Global Marine Battery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

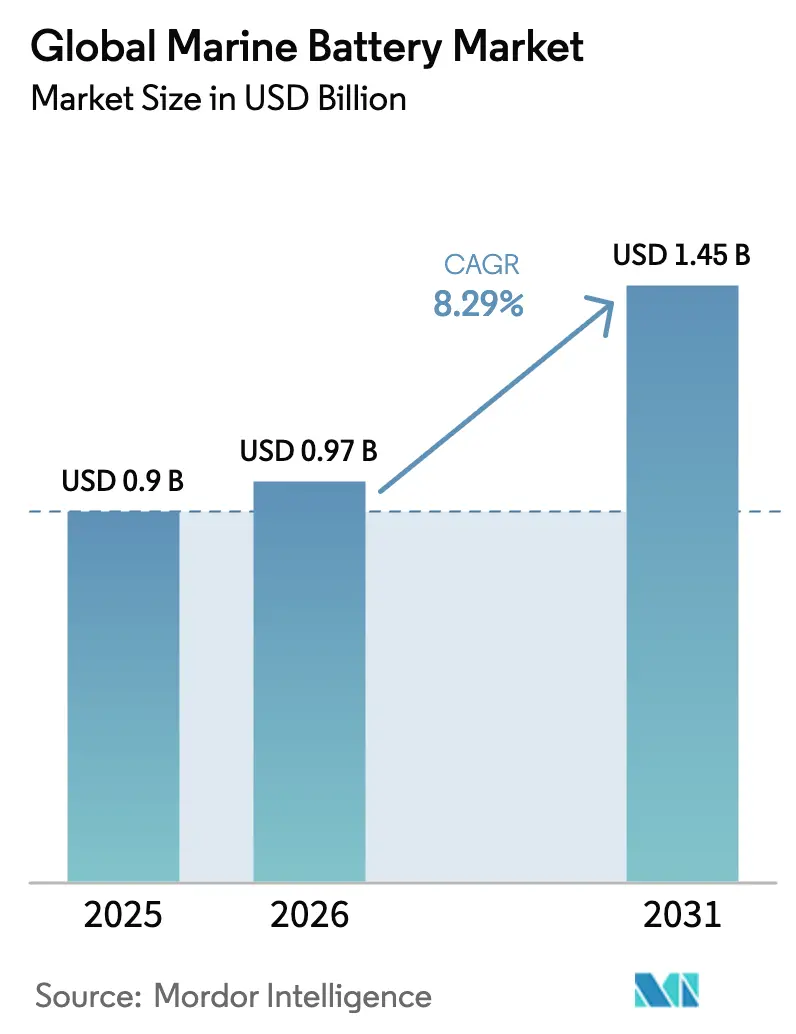

| Market Size (2026) | USD 0.97 Billion |

| Market Size (2031) | USD 1.45 Billion |

| Growth Rate (2026 - 2031) | 8.29% CAGR |

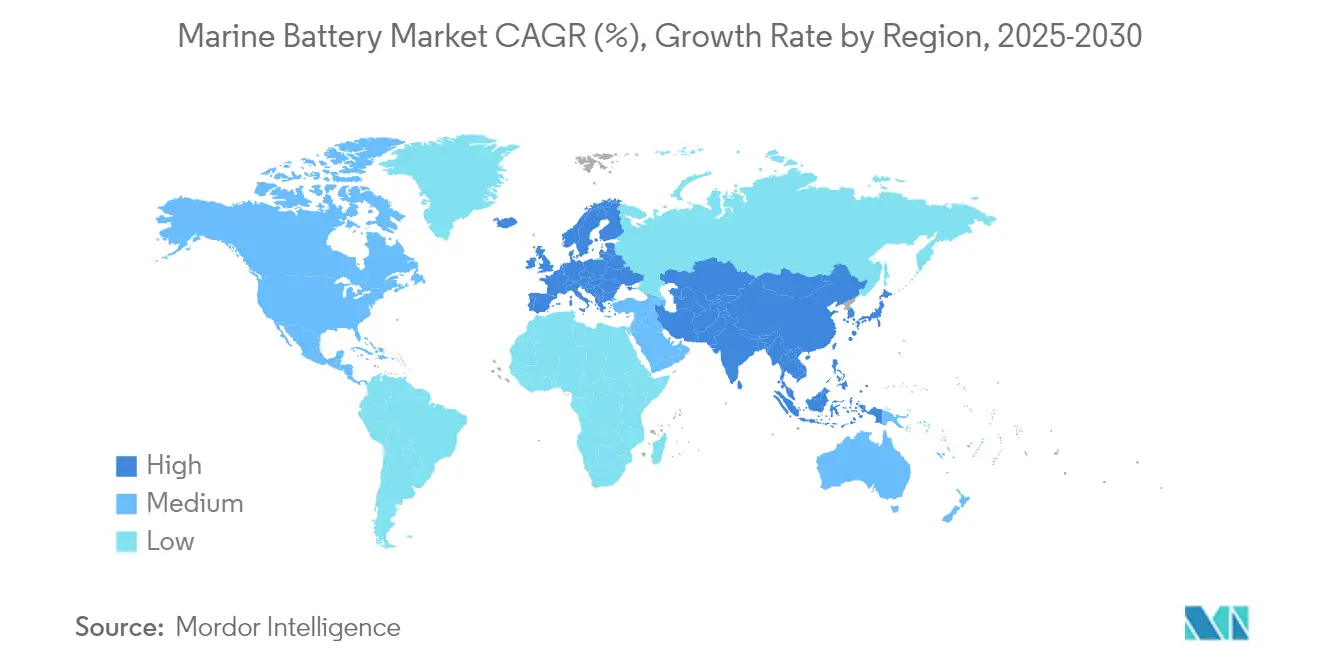

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

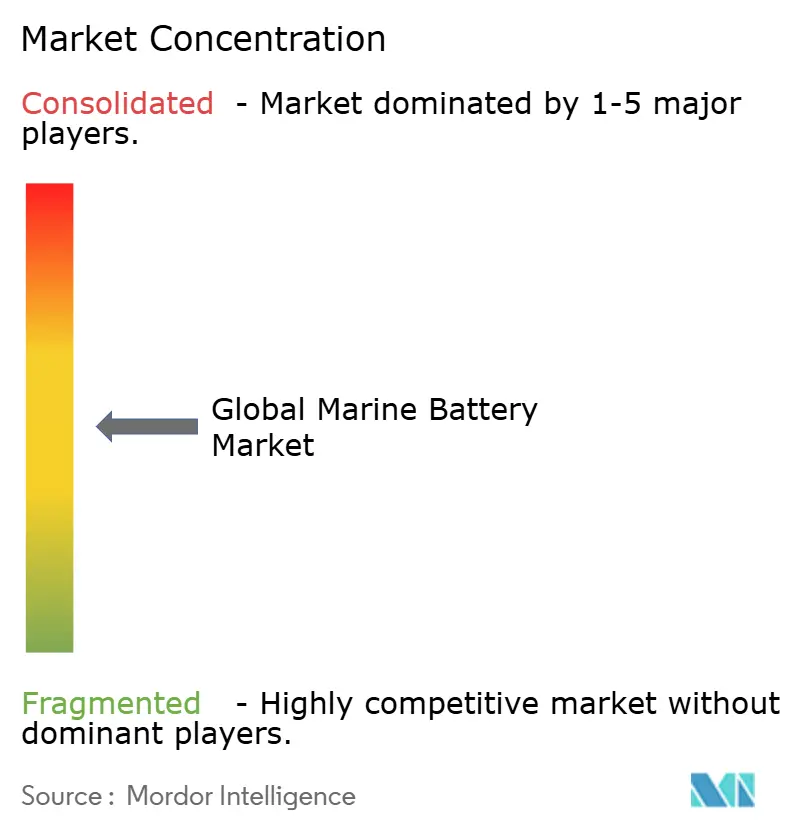

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Marine Battery Market Analysis by Mordor Intelligence

The marine battery market size is expected to grow from USD 0.90 billion in 2025 to USD 0.97 billion in 2026 and is forecast to reach USD 1.45 billion by 2031 at 8.29% CAGR over 2026-2031. Compliance pressure from the FuelEU Maritime Regulation and the IMO’s updated zero-carbon strategy pushes operators toward electric and hybrid propulsion. Lower cell costs, broader shore-power coverage at European and Asian ports, and the proven reliability of ferry retrofits all motivate owners to install large packs. Supply-chain partnerships between shipbuilders and automotive cell makers are also trimming lead times, while solid-state chemistry breakthroughs are broadening the vessel types that can sail on batteries alone.

Key Report Takeaways

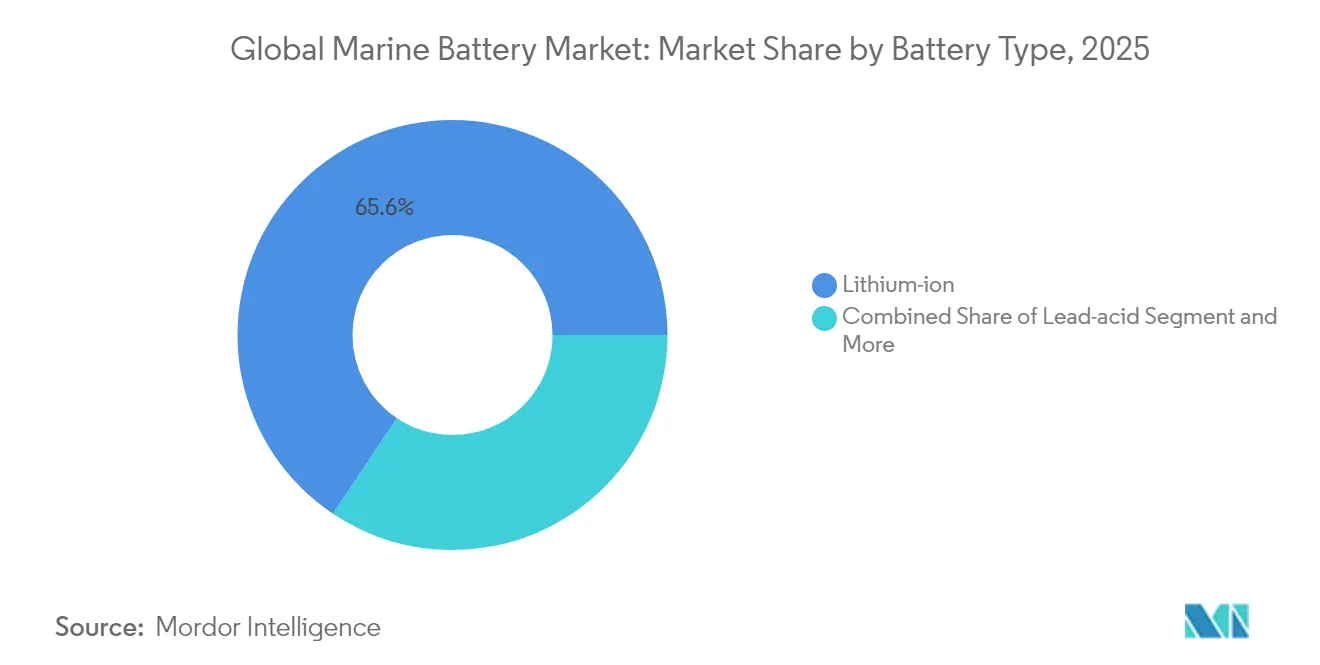

- By battery type, lithium-ion led with 65.62% revenue share in 2025, while solid-state batteries are forecast to expand at a 9.14% CAGR to 2031.

- By propulsion type, hybrid-electric systems held 63.72% of the marine battery market share in 2025, and fully electric designs are projected to grow at a 10.39% CAGR through 2031.

- By ship type, commercial vessels accounted for 71.68% of the marine battery market size in 2025; defense applications are projected to post the fastest 10.26% CAGR over the forecast period.

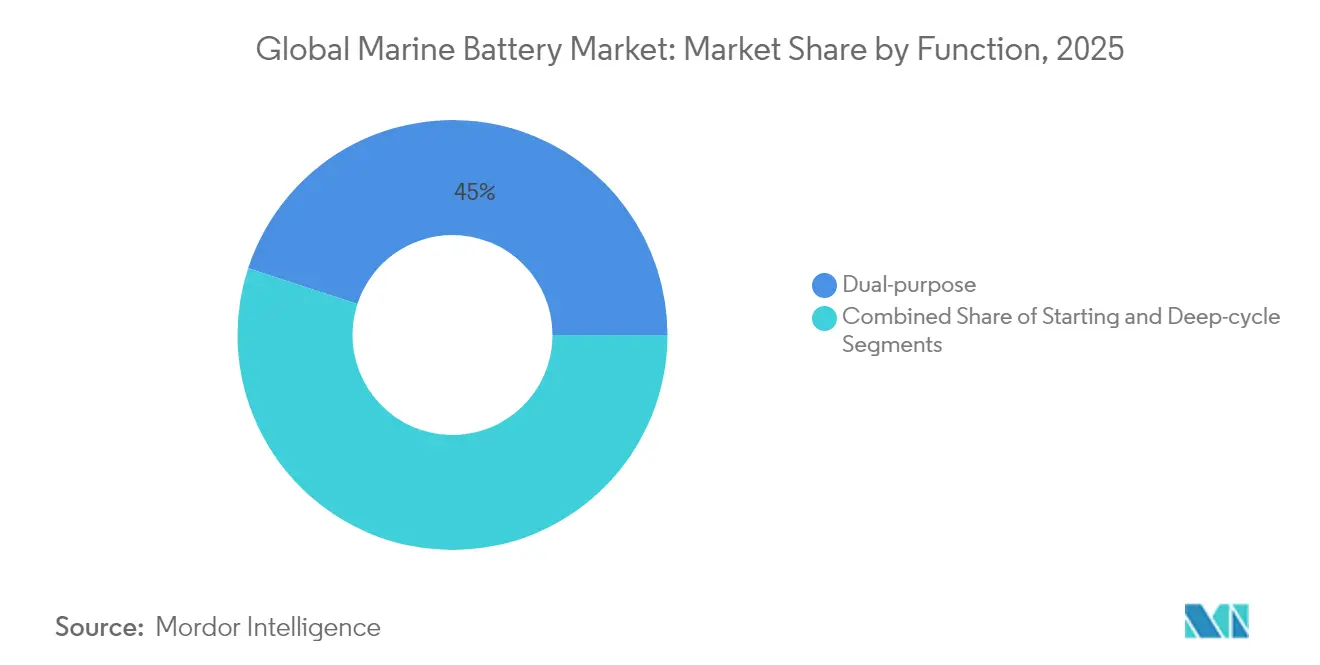

- By function, dual-purpose systems captured 44.98% revenue share in 2025 and are advancing at an 11.15% CAGR to 2031.

- By capacity, the 1–5 MWh range represented 54.10% share of the marine battery market size in 2025 and is set to rise at a 9.28% CAGR to 2031.

- By geography, Europe dominated with 42.20% revenue share in 2025, while Asia-Pacific is expected to record a 11.36% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Marine Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| IMO 2020 and EU Fit-for-55 Mandates | +2.1% | Europe, North America, Global | Medium term (2-4 years) |

| LFP/LTO Cell Price Fall Impacts Ownership Cost | +1.8% | Asia-Pacific, Europe | Short term (≤ 2 years) |

| Green-Port Incentives for Zero-Emission Berthing | +1.2% | Europe, spillover to North America | Medium term (2-4 years) |

| Inland-Waterways Adopt Battery Barges | +0.9% | Asia-Pacific, North America | Long term (≥ 4 years) |

| Silent-Running Submarine Demand | +0.7% | Developed markets | Long term (≥ 4 years) |

| Battery-Hybrid Adopts Offshore-Wind Services | +0.6% | Europe, Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

IMO 2020 & EU Fit-for-55 Emission Mandates Accelerating Electrification

Global and regional climate policies have aligned, making marine batteries an essential compliance tool. From 2025, FuelEU Maritime forces ships at berth to connect to shore power or use zero-emission technologies, and the IMO sets a 20% greenhouse-gas reduction target by 2030 [1]“FuelEU Maritime Regulation,” European Commission, ec.europa.eu. Operators, therefore, see battery packs as a direct route to avoid escalating carbon penalties, protect port access, and unlock lower running costs over the vessel's life.

Rapid Cost Decline of LFP/LTO Chemistries Improves TCO for Short-Sea Vessels

Cell prices for lithium iron phosphate and lithium titanate oxide continue to fall despite metal volatility, with a 40-50% drop expected by 2030. Real-world ferry data shows electric boats run for EUR 600-800 per year versus EUR 3,000-4,000 for similar diesel craft, cutting operating costs by up to 80%. The long cycle life, inherent safety, and lower maintenance of LFP-based packs deliver compelling economics on routes below 100 nautical miles.

European Green-Port Incentives for Zero-Emission Berthing

Northern European ports secured EUR 18.8 million in EU funding to build high-capacity shore-power systems and now offer tariff rebates for battery-equipped vessels [2]“EU-Funded Shore-Power Projects,” GAC Group, gac.com . Gothenburg plans a 70% CO₂ cut by 2030, while Portsmouth and Antwerp have upgraded berths that can recharge multi-megawatt packs during routine calls. Shore-side charging turns idle time into energy replenishment and extends zero-emission range on subsequent voyages.

Expansion of Inland-Waterway Logistics Corridors in China & U.S. Pushes Battery Barges

China has prioritized zero-carbon shipping on the Yangtze, and the United States is piloting battery cargo barges on the Mississippi network. Predictable routes, calm waters, and easy access to land-based chargers make inland waterways an ideal launchpad for multi-megawatt battery systems. National incentives in Beijing and Washington have therefore accelerated orders for large packs designed for barges and push-boats.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Retrofits Delayed by Limited Shipyard Slots | -1.4% | Europe, North America, Global | Short term (≤ 2 years) |

| Thermal-Runaway Concerns in Battery Rooms | -0.8% | Global, stricter in developed markets | Medium term (2-4 years) |

| High Cost of Marine-Certified Batteries | -0.6% | Global | Medium term (2-4 years) |

| South American Policy Shifts Threaten Limited Supply | -0.4% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Scarce Shipyard Capacity for Retrofits Causing Installation Bottlenecks

Yards that handle offshore wind and LNG carrier orders are close to capacity, pushing day rates up to USD 350,000 for specialized vessels and lengthening booking windows. Ferry operators now face multi-year waits for battery conversions, which defers near-term demand for the marine battery market [3]“Hybrid Marine Power System Performance,” Wärtsilä Corporation, wartsila.com.

Thermal-Runaway Safety Concerns for Large Battery Rooms

Lithium-ion fires on ro-ro carriers have highlighted unique hazards at sea. Class societies now mandate dedicated enclosures, gas extraction, and advanced suppression for installations above 1 MWh, raising costs and approval times.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Type: Solid-State Packs Redefine Performance

Lithium-ion chemistry held 65.62% revenue share in 2025 and remains the baseline for ferry and short-sea electrification. The marine battery market size for lithium-ion systems is projected to expand at high single-digit rates through 2031 as pack prices decline and cycle life improves. Solid-state variants, however, present a 9.14% CAGR opportunity by delivering up to triple energy density and an inherently safer solid electrolyte. Demonstrator modules charging to 80% in under 15 minutes are now entering pilot ferries, signaling an inflection point for the marine battery market.

Greater tolerance to temperature swings and elimination of liquid electrolytes reduce the need for bulky cooling gear in tight engine rooms. Several large shipyards expect production-scale solid-state packs to reach USD 100 per kWh around 2029, which should narrow the upfront premium. Lead-acid systems persist in backup roles where cost sensitivity outweighs weight penalties, while nickel-cadmium remains limited to niche defense programs. Fuel-cell hybrids, although promising for trans-ocean routes, continue to trail batteries in capital efficiency for sub-1,000 nautical-mile operations.

By Propulsion Type: Hybrid Systems Bridge the Transition

Hybrid-electric configurations captured 63.72% marine battery market share in 2025 because they cut fuel burn by up to 25% while retaining diesel range. Fleet data shows crew familiarization, class-approval processes, and port-charging windows are simpler when combustion engines remain on board. Still, fully electric newbuilds post a 10.39% CAGR thanks to rapidly expanding shore infrastructure and the falling cost of high-capacity packs. The marine battery market, therefore, follows a two-speed path where hybrids dominate retrofits and fully electric designs lead newbuilds on fixed ferry routes.

Energy-management software now orchestrates battery, generator, and hotel loads in real time, improving asset utilization and reducing maintenance. Conversion projects in Northern Europe demonstrate that once ports install megawatt-scale chargers, owners often plan to switch from hybrid to full electric within the first dry-dock cycle. Modular DC-hub architecture further simplifies the transition by allowing extra racks to be slotted in without major rewiring.

By Ship Type: Commercial Fleet Remains Core While Defense Surges

Commercial vessels maintained 71.68% marine battery market size in 2025, driven by ferries, coastal feeders, and offshore service boats. Predictable timetables allow frequent charging, and public funding de-risks capital outlay. In contrast, defense programs show a 10.26% CAGR because navies pay a premium for silent-running craft. Battery-only silent running extends mission envelopes, reduces detection risk, and aligns with net-zero mandates for government fleets.

Passenger-ferry tenders in California, Greece, and Japan now specify battery propulsion as a prerequisite, reinforcing baseline demand. Inland barges on river corridors in China and the United States provide another commercial growth pocket. On the military side, lithium-ion packages in new-generation submarines and the first battery-boosted destroyers validate high-energy chemistries under extreme duty cycles, creating spill-over confidence for commercial owners.

By Function: Dual-Purpose Packs Streamline Installations

Dual-purpose systems that handle both starting and deep-cycle duties represented 44.98% of revenue in 2025 and are growing at a 11.15% CAGR. The marine battery market values space and weight savings from consolidating separate starters and house banks into a single modular rack. Modern battery-management software balances charge profiles and prevents premature ageing. Operators gain lower weight, easier wiring, and shorter installation time.

Deep-cycle-only packs hold steady in cruise ships where hotel loads dwarf propulsion demand, but dual-purpose packs will dominate workboats, ferries, and tugs. Classification approvals for multi-role lithium iron phosphate modules signal broad acceptance. As a result, the marine battery market will see faster adoption among small-to-mid vessels that lacked space for separate banks in the past.

By Capacity Range: 1–5 MWh Is the Market’s Center of Gravity

Systems between 1 MWh and 5 MWh captured a 54.10% share of the marine battery market size in 2025 and grew at a 9.28% CAGR. This capacity fits most ferry crossings, offshore service duty cycles, and barge missions. Containerized skids speed up yard work and allow bolt-on additions during future refits. Above 5 MWh, engineering complexity escalates; only offshore wind service vessels and small container ships currently justify those packs.

Under-1 MWh systems power harbor craft, pilot boats, and emergency hotel loads. Although numerous in unit terms, they add less value. The mid-scale bracket, therefore, attracts the greatest manufacturing focus, driving down cost per kilowatt-hour and cementing its dominance within the marine battery market.

Geography Analysis

Europe commanded 42.20% revenue share in 2025 owing to legally binding greenhouse-gas caps and generous port subsidies. The marine battery market in the bloc benefits from a dense short-sea network where ferries and feeders call at ports several times a day, making shore-charging practical. Northern Europe tops early adoption, yet Mediterranean yards are now inserting battery rooms into cruise-ferry newbuilds to meet the 2030 berth-emission rule.

Asia-Pacific posts the fastest 11.36% CAGR for the marine battery market, led by China’s zero-carbon Yangtze program and the launch of a 50 MWh electric container ship. South Korean and Japanese yards contribute design know-how and domestic lithium supply. ASEAN countries follow, with Malaysia’s planned Johor plant targeting regional demand for fishing boats, tugs, and inter-island ferries.

North America shows steady growth on the back of defense contracts and state ferry upgrades in Washington, Alaska, and New York. Inland waterways add further momentum, as barge operators trial battery push-boats on fixed grain and coal routes. Latin America and Africa remain small today but possess lithium resources and new port modernization plans that could lift long-term uptake. Middle Eastern offshore operators also explore battery-hybrid service craft to cut emissions near rigs.

Competitive Landscape

Industry estimates indicate that the leading five companies collectively manage about half of the globally installed marine battery capacity. Corvus Energy remains the reference brand for high-capacity packs, having secured deals for hybrid tugs in the Panama Canal and a 25 MWh offshore vessel system. Siemens, Wartsila, and Rolls-Royce Power Systems wrap batteries into integrated propulsion packages, leveraging global servicing footprints.

Automotive giants such as CATL and BYD are entering through joint ventures with shipbuilders, promising mass-production scale and cost advantages. EST-Floattech, Echandia, and Shift carve niches by tailoring packs to smaller workboats and ferries with rapid delivery and specialized marine safety features. Competitive focus increasingly lies in thermal management, plug-and-play modularity, and class-friendly documentation rather than raw cell chemistry.

Joint development programs with yards and port authorities are emerging as a strategic lever. Vendors that can assure spare-part pipelines, 24 × 7 remote monitoring, and training services gain customer stickiness. Over the next five years, consolidation may rise as larger OEMs acquire niche pack integrators to fill technology gaps and secure footholds in the expanding marine battery market.

Global Marine Battery Industry Leaders

Siemens AG

Wartsila Corporation

Corvus Energy

EST-Floattech B.V

Akasol AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: CATL partnered with a Maersk unit to co-develop advanced packs for maritime applications, drawing on automotive experience to improve cycle life and safety.

- February 2025: Corvus Energy was chosen to supply a 25 MWh system for the world’s first fully electric offshore Commissioning Service Operation Vessel, enabling full-day zero-emission operations.

- August 2024: Echandia delivered battery systems to the San Francisco Bay Ferry fleet, supporting California’s push for zero-emission public transport.

- April 2024: Shift announced a new marine battery production plant in Johor to serve the ASEAN maritime industry.

Global Marine Battery Market Report Scope

Marine batteries act as a primary power source for naval vessels and use chemical energy to provide power for numerous applications such as windlass, lightning, start-stop, fish locator, and others. Marine batteries are designed for use on ships, with heavier plates and robust construction designed to withstand the vibration that can occur onboard any powerboat. These batteries are designed with sturdier and more elevated plates for electricity. The batteries are protected from the short circuit while bouncing around with the boat during rough waters. These batteries have thicker plates with high levels of antimony, making them capable of large discharges over long periods.

The marine battery market is segmented based on battery, ship type, and geography. By battery, the market is segmented into lithium-ion, nickel-cadmium, fuel cell, and lead-acid. By ship type, the market is segmented into commercial and defense. By geography, the market is segmented into North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa. The market sizing and forecasts have been provided in value (USD million).

| Lithium-ion | LFP |

| NMC/NCA | |

| LTO | |

| Lead-acid | |

| Nickel-cadmium | |

| Fuel Cell (PEM, SOFC) | |

| Solid-state |

| Hybrid Electric |

| Fully Electric |

| Auxiliary / Hotel Loads |

| Commercial | Ferries & RoPax |

| Cargo & Container | |

| Offshore Support & Wind SOV | |

| Inland Waterway & Barges | |

| Passenger & Leisure Craft | |

| Defense | Naval Surface Combatants |

| Submarines & UUVs |

| Starting |

| Deep-cycle |

| Dual-purpose |

| Less than 1 MWh |

| 1 - 5 MWh |

| Greater than 5 MWh |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Israel | |

| South Africa | |

| Rest of Middle East and Africa |

| By Battery Type | Lithium-ion | LFP |

| NMC/NCA | ||

| LTO | ||

| Lead-acid | ||

| Nickel-cadmium | ||

| Fuel Cell (PEM, SOFC) | ||

| Solid-state | ||

| By Propulsion Type | Hybrid Electric | |

| Fully Electric | ||

| Auxiliary / Hotel Loads | ||

| By Ship Type | Commercial | Ferries & RoPax |

| Cargo & Container | ||

| Offshore Support & Wind SOV | ||

| Inland Waterway & Barges | ||

| Passenger & Leisure Craft | ||

| Defense | Naval Surface Combatants | |

| Submarines & UUVs | ||

| By Function | Starting | |

| Deep-cycle | ||

| Dual-purpose | ||

| By Capacity Range | Less than 1 MWh | |

| 1 - 5 MWh | ||

| Greater than 5 MWh | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Israel | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected marine battery market size by 2031?

The marine battery market size is forecast to reach USD 1.45 billion by 2031, growing at an 8.29% CAGR over 2026-2031.

Which battery chemistry dominates ship applications today?

Lithium-ion packs hold 65.62% revenue share thanks to established supply chains, proven ferry retrofits, and falling cell prices.

Why do many operators start with hybrid instead of full electric propulsion?

Hybrid systems reduce fuel use by up to 25.0% while preserving diesel range, offering an easier first step toward full electrification as shore-charging networks expand.

Which region shows the fastest growth for marine batteries?

Asia-Pacific is set to post a 11.36% CAGR, driven by China’s inland-waterway plans, Japanese shipbuilder innovations, and new manufacturing capacity in Southeast Asia.

Page last updated on: