Ship Port Infrastructure Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 221.61 Billion |

| Market Size (2031) | USD 278.62 Billion |

| Growth Rate (2026 - 2031) | 4.69% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

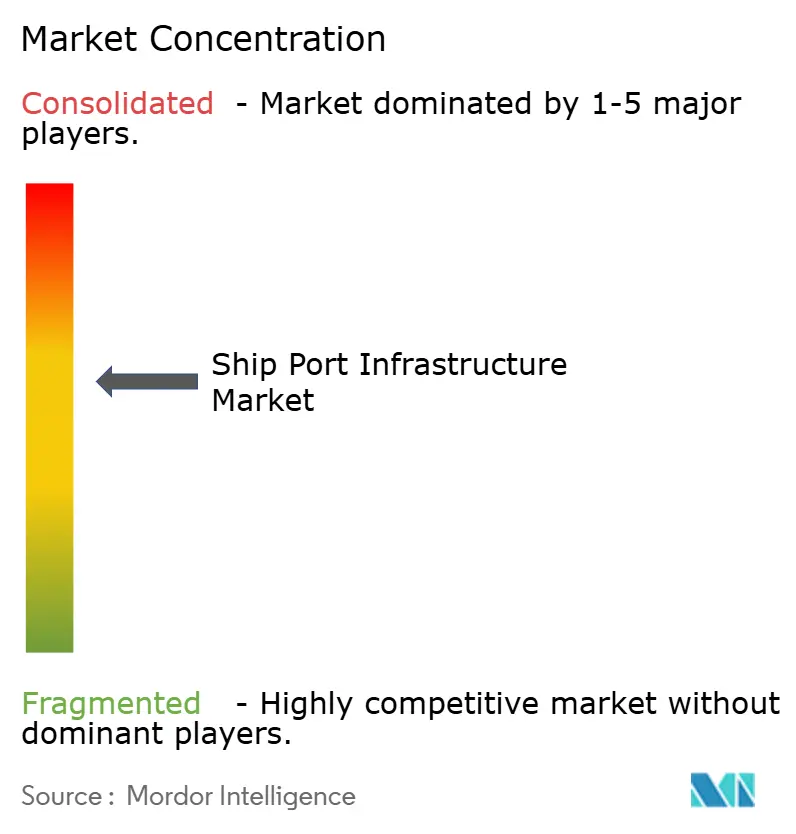

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ship Port Infrastructure Market Analysis by Mordor Intelligence

Ship Port Infrastructure Market size in 2026 is estimated at USD 221.61 billion, growing from 2025 value of USD 211.68 billion with 2031 projections showing USD 278.62 billion, growing at 4.69% CAGR over 2026-2031. This growth reflects a decisive global shift toward automation, climate-resilient engineering, and alternative-fuel readiness, reshaping competitive advantages in the ship port infrastructure market. Public-sector stimulus programs are unlocking large modernization pipelines, private 5G roll-outs tightening equipment synchronization, and mandatory decarbonization timelines force ports to electrify cargo-handling fleets and upgrade on-shore power systems. Near-shoring is also re-routing container volumes toward secondary coastal and inland nodes, broadening the geographic footprint of the ship port infrastructure market while intensifying the race for capital-efficient expansion.

Key Report Takeaways

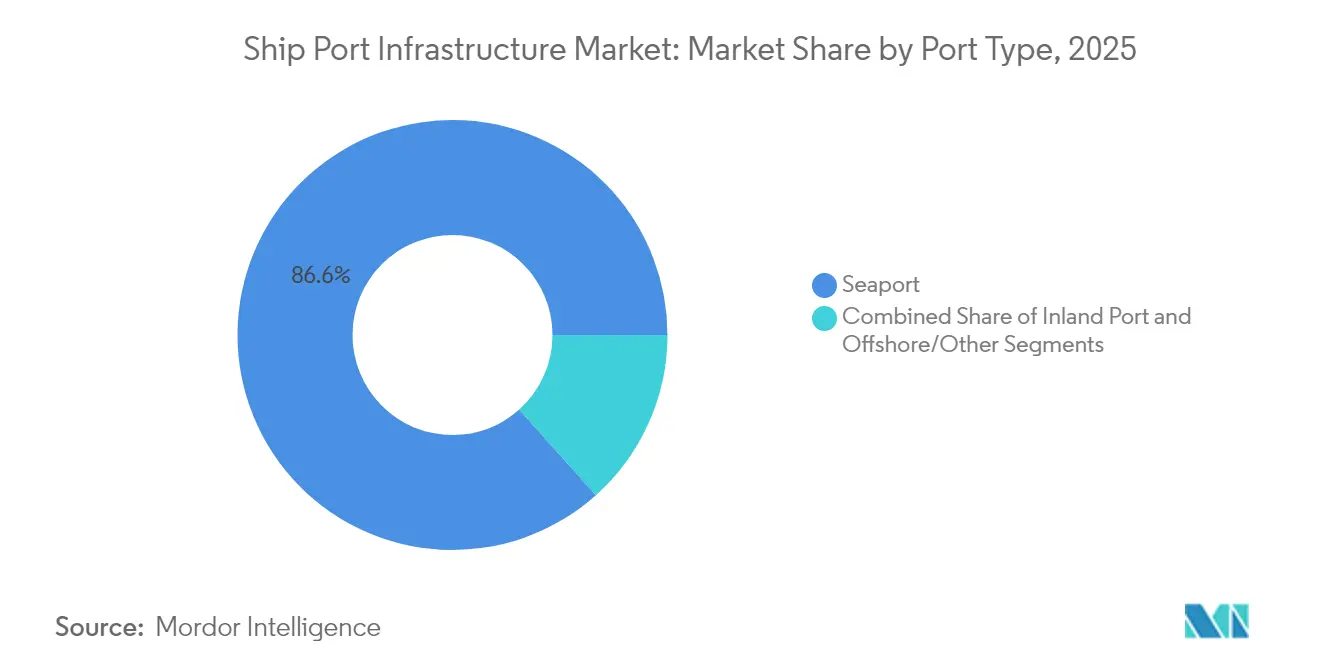

- By port type, seaports led with 86.62% of the ship port infrastructure market share in 2025, while inland ports are forecast to grow at a 4.82% CAGR through 2031.

- By application, cargo operations accounted for 90.55% share of the ship port infrastructure market size in 2025; the passenger segment is expected to post a 4.81% CAGR to 2031.

- By ownership model, public entities held 51.68% of the ship port infrastructure market size in 2025, whereas private operators are projected to expand at a 4.74% CAGR through 2031.

- By technology adoption level, conventional terminals commanded 65.35% of the ship port infrastructure market size in 2025, while fully automated facilities are scaling at a 4.71% CAGR to 2031.

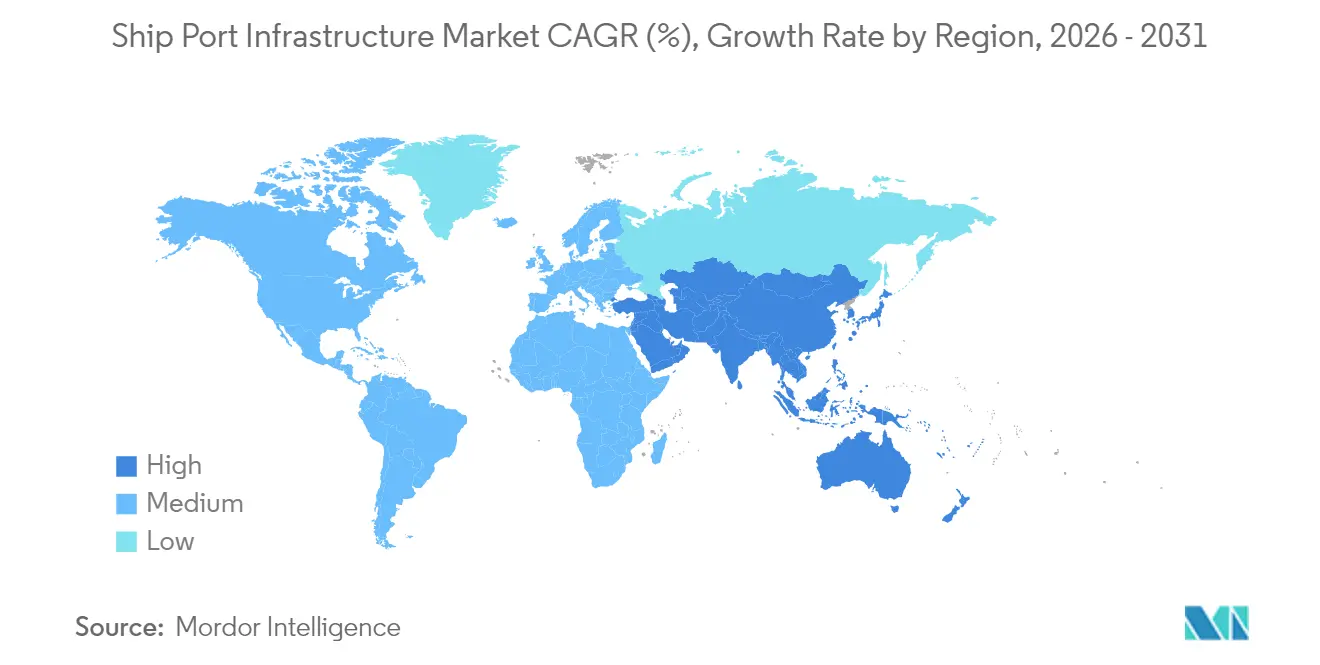

- By geography, Asia Pacific captured 38.42% of the ship port infrastructure market share in 2025 and is set to grow at a 4.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ship Port Infrastructure Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansionary Public-Sector Port Modernization Budgets | +1.2% | Global, with concentration in North America and EU | Medium term (2-4 years) |

| Rapid Container-Terminal Automation | +1.1% | Asia-Pacific core, expanding to EU and North America | Long term (≥ 4 years) |

| Mandatory IMO/ICS Decarbonization Timelines | +0.9% | Global | Long term (≥ 4 years) |

| Near-Shoring Shifting Cargo Flows to Secondary Seaports | +0.8% | North America and Latin America, spill-over to Asia-Pacific | Medium term (2-4 years) |

| Resilience Investments Against Climate-Linked Chokepoint | +0.6% | Coastal regions globally, priority in North America and EU | Long term (≥ 4 years) |

| Rapid Build-Out of Specialized Bulk Terminals | +0.4% | Global, with emphasis on commodity-exporting regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansionary Public-Sector Port Modernization Budgets

Government spending is reshaping capacity and technology priorities across the ship port infrastructure market. The United States allocated USD 580 million to 31 projects in 2024, while California ring-fenced USD 2.3 billion for port improvements that bundle berth expansion with digital yard-management platforms.[1]“Port Modernization Funding Overview,” California Department of Transportation, dot.ca.gov Similar momentum is visible in the European Union’s Connecting Europe Facility, which co-finances shore-power deployment and intermodal upgrades. Blended-finance structures enable quicker execution, as shown by DP World’s USD 1.2 billion London Gateway phase-II build that combines public guarantees with private equity.[2]“London Gateway Phase II Investment,” DP World, dpworld.comPorts securing multi-source funding can synchronise civil works expansion with automation roll-outs, compressing payback periods by lifting throughput per hectare. Yet capacity gains hinge on hinterland connectivity; berth productivity fails to translate into end-to-end velocity without rail-and-road alignment.

Rapid Container-Terminal Automation & Private-5G Roll-Outs

Automation is accelerating as terminals confront labour shortages and volatility in collective bargaining. Singapore’s Tuas Port operates more than 200 driverless vehicles under a private 5G network that supports millisecond equipment hand-offs, cutting unproductive moves by 20%. China leads with 52 automated berths online and 27 under construction, validating systems' economies of scale. Early adopters nevertheless gain a structural cost edge when industrial action halts manual peers, making automation the decisive differentiator for volume-sensitive carriers.

Mandatory IMO Decarbonisation Timelines Accelerating Green-Retrofit Capex

The IMO target of net-zero greenhouse-gas emissions by 2050 compels ports to electrify cargo gear, install shore power, and prepare for low-carbon bunkering. Rotterdam will build ammonia storage and hydrogen pipelines by electrifying 100% of straddle carriers by 2030. Studies by the Zero Emission Port Alliance show that 94% of new handling equipment purchases will be battery-electric by 2035. The financial burden includes grid upgrades, with many ports needing to triple their electrical import capacity. Operators moving first can levy green-premium tariffs as shipping lines integrate emissions ratings into port-call decisions.

Near-Shoring Shifts Cargo Flows to Secondary Seaports

Manufacturers moving closer to consumption zones diversify containers from mega-hubs to emerging gateways, enlarging the investable universe within the shipping port infrastructure market. Mexico’s Manzanillo is tripling annual capacity to 10 million TEU via a USD 3 billion master plan that capitalises on North American regionalisation.[3]“Master Plan Update 2025,” Administración del Sistema Portuario Nacional Manzanillo, asiponamanzanillo.gob.mx In the United States, the Port of Nevada provides an inland railhead that bypasses West Coast road congestion and trims door-to-door transit by two days. Secondary ports can monetise shorter vessel queues and dedicated acreage; however, they must match the data visibility standards of tier-1 terminals to keep high-value shippers. The competitive field, therefore, rewards facilities that pair acreage expansion with optical-character-recognition gates, automated stacking cranes, and cloud-based scheduling.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Multi-Billion-Dollar Upfront Capital Requirement | -0.9% | Global | Long term (≥ 4 years) |

| Labour-Union Resistance to Full Automation | -0.7% | North America and EU | Medium term (2-4 years) |

| Growing Cyber-Security Vulnerabilities | -0.4% | Global, priority in developed markets | Short term (≤ 2 years) |

| Escalating Annual Dredging Costs | -0.3% | Global, emphasis on coastal regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Multi-Billion-Dollar Upfront Capital Requirement & Long Pay-Back

Full automation and berth deepening stretch balance sheets across the ship port infrastructure market. Projects exceed, and lenders demand covenants tied to throughput guarantees, creating hurdles for midsize operators. Technology obsolescence risk further complicates underwriting; equipment cycles shrink as software-defined cranes replace mechanical upgrades every five years. Consequently, smaller concessions may pivot to phased semi-automation as an interim hedge.

Labour-Union Resistance to Full Automation at Legacy Hubs

Organised labour at West Coast US terminals halted operations in October 2024, revealing the strike leverage that unions retain even as automation proliferates. Contract renegotiations in January 2025 opened the door to hybrid skill paths—such as remote crane operators—that moderate job displacement. Nevertheless, ports bound by outdated labour clauses risk service unreliability and diversion of discretionary cargo to Asian competitors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Port Type: Seaports Maintain Primacy While Inland Nodes Accelerate

Seaports continue to dominate the ship port infrastructure market size, accounting for an 86.62% share in 2025, as only coastal facilities can berth ultra-large vessels. This dominance anchors the ship port infrastructure market size at the high end of the capital allocation spectrum, driving dredging, breakwater reinforcement, and automation outlays that dwarf those of inland and offshore installations. Volume visibility attracts third-party logistics providers and fintech platforms, creating network effects that reinforce seaport hegemony.

Seaport investments center on tandem-lift quay cranes, AI-enabled stack management, and on-dock rail integration, which can reduce truck idling by 30%. Inland ports, which will grow at a CAGR of 4.82% by 2031, leverage rail economics; the Port of Nevada’s 224-acre site processes remote customs clearance and rail transloading, which remove 600 daily truck trips from congested interstate corridors. Growth potential is spurred by e-commerce fulfillment centers migrating inland, signaling that the ship port infrastructure market will witness a nuanced balance between coastal scalability and interior agility.

By Application: Cargo Operations Anchor Revenues While Passenger Demand Recovers

Cargo handling represented 90.55% of the total ship port infrastructure market share in 2025, anchoring the market. Terminal operators funnel capital toward automated stacking cranes, optical gate systems, and blockchain-linked documentation that eliminate manual reconciliation delays. Container dwell time has become the principal metric through which investors benchmark asset productivity.

Passenger activities grow at a CAGR of 4.81% through 2031, cruise and ferry terminals are rebounding as vaccination passports and pent-up travel demand lift bookings. Ports in the Mediterranean and Caribbean are refurbishing embarkation lounges and installing LNG bunkering to serve new dual-fuel cruise ships. Higher spend per docked passenger offsets seasonal volatility, diversifies income streams, and raises asset valuations within the broader ship port infrastructure industry.

By Ownership Model: Public Dominance Persists Amid Private Efficiency Gains

Public authorities retained 51.68% control of the ship port infrastructure market size in 2025, safeguarding national-interest assets and trade security considerations. Nevertheless, fiscal constraints and competing social budgets encourage concessioning to global operators like PSA International, which recently secured a 30-year build-operate-transfer deal in Jakarta. Private entities accelerate project timelines by compressing procurement cycles and aligning incentives to throughput, while growing at a CAGR of 4.74%.

Hybrid public-private partnerships unlock multilateral finance, enabling emerging-market ports to attain international standards. Performance-based tariff structures encourage throughput guarantees and clarify lender repayment profiles, thereby expanding the investible tranche of the ship port infrastructure market.

By Technology Adoption Level: Conventional Operations Give Way to End-to-End Automation

Conventional processes accounted for 65.35% of the ship port infrastructure market size in 2025, illustrating the inertia of legacy asset bases. Yet fully automated yards are scaling rapidly, with 4.71% CAGR, as proof-of-concept projects like Rotterdam’s Maasvlakte II achieve 30-move-per-hour crane productivity without human drivers.

Investment returns hinge on integrated operating systems; siloed automation often under-delivers when different vendors program quay, yard, and gate modules. The transition path typically begins with automated stacking cranes and graduates to automated guided vehicles. It culminates in real-time digital twins orchestrating entire terminals, redefining competitive moats within the ship port infrastructure market.

Geography Analysis

Asia Pacific led the ship port infrastructure market share with a 38.42% regional share in 2025 and remains the fastest-growing territory at a 4.72% CAGR. China’s 52 automated berths and a national strategy that treats terminals as smart-manufacturing nodes gave Shanghai the first 50 million TEU throughput record in history. South Korea’s Busan added an automated phase that lifted yard density by 20%, illustrating how technology leapfrogging corrects land constraints. Although geopolitical frictions pose downside risk, regional governments continue to pour capex into digital-rail corridors that funnel hinterland exports to coastal hubs.

Europe maintains efficiency leadership in sustainability. Rotterdam’s 6.8 benefit-to-cost ratio adaptation plan channels EUR 2 billion into flood-barriers, ammonia bunkering, and green hydrogen pipelines. Hamburg’s Altenwerder terminal operates climate-neutral equipment and has become a test-bed for electricity-as-a-service models that shift battery ownership to utilities, reducing operator capex. Regulatory frameworks such as FuelEU Maritime reward early movers by extending green-corridor incentives to shipping lines that call at low-carbon ports, enriching the strategic profile of the ship port infrastructure market.

North America lags on automation but benefits from near-shoring and federal grants. The USD 580 million Port Infrastructure Development Program funnels funds toward berth rehabilitation and electrified rubber-tyred gantry cranes at Los Angeles and Long Beach. Labour uncertainty remains the region’s Achilles heel; the 2024 strike pushed carriers to divert 9% of Transpacific volumes to Mexican and Canadian gateways.

Regulatory Landscape

Port infrastructure investment decisions are increasingly influenced by decarbonization and enforcement requirements set at the international level. From January 2026, the International Maritime Organization brought into effect updated Procedures for Port State Control (Resolution A.1206(34)), which tightens how port-state control checks environmental compliance and broadens the grounds for detention linked to MARPOL Annex VI performance. This raises the bar for ports supporting fuel switching, emissions monitoring, and inspection readiness.

At the same time, national and regional policy frameworks are tightening around security, permitting, and long-horizon capacity planning. The European Commission unveiled an EU Ports Strategy in March 2026, focusing on competitiveness, sustainability, and security, including foreign ownership guidance and cybersecurity assessments for EU ports. In the United States, the Maritime Administration issued the FY 2026 Port Infrastructure Development Program Notice of Funding Opportunity with USD 488.6 million of discretionary funding, continuing federal grants that steer modernization projects toward measurable safety, efficiency, and reliability outcomes. The United Kingdom also advanced a new National Policy Statement for Ports in July 2026 to govern port development proposals, while India enacted the Indian Ports Act, 2025 to consolidate port laws and strengthen state-level maritime governance structures.

Value Chain Analysis

The ship port infrastructure value chain runs from planning and approvals (port authorities, maritime administrations, environmental agencies) to financing and delivery (public budgets, PPPs, lenders, EPCs), and then to operations and monetization (terminal operators, shipping lines, inland transport, and logistics service providers). Key upstream inputs include dredging and marine civil works, quay and yard equipment (cranes, automated guided vehicles, gate systems), power and grid connections for electrification, and terminal operating systems that integrate OT and IT. Engineering contractors and OEMs deliver the core assets, while integrators connect controls, cybersecurity, and data platforms that support automation and visibility across berth, yard, and gate.

Downstream, terminals increasingly package port infrastructure with value-added logistics and intermodal services to secure cargo flows and improve asset utilization. In July 2025, the Suez Canal Automotive Terminal at Port Said started operations under a long-term operating agreement involving Africa Global Logistics, NYK, and Toyota Tsusho, formalizing a specialized finished-vehicle node. In Europe, Volkswagen Group Logistics selected the Port of Venice as a strategic hub backed by more than EUR 60 million in related infrastructure investments, including rail capacity expansion. In June 2026, Hyundai Glovis announced plans for a large finished-vehicle hub at the Port of Amsterdam with storage and PDI functions (opening scheduled for January 2027), reinforcing ports as integrated processing, storage, and multimodal distribution platforms rather than only marine interfaces.

Competitive Landscape

The ship port infrastructure market is moderately consolidated. BlackRock’s USD 22.8 billion joint purchase of Hutchison’s overseas assets underscores rising institutional appetite for the stable cash flows embedded in the ship port infrastructure market. Strategic differentiation increasingly rests on data integration and climate credentials rather than simple berth length.

Operators are funding automation to lock in cost competitiveness. DP World earmarked USD 250 million for a modernised on-dock rail extension at Sydney’s Port Botany and completed a similar USD 400 million automation suite in Callao, Peru. PSA’s Tuas mega-terminal in Singapore consolidates seven city-centre terminals into a 65 million TEU complex, leveraging cloud-native orchestration to arbitrage quay crane allocation. Technology startups such as NextPort are embedding digital twins that simulate yard congestion scenarios, giving midsize operators a tactical toolkit to stay relevant.

Climate-aligned services also distinguish market leaders. Rotterdam, Los Angeles, and Valencia are establishing green-corridor pacts with shipping lines, bundling shore power, alternative-fuel bunkering, and verifiable emissions reporting. Ports without clear decarbonisation blueprints risk relegation to secondary routing as cargo owners press for supply-chain Scope 3 visibility.

Ship Port Infrastructure Industry Leaders

Man Infraconstruction Ltd.

APM Terminals

Essar Ports Limited

Larsen & Toubro Limited

Adani Ports & SEZ

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A clear opportunity area is the build-out and specialization of vehicle and RoRo-focused port infrastructure as OEMs and logistics providers look for higher throughput, rail-connected storage, and on-site processing. The Port of Brunswick handled 779,000 auto units in 2025, supported by a USD 100 million berth expansion and prior terminal investments. South Carolina Ports Authority also approved a design contract in May 2026 to expand RoRo operations at the North Charleston Terminal. In India, Adani Ports and Special Economic Zone partnered with Motherson in December 2025 to establish a RoRo terminal at Dighi Port, with stated annual capacity of 200,000 vehicles, underlining demand for yard optimization, integrated logistics, and export-ready handling.

A second opportunity band focuses on electrification, shore power, and alternative-fuel readiness, alongside automation and digital integration that improve reliability and labor resilience. APM Terminals inaugurated a new fully electrified container terminal at Suape, Brazil in June 2026, framing decarbonized equipment and power infrastructure as core modernization components. On funding and pipeline, the United States Maritime Administration made USD 488.6 million available under the FY 2026 Port Infrastructure Development Program NOFO, while the European Commission advanced an EU Ports Strategy in March 2026 with explicit emphasis on sustainability and security, including cybersecurity assessments. Together, these programs and operator actions translate regulatory and customer requirements into concrete modernization and retrofit work across regions and terminal types.

Recent Industry Developments

- July 2026: APM Terminals started a USD 570 million expansion of the Muelle Norte multipurpose terminal at the Port of Callao, Peru, with the project designed to raise container capacity to 1.75 million TEU. The expansion is intended to increase berth and yard capability in a key Pacific gateway, supporting larger volumes and more diversified cargo flows. It also reinforces a broader capex cycle among global operators focused on scalable infrastructure upgrades.

- June 2026: APM Terminals inaugurated its new container terminal at Suape, Brazil, positioned as the first fully electrified container terminal in Latin America with annual capacity of 400,000 TEU. Electrified equipment and associated power infrastructure support productivity gains while aligning with decarbonization requirements. The commissioning also provides an operational reference point for ports planning similar equipment and grid upgrades.

- December 2024: Man Infraconstruction Ltd participated in bidding for near-shore reclamation and protection works for the Vadhvan Port project, indicating continued activity in large-scale marine civil works in India without disclosing specific tender values. The engagement points to ongoing momentum in port development contracts and highlights the role of contractors in delivering greenfield capacity.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers spending linked to ship port infrastructure that enables the movement of vessels, cargo, and passengers through ports, and it is sized in USD value terms across major regions and port networks.

Scope exclusions: It excludes inland freight logistics outside port gates and routine vessel operating costs that are not directly tied to port infrastructure or port-side services.

Segmentation Overview

- By Port Type

- Seaport

- Inland Port

- Offshore/Other

- By Application

- Cargo

- Passenger

- By Ownership Model

- Public

- Private

- By Technology Adoption Level

- Conventional

- Semi-Automated

- Fully-Automated

- By Geography

- North America

- United States

- Canada

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Netherlands

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of Asia Pacific

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Turkey

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building the demand backdrop for port activity and investment, and then translating that into value pools that fit the market definition. We relied on public sources such as UNCTAD maritime statistics, the World Bank, IMF macro series, and OECD trade indicators to understand trade flows, port throughput direction, and investment capacity.

To make sure the numbers are grounded, we also reviewed sources such as national port authority publications, transport ministries, customs and trade releases, and IMO-facing maritime safety and policy updates. Company annual reports, investor presentations, and reputed press were used to confirm project timing, major capacity additions, and order pipelines. For cross-checking, we used selective paid company financials and intelligence, as well as a global tenders and contracts database, to track awarded projects and capex signals. These desk research sources are illustrative, and many other public documents and datasets were also used for clarification and validation.

Primary Interviews and Surveys

Primary work focuses on checking how port investment decisions are made and what actually drives pricing and volumes across different port settings. We spoke with port operators, engineering and construction stakeholders, equipment and service providers, and cargo-side users across major trading corridors. We then used that input to tighten assumptions on utilization, project phasing, and average spending per capacity unit.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 13% | APAC: 50% |

| Mid tier: 61% | Functional/Unit leaders: 35% | EMEA: 30% |

| Smaller Players: 14% | Managers: 52% | Americas: 20% |

Market-Sizing & Forecasting

The model begins with a top-down build where port activity and investment signals are used to reconstruct the total value pool by geography, and then it is split into the defined market scope. In practice, we track indicators such as container throughput (TEUs), bulk and liquid cargo volumes, port capacity expansion announcements, capex intensity by port type, and project commissioning timelines, which together explain why spending rises or slows.

Those totals are then corroborated with selective bottom-up approximations so the output stays realistic. This includes sample checks like capacity added multiplied by typical spend per berth or terminal module, and supplier and contractor revenue exposure discussions for major project categories. When the bottom-up view has gaps, we handle them by using proxy ratios from comparable ports, followed by expert review to avoid over-counting.

For forecasting, scenario analysis is used with a simple variable set that primary experts can validate quickly, including trade growth expectations, vessel size trends, infrastructure funding conditions, and regulatory-driven safety and modernization needs. The final forecast is adjusted only after the assumptions align with what stakeholders expect to see in tender activity and capacity utilization over the period.

Data Validation & Update Cycle

Outputs are checked against independent signals before sign-off, including throughput growth patterns, visible capex cycles, and any large project starts or delays that could create step-changes in yearly value. If results move too far from these external checks, the assumptions are reviewed, and follow-up calls are triggered to confirm the cause of the variance.

A second analyst review is performed to confirm definitions, currency handling, and arithmetic consistency across regions and port types. Any anomalies are reworked until they can be explained in plain terms. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery pass is completed so clients receive the most current view available.

Mordor Intelligence's Ship Port Infrastructure Market Estimate Compared With Other Published Estimates

Published market sizes for ship port infrastructure can look far apart, even when the topic label sounds identical, because the counted value pools are not always the same. The biggest drivers tend to be what is treated as port-side infrastructure versus broader logistics, how project timing is recognized, and whether the estimate follows real capex cycles or uses smooth growth.

In this market, the spread usually comes from scope choices, like folding in inland freight facilities, warehousing, or general shipping services that sit outside port infrastructure. Another driver is how pricing and currency are handled, since some estimates apply a single exchange rate and flat average spending, while others let unit costs change with commodity inputs and project mix. Here, port services tied to moving vessels, cargo, and passengers through ports are counted, and adjacent logistics is left out, which keeps the 2026 value anchored to observable throughput and project pipelines. This modeling choice is used by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 221.61 B (2026) | |

| Global Consultancy A | USD 245.00 B (2026) | This figure appears to include a wider port-adjacent spend bucket, especially logistics yard development and off-port connectivity, which inflates the value relative to infrastructure and port-side services only. |

| Industry Association B | USD 205.00 B (2026) | This estimate seems to lean on conservative capex reporting and may undercount smaller and mid-sized upgrade projects, especially when projects are phased and not captured as full-year value. |

The table shows that the main differences come from what gets counted and how uneven project cycles are treated year to year. By tying the total to throughput signals and investment cadence, and then confirming assumptions with stakeholder checks, the final number stays traceable to clear drivers and can be repeated when new port projects are announced.

Key Questions Answered in the Report

What is the current value of the ship port infrastructure market?

The ship port infrastructure market was valued at USD 221.61 billion in 2026 and is on track to hit USD 278.62 billion by 2031.

Which region leads the ship port infrastructure market?

Asia Pacific holds the top position with 38.42% share in 2025 and remains the fastest-growing territory at a 4.72% CAGR through 2031.

How significant is automation in shaping competitive advantages?

Fully automated terminals post 15-20% higher crane productivity and lower labor exposure, making automation a pivotal determinant of long-term cost leadership.

What role do public-private partnerships play in new port projects?

They bridge funding gaps by combining government guarantees with private capital, accelerating delivery while ensuring strategic oversight.

How are decarbonisation mandates influencing port investments?

IMO net-zero targets push ports to electrify equipment, install shore power, and develop alternative-fuel bunkering, often tripling grid capacity requirements.

Why are secondary ports gaining attention from shippers?

Near-shoring strategies and congestion avoidance divert volumes to smaller gateways that can offer dedicated acreage, faster turnaround, and integrated rail links.

Page last updated on: