South America Commercial HVAC Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

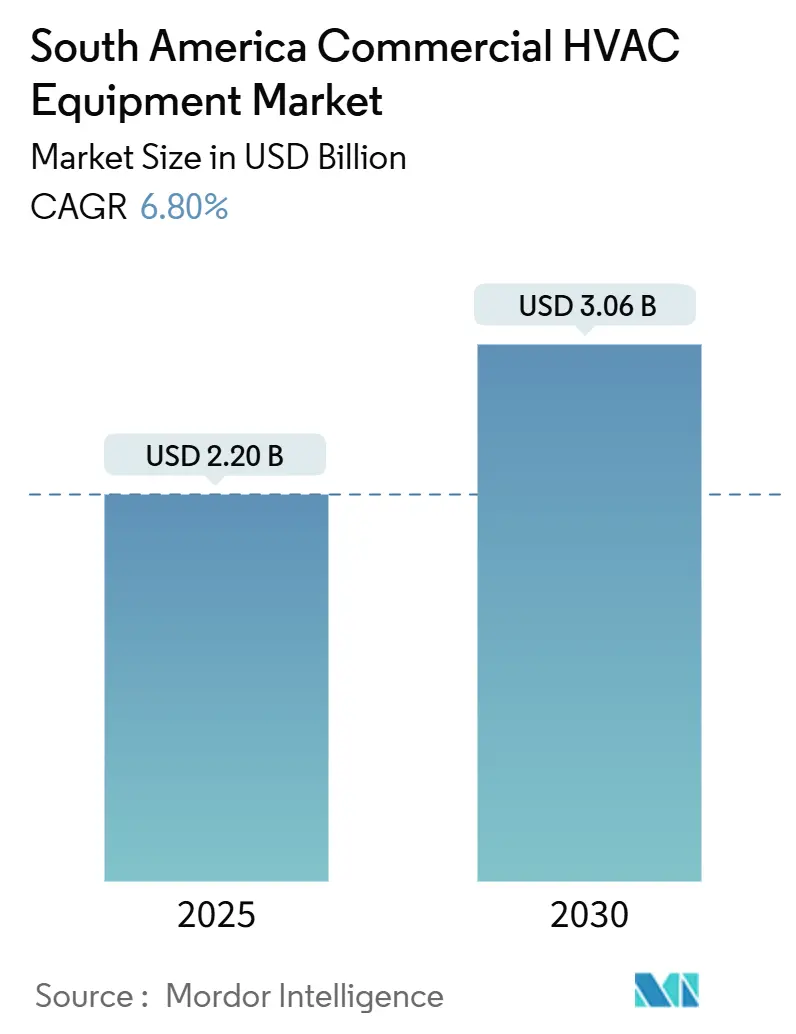

| Market Size (2025) | USD 2.20 Billion |

| Market Size (2030) | USD 3.06 Billion |

| Growth Rate (2025 - 2030) | 6.80% CAGR |

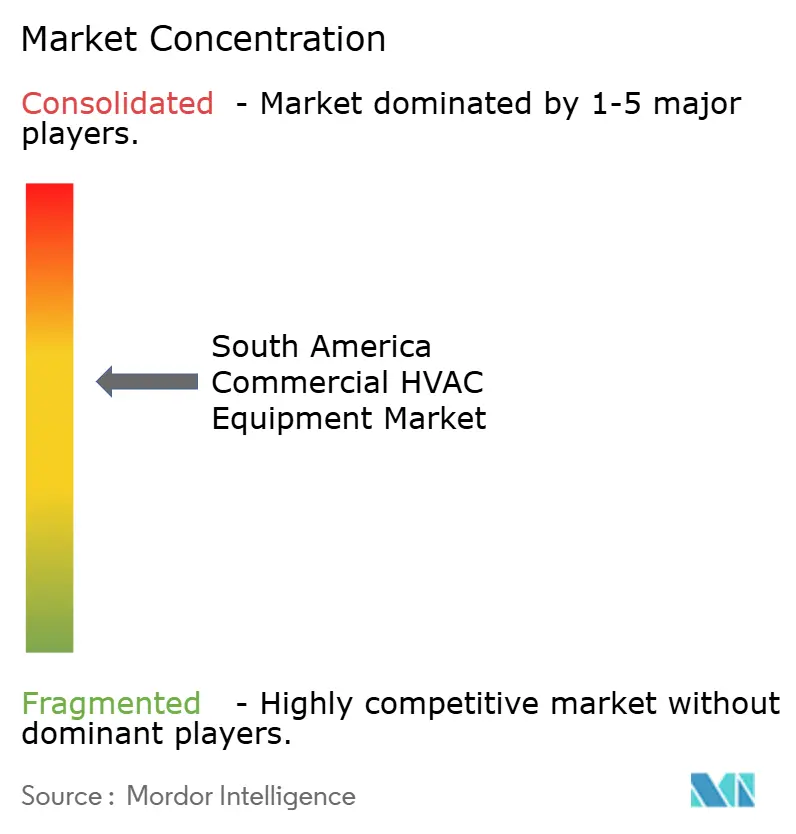

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Commercial HVAC Equipment Market Analysis by Mordor Intelligence

The South America commercial HVAC equipment market size stands at USD 2.20 billion in 2025 and is projected to reach USD 3.06 billion by 2030, expanding at a 6.8% CAGR during 2025-2030. Rapid urbanization, stricter energy-efficiency rules, and a surge of cold-chain warehouses and hyperscale data centers underpin this trajectory. Brazil’s air-conditioning sales climbed 38% in 2023 and a further 29% year-to-date in 2025, yet penetration remains far below developed-economy levels, leaving significant commercial whitespace. Retrofit programs dominate today, capturing 61.83% of the revenue in 2024, as building owners rush to replace legacy chillers with high-SEER variable-refrigerant-flow systems that meet corporate net-zero goals. New-build demand is accelerating in data center campuses and multinational retail chains, which are specifying integrated HVAC platforms with real-time monitoring and natural refrigerant options. Meanwhile, Asian manufacturers are localizing production to sidestep tariffs and currency risk, reinforcing competition and shortening delivery cycles.

Key Report Takeaways

- By installation type, retrofit projects accounted for 61.83% of the South America commercial HVAC equipment market share in 2024, while new-build activity is forecast to grow at an 8.01% CAGR through 2030.

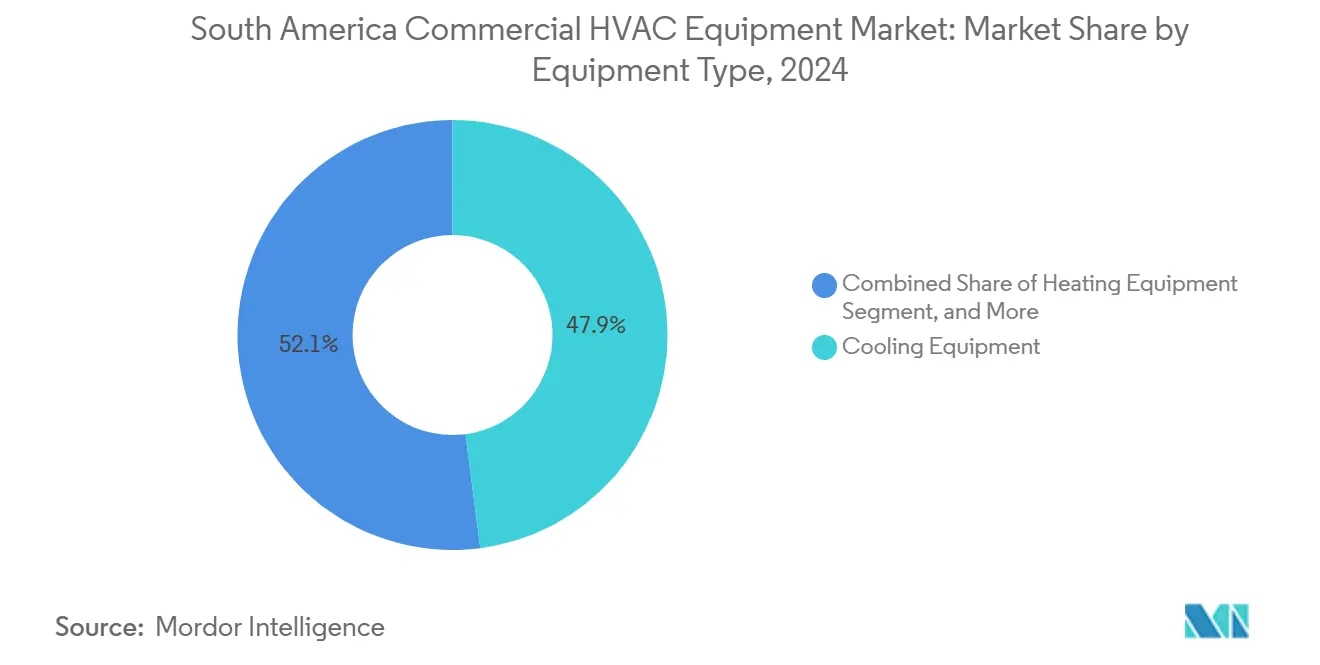

- By equipment type, cooling systems led with 47.94% revenue in 2024 of the South America commercial HVAC equipment market; integrated HVAC platforms are projected to expand at a 7.89% CAGR between 2025-2030.

- By capacity band, 51-200 kW units claimed 38.63% of the South America commercial HVAC equipment market size in 2024, but sub-20 kW units are advancing at a 7.33% CAGR, driven by the expansion of quick-service restaurants.

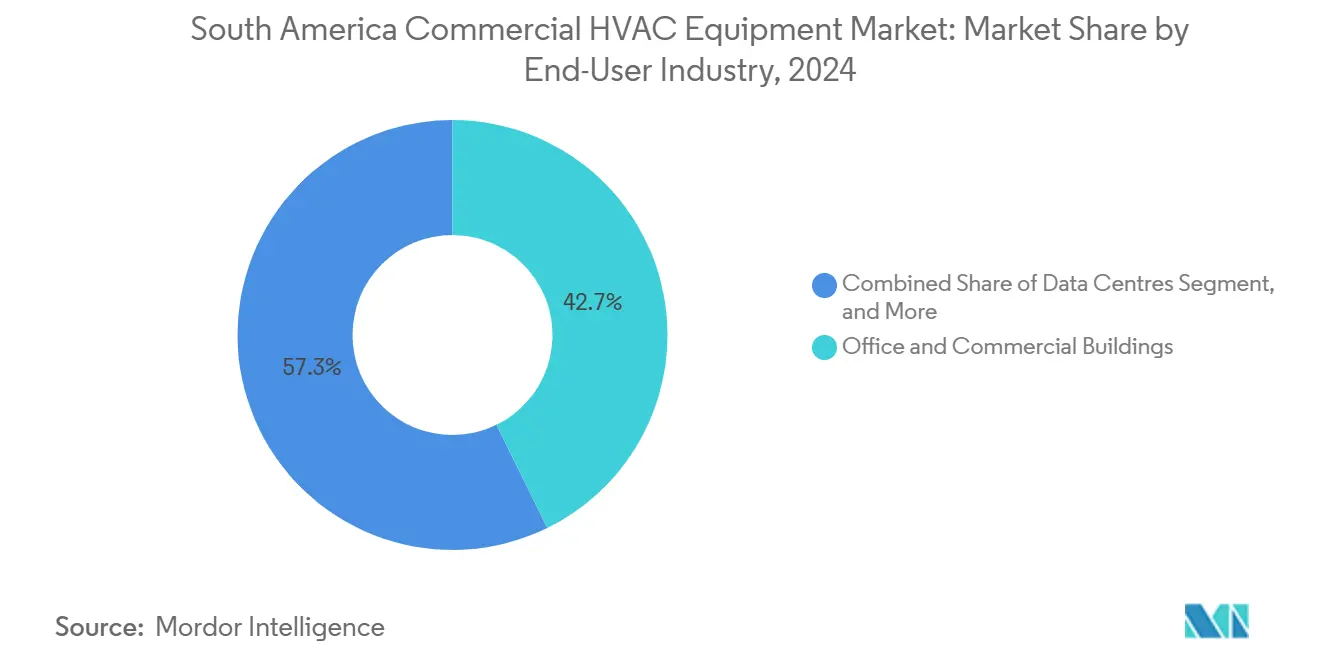

- By end user, office and commercial buildings captured 42.74% demand in 2024 of the South America commercial HVAC equipment market, whereas data centers are slated to record a 7.66% CAGR to 2030.

South America Commercial HVAC Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urbanization-linked commercial construction boom | +1.2% | Brazil, Argentina, Chile, Colombia | Medium term (2-4 years) |

| Mandatory energy-efficiency codes and labeling schemes | +1.0% | Brazil, Argentina, Chile, Colombia | Long term (≥ 4 years) |

| Expansion of cold-chain and quick-service retail formats | +0.9% | Regional urban and secondary cities | Short term (≤ 2 years) |

| Increasing availability of green finance for high-SEER systems | +0.8% | Colombia, Brazil, Chile | Medium term (2-4 years) |

| Surge in hyperscale data-center build-outs | +1.5% | Brazil, Colombia, Chile | Short term (≤ 2 years) |

| Corporate net-zero refrigerant commitments | +0.7% | Brazil, Chile, Colombia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Urbanization-Linked Commercial Construction Boom

Brazil’s construction industry expanded 2.3% in 2024 as post-pandemic recovery dovetailed with infrastructure rebuilding after Rio Grande do Sul floods, injecting roughly USD 20 billion into new projects.[1]Government of Brazil, “Emergency Reconstruction Funding Post-Floods,” gov.br São Paulo and Santiago have emerged as premier hubs for Class-A offices and life-science laboratories, each requiring multi-zone HVAC with building automation interfaces. Volkswagen’s USD 50 million upgrade to its Córdoba lorry facility illustrates selective industrial spend in Argentina despite macro volatility. Colombia’s high urbanization rate of more than 80% drives office, retail, and healthcare development into Bogotá, Medellín, and Cali, where occupancy permits increasingly depend on energy performance certificates. Chile’s 2024 Minergie label tailors Swiss Passivhaus benchmarks to seismic requirements, rewarding buildings that integrate heat-recovery ventilation and low-GWP chillers.

Mandatory Energy-Efficiency Codes and Building Labelling Schemes

Chile’s NCh 3308, issued May 2024, aligns ventilation minimums with ASHRAE 62.1, accelerating swap-outs of constant-air-volume systems for demand-controlled ventilation. Colombia’s RETSIT Resolution 40773, effective as of 30 December 2024, mandates energy audits for HVAC retrofits exceeding 50 kW and aligns with the nation’s Net-Zero Buildings Roadmap. Argentina’s Resolution 438/2024 now mandates efficiency labels for commercial splits and rooftops, with penalties for shipments that fail to comply.[2]Government of Argentina, “PAIS Tax Regulations,” argentina.gob.ar Brazil’s voluntary PROCEL Edifica label is expected to become compulsory for public buildings by 2026, unlocking concessional BNDES credit for A-rated projects. The IEA finds only one-third of South American countries enforce minimum HVAC performance standards, prompting multinationals to default to LEED or EDGE internal policies.

Expansion of Cold-Chain and Quick-Service Retail Formats

Emergent Cold South America operates 60+ temperature-controlled warehouses exceeding 4 million m³, stimulating procurement of industrial chillers above 200 kW. Arcos Dorados aims to commission 90-100 new McDonald’s restaurants in 2025, each outfitted with 10-15 kW packaged units for kitchen exhaust and dining-area comfort. ABRAVA data show Brazilian split-AC output jumped 71.3% in July 2024 versus the prior year, highlighting robust light-commercial demand. Chilean and Colombian grocers are choosing low-GWP refrigerants to hedge against higher power tariffs, Colombia’s commercial electricity rate climbed 12% in 2024, strengthening retrofit paybacks.

Increasing Availability of Green Finance for High-SEER Systems

Bancolombia floated USD 500 million in green bonds in 2024 and offers discounts of up to 2 points on commercial mortgages for projects exceeding a SEER of 14. Brazil’s BNDES covers 80% of equipment spend on PROCEL Edifica A-rated upgrades, while the IDB’s USD 3.4 billion ECO Invest facility hedges currency risk for imported high-efficiency chillers. IFC’s Cooler Finance initiative pegs annual sustainable-cooling demand at USD 600 billion by 2050, with South America absorbing roughly 15% of that pipeline. Chile’s 2024 green-mortgage framework allows borrowers to capitalize on energy savings, thereby lowering the loan-to-value ratio and increasing the adoption of variable-refrigerant-flow systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Currency volatility and macro-economic uncertainty | -0.9% | Argentina, Brazil, region-wide FX | Short term (≤ 2 years) |

| High front-loaded capex versus informal-sector alternatives | -0.6% | Brazil, Argentina, Colombia, Chile | Medium term (2-4 years) |

| Import tariffs and logistics bottlenecks on key components | -0.7% | Argentina, Brazil, region-wide ports | Short term (≤ 2 years) |

| Shortage of HVAC-R certified technicians | -0.5% | Brazil, Argentina, Chile, Colombia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Currency Volatility and Macro-Economic Uncertainty

Argentina’s 17.5% PAIS import tax and BOPREAL FX curbs inflate landed compressor costs by 10-15%. Brazil’s central bank maintained SELIC at 15% through 2024, which dampened developer cash flow as GDP growth cooled to 2.1%. The country filed 48 trade-remedy cases in 2024, raising costs for inverter compressors sourced from China. MERCOSUR’s new 45% local-value rule forces assemblers to source regionally or pay up to 20% in full tariffs.

Shortage of HVAC-R Certified Technicians for Advanced Systems

The IEA highlights HVAC roles as the hardest to fill, with South American firms citing a 62% shortage of digital and refrigeration skills. World Bank surveys show 83% of Argentine companies and 74% of Brazilian firms struggling to recruit skilled technicians.[3]World Bank, “Latin America Skills Survey 2024,” worldbank.org Brazil still lacks a binding commercial-building commissioning standard, hindering verification of installed performance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Integrated Systems Gain Traction

Cooling equipment captured 47.94% revenue in 2024, powered by summer peaks across tropical latitudes. Integrated platforms are poised to grow 7.89% through 2030 as developers specify variable-refrigerant-flow and BMS-ready chillers for Class-A towers and data halls. Heating remains niche, concentrated in southern cone microclimates, hybrid VRF solutions recovering waste heat are building a foothold. Ventilation demand is bolstered by Chile’s NCh 3308, which mandates outdoor-air exchange minima.

Samsung Electronics' USD 1.62 billion acquisition of FläktGroup, closed in 2025, adds European ventilation expertise to its portfolio, positioning the combined entity to serve hyperscale data centers and pharmaceutical clean rooms across South America. Johnson Controls' divestiture of its residential and light-commercial HVAC business to Bosch for USD 8.1 billion in July 2024 signals a strategic pivot toward integrated building-management systems and industrial controls, leaving a gap in the

By Capacity Rating: Below-20 kW Accelerates

Units rated 51-200 kW held 38.63% share in 2024, serving supermarkets and mid-rise offices across the South America commercial HVAC equipment market. Sub-20 kW systems are the fastest-growing niche at 7.33% CAGR, driven by fast-food chains and small-format retail. Above-200 kW chillers anchor data-center and cold-storage infrastructure, with Daikin and LG scaling regional output.

Carrier Global disclosed in its fourth-quarter 2024 earnings that it expects a 10-15% price increase for R-454B units in 2025, reflecting compressor and heat-exchanger redesigns, which may temporarily slow adoption in the below-20 kilowatt segment where price sensitivity is highest. Daikin Industries' USD 121 million facility in Tijuana, Mexico, scheduled to begin production in June 2025, will manufacture precision HVAC equipment for data centers, primarily in the 100-200 kilowatt range, to serve hyperscalers deploying artificial-intelligence workloads

By End-User Industry: Data Centers Outpace Traditional Segments

Office and commercial buildings delivered 42.74% demand in 2024, yet data centers will expand 7.66% annually to 2030 as hyperscalers chase AI workloads. Hospitality, healthcare, and education segments are leaning into VRF and chilled-beam solutions for efficiency and infection control.

Education institutions, including universities and technical schools, represent a smaller but growing segment, with Brazil's SENAI network of training centers upgrading HVAC systems to demonstrate energy-efficiency best practices to apprentices. Retail and supermarkets captured a significant share in 2024, with major chains upgrading to low-global-warming-potential refrigerant systems to comply with the Montreal Protocol's Kigali Amendment, Brazil's HPMP Stage 3, approved in 2024, allocates USD 36.5 million to eliminate 100% of HCFC consumption by 2030, with dedicated funding for chiller retrofits in supermarkets and cold-storage warehouses

By Installation Type: New-Build Gains Momentum

Retrofits owned 61.83% revenue in 2024, driven by compliance cycles and net-zero pledges across the South America commercial HVAC equipment market. New-build projects, however, will advance 8.01% CAGR amid a wave of data-center campuses and multinational retail rollouts that integrate high-SEER equipment from the outset.

Chile's Minergie certification, launched in October 2024, adapts Swiss Passivhaus standards to local seismic and climate conditions, creating a premium tier for new-build office towers and retail centers that adopt heat-recovery ventilation and high-efficiency chillers. Argentina's construction activity remains constrained by currency volatility, yet selective industrial expansions such as Volkswagen's USD 50 million investment in its Córdoba lorry plant signal demand for precision climate control in new manufacturing facilities

Geography Analysis

Brazil leads the South America commercial HVAC equipment market, driven by an 87% urbanization rate and a 38% increase in AC shipments in 2023. PROCEL Edifica is set to become mandatory for federal buildings by 2026, creating a retrofit boom financed through BNDES green credit lines. Asian OEMs are doubling down on local plants: Midea’s USD 120 million Pouso Alegre factory and LG’s USD 300 million Paraná facility shorten supply chains and buffer currency risk.

Argentina grapples with the PAIS import tax and BOPREAL FX hurdles that increase HVAC costs, yet efficiency labels now cover commercial splits and rooftops, encouraging owners to opt for compliant equipment. Chile’s Minergie and NCh 3308 standards raise the bar on ventilation and heat recovery, while green mortgage incentives lower financing costs. Colombia combines over 80% urbanization with strict RETSIT energy-audit rules, steering both retrofits and new builds toward high-efficiency systems. The remainder of South America, Peru, Ecuador, Uruguay, Paraguay, lags on enforcement but adopts international green-building labels to court institutional investors.

Rest of South America, including Peru, Ecuador, Uruguay, and Paraguay, represents a smaller but growing segment, with urbanization and rising disposable incomes driving demand for commercial HVAC equipment in capital cities. The International Energy Agency's 2024 South America energy-investment report noted that less than one-third of countries in the region enforce minimum energy-performance standards, leaving a regulatory gap that multinational developers fill by voluntarily adopting LEED or EDGE certifications to attract institutional tenants.

Competitive Landscape

The South America commercial HVAC equipment market features moderate fragmentation. Carrier Global, Trane Technologies, Johnson Controls, and Daikin Industries face stiff rivalry from Midea, LG, Samsung, and Gree, all intensifying local manufacturing to sidestep tariffs. Midea’s declared USD 1.95 billion R&D sprint targets USD 4 billion in near-term sales and a 20% lift in South America turnover by 2027. Samsung’s USD 1.62 billion acquisition of FläktGroup folds European ventilation into its portfolio and complements the Lennox JV, which focuses on VRF and low-GWP lines.

Johnson Controls’ USD 8.1 billion exit from the light-commercial HVAC market leaves a mid-capacity vacuum that Asian suppliers are moving to fill. Precision cooling for data centers is emerging as a lucrative niche, Carrier expects this vertical to account for over 15% of its regional revenue by 2025. Disruptors Hisense and Haier showcase modular chillers and residential VRF kits for the 51-200 kW band at RefriAméricas 2024. AHRI’s growing regional footprint may accelerate the adoption of standards and certification, smoothing multi-country compliance for multinationals.

White-space opportunities include precision HVAC for hyperscale data centers, where Carrier Global reported that data centers now represent over 10% of its commercial HVAC revenue and are expected to reach approximately 15% in 2025, driven by artificial-intelligence workloads that generate 30-40% more heat per rack than traditional compute

South America Commercial HVAC Equipment Industry Leaders

Midea Group Co., Ltd.

Trane Technologies plc

Johnson Controls International plc

Carrier Global Corporation

Rheem Manufacturing Company, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Daikin Industries commenced manufacturing at its USD 121 million Tijuana plant, shipping 100-200 kW precision HVAC systems to hyperscale data centers across South America

- February 2025: Carrier Global began large-scale production of R-454B commercial units, aiming for an 80% shipment mix during 2025 and implementing a 10-15% price adjustment to cover redesign costs

- January 2025: Carrier Global closed its USD 14.2 billion purchase of Viessmann Climate Solutions, broadening its heat-pump and integrated HVAC offerings for the region

- January 2025: Samsung Electronics completed its USD 1.62 billion acquisition of FläktGroup, integrating European ventilation and data-center cooling portfolios into its Latin American lineup

South America Commercial HVAC Equipment Market Report Scope

The South America commercial HVAC equipment market report is segmented by Equipment Type (Heating Equipment, Cooling Equipment, Ventilation Equipment, Integrated HVAC Systems), Capacity Rating (Below 20 kW, 21-50 kW, 51-200 kW, Above 200 kW), End-user Industry (Hospitality and Leisure, Office and Commercial Buildings, Healthcare Facilities, Data Centres, Education Institutions, Retail and Supermarkets), Installation Type (New-build, and Retrofit), and Geography (Brazil, Argentina, Chile, Colombia, Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

| Heating Equipment |

| Cooling Equipment |

| Ventilation Equipment |

| Integrated HVAC Systems |

| Below 20 kW |

| 21-50 kW |

| 51-200 kW |

| Above 200 kW |

| Hospitality and Leisure |

| Office and Commercial Buildings |

| Healthcare Facilities |

| Data Centres |

| Education Institutions |

| Retail and Supermarkets |

| New-build |

| Retrofit |

| Brazil |

| Argentina |

| Chile |

| Colombia |

| Rest of South America |

| By Equipment Type | Heating Equipment |

| Cooling Equipment | |

| Ventilation Equipment | |

| Integrated HVAC Systems | |

| By Capacity Rating | Below 20 kW |

| 21-50 kW | |

| 51-200 kW | |

| Above 200 kW | |

| By End-user Industry | Hospitality and Leisure |

| Office and Commercial Buildings | |

| Healthcare Facilities | |

| Data Centres | |

| Education Institutions | |

| Retail and Supermarkets | |

| By Installation Type | New-build |

| Retrofit | |

| By Country | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Rest of South America |

Key Questions Answered in the Report

What is the current value of the South America commercial HVAC equipment market?

The market is valued at USD 2.20 billion in 2025.

How fast is demand expected to grow?

Revenue is forecast to rise to USD 3.06 billion by 2030, reflecting a 6.8% CAGR.

Which equipment type leads revenue?

Cooling systems delivered 47.94% of 2024 sales.

Which capacity band is expanding quickest?

Sub-20 kW units are forecast to grow 7.33% a year through 2030.

Why are data centers important for HVAC suppliers?

Hyperscale campuses demand precision cooling and are projected to log a 7.66% CAGR, lifting HVAC revenue streams.

Page last updated on: