Macular Degeneration Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 18.21 Billion |

| Market Size (2031) | USD 27.32 Billion |

| Growth Rate (2026 - 2031) | 8.45% CAGR |

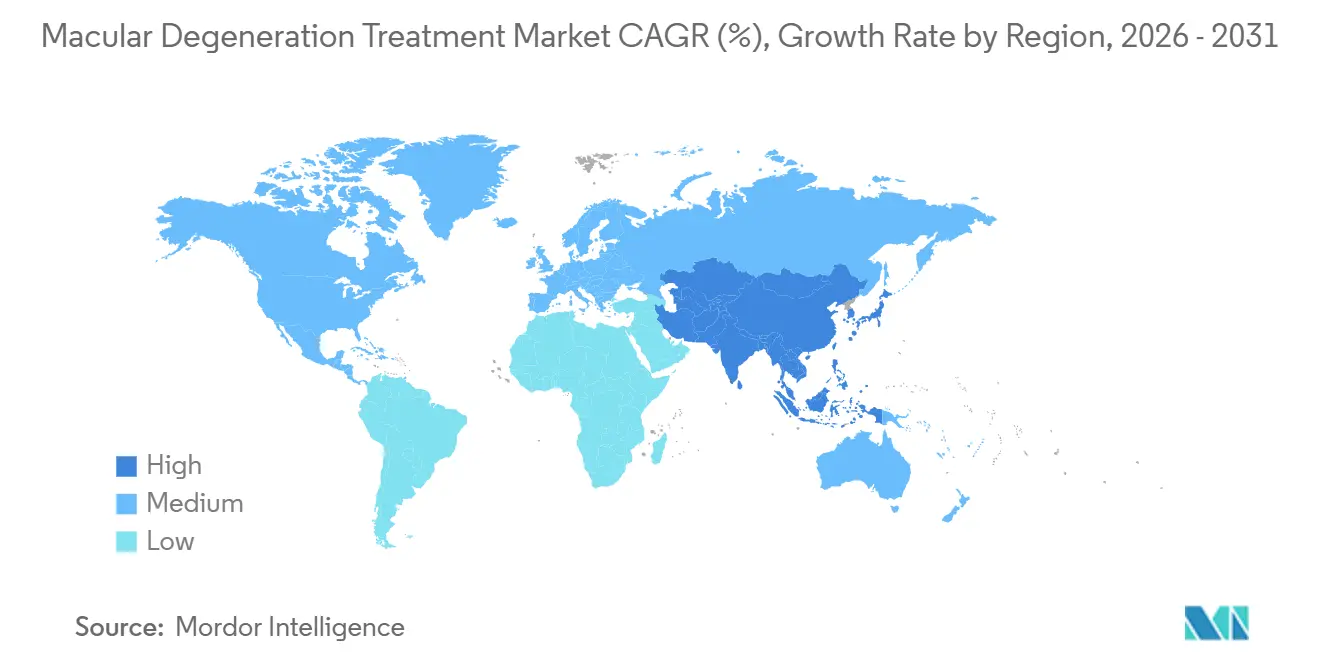

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

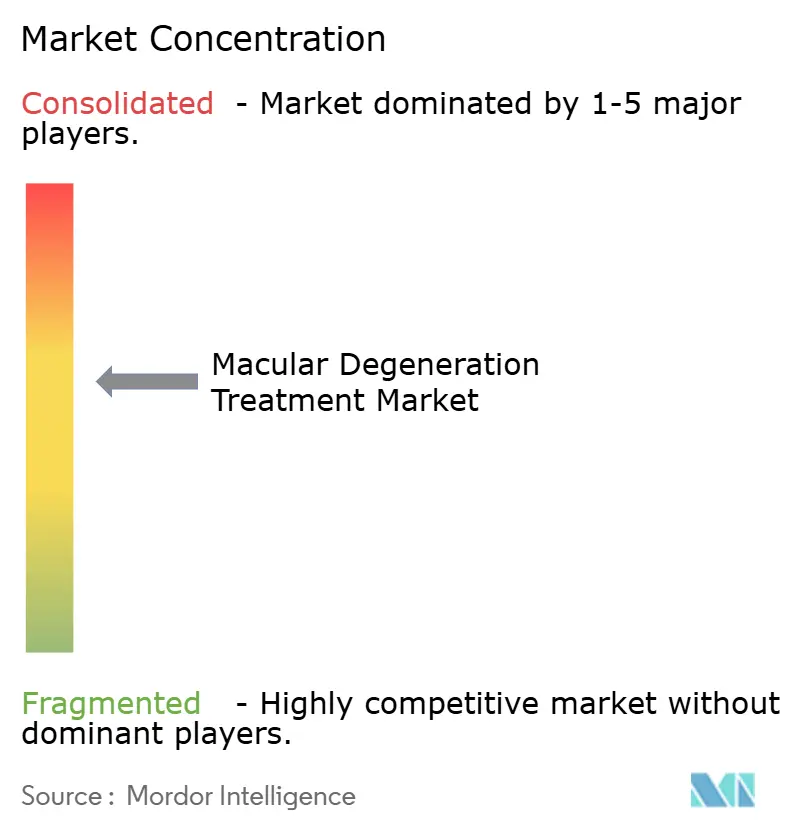

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Macular Degeneration Treatment Market Analysis by Mordor Intelligence

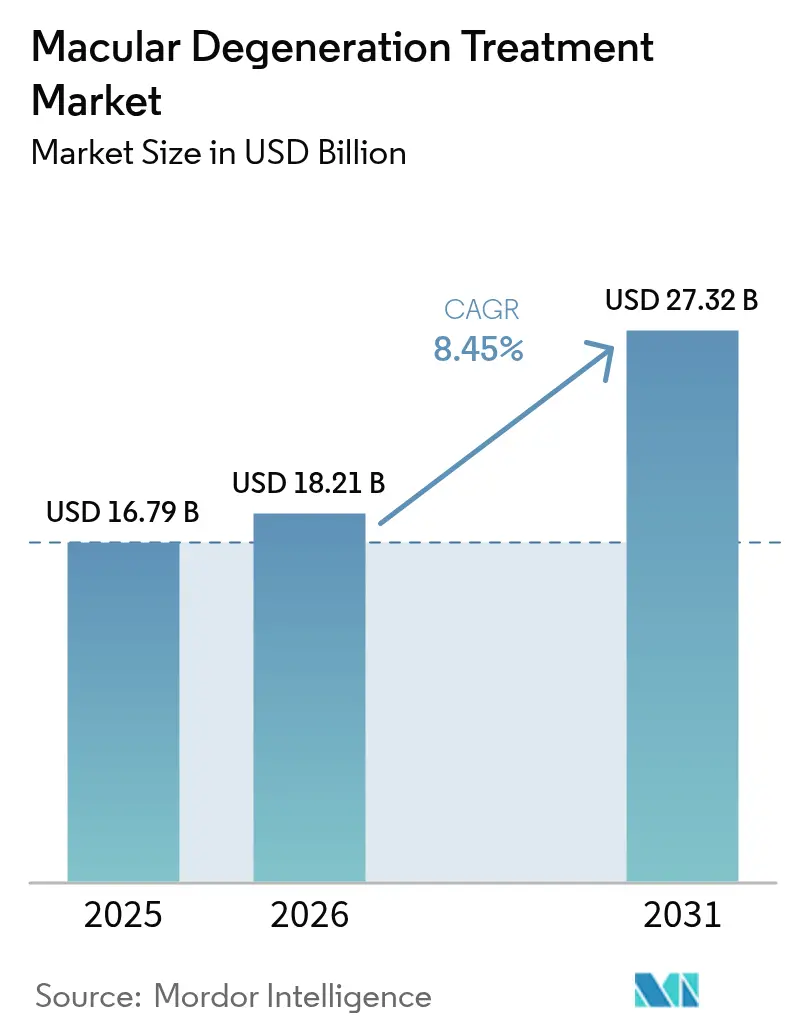

The macular degeneration treatment market size is projected to expand from USD 16.79 billion in 2025 and USD 18.21 billion in 2026 to USD 27.32 billion by 2031, registering a CAGR of 8.45% between 2026 to 2031. The macular degeneration treatment market is benefiting from durable anti-VEGF biologics that stretch dosing intervals to 16 weeks, complement inhibitors that open a new revenue stream in geographic atrophy, and AI-enabled optical coherence tomography (OCT) systems that detect high-risk drusen growth well before visual loss occurs. Gene-therapy pipelines, suprachoroidal delivery devices, and home-monitoring apps are broadening the therapeutic toolkit, while biosimilar discounts of 30-40% in Europe and emerging markets are stimulating treatment uptake without eroding overall value, as manufacturers counter price pressure with differentiated, longer-acting formats. North America remains the largest revenue generator due to Medicare Part B reimbursement, yet Asia-Pacific is the fastest-growing region as Japan, China, and South Korea accelerate public funding for aging-related vision care. Competitive intensity is high; originators are defending share through patent extensions, room-temperature-stable formulations, and digital-diagnostic bundles that reduce clinic workload and support value-based contracting.

Key Report Takeaways

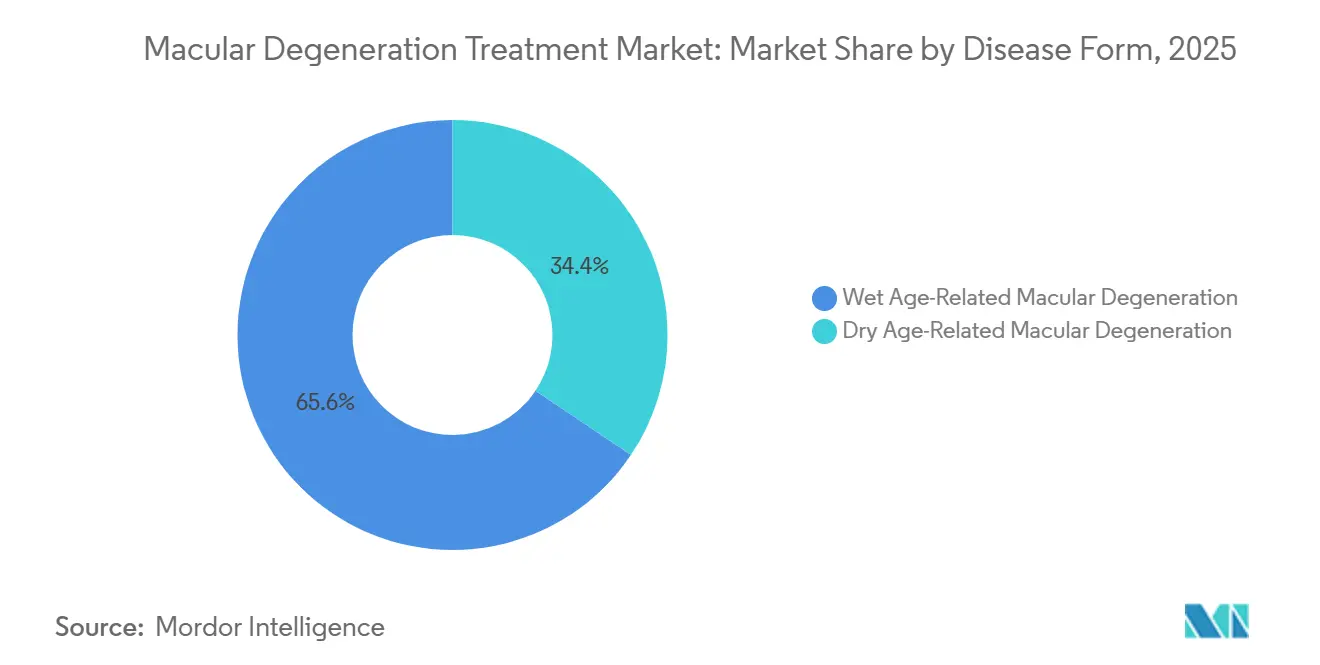

- By disease form, wet age-related macular degeneration led the macular degeneration treatment market with a 65.55% market share in 2025, while dry AMD is projected to expand at an 11.85% CAGR through 2031.

- By stage of disease, late-stage cases accounted for 45.53% of the macular degeneration treatment market size in 2025, whereas intermediate-stage is advancing at an 11.75% CAGR over 2026-2031.

- By route of administration, intravitreal injection accounted for 62.52% of revenue in 2025; suprachoroidal delivery is forecast to grow at a 10.12% CAGR during the same period.

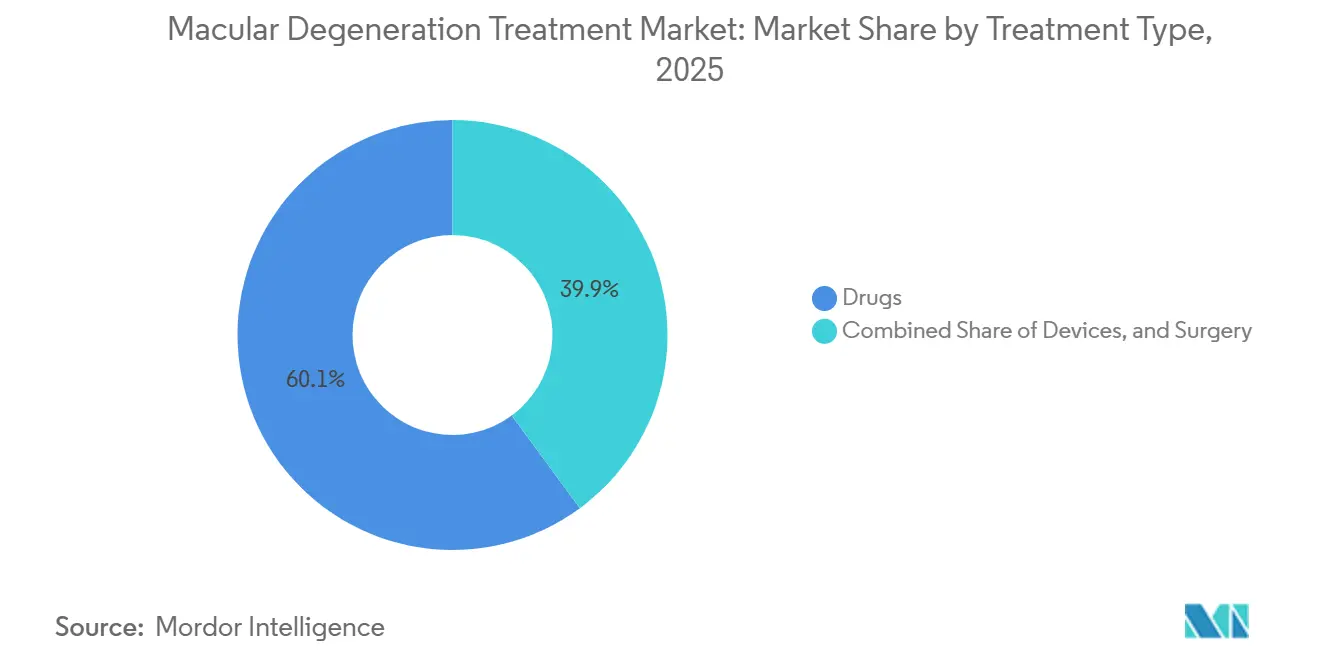

- By treatment type, drugs accounted for 60.15% of spending in 2025, and devices are rising at a 11.82% CAGR through 2031.

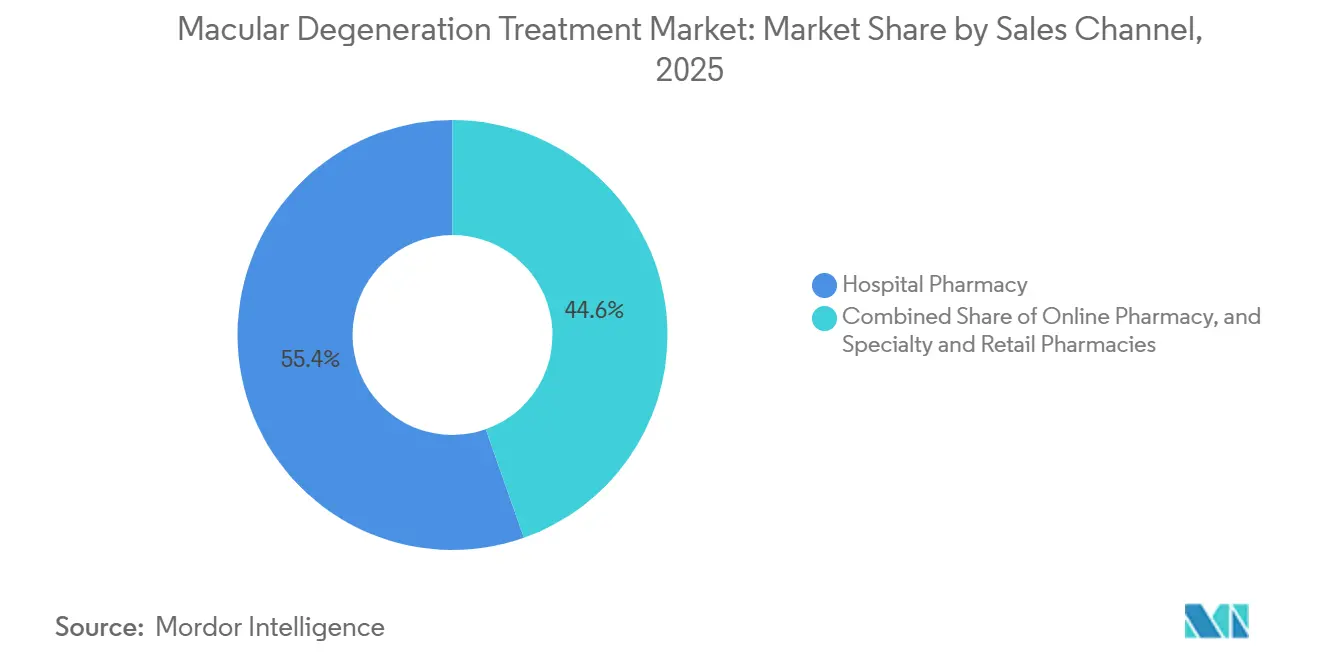

- By sales channel, hospital pharmacies held 55.45% share in 2025, whereas online pharmacies are set to climb at a 12.62% CAGR as telemedicine integrates specialty fulfillment.

- By geography, Asia-Pacific is set to record the fastest 10.72% CAGR through 2031, although North America commanded 42.55% revenue in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Macular Degeneration Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of AMD In Aging Populations | +2.1% | Global, with concentration in Japan, Germany, Italy, South Korea | Long term (≥ 4 years) |

| Rapid Expansion of Long-Acting Anti-VEGF Launches | +1.8% | North America, Europe, Australia | Medium term (2-4 years) |

| Improved Ophthalmic Imaging & AI-Enabled Early Detection | +1.3% | North America, APAC core (Japan, South Korea, Singapore) | Medium term (2-4 years) |

| Biosimilar-Led Price Erosion Widening Access in Ems | +1.0% | Europe, Latin America, Middle East, Southeast Asia | Short term (≤ 2 years) |

| Home-Monitoring Apps Boosting Diagnosed-to-Treated Ratio | +0.7% | North America, Western Europe | Short term (≤ 2 years) |

| Increasing Healthcare Expenditure on Vision Preservation | +0.9% | Global, led by OECD countries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of AMD in Aging Populations

Japan recorded 36.2 million citizens aged 65 and above in 2024, equal to 29.1% of its total population, while South Korea crossed the “super-aged” threshold at 20% in 2025. China expects 400 million people over 60 by 2030, and AMD incidence more than doubles with every decade after 60[1]Statistics Bureau of Japan, “Population Estimates 2024,” STAT, stat.go.jp. Germany, Italy, and Spain each exceeded a 23% elderly share in 2025, driving double-digit growth in retina clinic visits. Because central-vision loss restricts daily living, governments fund AMD care even during economic downturns, shielding the macular degeneration treatment market from cyclical risk. These demographic realities create durable visibility into demand for at least the next two decades.

Rapid Expansion of Long-Acting Anti-VEGF Launches

Roche’s bispecific faricimab enabled 60% of trial participants to maintain 16-week intervals, halving the injection frequency compared with monthly aflibercept. Genentech’s Port Delivery System, a surgically implanted refillable ranibizumab reservoir, extends dosing to six-month intervals and received FDA clearance in 2024. Regeneron’s Eylea HD gained approval in 2024 with 8 mg strength that permits 12-16-week maintenance after loading. Extended durability reduces visit-related costs by USD 1,200-1,800 per patient annually in the United States. As durability improves, patient adherence climbs, and payers realize net savings, amplifying volume without proportional cost expansion in the macular degeneration treatment market.

Improved Ophthalmic Imaging & AI-Enabled Early Detection

Heidelberg Engineering integrated AI algorithms that automatically quantify drusen volume and pigmentary changes, reducing manual grading time by 80%. Topcon’s Harmony platform flags >10% annual drusen growth, directing high-risk patients toward complement-inhibition therapy. Japan mandated AI-OCT in annual municipal check-ups for seniors starting April 2025, boosting early-stage AMD diagnoses by 34% in pilot prefectures. Sensitivity and specificity above 89% enable prophylactic therapy before photoreceptor loss, expanding the funnel from diagnosed to treated in the macular degeneration treatment market. Earlier intervention lowers long-term disability costs and strengthens payer alignment with preventive care models

Biosimilar-Led Price Erosion Widening Access in Emerging Markets

Samsung Bioepis introduced SB11, a ranibizumab biosimilar, in the European Union at a 35% discount in January 2025, accelerating treatment volumes by 22% in Central and Eastern Europe. Formycon’s FYB203 entered 12 EU countries at 40% under originator pricing in September 2025, with Spain and Italy mandating substitution for naïve patients. In India, ranibizumab biosimilars cost INR 8,500 (USD 102) versus INR 28,000 for the branded product, increasing injection uptake by 47% in tier-2 cities. Brazil’s public health system added bevacizumab biosimilars to its formulary, expanding coverage to 2.3 million additional beneficiaries. These moves temper spending pressure and enlarge patient pools, buttressing revenue growth even as unit prices fall.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Biologic and Gene Therapies | -1.4% | Global, acute in Latin America, Middle East, Africa, South Asia | Medium term (2-4 years) |

| Limited Reimbursement in Low-Income Regions | -0.9% | Sub-Saharan Africa, Southeast Asia (excluding Singapore), Central America | Long term (≥ 4 years) |

| Stringent Regulatory and Safety Requirements | -0.6% | Global, with extended timelines in EU, Japan | Medium term (2-4 years) |

| Chronic Treatment Burden and Patient Non-Compliance | -0.8% | Global, pronounced in rural and underserved areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Biologic and Gene Therapies

Originator anti-VEGF biologics list at USD 1,850-2,400 per dose in the United States, translating to USD 11,000-14,000 annually for monthly regimens. Gene-therapy candidates such as RGX-314 may launch at USD 600,000-750,000 per eye, echoing pricing precedents like Luxturna. In Brazil, one aflibercept injection equals 8.5 months of minimum-wage income, forcing legal action to secure public-sector supply. High upfront costs impede early intervention, causing patients to present later when therapy is less effective yet more expensive, thereby damping the macular degeneration treatment market growth potential[2]World Health Organization, “Global Report on Vision 2025,” WHO, who.int .

Limited Reimbursement in Low-Income Regions

Many public health systems earmark less than 2% of their budgets for ophthalmology. Kenya’s insurance covers cataract surgery but excludes intravitreal biologics. The Philippines reimburses only 43% of the actual price of ranibizumab, deterring two-thirds of diagnosed patients from initiating treatment. Guatemala employs 47 retina specialists for 18 million people, concentrating services in the capital. Registration delays of 18-24 months for biosimilars prolong monopolies, keeping prices high and limiting market penetration of macular degeneration treatments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Disease Form: Therapeutic Shift Toward Dry AMD

Wet AMD retained 65.55% of 2025 revenue, yet dry AMD is forecast to grow at an 11.85% CAGR as complement inhibitors secure commercial traction. The macular degeneration treatment market size for dry AMD is expected to widen rapidly once physicians gain confidence in lesion-growth reduction data. Monthly pegcetacoplan and avacincaptad pegol doses slowed geographic-atrophy expansion by up to 36%, a meaningful halt that supports premium reimbursement. Wet-form revenue is easing because biosimilar ranibizumab already accounts for 28% of European volume, and extended-interval aflibercept reduces vials per patient by 40% over three years[3]European Medicines Agency, “Ranibizumab Biosimilar SB11 Assessment Report,” EMA, ema.europa.eu.

Pipeline activity blurs categorical lines; up to 20% of dry AMD patients convert to neovascular disease, and combination trials are testing dual anti-VEGF plus complement blockade. Gene-therapy vectors encoding complement regulators, such as 4D-150, achieved early proof of concept with 68% vision stability at 12 months[4]4D Molecular Therapeutics, “Interim Data on 4D-150,” 4DMT, 4dmoleculartherapeutics.com . As durable agents migrate from clinic to market, dry-form uptake will offset biosimilar erosion on the wet side, preserving overall macular degeneration treatment market momentum.

By Stage of Disease: Intermediate-Stage Prevention Is the Fastest-Rising Niche

Late-stage disease accounted for 45.53% of revenue in 2025 because neovascular cases require frequent anti-VEGF dosing, and geographic atrophy now has disease-modifying options. The macular degeneration treatment market share for early-stage remains modest, but intermediate-stage volume is climbing at an 11.75% CAGR on the back of AI-OCT triage and risk-based reimbursement approvals in Germany and the Netherlands. Extended detection widens the eligible cohort: over 3.2 million Americans have intermediate dry AMD but show no symptoms; payers now reimburse prophylactic complement inhibition for the top-risk quintile.

Adherence bottlenecks curb late-stage growth, as 58% of patients discontinue monthly anti-VEGF therapy within five years. In contrast, intermediate-stage patients often maintain better visual acuity and are more motivated to comply with less-frequent dosing. National screening in Japan identified 340,000 high-risk citizens in its first year, demonstrating that policy mandates can accelerate the growth of the macular degeneration treatment market for preventive therapy.

By Treatment Type: Devices Accelerate While Drugs Mature

Drugs accounted for 60.15% of 2025 spending, led by anti-VEGF agents whose biosimilar versions depress unit pricing while sustaining high volume. Complement inhibitors added USD 1.1 billion last year and will scale further as payers embrace their lesion-slowing benefit, although monthly dosing moderates persistence. Devices are the fastest-growing slice at an 11.82% CAGR, buoyed by Medicare coverage for electronic magnifiers and retinal implants that restore limited functional vision.

The macular degeneration treatment market size for devices also benefits from the elderly's preference for non-invasive solutions once pharmacologic options plateau. Second Sight’s cortical implant entered limited European launch at USD 165,000 per unit, meeting pent-up demand among legally blind AMD patients. Telescopic contact lenses reached 18% penetration among eligible U.S. patients within 12 months, underscoring the willingness of patients to adopt wearable aids.

By Route of Administration: Suprachoroidal Delivery Gains Traction

Intravitreal injections accounted for 62.52% of revenue in 2025 because specialists are comfortable with well-established safety protocols. However, suprachoroidal administration is growing at a 10.12% CAGR, as Clearside’s microinjector shows reduced systemic exposure and higher choroidal drug concentrations. The macular degeneration treatment market size split between these routes will tighten if suprachoroidal gene-therapy vectors, such as RGX-314, confirm durable expression without surgical vitrectomy.

A 2025 patient survey found 68% would trade modest efficacy loss for fewer or less invasive injections, illustrating an appetite for route innovation. Yet adoption lags specialist certification; only 15% of U.S. retina physicians were trained in the suprachoroidal technique by end-2025. Scaling training programs is thus a gating factor for broader uptake.

By Sales Channel: Online Pharmacy Emerges as High-Growth Outlet

Hospital pharmacies still accounted for 55.45% of 2025 revenue, as most biologics require cold-chain storage and on-site preparation under sterile conditions. Specialty and retail pharmacies manage oral nutraceuticals and some prefilled syringes, but online channels are booming at a 12.62% CAGR thanks to Amazon Pharmacy and CVS digital offerings that ship AREDS2 vitamins and low-vision aids within 48 hours. The macular degeneration treatment market share for online channels will continue rising as manufacturers develop room-temperature-stable anti-VEGF formulations that meet home-delivery regulations.

Alto Pharmacy’s AMD program bundled tele-optometry consults with automated refills, pushing adherence to 89% versus 62% for brick-and-mortar counterparts. Walgreens’ partnership with Notal Vision to rent home OCT units tightens the feedback loop between monitoring and drug shipment, illustrating how digital ecosystems can capture recurring revenue in the macular degeneration treatment market.

Geography Analysis

North America generated 42.55% of 2025 revenue, underpinned by Medicare Part B reimbursement that pays USD 650-850 per injection, including drug and professional fees Eylea HD obtained a USD 2,105 Part B payment rate in 2024, encouraging volume discounts and supporting steady procedure growth despite biosimilar entry. Canada covers ranibizumab and aflibercept under provincial formularies, yet faricimab access lags, leading patients to appeal through Exceptional Access Programs that add six-week delays. Mexico expanded coverage for ranibizumab biosimilars in 2025 through Seguro Popular, yet rural areas continue to experience specialist shortages that limit penetration.

Asia-Pacific is the fastest-growing region, advancing at a 10.72% CAGR. Japan reimburses up to 90% of biologic costs for seniors, with out-of-pocket caps of JPY 80,000 (USD 550) per month, driving high adherence. China added ranibizumab biosimilars to 15 provincial lists, trimming patient costs by 70% and expanding the market for macular degeneration treatments among urban workers. South Korea’s risk-sharing pact for faricimab caps annual expenses at KRW 12 million (USD 9,200), fuelling rapid uptake. India remains constrained; fewer than 20% of diagnosed patients initiate anti-VEGF therapy due to out-of-pocket costs exceeding INR 25,000 (USD 300) per injection.

Europe enjoys broad access, yet budgets are tight. Germany and France mandate biosimilar substitution for treatment-naïve cases, propelling 24% volume share for SB11 within 18 months. The United Kingdom negotiated confidential discounts that lowered per-injection spending by roughly 40%, adding 22% capacity without extra budget. Spain and Italy imposed monthly injection quotas in 2025, delaying therapy for 12-18% of patients and spurring legal challenges now pending before the European Court of Justice.

The Middle East and Africa remain nascent contributors. Saudi Arabia’s Vision 2030 plan earmarked SAR 800 million (USD 213 million) for 40 new retina clinics, improving geographic coverage. South Africa’s public sector does not reimburse anti-VEGF agents, limiting access to the privately insured 9 million residents. Latin America is mixed; Brazil’s public system adopted bevacizumab biosimilars, while Argentina’s economic turmoil and triple-digit inflation in 2024 disrupted imports of branded biologics.

Competitive Landscape

The macular degeneration treatment market remains moderately concentrated, with Regeneron, Roche, and Novartis generating the majority of 2025 revenue, yet competitive pressures are intensifying. Originators are extending the lifecycle through high-dose or room-temperature-stable formulations and by bundling AI-diagnostic platforms that improve dosing precision and patient outcomes. Roche’s 4.2 million-image OCT database trains algorithms that predict individual response and schedule injections only when needed, lowering per-patient drug burden by 18% and fortifying brand loyalty.

Biosimilar manufacturers such as Samsung Bioepis and Formycon captured 24% of European ranibizumab and aflibercept volume within 18 months, prompting 30% discounts on Lucentis in Germany and spurring Bayer to bundle Eylea with diagnostic hardware in tenders. Patent cliffs loom: Aflibercept’s U.S. exclusivity expires in 2027, likely compressing EBITDA margins by 8-12 percentage points for originators.

Innovation is diversifying. Apellis and Astellas commercialized the first complement inhibitors for dry AMD but hold only 18% patient penetration amid monthly-dose fatigue; they are testing sustained-release implants to widen appeal. Gene-therapy aspirants such as REGENXBIO and Adverum target one-time dosing that could recast revenue models from recurring prescriptions to annuity-like payments. Smaller device firms Second Sight, IrisVision, VisionCare are carving out high-value niches among late-stage patients who seek restored functional vision over lesion stabilization.

Macular Degeneration Treatment Industry Leaders

F Hoffmann-La Roche Ltd (Genetech)

Novartis AG

Bausch Health Companies Inc

REGENXBIO Inc.

Regeneron Pharmaceuticals Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Regeneron secured FDA approval for Eylea HD 8 mg to treat macular edema following retinal vein occlusion, enabling every-eight-week maintenance after an initial loading phase.

- September 2025: The FDA granted fast-track designation to SAR402663, an investigational single-dose intravitreal gene therapy intended for neovascular AMD.

Global Macular Degeneration Treatment Market Report Scope

As per the scope of the report, macular degeneration is a retinal disorder that primarily affects older people. The early stages of the disease (early and intermediate AMD) are generally asymptomatic and gradually progress to the late stages, which may cause severe visual loss. Macular degeneration symptoms include blurry or fuzzy vision, difficulty recognizing familiar faces, and the inability to see in dim light or see spots. Macular degeneration diagnosis can be performed through a comprehensive dilated eye exam and other tests such as the Amsler grid, fluorescein angiography, optical coherence tomography (OCT), and pupil dilation.

The macular degeneration treatment market is segmented by disease form, disease stage, treatment type, route of administration, sales channel, and geography. By disease form, the market is segmented into dry age-related macular degeneration and wet age-related macular degeneration. By stage of disease, the market is segmented into early-stage AMD, intermediate-stage AMD, and late-stage AMD. By treatment type, the market is segmented into drugs, devices, and surgery. By route of administration, the market is segmented into intravenous route and intravitreal route. By sales channel, the market is segmented into hospital pharmacy, online pharmacy, and specialty & retail pharmacies. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size is provided in terms of value (USD).

| Dry Age-Related Macular Degeneration |

| Wet Age-Related Macular Degeneration |

| Early-Stage AMD |

| Intermediate-Stage AMD |

| Late-Stage AMD |

| Drugs | Anti-VEGF Agents |

| Complement Pathway Inhibitors | |

| Gene & Cell Therapies | |

| Dietary Supplements & Antioxidants | |

| Other Drugs | |

| Devices | Low-Vision Glasses |

| Contact Lenses | |

| Retinal Implants & Vision Aids | |

| Surgery | Laser Photocoagulation |

| Photodynamic Therapy | |

| Other Surgical Procedures |

| Intravitreal |

| Suprachoroidal |

| Intravenous |

| Hospital Pharmacy |

| Online Pharmacy |

| Specialty & Retail Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Disease Form | Dry Age-Related Macular Degeneration | |

| Wet Age-Related Macular Degeneration | ||

| By Stage of Disease | Early-Stage AMD | |

| Intermediate-Stage AMD | ||

| Late-Stage AMD | ||

| By Treatment Type | Drugs | Anti-VEGF Agents |

| Complement Pathway Inhibitors | ||

| Gene & Cell Therapies | ||

| Dietary Supplements & Antioxidants | ||

| Other Drugs | ||

| Devices | Low-Vision Glasses | |

| Contact Lenses | ||

| Retinal Implants & Vision Aids | ||

| Surgery | Laser Photocoagulation | |

| Photodynamic Therapy | ||

| Other Surgical Procedures | ||

| By Route of Administration | Intravitreal | |

| Suprachoroidal | ||

| Intravenous | ||

| By Sales Channel | Hospital Pharmacy | |

| Online Pharmacy | ||

| Specialty & Retail Pharmacies | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the macular degeneration treatment market in 2026?

The macular degeneration treatment market size stands at USD 18.21 billion in 2026 and is on course to reach USD 27.32 billion by 2031.

What is driving growth in Asia-Pacific?

Public reimbursement expansion in Japan, China, and South Korea plus rapid population aging is lifting Asia-Pacific revenue at a 10.72% CAGR.

Which treatment segment is growing the fastest?

Devices such as electronic magnifiers and retinal implants are expanding at an 11.82% CAGR as late-stage patients seek functional vision aids.

Why are complement inhibitors important?

They provide the first disease-modifying option for dry AMD, slowing geographic-atrophy lesion growth by up to 36% and filling a major unmet need.

Will biosimilars hamper market value?

Biosimilars lower unit prices but expand patient access; originators offset the impact with long-acting formulations, so total market value continues to rise.

When could gene therapy reach the market?

Pivotal trials for RGX-314 and ADVM-022 read out in late 2026, positioning the first one-time AMD gene therapies for potential approval by 2028.

Page last updated on: