Aerosol Refrigerants Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.4 Billion |

| Market Size (2031) | USD 1.69 Billion |

| Growth Rate (2026 - 2031) | 3.86% CAGR |

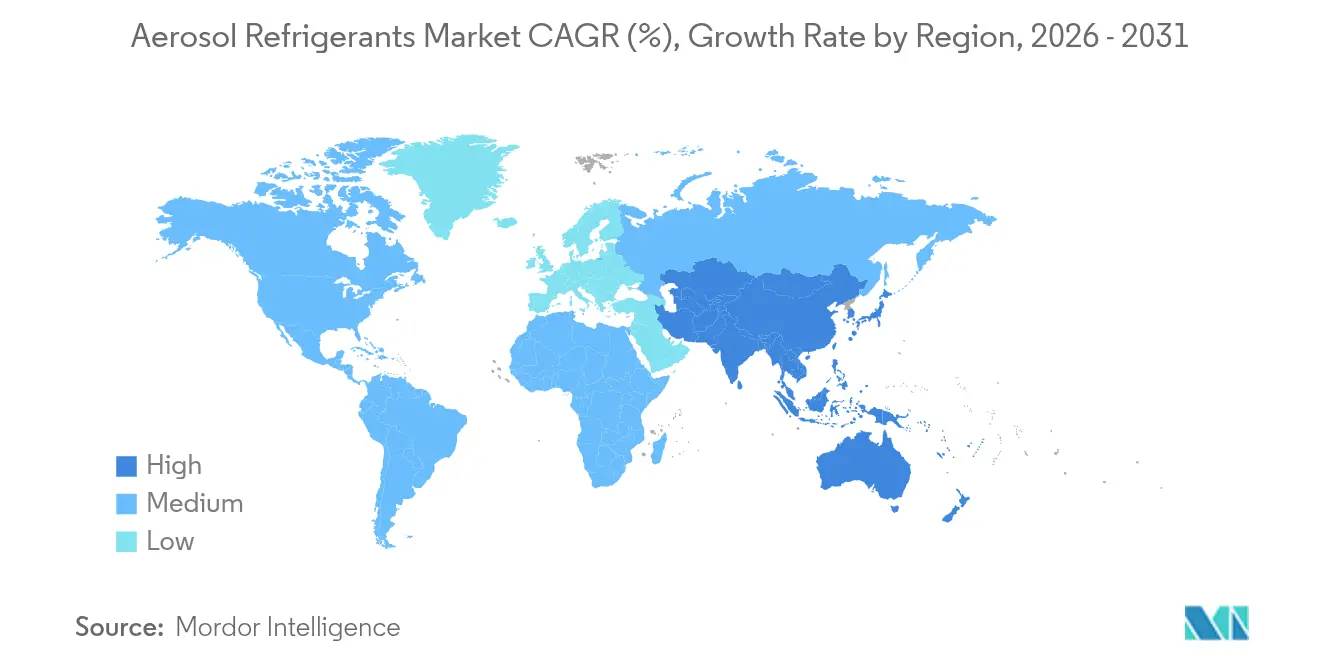

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

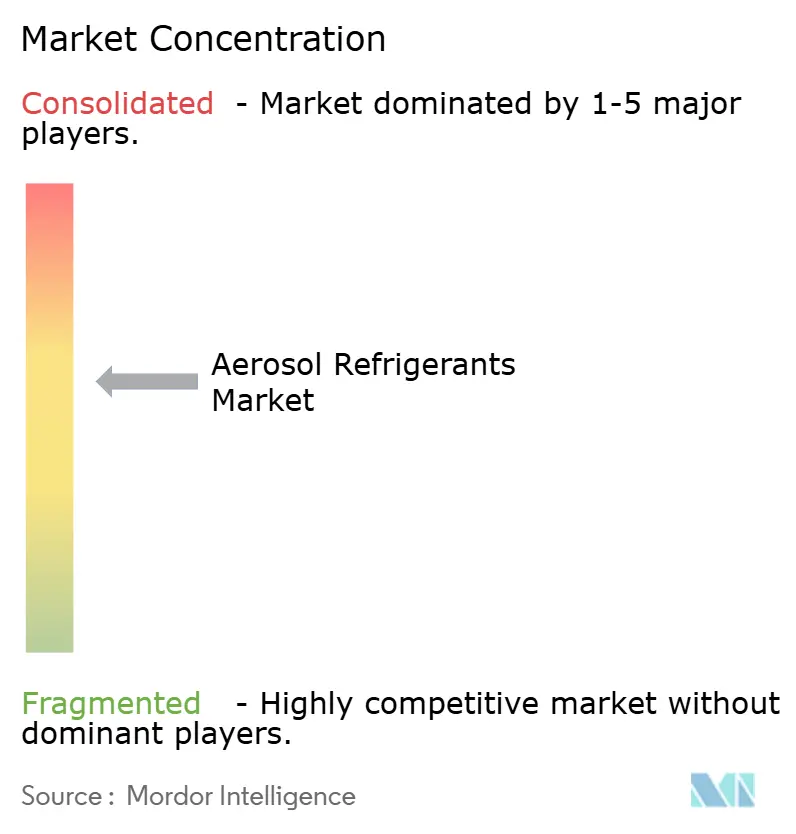

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aerosol Refrigerants Market Analysis by Mordor Intelligence

The Aerosol Refrigerants Market size is expected to grow from USD 1.35 billion in 2025 to USD 1.4 billion in 2026 and is forecast to reach USD 1.69 billion by 2031 at 3.86% CAGR over 2026-2031. This steady expansion reflects the sector’s migration away from high-GWP hydrofluorocarbons toward compliant propellants in response to the American Innovation and Manufacturing Act, European F-gas revisions and parallel phase-down rules across major economies. Demand is reinforced by stricter GWP caps that continue to raise legacy HFC prices, surging do-it-yourself (DIY) HVAC maintenance, the permanent build-out of ultra-cold pharmaceutical cold chains, and rising data-center cooling loads as artificial-intelligence workloads scale. Competitive activity remains moderate: incumbent producers are carving out low-GWP businesses, expanding cylinder capacity and partnering on immersion-cooling fluids to defend share while preparing for the A2L transition. Price volatility for R-454B and lingering safety-certification delays for A2L blends temper growth yet also widen openings for agile suppliers that can deliver compliant, small-pack aerosol formats into underserved regions.

Key Report Takeaways

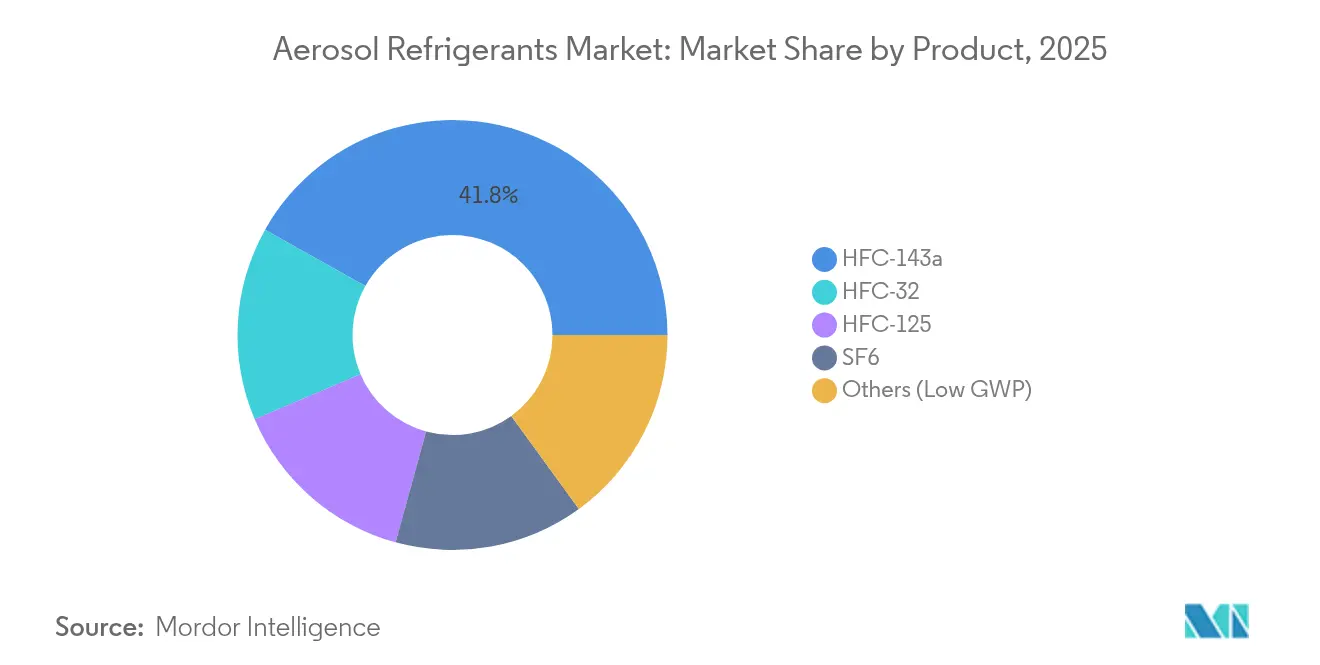

- By product, HFC-143a held a 41.85% aerosol refrigerants market share in 2025, whereas the Others (Low GWP) category is projected to grow the fastest at a 4.05% CAGR through 2031.

- By packaging form, aerosol cans (greater than or equal to 500 g) captured 58.30% of the aerosol refrigerants market size in 2025; others post the quickest expansion at a 4.62% CAGR to 2031.

- By application, refrigerators and freezers led with 31.88% revenue share in 2025, while specialty aerosol products advance at a 4.49% CAGR during the outlook period.

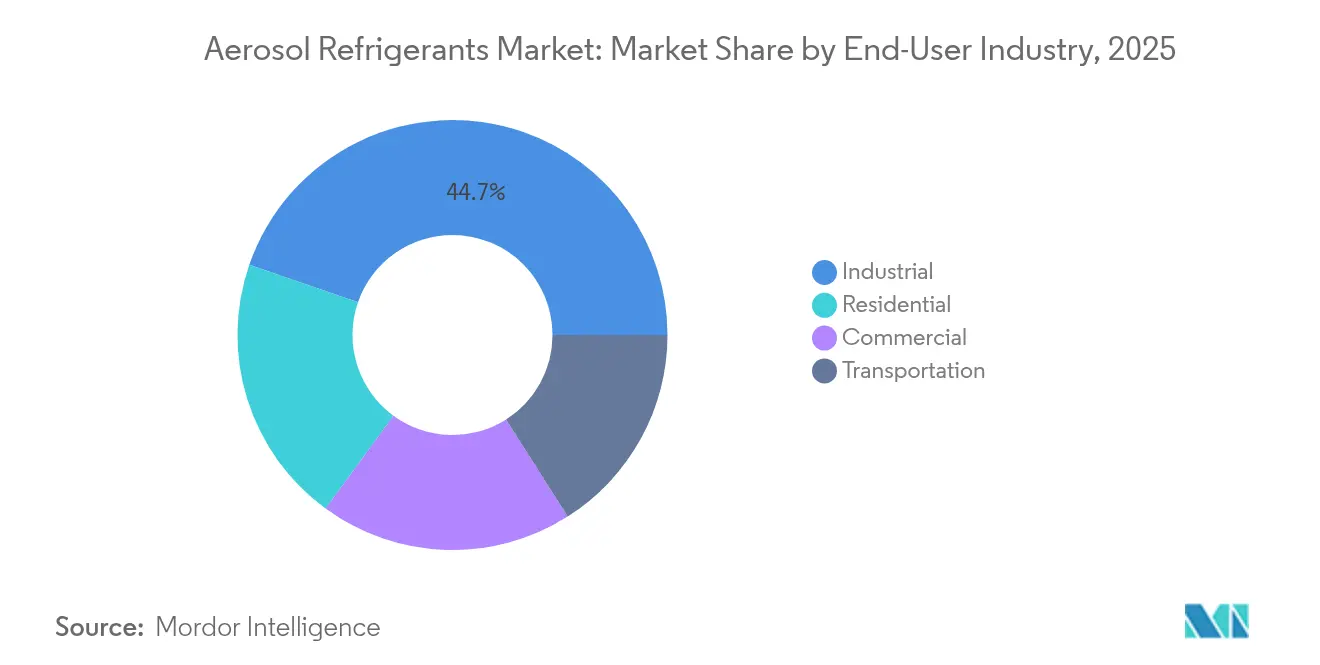

- By end-user industry, the industrial segment commanded 44.70% of the aerosol refrigerants market size in 2025, whereas commercial users record the highest projected CAGR at 4.41% through 2031.

- By geography, Asia-Pacific controlled 42.95% of 2025 value; the region is also register the strongest CAGR of 4.21% over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aerosol Refrigerants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid HFC Phase-Down Policies in North America and Europe Spurring Low-GWP Aerosol Propellants | +1.2% | North America and Europe, spillover to APAC | Medium term (2-4 years) |

| Surging DIY HVAC Maintenance and Recharge-Kit Sales via E-Commerce | +0.8% | Global, concentrated in North America and Europe | Short term (≤ 2 years) |

| Rising Demand for Ultra-Cold Vaccine Logistics (Portable Aerosol Refrigerants) | +0.6% | Global, priority in developed markets | Medium term (2-4 years) |

| Expanding Refurbishment Cycle of Commercial HVAC In Hyperscale Data-Centres | +0.7% | Global, concentrated in North America and APAC | Long term (≥ 4 years) |

| Rising Residential AC Penetration in Tropical Emerging Economies | +0.9% | APAC core, spillover to Latin America and MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid HFC phase-down policies spur low-GWP propellants

Production-quota cuts of 40% in the United States by 2024 and 30% in the European Union by 2027 tighten legacy refrigerant supply, pushing R-454B cylinder prices to USD 700–800 versus USD 250–300 for R-32. California’s SB 1206 bans bulk HFCs over 750 GWP from 2033, while the revised EU F-gas regulation has lifted high-GWP spot prices by up to 1,000%. These cost gaps accelerate equipment retrofits and favor aerosol refrigerant manufacturers able to supply A2L alternatives on short notice[1]California Air Resources Board, “Senate Bill 1206 HFC Restrictions,” arb.ca.gov .

Surging DIY HVAC maintenance supports e-commerce aerosol sales

Online retailers now offer compact recharge kits that let owners service split AC units without contractors. The trend gained traction through pandemic lockdowns and persists as R-22 and R-134a phase-outs raise service costs. Yet Section 608 of the U.S. Clean Air Act still requires certified recovery for most operations, limiting legitimate DIY use to minor top-ups and creating demand for sub-500 g aerosol cans clearly labeled for compliant uses.

Rising demand for ultra-cold vaccine logistics

Messenger-RNA vaccines, cell-based therapies and biologics all require -80 °C transport. Studies show hydrocarbon blends such as R-290/R-170 provide stable performance in cascade freezers, while Honeywell’s near-zero GWP Solstice Air propellant is already deployed in pressurized inhalers. Logistics providers therefore turn to portable aerosol refrigerants that offer instant, precise cooling and low environmental impact.

Expanding data-center refurbishment cycle

Hyperscale operators retrofitting for AI-chip heat loads are trialing two-phase immersion systems. Chemours and NTT DATA are testing Opteon 2P50 fluids, while Alliance Air is investing USD 121 million in Mexico to supply specialty cooling modules. Short maintenance windows favor aerosol propellants for interim top-offs or spot-cooling until full liquid-cooling retrofits complete.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Feed-Stock Price Volatility | -0.9% | Global, concentrated in North America and Europe | Short term (≤ 2 years) |

| Safety and Flammability Concerns with A2L Blends Limiting Retrofit Adoption | -1.1% | Global, acute in North America and Europe | Medium term (2-4 years) |

| Scarcity of Certified Recovery and Recycling Infrastructure in Developing Nations | -0.7% | APAC, MEA, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating feed-stock price volatility constrains budgets

Honeywell applied a 42% surcharge on R-454B in 2024 amid fluoro-chemical shortages, sending contract prices as high as USD 2,000 per cylinder. Contractors facing unpredictable lead times restrict maintenance work to full-system replacements, which reduces short-term aerosol sales despite longer-term conversion benefits once new units arrive.

Safety and flammability concerns limit retrofit adoption

ASHRAE 15-2022 and UL 60335 revisions mandate leak detectors, charge-size caps and special tools for A2L handling. Consumers often conflate A2L with highly flammable A3, delaying acceptance. Multifamily-building codes in several U.S. states still require dedicated shafts for A2L linesets, inflating retrofit costs and slowing aerosol refrigerant uptake for older equipment[2]Trane Technologies, “ASHRAE 15-2022 Implications for A2L Adoption,” trane.com .

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: HFC-143a dominance amid low-GWP transition

HFC-143a retained 41.85% of the aerosol refrigerants market share in 2025 thanks to proven performance and entrenched supply networks. The EPA’s phasedown schedule nevertheless caps its growth, while low-GWP HFO and hydrocarbon blends post a 4.05% CAGR as OEMs certify replacements. Chemours’ Opteon YF retrofit kits and the EPA’s most-recent Significant New Alternatives Policy (SNAP) listings position R-454C, R-455A and R-516A for swift uptake in refrigeration and mobile-air-conditioning segments. The aerosol refrigerants market size attributable to the Others (Low GWP) segment is therefore set to expand steadily as regulations tighten.

Continued HFC-143a availability ensures a controlled exit rather than abrupt discontinuation, giving industrial users time to adapt. Natural refrigerant uptake remains selective because propane and isobutane raise charge-limit and ventilation concerns inside pressurized cans.

By Packaging Form: Aerosol cans lead amid cylinder constraints

Aerosol cans of greater than or equal to 500 g held 58.30% value share in 2025, driven by DIY maintenance and their exemption from the strictest transport rules that govern larger cylinders. Persistent shortages of A2L-compliant cylinders further push technicians toward multi-can service kits. Conversely, new fabrication lines for small-diameter steel cylinders are coming online in the United States and Europe, promising to ease supply tightness by 2026.

Smaller format growth reflects consumer comfort with single-use containers and the need for precise, low-weight charges in mini-split systems. Enterprises, however, still prefer 1–5 kg cylinders for workshop efficiency once availability stabilizes.

By Application: Refrigerator servicing leads while specialty products surge

Refrigerators and freezers accounted for 31.88% of 2025 revenue, anchored by global appliance proliferation and ongoing maintenance demand. The specialty aerosol products niche, which includes ultra-cold vaccine shippers and pressurized respiratory devices, shows the fastest 4.49% CAGR as pharmaceutical cold-chain infrastructure becomes permanent. Portable -80 °C solutions rely on advanced propellants that balance low GWP with high latent-heat capacity, an area where the aerosol refrigerants industry is channeling R&D investments.

Heat-pump retrofits and data-center chillers add further upside. Governments promoting building electrification push legacy boiler replacements toward low-GWP heat-pump systems that still need interim service with aerosol propellants until sealed-system volumes dominate.

By End-User Industry: Industrial dominance amid commercial uptake

Industrial facilities held 44.70% of spending in 2025 because downtime risk in process cooling justifies premium propellant pricing and rapid-response service. Commercial buildings—from offices to supermarkets—are the fastest-growing customer class at 4.41% CAGR, propelled by global urban real-estate development and post-pandemic hospitality recovery. Residential units continue to scale in tropical nations, while the transportation segment pivots to R-1234yf retrofits for vehicle AC systems, adding incremental aerosol demand.

Geography Analysis

Asia-Pacific presently hosts the world’s largest installed base of room-air conditioners, and policy extensions for Article 5 countries allow manufacturers to ship R-32 and transitional A2L blends until late decade. China shipped 185 million units in 2024, up 29.1% year-on-year, underscoring local demand for maintenance propellants. India’s rising middle class is projected to take household AC penetration to 50% by 2037, creating a vast aftermarket for compliant aerosol can refills.

Emerging ASEAN economies—from Vietnam to Indonesia—present similar trajectories. Their hot-humid climates, young population profiles and growing e-commerce ecosystems combine to accelerate propellant sales. Japan and South Korea, meanwhile, deliver steady retrofit demand as white-goods makers switch to R-600a and R-1234yf yet still service installed HFC fleets.

In North America, the AIM Act’s production caps push contractors toward reclaim or low-GWP substitutes, and California’s SB 1206 GWP threshold of 750 in 2033 intensifies early adoption. DIY maintenance culture, aided by next-day online deliveries, sustains high turnover of 340 g to 680 g cans.

Europe’s aerosol refrigerants market faces the steepest price escalations for legacy HFCs—up to 1,000% since the first F-gas baseline year—which incentivizes low-GWP supply chains. Strict A2L building-code hurdles damp immediate uptake but drive innovation in packaging safety features such as pressure-relief membranes and tamper-evident valves.

South America benefits from Brazil’s 5.9 million-unit air-conditioner output, now only behind China. Local content rules encourage domestic propellant filling operations that feed both OEM lines and aftermarket. In the Middle East and Africa, 47% of air conditioners still utilise R-22, opening a sizeable replacement and retrofit pool once recovery and training infrastructure expands.

Competitive Landscape

The aerosol refrigerants market exhibits moderate concentration: the top five suppliers—Honeywell, Solvay, Daikin, Arkema and SINOCHEM LANTIAN —controlled just over 60% of 2024 revenues. Honeywell is spinning off its Solstice portfolio into Solstice Advanced Materials by late 2025, carving out a pure-play low-GWP entity poised to accelerate investments in A2L blends and medical propellants. Chemours signed a manufacturing pact with Navin Fluorine to scale Opteon immersion-cooling fluids and is piloting 2P50 with NTT DATA in Japan, signalling a move beyond traditional aerosol channels into data-center thermal management.

Cylinder shortages in 2024 exposed supply-chain fragility; Worthington Enterprises and other container specialists are now expanding seamless-steel capacity to meet stricter A2L pressure-ratings. Hudson Technologies’ partnership with LG Electronics highlights a reclaimed-refrigerant strategy aimed at circularity and quota relief. Smaller challengers target gap niches such as portable ultra-cold shippers and single-dose respiratory propellants, leveraging low fixed-asset footprints.

Technology investment emphasises flammability-mitigation hardware—integrated leak detection, QR-code-linked training modules and child-resistant actuators—all of which reinforce incumbents’ ability to sell premium-priced, standards-ready aerosol cans. Market positioning therefore hinges on combined mastery of regulations, packaging innovation and feed-stock security rather than sheer production scale.

Aerosol Refrigerants Industry Leaders

Honeywell International Inc.

DAIKIN INDUSTRIES, Ltd.

Solvay

Arkema

SINOCHEM LANTIAN CO., LTD.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: The Chemours Company partnered with Navin Fluorine International Limited to manufacture Opteon two-phase immersion cooling fluid at its Surat facility in India, with production expected to begin in FY27. This initiative aims to increase the availability of next-generation aerosol refrigerants, supporting cleaner and more efficient technologies used in aerosol propellants and cooling applications.

- March 2025: Honeywell announced the spin-off of its refrigerant and advanced-materials operations into Solstice Advanced Materials, a new publicly traded company planned to launch by the end of 2025. This move aims to increase the innovation and supply of environmentally friendly aerosol refrigerants used in cooling applications.

Global Aerosol Refrigerants Market Report Scope

The Aerosol Refrigerants Market report includes:

| HFC-143a |

| HFC-32 |

| HFC-125 |

| SF6 |

| Others (Low GWP) |

| Aerosol Can (greater than or equal to 500 g) |

| Small Cylinder (1-5 kg) |

| Others |

| Refrigerators and Freezers |

| Air Conditioners |

| Chillers |

| Heat Pumps |

| Specialty Aerosol Products |

| Residential |

| Commercial |

| Industrial |

| Transportation |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Product | HFC-143a | |

| HFC-32 | ||

| HFC-125 | ||

| SF6 | ||

| Others (Low GWP) | ||

| By Packaging Form | Aerosol Can (greater than or equal to 500 g) | |

| Small Cylinder (1-5 kg) | ||

| Others | ||

| By Application | Refrigerators and Freezers | |

| Air Conditioners | ||

| Chillers | ||

| Heat Pumps | ||

| Specialty Aerosol Products | ||

| By End-User Industry | Residential | |

| Commercial | ||

| Industrial | ||

| Transportation | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the aerosol refrigerants market and its expected growth?

The aerosol refrigerants market size was USD 1.4 billion in 2026 and is projected to reach USD 1.69 billion by 2031 at a 3.86% CAGR.

Which product type dominates global sales?

HFC-143a remains the leading product with 41.85% revenue share in 2025, although low-GWP blends are expanding fastest.

Why are aerosol cans more popular than small cylinders?

Cans of greater than or equal to 500 g avoid certain transport restrictions, align with DIY trends and mitigate current shortages of A2L-rated cylinders.

How are regulations influencing the market?

The AIM Act, EU F-gas rules and similar regional legislation are capping high-GWP production quotas, lifting prices and accelerating adoption of low-GWP aerosol propellants.

Which regions offer the highest growth prospects?

Asia-Pacific leads global demand and shows the strongest CAGR due to rising residential AC penetration in India and Southeast Asia.

Page last updated on: