Magnesium Alloys Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

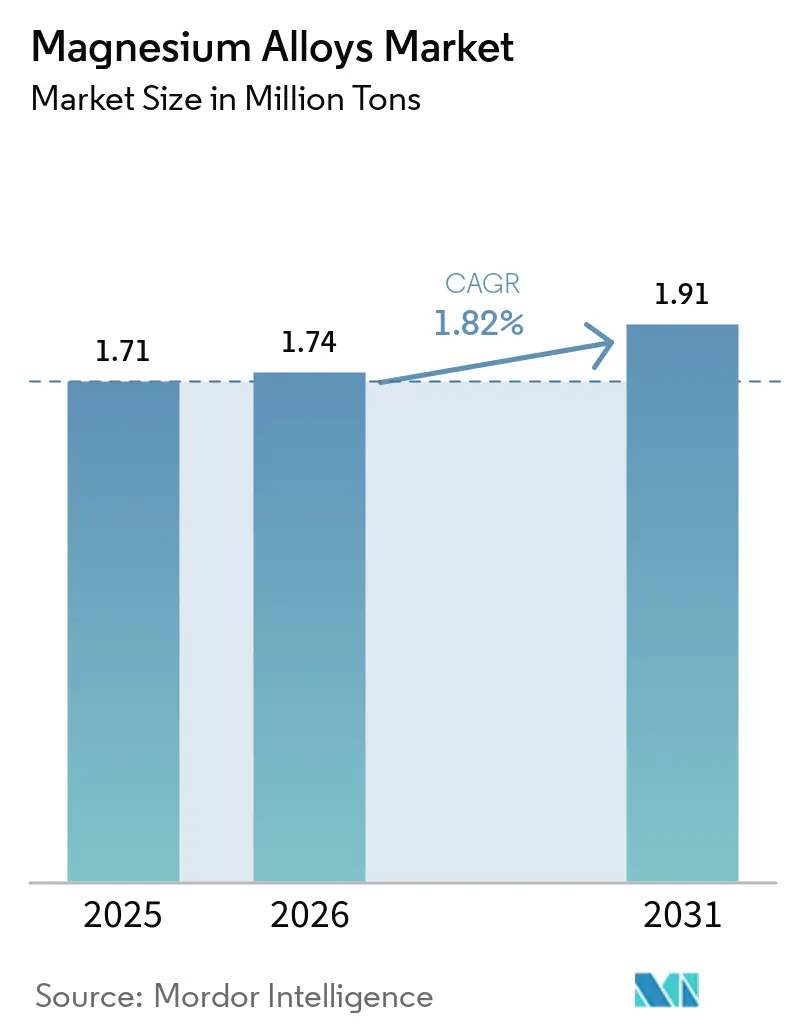

| Market Volume (2026) | 1.74 Million tons |

| Market Volume (2031) | 1.91 Million tons |

| Growth Rate (2026 - 2031) | 1.82% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Magnesium Alloys Market Analysis by Mordor Intelligence

The Magnesium Alloys Market size is expected to grow from 1.71 million tons in 2025 to 1.74 million tons in 2026 and is forecast to reach 1.91 million tons by 2031 at a 1.82% CAGR over 2026-2031. Legacy die-cast power-train uses are plateauing, yet soaring demand for wrought extrusions in electric-vehicle body-in-white structures and for bio-resorbable fixation devices is reshaping growth. Regulatory weight-reduction mandates, tighter EU fleet-average CO₂ ceilings, and multiple 2025 FDA breakthrough-device designations are channeling capital toward magnesium processing lines, additive-manufacturing powders, and closed-loop scrap recycling infrastructure. Automakers are swiftly replacing 6xxx-series aluminum with AZ-series magnesium profiles, achieving a significant reduction in mass. Meanwhile, orthopedic surgeons are adopting WE43 screws and stents, significantly reducing the need for expensive revision surgeries. Coupled with Asia Pacific's dominant share in primary supply and Norway's pioneering scrap-recovery initiative, these dynamics carve out a dual-faceted yet lucrative terrain for the magnesium alloys market.

Key Report Takeaways

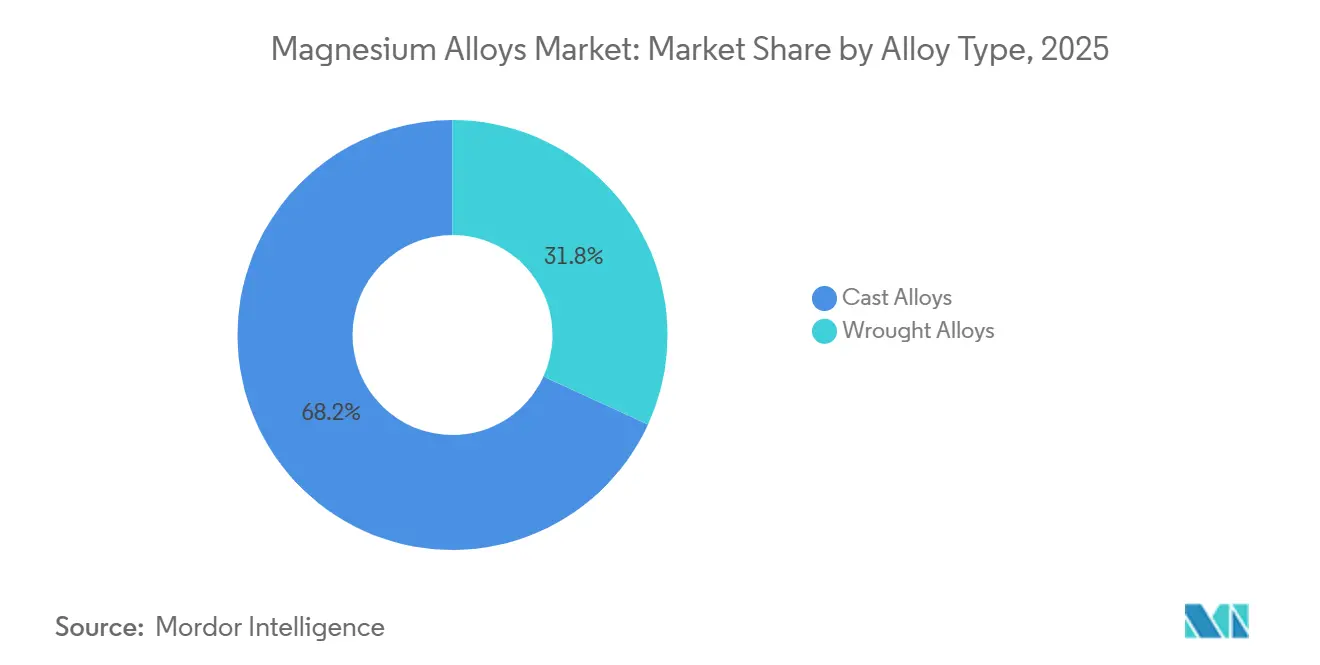

- By alloy type, cast alloys led with 68.17% magnesium alloys market share in 2025, whereas wrought alloys are forecast to register a 6.36% CAGR to 2031.

- By processing technology, die casting accounted for 55.18% of the magnesium alloys market size in 2025; additive-manufacturing feedstock is set to grow the fastest at 6.82% CAGR through 2031.

- By application, chassis and structural components held 38.76% of the 2025 volume, while orthopedic and cardiovascular implants are slated to expand at a 6.61% CAGR up to 2031.

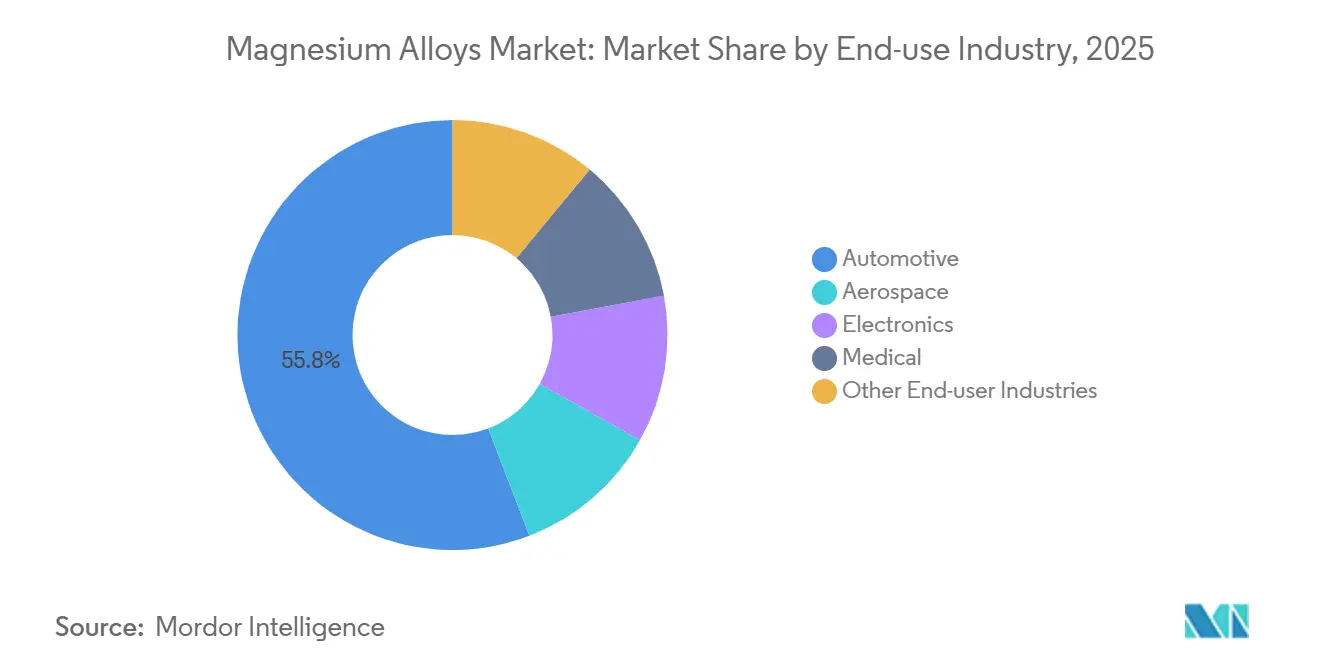

- By end-use industry, automotive captured 55.82% of 2025 shipments, but medical devices are expected to post a 7.22% CAGR over the outlook period.

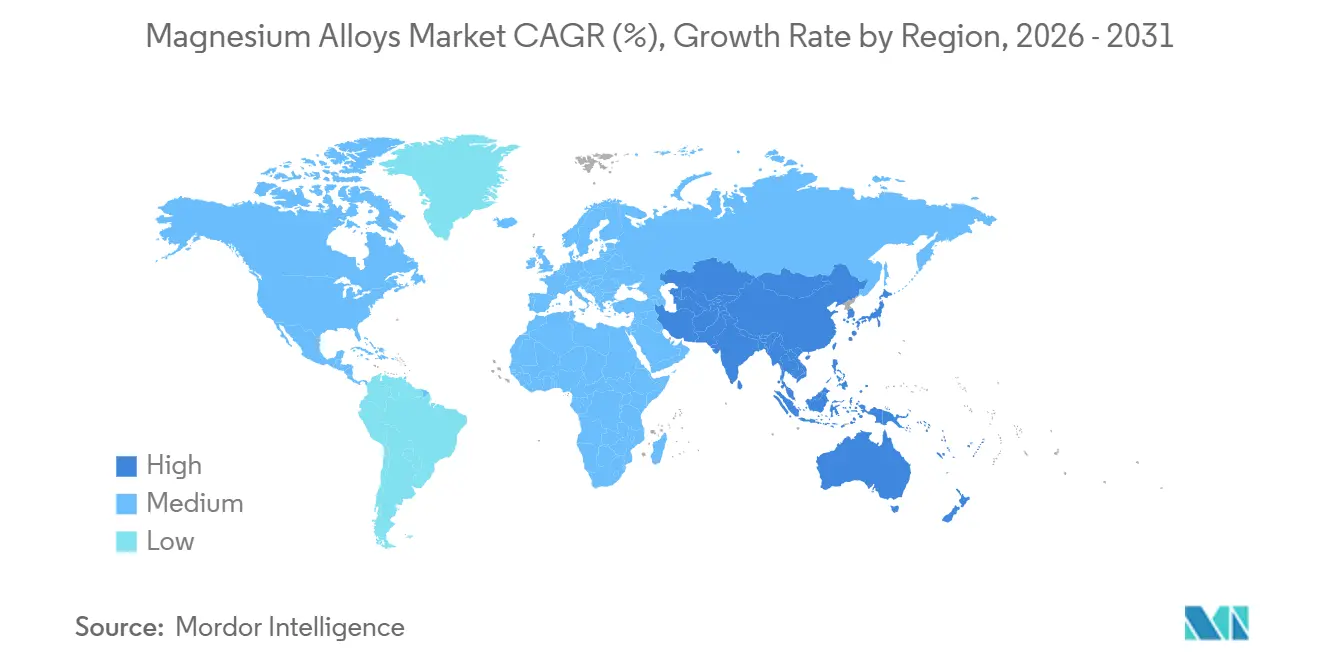

- By geography, Asia Pacific commanded 46.19% of the 2025 volume and is projected to compound at a 6.87% CAGR, the quickest regional clip for the magnesium alloys market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Magnesium Alloys Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory EV lightweighting mandates boost magnesium alloy demand | +0.6% | Global, with strongest uptake in EU and China | Medium term (2-4 years) |

| EU CO₂ fleet-average rules accelerate wrought Mg extrusions adoption | +0.4% | Europe, spillover to UK and Turkey | Short term (≤ 2 years) |

| US FDA clearances spur bio-resorbable Mg orthopedic fixation demand | +0.3% | North America, expanding to EU and Asia Pacific | Long term (≥ 4 years) |

| 5G handset makers shift to Mg–Li casting for EMI shielding | +0.2% | Asia Pacific core, particularly China, South Korea, Taiwan | Short term (≤ 2 years) |

| Closed-loop scrap recycling lowers the effective cost of Mg alloys | +0.3% | Global, early gains in Norway, Germany, Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mandatory EV Lightweighting Mandates Boost Magnesium Alloy Demand

Battery-electric vehicles (BEVs) are heavier than their combustion counterparts, prompting OEMs to reduce structural mass to reclaim lost range. China's 2027 New Energy Vehicle mandate sets a minimum range of 500 km on the CLTC, effectively necessitating a reduction in body-in-white weight[1]MIIT, “New Energy Vehicle Development Plan,” miit.gov.cn. By utilizing magnesium extrusions and mega-cast subframes, which are lighter than aluminum, automakers can achieve these targets without enlarging their batteries. Following ISO 16220 corrosion-testing standards, certification for AZ31B front-end carriers has streamlined qualification timelines. While premium models currently shoulder the cost disparity, advancements in recycling hint at a broader acceptance of magnesium alloys, potentially penetrating deeper into mid-volume segments.

EU CO₂ Fleet-Average Rules Accelerate Wrought Mg Extrusions Adoption

The EU has set a limit for emissions for 2025, which will gradually tighten by 2030. For every gram over the limit, there's a penalty. This has made light-weighting not just an option, but a necessity. Using direct-chill-cast and hot-extruded ZK60 profiles, manufacturers can reduce component mass while still achieving a yield strength of over 200 MPa[2]European Aluminium, “Automotive Manual,” european-aluminium.eu. Magna has launched a new line in Austria, providing magnesium for each Audi PPE chassis. Coatings free from hexavalent chromium and certified under ISO 10074 not only alleviate REACH pressures but also expedite supplier onboarding, bolstering the growth outlook for the magnesium alloys market.

US FDA Clearances Spur Bio-Resorbable Mg Orthopedic Fixation Demand

Magnesium implants have received the FDA's breakthrough-device status, and a trial reported a high union rate, bolstering clinical confidence. WE43 screws, which oxidize within a specific timeframe, help avoid revision-surgery costs. With expanding indications—from treating distal-radius fractures to being used in spinal cages—the market for magnesium alloys in medical devices is projected to grow steadily.

5G Handset Makers Shift to Mg–Li Casting for EMI Shielding

Millimeter-wave 5G demands high shielding. Samsung's Galaxy S25 Ultra features LA141 mid-frames, reducing thickness and enhancing thermal dissipation. Due to air-freight restrictions on Li-rich alloys, OEMs are testing the safer LA43 grades. These grades provide effective protection, leading to a broader adoption of magnesium alloys in APAC's handset supply chains.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Galvanic and pitting corrosion challenges in humid environments | -0.4% | Global, acute in coastal regions and tropical climates | Medium term (2-4 years) |

| Welding brittleness versus Al and Ti alloys | -0.2% | Global, particularly impacting structural automotive applications | Long term (≥ 4 years) |

| High-strength 6xxx Al extrusions displace Mg for crash-relevant parts | -0.3% | North America and Europe, where IIHS and Euro NCAP standards dominate | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Galvanic and Pitting Corrosion Challenges in Humid Environments

Magnesium's -2.37 V potential renders it highly anodic. Consequently, when salt-laden moisture connects joints of dissimilar metals, pits develop over time. While plasma-electrolytic oxidation can prolong the salt-spray life, it comes with a significant capital expenditure. Although rare-earth alloying offers some benefits, its susceptibility to price fluctuations poses challenges. As a result, corrosion remains the primary hurdle preventing the broader adoption of magnesium alloys in mainstream vehicles.

Welding Brittleness Versus Al and Ti Alloys

Due to the restricted slip systems in the HCP crystal structure, fusion welds produce the brittle Mg17Al12, resulting in a reduction in tensile elongation. While friction-stir welding boosts joint efficiency, it comes at the cost of significant cBN tool wear. As a result, automakers are leaning towards adhesive bonding or returning to aluminum, which tempers the immediate momentum of magnesium alloys in fully welded structures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Alloy Type: Wrought Gains Ground Despite Cast Dominance

Cast alloys supplied 68.17% of shipments in 2025, reflecting their die-casting efficiency for intricate housings. Nonetheless, wrought grades are sprinting ahead at 6.36% CAGR. BMW’s Neue Klasse platform will embed 22 kg of extruded AZ31B and ZK60 per car, sharpening the weight-saving edge essential to lithium-ion range optimization. Beyond cars, helicopter gearbox housings and UAV frames now specify ZK60A extrusions for vibration damping, underscoring broader diversification of the magnesium alloys market. Electronics still favor die-cast LA141 shells for 5G handsets, yet the design window is widening as additive-manufacturing powders enable lattice-filled implants that deliver biomechanical compatibility unmatchable by titanium.

In 2025, patented rare-earth-free wrought compositions emerged, addressing supply concerns and reducing material costs. While niche, the demand for gas-atomized WE43 powders in additive manufacturing enhances profitability and fuels research and development. Regulatory subsidies for recycling feedstock have led to an uptick in re-melting cast scrap into wrought billets. This not only shortens supply loops but also bolsters the sustainability credentials of the magnesium alloys market.

By Processing Technology: Die Casting Leads, Additive Manufacturing Surges

Die casting still commands 55.18% of throughput thanks to 45-90 s cycles and million-shot tooling life. Chinese OEMs are set to trial single-piece magnesium rear underbodies starting in 2027, having placed orders for large presses. Meanwhile, Magna's new line in Austria, catering to Audi's PPE, bolsters extrusions' market share. Additionally, advancements in press lubricants now facilitate the use of long AZ31 profiles.

Additive manufacturing grows at a 6.82% CAGR. EOS M290, utilizing WE43, achieves high density and yield strength directly from the powder bed, making it suitable for load-bearing ankle plates. Safety codes under ATEX 2014/34/EU have spurred investment in inert-gas print farms across Germany and Texas. Forging and powder metallurgy remain niche but benefit from demand in helicopter rotor hubs and lightweight bicycle cranks, keeping the magnesium alloys market diversified across processes.

By Application: Medical Implants Outpace Automotive Structures

In 2025, automotive chassis and structural components captured 38.76% share of application volume, underscoring automakers' emphasis on front-end modules, seat frames, and instrument-panel beams. Here, magnesium die castings and extrusions offer substantial weight savings compared to aluminum and steel. General Motors' Ultium electric platform, which supports the Cadillac Lyriq and GMC Hummer EV, integrates magnesium die castings in the battery-tray structure, achieving a notable mass reduction over an all-aluminum design. Powertrain and drivetrain components, including transmission cases, oil pans, and clutch housings, represented a considerable portion of the volume. However, this segment is under pressure as the rise of battery-electric vehicles phases out multi-speed transmissions. Interior and exterior automotive parts, like steering-wheel cores and liftgate inner panels, claimed a share, limited by surface-finish demands that require extra painting or chrome plating.

Orthopedic and cardiovascular implants are projected to grow at 6.61% through 2031, marking them as the fastest-growing application segment. Surgeons are increasingly turning to bioresorbable magnesium screws, plates, and stents, which not only eliminate the need for revision surgeries but also cut patient recovery times. Syntellix's MAGNEZIX compression screws, which received FDA clearance in October 2024, achieved significant sales within their first year, gaining traction in the US distal radius fracture market. Electronic device housings, covering smartphones, laptops, and wearables, accounted for a notable portion of application volume. This surge is largely attributed to 5G handset manufacturers pivoting to magnesium-lithium die castings for enhanced EMI shielding and thermal management. Apple's refreshed MacBook Pro 16-inch in October 2025, while retaining its aluminum unibody, introduced a die-cast magnesium AZ91D internal chassis, trimming the device's weight. Aerospace applications, from helicopter gearbox housings to satellite components, made up a smaller portion of the volume but command premium prices due to rigorous AS9100 and NADCAP certification standards.

By End-Use Industry: Medical Devices Lead Growth Trajectory

In 2025, the automotive and transportation sectors led the way, accounting for 55.82% of the volume. This shift was largely driven by lightweighting mandates and the rise of electric vehicles, leading to a move away from traditional steel and aluminum in favor of newer materials for non-structural and semi-structural components. Yet, the medical devices sector is outpacing all others at 7.22% CAGR through 2031. This surge is fueled by clinical findings highlighting magnesium's elastic modulus, which aligns more closely with cortical bone than titanium's. This alignment reduces stress-shielding and accelerates osseointegration. Biotronik's Magmaris coronary scaffold, which earned the FDA's breakthrough-device nod in February 2025, boasts a 12-month resorption period and a lower target-lesion failure rate compared to permanent drug-eluting stents. In 2025, the US orthopedic implant market utilized magnesium alloys, primarily in trauma fixation screws, plates, and intramedullary nails. By 2031, this penetration is projected to capture a significant share of the trauma-fixation market.

Electronics accounted for a notable portion of the end-use volume in 2025. This was driven by the demand for smartphone and laptop housings, which necessitate electromagnetic shielding and thermal conductivity. Xiaomi's Mi 15 Pro, unveiled in December 2025, featured a die-cast LA43 magnesium-lithium mid-frame. This innovation not only boosted 5G signal strength but also lowered the device's operating temperature compared to its aluminum counterpart. The aerospace sector claimed a smaller share of the volume, focusing on helicopter transmission housings and UAV airframes. Here, magnesium's specific stiffness outperformed aluminum. This advantage translates to a range extension for battery-powered drones. Other industries, spanning power tools, sporting goods, and industrial machinery, held a combined share. Notably, cordless power-tool giants like Makita and DeWalt have embraced magnesium die-cast housings. This shift has led to a reduction in tool mass, significantly enhancing ergonomics and diminishing operator fatigue during prolonged use. While ISO 9001 quality management certification is ubiquitous across all sectors, medical device producers also prioritize ISO 13485 compliance to meet regulatory standards.

Geography Analysis

Asia Pacific retains 46.19% of 2025 shipments and posts the fastest 6.87% CAGR through 2031. In 2025, China's Baowu bolstered its dominance by bringing new capacity online and cementing its primary market share. Meanwhile, BYD's Seal sedan is already integrating magnesium components. In a notable collaboration, Japan's Toyota and Panasonic are co-developing magnesium-lithium battery enclosures, hinting at a future cross-industry synergy. South Korea's leading handset manufacturers secured LA alloys in 2025, effectively bridging the supply-demand gap in the magnesium alloys market.

North America's market share is largely driven by industry giants Ford and GM, alongside the growing medical adoption of WE43 screws. US Magnesium's Great Salt Lake facility acts as a buffer for OEMs against geopolitical uncertainties. Highlighting the medical sector's momentum, Syntellix captured a share of the distal-radius fixation market just a year post-FDA approval. In Canada, Bombardier and CAE are utilizing extruded ZK60 for their simulation rigs, while in Mexico, Guanajuato die-casters are embedding magnesium into Q5 e-tron carriers.

Europe is navigating stringent CO₂ regulations. In 2025, Germany, bolstered by recycling initiatives from Magna and Hydro that cut carbon footprints, consumed a notable amount of magnesium. The EU's mandate for recycled content is steering OEMs towards secondary feedstock contracts, reinforcing the region's commitment to circularity in the magnesium alloys market.

While South America and the Middle East and Africa may be smaller players, they are making significant strides. Brazil's INMETRO has harmonized local standards with ISO 16220, paving the way for domestic suppliers to cater to OEMs. In a forward-looking move, Saudi Arabia is set to unveil a Jubail smelter by 2028, adding new primary capacity to the market.

Competitive Landscape

The magnesium alloy market remains moderately fragmented. Chinese state-owned enterprises (SOEs) offer prices lower than their Western counterparts, yet they grapple with challenges in delivering premium-quality products. Meanwhile, specialty powder suppliers are ramping up their atomizer production, targeting a lucrative additive-manufacturing market. Process-control innovations are sharpening competitive advantages: MAGONTEC’s inline X-ray CT technology has reduced scrap rates, while Dynacast’s plasma-electrolytic oxidation line has successfully halved lead times for coated components. Patent filings have surged, with a notable share owned by industry giants, highlighting a trend of escalating innovation. However, the competition between high-strength aluminum and carbon composites for the same lightweighting budgets is constraining pricing power in the market.

Magnesium Alloys Industry Leaders

Meridian Lightweight Technologies

Dynacast

Norsk Hydro ASA

Baowu Magnesium Technology Co., Ltd.

Luxfer MEL Technologies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Russian scientists developed a new processing method for magnesium alloys, allowing implants to maintain their desired shape for a longer duration and dissolve uniformly within the body. During their research, the scientists identified a heat treatment process for a sample 3D-printed using WE43 magnesium alloy powder, which enabled the implant to dissolve up to 1.5 times more slowly.

- March 2025: Great Wall Motor and Baowu Magnesium formed a joint laboratory focused on lightweight magnesium components for new-energy vehicles.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the magnesium alloy market as all commercially produced cast and wrought grades that contain at least eighty-five percent magnesium by weight and are sold for structural or functional use across automotive, aerospace, electronics, medical, and general engineering channels. Output that moves through captive foundries or tier-one die casters is tracked because it eventually reaches the same end markets through integrated supply chains.

Scope exclusion: Recycled magnesium scrap traded without re-alloying and specialty magnesium compounds are outside this assessment.

Segmentation Overview

- By Alloy Type

- Cast Alloys

- Wrought Alloys

- By Processing Technology

- Die Casting

- Extrusion

- Forging

- Powder Metallurgy

- Additive Manufacturing Feedstock

- By Application

- Chassis and Structural Components

- Powertrain and Drivetrain Components

- Interior and Exterior Automotive Parts

- Electronic Device Housings

- Orthopedic and Cardiovascular Implants

- Others

- By End-use Industry

- Automotive

- Aerospace

- Electronics

- Medical

- Other End-user Industries

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Structured interviews with Asian smelter managers, European high-pressure die casting engineers, North American orthopedic implant designers, and logistics intermediaries allow us to vet secondary numbers, fine-tune utilization rates, and sense check regional price spreads before model lock-in.

Desk Research

Our analysts start with public Tier-1 references such as USGS mineral statistics, International Magnesium Association shipment reports, UN Comtrade customs codes, OECD vehicle build data, Eurostat metallurgy dashboards, and peer-reviewed journals that track corrosion and welding advances. Company filings, investor decks, and trade press add color on capacity additions, while D&B Hoovers and Dow Jones Factiva supply financial and deal intelligence for major smelters. The sources listed illustrate the range we consult and are not exhaustive.

Market-Sizing & Forecasting

The model begins with a top-down production to demand reconcile that layers national smelter output, net trade flows, and alloying capture rates. Results are cross-checked through selective bottom-up tests such as sampled average selling price times volume for die castings and extrusion billet roll-ups. Key variables include passenger vehicle build counts, average magnesium per vehicle, wide-body airframe deliveries, smartphone metal housing penetration, and benchmark alloy prices. Multivariate regression, supplemented by scenario analysis for electric vehicle penetration, generates the five-year forecast and flags high-impact drivers. Data gaps in smaller regions are bridged with weighted proxies drawn from neighboring market behavior and validated by local experts.

Data Validation & Update Cycle

Outputs pass a two-step analyst review that screens anomalies against independent price and trade series. A final sign-off occurs once year-on-year deltas fall within predetermined tolerance bands. Our reports refresh annually, and mid-cycle updates are issued when material supply shocks, regulation, or technology shifts occur.

Why Mordor's Magnesium Alloys Baseline Earns Trust

Published estimates often diverge because firms choose different product scopes, unit conventions, and refresh cadences.

Key gap drivers in our space include whether captive die-cast volumes are counted, how quickly smelter restarts are reflected, and if wrought products such as extrusion billets are folded into totals. Mordor incorporates all three, applies country-level trade reconciliations, and updates models every twelve months, which is where other publishers tend to lag.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 1.65 million tons (2025) | Mordor Intelligence | - |

| USD 2.01 billion (2024) | Global Consultancy A | Omits captive consumption in Asian auto-casting clusters |

| USD 2.37 billion (2023) | Trade Journal B | Excludes wrought products and aftermarket alloys |

| USD 3.12 billion (2019) | Industry Association C | Uses older base year and price uplift multipliers without regional granularity |

Taken together, the comparison shows that Mordor Intelligence delivers a balanced, transparent baseline whose traceable variables and repeatable steps let decision makers anchor strategy with confidence.

Key Questions Answered in the Report

How great will global demand for magnesium alloys be by 2031?

Shipments are forecast to reach 1.91 million tons by 2031, up from 1.74 million tons in 2026 at a 1.82% CAGR.

Which segment is projected to add volume fastest?

Wrought alloys are set to expand at a 6.36% CAGR through 2031 as automakers integrate them into electric-vehicle structures.

Why are magnesium implants gaining popularity in orthopedics?

FDA-cleared WE43 screws resorb within 18 months, eliminating revision surgeries and raising union rates to 94%.

What makes the Asia Pacific dominant in supply?

In 2025, China solidified its regional leadership by commissioning a new facility, further asserting its dominance over primary output.

Which restraint most limits automotive structural use?

Galvanic corrosion in humid coastal regions necessitates costly coatings, tempering broader adoption in high-volume vehicles.

Page last updated on: