Maritime Surveillance Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 27.44 Billion |

| Market Size (2031) | USD 38.02 Billion |

| Growth Rate (2026 - 2031) | 6.74% CAGR |

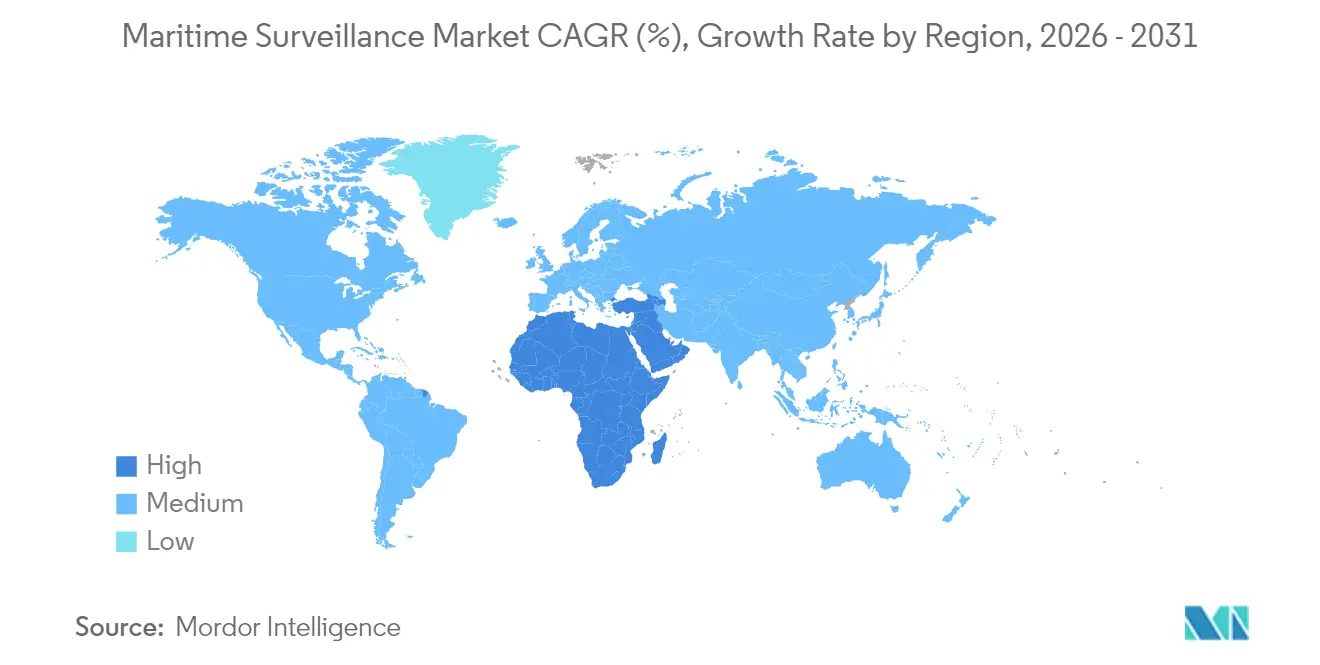

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

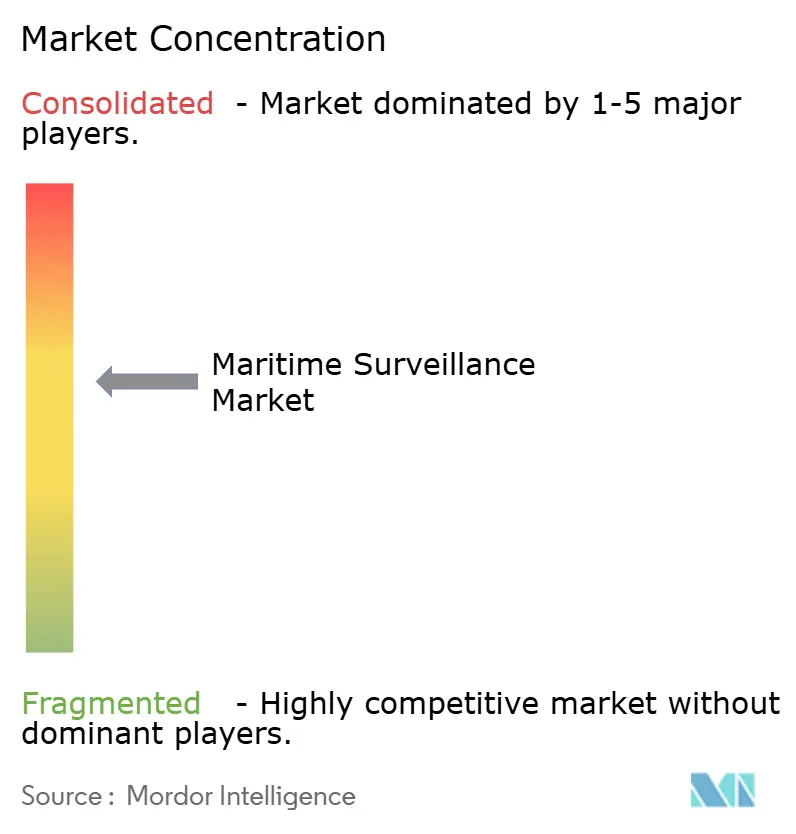

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Maritime Surveillance Market Analysis by Mordor Intelligence

The maritime surveillance market size in 2026 is estimated at USD 27.44 billion, growing from 2025 value of USD 25.71 billion with 2031 projections showing USD 38.02 billion, growing at 6.74% CAGR over 2026-2031. Rising grey-zone coercion in exclusive economic zones, accelerated naval modernization, and adoption of autonomous ISR swarms underpin this momentum. Governments prioritize sensor-fusion architectures that compress detect-to-engage timelines, while export-control chokepoints spur allied co-development of advanced sensors. Demand gravitates toward software-defined command-and-control (C2) layers that orchestrate multi-domain data streams at kill-web speed, stimulating procurement of AI-enabled analytics. Simultaneously, lifecycle cost pressures encourage modular upgrades that reuse hulls but insert new radars or cloud-linked processors, creating retrofit opportunities for primes and tier-2 software vendors.

Key Report Takeaways

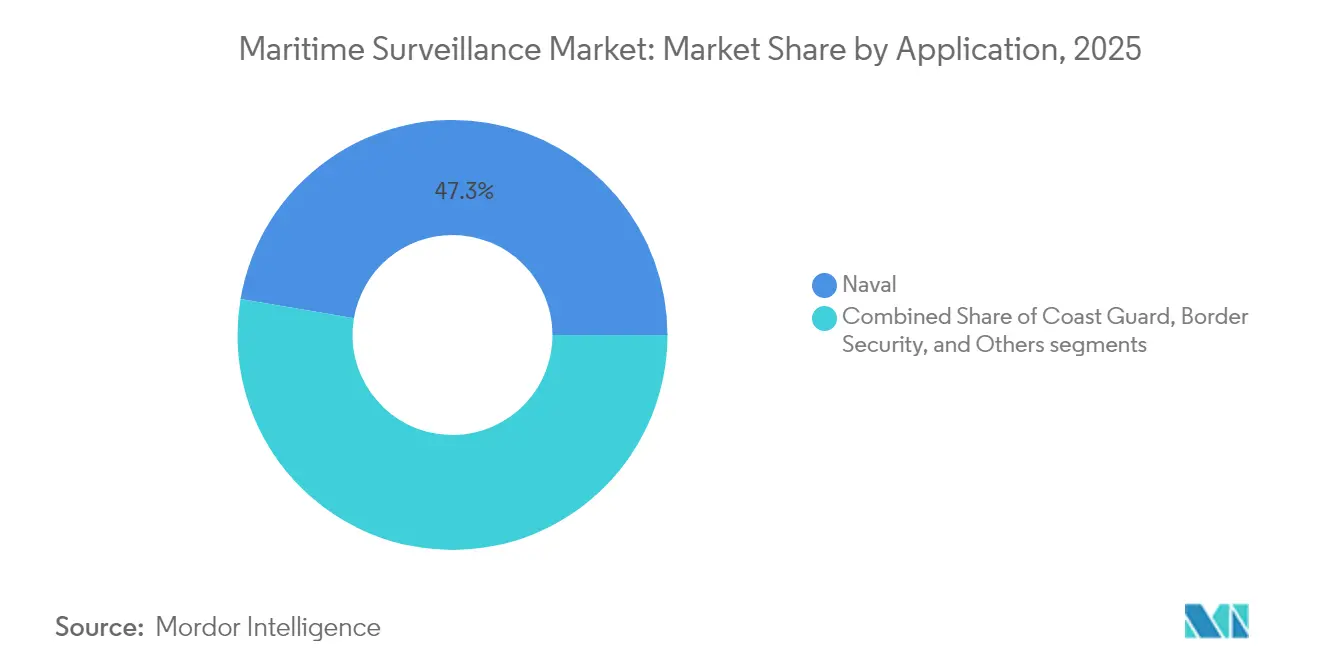

- By application, naval operations led with 47.32% revenue share in 2025; border security is projected to expand at an 8.05% CAGR through 2031.

- By platform, coastal/fixed installations captured 38.40% of the maritime surveillance market share in 2025, while airborne systems are advancing at an 8.28% CAGR to 2031.

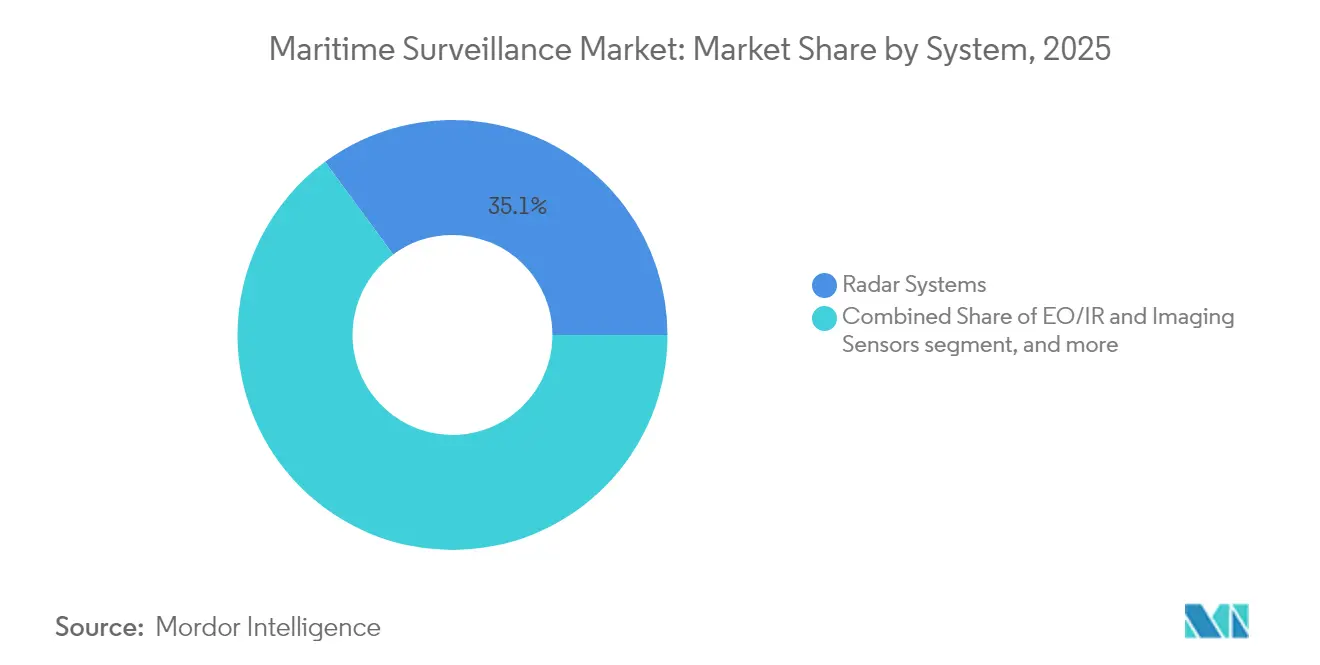

- By system, radar accounted for a 35.10% share of the maritime surveillance market in 2025, and integrated C2/analytics software is progressing at an 8.76% CAGR through 2031.

- By component, hardware held a 64.60% share of the maritime surveillance market in 2025; software recorded the fastest growth at a 9.12% CAGR.

- By geography, North America commanded a 35.10% share of the maritime surveillance market in 2025, whereas the Middle East and Africa registered an 8.94% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Maritime Surveillance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grey-zone maritime coercion and contested EEZs | +1.2% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Indo-Pacific naval modernization race | +1.5% | APAC, North America, Europe | Long term (≥4 years) |

| Rapid fielding of autonomous ISR strike swarms | +0.8% | Global, led by North America and Europe | Short term (≤2 years) |

| AI-enabled sensor-fusion for kill-web speed | +1.1% | Global, advanced military markets | Medium term (2-4 years) |

| Hypersonic-era early-warning radar upgrades | +0.9% | North America, Europe, APAC | Long term (≥4 years) |

| Space-to-sea ISR layer for joint all-domain ops | +1.3% | Global, space-capable nations | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Grey-zone maritime coercion and contested EEZs

States leverage non-kinetic tactics below conflict thresholds to assert claims, as seen in South China Sea ship militia maneuvers.[1]Source: Center for Strategic and International Studies, “Dangerous Ground: South China Sea Fisheries,” csis.org Continuous monitoring that discriminates fishing trawlers from covert militia hulls is therefore essential. The Enhanced Defense Cooperation Agreement supports the Philippines' acquisition of persistent surface-air sensor grids to cross-cue unmanned assets.[2]Source: Philippine Department of National Defense, “EDCA Implementation Strengthens Maritime Security,” dnd.gov.ph This environment boosts orders for high-resolution coastal radar, AIS spoofing detection, and pattern-of-life analytics that flag abnormal loitering.

Indo-Pacific naval modernization race

Regional defense budgets rise 7.2% annually, funding carrier groups, destroyers, and long-range missiles that depend on resilient surveillance backbones. Japan integrates multifunction radar masts for counter-strike missions, while Australia’s AUKUS submarine enterprise specifies an acoustic array networked to space-based relays.[3]Source: Australian Department of Defence, “AUKUS Submarine Program Progress Update,” defence.gov.au Interoperability mandates open-architecture mission systems, propelling maritime surveillance market demand for modular, sovereign-configurable suites.

Rapid fielding of autonomous ISR strike swarms

The US Ghost Fleet Overlord tests validated unmanned surface vessels that self-organize across theaters. Swarm logic optimizes sensor placement, multiplying surveillance footprints without equivalent manpower. Commercial offshore operators mirror this with autonomous AUVs for pipeline inspection, illustrating civil-mil convergence that widens the maritime surveillance market. Edge-cloud fusion engines that ingest dozens of low-power feeds now outpace human analysts, elevating software value.

AI-enabled sensor-fusion for kill-web speed

Hypersonic threats compress decision loops to seconds, spurring adoption of machine-learning classifiers that triage multiband inputs at machine velocity. NATO’s Maritime Unmanned Systems Initiative pushes federated data models so allies share real-time tracks. Vendors embedding explainable AI gain an advantage, as customers insist on human-in-the-loop assurance without losing speed.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Export-control choke-points on advanced sensors | -0.7% | Global, non-allied nations | Short term (≤2 years) |

| Multi-domain C2 interoperability gaps | -0.6% | Global, coalition ops | Medium term (2-4 years) |

| High lifecycle cost of AESA and DEW-ready radars | -0.8% | Global, budget-constrained | Long term (≥4 years) |

| Cyber-attack surface expansion in networked fleets | -0.5% | Global, advanced navies | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Export-control choke-points on advanced sensors

Export-control choke-points on advanced sensors continue to fracture procurement pathways. Under the US International Traffic in Arms Regulations (ITAR) and the European Union's (EU's) dual-use control lists, gallium nitride (GaN) power amplifiers, ultra-low-noise receivers, and digital radio-frequency memory chips are treated as strategic assets. Licenses for these components can stretch 12-18 months and often contain strict re-export clauses that complicate multinational integration programs. As a result, allied navies secure next-generation AESA arrays and electronic-warfare-resistant processors first, while non-aligned buyers are funneled toward less capable legacy designs. To mitigate the gap, several Asia–Pacific and Middle Eastern shipyards have launched co-production lines, pairing local assembly with tier-2 semiconductor fabrication, thereby planting seeds for future joint ventures that might eventually bypass current choke-points

Multi-domain C2 interoperability gaps

Multi-domain C2 interoperability gaps stem from decades of platform-specific data formats, bandwidth-hungry video feeds, and incompatible encryption suites. Older vessels still broadcast track files in proprietary message sets that new unmanned assets cannot parse, forcing operators to employ protocol translators that add latency and risk data truncation during peak activity. Although NATO’s Federated Mission Networking framework defines a common standard, implementation varies by nation, and coalition exercises routinely surface schema mismatches that delay fused targeting solutions. These issues grow more acute as maritime forces attempt to synchronize with space, cyber, and land sensors, revealing that technical fixes must be paired with sustained governance and cyber-accreditation reforms to deliver a truly joint all-domain picture

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Naval Dominance Drives Border Security Surge

Naval missions generated USD 12.16 billion of the maritime surveillance market size in 2025 and retained 47.32% leadership owing to fleet modernization across the US, China, and India. Sensor-rich destroyers link with space relays to extend detection horizons, while carrier air wings integrate AI-enabled EO/IR pods for sea-control operations. The maritime surveillance industry also sees high-endurance unmanned surface vessels (USVs) blended into battle networks, lowering per-mile coverage cost. Border security trailblazes growth at an 8.05% CAGR as coastal nations automate migration interdiction and anti-smuggling patrols using shore radars fused with UAV feeds.

Commercial ports, fisheries, and offshore energy operators adopt dual-use surveillance suites, benefitting from spill-over R&D. Environmental agencies exploit AI classifiers originally coded for submarine detection to flag illegal dumping. This convergence broadens the buyer base, enlarging the maritime surveillance market even where defense budgets plateau.

By Platform: Airborne Systems Accelerate Beyond Coastal Infrastructure

Coastal and fixed sites accounted for 38.40% of the maritime surveillance market share in 2025, anchored by long-range over-the-horizon radars guarding straits and EEZ borders. Yet airborne assets outpace stationary nodes with an 8.28% CAGR as P-8 Poseidon upgrades and UAV procurements proliferate. The maritime surveillance industry embraces attritable drones that loiter 24+ hours, passing detections via satcom to distributed ops centers.

Surface vessels integrate low-probability-of-intercept radars and deck-mounted EO turrets, extending sensing arcs for distributed lethal networks. Sub-surface acoustic arrays map helical routes of quiet diesel-electric subs, though capex confines uptake to major navies. As airborne ISR costs fall, smaller states leapfrog to aerial coverage rather than erect costly coastal towers, reshaping geographic spend patterns within the maritime surveillance market.

By System: Software Analytics Outpace Radar Dominance

Given its all-weather tracking value, radar still commands a 35.10% share of the maritime surveillance market. However, integrated C2 and analytics suites expand 8.76% annually as navies prioritize cognitive systems that slash operator burden. Sensor-agnostic middleware ingests radar, sonar, AIS, and satellite images to build single-pane maritime pictures. Vendors differentiate through real-time anomaly detection, false-alarm suppression, and predictive course-of-action algorithms.

EO/IR payloads add positive ID, feeding classification AI that has migrated from self-driving car perception stacks. Sonar chains detect undersea infrastructure threats, while passive RF arrays such as TwInvis exploit civilian broadcasts to locate stealth aircraft without emitting. This multi-phenomenology demand invigorates the maritime surveillance industry’s software segment, converting hardware data streams into decision advantage.

By Component: Software Revolution Transforms Hardware-Centric Market

Hardware kept 64.60% of the maritime surveillance market in 2025 due to capital-intensive antennas and stabilized gimbals. Nonetheless, software revenues are growing 9.12% yearly, reflecting cloud-edge pipelines that deploy micro-services afloat. AI model updates enhance threat libraries without dry-dock periods, sustaining platform relevance. This shift aligns with customers' desire for open APIs that avoid vendor lock-in, compelling primes to open proprietary buses or risk displacement by agile ISVs.

Cybersecure DevSecOps pipelines emerge as differentiators; navies demand software bills-of-material and continuous vulnerability scanning. Consequently, the maritime surveillance market now values certification bodies and digital-twin testing labs on par with physical test ranges.

Geography Analysis

North America retained 35.10% of the maritime surveillance market share in 2025, supported by USD 19 billion yearly US Navy and Coast Guard modernization outlays. Distributed maritime operations hinge on sensor-rich surface combatants, while the Coast Guard backs Offshore Patrol Cutters with AESA and AI analytics for counter-narcotics. Canada funds Polar Epsilon Next to surveil melting Arctic sea lanes via RADARSAT-Constellation imagery downlinked to Halifax. Mexico integrates coastal radars with UAVs to curb drug-laden semi-submersibles.

The Middle East and Africa posts the fastest 8.94% CAGR as GCC states shield the Strait of Hormuz tanker routes amid drone and mine incidents. Saudi Arabia bundles maritime surveillance packages into Vision 2030 coastal megaprojects. UAE pioneers unmanned surface picket lines, leveraging foreign partnerships for sovereign data control. Israel deploys autonomous patrol craft around gas rigs, coupling ELINT sensors with AI correlation engines. South Africa upgrades Kelvin radar chain to monitor illegal fishing and vessel-borne pollution around the Cape.

Europe and Asia-Pacific exhibit steady uptake tied to unique threat vectors. Europe funds Mediterranean SAR and Arctic situational awareness using Galileo PRS signals for encrypted vessel tracking. Asia-Pacific modernization remains the maritime surveillance market’s strategic fulcrum, but export-control bifurcation means US allies access GaN radars while others diversify toward Israeli or indigenous sensors. Japan rolls out shipborne OQQ-25 sonars; Australia seeds sovereign AI labs for anti-submarine warfare analytics; India fields coastal surveillance chains under Project Sagarmala.

Competitive Landscape

The maritime surveillance market is moderately consolidated. Lockheed Martin, Elbit Systems, and Thales anchor naval radar and C2, enjoying deep classified program pipelines. Strategic moves in 2024 signal a pivot to software; Lockheed’s USD 1.2 billion Aegis refresh integrates satellite data in real time. Thales delivered GaN-based Sea Fire radars, touting 25% lower power draw.

Mid-tier specialists expand through M&A: Kongsberg’s USD 85 million purchase of Maritime Robotics grants autonomous vessel IP, while L3Harris debuts AI-fused sensor suites for P-3 upgrades. Start-ups target edge analytics; Terma pairs with Microsoft Azure Government to host classified maritime AI models. Competition intensifies around passive radar and cyber-resilient mesh networks, with Hensoldt’s TwInvis and Northrop’s ZPY-8 integrations illustrating shifting R&D weight toward multi-phenomenology sensing.

Success hinges on meeting export regulations and cyber accreditation. Vendors offering ITAR-compliant open architectures with zero-trust baselines win multinational tenders. Partnerships between primes and cloud hyperscalers aim to balance classified handling with elastic compute, shaping the future structure of the maritime surveillance industry.

Maritime Surveillance Industry Leaders

Thales Group

Kongsberg Gruppen ASA

Saab AB

Elbit Systems Ltd.

L3Harris Technologies, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Dassault Aviation secured a contract from the French Defense Procurement and Technology Agency (DGA) to supply five Falcon 2000 Albatros aircraft for the Maritime Surveillance and Intervention Aircraft (AVSIMAR) program.

- July 2025: Defense contractor Lockheed Martin developed an AI-powered Synthetic Aperture Radar (SAR) system for enhanced maritime surveillance. The company demonstrated automatic target recognition capabilities during flight tests on the US West Coast, integrating autonomous sensor control for improved maritime target detection and tracking.

Global Maritime Surveillance Market Report Scope

Maritime surveillance involves the collection, analysis, data fusion, and sharing of data. The information is captured through a wide variety of sensors and sensor combinations operating in various segments of the spectrum (electronic signals, imagery, communications, and acoustics, amongst others.

The report has been segmented by application, component, type, and geography. By application, the market is segmented into naval, coastguard, and others. The market is segmented by components: radar, sensor, transponder, and others. By type, the market is segmented into surveillance and tracking, detector, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa. The report also covers market sizes and forecasts of different geographical regions. Moreover, the report offers a market forecast represented by USD million. Furthermore, the report includes various key statistics on the market status of leading market players and provides key trends and opportunities in maritime surveillance.

| Naval |

| Coast Guard |

| Border Security |

| Others |

| Coastal/Fixed Installations |

| Surface Vessels |

| Airborne (MPA, UAV) |

| Sub-Surface (UUV/USV relay) |

| Radar Systems |

| EO/IR and Imaging Sensors |

| AIS and Identification Systems |

| Sonar and Acoustic |

| Integrated C2/Analytics Software |

| Communications and Datalinks |

| Hardware |

| Software |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| Israel | ||

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Application | Naval | ||

| Coast Guard | |||

| Border Security | |||

| Others | |||

| By Platform | Coastal/Fixed Installations | ||

| Surface Vessels | |||

| Airborne (MPA, UAV) | |||

| Sub-Surface (UUV/USV relay) | |||

| By System | Radar Systems | ||

| EO/IR and Imaging Sensors | |||

| AIS and Identification Systems | |||

| Sonar and Acoustic | |||

| Integrated C2/Analytics Software | |||

| Communications and Datalinks | |||

| By Component | Hardware | ||

| Software | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| Israel | |||

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the global value of the maritime surveillance market in 2026?

The maritime surveillance market size is valued at USD 27.44 billion in 2026.

How fast will maritime surveillance revenues grow between 2026 and 2031?

Aggregate revenues are projected to rise at a 6.74% CAGR, reaching USD 38.02 billion by 2031.

Which application area is expanding the quickest?

Border security leads growth at an 8.05% CAGR as nations automate coastal interdiction and anti-smuggling patrols.

Which platform type is seeing the strongest demand increase?

Airborne platforms, including maritime patrol aircraft and UAVs, are advancing at an 8.28% CAGR through 2031.

Which region is expected to record the highest growth rate?

Middle East and Africa shows the fastest regional CAGR at 8.94% due to heightened tanker-lane security investments.

What technology trend is transforming future surveillance capabilities?

AI-enabled sensor-fusion that delivers kill-web-speed decisions is reshaping command-and-control architectures across fleets.

Page last updated on: