Hypogonadism Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

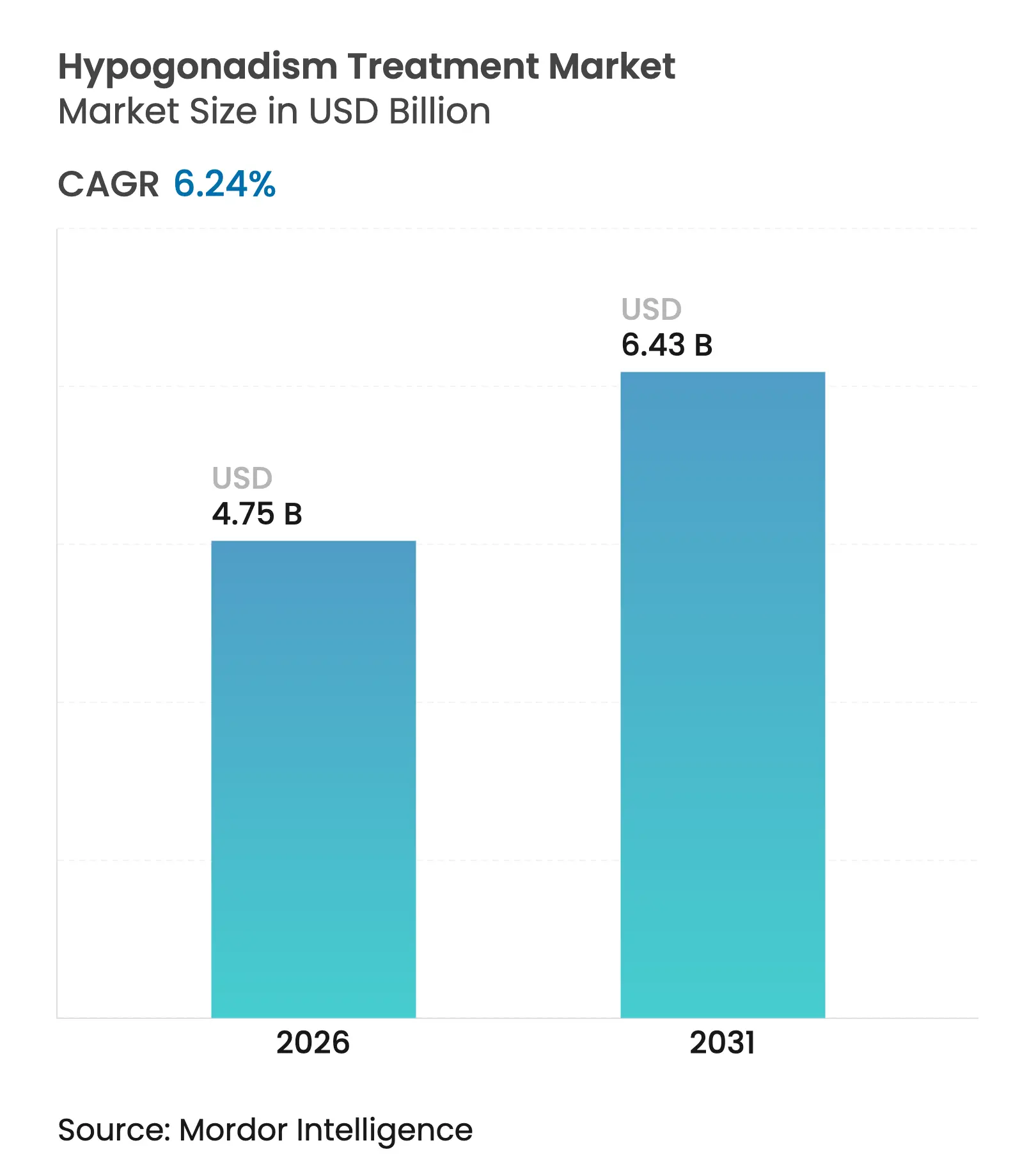

| Market Size (2026) | USD 4.75 Billion |

| Market Size (2031) | USD 6.43 Billion |

| Growth Rate (2026 - 2031) | 6.24 % CAGR |

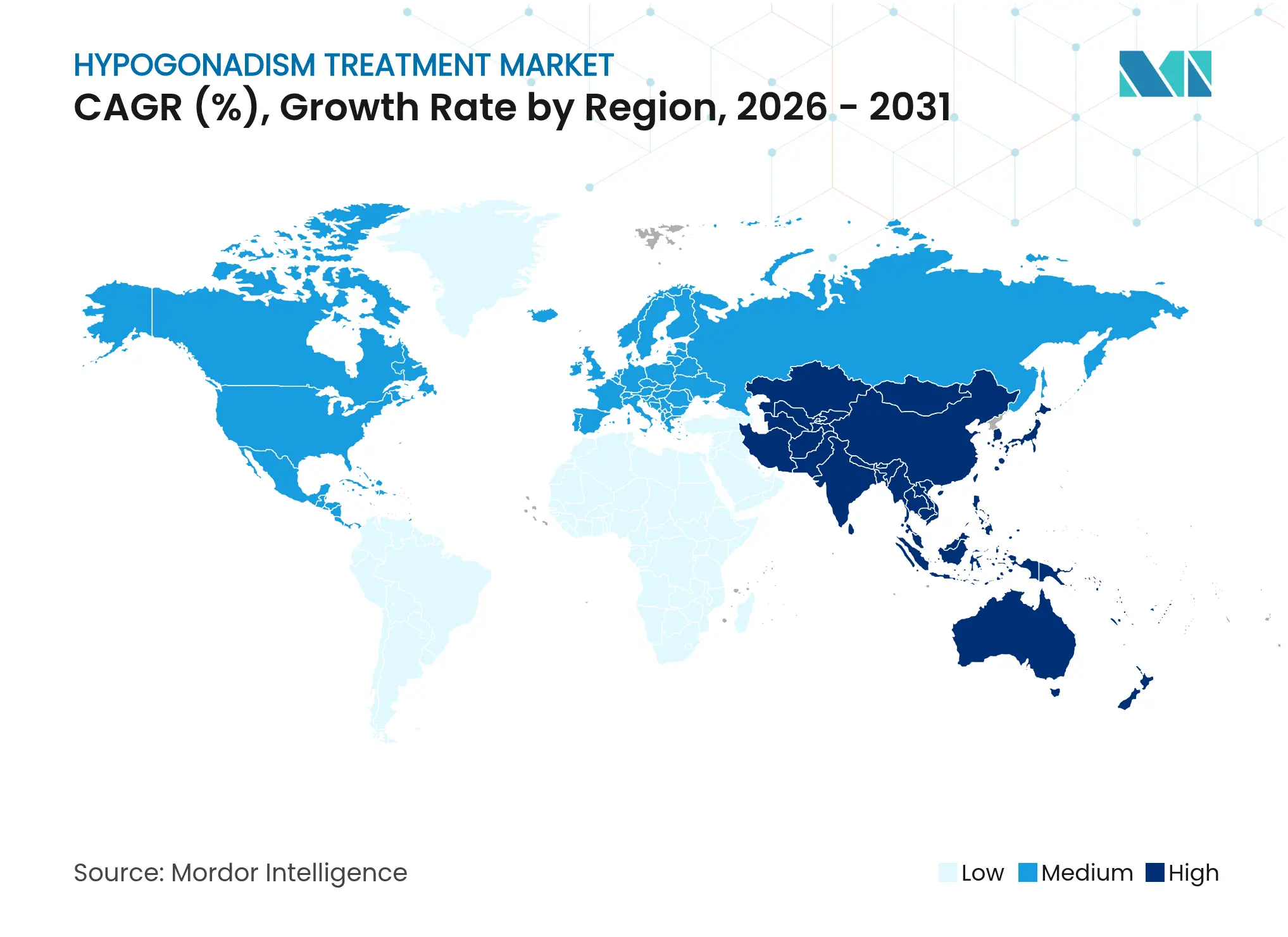

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

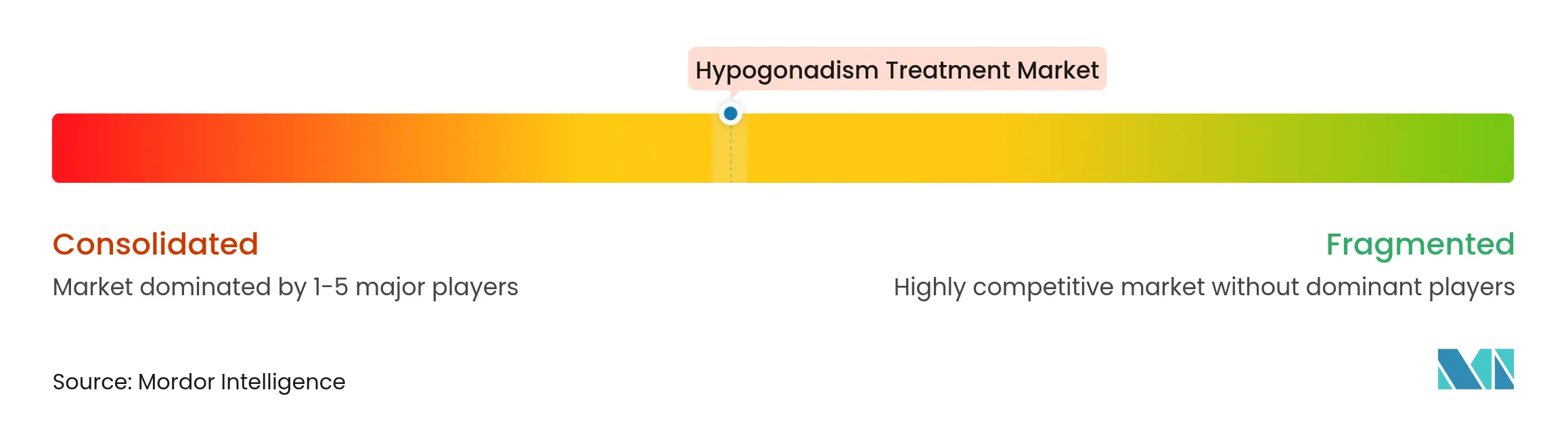

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Hypogonadism Treatment Market Analysis by Mordor Intelligence

The hypogonadism treatment market size was valued at USD 4.47 billion in 2025 and estimated to grow from USD 4.75 billion in 2026 to reach USD 6.43 billion by 2031, at a CAGR of 6.24% during the forecast period (2026-2031). Recent removal of United States Food and Drug Administration cardiovascular warnings from all testosterone labels, issued in February 2025, has resolved years of regulatory friction and immediately broadened eligibility for men with biochemically proven testosterone deficiency. Simultaneously, a swelling cohort of older males, incremental advances in diagnostic precision and an expanding pipeline of selective androgen receptor modulators (SARMs) support sustained uptake. North American telehealth operators intensify competitive pressures by lowering consultation hurdles, while product‐specific innovations—such as prefilled single-dose testosterone cypionate and high-bioavailability oral undecanoate capsules—directly tackle safety, convenience and adherence constraints that historically restrained long-term therapy adoption. Collectively, these factors establish a demand environment in which payers, clinicians and developers align behind a more permissive posture toward testosterone restoration for clearly identified endocrine deficiency rather than elective vitality enhancement.

Key Report Takeaways

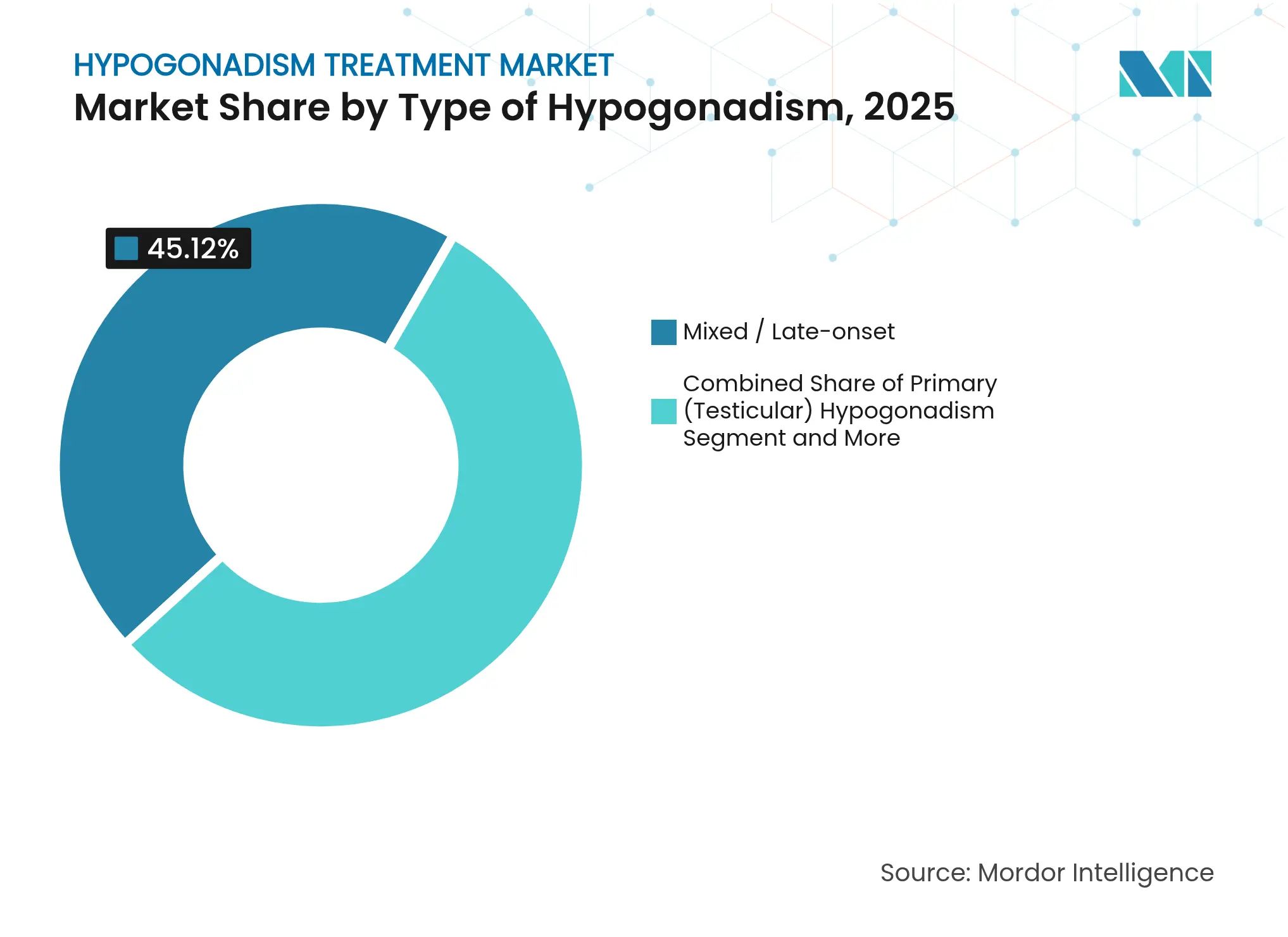

- By type of hypogonadism, mixed/late-onset presentations held 45.12% of 2025 hypogonadism treatment market share, whereas secondary/central hypogonadism is set to grow at a 9.25% CAGR through 2031.

- By therapy class, testosterone replacement therapy accounted for 83.86% of 2025 revenue, while SARMs are projected to advance at a 13.42% CAGR to 2031.

- By route of administration, topical gels captured 35.74% of 2025 demand, and oral/buccal tablets are poised for the quickest expansion at a 10.42% CAGR during the forecast horizon.

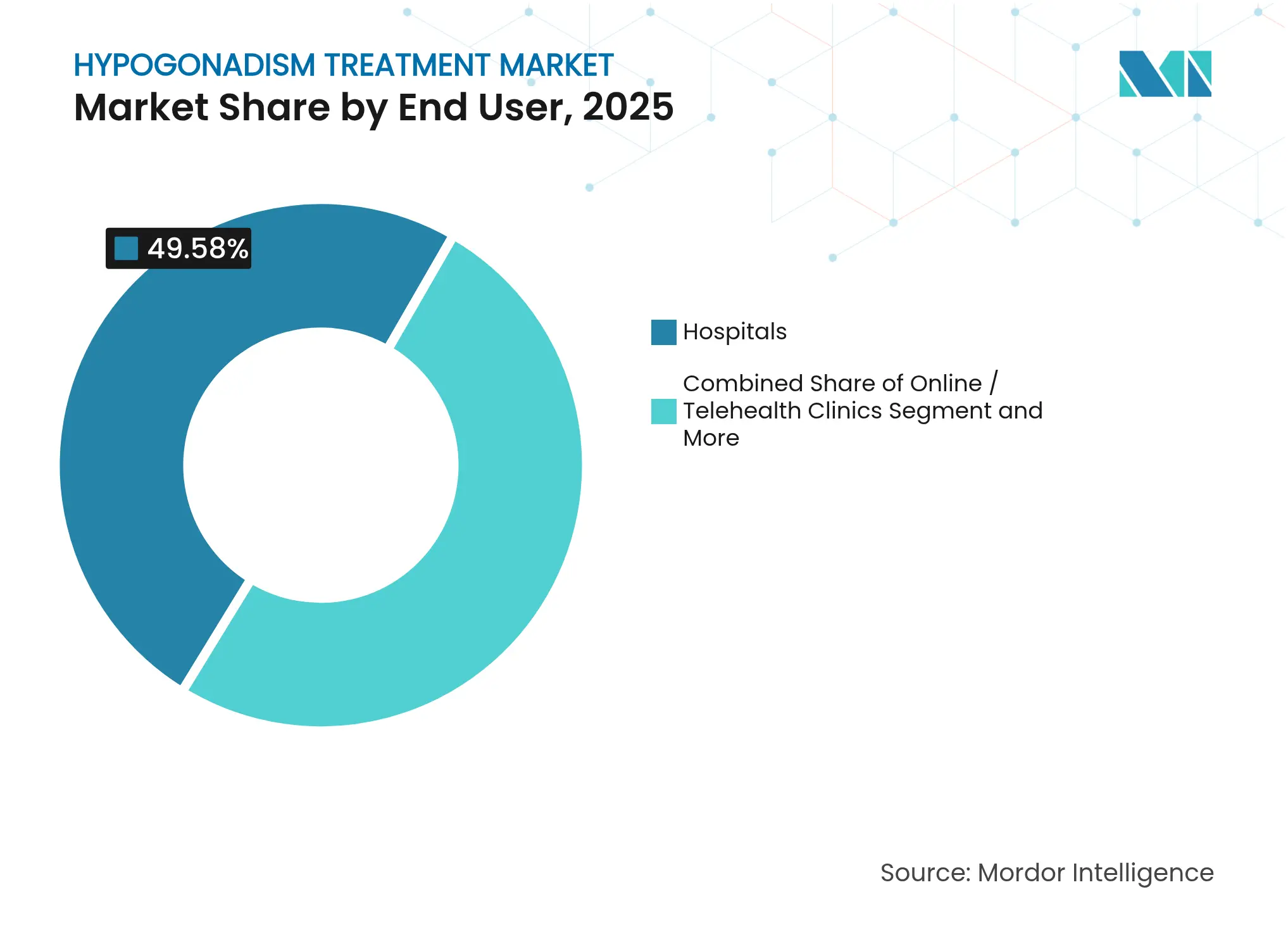

- By end user, hospitals contributed 49.58% of sales in 2025; online and telehealth clinics are forecast to climb at a 14.02% CAGR through 2031.

- By gender, male patients represented 89.74% of 2025 consumption, yet the transgender and non-binary segment is projected to grow at a 16.95% CAGR by 2031.

- By geography, North America commanded 38.95% of 2025 revenue, while Asia-Pacific is anticipated to rise at a 10.19% CAGR across the assessment period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hypogonadism Treatment Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising Prevalence Of Age-Related Hypogonadism

Rising Prevalence Of Age-Related Hypogonadism

| +1.8% | Global, concentrated in North America & Europe | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:

+1.8%

| Geographic Relevance:

Global, concentrated in North America & Europe

| Impact Timeline:

Long term (≥ 4 years)

|

Greater Awareness & Screening Initiatives

Greater Awareness & Screening Initiatives

| +1.2% | North America & EU, expanding to APAC | Medium term (2-4 years) | |||

Product Line Extensions In Testosterone Delivery

Product Line Extensions In Testosterone Delivery

| +0.9% | Global, with early adoption in US & EU | Short term (≤ 2 years) | |||

Selective Androgen Receptor Modulators Pipeline Traction

Selective Androgen Receptor Modulators Pipeline Traction

| +1.1% | Global, led by US regulatory pathway | Medium term (2-4 years) | |||

Telemedicine-Based TRT Clinics Scaling In U.S. & EU

Telemedicine-Based TRT Clinics Scaling In U.S. & EU

| +0.7% | North America & EU primarily | Short term (≤ 2 years) | |||

Relaxed U.S. 503B Outsourcing Rules For Pellet Implants

Relaxed U.S. 503B Outsourcing Rules For Pellet Implants

| +0.5% | United States | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Prevalence Of Age-Related Hypogonadism

Ageing biology remains the single most durable underpinning for long-run therapy demand. Serum testosterone typically recedes 1-2% annually after age 30, leaving a steadily expanding pool of men whose hormone levels slip below physiological thresholds for anabolic, metabolic and sexual health. Population longevity intensifies this phenomenon by prolonging the period during which deficiency symptoms appear, prompting health systems to embed systematic screening into routine senior men’s care. Japan’s EARTH study tracked 60 months of testosterone therapy and demonstrated durable symptom relief, thereby validating long-duration treatment in geriatric cohorts[1]Kazuyoshi Shigehara et al., “Testosterone Replacement Therapy Can Improve a Biomarker of Liver Fibrosis in Hypogonadal Men,” World Journal of Men’s Health, wjmh.org. Similar findings across Europe support calls for expanded public-health awareness campaigns, reinforcing the positive feedback loop between demographic ageing and market expansion.

Greater Awareness & Screening Initiatives

Updated clinical practice parameters now direct primary‐care physicians to evaluate testosterone in men with characteristic symptoms and consistent morning serum levels below laboratory reference ranges. Novel population-wide reference values drawn from more than 200,000 laboratory samples sharpen diagnostic certainty. Electronic health record triggers and direct-to-consumer test kits simplify first contact, while virtual consult platforms rapidly transition qualified patients into therapy. Together these mechanisms convert latent demand into treated prevalence, raising the ceiling for hypogonadism treatment market growth.

Product Line Extensions In Testosterone Delivery

Manufacturers are re-engineering legacy formulations to answer clinician concerns around contamination, dose variability and hepatic load. Azmiro—the first FDA-approved prefilled single-dose testosterone cypionate—removes multi-dose vial sterility hazards and delivers precise volumetric administration. Concurrently, KYZATREX oral undecanoate leverages lymphatic uptake to achieve 88% normalization of testosterone in pivotal trials without triggering first-pass hepatic strain, securing patent protection through 2040. Streamlined compounding rules for subcutaneous pellets under Section 503B add yet another adherence-friendly option. Each incremental convenience win translates into better persistence and, therefore, higher lifetime therapy value.

Selective Androgen Receptor Modulators Pipeline Traction

Tissue-selective agents like enobosarm deliver anabolic benefits to muscle and bone with minimal prostate or erythrocyte activation, answering long-standing safety objections to traditional testosterone. Phase 3 oncology and sarcopenia trials showcase lean-mass gains alongside improved functional endpoints, widening future addressable populations. Newer oral agonists such as LPCN 1148 have reduced hepatic encephalopathy flares while increasing skeletal muscle index in cirrhotic males. Although regulatory pathways remain complicated by historical supplement misuse, the clinical data trajectory positions SARMs as a credible competitor—and eventual adjunct—to conventional testosterone across many hypogonadism cohorts.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Safety & Cardiovascular Risk Perceptions

Safety & Cardiovascular Risk Perceptions

| -1.4% | Global, historically concentrated in US & EU | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:

-1.4%

| Geographic Relevance:

Global, historically concentrated in US & EU

| Impact Timeline:

Short term (≤ 2 years)

|

Social Stigma Surrounding Hormone Therapy

Social Stigma Surrounding Hormone Therapy

| -0.8% | Global, varying by cultural context | Long term (≥ 4 years) | |||

Reimbursement Hurdles & Prior-Authorization Delays

Reimbursement Hurdles & Prior-Authorization Delays

| -1.1% | North America & EU primarily | Medium term (2-4 years) | |||

API Supply Disruptions After China's Environmental

Crack-Downs

API Supply Disruptions After China's Environmental

Crack-Downs

| -0.9% | Global supply chain impact | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Safety & Cardiovascular Risk Perceptions

The TRAVERSE trial’s 5,246-patient dataset confirmed non-inferiority for major adverse cardiovascular events, enabling FDA removal of boxed warnings in early 2025. Nonetheless, marginal rises in atrial fibrillation and pulmonary embolism observed among testosterone users reignite debate over risk-benefit calculus. Physicians must now reconcile reduced headline warnings with new class-wide blood-pressure alerts covering all delivery forms[2]The Medical Letter, “In Brief: Azmiro,” medicalletter.org. Until consensus cardiovascular monitoring protocols stabilize, some prescribers and payers may employ stricter initiation criteria, curbing near-term uptake.

Social Stigma Surrounding Hormone Therapy

Associations between exogenous testosterone and performance enhancement or gender transition can deter symptomatic men from seeking evaluation. In certain regions, masculinity norms discourage discussion of fatigue, infertility or decreased libido, suppressing help-seeking behaviour. Public-education initiatives led by medical societies increasingly frame hypogonadism as a treatable endocrine deficiency rather than a lifestyle choice, yet cultural inertia remains tangible. Persistent stigma exerts a soft but chronic drag on the hypogonadism treatment industry by constraining diagnosis and adherence among otherwise appropriate candidates.

Segment Analysis

By Type of Hypogonadism: Mixed Presentations Drive Clinical Complexity

Mixed or late-onset presentations captured 45.12% of 2025 revenue, making them the largest slice of the hypogonadism treatment market. This dominance arises because progressive Leydig‐cell senescence often combines with partial hypothalamic or pituitary insufficiency, producing hormonally ambiguous profiles that demand treatment once clinical symptoms emerge. Secondary or central etiologies, while only a quarter of current incidence, will outpace all other categories at a 9.25% CAGR through 2031 as imaging and hormone panels detect subtle pituitary lesions sooner.

Clinicians increasingly parse mixed pathology into organic versus functional subsets, consistent with Italian Society of Andrology recommendations that drive tailored regimens. Awareness that chronic illness, obesity and medication burden can induce reversible central suppression encourages early therapeutic trials combined with lifestyle modification. As guideline adoption widens, the secondary segment’s contribution to hypogonadism treatment market size is projected to swell, bringing sophisticated diagnostic workflows into primary care and tele-endocrinology settings alike.

Note: Segment shares of all individual segments available upon report purchase

By Therapy Class: SARMs Challenge Testosterone Dominance

Testosterone formulations delivered 83.86% of 2025 hypogonadism treatment market size, underscoring their entrenched clinical role. Yet SARMs are forecast to surge at 13.42% CAGR, signalling a pivot toward molecules that isolate anabolic benefit from androgenic liability. Repeated demonstration of lean-mass gain in cachexia and age-related sarcopenia positions SARMs as either step-up therapy for high-risk men or first-line for patients wary of erythrocytosis and prostate events.

Progress remains gated by ongoing Phase 3 endpoints and FDA comfort with long-term safety datasets, but venture funding and pharmaceutical licensing deals suggest strong confidence in eventual commercialization. Once approved, SARMs could erode testosterone’s hypogonadism treatment market share both through direct substitution and combination protocols that lower total androgen exposure while maintaining eugonadal benefits.

By Route of Administration: Oral Formulations Gain Momentum

Topical gels held 35.74% of global revenue in 2025, reflecting decades of preference for non-invasive self-administration. However, the oral/buccal segment is advancing fastest, expanding at a 10.42% CAGR as pharmacokinetic hurdles are overcome by lymphatic absorption technologies. KYZATREX pivotal data show trough maintenance within physiologic bands without hepatotoxicity, persuading endocrinologists to consider pills for compliant candidates who dislike dermal transfer risks.

Injectable depots remain essential for men prioritizing quarterly dosing, now enhanced by sterile single-dose cypionate syringes that cut clinic preparation time. Pellet implants occupy a durable niche among patients who desire multi-month stability with minimal compliance burden. Collectively, diversified delivery drives patient‐centric tailoring, bolstering both adherence and lifetime value per treated individual in the hypogonadism treatment market.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By End User: Telehealth Disrupts Traditional Care Models

Hospitals generated 49.58% of 2025 expenditure owing to their pivotal role in complex endocrine workups and comorbidity management. Yet online clinics exhibit a 14.02% CAGR as app-based questionnaires, mailed laboratories and at-home sample collection compress the diagnostic interval. Virtual follow-up also mitigates geographic disparities, activating demand in communities underserved by endocrinologists.

Specialty centers retain an edge in multifactorial cases—such as infertility co-management or pituitary adenoma surveillance—but frequently partner with telemedicine firms to extend reach. Pharmacists, empowered by state collaborative practice agreements, open another front by running protocolized refill programs for stable patients. This fragmentation diffuses channel power and compels traditional providers to adopt hybrid models to protect share within the hypogonadism treatment industry.

Note: Segment shares of all individual segments available upon report purchase

By Gender: Transgender Segment Drives Fastest Growth

Male cisgender patients represented 89.74% of therapy volume in 2025, given the biological predominance of testicular insufficiency. Nevertheless, the transgender and non-binary cohort will expand at a 16.95% CAGR owing to broader social acceptance and increasing insurance alignment on gender-affirming hormone care. Clinical protocols for masculinizing therapy in this population often overlap dosing regimens used in primary hypogonadism, thereby leveraging existing supply chains.

Female androgen deficiency remains a smaller but clinically validated niche—particularly following oophorectomy—where low-dose formulations improve libido and mood. Ongoing psychiatric research underscores quality-of-life gains from appropriate testosterone titration in post-menopausal women. Expansion of gender-inclusive endocrinology curricula ensures future prescribers can navigate dosing nuance across sex spectra, supporting incremental lift to hypogonadism treatment market growth.

Geography Analysis

North America secured 38.95% of 2025 global sales supported by mature payer structures, direct-to-consumer testing and widespread telehealth infrastructure. Clinician familiarity with long-acting injectables and topical gels further entrenches penetration among symptomatic men. Yet the region’s saturated awareness and strict prescription oversight temper volume acceleration.

Asia-Pacific will set the growth pace at a 10.19% CAGR as demographic ageing converges with rapid healthcare-access expansion. Japanese longitudinal data proving symptom benefit over 60 months catalyze regional guideline harmonization. China’s parallel surge in menopausal hormone therapy illustrates cultural normalization of endocrine interventions, likely spilling over into male deficiency management. India’s urban clinics increasingly market bundled lab panels and teleconsults targeting fatigue and metabolic syndrome, thus broadening addressable hypogonadism treatment market size.

Europe combines universal coverage with stringent prescribing criteria, producing steady but moderate volume gains. Market potential grows as the European Association of Urology refines late-onset hypogonadism definitions to streamline initiation. The Middle East and Africa, though embryonic, show positive directionality given private-sector hospital growth and expatriate demand for Western standard care. South America’s moderating inflation and progressive medical licensure reciprocity foster cross-border telehealth initiatives that inject new competition into urban centres.

Competitive Landscape

Market Concentration

The hypogonadism treatment market is moderately consolidated. AbbVie, Pfizer and Endo International maximise scale via depth across gels, injectables and adjunct therapies, leveraging sales forces that already co-detail urology and primary-care products. AbbVie recorded USD 56.334 billion in 2024 net revenue, underwriting continuous life-cycle management of its hormone portfolio. Pfizer preserves franchise relevance through supply agreements on generic testosterone esters filed with regulators worldwide.

Disruptive entrants build brand equity around convenience. Marius Pharmaceuticals’ intellectual-property moat for KYZATREX secures exclusivity until 2040, incentivising direct-to-consumer outreach that bypasses traditional detailing. Azurity’s Azmiro pivots on delivery innovation to win prescriber trust in hospital and home-health channels. Telehealth conglomerates use subscription frameworks with automated laboratory scheduling to lock in multiyear customer lifetime value, pressuring legacy retail pharmacies.

Compounding outsourcing facilities operating under Section 503B inject bespoke pellet or cream variants for patients intolerant to commercial SKUs, intensifying price transparency. Long-run differentiation will pivot on combining therapeutic breadth with digital adherence monitoring, closing the loop among prescribers, labs and patients.

Hypogonadism Treatment Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Marius Pharmaceuticals received a sixth United States patent allowance for KYZATREX, extending exclusivity to 2040 and reinforcing its oral testosterone leadership.

- December 2024: Azurity Pharmaceuticals launched Azmiro, the first FDA-approved single-dose prefilled testosterone cypionate syringe for outpatient and self-administration.

Table of Contents for Hypogonadism Treatment Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Prevalence Of Age-Related Hypogonadism

- 4.2.2Greater Awareness & Screening Initiatives

- 4.2.3Product Line Extensions In Testosterone Delivery

- 4.2.4Selective Androgen Receptor Modulators (SARMs) Pipeline Traction

- 4.2.5Telemedicine-Based TRT Clinics Scaling In U.S. & EU

- 4.2.6Relaxed U.S. 503B Outsourcing Rules For Pellet Implants

- 4.3Market Restraints

- 4.3.1Safety & Cardiovascular Risk Perceptions

- 4.3.2Social Stigma Surrounding Hormone Therapy

- 4.3.3Reimbursement Hurdles & Prior-Authorization Delays

- 4.3.4API Supply Disruptions After China's Environmental Crack-Downs

- 4.4Porter's Five Forces

- 4.4.1Threat of New Entrants

- 4.4.2Bargaining Power of Buyers

- 4.4.3Bargaining Power of Suppliers

- 4.4.4Threat of Substitutes

- 4.4.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Type of Hypogonadism

- 5.1.1Primary (Testicular) Hypogonadism

- 5.1.2Secondary/Central Hypogonadism

- 5.1.3Mixed / Late-onset

- 5.2By Therapy Class

- 5.2.1Testosterone Replacement Therapy

- 5.2.2Estrogen Therapy

- 5.2.3Progesterone Therapy

- 5.2.4SARMs & Novel Androgens

- 5.2.5Gonadotropin-releasing Hormone Analogues

- 5.3By Route of Administration

- 5.3.1Topical Gel

- 5.3.2Transdermal Patch

- 5.3.3Intramuscular Injection

- 5.3.4Sub-cutaneous / Implantable Pellet

- 5.3.5Oral / Buccal Tablets

- 5.4By End User

- 5.4.1Hospitals

- 5.4.2Specialty Clinics

- 5.4.3Online / Telehealth Clinics

- 5.4.4Home-care Settings

- 5.5By Gender

- 5.5.1Male

- 5.5.2Female

- 5.5.3Transgender & Non-binary

- 5.6Geography

- 5.6.1North America

- 5.6.1.1United States

- 5.6.1.2Canada

- 5.6.1.3Mexico

- 5.6.2Europe

- 5.6.2.1Germany

- 5.6.2.2United Kingdom

- 5.6.2.3France

- 5.6.2.4Italy

- 5.6.2.5Spain

- 5.6.2.6Rest of Europe

- 5.6.3Asia-Pacific

- 5.6.3.1China

- 5.6.3.2Japan

- 5.6.3.3India

- 5.6.3.4South Korea

- 5.6.3.5Australia

- 5.6.3.6Rest of Asia-Pacific

- 5.6.4Middle East and Africa

- 5.6.4.1GCC

- 5.6.4.2South Africa

- 5.6.4.3Rest of Middle East and Africa

- 5.6.5South America

- 5.6.5.1Brazil

- 5.6.5.2Argentina

- 5.6.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1AbbVie Inc

- 6.3.2Pfizer Inc

- 6.3.3Endo International

- 6.3.4Eli Lilly

- 6.3.5Bayer

- 6.3.6Ferring Pharmaceuticals

- 6.3.7Merck KGaA (Serono)

- 6.3.8Teva

- 6.3.9Viatris (Mylan)

- 6.3.10Clarus Therapeutics

- 6.3.11Acerus Pharma

- 6.3.12Besins Healthcare

- 6.3.13Novo Nordisk

- 6.3.14Ipsen

- 6.3.15Lupin Ltd

- 6.3.16Cipla Ltd

- 6.3.17Sandoz AG

- 6.3.18BioTE Medical

- 6.3.19Antares Pharma

- 6.3.20Endoceutics

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Hypogonadism Treatment Market Report Scope

Hypogonadism is a rare hormonal disorder characterized by insufficient production of testes or ovaries, result in diminished production of sex hormones. Hypogonadism Treatment Market is segmented By Type, Treatment Type, Route of Administration and Geography.