Size and Share of Portable Communication Systems In Military Applications

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

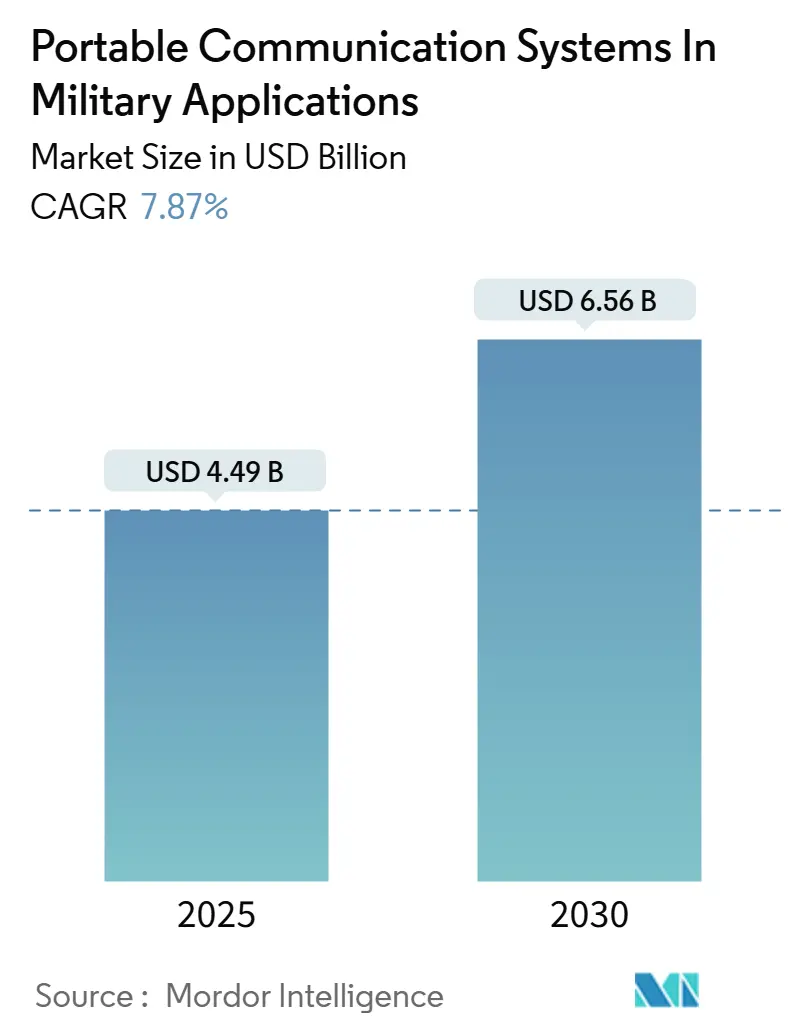

| Market Size (2025) | USD 4.49 Billion |

| Market Size (2030) | USD 6.56 Billion |

| Growth Rate (2025 - 2030) | 7.87% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

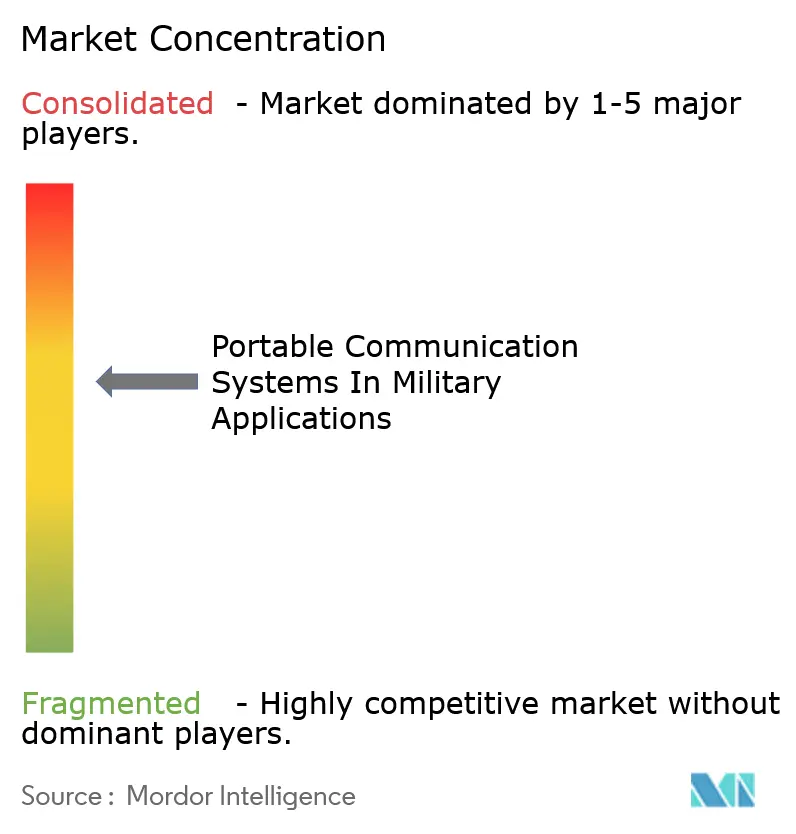

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Analysis of Portable Communication Systems In Military Applications by Mordor Intelligence

The portable communication systems in the military applications industry analysis size is valued at USD 4.49 billion in 2025 and is projected to reach USD 6.56 billion by 2030, reflecting a 7.87% CAGR over the forecast period.

Growth is fueled by defense ministries shifting from single-channel voice sets to software-defined platforms that host multiple waveforms, integrate 5G links, and mesh with Low-Earth-Orbit (LEO) satellites. Programs such as the U.S. Army Integrated Tactical Network and NATO’s STANAG 4677 mandate tight interoperability and continuous cybersecurity patching, creating demand for multi-band radios that update over the air.

Battery breakthroughs that cut weight by 30% and double run-time are closing a long-standing endurance gap for 72-hour patrols. At the same time, cognitive spectrum-management algorithms proven in DARPA tests are mitigating congested urban frequencies and reducing downtime by up to 70%. Competitive intensity rises as commercial 5G vendors adapt private-network chips that undercut legacy pricing by nearly 40%.

Key Report Takeaways

- By communication type, radio systems led with a 52.35% market share of the man-portable military communication systems market in 2024; 5G/6G tactical links are forecast to expand at a 9.12% CAGR through 2030.

- By frequency band, HF/VHF/UHF held 51.85% revenue in 2024, while millimetre-wave solutions are projected to grow at a 9.66% CAGR during the same period.

- By technology, software-defined radio accounted for 43.71% share of the man-portable military communication systems market size in 2024, and cognitive/AI-driven radios are advancing at an 8.73% CAGR to 2030.

- By component, transceivers and modems captured 47.16% of the revenue in 2024; batteries and power units are expected to rise at an 8.45% CAGR between 2025 and 2030.

- By end-user, infantry dominated with 53.81% of the man-portable military communication systems market share in 2024, whereas special operations forces exhibit the fastest 7.76% CAGR outlook.

- By platform, hand-held devices contributed 49.74% revenue in 2024, while wearable form factors are poised for a 9.67% CAGR through 2030.

- North America retained a 44.83% share in 2024, yet Asia-Pacific is forecast to deliver the highest 9.95% CAGR over the outlook horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Insights and Trends of Portable Communication Systems In Military Applications

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding multi-domain operations doctrine | +1.2% | Global, led by US, NATO, Quad | Medium term (2-4 years) |

| Battlefield digitisation programmes in NATO and Quad nations | +1.1% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Surge in low-earth-orbit defence satcom constellations | +0.9% | Global, early uptake in North America and Europe | Medium term (2-4 years) |

| AI-enabled spectrum management for contested EW environments | +0.8% | Global, priority Indo-Pacific and Eastern Europe | Short term (≤ 2 years) |

| Soldier-worn power/weight breakthroughs | +0.7% | North America, Europe, spillover Asia-Pacific | Medium term (2-4 years) |

| Integration of native 5G/6G waveforms into tactical radios | +1.0% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding Multi-Domain Operations Doctrine

Joint All-Domain Command and Control architectures demand that dismounted radios relay targeting data across land, air, maritime, cyber, and space nodes within seconds, compressing kill-chain timelines from minutes to single-digit seconds.[1]Jen Judson, “Project Convergence Compresses Kill Chain,” defensenews.com NATO’s 2024 concept paper stipulates Link 16, JREAP, and Variable Message Format coexistence inside hand-held form factors, forcing vendors to embed multi-waveform chipsets.[2]NATO ACT, “Multi-Domain Operations Concept,” nato.int Project Convergence exercises in 2024 verified under-five-minute sensor-to-shooter loops, validating procurement of software-defined radios that can dynamically join joint fires networks. Australia, Japan, and other Indo-Pacific allies followed with billion-dollar upgrades aligning with AUKUS or Quad frameworks. These parallel investments lift baseline volumes and unify interface standards, accelerating global adoption of dual-mode radio–satellite designs.

Battlefield Digitisation Programmes in NATO and Quad Nations

Morpheus in the UK, Digitalisierung der Landstreitkräfte in Germany, and India’s USD 3.5 billion Tactical Communication System exemplify wholesale transitions from voice-centric sets to soldier-worn IP networks.[3]Jonathan Saul, “Urban Spectrum Congestion Threatens Troops,” reuters.com Contract awards across Europe and Asia-Pacific require over-the-air upgrades, biometric log-ins, and encrypted apps that mirror commercial smartphones. Marine Corps networking kits embed antennas inside plate carriers, freeing operators’ hands and shortening reaction time. Poland’s 2024 order for AI-driven FONET radios shows how smaller NATO countries leapfrog directly to cognitive technology. Volume commitments secure economies of scale, making advanced features affordable to mid-tier militaries by 2027.

Surge in Low-Earth-Orbit Defence Satcom Constellations

Starshield, the Space Development Agency’s Proliferated Warfighter Space Architecture, and the EU’s IRIS² are placing hundreds of satellites that link directly to man-portable terminals with <30 ms latency.[4]SpaceNews Staff, “DoD Boosts PLEO Satcom Budget,” spacenews.com LEO orbits sidestep geostationary chokepoints and offer jam-resistance by sheer path diversity. The weight of soldier-carried terminals has fallen below 2 kg, enabling full-motion video streaming from dismounts to brigade command posts. Refuel-on-orbit services extend constellation life, lowering per-user cost by as much as 60% over a decade. Nations without organic space assets can now rent bandwidth, widening addressable demand for satcom-enabled handsets.

AI-Enabled Spectrum Management for Contested EW Environments

DARPA contests proved that machine-learning algorithms extract and exploit idle spectrum slices 40% faster than manual planning. Early fielding across US brigade combat teams cut jamming-induced outages by 70% during 2024 exercises. NATO STANAG 4677 now obliges radios to include cognitive waveforms that sense, decide, and hop in sub-millisecond cycles. Thales' handheld prototypes apply reinforcement learning to anticipate jammer behavior, pre-emptively relocating channels and slashing detection risk. Quantum-resistant encryption grants future-proof security, yet increases processing loads and pushes designers to integrate efficient batteries.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Congested RF spectrum in urban theatres | -0.6% | Global, acute Middle East and Asia-Pacific cities | Short term (≤ 2 years) |

| Export-control barriers (ITAR, Wassenaar) | -0.5% | Global, non-NATO markets most affected | Long term (≥ 4 years) |

| Cyber-hardening cost inflation vs. defense budgets | -0.4% | North America, Europe, emerging markets | Medium term (2-4 years) |

| Supply-chain chokepoints for GaN power amplifiers | -0.3% | Global, capacity clustered Taiwan and South Korea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Congested RF Spectrum in Urban Theatres

Combat in Gaza, Mosul, and Mariupol exposed saturation of 2.4 GHz and 5 GHz bands by civilian LTE, Wi-Fi, and IoT devices, eroding military link margin by 40%. The ITU’s 2024 World Radiocommunication Conference added only 40 MHz for defense, far short of requests. FCC coexistence rules for 3.1-3.45 GHz imposed USD 800 hardware filters per radio and extended schedules by six months. AI hopping at 1,000 channel/s counters jamming, but raises power draw 25%, shortening battery life. Higher transmit power and dense relay nodes inflate procurement and logistics bills at the battalion level.

Export-Control Barriers (ITAR, Wassenaar)

Category XI listings treat frequency-hopping, encrypted radios as munitions, adding 6-12 month license queues and banning sales to 40 nations. Wassenaar’s 2024 cryptography update forces vendors to strip quantum-safe algorithms from export variants, doubling code bases and fragmenting R&D. L3Harris noted USD 120 million lost orders in 2024, while EU dual-use rules now even govern intra-EU transfers. Indian offset laws compel 30% local content, reshaping supply chains and raising per-unit cost by 18%. These hurdles slow the global diffusion of advanced features and favor suppliers from non-signatory states.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Competitive Landscape

L3Harris Technologies Inc., General Dynamics Corporation, Raytheon Technologies Corporation, Elbit Systems Ltd, and Thales Group are some of the prominent players in the portable communication systems in military applications market. The defense manufacturing companies worldwide are focused on designing and developing inexpensive and lightweight man-portable communication systems to reduce the burden on dismounted infantrymen.

Also, there is a huge focus on man-portable communication systems that are secure and can communicate over a large portion of the spectrum while supporting multiple protocols. Thus, a high level of R&D is required to produce man-portable military communication solutions that incorporate newer technologies and lightweight materials to improve the effectiveness of the mission and the agility of the soldier.

Players are currently focusing on such technologies to develop new products and gain new contracts with the militaries, thereby enhancing their market presence and growth. In addition, there is also an increased focus on developing indigenous systems. For instance, the Indian Army is working on revamping its communication systems by procuring indigenous Very/Ultra High Frequency (V/UHF) Manpack SDRs under the Make-II category. Such developments are expected to drive the growth of the local players during the forecast period.

Leaders of Portable Communication Systems In Military Applications

L3Harris Technologies, Inc.

General Dynamics Corporation

Raytheon Technologies Corporation

Elbit Systems Ltd.

Thales Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: The Indian Army signed a contract for the procurement of its first indigenously designed and manufactured Software Defined Radios (SDRs). These SDRs were developed by the Defence Research and Development Organisation (DRDO) and are being produced by Bharat Electronics Limited (BEL).

- September 2025: Thales, in partnership with Malaysian company Advanced Defence Systems (“ADS”) Sdn. Bhd. secured a contract to deliver HF XL TRC 3900 vehicle-mounted radio stations. The contract includes radios, amplifiers, and antennas.

- January 2025: The US Army awarded L3Harris Technologies for the production orders for full-rate Manpack and Leader radios under the Handheld, Manpack & Small Form Fit (HMS) program. These orders are valued at nearly USD 300 million.

Scope of Report on Portable Communication Systems In Military Applications

Man-portable communication devices, such as handheld tactical radios, handheld satellite communication devices, both handheld and man-portable/transportable antennas, transmitters, and receiver systems, man-portable tactical terminals, manpack transceivers, and wearable communication systems used by the land, naval, and air forces are included in the study. The market is segmented by communication type (satellite and radio) and geography (North America, Europe, Asia-Pacific, Latin America, and Middle-East and Africa). The report offers the market size and forecasts for all the above segments in value (USD billion).

| Satellite |

| Radio |

| North America | United States |

| Canada | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Latin America | Brazil |

| Rest of Latin America | |

| Middle-East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle-East and Africa |

| Communication Type | Satellite | |

| Radio | ||

| Geography | North America | United States |

| Canada | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Latin America | Brazil | |

| Rest of Latin America | ||

| Middle-East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current Man-portable Military Communication Systems Market size?

The Man-portable Military Communication Systems Market is projected to register a CAGR of greater than 3.4% during the forecast period (2025-2030)

Who are the key players in Man-portable Military Communication Systems Market?

L3Harris Technologies, Inc., General Dynamics Corporation, Raytheon Technologies Corporation, Elbit Systems Ltd. and Thales Group are the major companies operating in the Man-portable Military Communication Systems Market.

Which is the fastest growing region in Man-portable Military Communication Systems Market?

North America is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Man-portable Military Communication Systems Market?

In 2025, the North America accounts for the largest market share in Man-portable Military Communication Systems Market.

What years does this Man-portable Military Communication Systems Market cover?

The report covers the Man-portable Military Communication Systems Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Man-portable Military Communication Systems Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: