Technology, Media and Telecom

5th MayAccelerating Additive Manufacturing Adoption in India

3 Min Read

The Massive Machine Type Communication Market Report is Segmented by Communication Channel Type (Wired, and Wireless), Connectivity Technology (NB-IoT, LTE-M, and More), Deployment Model (Public Network, Private Network, and More), Application (Smart Metering, Asset Tracking, and More), End-User Industry (Utilities, Transportation and Logistics, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

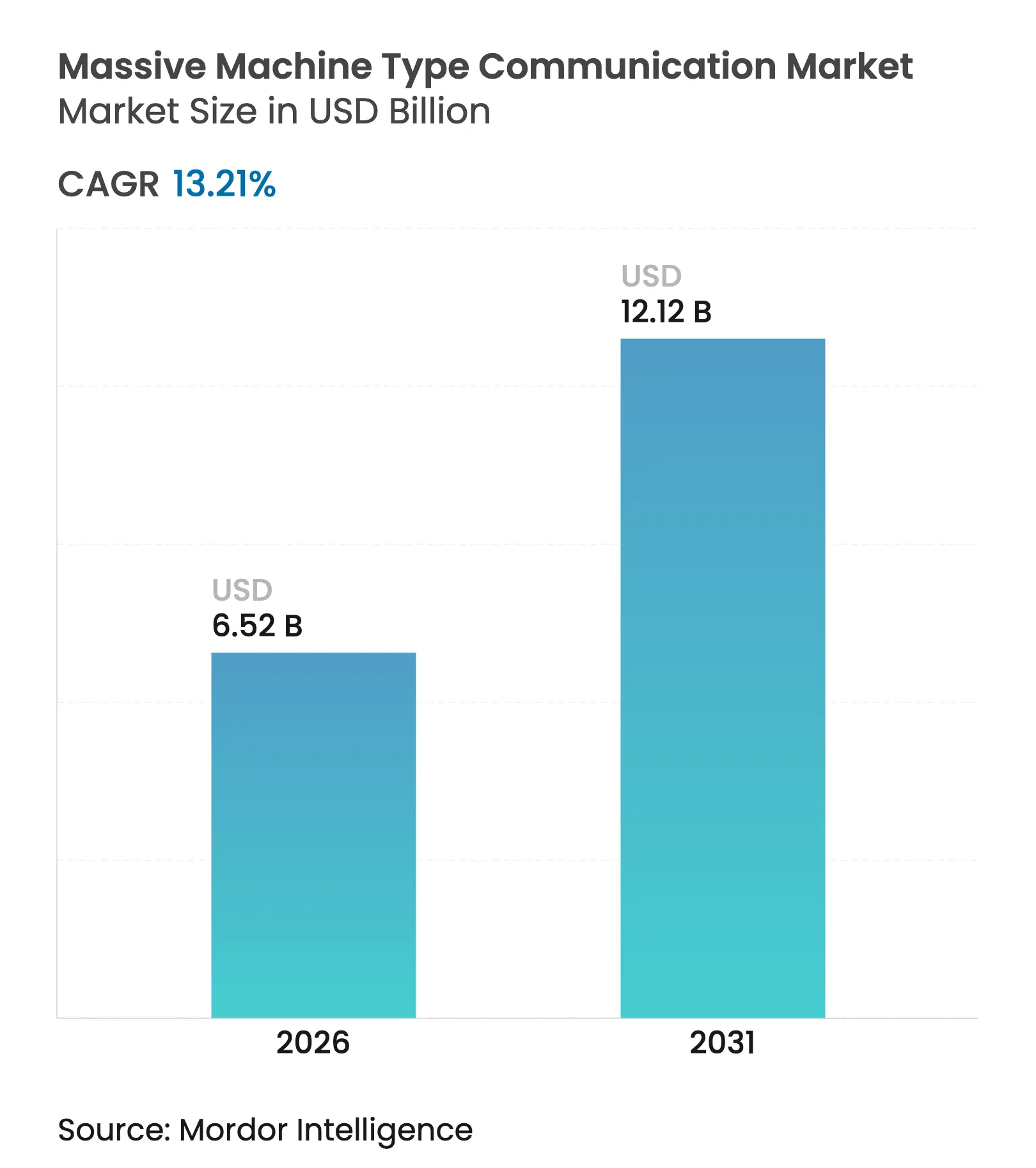

| Market Size (2026) | USD 6.52 Billion |

| Market Size (2031) | USD 12.12 Billion |

| Growth Rate (2026 - 2031) | 13.21 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Massive Machine Type Communication market size in 2026 is estimated at USD 6.52 billion, growing from 2025 value of USD 5.76 billion with 2031 projections showing USD 12.12 billion, growing at 13.21% CAGR over 2026-2031. This steady climb is shaped by utilities and industrial operators embedding NB-IoT, LTE-M, and emerging 5G RedCap modules into endpoints that previously lacked reliable backhaul. Wireless deployments already account for 79.77% of connections and are advancing at a 14.44% pace as operators expand nationwide coverage and introduce network-slicing offers. Asia Pacific retains the largest regional footprint, capturing 45.7% revenue in 2024, while private cellular networks gain traction as manufacturers seek full control of data flow and latency. Competition is intensifying as infrastructure vendors bundle RedCap support into 5G Standalone upgrades and chipset suppliers cut idle-mode power budgets below 100 mW, setting a new baseline for battery-powered sensors.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Growing 5G network rollouts accelerating mMTC adoption Growing 5G network rollouts accelerating mMTC adoption | +3.2% | Global, led by Asia Pacific and Europe | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+3.2% | Geographic Relevance:Global, led by Asia Pacific and Europe | Impact Timeline:Medium term (2-4 years) |

Proliferation of low-cost IoT sensors and modules Proliferation of low-cost IoT sensors and modules | +2.8% | Global, strong in Asia Pacific and North America | Short term (≤ 2 years) | |||

Government-led smart-city programs worldwide Government-led smart-city programs worldwide | +2.4% | Asia Pacific core, spill-over to Middle East and South America | Medium term (2-4 years) | |||

Adoption of digital twins in industrial automation Adoption of digital twins in industrial automation | +2.1% | North America, Europe, developed Asia Pacific | Long term (≥ 4 years) | |||

Satellite-based NB-IoT backhaul for remote assets Satellite-based NB-IoT backhaul for remote assets | +1.5% | Global, key in mining regions of Australia, Africa, South America | Medium term (2-4 years) | |||

Energy-harvesting chipsets enabling battery-less devices Energy-harvesting chipsets enabling battery-less devices | +1.2% | Europe and North America | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Growing 5G Network Rollouts Accelerating mMTC Adoption

Sixty operators had live 5G Standalone networks by late 2024, and many paired those deployments with RedCap-enabled radios that bridge the gap between narrowband IoT and full-feature. China Mobile alone activated more than 600,000 RedCap base stations across 200 cities, giving industrial firms deterministic latency and uplink rates previously unattainable on LPWAN. Module costs fell from USD 30 in 2023 to USD 20 in 2024, tipping investment decisions toward cellular devices that guarantee quality of service. Regulators add momentum: China’s Ministry of Industry and Information Technology requires 100 prefecture-level cities to host RedCap infrastructure by year-end 2025, ensuring continued demand.[1] Ministry of Industry and Information Technology, “RedCap Deployment Mandates,” miit.gov.cn Operators are also bundling RedCap with network slicing, allowing utilities to pre-book spectrum for smart-meter bursts during billing peaks.

Proliferation of Low-Cost IoT Sensors and Modules

NB-IoT module prices slipped below USD 3 in 2024 as Chinese fabs scaled production beyond 500 million cumulative units. This threshold lets utilities embed cellular radios in water, gas, and electricity meters while staying inside a USD 5 hardware budget cap. Qualcomm’s Snapdragon X35 RedCap modem and LTE-M-oriented 9207, unveiled in March 2025, further lower entry barriers for asset-tracking and predictive-maintenance projects by offering 10-year battery life on coin-cell power. Hybrid chipsets such as Sequans Monarch 2 GM02S combine NB-IoT and LTE-M on one die, shrinking board area for wearable-health devices. As hardware sinks in cost, operators now price connectivity near USD 0.50 per device per year, placing the Massive Machine Type Communication market on par with unlicensed LPWAN in total cost.

Government-Led Smart City Programs Worldwide

South Korea’s fourth Smart City Plan directs KRW 1.2 trillion (USD 900 million) toward cellular street-lighting, waste, and air-quality sensors in 25 municipalities between 2024 and 2028. India’s 5G Intelligent Village program links rural clinics and co-ops via NB-IoT and LTE-M, spawning 50,000 live connections in its first six months. Thailand, Singapore, and Japan all attach funding or mandates to IoT infrastructure in new urban development, offering integrators multi-year revenue certainty. These public initiatives shorten payback periods for vendors and remove demand-side risk, accelerating the Massive Machine Type Communication market by anchoring predictable device rollouts.

Adoption of Digital Twins in Industrial Automation

Digital-twin platforms need round-trip latency below 50 milliseconds and uplink throughput above 10 Mbps for real-time synchronization—parameters met only by 5G RedCap or Wi-Fi 6E in controlled coverage zones. Siemens integrated its Xcelerator suite with AWS IoT Core to ingest sensor data from factory floors and run live predictive models. Wanhua Chemical reported 12% energy savings after linking 5,000 RedCap terminals to digital twins that fine-tune reactor temperatures. European carmakers operate private 5G networks to guarantee sub-10-millisecond latency for robotic arms, demonstrating the high-value industrial cases that propel the Massive Machine Type Communication market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Fragmented spectrum allocation policies across regions Fragmented spectrum allocation policies across regions | −1.8% | Europe, North America, emerging markets | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:−1.8% | Geographic Relevance:Europe, North America, emerging markets | Impact Timeline:Medium term (2-4 years) |

High power-budget constraints in massive-scale deployments High power-budget constraints in massive-scale deployments | −1.2% | Global utilities and agriculture | Short term (≤ 2 years) | |||

Security vulnerabilities in ultra-low-cost end nodes Security vulnerabilities in ultra-low-cost end nodes | −0.9% | North America and Europe | Short term (≤ 2 years) | |||

Skills gap in managing billions of cellular IoT devices Skills gap in managing billions of cellular IoT devices | −0.7% | Emerging markets worldwide | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Fragmented Spectrum Allocation Policies Across Regions

Europe standardizes Bands 8, 20, and 28 for NB-IoT, while North America relies on Bands 5, 12, and 13, forcing vendors to ship multiple hardware variants and lifting bill-of-materials cost by up to 30%. The resulting patchwork complicates roaming, leaves enterprises managing dual-mode devices, and curtails scale economies that would otherwise lower Massive Machine Type Communication market equipment prices. AT&T’s decision to sunset NB-IoT and repurpose Band 5 for mid-band 5G underscores the vulnerability of sensors to operator spectrum strategies. Without global harmonization, module designers must hedge bets across NB-IoT, LTE-M, and RedCap, adding complexity and cost.

Security Vulnerabilities in Ultra-Low-Cost End Nodes

In 2024 the U.S. Cybersecurity and Infrastructure Security Agency issued 14 alerts covering default credentials and unpatched firmware in industrial IoT gateways. The European Union’s Cyber Resilience Act tightens rules by mandating secure boot, encrypted updates, and documented disclosure processes, inflating compliance costs by roughly 20% for the lowest-end modules.[2]European Commission, “Cyber Resilience Act,” ec.europa.eu Mirai-style botnets remain active, with 100,000 hijacked devices damaging smart-city services last year. Enterprises hence confront a trade-off between sub-USD 3 hardware and the security overhead that shortens battery life, slowing some Massive Machine Type Communication market deployments.

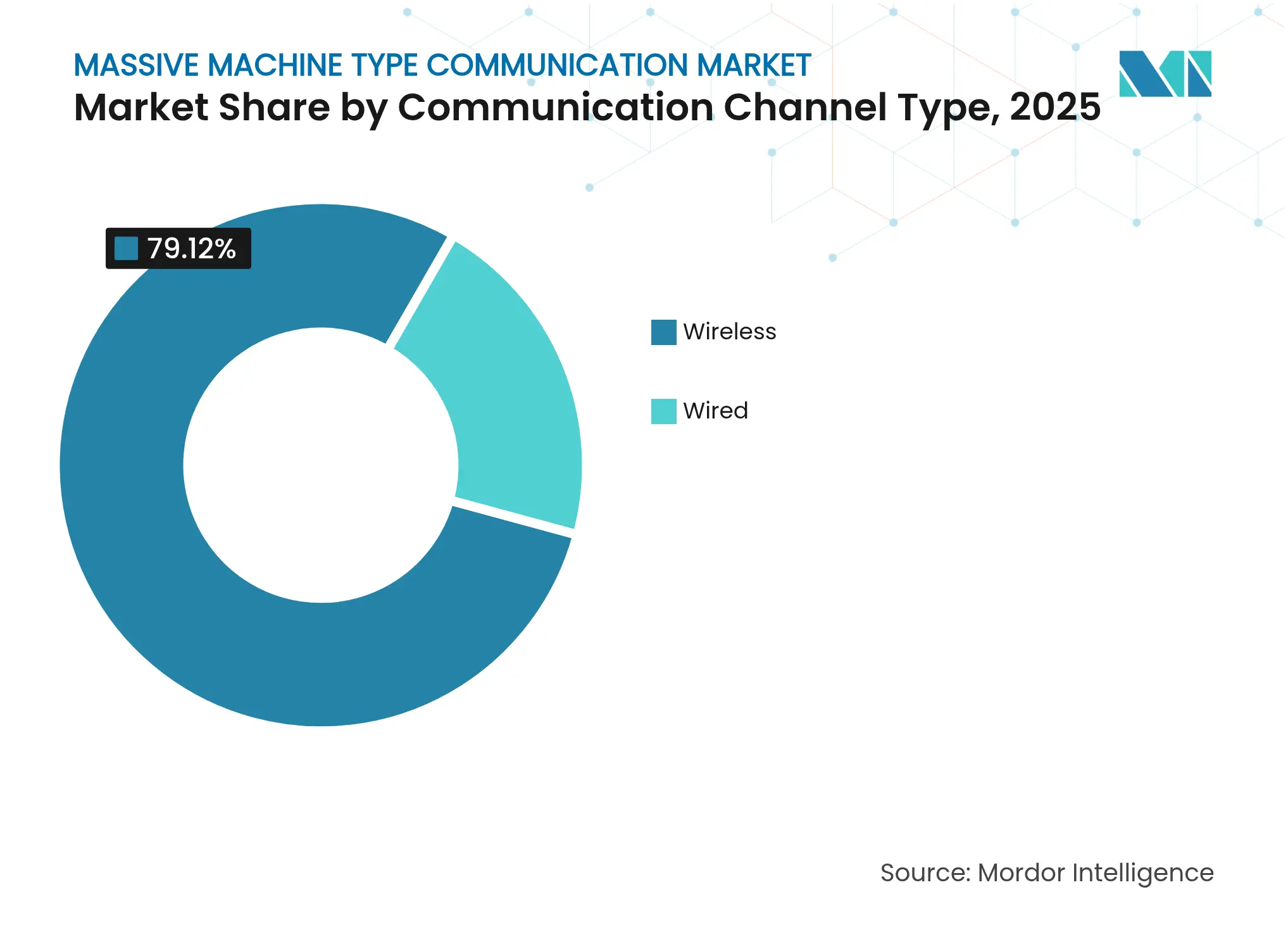

By Communication Channel Type: Wireless Dominates on Infrastructure Economics

Wireless connectivity captured 79.12% of the Massive Machine Type Communication market share in 2025 and maintains a 14.02% growth trajectory as utilities favor NB-IoT and LTE-M over costly trenching for cable. Operators price plans as low as USD 0.50 per node per year, driving a 70% cut in total ownership compared with fiber runs to dispersed meters. Satellite backhaul standardized in 3GPP Release 17 extends reach to the 15% of land where towers remain impractical, adding fresh revenue for carriers in agriculture and mining.

Fiber and Ethernet persist where sub-millisecond latency and multi-gigabit throughput are must-have, such as data centers and automotive production lines. Even so, 5G RedCap now offers 1 Gbps peak uplink under network-slice guarantees, tightening the performance gap with wired connections. As RedCap modules remain under USD 20 and energy-harvesting chips remove battery-swap labor, analysts expect the Massive Machine Type Communication market size for wireless deployments to approach USD 10.02 billion by 2031.

Note: Segment shares of all individual segments available upon report purchase

By Connectivity Technology: RedCap Disrupts NB-IoT Incumbency

NB-IoT retains a 47.83% share of the Massive Machine Type Communication market size thanks to mature module ecosystems and near-universal coverage in China. Yet industrial automation and smart-city systems are already migrating to 5G RedCap to meet sub-50-millisecond latency and 10 Mbps uplink needs. China Mobile’s 600,000 RedCap radios offer a blueprint others will follow, while module costs are forecast to hit USD 10 in 2027 as volumes exceed 50 million units.

LTE-M defends its position in North America through voice and mobility support, especially in fleet monitoring. Dual-mode chipsets like Sequans Monarch 2 ease transitions should carriers decommission NB-IoT bands. Wi-Fi 6/6E, at 16.74%, thrives in indoor smart-building applications where enterprises own the spectrum but sacrifice carrier-grade service guarantees. The interplay among these access types keeps the Massive Machine Type Communication market vibrant but fragmented.

By Deployment Model: Private Networks Gain as Sovereignty Concerns Mount

Public networks account for 63.92% of 2025 spending, yet private 5G deployments grow at 14.35% because factories and energy sites require deterministic performance and data sovereignty. German regulations let firms license local 3.7-3.8 GHz spectrum, and more than 200 enterprises now run private systems, including Bosch and BMW. In the United States, the Department of Defense earmarked USD 600 million for on-base private 5G, signaling institutional faith in the model.

Hybrid approaches combine nationwide public coverage with on-premises micro-cores, letting logistics partners roam while safeguarding in-warehouse latency. This architecture is especially attractive in the Massive Machine Type Communication industry for applications that straddle production floors and distribution corridors. As spectrum-leasing frameworks mature, analysts expect private networks to claim over 34.15% of revenues by 2031.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

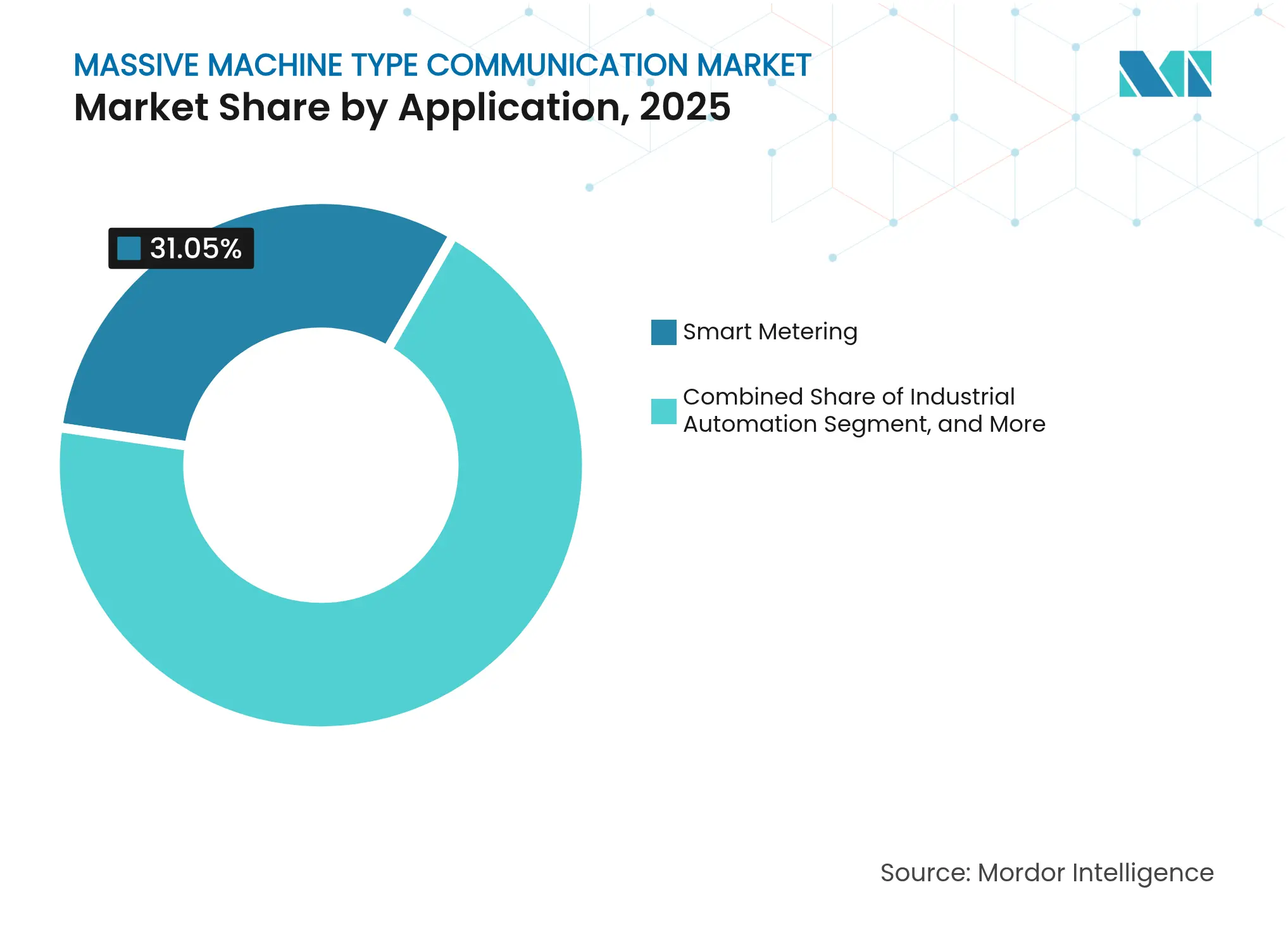

By Application: Industrial Automation Outpaces Smart Metering

Smart metering still leads with 31.05% revenue, but growth moderates as many utilities finish replacing first-generation automatic meter reading. Conversely, industrial automation grows 15.22% annually on the back of digital twins that cut downtime by 30%. Early adopters such as Wanhua Chemical saved 12% energy in petrochemical reactors, proving direct return on investment. Asset tracking holds 21.64% share by connecting containers across borders, leveraging LTE-M’s power-saving features with voice fallback for driver support.

Smart agriculture and smart buildings each contribute low-double-digit slices, benefiting from energy-harvesting sensors that remove maintenance overhead. Analysts forecast that the Massive Machine Type Communication market size related to industrial automation will pass USD 3.28 billion by 2031 as more factories view real-time data flow as core infrastructure.

Note: Segment shares of all individual segments available upon report purchase

By End-User Industry: Manufacturing Surges on Digital-Twin Adoption

Utilities spent 26.12% of 2025 outlays to enable remote disconnection and time-of-use tariffs. Manufacturing, however, accelerates at a 15.54% CAGR as predictive maintenance and quality-inspection use cases multiply. Bosch, BMW, and other adopters prove that tying cellular sensors to cloud analytics raises overall equipment effectiveness by double-digit percentages.

Transportation and logistics at 19.74% share rely on Massive Machine Type Communication market connectivity to reduce theft and cold-chain spoilage. Energy, mining, healthcare, agriculture, and consumer electronics fill the balance. With 400 global mines trialing 5G for underground safety and remote diagnostics, industrial sectors collectively steer future revenue more than consumer gadgets.

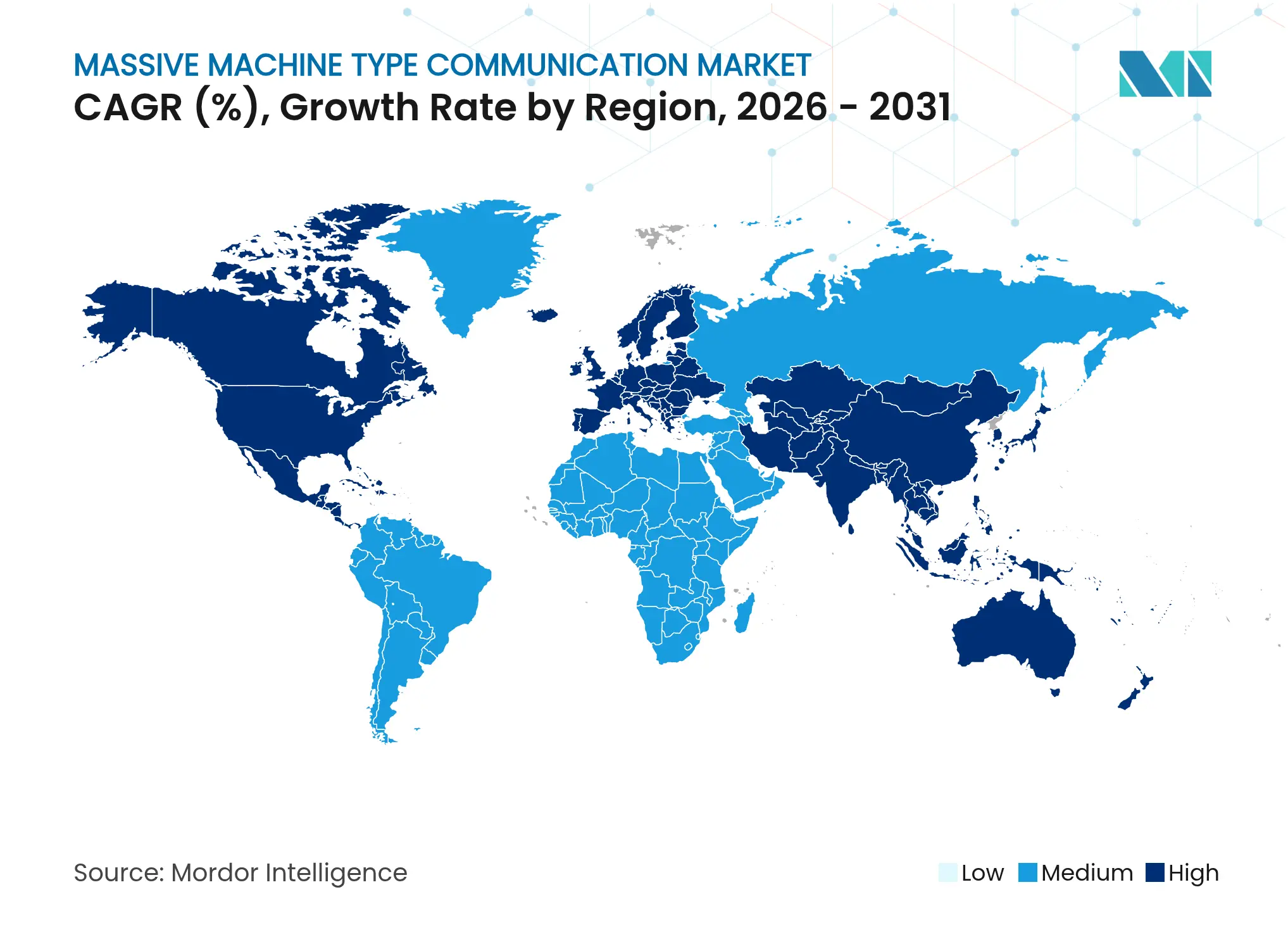

Asia Pacific generated 45.12% revenue in 2025 and is on a 14.18% CAGR path toward 2031. China powers that lead with 2.3 billion cellular IoT connections, supported by mandates that every prefecture-level city deploy RedCap infrastructure. India’s Intelligent Village program and Japan’s SME-focused spectrum subsidies show how public funding anchors demand, while Australia leverages satellite NB-IoT for livestock monitoring over vast ranches.

North America holds 28.08% market share. AT&T migrated NB-IoT subscribers to LTE-M in early 2025, a move that underscores spectrum-refarming risk but also clears paths for RedCap adoption. Verizon’s partnership with Skylo added satellite overlay for Alaska and offshore oil rigs, extending reach where towers are uneconomical. Canada and Mexico each carved mid-band allocations tailored to private 5G, reflecting growing enterprise ownership of connectivity.

Europe accounts for 20.02% revenue amid balanced regulatory pushes and carrier initiatives. Vodafone’s 170,000-site RedCap tender signals that multinationals will soon see uniform service across the region. Germany and France opened dedicated bands for private networks, letting factories bypass public infrastructure and fine-tune latency guarantees. The EU Cyber Resilience Act raises security baselines, potentially slowing ultra-low-cost module imports but boosting trust among industrial buyers.

South America, the Middle East, and Africa together represent roughly 6.78% of current revenues, yet smart-meter rollouts and agriculture pilots in Chile, Brazil, the United Arab Emirates, and South Africa illustrate rising interest. Satellite NB-IoT is especially compelling across mining belts in Peru and gold fields in Ghana, where terrestrial rollouts remain years away.

Market Concentration

The Massive Machine Type Communication market features moderate concentration. Huawei, Ericsson, and Nokia collectively supply roughly 60% of base-station gear, while Qualcomm, Intel, and Samsung command about 70% of modem revenue. Each vendor now bakes RedCap into core product lines, ensuring feature parity and de-risking carrier adoption.[3]Huawei Technologies, “Net5.5G and RedCap Infrastructure,” huawei.com

Mobile operators adopt blended strategies. Vodafone and Deutsche Telekom bundle connectivity with device management to fend off hyperscaler incursions. AT&T and Verizon focus on spectrum efficiency, freeing low-band frequencies for 5G mid-band while nudging customers toward LTE-M and RedCap. Such moves create openings for dual-mode module vendors who soften technology-shift shocks.

Component specialists diversify solutions. e-peas and STMicroelectronics ship energy-harvesting chips that slash maintenance costs for one-million-node projects, while Sequans channels France 2030 funds into sub-USD 10 eRedCap modems. Semtech’s integration of Sierra Wireless gives customers hybrid cellular-LoRaWAN options to hedge against carrier coverage gaps. As service level agreements tighten, software orchestration layers, not just hardware, become critical differentiators.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Massive machine type communication (MTC), also known as massive machine communication (MMC) or massive Machine to Machine communication, is a type of communication between machines over wired or wireless networks where data generation, information exchange, and actuation occur with minimal or no human intervention.

The Massive Machine Type Communication Market Report is Segmented by Communication Channel Type (Wired, Wireless), Connectivity Technology (NB-IoT, LTE-M, 5G NR RedCap, Wi-Fi 6/6E), Deployment Model (Public Network, Private Network, Hybrid Network), Application (Smart Metering, Asset Tracking, Industrial Automation, Smart Agriculture, Smart Buildings), End-User Industry (Utilities, Transportation and Logistics, Manufacturing, Energy and Mining, Healthcare, Agriculture, Consumer Electronics), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Accelerating Additive Manufacturing Adoption in India

3 Min Read

Pricing Strategy for Semiconductor Components

3 Min Read

Market Analysis of Synthetic Food Colorants for a Beverage Leader

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.