Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The Short-Wave Infrared Imaging Market is Segmented by Wavelength (≤1 Μm (0. 9 Μm Band), 1 Μm-1. 4 Μm, and More), Cooling Technology (Uncooled SWIR, and Cooled SWIR), Sensor Type (Line Detectors, and Area/Imagers), Level of Integration (Sensor-Only Modules, and More), End-User Industry (Automotive, and More), Application (Security and Surveillance, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

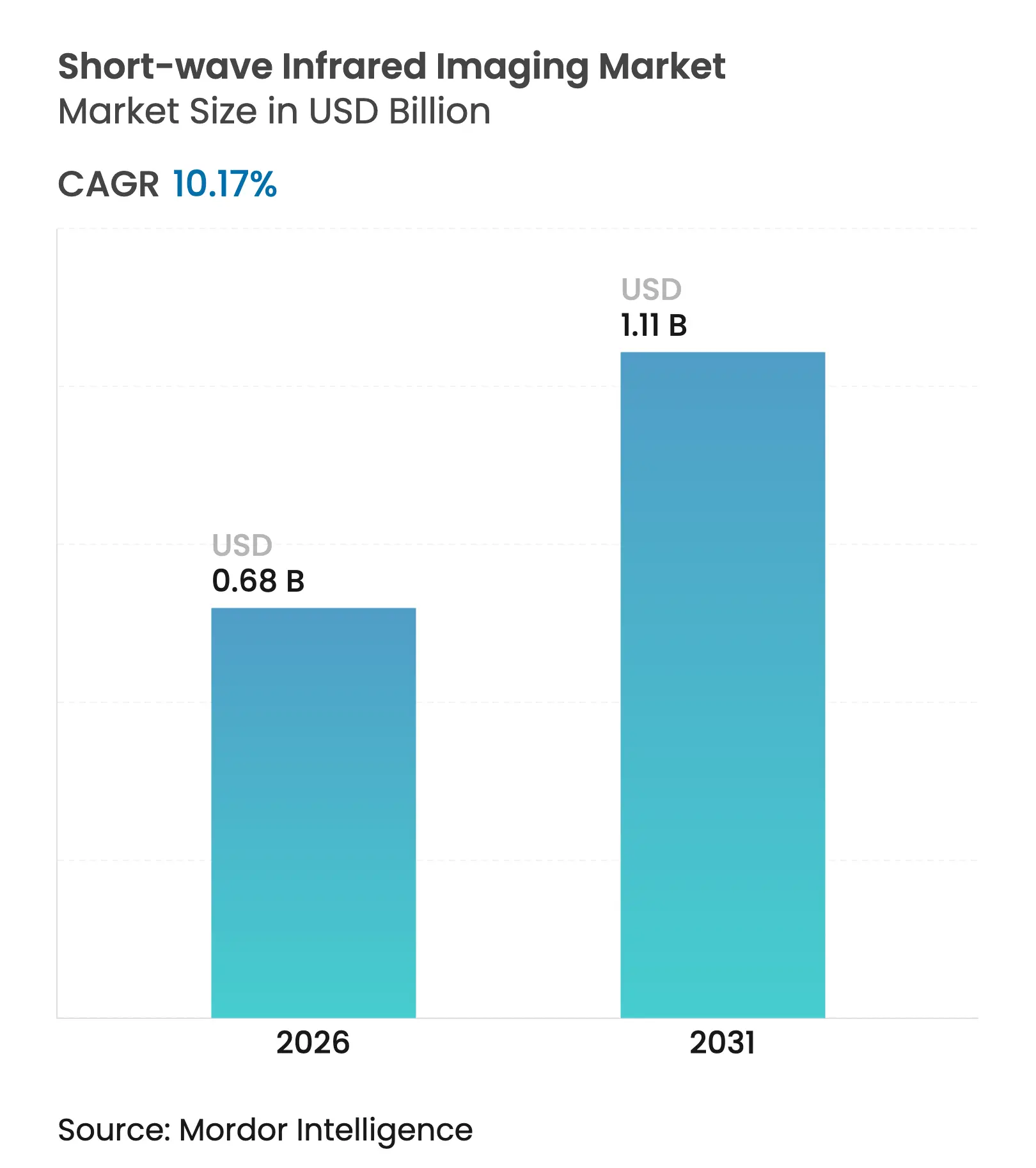

| Market Size (2026) | USD 0.68 Billion |

| Market Size (2031) | USD 1.11 Billion |

| Growth Rate (2026 - 2031) | 10.17 % CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

short-wave infrared imaging market size in 2026 is estimated at USD 680 million, growing from 2025 value of USD 618 million with 2031 projections showing USD 1.11 billion, growing at 10.17% CAGR over 2026-2031. Robust defense procurement cycles, accelerating deployment of uncooled detectors in machine-vision lines, and early automotive design-wins underpin this expansion.[1]U.S. Geological Survey, “Mineral Commodity Summaries 2024,” usgs.gov Breakthrough quantum-dot sensors priced below EUR 50 are dismantling legacy cost barriers, opening the technology to mass-market consumer and mobility applications. Automotive OEMs are validating SWIR for all-weather ADAS, while industrial OEMs integrate broadband SWIR cameras for moisture, contaminant, and through-silicon inspection. Asia-Pacific fabrication capacity and China’s strategic semiconductor investments are reshaping global supply chains despite persistent ITAR/EAR export hurdles.[2]Bureau of Industry and Security, “Implementation of Additional Export Controls,” bis.doc.gov

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Increasing penetration in military and

defense

Increasing penetration in military and

defense

| +2.8% | North America, Europe | Medium term (2-4 years) |

% Impact on CAGR Forecast

:

+2.8%

|

Geographic Relevance

:

North America, Europe

|

Impact Timeline

:

Medium term (2-4 years)

|

Industrial machine-vision quality-inspection

boom

Industrial machine-vision quality-inspection

boom

| +2.1% | Asia-Pacific manufacturing hubs | Short term (≤ 2 years) | |||

Rapid adoption in ADAS and autonomous

vehicles

Rapid adoption in ADAS and autonomous

vehicles

| +1.9% | North America, Europe | Medium term (2-4 years) | |||

Cost decline via quantum-dot and organic

photodiode sensors

Cost decline via quantum-dot and organic

photodiode sensors

| +1.7% | Global, fabs concentrated in APAC | Short term (≤ 2 years) | |||

Under-display 3-D sensing in next-gen

smartphones

Under-display 3-D sensing in next-gen

smartphones

| +1.4% | Asia-Pacific consumer electronics | Long term (≥ 4 years) | |||

AI-enabled material classification

AI-enabled material classification

| +1.2% | North America, Europe | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Increasing Penetration in Military and Defense

Defense modernization budgets sustain stable, multi-year demand for SWIR imagers that outperform visible and thermal systems in smoke, fog, and low-light conditions. SCD USA’s MIRA camera has been designed into man-portable and armored platforms, validating the technology for mobile soldiers.[3]SCD USA, “MIRA SWIR Camera Design-In Wins,” edrmagazine.euPrinceton Infrared Technologies is delivering next-generation sensors to NASA and the U.S. Space Development Agency, extending SWIR’s reach to space-borne reconnaissance. Photonis secured the U.K. MoD’s TALON fused sight contract, signaling SWIR’s transition from niche payloads to baseline soldier optics. Combined, these programs anchor revenue visibility for established suppliers and promote continued R&D investment.

Industrial Machine-Vision Quality-Inspection Boom

High-volume manufacturing plants now use SWIR cameras to see through silicon, detect moisture, and sort materials impossible to differentiate with visible light. Balluff notes rapid adoption in food, pharma, and electronics lines where non-contact moisture sensing raises throughput balluff.com. Sony’s SenSWIR sensors capture visible, NIR, and SWIR in one device, cutting system cost and footprint for deep-learning inspection stations novuslight.com. Machine-vision demand, projected to reach USD 9.3 billion by 2028, positions SWIR as a core spectral modality rather than a niche add-on automate.org. Falling detector costs accelerate this trend, enabling OEMs to retrofit legacy lines without prohibitive capex.

Rapid Adoption in ADAS and Autonomous Vehicles

Automakers seek spectral diversity to maintain object detection in rain, fog, and glare where visible sensors fail. Hitachi Astemo is evaluating TriEye’s CMOS SWIR chip for next-generation driver-assistance stacks. The RASMD database with 100,000 matched RGB–SWIR frames provides critical training data for sensor-fusion algorithms arxiv.org. TriEye’s 0.4-1.6 µm sensor runs at 120 fps and costs a fraction of InGaAs, enabling high-volume automotive integration. Industry forecasts show automotive SWIR revenue rising from USD 4 million in 2024 to USD 21 million by 2027 as pilot programs enter production.

Cost Decline via Quantum-Dot and Organic Photodiode Sensors

Colloidal quantum-dot arrays deliver SWIR sensitivity on standard CMOS wafers, slashing detector pricing by an order of magnitude. Emberion’s EUR 50 sensor achieves 120 dB dynamic range at room temperature. Quantum Science’s registered product INFIQ dots tune absorption across 0.9-2.0 µm while remaining compatible with high-volume deposition lines. Lead-free formulations from ICFO remove toxicity barriers, easing smartphone regulatory compliance. Cost erosion widens the addressable market and feeds a volume-driven cost-down flywheel.

Restraints Impact Analysis

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High cost of InGaAs sensors and optics

High cost of InGaAs sensors and optics

| -2.3% | Emerging markets hardest hit | Short term (≤ 2 years) |

% Impact on CAGR Forecast

:

-2.3%

|

Geographic Relevance

:

Emerging markets hardest hit

|

Impact Timeline

:

Short term (≤ 2 years)

|

Export regulations (ITAR/EAR) limiting

supply chains

Export regulations (ITAR/EAR) limiting

supply chains

| -1.8% | Primarily affects U.S. companies | Medium term (2-4 years) | |||

Indium-phosphide wafer supply bottlenecks

Indium-phosphide wafer supply bottlenecks

| -1.5% | Asia-Pacific fabs | Medium term (2-4 years) | |||

Data-privacy concerns for consumer imaging

Data-privacy concerns for consumer imaging

| -0.9% | Europe, North America | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

High Cost of InGaAs Sensors and Optics

Epitaxial InGaAs wafers remain 10-20 times the cost of silicon, keeping fully-cooled cameras above USD 20,000 list price in many markets usgs.gov. Limited 4-inch InP substrate supply and slow ramp to 6-inch lines hinder economies of scale. These economics constrain adoption in agriculture and infrastructure monitoring where ROI thresholds are tight. Quantum-dot and hybrid CMOS alternatives are beginning to erode the price premium, but legacy programs tied to stringent military reliability standards still rely on high-cost InGaAs optics.

Export Regulations (ITAR/EAR) Limiting Supply Chains

U.S. ITAR and EAR rules classify many SWIR sensors as dual-use goods, adding licensing hurdles and lengthening delivery cycles by several months. Teledyne FLIR has developed non-ITAR airborne payloads to regain competitiveness but still faces partner reluctance in certain regions.[4]Teledyne FLIR Defense, “Non-ITAR Long-Range Airborne Imaging System,” flir.comEuropean firms such as Xenics and Lynred, operating outside U.S. export regimes, leverage this gap to win contracts in the Middle East and Asia. Regulatory uncertainty also discourages venture investment in U.S. start-ups targeting global commercial markets.

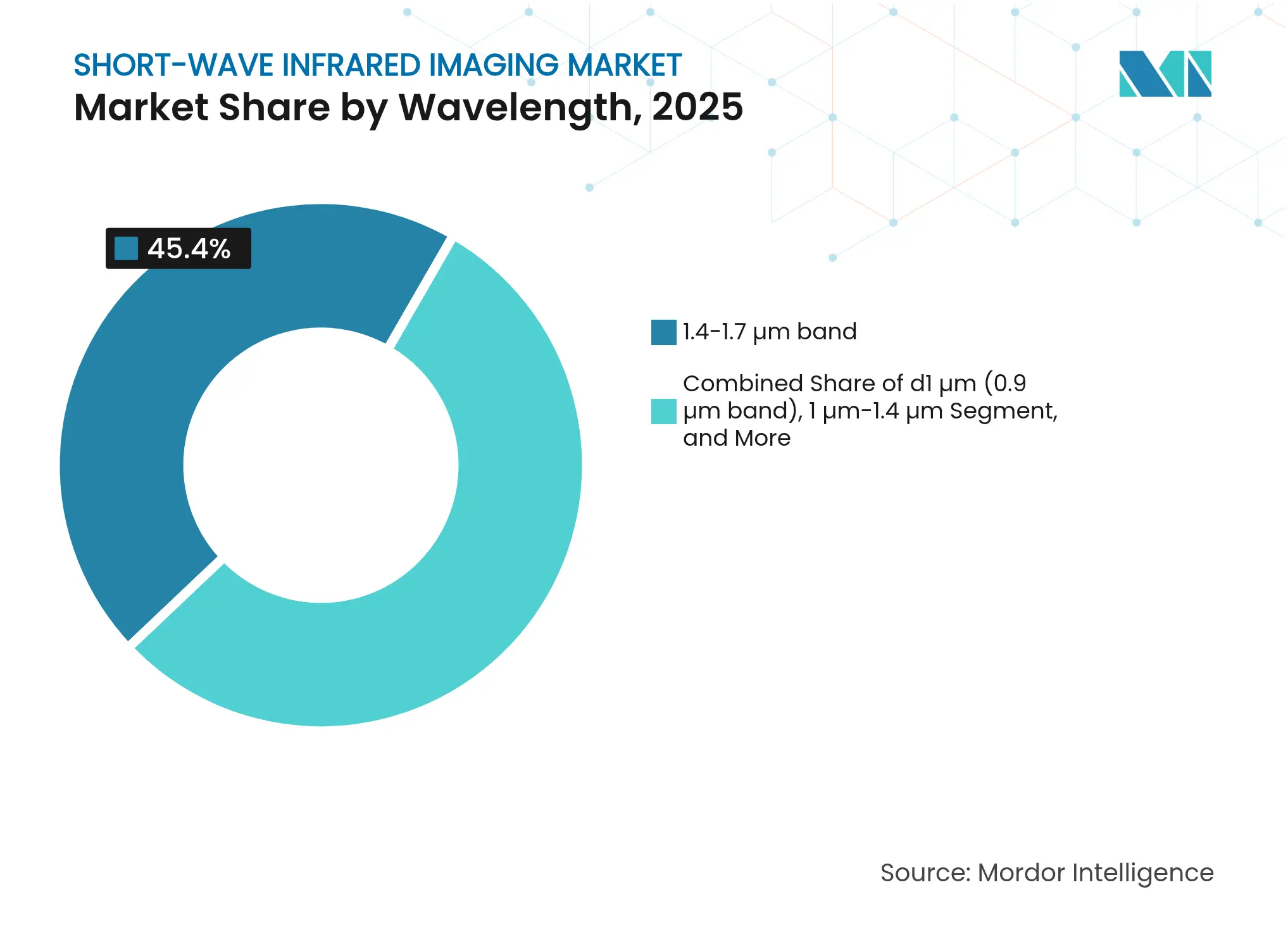

By Wavelength: Mid-Range Bands Drive Adoption

The 1.4-1.7 µm band generated 45.40% of 2025 revenue, reflecting a sweet-spot between atmospheric transmission and mature detector sensitivity across surveillance and machine-vision deployments. The ≥2.1 µm range is gaining ground at a 11.93% CAGR because advanced spectroscopy and gas-leak detection need deeper penetration and narrower absorption lines.

Technology convergence is blurring traditional spectral silos. Acuros eSWIR cameras now cover 0.3-2.0 µm in one device, suggesting future buyers may specify broadband performance instead of discrete bands. As quantum-dot response stretches toward 2.5 µm, premium analytical tasks could migrate from mid-wave to the short-wave infrared imaging market for lower cost and simpler cooling requirements.

Note: Segment shares of all individual segments available upon report purchase

By Cooling Technology: Uncooled Systems Gain Ground

Uncooled architectures delivered 62.30% revenue in 2025 and are rising 9.5% annually as industrial and automotive users prioritize low power and small form factor. Room-temperature quantum-dot arrays routinely hit 120 dB dynamic range, narrowing the historic performance gap with cooled InGaAs detectors.

Cooled assemblies remain critical for kilometer-range surveillance and airborne ISR where sub-noise-floor sensitivity is mission-critical. Yet procurement officers increasingly accept uncooled modules for man-portable optics, creating a mixed fleet that shifts overall volumes toward uncooled units, thereby lowering the average selling price of the short-wave infrared imaging market.

By Sensor Type: Area Imagers Dominate but Line Detectors Accelerate

Area arrays accounted for 67.20% of 2025 shipments on the back of security cameras, scientific instruments, and ADAS prototyping. High-speed variants exceed 1,700 fps while preserving VGA resolution, supporting missile-tracking and semiconductor inspection.

Line-scan sensors are forecast to post an 10.85% CAGR through 2031 as web inspection, lithium-ion battery foil analysis, and hyperspectral scanners favor linear architectures. Hybrid chips that toggle between full-frame and line-scan modes inside a single die promise to unify supplier roadmaps and simplify inventory.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

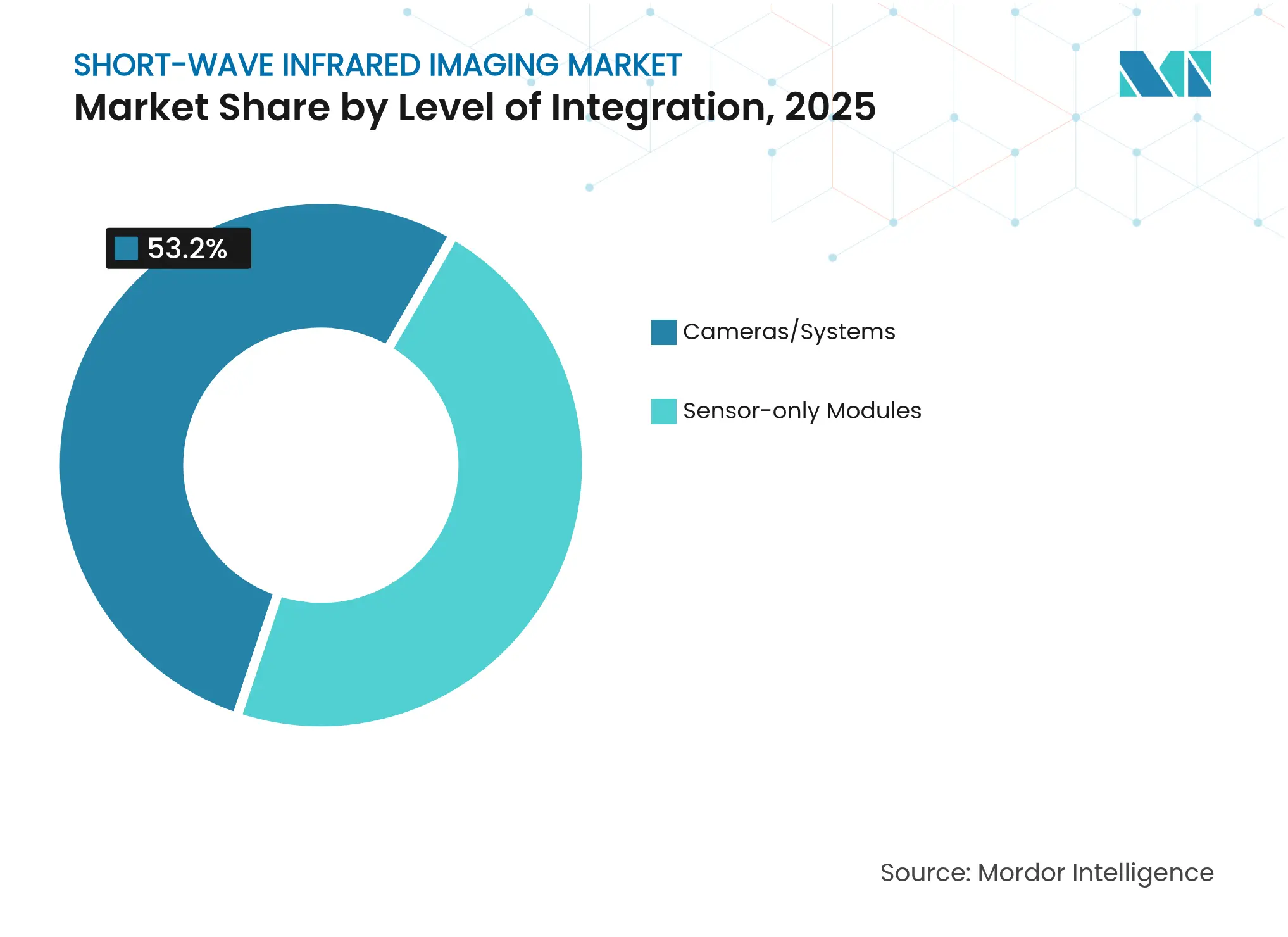

By Level of Integration: Complete Systems Preferred

Turn-key cameras captured 53.20% of 2025 revenue as integrators without optics expertise seek quick deployment. Plug-and-play Ethernet and USB3 modules reduce engineering overhead, accelerating design-in cycles for factories and research labs.

Sensor-only modules, expanding at 10.22% CAGR, cater to defense primes and automotive Tier 1s that embed SWIR into gimbals, lidar stacks, or multi-sensor pods. onsemi’s vertical integration following the SWIR Vision Systems acquisition underscores the margin potential when device makers own the full camera stack.

Note: Segment shares of all individual segments available upon report purchase

By End-User Industry: Defense Leads, Automotive Surges

Defense users commanded 60.30% of 2025 spending, benefiting from stable budgets and multi-year platform cycles. Vehicle, drone, and soldier-borne optics continue to specify SWIR for smoke and fog penetration that thermal imagers cannot match.

Automotive and transportation, advancing at 14.05% CAGR, will narrow the gap as OEMs integrate SWIR into sensor-fusion stacks for L3 autonomy. Early production programs are already driving economies of scale that lower cost for adjacent industrial and medical sectors, reinforcing cross-pollination within the short-wave infrared imaging industry.

By Application: Surveillance Dominant, ADAS Fastest

Security and surveillance delivered 55.10% of 2025 revenue, underpinned by border control, critical-asset monitoring, and law-enforcement night-vision upgrades. Continuous operation regardless of ambient illumination cements SWIR as a mainstay for perimeter defense.

ADAS and autonomous driving applications will post a 15.12% CAGR to 2031 after TriEye, Adasky, and other start-ups proved reliable obstacle detection in fog, snow, and direct sunlight. Quality-inspection lines and fluorescence-guided surgery represent steady growth niches that leverage the same spectral advantages for very different end-markets.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

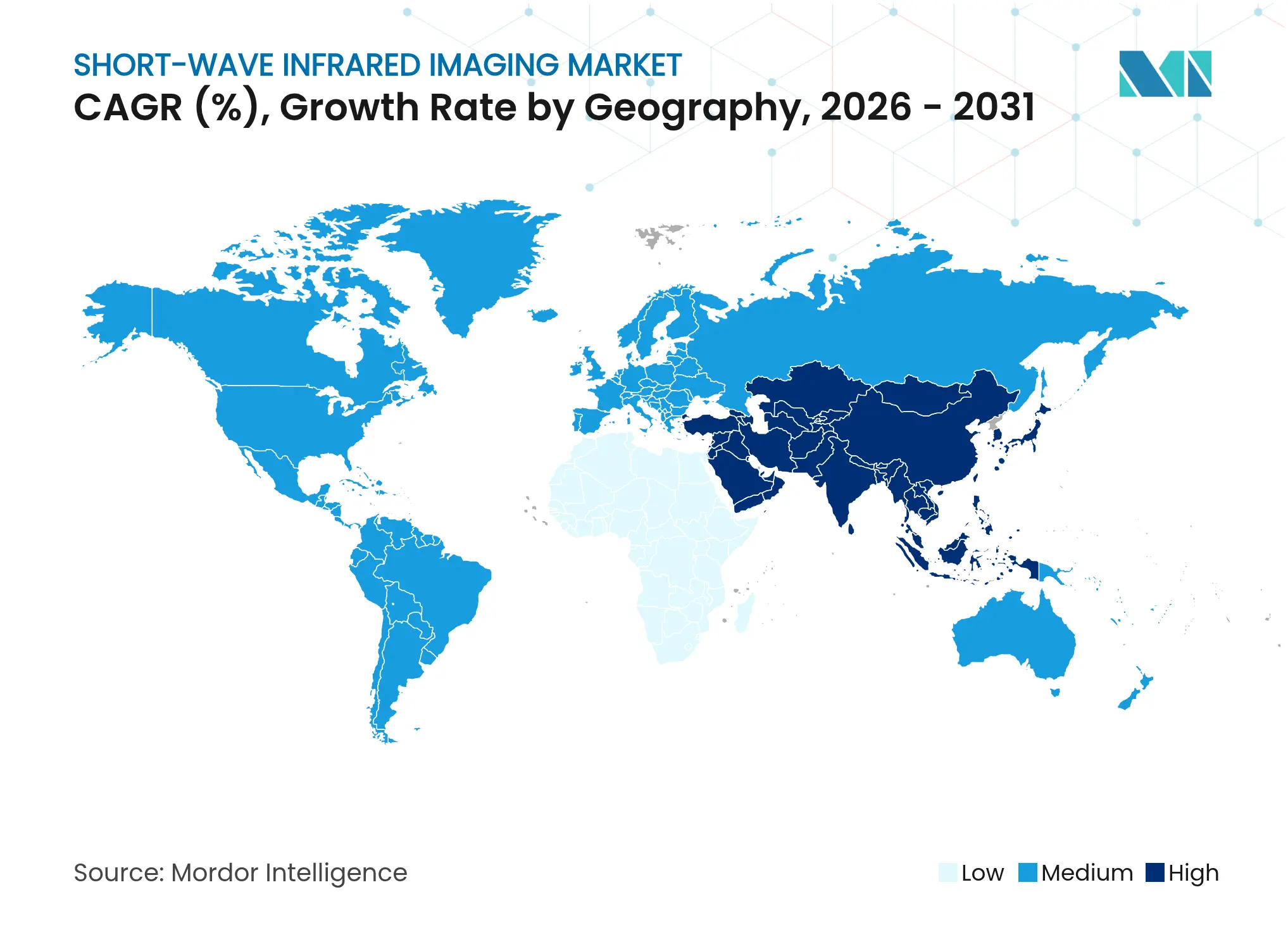

North America held 37.60% of 2025 revenue thanks to concentrated defense spending, early industrial pilots, and a rich ecosystem of sensor start-ups. AVT secured USD 16 million in Department of Defense imaging contracts that embed SWIR into ground systems, underscoring continued military pull-through Nonetheless, strict export controls narrow overseas addressable markets for U.S. suppliers.

Asia-Pacific is the fastest-growing region at 11.42% CAGR, propelled by China’s semiconductor self-reliance drive and Japan’s leadership in stacked-pixel sensor fabrication. China’s burgeoning satellite constellation integrates SWIR payloads for methane detection and crop monitoring, highlighting sovereign demand for industrial policy reasons. Sony’s partnership with Ultralytics layers AI onto SWIR edge sensors, showcasing regional collaboration between hardware and software champions.

Europe remains influential through vendors like Lynred and Xenics that combine strong aerospace heritage with expanding machine-vision portfolios. Lynred’s buyout of New Imaging Technologies adds small-pixel high-definition arrays, positioning the firm to compete head-on in industrial automation. European exporters benefit from lighter regulatory burdens compared with ITAR, allowing agile pursuit of Middle-East and Asia tenders.

Market Concentration

The short-wave infrared imaging market is moderately concentrated. Teledyne FLIR, SCD, and Sensors Unlimited anchor the high-performance tier, while quantum-dot newcomers erode price premiums. Consolidation is reshaping the field: onsemi absorbed SWIR Vision Systems to pair CQD sensors with CMOS processing, and Lynred purchased New Imaging Technologies to secure vertically integrated arrays.

Technology differentiation now eclipses scale as the prime competitive weapon. Emberion and Quantum Science ship low-cost detectors suited to consumer, medical, and mobility devices, forcing incumbents to accelerate cost-down roadmaps. European and Asian firms capitalize on U.S. export-control hurdles to capture international orders, while U.S. players focus on domestic defense upgrades.

Software-defined imaging is the next frontier. Vendors that pair SWIR hardware with AI analytics lock in recurring revenue from feature licenses and updates. Access to annotated spectral datasets, such as RASMD, will separate leaders from laggards as customers demand turnkey classification rather than raw imagery.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUES)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

The market study analyses the market trends and opportunities for different types of short-wave infrared imaging, such as 1 micron, 1.7 micron, and 2.1 micron, that are used in the various end-user industries in multiple regions. Further, the study analyzes the impact of COVID-19 on the market players and its stakeholders across the supply chain. Additionally, the disruption factors impacting the market's growth in the near future have been covered in the study regarding drivers and restraints.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.