Maritime Patrol Aircraft Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 15.17 Billion |

| Market Size (2031) | USD 21.03 Billion |

| Growth Rate (2026 - 2031) | 6.75% CAGR |

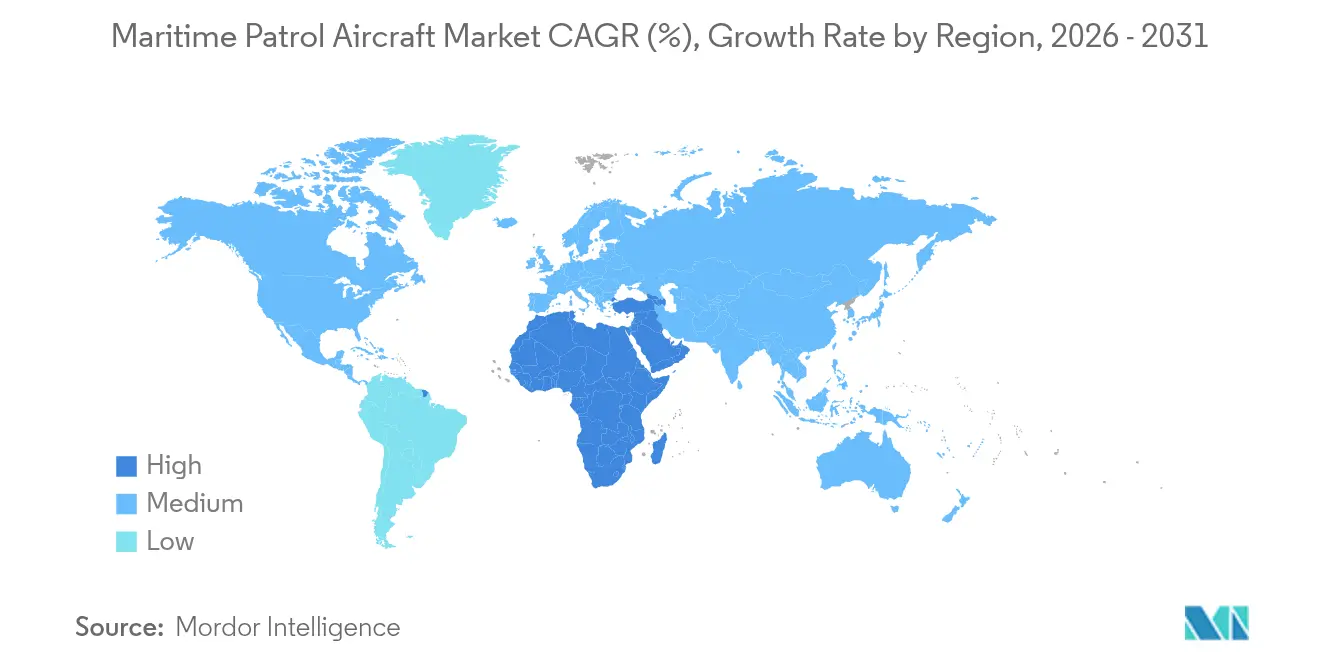

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

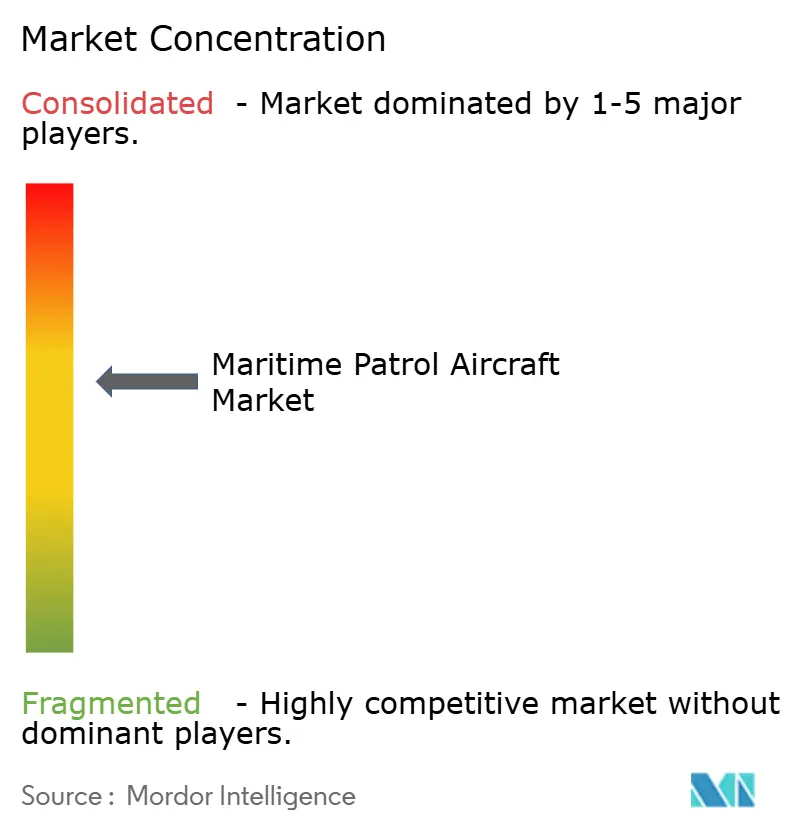

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Maritime Patrol Aircraft Market Analysis by Mordor Intelligence

Maritime patrol aircraft market size in 2026 is estimated at USD 15.17 billion, growing from 2025 value of USD 14.21 billion with 2031 projections showing USD 21.03 billion, growing at 6.75% CAGR over 2026-2031. Growing submarine activity, rising blue-economy enforcement, and the shift toward manned-unmanned teaming underpin sustained demand. Fleet-replacement cycles for Cold War-era aircraft continue to generate large, multi-year procurement pipelines, while cost pressures are accelerating interest in modular sensor pods and hybrid-electric propulsion. North America maintains leadership on the back of the US Navy’s P-8A program and allied standardization. Yet, the Middle East and Africa show the fastest growth as coastal states fund new maritime-security missions.[1]Source: FlightGlobal, “Boeing lands $3.4 billion contract for Canadian, German P-8As,” flightglobal.com Supply-chain bottlenecks in specialized sonobuoys and export-control limits on advanced radars remain structural constraints that could alter competitive dynamics over the decade.

Key Report Takeaways

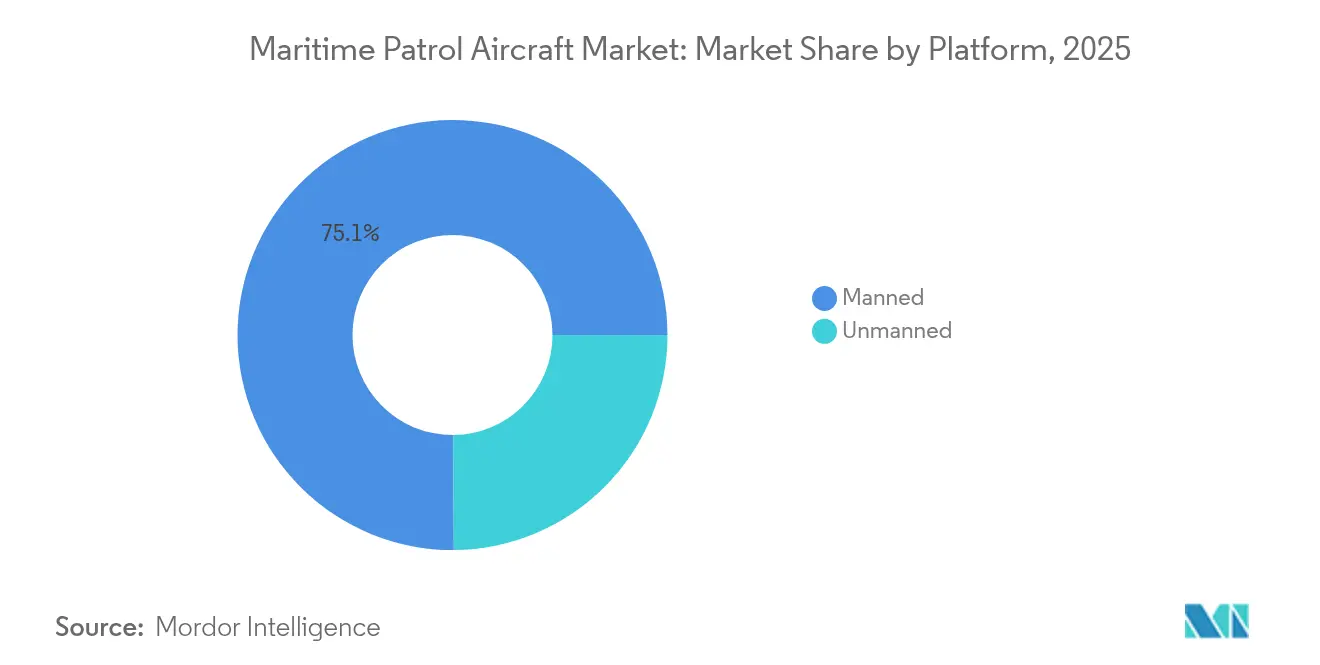

- By platform type, manned aircraft held 75.10% of the maritime patrol aircraft market share in 2025, while unmanned systems posted the fastest 9.78% CAGR through 2031.

- By propulsion, jet-powered designs dominated revenue by 85.05% in 2025, but electric systems are advancing at 11.86% CAGR as hybrid-electric programs mature.

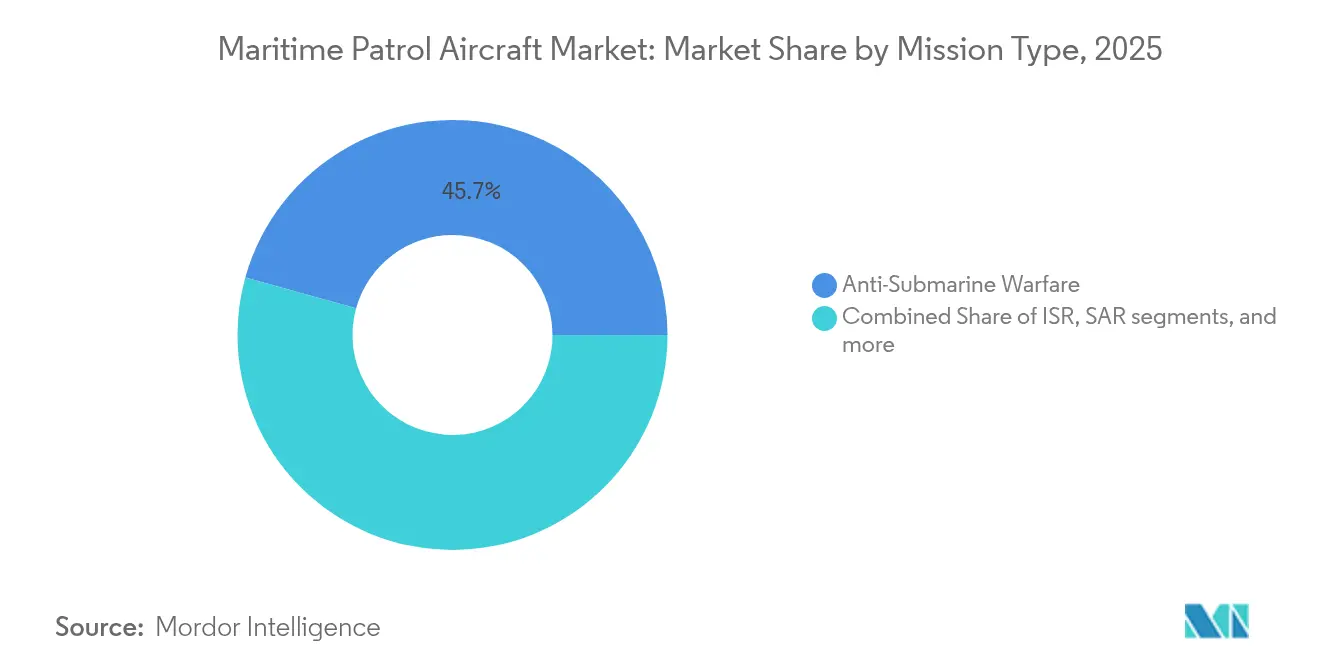

- By mission, anti-submarine warfare accounted for 45.70% of the maritime patrol aircraft market size in 2025; border and EEZ patrol is rising at a 9.35% CAGR to 2031.

- By end user, naval forces led with 61.65% revenue share in 2025, while coast guards recorded the highest 11.88% CAGR through 2031.

- By geography, North America commanded a 38.20% market share in 2025; the Middle East and Africa are projected to advance at a 10.06% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Maritime Patrol Aircraft Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating long-range anti-submarine warfare requirements | +1.8% | Global, with concentration in Indo-Pacific and North Atlantic | Medium term (2-4 years) |

| Replacement of ageing P-3/P-8 fleets with multi-mission platforms | +2.1% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Integration of unmanned "loyal-wingman" concepts with MPAs | +1.2% | North America, Australia, with spillover to NATO allies | Medium term (2-4 years) |

| Modular sensor pods enabling rapid role change | +0.9% | Global, early adoption in technologically advanced markets | Short term (≤ 2 years) |

| Blue-economy monitoring mandates (IUU fishing, seabed mining) | +0.7% | Global coastal states, emphasis on developing nations | Long term (≥ 4 years) |

| Defence "Green-Deal" push for hybrid-electric propulsion | +0.5% | Europe, North America, with gradual global adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Long-Range Anti-Submarine Warfare Requirements

Renewed submarine build-ups by China and Russia compelled navies to prioritise platforms with 11-plus-hour endurance, multistatic sonar processing, and extended sensor fusion. The US Navy completed P-8A Increment 3 Block 2 upgrades in 2025 to meet these requirements. Germany’s order of 8 P-8As and Japan’s record JPY 7.95 trillion (USD 54.70 billion) defence budget underline the shift from coastal to blue-water ASW. Indo-Pacific nations with expansive EEZs see persistent surveillance as essential for deterring undersea incursions that legacy P-3 fleets cannot counter.

Replacement of Ageing P-3/P-8 Fleets with Multi-Mission Platforms

More than 600 veteran Orion aircraft across 20 countries are nearing retirement, positioning fleet renewal as the largest modernisation wave in maritime aviation history. South Korea accelerated its transition to P-8A after a 2025 P-3 crash, illustrating how safety events compress replacement timelines. France’s Airbus A321 MPA choice over a smaller Falcon platform signals a preference for payload-rich, multi-mission airframes. Nations lacking large defence budgets are adopting lower-cost C295 or C-130 mission kits to bridge capability gaps.

Integration of Unmanned “Loyal-Wingman” Concepts with MPAs

Successful teaming trials between Boeing’s MQ-28 Ghost Bat and RAAF E-7A early-warning aircraft in June 2025 validated open-architecture protocols for future maritime patrol cooperation.[2]Source: Boeing, “Boeing, RAAF Demonstrate MQ-28 Teaming with E-7A Wedgetail,” boeing.com The US Marine Corps exercises with Kratos XQ-58A drones displayed forward-sensor roles that extend P-8A coverage. General Atomics paired SeaGuardian UAVs with Saab airborne-warning sensors, underscoring a trend toward distributed, unmanned pickets supporting manned commanders. The approach allows states with limited pilots to blanket larger sea areas without proportionate manpower growth.

Modular Sensor Pods Enabling Rapid Role Change

Northrop Grumman’s OpenPod permits quick swapping between EO/IR, SIGINT, or targeting payloads without structural changes. L3Harris SPYDR II’s Rapid Aircraft Payload Deployment System achieves similar flexibility, reducing turnaround time from days to hours. Lockheed Martin’s C-130 maritime kit offers anti-ship missile launch capability as a roll-on pallet, supporting smaller air forces that cannot afford purpose-built fleets. The modular doctrine matches shrinking budgets and enables rapid response to shifting mission priorities such as disaster relief or counter-piracy.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ballooning unit cost amid low production volumes | -1.4% | Global, particularly affecting smaller defense budgets | Short term (≤ 2 years) |

| Preference shift toward maritime-surveillance drones | -0.8% | Developed markets with advanced UAV capabilities | Medium term (2-4 years) |

| Supply-chain chokepoints for specialised ASW sonobuoys | -0.6% | Global, with acute impact on non-US allies | Short term (≤ 2 years) |

| Export-control barriers on next-gen AESA maritime radars | -0.4% | International markets dependent on US/European technology | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ballooning Unit Cost Amid Low Production Volumes

Unit prices climbed as programs such as MQ-4C dropped from 70 to 27 aircraft, raising per-aircraft cost beyond USD 400 million and stressing customer budgets.[3]Source: Inside Defense, “Drastic cost increase of MQ-4C reflects widespread problem,” insidedefense.com Despite adopting an efficiency-focused production system, Boeing faces similar diseconomies while scaling P-8A output to 1.5 jets per month. RAND analysis shows that each 10% uptick in annual volume can trim about 3% from flyaway cost, underscoring the affordability challenge small-batch buyers endure. Rising complexity in sensor suites magnifies this price curve, creating difficult trade-offs for nations with constrained defence spending.

Supply-Chain Chokepoints for Specialised ASW Sonobuoys

Global production remains dominated by a single joint venture, ERAPSCO, leaving inventories vulnerable to surge demand. The US Navy’s purchase of 166,500 sonobuoys worth USD 219.8 million in 2024 highlighted the strain on manufacturing capacity. Pacific Forum researchers argue Australia could alleviate risk by adding an independent production line, but certification timelines remain long. For mid-tier navies, limited access to SSQ-125A multistatic devices can degrade readiness during protracted ASW operations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform Type: Unmanned Systems Drive Future Growth

The manned fleet retained 75.10% share of maritime patrol aircraft market revenue in 2025, anchored by the P-8A Poseidon and Japan’s P-1, both suited for complex, crew-intensive missions. However, unmanned platforms post a 9.78% CAGR and will steadily erode manned dominance as AI-enabled autonomy matures. Loyal-wingman trials confirm operational viability, and the US Navy’s strong interest in MQ-28 insertion aboard carriers illustrates strategic commitment to mixed fleets.

Cost efficiency, endurance beyond crew limits, and lower risk in contested zones sustain the unmanned appeal. SeaGuardian’s 2024 RIMPAC debut featured sonobuoy dispense and LRASM cueing, proving that UAVs can now execute core ASW and anti-surface tasks. Hybrid architectures where a manned MPA orchestrates multiple autonomous sentinels will dominate force-design discussions through 2031.

By Propulsion System: Electric Revolution Accelerates

Jet engines controlled 85.05% of revenue in 2025, yet hybrid-electric demonstrators such as DARPA’s XRQ-73 achieved first flight, supporting a 11.86% CAGR for electric systems. GE Aerospace’s 1-MW hybrid module for Group 3 UAVs under US Army funding showcases transition momentum.

Electric propulsion reduces acoustic signature, increases loiter time, and aligns with defence-sector carbon goals. The maritime patrol aircraft market size for hybrid-electric demonstrators is modest today, but benefits from dual civilian-military R&D paths. Turboshafts retain relevance for vertical-lift patrol craft, yet sustained electrification funding in Europe and North America hints at wider adoption after 2028.

By Mission Type: Border Patrol Emerges as Growth Driver

Anti-submarine warfare dominated the maritime patrol aircraft market, with a 45.70% share in 2025 as undersea threats intensified. Governments, however, are boosting surface-oriented patrol budgets to protect fishing grounds and seabed resources, pushing border and EEZ security to a 9.35% CAGR.

Persistent IUU enforcement needs sensors tuned to small vessel detection and datalink architectures to share evidence with coastguard cutters. Anti-surface and ISR tasking converge on multi-mission airframes, prompting OEMs to offer rapid role-change kits and cross-domain datalinks for simultaneous ASW, surface, and electronic surveillance missions.

By End User: Coast Guards Drive Modernization

Naval operators held 61.65% revenue in 2025, yet coast-guard agencies post a 11.88% CAGR thanks to broader blue-economy mandates. The US Coast Guard accepted its 17th C-130J and secured USD 183.6 million for additional units, highlighting sovereign investments in long-range surveillance.

Developing nations mirror this trend; India approved 15 C-295 patrol aircraft split between the Navy and the Coast Guard to share maintenance footprints while covering vast EEZs. Across all regions, coast-guard missions now encompass narcotics interdiction, disaster response, and environmental monitoring, driving demand for affordable, modular aircraft.

Geography Analysis

North America commanded 38.20% of the maritime patrol aircraft market revenue in 2025, buoyed by the US Navy’s USD 3.4 billion P-8A buy for Canada and Germany and the ongoing CP-140 Aurora replacement. Indigenous production capacity, established subsystem suppliers, and continuous R&D pipelines safeguard the region’s leadership. Canada’s participation underpins interoperability, while Mexico’s prospective procurement reflects trilateral security integration. Coast Guard Force Design 2028, targeting 15,000 new personnel and next-generation ISR assets, reinforces sustained domestic demand.

Europe continues a robust modernisation cycle as NATO fleets phase out P-3 Orions. Germany’s first P-8A, delivered in February 2025, marked a pivotal milestone in alliance standardisation. France’s Airbus A321 MPA decision underscores the influence of industrial policy on procurement, while Spain’s 16-aircraft C295 order sustains regional workshare. European sustainability policies spur investment in hybrid-electric concepts and sustainable aviation fuel trials for MPAs.

The Middle East and Africa are the fastest expanding regions at 10.06% CAGR to 2031 as Gulf states and African littoral nations strengthen maritime-security architectures. UAE completed its 5-aircraft GlobalEye program and signed a USD 190 million support contract ensuring readiness through the decade. Nigeria’s 50-aircraft procurement pipeline includes patrol models that address piracy and illegal bunkering threats. Offshore energy infrastructure, rising illegal fishing, and Red Sea security tensions drive spending across the region.

Asia-Pacific demonstrates dynamic, multi-tier demand. Japan’s record defence budget funds enhanced P-1 upgrades, while South Korea advances P-8A induction by 2027. India’s C-295 buy for the navy and coast-guard roles exemplifies dual-service acquisition models. Australia’s capital expenditure surge to AUD 6.27 billion by 2029 prioritises maritime domain awareness. Collectively, vast EEZs, contested sea lanes, and accelerating submarine activity underpin a strong regional outlook.

Competitive Landscape

The maritime patrol aircraft market displays moderate concentration. Major players such as The Boeing Company, Lockheed Martin Corporation, and Saab AB are leveraging established government relationships and in-house mission-system integration. Boeing’s backlog spans US, Canadian, and German P-8A orders; Lockheed Martin capitalises on modular C-130 kits and AESA radar exports; and Saab differentiates via multi-domain GlobalEye solutions that blend radar, EW, and SIGINT.

The focus of innovation is shifting toward software and autonomy. General Atomics flew Avengers with AI copilots and is developing the YFQ-42A collaborative combat aircraft, signalling a pivot from pure platform to algorithmic advantage. Northrop Grumman and L3Harris pursue open-architecture pods that broaden aircraft utility and shorten upgrade cycles.

Supply-chain vulnerabilities represent both a threat and an opportunity. ERAPSCO’s dominance of sonobuoys exposes fleets to shortages, encouraging new entrants backed by Australian or Japanese industrial policy. Export-control friction on X-band and AESA radars has accelerated South Korean indigenous development, signalling regional diversification of critical subsystems.

Future competition will hinge on ecosystem partnerships that merge airframe OEMs with AI software vendors, advanced sensor houses, and green propulsion specialists. Companies able to orchestrate these networks are positioned to capture incremental value as mission complexity rises.

Maritime Patrol Aircraft Industry Leaders

The Boeing Company

Lockheed Martin Corporation

Airbus

Saab AB

Leonardo S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: The German Navy unveiled its first fully marked P-8A Poseidon as a potential replacement for its P-3C Orion Maritime Patrol Aircraft. The Bundeswehr announced that Boeing's Seattle factory has completed the full German livery for the inaugural P-8A Poseidon Maritime Patrol Aircraft (MPA) of the German Navy (Deutsche Marine).

- February 2025: Airbus Defence and Space, with Thales, secured a 24-month contract from the French Defence Procurement Agency for a risk-assessment study on future maritime patrol aircraft. The A321 MPA is designed as a “flying frigate,” offering autonomy, reliability, and support for the oceanic nuclear deterrence component.

- November 2024: Boeing clinched a USD 1.68 billion contract modification to produce and deliver seven Lot 13 P-8A Poseidon maritime patrol aircraft to the US Navy.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the maritime patrol aircraft (MPA) market as all new-build, fixed or rotary-wing airframes, crewed or remotely piloted, that are purpose-engineered for long-endurance sea surveillance, anti-submarine or anti-surface warfare, and search and rescue missions. We count factory-installed mission systems in the selling price.

Scope Exclusion: Retrofit kits for legacy transports and generic ISR drones without maritime hardening sit outside this assessment.

Segmentation Overview

- By Platform Type

- Manned

- Unmanned

- By Propulsion System

- Jet Engine

- TurboFan

- TurboProp

- TurboShaft

- Electric Propulsion

- Jet Engine

- By Mission Type

- Anti-Submarine Warfare

- Intelligence, Surveillance and Reconnaissance (ISR)

- Search and Rescue (SAR)

- Anti-Surface Warfare

- Border / EEZ Patrol

- By End User

- Naval Forces

- Coast Guards

- Other Government Agencies

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Our analysts spoke with naval planners, program managers, sustainment chiefs, and procurement attachés across North America, Europe, and Asia-Pacific; their feedback clarified retirement schedules, upcoming tenders, and typical lead times, allowing us to stress test desk findings and bridge gaps.

Desk Research

We first mapped historic deliveries and budget lines using open defense appropriations, NATO and SIPRI transfer logs, fleet registers, and tender notices; these anchor unit counts and costs. Supplemental insight flows from International Maritime Bureau piracy statistics, ICAO traffic tables, trade yearbooks, and OEM filings gathered through D&B Hoovers alongside news archived on Dow Jones Factiva and Aviation Week, letting us track threat levels and technology shifts. Many other public records were reviewed to tighten timelines and cost curves.

Market-Sizing & Forecasting

Mordor's model starts with a top-down rebuild: declared program outlays and maritime branch capital budgets are translated into annual aircraft equivalents through benchmark acquisition costs, then cross-checked with sampled OEM price-volume disclosures. Key variables like protected coastline length, submarine incident frequency, platform replacement age, real defense spending growth, sensor suite cost share, and learning curve price erosion feed a multivariate regression that projects demand through 2030. Scenario analysis brackets upside from faster unmanned adoption.

Data Validation & Update Cycle

Each draft runs through variance dashboards that flag anomalies versus historic delivery series and peer ratios; a second analyst signs off after resolution. Reports refresh yearly, with interim updates triggered by any single contract worth more than five percent of prior year demand.

Why Our Maritime Patrol Aircraft Baseline Earns Trust

Published estimates often diverge because providers mix scopes, convert currencies on different dates, or fold refurbishment spend into aircraft value. According to Mordor analysts, our disciplined scope selection and annual refresh give decision makers a balanced middle figure.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 14.21 B (2025) | Mordor Intelligence | - |

| USD 18.66 B (2025) | Global Consultancy A | Includes sensor retrofits and depot overhauls |

| USD 7.50 B (2024) | Regional Consultancy B | Omits unmanned coastal patrol aircraft |

| USD 19.41 B (2024) | Trade Journal C | Blends patrol aircraft with wider surveillance rotorcraft |

These comparisons show that our transparent variables and repeatable steps offer a dependable baseline that clients can audit with publicly traceable inputs.

Key Questions Answered in the Report

What is the current size of the maritime patrol aircraft market?

The maritime patrol aircraft market is valued at USD 15.17 billion in 2026 and is projected to reach USD 21.03 billion by 2031, witnessing a 6.75% CAGR over 2026-2031.

Which segment is growing fastest within the market?

Unmanned platforms are the fastest-growing, posting a 9.78% CAGR through 2031 as manned-unmanned teaming gains traction.

Why are coast guards investing heavily in new patrol aircraft?

Expanding blue-economy enforcement, narcotics interdiction and disaster-response roles are driving coast-guard demand, resulting in a 11.88% CAGR to 2031.

Which region leads in maritime patrol aircraft procurement?

North America leads with 38.20% market share on the strength of the US P-8A program and allied aircraft acquisitions.

What technologies are reshaping future maritime patrol aircraft?

Key technologies include hybrid-electric propulsion, modular sensor pods and AI-enabled loyal-wingman drones that extend surveillance reach while reducing crew risk.

What supply-chain risks could hinder market growth?

Dependence on a single sonobuoy supplier and export-control barriers on advanced radars create vulnerabilities that may delay capability upgrades for several navies.

Page last updated on: