Waldenstrom's Macroglobulinemia (WM) Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

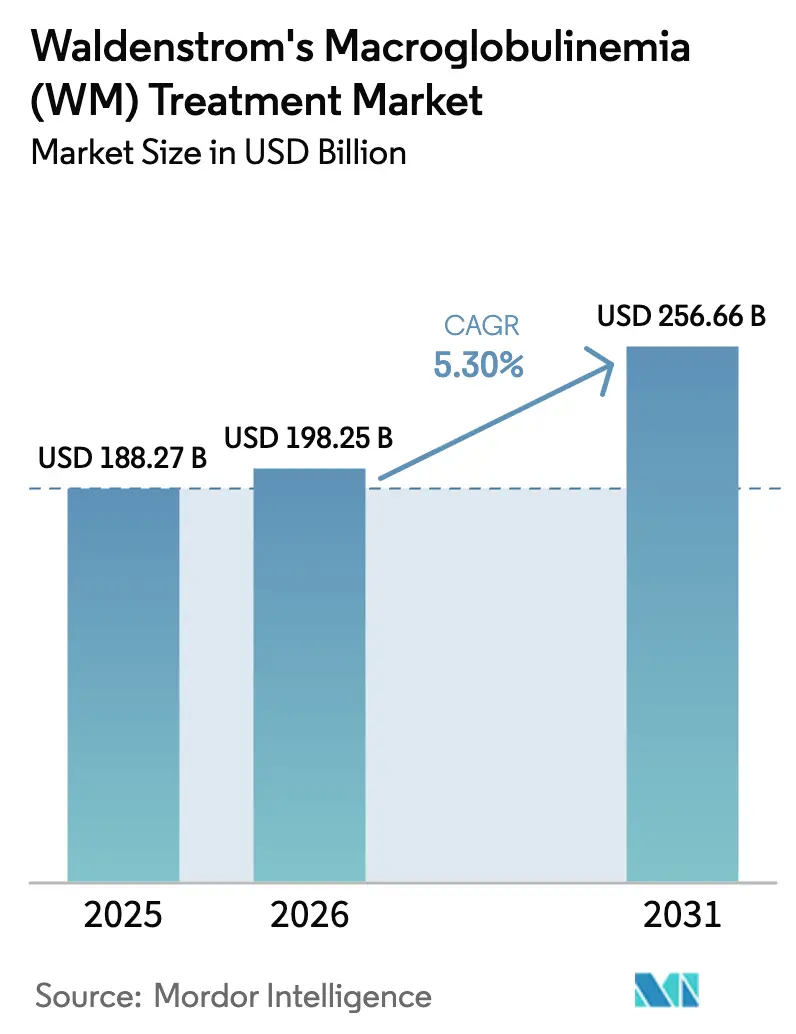

| Market Size (2026) | USD 198.25 Billion |

| Market Size (2031) | USD 256.66 Billion |

| Growth Rate (2026 - 2031) | 5.30% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Waldenstrom's Macroglobulinemia (WM) Treatment Market Analysis by Mordor Intelligence

The Waldenstrom's Macroglobulinemia Treatment Market size is projected to expand from USD 188.27 billion in 2025 and USD 198.25 billion in 2026 to USD 256.66 billion by 2031, registering a CAGR of 5.30% between 2026 to 2031.

The increasing prevalence and incidence of cases of Waldenstrom's macroglobulinemia and increasing drug approvals by the regulatory bodies are escalating the growth of the market. Regulatory advancements are driving momentum in the industry. In January 2024, the FDA granted accelerated approval to zanubrutinib for previously treated patients. This was followed by the FDA's acceptance of BeiGene's supplemental biologics license application in October 2025, expanding the drug's use to frontline therapy. These developments collectively improve access to therapy and streamline treatment initiation. Additionally, precision diagnostics are optimizing care pathways. The routine detection of the MYD88 L265P mutation now informs BTK inhibitor selection in academic settings, accelerating time-to-treatment and reducing cycles of less effective therapies.

Key Report Takeaways

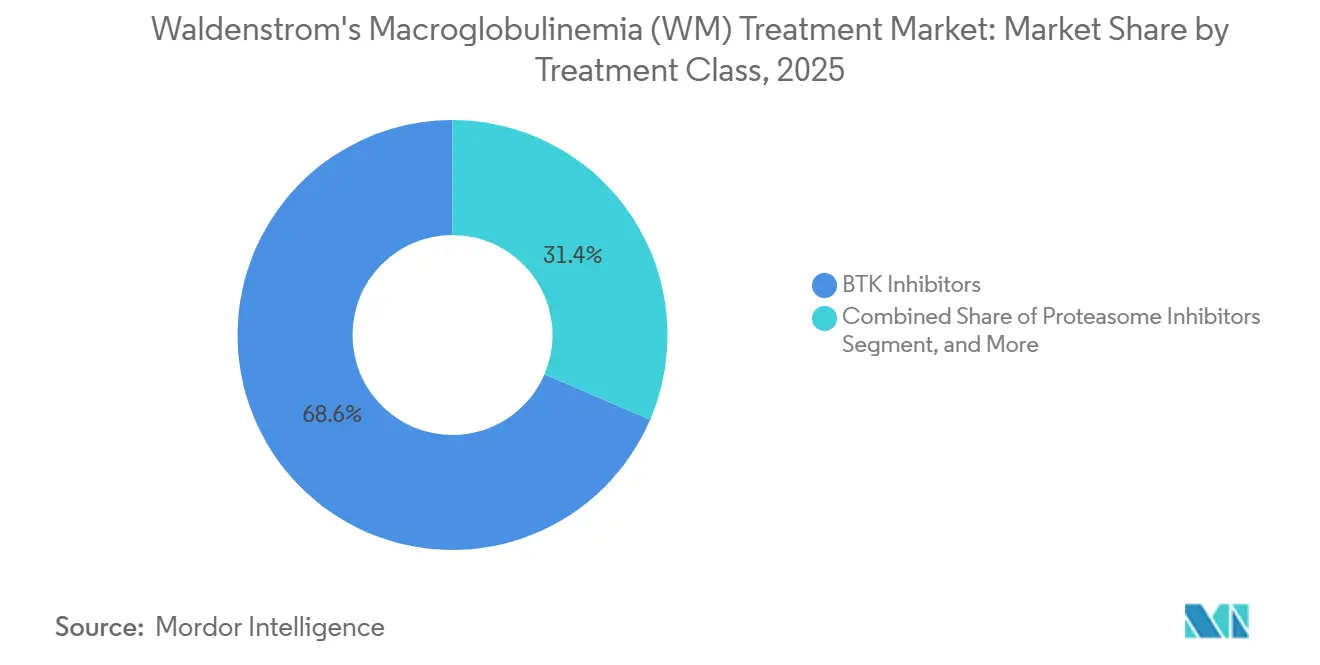

- By treatment class, BTK inhibitors led with 68.56% revenue share in 2025, while proteasome inhibitors are forecast to expand at a 5.87% CAGR through 2031.

- By line of therapy, first-line held 55.45% revenue share in 2025, while second-line is projected to grow at a 6.39% CAGR through 2031.

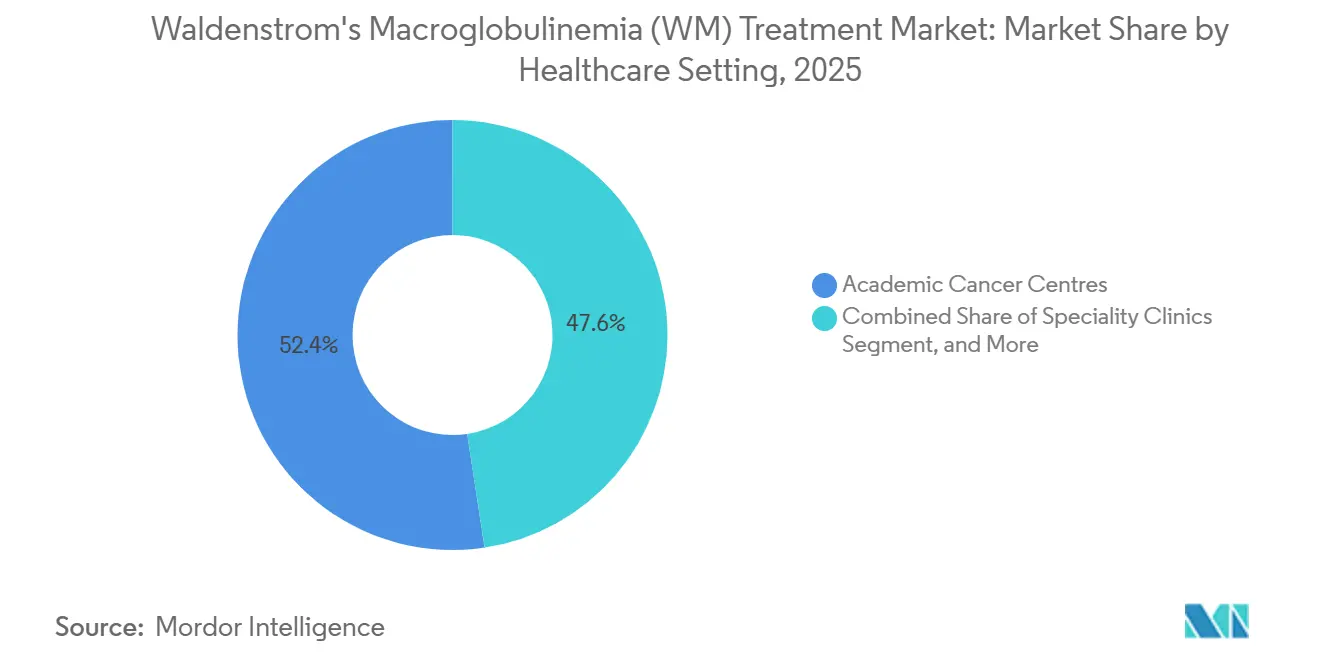

- By healthcare setting, academic cancer centers accounted for 52.37% revenue share in 2025, while specialty clinics are forecast to expand at a 6.80% CAGR through 2031.

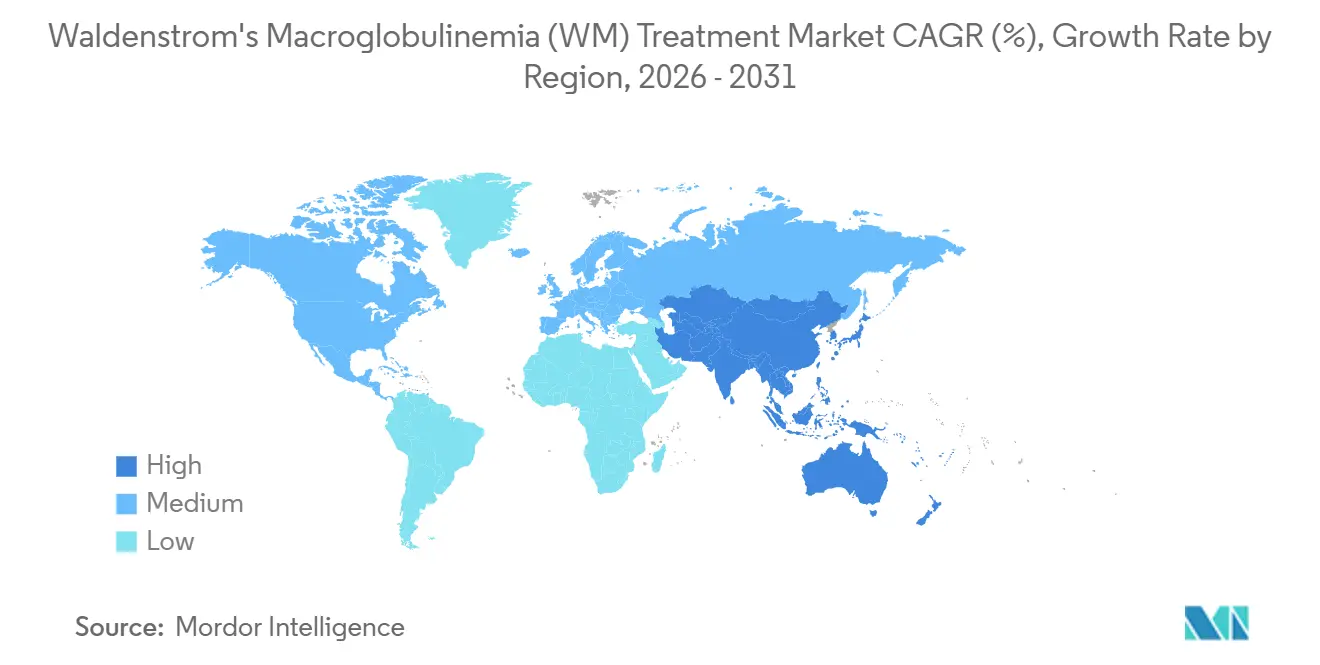

- By geography, North America held 45.62% in 2025, while Asia-Pacific is projected to advance at a 6.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Waldenstrom's Macroglobulinemia (WM) Treatment Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Growing diagnosed prevalence via next-gen genomic testing | +0.9% | Global, with North America and Europe leading adoption | Short term (≤ 2 years) |

| FDA/EMA approvals & label expansions of BTK inhibitors | +1.2% | North America, Europe, Asia-Pacific (China, Japan) | Medium term (2-4 years) |

| Ageing population enlarging treatment-eligible cohort | +0.7% | Global, particularly North America, Europe, Japan | Long term (≥ 4 years) |

| Non-covalent BTK degraders addressing resistance gaps | +0.8% | North America, Europe, select Asia-Pacific markets | Medium term (2-4 years) |

| Liquid-biopsy MRD tools triggering earlier intervention | +0.6% | North America, Europe, Australia | Short term (≤ 2 years) |

| Advocacy-funded trial acceleration in rare haematologics | +0.4% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Diagnosed Prevalence Via Next-Gen Genomic Testing

Next-generation sequencing panels that detect MYD88 L265P and CXCR4 mutations reduced the median time-to-diagnosis from 14.3 months in 2020 to 6.8 months in 2025. This advancement expanded the patient population eligible for treatment and enabled earlier intervention for high-risk individuals. In March 2024, Medicare coverage was extended to Foundation Medicine’s FoundationOne Heme test. This test sequences 406 genes and, with significant payment support towards its USD 5,800 list price, has driven increased adoption in community settings, promoting standardized testing practices. Launched in September 2024, Illumina’s TruSight Oncology 500 assay offers a 7-day turnaround time, expediting decision-making compared to traditional methods and facilitating the timely initiation of BTK inhibitors.[1]Illumina, “TruSight Oncology 500 Product Overview,” Illumina, illumina.com Additionally, the European Medicines Agency’s 2024 directive mandated MYD88 mutation testing before prescribing BTK inhibitors, making it a regulatory requirement across the region.[2]European Medicines Agency, “Guidance on MYD88 Testing Prior to BTK Inhibitor Use,” European Medicines Agency, ema.europa.eu These advancements have redefined the diagnostic framework for the Waldenström's Macroglobulinemia market and strengthened the adoption of molecularly guided therapy selection across treatment settings.

FDA/EMA Approvals & Label Expansions of BTK Inhibitors

In January 2024, the FDA granted accelerated approval to zanubrutinib for previously treated WM, expanding access to this selective BTK inhibitor, recognized for its favorable tolerability in routine clinical practice. Similarly, the EMA issued a conditional marketing authorization in May 2024, enabling reimbursement across 27 EU member states and improving patient access within hospital formularies. In October 2025, Acalabrutinib received FDA priority review for frontline use, supported by ELEVATE-WM data demonstrating a 94% overall response rate, thereby enhancing competitive options for initial therapy selection. Japan’s PMDA approved zanubrutinib in December 2024, with the national insurance framework capping co-pays at JPY 100,000, reducing financial barriers for older patients who are more likely to require treatment. These approvals and label expansions are expected to drive significant near-term volume growth in the Waldenström's Macroglobulinemia market across the United States, the European Union, and Japan.

Ageing Population Enlarging Treatment-Eligible Cohort

By 2030, the global population aged 65 and older is expected to grow from 771 million in 2022 to 994 million, increasing the at-risk population for WM and driving consistent therapy demand throughout the decade.[3]United Nations, “World Population Prospects 2022,” United Nations, un.org In the United States, the number of adults aged 70 and above is projected to reach 43.2 million by 2030, which is likely to boost diagnostic volumes if the age-specific incidence remains stable.[4]U.S. Census Bureau, “Population Projections,” U.S. Census Bureau, census.gov In 2024, individuals aged 65 and older accounted for 21.3% of Europe's population, with some countries exceeding 23%, a trend linked to higher referral volumes to tertiary centers. In Japan, citizens aged 75 and above represented 15.5% of the population in 2024, reflecting a rise in hematologic cancer cases and increased pressure on academic centers.[5]Eurostat, “Population Structure and Ageing,” European Commission, ec.europa.eu Median overall survival for WM has improved from 8.3 years in 2015 to 12.7 years in 2024, extending therapy duration and expanding the treatment base in the Waldenström's Macroglobulinemia market.

Non-Covalent BTK Degraders Addressing Resistance Gaps

Covalent BTK inhibitors primarily target the C481 residue; however, mutations at C481S, observed in approximately 30% of relapsed patients, disrupt binding and drive resistance. This highlights the need for alternative therapies with different binding mechanisms. Non-covalent BTK inhibitors and degraders have demonstrated the ability to retain activity against C481S-mutant clones, effectively restoring disease control in ibrutinib-refractory cases. Nurix’s NX-5948, a cereblon-recruiting BTK degrader, entered Phase 1/2 trials in August 2025. Interim results showed a 67% partial response rate among 12 evaluable WM patients, supporting the continued development of targeted protein degradation for this patient group. BeiGene’s BGB-16673 achieved a 78% overall response rate in a Phase 1 study involving patients who had progressed on ibrutinib, indicating potential sequencing strategies as resistance emerges. In October 2025, the FDA granted Fast Track designation to NX-5948, accelerating review timelines and supporting its expedited development plans.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High annual therapy cost & restricted reimbursement | -0.7% | Global, particularly emerging markets and Europe | Medium term (2-4 years) |

| Limited WM expertise in low-resource regions | -0.5% | Sub-Saharan Africa, South Asia, Latin America | Long term (≥ 4 years) |

| Cardiotoxicity concerns curbing combo-regimen uptake | -0.3% | Global, with heightened scrutiny in North America and Europe | Short term (≤ 2 years) |

| Radio-isotope supply bottlenecks for I-131 therapies | -0.2% | Global, with manufacturing concentrated in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Annual Therapy Cost & Restricted Reimbursement

With an annual list price of USD 179,000, zanubrutinib imposes significant pressure on payer budgets in the United States, resulting in utilization management measures that can delay treatment initiation. In November 2024, NICE declined routine NHS funding for zanubrutinib, citing an incremental cost-effectiveness ratio of GBP 87,000 (approximately USD 110,000), which exceeds the UK's GBP 30,000 threshold. Similarly, in March 2024, CADTH recommended against public reimbursement for ibrutinib as a frontline treatment for WM due to uncertainties in the long-term economic model, limiting its adoption in Canada's public programs.

Limited WM Expertise in Low-Resource Regions

In Sub-Saharan Africa, fewer than 120 hematologists hold subspecialty certification in lymphoma. This shortage significantly limits the capacity for timely diagnoses and evidence-based treatments, particularly in remote regions. A comparative analysis highlights that in low-resource settings, diagnosis is delayed by 11 months after symptom onset, compared to 6.8 months in high-income countries, further compounding the disease burden at presentation. In India, a workforce survey from 2024 shows that out of 1,200 medical oncologists, only 340 completed hematologic malignancy fellowships. Additionally, the majority of these specialists are concentrated in metropolitan centers, restricting regional access to WM-specific care. Telemedicine has partially addressed these gaps, with services like eConsult managing 420 WM consultations in 2025. However, reimbursement policies for asynchronous care continue to vary across states in the United States.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Class: BTK Inhibitors Dominate, Proteasome Inhibitors Gain

In 2025, BTK inhibitors captured a dominant 68.56% share of the treatment-class revenue, reflecting strong prescriber confidence and their position as the preferred option for eligible patients in the Waldenström's Macroglobulinemia market. Data from clinical trials highlighted the advantages of zanubrutinib over ibrutinib, with zanubrutinib demonstrating a longer median progression-free survival of 42.7 months compared to 20.3 months for ibrutinib, emphasizing the durability and continuity of selected BTK regimens. Additionally, zanubrutinib was associated with fewer Grade 3 or higher adverse events than ibrutinib, a critical consideration when cardiac risks influence treatment decisions. These clinical outcomes reinforce the central role of BTK inhibitors in first-line and early-relapse treatments for Waldenström's Macroglobulinemia. At the same time, the expanding pipeline of non-covalent agents and degraders continues to drive attention toward addressing resistance mechanisms. The regulatory progress of acalabrutinib in frontline WM further supports the expectation that multiple BTK options, differentiated by clinical profiles, will coexist, enabling more refined patient-level decisions as clinical guidelines evolve.

Proteasome inhibitors are projected to grow the fastest, with a compound annual growth rate (CAGR) of 5.87% through 2031. This growth is driven by the increasing adoption of bortezomib-based regimens, particularly among patients who develop atrial fibrillation on BTK therapy, a safety concern that significantly impacts treatment sequencing in both community and academic settings.

By Line of Therapy: Second-Line Settings Accelerate

In 2025, first-line therapy accounted for 55.45% of total line-of-therapy revenue, while second-line settings are anticipated to grow at a 6.39% CAGR through 2031. This growth is driven by factors such as resistance biology and safety considerations, which are influencing real-world treatment sequences. China's progress in reimbursing zanubrutinib has enhanced its frontline accessibility. Simultaneously, U.S. regulatory decisions in 2025 have played a pivotal role in shaping its adoption. These developments collectively supported its uptake at the initial stages of treatment. On the other hand, the future of second-line treatments depends on addressing the C481S-mediated resistance. This resistance occurs in approximately 30% of relapsed cases, prompting a shift to either non-covalent agents or BTK degraders as they gain maturity. Nurix's NX-5948 demonstrated a 67% partial response rate in patients with ibrutinib-refractory WM during a 2025 interim analysis. This outcome not only attracted investor interest but also highlighted degradation as a promising strategy in the Waldenström's Macroglobulinemia market. Data from registries indicate that after two prior treatment lines, the median progression-free survival drops to 9.2 months. With a limited number of approved agents, sequencing options become restricted, emphasizing the clinical importance of introducing new mechanisms in later treatment lines.

By Healthcare Setting: Specialty Clinics Rise

In 2025, academic cancer centers accounted for 52.37% of revenue in healthcare settings, reflecting their specialized expertise and leadership in clinical trials, particularly in enrolling patients into WM protocols. A significant portion of WM clinical trials is conducted exclusively at these academic centers, emphasizing their dominance in addressing complex sequencing challenges and providing access to novel mechanisms. Specialty clinics are projected to grow at a CAGR of 6.80% through 2031, driven by advancements such as liquid-biopsy MRD tools and telemedicine, which enable timely care in community settings while reducing referral delays. In 2025, Mayo Clinic's eConsult program managed 420 WM cases, demonstrating reduced travel costs per patient and presenting a practical approach to delivering high-quality care outside major tertiary centers.

Geography Analysis

In 2025, North America, with its established prescriber base and payer structures, is expected to maintain its leadership in accommodating high-cost oncology drugs. Meanwhile, the Asia-Pacific region is projected to experience rapid growth through 2031, driven by expanding reimbursement schemes for BTK inhibitors in the Waldenström's Macroglobulinemia market. Improved market access in China and Japan is already increasing initiation rates, while Australian subsidies have reduced out-of-pocket expenses that previously hindered uptake. Europe, while holding a significant market volume, is advancing at a slower pace. Decisions such as NICE’s 2024 stance on zanubrutinib are shaping treatment choices, resulting in slower alignment with jurisdictions offering early access.

Asia-Pacific’s growth trajectory is further supported by its large and aging population, which is expected to increase the number of eligible patients over time. This demographic trend amplifies the impact of enhanced reimbursements in major countries on the Waldenström's Macroglobulinemia market. The adoption of molecular diagnostics in routine evaluations by clinical teams is narrowing the gap between symptom identification and treatment initiation. This development is increasing the proportion of patients benefiting from targeted therapies earlier in their treatment journey. In Japan and Australia, affordable co-pay structures and national formularies are ensuring the continuation of therapy, which is critical for diseases requiring long-term management. In contrast, the Middle East and Africa, along with South America, continue to face challenges such as limited expert availability and funding, which are keeping their market shares relatively small despite recent policy initiatives.

Regulatory Landscape

Waldenstrom's macroglobulinemia (WM) treatment development is shaped by accelerated and rare-disease pathways across major agencies, including the US Food and Drug Administration (FDA) and the European Medicines Agency (EMA). Approved BTK inhibitors such as zanubrutinib (Brukinsa) and ibrutinib (Imbruvica) anchor current standards, while newer programs use designations to compress development timelines and broaden regulator interactions for relapsed/refractory disease. Examples include the FDA granting Breakthrough Therapy Designation to Cellectar Biosciences' iopofosine I 131 (June 2025) and Fast Track status for Nurix Therapeutics' BTK degrader NX-5948 (bexobrutideg). In the United States, Orphan Drug Designation remains a central lever for WM programs by supporting trial economics and exclusivity incentives.

In Europe, regulatory alignment for late-line WM is increasingly tied to conditional routes and scientific advice. Cellectar reported EMA Scientific Advice Working Party confirmation of eligibility to file for Conditional Marketing Authorization for iopofosine I 131 in post-BTK inhibitor WM (October 2025). Alongside drug review pathways, mutation-informed treatment selection has gained formal policy weight in some markets through guidance that reinforces biomarker testing prior to targeted therapy use, tightening the link between diagnostic adoption and access to BTK-centered regimens.

Competitive Landscape

The Waldenström's Macroglobulinemia market exhibited a moderate concentration, with the top three companies collectively commanding a majority share. Notably, no single entity surpassed the 28% mark, indicating potential opportunities for new entrants to focus on resistance biology or target underserved regions. Competition primarily revolves around label expansions and safety differentiation. For example, BeiGene received FDA acceptance in October 2025 for its frontline application of zanubrutinib. If approved, this would expand the drug's usage to earlier stages of care. Furthermore, combination therapies are gaining traction; the pairing of venetoclax with rituximab achieved an impressive 92% overall response rate in 2024. This not only underscored the efficacy of well-tolerated regimens but also intensified pricing and positioning challenges for single-agent alternatives.

Emerging mechanisms are capturing the attention of both investors and clinicians. Nurix, for instance, advanced its NX-5948 with promising interim data and, in October 2025, secured a notable USD 85 million in funding. This move highlights the growing interest in targeted protein degradation, especially in the context of resistant Waldenström's Macroglobulinemia. Meanwhile, Cellectar's CLR 131, a radiotherapeutic, carved out a unique niche but grappled with radio-isotope supply challenges, hindering its immediate scalability. On the other hand, InnoCare's orelabrutinib, a domestic BTK option in China, showcased significant sales momentum through 2025. This success story underscores the potential of regional champions in solidifying market access within their local landscapes.

Waldenstrom's Macroglobulinemia (WM) Treatment Industry Leaders

TG Therapeutics, Inc.

Curis, Inc.

X4 Pharmaceuticals, Inc.

Nurix Therapeutics, Inc.

BeOne Medicines GmbH

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key whitespace in WM is the post-BTK inhibitor setting, where resistance biology and tolerability constraints narrow the path to durable options. That dynamic is pulling investment and trial activity toward new mechanisms such as targeted radiotherapeutics and BTK degraders. Cellectar Biosciences has advanced iopofosine I 131 in relapsed/refractory WM with regulatory momentum, including FDA Breakthrough Therapy Designation in June 2025 and EMA steps toward Conditional Marketing Authorization in October 2025. The company also reported 12-month follow-up data from its Phase 2b CLOVER WaM study in May 2026.

Nurix Therapeutics has positioned NX-5948 (bexobrutideg) as a protein-degradation alternative for relapsed or refractory WM, supported by FDA Fast Track designation (December 2024), which allows faster iteration in dose and cohort expansion as safety and activity signals emerge. Opportunities are also forming around time-limited combination regimens aimed at deeper responses and finite therapy duration, which can change utilization patterns in a disease managed with long-term continuous treatment. ClinicalTrials.gov postings indicate active Phase 2 studies across both treatment-naive and previously treated WM populations, including Memorial Sloan Kettering Cancer Center initiating a Phase 2 trial of pirtobrutinib, venetoclax, and rituximab in treatment-naive WM (November 2025) and Beth Israel Deaconess Medical Center initiating a Phase 2 trial of epcoritamab in previously treated WM (December 2024). With increasing routine use of MYD88 and CXCR4 testing in care pathways, these programs broaden competition beyond covalent BTK monotherapy into combination, immunotherapy, and radiotherapeutic approaches where sequencing and reimbursement differentiation become central.

Recent Industry Developments

- July 2026: Curis, Inc. reported that the FDA lifted a partial clinical hold on its Phase 1/2 TakeAim Lymphoma study evaluating emavusertib in combination with ibrutinib, enabling the company to move back to enrollment activities for cohorts that include Waldenstrom macroglobulinemia. The update restores near-term clinical execution for an IRAK4-pathway strategy that is mechanistically linked to MYD88-driven disease biology.

- June 2025: Cellectar Biosciences announced that the FDA granted Breakthrough Therapy Designation to iopofosine I 131 as a monotherapy approach for relapsed or refractory Waldenstrom macroglobulinemia. The designation increases the intensity of FDA engagement and supports a faster path to a registrational approach for a radiotherapeutic option in a setting with limited alternatives after BTK inhibitor exposure.

- December 2024: Japan's PMDA approved zanubrutinib for Waldenstrom macroglobulinemia, widening access to a selective BTK inhibitor in a major Asia-Pacific market. The approval supported broader formulary adoption and strengthened the global footprint of BTK inhibitor-based WM management.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of therapies and procedures used to treat Waldenstrom macroglobulinemia, counted as revenues linked to patient treatment across key care settings and geographies.

Scope exclusions: We exclude diagnosis-only services, general laboratory testing that is not part of WM treatment delivery, and broader lymphoma spend that cannot be clearly attributed to WM cases.

Segmentation Overview

- By Treatment Class

- BTK Inhibitors

- Proteasome Inhibitors

- BCL-2 Inhibitors

- PI3K/mTOR Inhibitors

- Plasmapheresis

- Chemotherapy & Others

- By Line of Therapy

- First-Line

- Second-Line

- Third-Line & Beyond

- By Healthcare Setting

- Academic Cancer Centres

- Community/Regional Hospitals

- Speciality Clinics

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the disease and treatment context, then to anchor the model with public data series that can be checked and repeated. We referred to sources such as the US National Cancer Institute (SEER), CDC publications, WHO and IARC cancer statistics, and OECD health indicators to understand incidence patterns, diagnosis age bands, and treatment access by region.

Alongside these, we reviewed drug label documents and safety updates from regulators such as the FDA and EMA, plus clinical trial registries and peer-reviewed hematology journals, to map standard regimens and typical treatment sequences. Company filings and investor presentations were also reviewed to interpret therapy focus, geographic mix, and reported demand signals. A paid subscription database for company financials and a patent database were used selectively to support validation of specific assumptions. The desk sources listed here are illustrative only, since many other public and proprietary references were reviewed for data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work focused on validating how WM patients are managed in real settings, including how often active treatment is started versus watchful waiting, and which therapy classes are used by line of therapy. We spoke with clinicians, hospital pharmacy stakeholders, and industry participants across major regions, so assumptions on uptake, duration, and switching could be tightened when desk sources were not specific to WM.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 16% | APAC: 42% |

| Mid tier: 59% | Functional/Unit leaders: 26% | EMEA: 35% |

| Smaller Players: 16% | Managers: 58% | Americas: 23% |

Market-Sizing & Forecasting

Sizing is built using a top-down, patient-pool based demand model where incidence and prevalence signals are translated into an addressable treated population by region, then converted into value using therapy mix and pricing. For WM, the build follows the clinical pathway: diagnosed patients, eligibility for treatment versus monitoring, distribution by line of therapy, and expected duration of use.

Inputs that shift the totals include treated rate (share of diagnosed patients initiating therapy), class mix across BTK inhibitors and other regimens, average duration until switch or discontinuation, setting split across academic centers and community hospitals, and country-level access or reimbursement timing. We then corroborate using selective bottom-up checks, such as sampled regimen cost per month multiplied by estimated treated volumes, plus channel discussions on uptake trends. Gaps are handled by applying conservative proxies from comparable countries with similar care pathways. Forecasts are produced using scenario analysis, where the base case reflects physician-validated adoption curves, expected label expansion effects, and gradual pricing pressure. Sensitivity cases then test faster or slower uptake and changes to treatment duration.

Data Validation & Update Cycle

Validation is done through multiple checks so the final totals do not rely on any single source or assumption. We compare model outputs against independent signals such as incidence trends, therapy class adoption narratives from clinicians, and reported treatment practice changes. Outliers are flagged for rework when country results look inconsistent with access and care setting realities.

Before sign-off, the build is reviewed step by step by another analyst, and key assumptions are rechecked with follow-up outreach when material variance appears. Reports are refreshed annually, with interim updates when major events occur, such as approvals, safety warnings, or meaningful pricing changes. Right before delivery, a fresh data pass is performed so clients receive an updated view based on the latest available information.

Mordor Intelligence's Waldenstrom Macroglobulinemia Market Size Compared Against Other Published Estimates

Published market sizes for WM treatment often vary even when the same disease name is used, because the counted items and the patient pathway assumptions are not always aligned. Differences usually come from what is included as treatment value, how treated patients are defined, and how pricing and duration are rolled forward year to year.

The main gap comes from whether procedure-based components and non-drug treatment steps are counted alongside drug therapy, where Mordor Intelligence includes plasmapheresis within the WM treatment value only when it is used as part of WM management, rather than being counted as general hospital services. Another driver is the treated rate assumption, since some estimates implicitly assume most diagnosed patients are on continuous therapy, while real-world practice includes watchful waiting and stepwise switching by line of therapy. Currency timing and refresh cadence also matter, because small patient populations can look meaningfully different when updated for a new launch, a safety label change, or a country reimbursement expansion.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 188.27 B (2025) | |

| Global Consultancy A | USD 504.00 M (2025) | Uses a drug-only revenue scope and appears to exclude procedure elements and broader care setting spend, and the smaller base suggests a narrower treated population assumption or a limited geography roll-up. |

| Industry Publisher B | USD 2.10 B (2025) | Likely applies broad therapy spend assumptions with simplified patient flow (for example, higher treated share or longer continuous duration), and may not normalize pricing progression and currency conversion consistently across regions. |

The table shows that most of the spread can be explained by scope choices and by how treated patients and duration are converted into yearly value. By keeping the patient pathway explicit and then stress-testing therapy mix, duration, and pricing with real-world feedback, the resulting estimate stays traceable to a small set of clear, repeatable inputs.

Key Questions Answered in the Report

What is the current size and growth outlook for the Waldenström's Macroglobulinemia market?

The Waldenström's Macroglobulinemia market size is USD 188.27 billion in 2026 and is set to grow at a 5.3% CAGR to 2031, reaching USD 256.66 billion.

Which treatments lead adoption in Waldenström's Macroglobulinemia and why?

BTK inhibitors lead with 68.56% treatment-class revenue in 2025, supported by durability and tolerability signals from head-to-head evidence such as the ASPEN trial.

Which regions are expanding fastest for Waldenström's Macroglobulinemia?

Asia-Pacific is the fastest growing region with a projected 6.15% CAGR through 2031, aided by Chinas reimbursement and broader regional access decisions.

What are the key barriers to access in Waldenström's Macroglobulinemia?

High annual therapy costs, reimbursement denials or restrictions, limited specialist availability in low-resource regions, and safety monitoring demands for combination regimens remain the main hurdles.

How is resistance to BTK inhibitors being addressed in Waldenström's Macroglobulinemia?

Non-covalent BTK inhibitors and BTK degraders like NX-5948 retain activity against C481S-mutant disease and are advancing with regulatory support, including FDA Fast Track designation.

Which care settings are shaping patient management in Waldenström's Macroglobulinemia?

Academic centers retain a leading revenue role, while specialty clinics are growing faster due to MRD tools and telemedicine that enable more care to stay local.

Page last updated on: