Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 12.03 Billion |

| Market Size (2026) | USD 12.54 Billion |

| Market Size (2031) | USD 15.39 Billion |

| Growth Rate (2026 - 2031) | 4.20% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Luxury Furniture Market Analysis by Mordor Intelligence

Europe luxury furniture market size in 2026 is estimated at USD 12.54 billion, growing from 2025 value of USD 12.03 billion with 2031 projections showing USD 15.39 billion, growing at 4.2% CAGR over 2026-2031. The market’s expansion is steered by affluent millennials’ growing purchasing power, a durable “home-as-sanctuary” mindset, and continuing migration of high-net-worth individuals into EU capitals[1]Henley & Partners, “WEXIT: Wealthy Brits Exit UK for EU Ahead of Budget,” henleyglobal.com. Robust digital engagement underpinned by 3D configurators, virtual showrooms, and white-glove delivery shortens the consideration cycle for five- and six-figure purchases, stimulating incremental revenue across the luxury furniture market. At the same time, the EU Deforestation Regulation and related due diligence rules push suppliers toward certified inputs, giving first-movers with transparent sourcing a defensible edge. Competitive dynamics remain moderately fragmented; yet merger activity such as Design Holding’s consolidation of Flos and B&B Italia manifests an unmistakable gravitation toward larger portfolios capable of financing omnichannel infrastructure and compliance systems. Key demand clusters remain concentrated in Germany, France, and Italy, but Spain delivers the fastest trajectory as tourism and second-home acquisitions rebound. Opportunistic strategies that fuse circular-economy models with understated “quiet luxury” aesthetics position brands to defend margins and loyalty amid rising operational complexity.

Key Report Takeaways

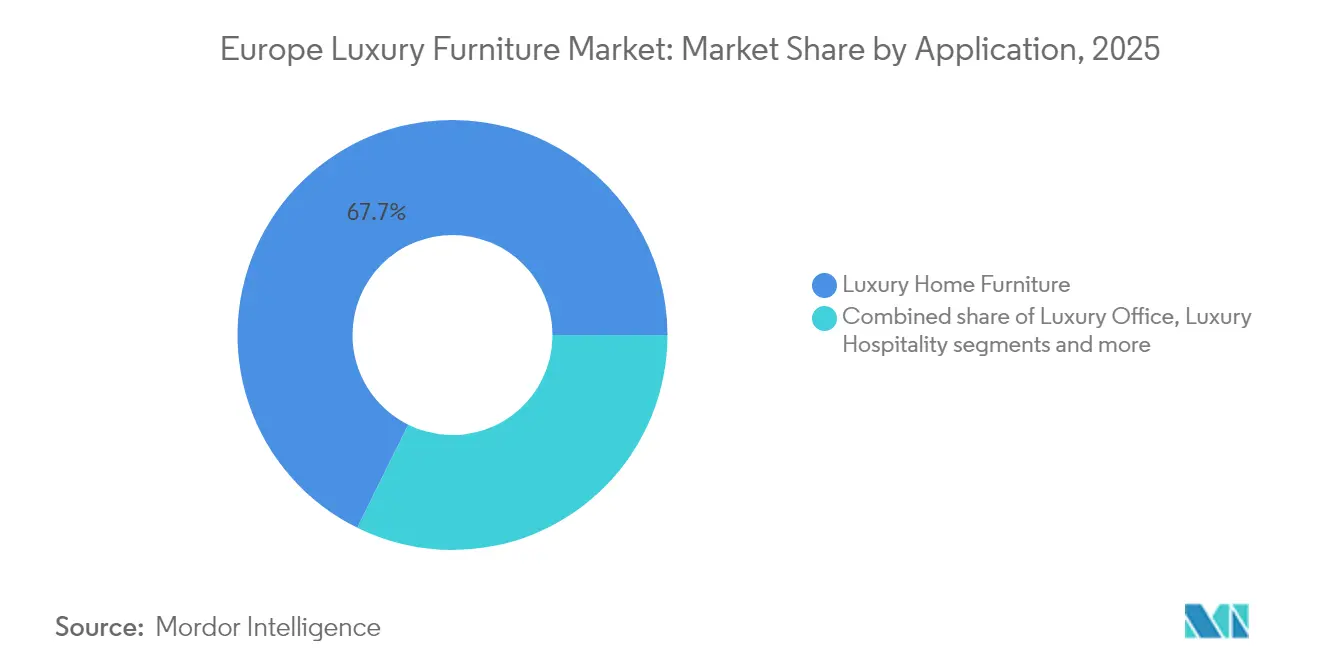

- By application, luxury home furniture held 67.70% of the Europe luxury furniture market share in 2025, while hospitality furniture is projected to advance at a 5.46% CAGR through 2031.

- By material, wood commanded a 42.75% share of the Europe luxury furniture market size in 2025; sustainable and green materials are expected to expand at a 5.85% CAGR between 2026-2031.

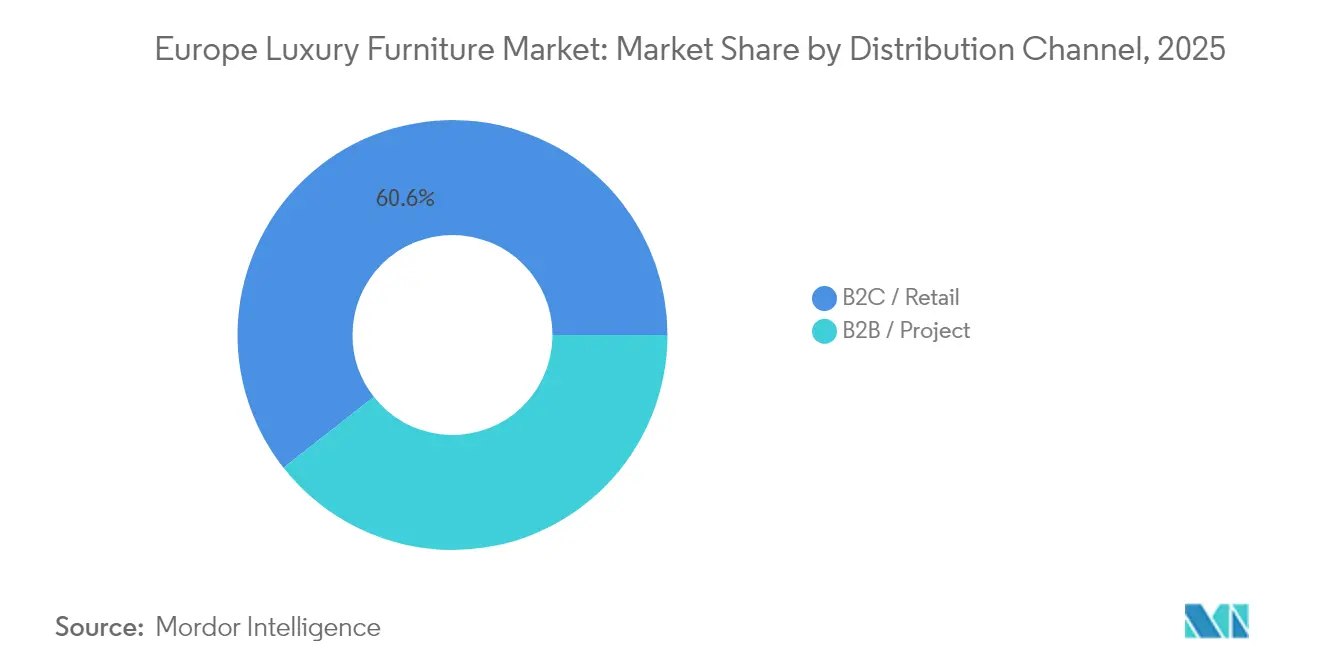

- By distribution channel, B2C retail captured 60.60% share of the Europe luxury furniture market size in 2025 and is set to grow at a 6.10% CAGR to 2031.

- By geography, Germany led with 27.55% revenue share in 2025, whereas Spain is expected to achieve the fastest 5.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Luxury Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising disposable income of affluent millennials | +0.8% | Germany, France, Netherlands, Switzerland | Medium term (2-4 years) |

| Post-pandemic “home as a sanctuary” renovation boom | +1.2% | Germany, UK, France | Short term (≤2 years) |

| Surge in high-net-worth immigration to EU capitals | +0.6% | Germany, France, Italy, Spain, Netherlands | Medium term (2-4 years) |

| Growing e-commerce adoption for high-ticket décor | +0.9% | Germany, Netherlands, Nordics | Long term (≥4 years) |

| Premium demand for “quiet luxury” artisanal pieces | +0.7% | Italy, France, Switzerland, Germany | Long term (≥4 years) |

| Circular-economy certified luxury refurbishment programs | +0.5% | EU-wide | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Disposable Income of Affluent Millennials

Affluent Millennials are now entering the peak household-formation stage, lifting per-capita spending on premium sofas, modular tables, and bespoke cabinetry. Brands report that millennial clients allocate bigger shares of renovation budgets to sustainably sourced, design-led furniture that doubles as a lifestyle statement. Unlike previous generations, these buyers scrutinize transparency credentials—FSC labels, traceable leathers, and carbon disclosures—before committing. Social-media curation accelerates trend adoption as influencers present high-end living spaces, creating copycat demand across the Europe luxury furniture market. Retail conversion data indicate millennials drive more than one-third of omnichannel revenue, validating investments in AR-powered configurators and virtual consultations. This cohort also exhibits higher tolerance for extended lead times if craftsmanship stories resonate, offering cushion to artisans managing limited production runs.

Post-Pandemic “Home as a Sanctuary” Renovation Boom

Remote-work norms remain sticky, anchoring incremental expenditure on home offices, outdoor lounges, and wellness-focused bedroom suites. Consumers channel vacation savings into high-spec renovations, a behavior that persists even after travel restrictions are eased. European builders report that turnkey packages frequently incorporate premium Italian or Spanish furniture brands, boosting factory order backlogs. Secondary markets emerge in countryside estates and alpine chalets, widening the geographic dispersion of demand within the Europe luxury furniture market. Hospitality developers replicate residential aesthetics to justify higher ADR, funneling contract orders toward bespoke pieces. Suppliers hedge renovation-cycle risk by offering modular collections that facilitate later reconfiguration without full replacement, sustaining revenue through accessory sales.

Surge in High-Net-Worth Immigration to EU Capitals

An estimated 9,500 UK-based millionaires plan relocation to EU hubs such as Paris, Milan, and Madrid in 2024, shifting immediate furnishing budgets exceeding USD 300,000 per household. Luxury retailers respond with concierge design teams capable of delivering fully staged properties within 45 days. Interior architects prefer established European brands for rapid compliance with local fire-safety and sustainability codes, enhancing domestic manufacturers’ pipeline visibility. Banking advisers bundle relocation finance with furniture procurement services, embedding convenience and driving volume. This inflow of liquid wealth stabilizes top-line growth even when domestic sentiment softens, buffering cyclical volatility in the Europe luxury furniture market. The trend’s durability hinges on competitive tax regimes; however, Switzerland’s population passing 9 million suggests continued attractiveness of EU residency [2]The Federal Council, “Swiss Resident Population Exceeds 9 Million in 2024,” admin.ch.

Growing E-Commerce Adoption for High-Ticket Décor

Seamless integration of 8K visualization, AI-driven style advisors, and blockchain-verified authenticity is normalizing online purchases above USD 20,000. German platforms record cart-to-checkout rates surpassing 12% when live chat with certified interior designers is available. Hybrid service models deliver physical fabric swatches within 24 hours, countering tactile hesitations without undermining digital convenience. White-glove providers guarantee two-person delivery, assembly, and debris removal, converting logistics into a brand experience that fuels positive reviews [3]Ryder System, “White Glove Delivery,” ryder.com. Data analytics guide localized warehousing to curb last-mile emissions and costs, aligning with ESG mandates. Over time, online performance marketing outpaces print catalog ROI, further tipping budget allocation toward digital in the Europe luxury furniture market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile hardwood & leather input costs | -0.9% | Germany, Italy, France | Short term (≤2 years) |

| Counterfeit designer furniture online | -0.4% | EU-wide | Medium term (2-4 years) |

| Luxury-tax expansion in Southern Europe | -0.6% | Spain, Italy, France | Medium term (2-4 years) |

| High last-mile white-glove logistics costs | -0.7% | Global | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Volatile Hardwood & Leather Input Costs

Market prices for American walnut and European oak jumped 18-24% YOY in 2024 amid supply bottlenecks and phytosanitary restrictions. Italian tanneries also faced bovine-hide shortages, intensifying cost pressure across upholstered categories. Contract pricing lags impede immediate pass-through, eroding EBIT margins by up to 300 basis points for mid-sized manufacturers. Some brands forward-purchase FSC-certified logs and store them for seasoning, but carrying costs strain balance sheets. Alternative materials, engineered veneers, lab-grown leather mitigate exposure yet require investment and consumer education. Elevated costs influence SKU rationalization, nudging makers to trim fringe colorways and focus on volume drivers within the Europe luxury furniture market.

Luxury-Tax Expansion in Southern Europe

Fiscal pressures spur Spain and Italy to contemplate broader luxury levies, including higher transfer taxes on prime real estate and potential surcharges on premium interiors[4]Livingstone Estates, “Spain Property Tax Could Impact Non-EU Buyers in 2025,” livingstone-estates.com. Early drafts exempt sustainable products, but uncertainty already delays some overseas purchases. Developers hedge by bundling furniture into overall property pricing, seeking to reduce separate tax exposure. Luxury brands intensify outreach in tax-neutral hubs such as Monaco and Andorra, redistributing marketing spend. A two-tier demand profile emerges: domestic buyers postpone, while foreign ultra-high-net-worth individuals absorb extra cost. Policy clarity will shape whether near-term softness morphs into structural restraint for the Europe luxury furniture market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Residential Dominance and Hospitality Tailwind

Europe's luxury furniture market size for home application stood at USD 8.14 billion in 2025, equal to 67.70% share, driven by persistent home-improvement cycles. Living-room seating commands the highest value, buoyed by modular sectional designs that accommodate flexible layouts. Dining sets featuring extendable mechanisms satisfy hybrid entertainment preferences, while premium wardrobes integrate IoT humidity control to protect couture garments. Luxury kitchen cabinetry shows 14% YOY growth as cooking remains a lifestyle hobby among affluent households. Importantly, resale values of branded pieces sustain high upgrade frequency; auction data reveal some limited-edition sofas retain 85% of original retail after five years, strengthening perception of furniture as a capital asset inside the Europe luxury furniture market.

Hospitality furniture is projected to grow at a 5.46% CAGR, widening its 2025 base of USD 1.34 billion as RevPAR in Europe capitals rebounds and pipeline additions accelerate. Operators of boutique hotels demand residential-grade comfort, commissioning bespoke headboards, marble-clad nightstands, and sustainably sourced lounge chairs to differentiate. Procurement cycles compress as design-and-build firms rely on digital libraries for faster approval, favoring suppliers with robust BIM resources. Restoration projects, such as The Dylan Amsterdam’s phased upgrade, illustrate multi-year revenue streams where suppliers refresh suites in rotations, ensuring steady order visibility. Cruise-ship refurbishment and luxury senior living complexes add adjacency opportunities, further diversifying the Europe luxury furniture market.

By Material: Wood Heritage and Sustainable Innovation

Wood retained 42.75% of Europe's luxury furniture market share in 2025, underpinned by continental reverence for natural patina and tactile warmth. German studios highlight end-grain joinery and hand-rubbed oil finishes that accentuate walnut grain, communications that resonate with collectors. Scandinavian brands popularize ash and birch variants treated with water-based lacquers, appealing to eco-minded buyers. Supply-chain transparency—chain-of-custody certificates, GPS-tagged logging sites—now features prominently in marketing collateral, turning compliance into storytelling. Cross-material integrations—wood with brushed brass caps or smoked-glass inlays—extend design vocabulary, sustaining relevance across style cycles.

Sustainable and green materials, though only 9.95% share, pursue a 5.85% CAGR led by recycled plastics and plant-based resins in structural frames. Mater’s “Waste Craft” collection transforms industrial offcuts into terrazzo-style table surfaces that meet scratch-resistance specs while reducing embodied carbon by 30%. Bio-leather derived from mycelium gains traction for headboards and wall panels after passing flammability tests. Circular composites allow disassembly at the component level, facilitating end-of-life recycling and aligning with EU Ecodesign rules effective 2027. Early adoption unlocks BREEAM credits, positioning products for commercial projects seeking green-building certification and propelling volume within the Europe luxury furniture market.

By Distribution Channel: Omnichannel Retail Supremacy

B2C retail captured 60.60% of the Europe luxury furniture market size in 2025, reflecting consumer preference for brand-controlled experiences. Flagship stores now incorporate maker studios where artisans demonstrate joinery or leather tooling, deepening shopper immersion. Digital augmentation—handheld tablets offering AR placement views—shortens decision cycles on the showroom floor. Brands monetize data from loyalty apps to push personalized after-sales offers such as care-kit subscriptions and matching accessories. High-street rents in Tier 1 cities remain elevated, but incremental revenue from experiential events recoups costs, displaying the resilience of brick-and-mortar in an omnichannel paradigm.

E-commerce underpins the channel’s 6.10% CAGR, with average order values above USD 7,500 on desktop and USD 5,800 on mobile. Return rates stay below 2% due to accurate dimensional visualizations, far outperforming mass-furniture averages. Retailers pilot remote virtual-reality trunk shows that stream directly from Milan Design Week, letting VIP clients book limited editions instantly. Project-based B2B remains relevant; hospitality buyers value factory tours and prototyping labs that reassure on durability standards. Yet B2B digital portals emerge, allowing architects to configure volume orders and track production milestones, a capability that promises future share gains in the Europe luxury furniture market.

Geography Analysis

Germany held 27.55% of Europe's luxury furniture market share in 2025. The market benefits from robust household wealth median net assets exceeding USD 250,000, and cultural appreciation of engineered craftsmanship. Domestic manufacturers exploit Industry 4.0 facilities that enable mass-customization without compromising artisanal detailing, shortening lead times to six weeks versus the nine-week European average. Federal subsidies for energy-efficient refurbishments further stimulate premium window seats, built-in libraries, and custom cabinetry demand. ESG-driven consumers reward brands that publish life-cycle assessments, evidenced by a 20% sales uplift for ranges carrying PEFC certifications.

France also holds a significant position, anchored by Parisian residential refurbishments where turnkey interior packages command USD 1,000 per square foot. Luxury apartments in the Golden Triangle increasingly come pre-furnished to expedite occupancy, simplifying procurement for overseas buyers. Provincial châteaux conversions into boutique hotels spur contract orders for reproduction Louis XVI case goods blended with contemporary upholstery. The French luxury furniture sector leverages fashion-house adjacency Hermès, Dior to co-launch home lines, creating cross-category halo effects within the Europe luxury furniture market.

Italy effortlessly marries heritage ateliers with design-led industrial producers concentrated in Brianza and Veneto. Milan Design Week 2025 drew record footfall, with export orders up 11% YOY as international specifiers sought authentic “Made in Italy” provenance. Tax incentives on energy-efficient home upgrades and a cultural predisposition for family heirlooms to buy domestic demand. Italian firms double down on vertical integration from sawmills to showrooms, insulating margins against raw-material volatility. Partnerships with automotive marque Maserati underscore lifestyle convergence that propagates Italian influence across the Europe luxury furniture market.

Spain rises fastest and is projected to post a 5.05% CAGR to 2031. Luxury coastal developments in Marbella and Ibiza specify turnkey interiors before title transfer, accelerating demand bursts. Proposed 100% property taxes on non-EU buyers triggered lobbying that led to moderated thresholds, reducing immediate risk yet leaving investors cautious. Still, robust tourism recovery, foreign arrivals surpassed 93 million in 2024, drives hospitality refurbishments that prioritize locally sourced, sustainable timber to meet Balearic environmental mandates. Catalonian upholstery clusters capitalize on shorter lead times to service both domestic and French buyers, reinforcing Spain’s strategic role inside the Europe luxury furniture market.

Competitive Landscape

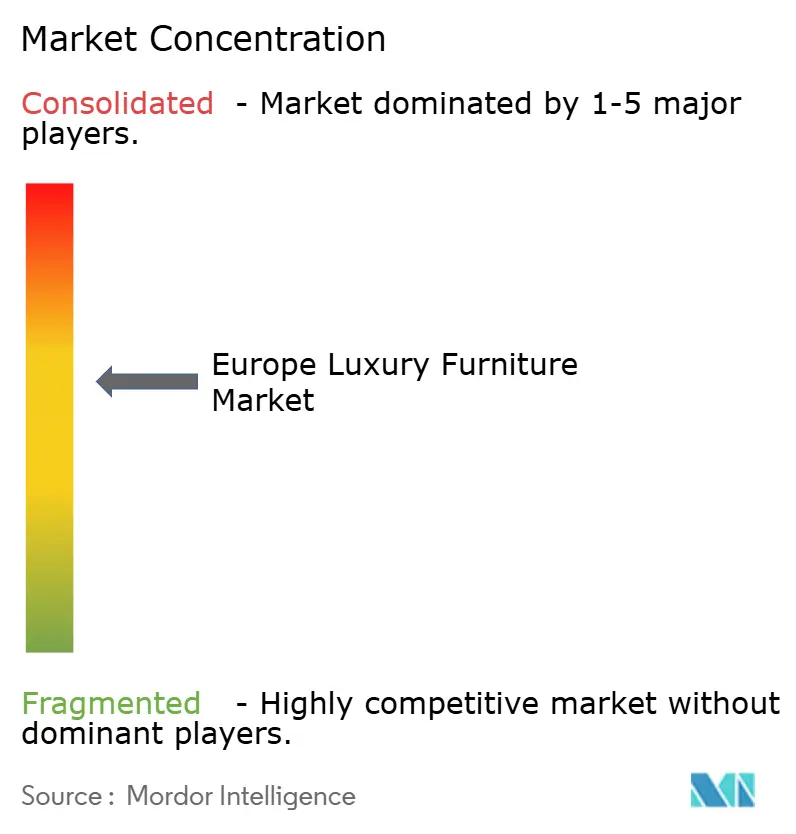

Europe's luxury furniture market, while moderately fragmented, is witnessing a surge in consolidation, driven by both private-equity and strategic acquisitions. Design Holding’s rebranding to Flos B&B Italia Group seamlessly merges lighting and furniture, capitalizing on cross-selling opportunities and streamlining the procurement of premium metals. This strategic move has resulted in an 80 basis point reduction in material costs. Meanwhile, Minotti, Poltrona Frau, and Molteni are rolling out mono-brand flagships in global hotspots like Miami, Shanghai, and Dubai, bolstering their order pipelines and mitigating European macroeconomic risks. In a bold move, private equity firm Trilantic Europe has taken a majority stake in Sklum, aiming to expand its digitally native model beyond Spain. They have also invested in a sprawling 160,000 m² logistics hub, poised to slash shipping times by 40%.

In the digital realm, Vitra and Walter Knoll are pioneering investments in VR and NFT authentication. This innovation allows customers to register ownership on the blockchain, facilitating rights transfer during resale and acting as a deterrent against counterfeiting. Sustainability is a key focus: Mater and TAKT's cradle-to-cradle assessments are drawing in institutional buyers keen on reducing scope-3 emissions. Artisanal studios like Giorgetti are blending tradition with technology, preserving hand-finished details while adopting CNC milling for structural components. The competition is heating up in the circular niche, with refurbished lines now accounting for up to 25% of total revenue for leading brands.

Strategic partnerships are amplifying brand equity: Giorgetti collaborates with Maserati for a bespoke Grecale interior kit, and Flokk's acquisition of U.S. office-furniture maker Stylex bolsters its contract capabilities. Fashion and furniture are increasingly intertwined; Trussardi Casa, rejuvenated by Miroglio Group, is harmonizing its collections with apparel color palettes for enhanced merchandising. However, as EU regulatory compliance tightens, mandating audited chain-of-custody and CSRD reporting, smaller workshops may find the costs burdensome. It could lead to a market shake-out, potentially elevating the concentration score of Europe's luxury furniture market over time.

Europe Luxury Furniture Industry Leaders

Roche Bobois

Poltrona Frau

B&B Italia

Minotti

Ligne Roset

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Miroglio Group completed its acquisition of Trussardi, emphasizing Trussardi Casa as a strategic growth pillar. Plans include a Dubai high-rise partnership with Luxury Living Group, supplying turnkey furnishings that blend Italian craftsmanship with Middle-Eastern design cues. The initiative targets USD 120 million in incremental home-segment revenue over five years.

- April 2025: Poltrona Frau opened a permanent display at Kyoto Takashimaya department store through Otsuka Furniture. The installation marks the Italian brand’s first Japanese shop-in-shop, featuring best-selling Archibald chairs and leveraging Japan’s high appreciation for leather artistry to expand Asia-Pacific share.

- January 2025: Flokk acquired U.S. office-furniture specialist Stylex. The transaction grants Flokk immediate manufacturing presence in North America, enabling faster lead times for executive seating programs and cushioning currency volatility exposure.

- January 2024: TAKT expanded its EU Ecolabel-certified range with new FSC-certified oak dining sets. A branded take-back program accompanies each sale, guaranteeing refurbishment or recycling after 10 years of ownership. Early adopters include Copenhagen’s Noma, lending culinary prestige to the collection.

Europe Luxury Furniture Market Report Scope

Luxury furniture is conducive to sumptuous living and includes elements that are elegant, sumptuous, and indulgent.

The Europe luxury furniture market is segmented by product type, end-user, distribution channel, and geography. By product type, the market is sub-segmented into lighting, tables, chairs, and sofas, accessories, bedrooms, cabinets, and other product types. By end-user, the market is sub-segmented into residential and commercial. The distribution channel of the market is sub-segmented into home centers, flagship stores, specialty stores, online, and other distribution channels. Geography the market is sub-segmented into Germany, the United Kingdom, France, Spain, Russia, Italy, and the rest of Europe. The report offers market size and forecasts for the Europe luxury furniture market in value (USD) for all the above segments.

By Application

| Luxury Home Furniture | Chairs and Sofas |

| Tables (Side, Coffee, Dressing, etc.) | |

| Beds | |

| Wardrobes | |

| Dining Tables / Dining Sets | |

| Kitchen Cabinets | |

| Other Home Furniture (Bathroom, Outdoor, etc.) | |

| Luxury Office Furniture | Chairs |

| Tables | |

| Storage Cabinets | |

| Desks | |

| Sofas and Other Soft Seating | |

| Other Office Furniture | |

| Luxury Hospitality Furniture | |

| Other Applications (Educational, Healthcare, Retail Malls, Government Offices, etc.) |

By Material

| Wood |

| Metal |

| Glass |

| Leather |

| Plastic and Other Synthetics |

| Sustainable / Green Materials |

By Distribution Channel

| B2C / Retail | Home Centers |

| Specialty Furniture Stores | |

| Online Flagship Store | |

| Other Distribution Channels | |

| B2B / Project |

By Geography

| Germany |

| France |

| United Kingdom |

| Italy |

| Spain |

| Netherlands |

| Belgium |

| Switzerland |

| Nordics |

| Rest of Europe |

| By Application | Luxury Home Furniture | Chairs and Sofas |

| Tables (Side, Coffee, Dressing, etc.) | ||

| Beds | ||

| Wardrobes | ||

| Dining Tables / Dining Sets | ||

| Kitchen Cabinets | ||

| Other Home Furniture (Bathroom, Outdoor, etc.) | ||

| Luxury Office Furniture | Chairs | |

| Tables | ||

| Storage Cabinets | ||

| Desks | ||

| Sofas and Other Soft Seating | ||

| Other Office Furniture | ||

| Luxury Hospitality Furniture | ||

| Other Applications (Educational, Healthcare, Retail Malls, Government Offices, etc.) | ||

| By Material | Wood | |

| Metal | ||

| Glass | ||

| Leather | ||

| Plastic and Other Synthetics | ||

| Sustainable / Green Materials | ||

| By Distribution Channel | B2C / Retail | Home Centers |

| Specialty Furniture Stores | ||

| Online Flagship Store | ||

| Other Distribution Channels | ||

| B2B / Project | ||

| By Geography | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Belgium | ||

| Switzerland | ||

| Nordics | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the 2026 value of the European luxury furniture market?

The market stands at USD 12.54 billion in 2026.

How fast will the European luxury furniture market grow through 2031?

It is projected to record a 4.20% CAGR, reaching USD 15.39 billion.

Which application dominates spending?

Luxury home furniture leads with 67.70% share in 2025.

Which geography grows fastest?

Spain, at a projected 5.05% CAGR between 2026-2031.

What material segment is expanding quickest?

Sustainable and green materials, set for a 5.85% CAGR.

Which channel shows top growth?

B2C retail is poised for a 6.10% CAGR as omnichannel models mature.

Page last updated on: