Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

Low Light Imaging Market is Segmented by Sensor Technology (CCD, Front-Illuminated CMOS, and More), Spectral Range (Visible, Near-Infrared, and More), Application (Scientific and Industrial Imaging, Medical and Life-Sciences Imaging, and More), Imaging Device Type (Image Sensors, Camera Modules, and More), End-User Industry (Consumer Electronics, Automotive, and More), and Geography.

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

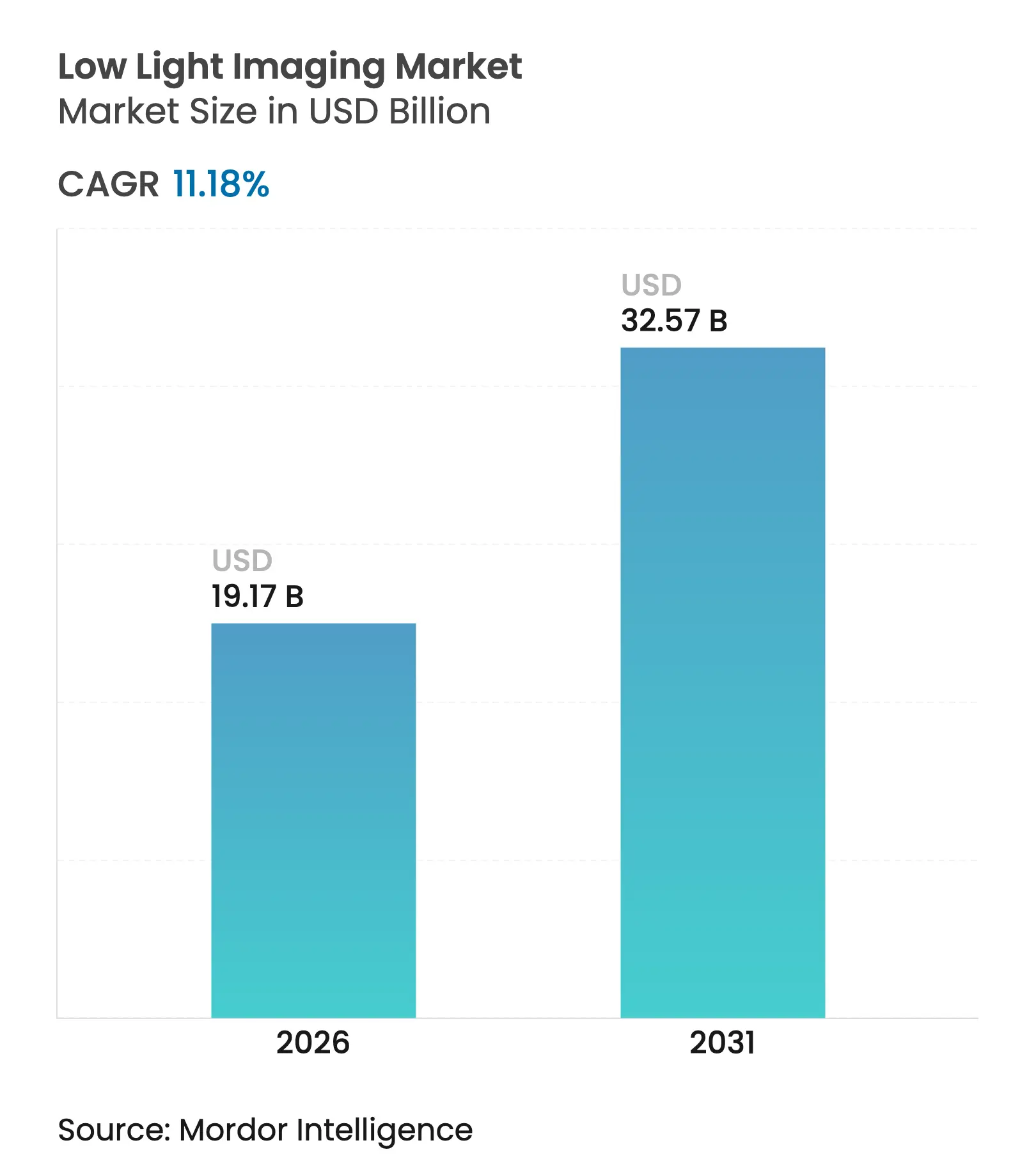

| Market Size (2026) | USD 19.17 Billion |

| Market Size (2031) | USD 32.57 Billion |

| Growth Rate (2026 - 2031) | 11.18 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The Low Light Imaging market size is expected to grow from USD 17.24 billion in 2025 to USD 19.17 billion in 2026 and is forecast to reach USD 32.57 billion by 2031 at 11.18% CAGR over 2026-2031. The present growth trajectory is being propelled by mass-market smartphone adoption of professional-grade night photography, escalating safety requirements for L2+ autonomous vehicles, and continuous upgrades to security infrastructure across emerging economies. Sensor makers have lowered the cost-performance barrier through novel backside-illuminated and stacked CMOS architectures, while software-defined imaging pipelines allow handset vendors to deliver brighter images without enlarging sensor footprints. Automotive original equipment manufacturers are standardizing 24/7 vision capabilities, which amplifies demand for sensors with very high dynamic range and fast global shutters. Rising material prices for sub-2 nm wafers nonetheless pose short-term cost pressure, but multi-regional fab investments signal eventual supply relief. As a result, the low-light imaging market continues to migrate from discrete hardware competition to integrated hardware-software solutions that unlock higher margins and expand addressable use cases.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Smartphone-centric low-light photography boom

Smartphone-centric low-light photography boom

| +2.8% | Global, with APAC leading adoption | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+2.8%

|

Geographic Relevance

:

Global, with APAC leading adoption

|

Impact Timeline

:

Medium term (2-4 years)

|

Advances in BSI-CMOS and stacked sensor architecture

Advances in BSI-CMOS and stacked sensor architecture

| +2.1% | North America and Asia-Pacific core markets | Long term (≥ 4 years) | |||

AI-powered computational imaging pipelines

AI-powered computational imaging pipelines

| +1.9% | Global, concentrated in tech hubs | Medium term (2-4 years) | |||

Security and surveillance demand for 24×7 vision

Security and surveillance demand for 24×7 vision

| +1.7% | Global, with MEA and APAC acceleration | Short term (≤ 2 years) | |||

Low-light imaging for L2+ autonomous vehicles

Low-light imaging for L2+ autonomous vehicles

| +1.5% | North America, Europe, China | Long term (≥ 4 years) | |||

Dawn/Dusk agritech drone analytics

Dawn/Dusk agritech drone analytics

| +1.0% | Global agricultural regions | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Smartphone-centric Low-Light Photography Boom

Night-mode photos have become a decisive purchase criterion for mid- and high-tier smartphones. Samsung’s 200 MP ISOCELL HP9 telephoto sensor employs a new microlens stack that channels more photons per pixel, lifting signal-to-noise ratios when ambient light is below 5 lux.[1]Samsung Electronics, “Samsung Unveils Versatile Image Sensors for Superior Smartphone Photography,” news.samsung.com Sony followed with its LYT-818 that lowers random noise to 0.95 e-, signaling a pivot from megapixel races to quantum efficiency improvements. Content-centric social networks intensify this arms race because users share low-light images in real time. OmniVision’s 50 MP mobile sensor that marries Quad-Phase Detection autofocus and backside illumination shows that competitive differentiation is spreading to upper-mid-range price points. Consequently, the low light imaging market gains volume leverage that offsets some wafer cost inflation.

Advances in BSI-CMOS and Stacked Sensor Architecture

Back-illuminated CMOS has been mainstream for more than a decade, yet recent iterations focus on three-dimensional stacking that layers photodiodes, logic, and memory to shorten signal paths and raise full-well capacity.[2]Photonics Media, “3D-Stacked CMOS Sparks Imaging's Innovation Era,” photonics.comSouth Korean researchers raised responsivity to 0.29 A/W using CBIC electrode materials, extending dynamic range to 122 dB without external cooling. Sony’s IMX925 industrial sensor integrates global shutter in a stacked format and outputs 394 fps, demonstrating performance potential for robotics and quality inspection. Nikon’s partially stacked full-frame chip in the Z6 III reinforces that hybrid stacking scales into professional cameras. These breakthroughs alter product road-maps across the low light imaging market.

AI-Powered Computational Imaging Pipelines

Image capture is shifting from purely photonic constraints to algorithmic optimization. Prophesee’s Metavision de-blur engine, optimized for Snapdragon 8 Gen 3, fuses event-based frame data to remove motion smear in sub-30 lux scenes. Tsinghua University’s Tianmouc chip reaches 10,000 fps while compressing bandwidth by 90%, enabling low-latency decision making in autonomous drones.[3]Paul Marks, “Cutting-Edge Vision Chip Brings Human Eye-Like Perception to Machines,” techxplore.com A neuromorphic exposure controller from the University of Hong Kong boosts daytime driving object detection accuracy by 47.3% through millisecond-level exposure adjustments. These innovations lower reliance on large sensors, which in turn influences bill-of-materials strategies across the low light imaging market.

Security and Surveillance Demand for 24×7 Vision

Urbanization and evolving threat vectors keep municipal and enterprise buyers focused on cameras that deliver full-color footage at night. Hikvision’s DarkFighter 2.0 merges ƒ/1.0 optics with deep-learning analytics for object classification in sub-1 lux scenes. KingRay introduced a full-color night-vision sensor for AI patrol robots that retain chromatic accuracy to 0.002 lux, broadening deployment beyond fixed installations. IronYun and NVIDIA have demonstrated generative AI applications that enrich forensic search accuracy amid sparse lighting, decreasing operator workload ipvm.com. Large-aperture CMOS cameras providing 24/7 color streams are becoming baseline specifications for public-area surveillance.[4]LTS Security, “Color 24/7 Key Technologies,” ltsecurityinc.com Security upgrades therefore continue to anchor volumes within the low light imaging market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising cost of next-gen image sensors Rising cost of next-gen image sensors | -1.8% | Global, with premium segment concentration | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-1.8% | Geographic Relevance:Global, with premium segment concentration | Impact Timeline:Short term (≤ 2 years) |

Semiconductor supply-chain bottlenecks Semiconductor supply-chain bottlenecks | -1.2% | Global, with Asia-Pacific manufacturing focus | Medium term (2-4 years) | |||

Thermal-noise floor limits in uncooled designs Thermal-noise floor limits in uncooled designs | -0.9% | High-performance applications globally | Long term (≥ 4 years) | |||

Privacy and regulatory pushback on night monitoring Privacy and regulatory pushback on night monitoring | -0.7% | Europe, North America regulatory focus | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Cost of Next-Gen Image Sensors

Wafers processed at 1.4 nm are expected to carry a USD 45,000 price tag by 2028, 50% higher than today’s 2 nm runs. Capital outlays remain high; Sony alone invested USD 10 billion in sensor lines over six years. Although Japan’s chipmaker consortium plans USD 31 billion in new capacity by 2029, near-term price rises squeeze mass-market handset margins and delay camera upgrades in budget segments of the low-light imaging market.

Semiconductor Supply-Chain Bottlenecks

The production network remains geographically concentrated. Toppan relocated critical filter production to China to lift local output by 40%. Analysts forecast normalization by early 2025, yet geopolitical friction and mature-node backlogs keep lead times volatile. Automotive OEMs hedge by dual-sourcing; Onsemi pairs captive fabs with foundry partners to buffer EyeSight sensor demand. Such diversification partially protects the low-light imaging market, yet raises inventory costs.

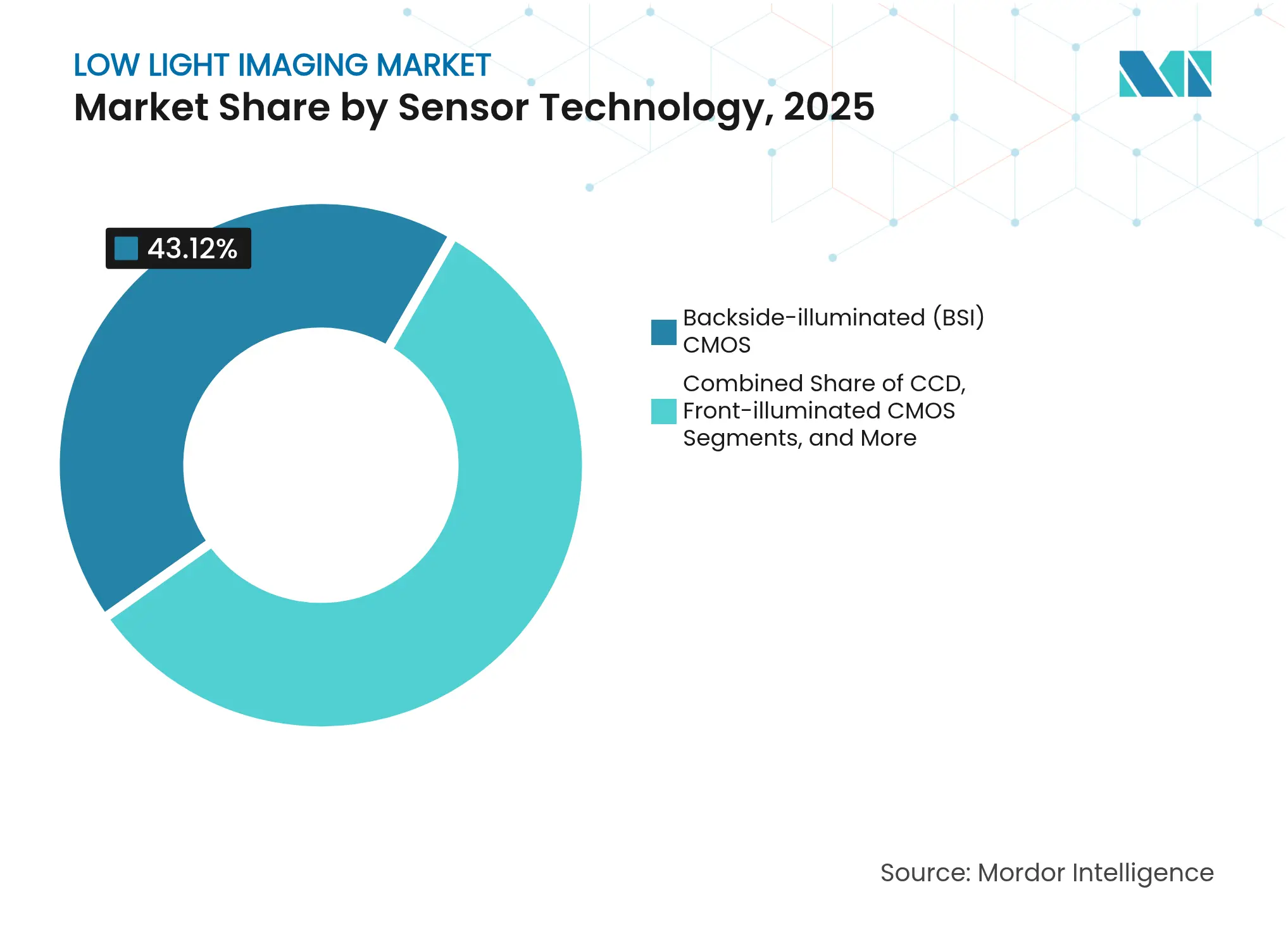

By Sensor Technology: Stacked CMOS Redefines Premium Performance

Backside-illuminated CMOS held 43.12% of 2025 revenues in the low light imaging market. Manufacturers favor the architecture because it lifts photon absorption and is well tuned for high-volume mobile production. Stacked CMOS, however, is forecast to deliver a 12.28% CAGR through 2031 thanks to its ability to place photodiodes, ADCs, and memory on separate tiers. This inherently shortens interconnects and boosts frame rates for fast-moving scenes. The IMX925 global-shutter sensor illustrates the added value in industrial robotics, while Nikon’s partially stacked full-frame sensor signals broader uptake in professional cameras. As stacking yields improve, conventional BSI may gradually migrate to price-sensitive tiers. The transition underscores how the low light imaging market now prizes integration density and on-chip processing more than pixel count.

Market participants reinforce the trend. Sony’s Pregius S technology combines stacked CMOS with a global shutter that achieves 24.55 MP at 394 fps, aligning with factory automation needs. Korea’s CBIC electrode innovation shows stacked approaches remain materials intensive, but performance won out as markets demanded sub-2 e- noise floors. Over the forecast horizon stacked architectures are likely to claim half of premium handset contracts, yet BSI CMOS remains essential for unit-driven segments. Consequently, vendors must balance dual road-maps to cover divergent price bands within the low light imaging market.

Note: Segment shares of all individual segments available upon report purchase

By Spectral Range: SWIR Demand Builds Beyond Niche Status

Visible-band sensors constituted 44.32% of 2025 shipments. Smartphones, notebooks, and mainstream surveillance continue to rely on this range because displays and analytics are optimized for RGB content. Short-wave infrared, while accounting for a single-digit share, is projected to rise at a 12.57% CAGR. Industrial machine-vision systems adopt SWIR to inspect moisture and polymer compositions, and militaries seek broader situational awareness under obscurants. Lynred’s acquisition of New Imaging Technologies underscores this pivot to commercial SWIR cameras. Quantum dot photodetectors have already extended the cut-off wavelength to 18 µm, creating a future path for very long wave applications. By 2030, SWIR modules are expected to penetrate smart agriculture and medical endoscopy, adding incremental volume to the low-light imaging market.

Near-infrared remains integral to automotive driver-monitoring systems and smartphone face unlock, while LWIR retains a specialized role in defense thermography. Vendors that combine visible and NIR sensitivity in single pixels can sell multipurpose devices that lower the bill-of-materials for smart home cameras. Spectral diversification, hence, becomes a strategic hedge for suppliers confronting consumer cycles in the low-light imaging industry.

By Application: Space and Astronomy Register the Highest Trajectory

Security and surveillance drew 36.74% of 2025 spending. Large city-wide camera roll-outs and AI-enabled video analytics generate repeat sensor demand. Yet space and astronomy applications are poised to climb at a 12.88% CAGR. NASA has demonstrated superconducting detectors with sub-0.3 e noise, and wide-field slitless spectrometers address exoplanet surveys that need high sensitivity above Earth’s atmosphere. Commercial entities aiming at earth-observation constellations prefer CMOS over CCD for radiation tolerance and faster readout. Scientific and industrial imaging follows with steady replacement cycles in semiconductor inspection and materials research. Medical and life-science labs continue adopting NIR and fluorescence imaging for real-time surgical guidance. These varied demands collectively widen the total low-light imaging market size.

The heightened interest in space pushes suppliers to develop radiation-hardened, ultralow-noise sensors. Meanwhile, smartphone makers tap the same quantum-efficiency improvements to wow consumers with astrophotography modes, demonstrating cross-pollination of technologies. As a result, the low light imaging market benefits from a virtuous innovation loop across disparate verticals.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

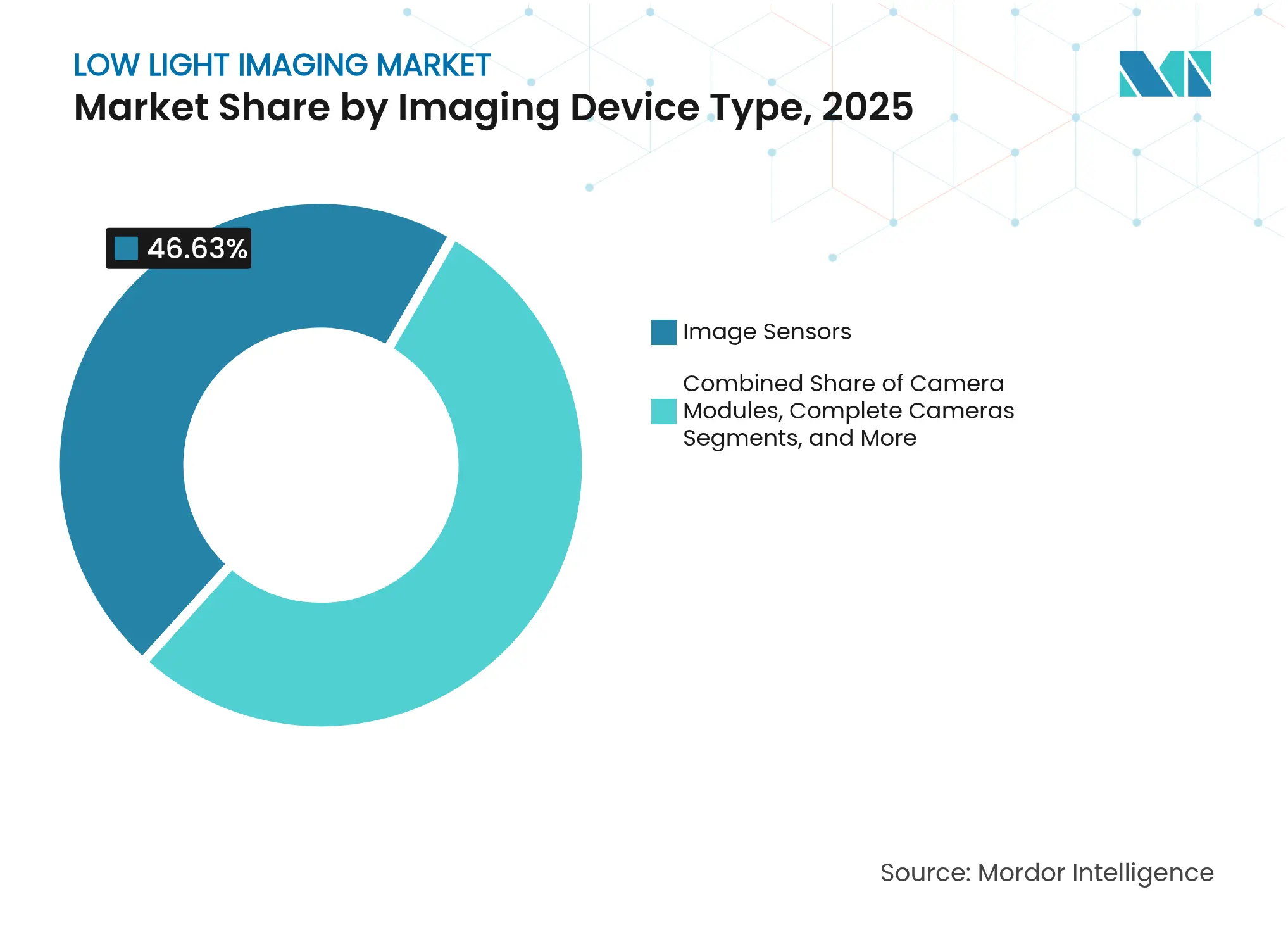

By Imaging Device Type: Camera Modules Outpace Discrete Sensors

Image sensors retained 46.63% of 2025 revenue because every downstream module requires a die. Yet fully integrated camera modules are forecast to expand at a 12.98% CAGR. Smartphone OEMs demand turnkey modules containing wafer-level optics, actuators, and emerging AI co-processors to shorten design cycles. OmniVision’s 1-inch sensor with 18-stop dynamic range ships inside reference camera modules for flagship handsets. Teledyne e2v and Airy3D collaborated to embed 3D depth mapping within a 2 MP global-shutter design, proving that value shifts to in-package functionality. AR/VR devices will further push for flexible interconnect tapes as described in Meta’s recent patent filings. Consequently, module assemblers gain bargaining power in the low-light imaging market while pure-play die vendors must co-innovate or risk commoditization.

Complete cameras still matter in scientific, cinematic, and machine-vision niches that require bespoke optics. Accessories such as illuminators, liquid lenses, and spectral filters create ancillary revenue but are vulnerable to vertical integration by module vendors. To stay competitive, component suppliers add unique coatings or AI algorithms that clip directly onto the module pipeline. This symbiotic evolution underpins broader ecosystem growth for the low-light imaging market.

Note: Segment shares of all individual segments available upon report purchase

By End-User Industry: Automotive Becomes the Prime Growth Engine

Smartphones, smart speakers, and webcams allowed consumer electronics to keep a 48.45% share in 2025, yet CAGR slows as replacement cycles lengthen. Automotive sensors, in contrast, are set to grow 13.53% annually because each electric vehicle now integrates exterior ADAS cameras, driver monitoring, and occupancy sensing. Sony projects eight cameras per vehicle by 2025 and up to twelve by 2028. Subaru chose Onsemi’s Hyperlux sensor for its next-generation EyeSight system, citing 140 dB dynamic range as critical for dusk driving. Health monitoring adds further content as OmniVision and Philips integrate pulse and respiration analytics with single NIR imagers. Military and defense budgets drive upgrades to low-light targeting pods and handheld goggles, while industrial machine vision automates dark warehouses. The diversity of use cases ensures sustained demand curves across the low-light imaging market.

Commercial vehicles also contribute incremental sensor attach rates because regulation now requires blind-spot cameras. Agriculture drones fly pre-dawn to monitor crop stress using NIR indices, adding another automotive-adjacent channel. The evolution from utility to intelligence cements imaging as a central component in mobility platforms, reinforcing the structural growth of the low-light imaging market.

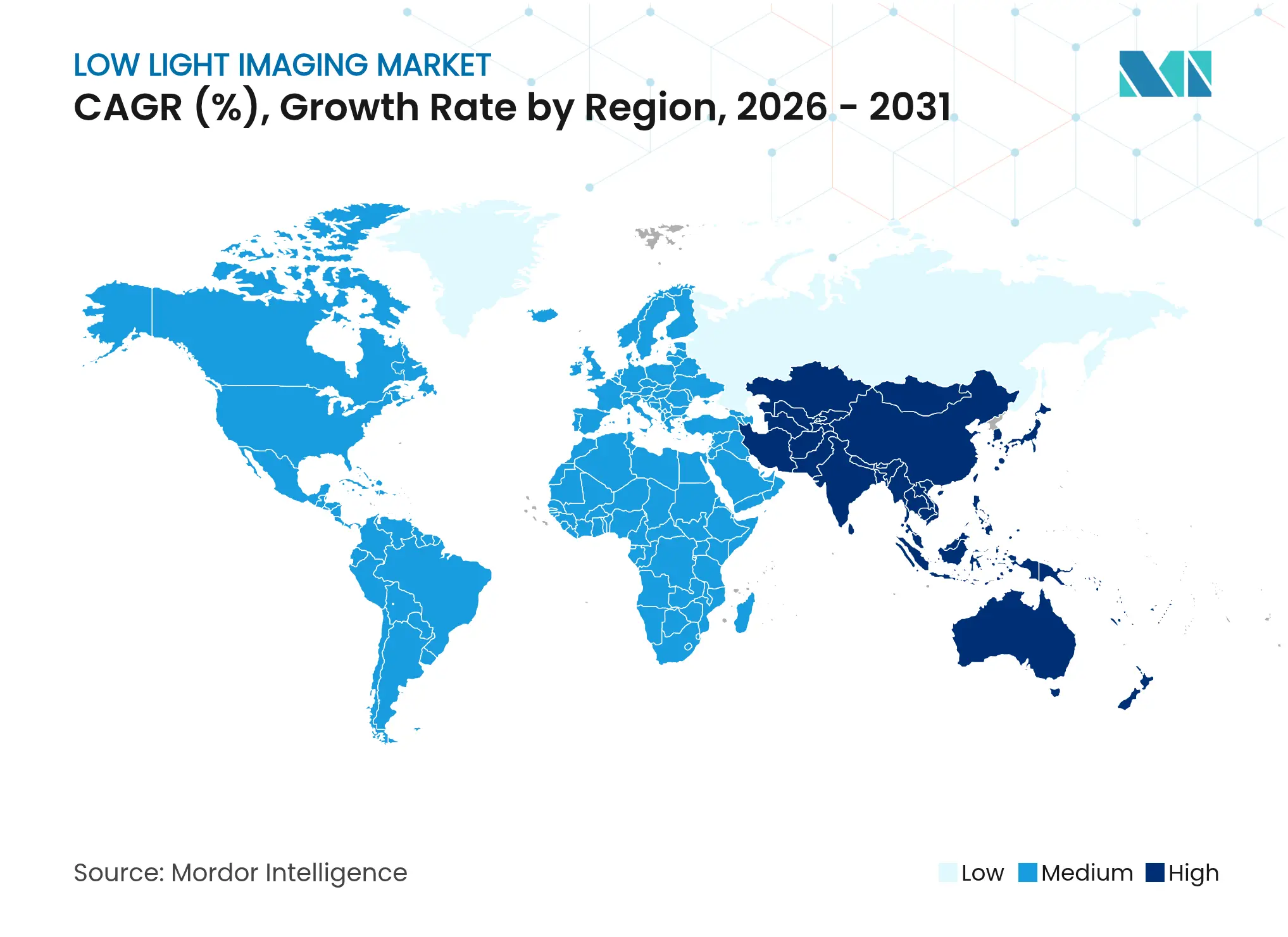

Asia-Pacific commanded 41.05% of 2025 revenue owing to integrated semiconductor supply chains, government incentives, and a massive installed base of smartphone users. China’s domestic dynamic-visual-sensor sector lists players such as Sony, Prophesee, and Hillhouse Technology, collectively amplifying local competition. Japanese and Korean firms keynote the premium tier; Sony collaborated with Samsung on automotive chips to safeguard capacity allocation. Taiwan’s foundries expand 12-inch wafer lines to support stacked CMOS nodes, ensuring ecosystem resilience despite global fab shortages. As 5G coverage surpasses 80% of APAC’s urban population, consumers live-stream low-light video and reinforce regional sensor demand.

North America trails Asia-Pacific in volume yet leads technology adoption in autonomous vehicles and defense. California startup ecosystems commercialize neuromorphic and event-based sensors, attracting investment flows that feed next-generation architecture experiments. Federal funding for smart-city pilots stimulates procurement of AI-enhanced surveillance cameras across transit hubs, augmenting sales across the low-light imaging market. Europe balances stringent privacy regulation with the push for safer roadways. Euro NCAP’s 2026 standards require advanced night-time pedestrian detection, accelerating camera upgrades within German premium OEMs. The Middle East modernizes infrastructure for mega-projects and adopts 24/7 video analytics for stadium and airport security. South America experiences a gradual uptake tied to industrial automation and expanding e-commerce logistics.

Currency fluctuations play a secondary role. Yen weakness benefits Japanese exporters, whereas strengthening the yen compresses Korean margins. Trade policy also shapes supply; export controls on advanced lithography equipment compel Chinese sensor fabs to focus on mature nodes, leaving premium segments open to foreign suppliers. Over the forecast horizon, Asia-Pacific remains the manufacturing hub and largest end-market, while regulatory mandates make Europe and North America strategic in premium automotive and security verticals. These regional dynamics ensure balanced expansion of the low-light imaging market.

Market Concentration

Sony retained a 53% shipment share in 2024 thanks to decades of investment in wafer-level optics, stacked pixel designs, and proprietary algorithms. Such vertical integration yields economies of scale that few rivals can match. Samsung leverages its memory and logic prowess to push 200 MP mobile sensors, although share consolidation is difficult because OmniVision, GalaxyCore, and Onsemi specialize in high-growth niches. The competitive environment is therefore moderately concentrated, with the top five vendors accounting for nearly 78% of revenue. This concentration keeps average selling prices firm even as unit demand diversifies.

Emerging challengers employ targeted strategies. GalaxyCore tripled its profit by serving AI glasses and entry-level automotive cameras in China, circumventing premium handset battles. Hamamatsu strengthened its scientific portfolio by acquiring BAE Systems’ imaging group, now Fairchild Imaging, to secure low-noise CMOS know-how. Meta’s AR/VR patent filings underscore future competition from non-traditional electronic giants, signaling that software ecosystems will dictate sensor feature sets. Lynred’s purchase of NIT consolidates SWIR supply bases, providing one-stop offerings for industrial users.

Partnerships dominate strategic moves. AMD bought Enosemi to fuse photonics with compute for AI workloads. Omnivision and AVIVA team on ASA-compliant cameras for software-defined vehicles, ensuring compliance with evolving automotive standards ovt.com. Onsemi extended its DENSO partnership through equity linkage that guarantees long-term supply for next-generation ADAS chips. As specialized use cases expand, collaborative innovation rather than outright consolidation will shape future leadership within the low-light imaging market.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Market Definitions and Key Coverage

Our study defines the low-light imaging market as all visible-to-near-infrared sensors, camera modules, and integrated software pipelines that enable image capture below 10 lux across consumer, automotive, security, scientific, and industrial use cases.

Scope exclusion: stand-alone long-wave thermal imagers that lack visible-range capability are not counted.

Segmentation Overview

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed fabless sensor designers in Japan, tier-1 automotive camera integrators in Germany, Asian smartphone ODMs, and city-security OEMs across the Gulf. Dialog focused on penetration rates, price erosion, and impending design wins; survey follow-ups validated wafer conversion yields and shipment seasonality.

Desk Research

We began with public datasets from bodies such as UN Comtrade (cross-border sensor shipments), SEMI (wafer starts), Eurostat (vehicle camera fitment), and FCC equipment authorizations, which anchor volume and trade flows. Additional context came from IEEE Xplore papers on backside-illuminated CMOS efficiency, patent families via Questel, and annual filings of leading image-sensor vendors that disclose ASP trends. Subscription tools like D&B Hoovers and Dow Jones Factiva let our analysts size company revenue slices by end market. These sources, among several others not exhaustively listed here, ground the baseline.

A second pass mined regional standards, China NCAP night-vision rules, and US NDAA camera sourcing guidelines, plus association portals such as SIA and GSA to capture regulatory and demand signals. This record-keeping aids us when reconciling regional splits with global totals.

Market-Sizing & Forecasting

A top-down model scales global smartphone, vehicle, and surveillance-camera pools by night-mode or HDR adoption, then applies segment-specific ASP curves before currency normalization. Selective bottom-up cross-checks, sampled supplier roll-ups, and channel inventory audits trim over- or under-shoots. Key variables include: smartphone low-light feature attach rate, L2+ vehicle camera count, urban CCTV node growth, sensor pixel-size roadmap, and silicon wafer capacity utilization. Five-year projections leverage multivariate regression blended with ARIMA smoothing, while primary expert consensus guides scenario bounds where visibility is low.

Data Validation & Update Cycle

Outputs undergo variance scans against quarterly sensor shipment trackers and Customs alerts; anomalies trigger re-checks with respondents. Two-tier analyst reviews precede sign-off. Reports refresh each year, with interim updates issued when material supply-chain or regulatory events surface.

Why Mordor's Low Light Imaging Baseline Earns Trust

Benchmark comparison

Published values often diverge because firms set different spectral cut-offs, bundle software irregularly, or refresh on mismatched calendars.

Our disciplined scope, yearly resets, and dual-path modeling minimize those gaps.

Key gap drivers include competitors tallying pure thermal modules, using flat ASP assumptions, or freezing smartphone unit outlooks made pre-COVID. Our rolling sensor-price tracker and quarterly smartphone sheet correct such drift.

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 17.24 B | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 20.03 B | Global Consultancy A | Includes standalone thermal imagers and applies single global ASP | ||

USD 16.84 B | Regional Consultancy B | Omits automotive HDR sensor demand and uses 2023 smartphone baseline |

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

US Market Entry for Taiwanese Machine Tool Manufacturers

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.