Magnesium Oxide Nanopowder Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

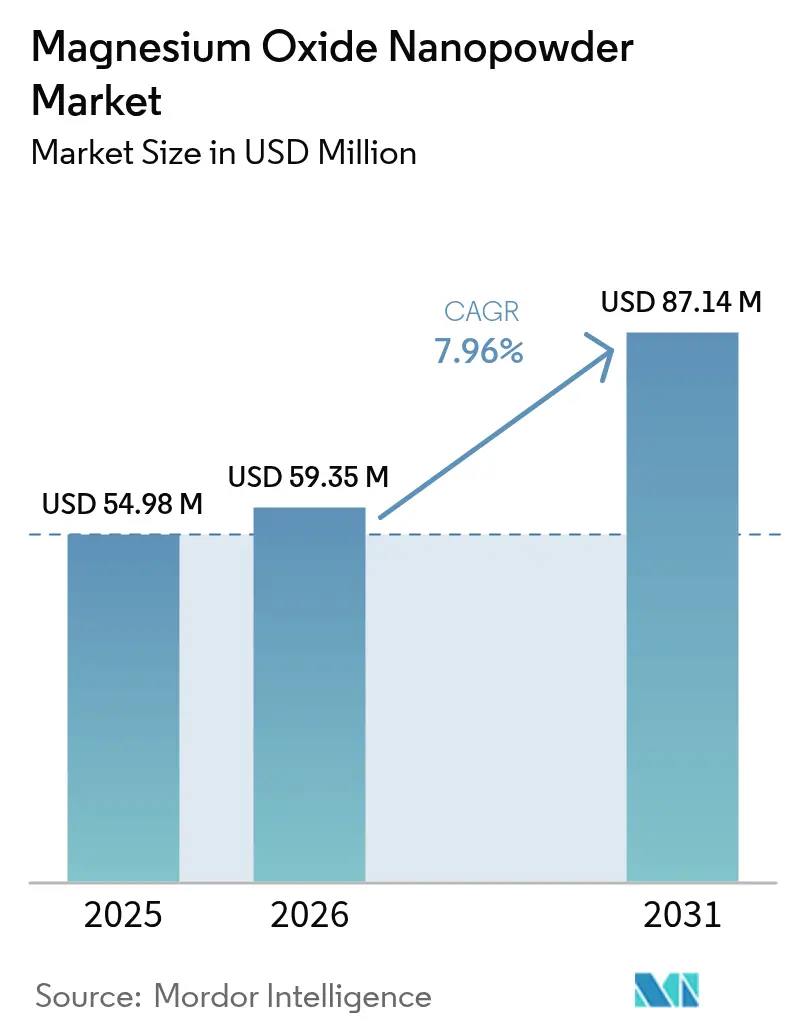

| Market Size (2026) | USD 59.35 Million |

| Market Size (2031) | USD 87.14 Million |

| Growth Rate (2026 - 2031) | 7.96% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Magnesium Oxide Nanopowder Market Analysis by Mordor Intelligence

The Magnesium Oxide Nanopowder Market size was valued at USD 54.98 million in 2025 and estimated to grow from USD 59.35 million in 2026 to reach USD 87.14 million by 2031, at a CAGR of 7.96% during the forecast period (2026-2031). Most revenue still flows from legacy refractory demand, yet momentum is clearly shifting toward high-value applications in fuel additives, electrical insulation, flame-retardant polymer compounds and early solid-state battery prototypes. Supply security is shaped by China’s 52% share of primary magnesium production in 2024, which delivers cost advantages for Asian processors but exposes global buyers to policy-driven volatility. Competitive positioning increasingly depends on proprietary synthesis routes that deliver narrow particle-size distributions and functionalized surfaces needed in advanced composites and electrolytes. Finally, tightening workplace-exposure limits for engineered nanomaterials in North America and the EU are raising compliance costs, but they also favour established producers with certified quality systems.

Key Report Takeaways

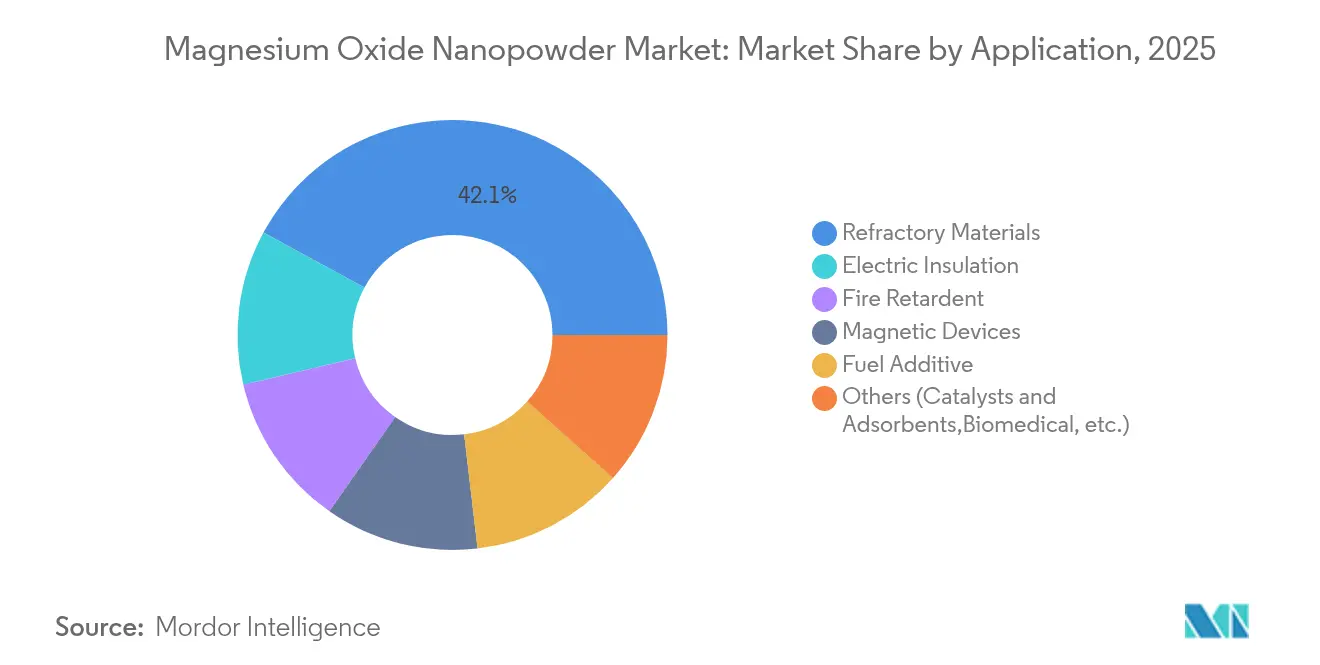

- By application, refractory materials led with 42.10% revenue share in 2025; fuel additives are forecast to expand at an 8.63% CAGR to 2031.

- By synthesis method, physical methods held 41.75% of the magnesium oxide nanopowder market size in 2025; chemical precipitation techniques are advancing at a 8.78% CAGR to 2031.

- By end-user industry, metallurgy accounted for 36.35% of the magnesium oxide nanopowder market share in 2025, while other end-user industries are projected to post the highest CAGR at 8.25% through 2031.

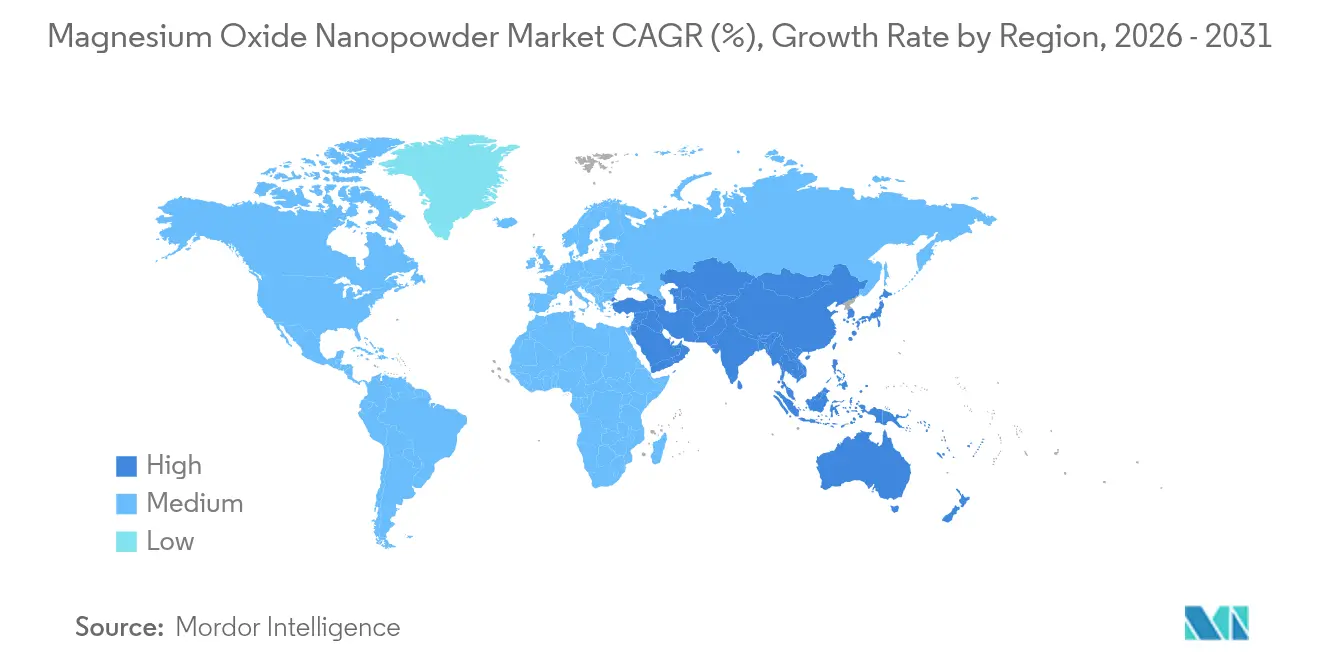

- By geography, Asia-Pacific commanded 51.72% share of the magnesium oxide nanopowder market size in 2025 and remains the fastest-growing region with an 8.55% CAGR forecast to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Magnesium Oxide Nanopowder Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand from refractory industry | +1.8% | Global, concentrated in Asia-Pacific steel hubs | Medium term (2-4 years) |

| Growth in electrical insulation applications | +1.5% | North America and EU electronics manufacturing, APAC expansion | Long term (≥4 years) |

| Increasing use as fuel additive | +1.2% | Global automotive markets, early adoption in Asia-Pacific | Short term (≤2 years) |

| Expanding adoption in flame-retardant polymer composites | +1.0% | North America and EU construction, automotive safety regulations | Medium term (2-4 years) |

| Emergent role in solid-state battery electrolytes | +0.8% | Asia-Pacific battery manufacturing, spill-over to North America | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Demand from Refractory Industry

Magnesia-carbon bricks incorporating nanoscale magnesium oxide show higher densification that lowers porosity-induced failure in basic oxygen and electric arc furnaces. Steelmakers in China, Japan and South Korea have standardised nanopowder grades in ladle, tundish and continuous-caster linings to withstand rapid thermal cycling. Consolidation among integrated steel producers means fewer buyers wield greater purchasing power, but they pay premiums for reliability that avoids unplanned shutdowns. As electric arc furnace capacity expands across Asia-Pacific, magnesium oxide nanopowder market demand remains closely correlated with rising scrap-based steel output. Suppliers with vertically integrated production and refractory formulation expertise can capture long-term contracts anchored in joint R&D agreements.

Growth in Electrical Insulation Applications

Epoxy systems loaded with 1 wt% magnesium oxide nanoparticles maintain a dielectric constant of 13 at 230 °C and double the thermal conductivity versus neat resin. These attributes solve the chronic trade-off between heat dissipation and electrical resistivity in silicon carbide power modules and traction inverters. Electric-vehicle drive-train voltages above 800 V, combined with miniaturised form factors, amplify the need for high-temperature insulation fillers that stay chemically inert under partial discharge. Asia-Pacific cable makers are scaling polyethylene compounds filled with freeze-dried magnesium oxide foams that suppress space-charge accumulation. As wind-turbine inverters grow in capacity, European utilities are also specifying nanoparticle-filled potting compounds for offshore substations.

Increasing Use as Fuel Additive

Diesel blends doped with magnesium oxide nanoparticles cut unburned hydrocarbons and reduce particulate matter without adding heavy-metal residues[1]ScienceDirect, “Nanomagnesia as Diesel Additive,” sciencedirect.com. Engine-bench trials show viscosity reductions that improve injector spray patterns and raise brake-thermal efficiency. Euro 7 emissions rules set for 2027 create a regulatory push in the EU, mirrored by China VII standards, both favouring combustion-improvement additives. Commercial-scale trials in India demonstrate dosing concentrations below 20 ppm, which keeps additive cost per litre within automaker targets. This window of opportunity supports differential pricing that offsets the premium cost of high-purity powders.

Expanding Adoption in Flame-Retardant Polymer Composites

Polypropylene loaded with 30 wt% magnesium hydroxide nanoparticles reached a 29.3% limiting-oxygen index, passing UL-94 V-0 without halogenated additives. Construction panels and automotive interior trims use these mineral additives to comply with EU Construction Products Regulation fire-classification standards. Magnesium oxide’s high specific-heat capacity absorbs significant energy during endothermic decomposition, while released water vapour dilutes flame-zone oxygen. Unlike aluminium trihydrate, magnesium-based systems maintain mechanical strength at elevated temperatures, which suits electric-vehicle battery casings that face stringent fire-penetration tests. North American property insurers have started offering premium discounts for buildings specified with halogen-free flame-retardant composites.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production and purification costs | -2.1% | Global, particularly affecting North America and EU manufacturers | Short term (≤2 years) |

| Aggregation and agglomeration issues | -1.4% | Global manufacturing, critical for Asia-Pacific volume production | Medium term (2-4 years) |

| Tightening workplace exposure regulations for nanoparticles | -1.0% | North America and EU regulatory frameworks, expanding globally | Long term (≥4 years) |

| Volatile magnesium feedstock supply | -0.8% | Global supply chains, concentrated risk from China dependency | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

High Production and Purification Costs

Sol-gel plants capable of 1,425 kg day⁻¹ output require capital spending above USD 45,000 and return on investment stretches beyond three years under today’s price structure. Energy-intensive hydrothermal and calcination steps heighten sensitivity to carbon-pricing trajectories in the EU and selected US states. Purity specifications tighter than 99.8 wt% raise reagent and filtration costs that cannot be amortised across commodity volumes. Smaller producers outside Asia-Pacific face scale disadvantages, which limits their ability to bid for large refractory tenders or automotive additive supply contracts.

Aggregation and Agglomeration Issues

Magnesium oxide nanoparticles carry high surface energies that drive agglomeration, eroding dispersion quality in polymer matrices and fluid suspensions. Chemical surfactants alleviate clustering but introduce impurities disallowed in battery electrolytes or biomedical products. Low-temperature freeze-drying yields porous lattices that re-disperse more readily, yet the extra processing adds cost and lengthens lead times. End-users often require tailor-made surface treatments, creating inventory fragmentation and complex quality-assurance regimes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Refractory Materials Lead While Fuel Additives Accelerate

Refractory materials generated 42.10% of the magnesium oxide nanopowder market size in 2025, anchored in magnesia-carbon bricks and tundish linings for steel and aluminium melt processing. Technical upgrades in electric arc furnaces favour finer particle distributions that densify brick microstructures. As scrap-based steel makes deeper inroads across Asia, energy-efficient linings remain critical for productivity. Market leadership is expected to persist through 2030, though its proportional share will slip as newer uses scale.

The fuel-additive category shows an 8.63% CAGR to 2031, reflecting unprecedented regulatory pressure to cut particulate and NOx emissions in both on-road and off-road fleets. Nanoparticle dispersions improve atomisation, raise flame temperature uniformity and reduce soot precursors without compromising engine hardware warranties. Pilot fleet tests in the EU and China report fuel-economy gains above 2%. Although the segment starts from a small baseline, its growth pace makes it a focal point for producers targeting automotive clients seeking drop-in solutions.

By Synthesis Method: Chemical Precipitation Gains on Physical Methods

Physical routes such as flame spray pyrolysis and vacuum vapour deposition held 41.75% of 2025 revenue, benefiting from amortised equipment and throughput suited to refractory grades. The downside remains broad particle-size ranges that do not meet premium electronics or biomedical specs. Producers with legacy physical assets face upgrade decisions as demand migrates upslope on the value chain.

Chemical precipitation displays a 8.78% CAGR to 2031, supported by superior control over stoichiometry, morphology and surface hydroxyl concentration. Closed-loop reactors coupled with inline particle-size analysers now run continuous-flow regimes that improve yield and cut solvent loss. Life-cycle assessments show lower greenhouse-gas intensity when using renewable electricity, which aligns with buyer procurement policies targeting net-zero supply chains. Green or bio-based synthesis is emerging from lab to pilot scale, though unit cost remains higher and capacity limited.

By End-User Industry: Metallurgy Dominance Faces Diversification Pressure

Metallurgy accounted for 36.35% of the magnesium oxide nanopowder market share in 2025 as integrated mills continue to absorb the bulk of refractory-grade demand. Knowledge transfer between suppliers and mill research centres helps sustain higher absorption rates compared with other sectors. Yet the share is projected to decline gradually as downstream diversification accelerates.

Other end-user industries, a bucket that includes chemicals, healthcare and energy storage, will expand at an 8.25% CAGR between 2026 and 2031. Biocompatible coatings, antimicrobial textiles and photothermal cancer therapies are early-stage but attract venture funding and academic collaboration. In grid-scale batteries, magnesium oxide serves as a sintering aid in solid electrolytes, dovetailing with renewable-integration policies in China and the United States. Such breadth enables suppliers to spread risk beyond cyclic metals demand cycles.

Geography Analysis

Asia-Pacific owned 51.72% of 2025 revenue in the magnesium oxide nanopowder market and is forecast to advance at an 8.55% CAGR through 2031, underpinned by integrated supply chains, cost-advantaged feedstock and dense clusters of steel, electronics and battery manufacturers. China anchors regional demand, yet Japan’s ceramics expertise and South Korea’s semiconductor ecosystem provide incremental pull for ultra-high-purity grades. Government stimulus aimed at energy-transition hardware drives additional volume in electric-vehicle thermal management and solid-state battery pilot lines.

North America is a smaller but technologically rich arena in which aerospace, defence and advanced power electronics consume high-spec powders. The United States requisitioned domestic supply security measures, and start-ups such as Magrathea are piloting carbon-neutral magnesium extraction from seawater, which could de-risk feedstock procurement and reinforce local value chains by the late 2020s. Canada’s critical-minerals strategy includes grants that lower capital hurdles for nanopowder finishing lines, potentially repositioning the region as an exporter of specialty grades rather than an importer.

Europe maintains steady growth as building codes tighten flame-retardancy thresholds and automakers adopt magnesium-rich e-mobility components. Germany leads consumption due to its automotive and chemical base, whereas the United Kingdom taps aerospace and defence projects requiring high-temperature insulation. EU circular-economy regulations encourage mineral-based fire-retardant fillers over halogenated alternatives, offering regulatory tailwinds for magnesium oxide nanopowder market expansion. The bloc’s energy-strategy directives also channel funds into solid-state battery consortia where MgO plays a critical interface role.

Competitive Landscape

Competitive intensity is moderate because high-purity nanomaterial production requires specialised reactors, controlled atmospheres and robust quality-assurance frameworks that act as entry barriers. American Elements, Nanoshel, and Hongwu International anchor the premium tier, leveraging vertical integration from feedstock to custom dispersions. Mid-tier players in China supply refractory and fuel-additive grades at scale, and some are moving up the value chain by licensing precipitation patents from academic institutes.

Technology leadership rests on process know-how that narrows particle-size distribution below 30 nm with tight control over agglomeration. Producers have introduced surface-functionalised powders bearing silane or phosphate groups that boost compatibility with polymer matrices, opening lucrative channels in electric-vehicle battery casings. Intellectual-property data show a rising share of filings linked to green synthesis, continuous processing and MgO-coated battery anodes, signalling strategic pivots toward energy-storage end-markets.

Collaborative models are strengthening as end-users invest in joint pilot lines to co-engineer formulations. A Japanese semiconductor maker recently signed a multi-year supply and development agreement with a US nanopowder firm focused on ultra-low-chloride MgO for GaN power devices. Similar alliances in Europe pair magnet producers with nanopowder suppliers to refine MgO intermediates for sintered Nd-Fe-B magnets, capitalising on the region’s re-shoring of permanent-magnet supply.

Magnesium Oxide Nanopowder Industry Leaders

Merck KGaA

US Research Nanomaterials

American Elements

Sigma-Aldrich (MilliporeSigma)

SkySpring Nanomaterials

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: The US Environmental Protection Agency has updated its 40 CFR 721 regulations. These changes introduce new significant-use restrictions and require the use of respirators when handling magnesium oxide nanopowder.

- February 2024: University of Texas at Austin has published new safety guidelines for working with nanomaterials. These updates focus on safe handling of magnesium oxide nanopowder and proper monitoring of exposure risks.

Global Magnesium Oxide Nanopowder Market Report Scope

The global magnesium oxide nanopowder market report includes:

| Refractory Materials |

| Electric Insulation |

| Fuel Additive |

| Fire Retardent |

| Magnetic Devices |

| Others (Catalysts & Adsorbents,Biomedical, etc.) |

| Physical Methods |

| Chemical Precipitation |

| Green/Bio-based Synthesis |

| Metallurgy |

| Construction |

| Oil & Gas |

| Automotive |

| Electrical & Electronics |

| Other End-user Industries (Chemical & Petrochemical,Healthcare & Pharmaceuticals, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Application | Refractory Materials | |

| Electric Insulation | ||

| Fuel Additive | ||

| Fire Retardent | ||

| Magnetic Devices | ||

| Others (Catalysts & Adsorbents,Biomedical, etc.) | ||

| By Synthesis Method | Physical Methods | |

| Chemical Precipitation | ||

| Green/Bio-based Synthesis | ||

| By End-user Industry | Metallurgy | |

| Construction | ||

| Oil & Gas | ||

| Automotive | ||

| Electrical & Electronics | ||

| Other End-user Industries (Chemical & Petrochemical,Healthcare & Pharmaceuticals, etc.) | ||

| By Geography (Value) | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What factors drive the rapid growth of the magnesium oxide nanopowder market?

Stringent emissions rules, rising demand for halogen-free flame-retardant polymers, and progress in solid-state batteries are pushing the market toward an 7.96% CAGR through 2031.

How large is the magnesium oxide nanopowder market today?

The market size is USD 59.35 million in 2026 and is expected to climb to USD 87.14 million by 2031.

Which application segment is growing the fastest?

Fuel additives exhibit the highest growth rate at 8.63% CAGR owing to vehicle-emissions legislation that favors combustion-efficiency enhancers.

Why does Asia-Pacific dominate the market?

The region combines abundant magnesium feedstock, integrated electronics and automotive manufacturing hubs, and strong policy support for new-energy technologies, resulting in 51.72% revenue share in 2025.

What challenges could slow market expansion?

High production costs, nanoparticle agglomeration, stricter workplace-safety regulations and dependence on Chinese magnesium feedstock weigh on growth potential even as demand rises globally.

Page last updated on: