection use cases proliferate. Streaming pipelines push updates into downstream applications within milliseconds, elevating data-quality SLAs and demanding fine-grained error-handling built into MDM cores.

API-first microservices broaden developer adoption, letting digital-product teams tap governed master data without complex middleware. The Master Data Management market therefore pivots toward low-latency orchestration where data contracts, versioning, and observability take center stage.

By Cloud Deployment Type: Hybrid Models Balance Control with Scalability

Multi-tenant SaaS delivers 41.30% of cloud installations thanks to rapid pay-as-you-go rollouts. Still, hybrid architectures are climbing at 21.32% CAGR, enabling headquarters to keep sensitive master records on-premise while leveraging cloud analytics for less regulated datasets. European enterprises, facing GDPR and upcoming AI Act requirements, exemplify the demand for architectures that partition workloads by jurisdiction while presenting a unified data-governance façade.

Vendors now package policy-based routing that decides where master attributes reside and how they synchronize, ensuring compliance without losing cloud elasticity—an approach quickly becoming a baseline requirement for multinational deployments.

Geography Analysis

North America led with a 38.55% share of the Master Data Management market in 2025, supported by stringent sectoral regulations and early AI adoption. U.S. firms such as WeightWatchers streamlined 30 million client records using Oracle Customer Hub, illustrating how mature governance programs translate into lower customer-experience frictions. Canadian and Mexican enterprises are close behind, exploiting cross-border commerce and USMCA incentives to modernize data architectures.

Asia Pacific is forecast to grow at 19.14% CAGR through 2031 as data-localization mandates reshape enterprise strategies. China’s rapid data-center build-out, coupled with constraints on cross-border transfers, drives demand for domestically hosted MDM solutions that interoperate with global supply-chain data . India’s 2025 Digital Personal Data Protection Act draft rules intensify the focus on consent management and data-lineage transparency, prompting local firms to adopt governance-rich platforms ahead of enforcement thresholds. ASEAN’s 20% data-center revenue growth signals rising capacity to support region-wide MDM rollouts

Europe maintains steady expansion under GDPR, DORA, and the incoming EU AI Act, positioning the region as a global benchmark for comprehensive data governance. Institutions such as Deutsche Börse centralized master data with SAP Master Data Governance to cut manual maintenance and accelerate product launches. Heightened enforcement actions in nations like the Netherlands propel investment in lineage-rich solutions that can evidence compliance when regulators demand audits. Hybrid architectures dominate European roadmaps, balancing sovereignty with the need to tap global cloud ecosystems.

Competitive Landscape

The Master Data Management market is moderately fragmented: top legacy vendors IBM, SAP, and Oracle compete with cloud-native challengers Reltio, Stibo Systems, and Semarchy, while hyperscalers embed native governance services that threaten standalone platforms. Salesforce’s USD 8 billion purchase of Informatica melds CRM data with enterprise-grade governance, signalling consolidation that blends front-office context with back-office rigor.

Innovation patterns show a pivot toward AI-embedded governance; Informatica processed trillions of transactions using CLAIRE AI to automate profiling and matching, whereas Palantir patented attribute-analysis engines that enrich master records during ingest. Vertical templates are now mainstream: Stibo Systems’ STEP for retail and Semarchy’s Snowflake integration exemplify turnkey offerings that shorten deployment cycles for focused use cases.

Vendor strategy increasingly centers on partnerships. Stibo Systems joined Microsoft’s software ecosystem to fuse Azure OpenAI with product-data optimization, and Reltio linked with Workato to combine workflow automation and data activation. Private-equity backing, such as Pamlico Capital’s investment in Profisee, funds accelerated R&D aimed at SME-friendly cloud propositions. Collectively, these moves illustrate a market in which speed-to-value and domain fit often outweigh breadth of generic functionality.

Master Data Management Industry Leaders

IBM

Oracle

Informatica Inc.

SAP SE

Ataccama

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Salesforce agreed to acquire Informatica for USD 8 billion, fusing CRM with end-to-end data governance capabilities.

- April 2025: Semarchy launched its MDM platform on Snowflake AI Data Cloud, unifying warehousing and governance functions.

- April 2025: Informatica released AI-powered cloud integration upgrades covering 300+ connectors and no-code pipelines.

- March 2025: Profisee secured growth funding from Pamlico Capital to accelerate cloud-native MDM innovation.

Global Master Data Management Market Report Scope

To maintain the consistency, correctness, stewardship, semantic consistency, and accountability of the enterprise's official shared master data assets, business and information technology collaborate through the discipline of master data management (MDM), which is facilitated by technology.

The master data management market is segmented by component (software, service), by deployment model (on-premise, cloud), by enterprise size (large enterprises, small and medium enterprises), by application (supplier, product, customer), by industry vertical (IT and telecommunication, BFSI, healthcare, government, retail, manufacturing, education), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, Rest of the World). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

| Software |

| Services |

| On-premise |

| Cloud |

| Large Enterprises |

| Small and Medium Enterprises |

| Customer |

| Product |

| Supplier |

| Finance and Reference Data |

| Asset and Location |

| BFSI |

| Healthcare and Life Sciences |

| Retail and e-Commerce |

| Manufacturing |

| IT and Telecom |

| Government and Public Sector |

| Energy and Utilities |

| Others (Education, Media, etc.) |

| Batch ETL |

| Real-time/Event-driven |

| API-led Micro-services |

| Multi-tenant SaaS |

| Single-tenant SaaS |

| Self-managed Cloud (IaaS) |

| Hybrid (Cloud + On-prem) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | GCC (Saudi Arabia, UAE, Qatar, etc.) |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Component | Software | ||

| Services | |||

| By Deployment Model | On-premise | ||

| Cloud | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By Application Domain | Customer | ||

| Product | |||

| Supplier | |||

| Finance and Reference Data | |||

| Asset and Location | |||

| By Industry Vertical | BFSI | ||

| Healthcare and Life Sciences | |||

| Retail and e-Commerce | |||

| Manufacturing | |||

| IT and Telecom | |||

| Government and Public Sector | |||

| Energy and Utilities | |||

| Others (Education, Media, etc.) | |||

| By Integration Pattern | Batch ETL | ||

| Real-time/Event-driven | |||

| API-led Micro-services | |||

| By Cloud Deployment Type | Multi-tenant SaaS | ||

| Single-tenant SaaS | |||

| Self-managed Cloud (IaaS) | |||

| Hybrid (Cloud + On-prem) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Netherlands | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| ASEAN | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | GCC (Saudi Arabia, UAE, Qatar, etc.) | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the Master Data Management market?

The Master Data Management market stands at USD 21.63 billion in 2026 and is projected to reach USD 50.85 billion by 2031.

Which deployment model is growing fastest

Cloud implementations lead growth, expanding at 20.88% CAGR as enterprises shift workloads to scalable, pay-per-use architectures.

Why is healthcare the fastest-growing vertical?

Healthcare records unify patient identities and provider data to power AI-driven clinical decisions, driving a 18.73% CAGR through 2031.

How are generative-AI projects influencing MDM investments?

AI initiatives demand pristine training data, increasing MDM platform adoption to automate cleansing, enrichment, and lineage tracking.

What restraints could slow market expansion?

global shortage of data-steward talent and unresolved technical debt within legacy systems can stretch project timelines and budgets.

Page last updated on: