Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 0.99 Billion |

| Market Size (2026) | USD 1.04 Billion |

| Market Size (2031) | USD 1.28 Billion |

| Growth Rate (2026 - 2031) | 4.24% CAGR |

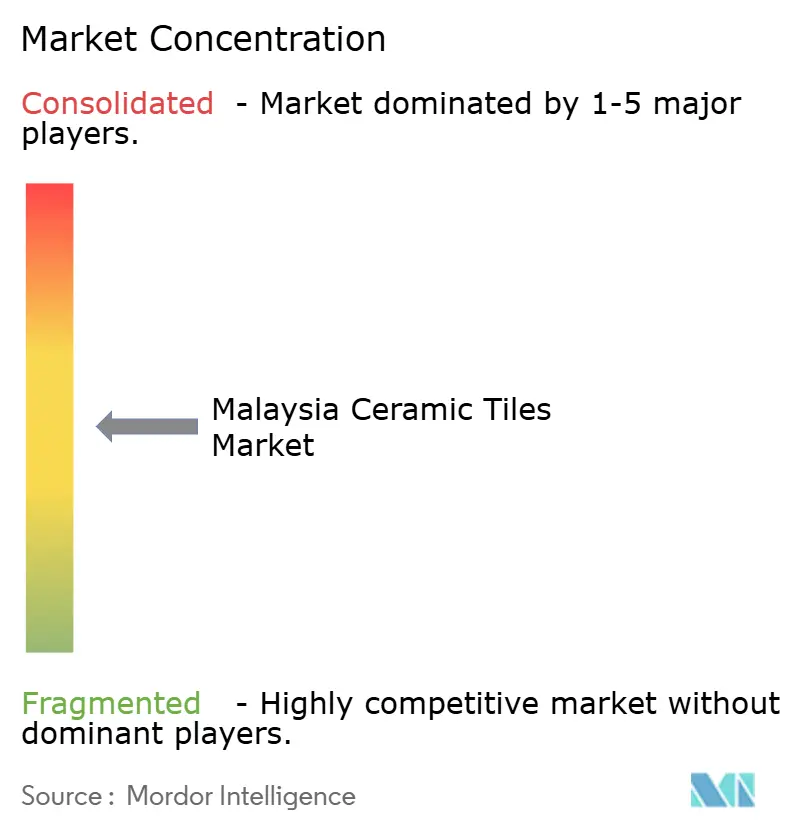

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malaysia Ceramic Tiles Market Analysis by Mordor Intelligence

The Malaysia ceramic tiles market size is projected to be USD 0.99 billion in 2025, USD 1.04 billion in 2026, and reach USD 1.28 billion by 2031, growing at a CAGR of 4.24% from 2026 to 2031. Central Malaysia’s Klang Valley accounts for 35.73% of 2025 revenue, supported by higher per-capita spending on decorative surfaces that is set to reach RM 760 million in 2026 and by RM 183.7 billion of construction contracts awarded in 2024. Planned outlays under the Thirteenth Malaysia Plan earmark RM 430 billion for public infrastructure, housing, and transport, which sustains demand across residential renovations and commercial fit-outs. East Malaysia is the fastest-growing region through 2031 at a 5.30% CAGR as federal investment in the Pan Borneo Highway and related energy logistics unlocks new development corridors. Import penetration remains high, with China shipping USD 219.6 million of tiles to Malaysia in 2024 and total volume near 66 million at an average USD 3.5/m², which tightens domestic pricing and pushes manufacturers toward premium large-format slabs and omnichannel sales[1]World Integrated Trade Solution, “Malaysia Imports of Ceramic Tiles,” World Bank, wits.worldbank.org.

Key Report Takeaways

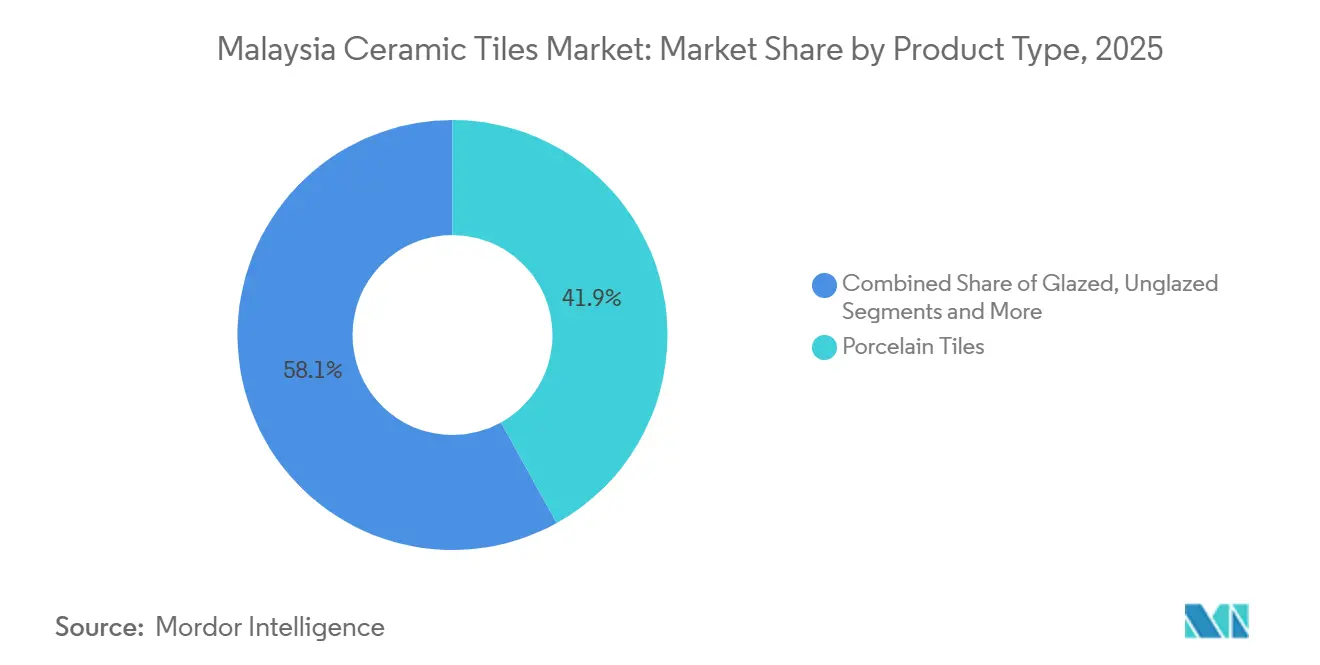

- By product type, porcelain led with 41.94% revenue share in 2025 in the Malaysia Ceramic Tiles Market, and porcelain is forecast to expand at a 4.89% CAGR through 2031.

- By application, floor tiles accounted for 58.91% of 2025 revenue in the Malaysia Ceramic Tiles Market, and floor applications are projected to grow the fastest at a 4.57% CAGR to 2031.

- By end-user, residential held 70.83% of the 2025 demand in the Malaysia Ceramic Tiles Market, whereas commercial is the fastest-growing at a 4.76% CAGR through 2031.

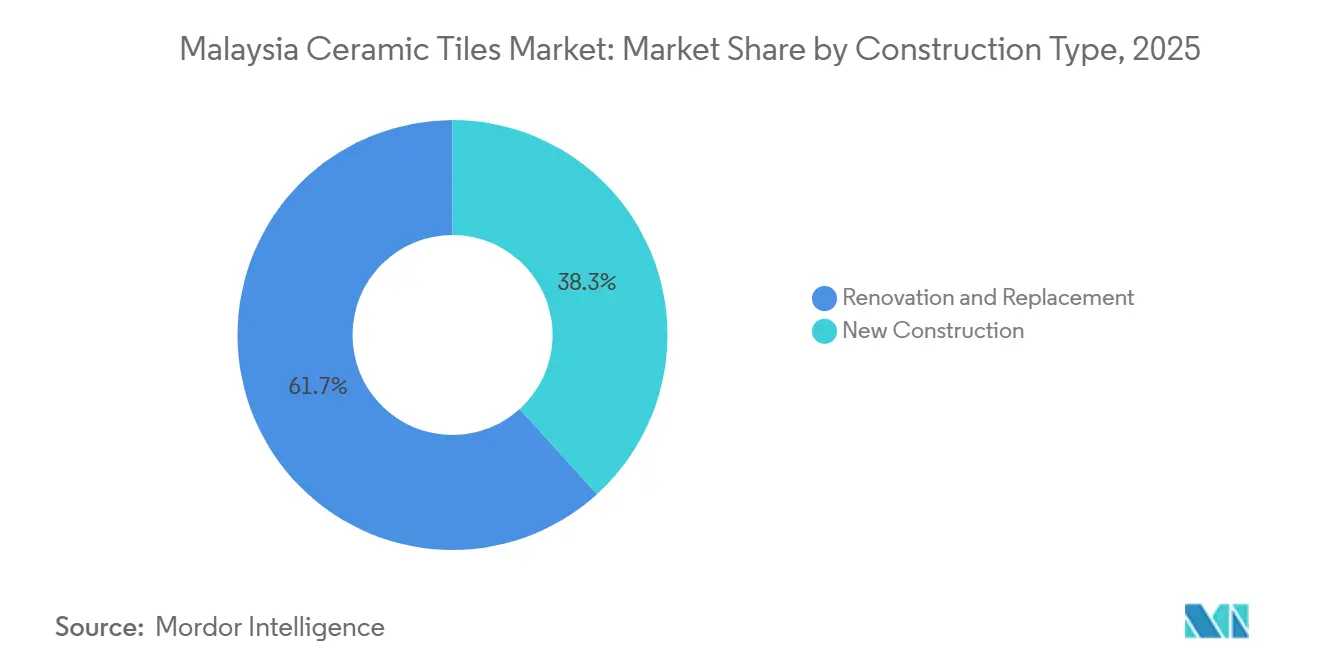

- By construction type, renovation captured 61.72% of 2025 spend in the Malaysia Ceramic Tiles Market, while new construction is expected to expand at a 5.28% CAGR through 2031.

- By distribution channel, home improvement and DIY stores controlled 41.07% of 2025 sales in the Malaysia Ceramic Tiles Market, while online retail is the fastest-growing at a 5.79% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Malaysia Ceramic Tiles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Affordable Housing Programs Sustain Base Demand | +1.2% | National, with concentrations in Klang Valley, Johor Bahru, Penang | Medium term (2-4 years) |

| Construction Rebound Supports Tile Consumption | +1.8% | National, particularly Central and Southern Malaysia | Short term (≤ 2 years) |

| Robust Renovation and Replacement Activity | +1.3% | National, with early gains in Kuala Lumpur, Petaling Jaya, Shah Alam | Short term (≤ 2 years) |

| Omnichannel Retail and Free 3D Design Accelerate Decisions | +0.6% | Urban centers, including Klang Valley, Georgetown, Johor Bahru | Medium term (2-4 years) |

| Local Large-Format Porcelain Slab Capability Emergence | +0.7% | Central Malaysia production hubs, spillover to APAC exports | Long term (≥ 4 years) |

| Eco-Labels and ESG-Linked Specifications Tilt Choices | +0.4% | National public procurement and private GBI-certified projects | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Affordable Housing Programs Sustain Base Demand

Malaysia’s Thirteenth Malaysia Plan targets one million affordable homes between 2026 and 2035 through federal, state, and private collaboration, which embeds ceramic tile specifications for kitchens, bathrooms, and common areas into standard build scopes. Budget support for affordable-housing lines and the Housing Credit Guarantee Scheme continues to enable first-time buyers in B40 and M40 groups, reinforcing steady baseline tile demand across mass-market projects. The Twelfth Malaysia Plan delivered 492,360 affordable houses by March 2025, which was 98% of its target, and an upswing in affordable-property transactions during 2024 aligned with stronger renovation activity after handover. Industrialized Building System adoption requirements on public housing aim for 70% content, which compresses schedules by 20–25% and reduces on-site labor by 30–40%, improving the predictability of tile installation windows. Fiscal measures such as selective stamp-duty concessions and rent-to-own options sustain pipeline conversions for price-sensitive buyers, supporting unit finishes that lean on durable, low-maintenance tiles in wet areas.

Construction Rebound Supports Tile Consumption

Malaysia’s construction work value reached RM 42.0 billion in Q4 2024, up 23.1% year-on-year, with momentum centered in residential and non-residential buildings that consume tiles at the fit-out stage[2]Department of Statistics Malaysia, “Quarterly Construction Statistics Q4 2024,” Department of Statistics Malaysia, dosm.gov.my. Private-sector projects contributed RM 27.0 billion in Q4 2024, or 64.2% of the total, while public-sector outlays reached RM 15.1 billion, reflecting broad-based demand catalysts for flooring and wall finishes. Within states, Selangor alone accounted for RM 9.4 billion of Q4 value, followed by Johor at RM 7.4 billion and Sarawak at RM 4.6 billion, highlighting the spatial focus of near-term tile consumption. The East Coast Rail Link is nearing full completion, and the Penang Light Rail Transit program advances, which tends to bring follow-on commercial and township developments that adopt tiles for public areas and mixed-use assets. Ongoing regulatory frameworks, including CIDB standards and green criteria embedded in public tenders, sustain specification patterns that reward certified materials and suppliers with proven delivery performance.

Robust Renovation and Replacement Activity

Malaysia’s home-ownership rate and an aging stock of public housing blocks drive upgrades for kitchens, bathrooms, and common areas, with federal allocations set aside in 2026 for urgent repairs and lift replacements across selected schemes. Renovation and replacement captured 61.72% of 2025 tile spending, reflecting demand for refresh cycles in occupied units and strata properties where owners prioritize quick-turn installations with predictable quality. Residential transactions rose in 2024 by both volume and value, improving the base for post-handover upgrades that typically use porcelain for floors and glazed ceramic for wet walls. The channel mix supports this shift, as Home Improvement and DIY stores drive weekend project traffic while online platforms offer visualization tools that enable side-by-side comparisons before purchase. Compliance with relevant national and green standards continues to influence adhesive and tile choices, especially where Environmental Product Declarations and low-VOC requirements are specified by project owners.

Omnichannel Retail and Free 3D Design Accelerate Decisions

Online retail is the fastest-growing distribution channel at a 5.79% CAGR through 2031, supported by virtual room visualizers, rapid last-mile delivery across Kuala Lumpur, and improved packaging that reduces breakage risk. Niro Ceramic Group provides free 3D design support and technical drawings, combining showroom experiences with strong inventory backing to compress decision cycles in both residential and commercial projects. Leading domestic brands have launched direct-to-consumer portals that integrate augmented reality previews, which lower the need for extended showroom visits and help end-users finalize layouts and grout-line patterns on mobile devices. DIY retailers complement this with live-streamed demonstrations, influencer content, and tutorials that build confidence among first-time renovators and small contractors. Mobile applications such as Alpha Tiles’ app enable on-site comparisons and approvals during contractor meetings, which shortens feedback loops between owners, designers, and installers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low-Cost Import Pressure from Regional Suppliers | -1.1% | National, with the highest impact on price-sensitive B40/M40 segments | Short term (≤ 2 years) |

| Rising Electricity and Gas Input Costs | -0.9% | National, most acute in Peninsular Malaysia manufacturing hubs | Medium term (2-4 years) |

| Skilled Tiling Labor Gaps and Execution Quality Risks | -0.7% | National, with acute shortages in Klang Valley, Johor Bahru, Penang | Medium term (2-4 years) |

| Slow BIM/Digital Uptake Among SMEs Delays Productivity Gains | -0.5% | National, most pronounced among G1–G3 contractors and mid-tier design firms | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Low-Cost Import Pressure from Regional Suppliers

Imports from China totaled USD 219.6 million in 2024 and reached approximately 66 million m² at an average USD 3.5/m², which constrains domestic pricing power and intensifies competition in cost-sensitive segments. Price-focused households often prioritize upfront costs over warranties or technical support, which channels demand for imported options at the lower end of the price spectrum. Chinese exports to Malaysia continued to expand into 2025 across a wide range of formats, reinforcing the need for local differentiation in product and service. Domestic manufacturers counter this by focusing on large-format slab capabilities, rapid customization through advanced digital glazing, and comprehensive installer support that is hard to replicate from abroad. Certification advantages in public tenders and omnichannel service bundles further insulate value propositions that emphasize total cost of ownership rather than unit price.

Rising Electricity and Gas Input Costs

Energy is a significant share of ex-factory cost, and recent tariff structures require careful load management across peak and off-peak windows to avoid margin erosion. Natural gas prices referenced for industry customers show quarterly variability, exposing kiln operations to higher input cost swings and complicating long-range production planning. Gas demand grew in 2024, and the broader energy mix remains sensitive to global fuel dynamics, which raises uncertainty for heavy energy users in manufacturing. Manufacturers that have invested in regenerative burners and waste-heat recovery demonstrate measurable efficiency gains, which can partially offset inflation in fuel and electricity. National energy transition objectives and efficiency regulations encourage continued upgrades to plant systems that reduce emissions intensity while improving long-term resilience in cost structures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Digital Glazing Lifts Porcelain Leadership

Porcelain tiles held 41.94% of 2025 revenue and are projected to grow at a 4.89% CAGR to 2031 as specifiers emphasize durability in high-traffic residential and commercial areas. The Malaysia ceramic tiles market size for porcelain is supported by digital glazing that replicates premium stones and by slab formats that reduce grout lines for a cleaner finish in hospitality and healthcare settings. Advanced printheads now allow selective glazing and precise graphics on thicker bodies, which improves both aesthetics and lead times for local buyers. Domestic slab capability compresses delivery windows to weeks rather than months, which aligns with the needs of fast-tracked fit-outs and phased renovation schedules.

Glazed ceramic remains important in cost-sensitive renovations and affordable units, while unglazed formats serve industrial areas where slip resistance is critical. Mosaics retain a role in boutique projects and heritage refurbishments that seek unique accents and artisanal patterns across compact surfaces. Domestic brands with ISO-aligned quality systems enhance export readiness as specification frameworks in the region prioritize certified products. This steady shift toward performance and reliability supports premiumization within the Malaysia ceramic tiles industry, even as low-cost imports remain a factor at the bottom of the price spectrum.

By Application: Commercial Walls Gain Ground with Hygienic Finishes

Floor applications accounted for 58.91% of 2025 demand and are set to post steady growth as residential upgrades and institutional projects reinforce preference for durable porcelain across living areas and high-traffic corridors. Wall applications are projected to grow the fastest at a 4.84% CAGR through 2031 as hotels, retail, and healthcare prioritize anti-microbial glazes and seamless vertical surfaces for maintenance and hygiene. The Malaysia ceramic tiles market size in wall applications benefits from growing use in public buildings, where infection-control guidelines favor non-porous, easy-clean materials across lobbies and patient areas. Large-format products further reduce grout density, which helps facilities attain desired cleaning standards and reduce downtime between turnovers.

In residential settings, wall tiles support kitchen backsplashes and bathroom refits, while in commercial interiors, they provide a cost-effective alternative to natural stone on feature walls. Roofing tile usage remains concentrated in landed properties and niche energy-saving renovations that seek thermal benefits in hot climates. Broadly, application choices reflect a balance of lifecycle cost, installation speed, and compliance with green criteria that favor documented low-VOC adhesives and tiles with Environmental Product Declarations[3]Malaysian Investment Development Authority, “Green Building and Materials Certification in Malaysia,” MIDA, mida.gov.my. As project pipelines span residential, institutional, and transport facilities, tiles continue to anchor finish schedules because of versatility, hygiene performance, and competitive installed cost.

By End-User: Hospitality and Institutional Fit-Outs Raise Specifications

Residential end-users consumed 70.83% of tiles in 2025 as affordable housing delivery and unit turnovers sustained upgrading activity in kitchens and bathrooms. The Malaysia ceramic tiles market benefits from consistent owner-driven renovations and strata maintenance cycles that prioritize durable, low-maintenance surfaces. Commercial demand is set to grow the fastest at 4.76% CAGR through 2031, anchored by hospitality, retail, healthcare, education, and transport hubs that require performance features such as anti-slip ratings and rapid installation. Larger projects lean on domestic suppliers for just-in-time delivery and technical support that reduces installation risk in large-format jobs.

As new and upgraded airports, hospitals, and stations move through design and build, specifiers choose porcelain for its strength, ease of maintenance, and expanding range of stone-look and concrete-look designs. Corporate fit-outs and institutions also recognize low-emission requirements, which shift preferences toward certified local materials. Hospitality continues to drive premiumization in lobbies, ballrooms, and spa areas, while retail emphasizes safety and slip resistance in customer pathways. These use cases support sustained product innovation and service differentiation across the Malaysia ceramic tiles market as brands compete on both design and delivery.

By Construction Type: IBS-Ready Tiles Support Faster Handover

Renovation and replacement captured 61.72% of 2025 spending as homeowners upgraded older stock and strata properties executed lifecycle refits for common areas and amenities. The Malaysia ceramic tiles market sees steady renovation volumes supported by accessible retail channels and visualization tools that simplify design choices for owners and small contractors. New construction, though smaller in share, is projected to expand the fastest at a 5.28% CAGR through 2031, guided by affordable housing targets and sustained public development expenditure across transport and utilities. Public projects carry a 70% IBS content requirement, which shortens schedules and reduces onsite labor, and this supports large-format tiles that install with fewer pieces and joints[4]Construction Industry Development Board Malaysia, “IBS and Construction 4.0 Initiatives,” CIDB, cidb.gov.my.

Affordable-housing schemes encourage standardized bathroom and kitchen packages with base tile specifications, while premium projects incorporate larger formats and advanced finishes. Within both streams, consistent supply, batch matching, and post-installation support are important to minimize rework. As IBS and modular adoption deepens, demand tilts further toward system-compatible tile options that speed up on-site coordination and reduce wastage. These changes keep installation efficiency and lifecycle performance at the center of purchase decisions across the Malaysia ceramic tiles industry.

By Distribution Channel: AR and 3D Design Shift Discovery to Digital

Home Improvement and DIY stores controlled 41.07% of 2025 sales and continue to dominate large-ticket weekend purchases where tactile inspection and side-by-side viewing influence selection. The Malaysia ceramic tiles market also reflects growing online behavior as buyers research surface finishes digitally before visiting showrooms, then complete orders via mobile apps with scheduled delivery. Online retail is the fastest-growing channel at a 5.79% CAGR through 2031, driven by AR visualizers, better packaging, and rapid logistics coverage in urban centers. Free 3D design services and technical drawings from leading brands compress decision cycles and strengthen conversion across both residential and commercial accounts.

Specialty tile and stone stores curate high-end collections and imported series for boutique hospitality and luxury residential projects. Direct sales to contractors remain crucial in large-format jobs, where just-in-time delivery and application guidance can determine installation outcomes. Mobile apps from domestic brands provide on-site access to catalogs, which lowers friction in final approvals during site meetings. Together, these shifts broaden discovery, shorten cycles, and reinforce omnichannel as a defining feature of the Malaysia ceramic tiles market.

Geography Analysis

Central Malaysia, anchored by Klang Valley, commanded 35.73% of 2025 revenue due to higher discretionary spend on decorative surfaces and the concentration of residential renovations, commercial fit-outs, and data-centric infrastructure. Selangor contributed RM 9.4 billion of Q4 2024 construction work, supported by non-residential buildings, residential projects, and civil engineering activity that together underpin steady tile procurement. Transit-oriented zones in the region include affordable quotas that hardwire tile are spent into baseline construction specifications across kitchens, bathrooms, and public spaces. Major rail and urban-transit projects support sustained commercial fit-out demand, which includes stone-look porcelain for lobbies and composite systems for concourses. The Malaysia ceramic tiles market share in Central Malaysia benefits from extensive installer networks and omni-channel retail density across Kuala Lumpur, Petaling Jaya, and Shah Alam.

Southern and Northern corridors show healthy pipelines linked to industrial investments, logistics hubs, and transport connectivity. Johor’s proximity to Singapore supports mixed-use townships and higher-end residential products with open-plan layouts that favor larger formats, while Penang leverages technology manufacturing and airport expansion to anchor premium specifications for clean-room adjacent spaces. Federal road maintenance and regional upgrades sustain retail and hospitality refurbishments, which support steady tile off-take across suburban centers and industrial estates. In both regions, GBI-certified projects influence procurement toward ISO-certified suppliers with EPD documentation. These dynamics favor domestic brands with reliable availability, consistent batch matching, and local technical support.

East Coast and East Malaysia account for a growing share of incremental demand as megaprojects and sustainability targets accelerate. East Malaysia, covering Sabah and Sarawak, is the fastest-growing region with a 5.30% CAGR through 2031, propelled by the Pan Borneo Highway, energy logistics, and a state-level blueprint that sets green building targets. Sarawak recorded RM 4.6 billion of construction work in Q4 2024, with activity spanning power plants and maritime infrastructure, which drives fit-out needs for associated commercial premises. Airport expansions in Kota Kinabalu, Tawau, and Miri reinforce the use of large-format tiles for terminals and concession areas, while civic projects adopt certified finishes to meet sustainability goals. As supply chains strengthen and local distributors deepen inventory coverage, the Malaysia ceramic tiles market size in East Malaysia is positioned to capture a larger portion of premium and mid-market spend.

Competitive Landscape

Malaysia’s ceramic tiles sector is moderately concentrated, with several sizable domestic producers balanced by substantial import inflows that keep pricing competitive. Competitive strategies emphasize large-format slab capabilities, ISO-aligned environmental systems, and omnichannel journeys that include free 3D design and rapid delivery, which together build defensible differentiation against low-cost imports. Partnerships with technology suppliers have enabled higher-resolution digital printing and selective glazing at scale, which improves aesthetics while preserving lead-time advantages.

Guocera’s collaboration with Gruppo B&T to install a slab plant in Johor positions the firm as the first domestic manufacturer capable of 120×240 cm formats with Industry 4.0 automation, reducing dependence on imports for premium formats. Niro Ceramic Group expanded its large-format portfolio with designer-focused collections and provides free 3D design services, which strengthen conversion across retail and project channels. White Horse invested in efficiency upgrades such as regenerative burners to reduce gas consumption, while also maintaining quality and environmental certifications that align with public and private tender requirements.

New entrants and adjacent players are reinforcing premium segments and showroom experiences. Hafary launched “The House of MML” in Petaling Jaya as an immersive flagship that showcases luxury tiles for high-end residential and hospitality projects. Dongpeng Malaysia expanded displays and services for sintered stone and oversize slabs, offering planning support and installation across multiple states. Digital tools such as Alpha Tiles’ app are integrated into contractor workflows for on-site comparisons, tightening decision loops from proposal to purchase. These combined moves reinforce a clear trajectory in the Malaysia ceramic tiles market toward design-led premiumization, faster delivery, and certified performance.

Malaysia Ceramic Tiles Industry Leaders

White Horse Ceramic Industries

Guocera (Hong Leong Industries)

Kim Hin Industry Berhad

MML (Malaysian Mosaics)

Niro Ceramic Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Dongpeng Malaysia showcased its MAX SIZE sintered stone collection and expanded free planning and installation services across showrooms in Petaling Jaya, Penang, and Sarawak.

- July 2025: Jubin Warisan Malaysia and Universiti Kebangsaan Malaysia partnered with GNG Tiles to launch a heritage-inspired collection that blends traditional motifs with modern geometry for local residential renovations.

- February 2025: Siam Cement Group announced capacity expansion across Southeast Asia, including a new Malaysian line dedicated to large-format porcelain and SPC composites.

- December 2024: KERAjet unveiled its K10 piezoelectric printhead, enabling selective digital glazing and higher discharge rates for Malaysian tile makers targeting mass customization.

Malaysia Ceramic Tiles Market Report Scope

The ceramic industry is the businesses related to making, marketing, and selling ceramics and ceramic parts, which includes tiles, pots and etc. This report aims to provide a detailed analysis of the Malaysia Ceramic Tiles Market. The report focuses on the market dynamics, emerging trends in the segments, and insights into various product and application types. Also, analyzes the key players, and competitive landscape. The Malaysian Ceramic Tiles Market is Segmented by Product (Glazed, Porcelain, Scratch Free, and Other Products), by Application (Floor Tiles, Wall Tiles, and Other Applications), by Construction Type (New Construction, Replacement, and Renovation), and End User (Residential and Commercial). The Report Offers Market Size and Forecasts for the Malaysian Ceramic Tiles Market in Value (USD) for all the Above Segments.

By Product Type

| Porcelain Tiles |

| Glazed Ceramic Tiles |

| Unglazed Ceramic Tiles |

| Mosaic Tiles |

| Others (Decorative, Patterned, Handmade) |

By Application

| Floor |

| Wall |

| Roofing |

By End-User

| Residential | |

| Commercial | Hospitality (Hotels, Resorts) |

| Retail Spaces | |

| Offices & Institutions | |

| Healthcare | |

| Educational Facilities | |

| Transport Hubs (Airports, Metro, Bus Terminals) | |

| Other Commercial Users |

By Construction Type

| New Construction |

| Renovation and Replacement |

By Distribution Channel

| Specialty Tile & Stone Stores |

| Home Improvement & DIY Stores |

| Online Retail |

| Direct Sales to Contractors |

By Geography

| Northern Malaysia |

| Central Malaysia (Klang Valley) |

| Southern Malaysia |

| East Coast Malaysia |

| East Malaysia (Sabah & Sarawak) |

| By Product Type | Porcelain Tiles | |

| Glazed Ceramic Tiles | ||

| Unglazed Ceramic Tiles | ||

| Mosaic Tiles | ||

| Others (Decorative, Patterned, Handmade) | ||

| By Application | Floor | |

| Wall | ||

| Roofing | ||

| By End-User | Residential | |

| Commercial | Hospitality (Hotels, Resorts) | |

| Retail Spaces | ||

| Offices & Institutions | ||

| Healthcare | ||

| Educational Facilities | ||

| Transport Hubs (Airports, Metro, Bus Terminals) | ||

| Other Commercial Users | ||

| By Construction Type | New Construction | |

| Renovation and Replacement | ||

| By Distribution Channel | Specialty Tile & Stone Stores | |

| Home Improvement & DIY Stores | ||

| Online Retail | ||

| Direct Sales to Contractors | ||

| By Geography | Northern Malaysia | |

| Central Malaysia (Klang Valley) | ||

| Southern Malaysia | ||

| East Coast Malaysia | ||

| East Malaysia (Sabah & Sarawak) | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the Malaysia ceramic tiles market?

The Malaysia ceramic tiles market size is USD 1.04 billion in 2026 and is projected to reach USD 1.28 billion by 2031 at a 4.24% CAGR.

Which product category leads demand in Malaysia?

Porcelain leads, holding 41.94% of 2025 revenue, and is forecast to grow at a 4.89% CAGR through 2031 due to durability and design versatility.

Which channels are growing fastest for tile purchases in Malaysia?

Online retail is the fastest-growing channel at a 5.79% CAGR through 2031, supported by AR visualizers, rapid delivery, and omnichannel integrations.

Which region is the fastest-growing for tile consumption?

East Malaysia is the fastest-growing region through 2031 at a 5.30% CAGR, driven by Pan Borneo investments and green-building targets.

What are the main headwinds facing tile manufacturers in Malaysia?

Key headwinds include low-cost imports, rising energy costs, skilled tiling labor gaps, and slow BIM uptake among SMEs.

Page last updated on: